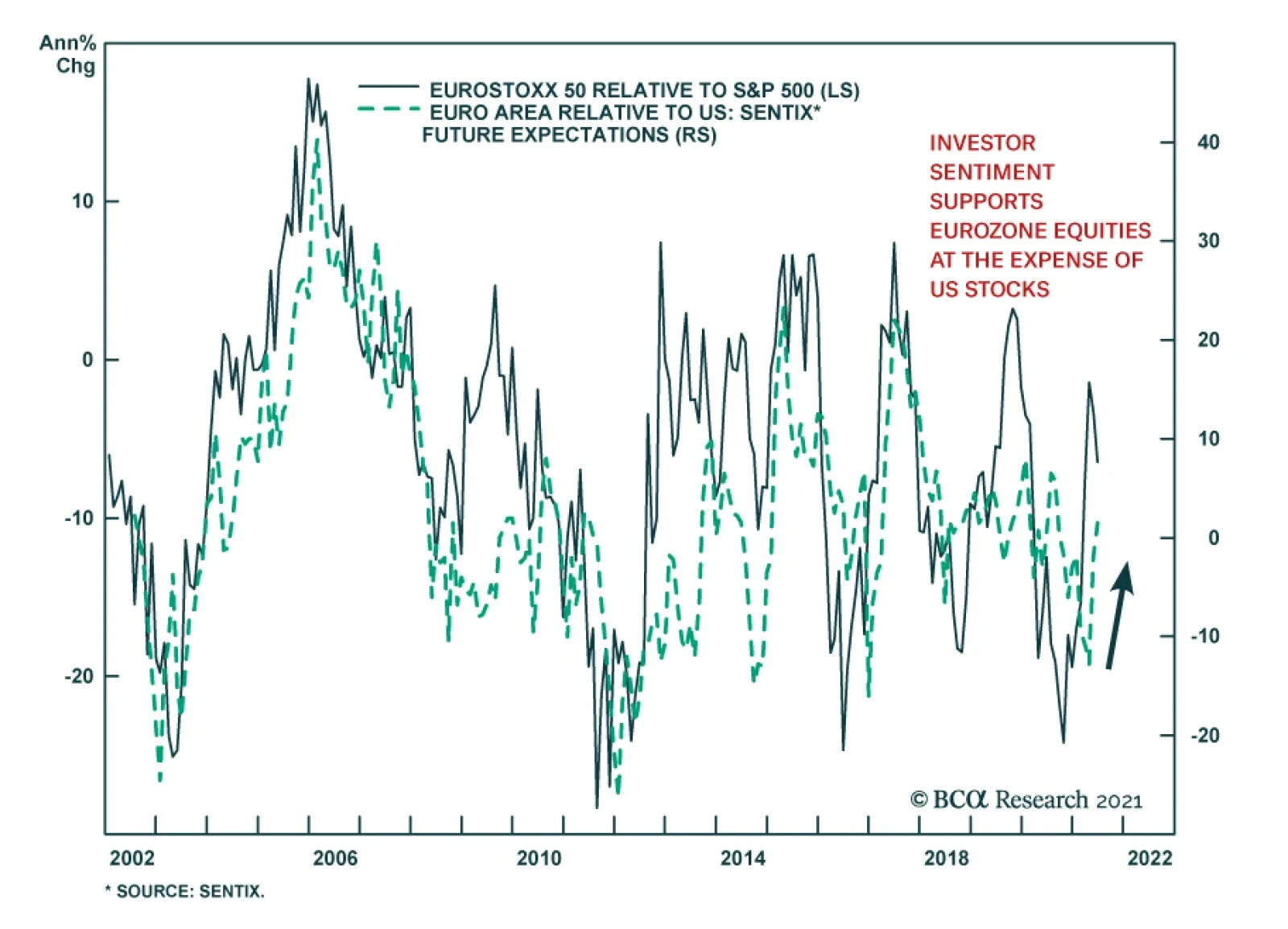

Euro Area

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

Highlights Q2/2021 Performance Breakdown: Our recommended model bond portfolio underperformed the custom benchmark index by -6bps during the second quarter of the year. Winners & Losers: The government bond side of the portfolio underperformed by -21bps, led overwhelmingly by our underweight to US Treasuries (-18bps). Spread product allocations outperformed by +15bps, primarily due to overweights on US high-yield (+11bps) and US CMBS (+3bps). Portfolio Positioning For The Next Six Months: We are maintaining an overall below-benchmark portfolio duration stance, against a backdrop of persistent above-trend global growth and a highly stimulative fiscal/monetary policy mix. We are maintaining a moderate overweight to global spread product versus government debt, concentrated on an overweight to US high-yield where valuations look the least stretched. We are making two changes to the portfolio allocations heading into Q3: shifting the Treasury curve exposure to have more of a flattening bias, while downgrading EM USD-denominated corporates to neutral. Feature The trend in global bond yields so far in 2021 has been a tale of two quarters. The first three months of the year saw a surge in yields worldwide on the back of rapidly improving economic data, the rollout of COVID-19 vaccines and supply squeezes triggering rapid increases in inflation. During the second three months of the year, however, global yields drifted a bit lower in response to more mixed economic data, the spread of the Delta variant and slightly hawkish shifts from a few key central banks – most notably, the Fed – even with economic confidence measures remaining upbeat across the developed economies. The decline in yields has not been seen across the maturity spectrum, though. The yield-to-maturity of the Bloomberg Barclays Global and US Treasury 10+ year indices fell by -12bps and -30bps, respectively, from recent peaks. At the same time, shorter term bond yields have been relatively stable as central banks continue to signal that interest rate hikes are still well off into the future. In contrast to government bonds, credit markets have remained calm with spreads tight for developed market corporates and emerging market (EM) debt. With that in mind, we present our quarterly review of the BCA Research Global Fixed Income Strategy (GFIS) model bond portfolio during the second quarter of 2021. We also present our recommended positioning for the portfolio for the next six months (Table 1), as well as portfolio return expectations for our base case and alternative investment scenarios. The latter half of 2021 should prove to be even more challenging for bond investors, who must disentangle less consistent messages across countries on the Delta variant, vaccinations, inflation and the outlook for both monetary and fiscal policy. Table 1GFIS Model Bond Portfolio Recommended Positioning For The Next Six Months

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

As a reminder to existing readers (and to new clients), the model portfolio is a part of our service that complements the usual macro analysis of global fixed income markets. The portfolio is how we communicate our opinion on the relative attractiveness between government bond and spread product sectors. We do this by applying actual percentage weightings to each of our recommendations within a fully invested hypothetical bond portfolio. Q2/2021 Model Bond Portfolio Performance: Mixed Returns Chart 1Q2/2021 Performance: Credit Gains & Duration Losses

Q2/2021 Performance: Credit Gains & Duration Losses

Q2/2021 Performance: Credit Gains & Duration Losses

The total return for the GFIS model portfolio (hedged into US dollars) in the second quarter was +1.13%, slightly underperformed the custom benchmark index by -6bps (Chart 1).1 In terms of the specific breakdown between the government bond and spread product allocations in our model portfolio, the former generated -21bps of underperformance versus our custom benchmark index while the latter outperformed by +15bps. We have remained significantly underweight US Treasuries and positioned for a bearish steepening of the US Treasury curve since just before last year's US presidential election. That tilt was a big contributor to the excess return of the portfolio in Q1 (+63bps) that was partially given back (-18bps) in Q2 as longer maturity Treasury yields fell during the quarter. Our inflation-linked bond allocations in the US and Europe (+5bps) helped mitigate the loss on the government bond side from our below-benchmark duration stance and general curve steepening bias in most countries in the portfolio (Table 2). Table 2GFIS Model Bond Portfolio Q2/2021 Overall Return Attribution

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

The sum of excess returns during the quarter from countries that we overweighted (Germany, France, Italy, Spain, and Japan) was zero. Improving growth momentum and stronger economic confidence helped push yields higher in those countries. Therefore, those positions could not offset the losses from the underweight to US Treasuries. We did make two shifts in the country allocation within the government bond portion of the portfolio during Q2, downgrading Canada to underweight on April 20 and upgrading Australia to overweight on June 9. Neither change meaningfully contributed to the return of the portfolio. Meanwhile, our moderate overall overweight tilt on spread product versus government bonds fueled the outperformance from the credit side of the portfolio, led by US high-yield (+11bps) and US CMBS (+3bps). Overall gains from spread product were impressive in both USD-hedged total return terms (+95bps) and relative to our custom benchmark (+15bps), despite spreads entering Q2 at fairly tight levels. In the second quarter, improving economic confidence and easing credit conditions allowed spreads to narrow even further for corporate debt in the US and Europe, as well as for EM USD-denominated credit. The bar charts showing the total and relative returns for each individual government bond market and spread product sector are presented in Charts 2 & 3. Chart 2GFIS Model Bond Portfolio Q2/2021 Government Bond Performance Attribution

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

Chart 3GFIS Model Bond Portfolio Q2/2021 Spread Product Performance Attribution By Sector

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

Biggest Outperformers: Overweight US high-yield: Ba-rated (+5bps), B-rated (+4bps), and Caa-rated (+3bps) Overweight US TIPS (+4bps) Overweight US CMBS (+3bps) Overweight Euro Area high-yield (+1bps) Biggest Underperformers: Underweight US Treasuries with a maturity greater than 10 years (-17bps), Underweight US Treasuries with a maturity between 7 and 10 years (-3bps) Underweight US Treasuries with a maturity between 5 and 7 years (-2bps) Underweight EM USD sovereigns (-1bps) Underweight UK GIlts with a maturity greater than 10 years (-1bps) Chart 4 presents the ranked benchmark index returns of the individual countries and spread product sectors in the GFIS model bond portfolio for Q2/2021. Returns are hedged into US dollars (we do not take active currency risk in this portfolio) and adjusted to reflect duration differences between each country/sector and the overall custom benchmark index for the model portfolio. We have also color coded the bars in each chart to reflect our recommended investment stance for each market during Q2 (red for underweight, dark green for overweight, gray for neutral). Chart 4Ranking The Winners & Losers From The GFIS Model Bond Portfolio Universe In Q2/2021

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

Ideally, we would look to see more green bars on the left side of the chart where market returns are highest, and more red bars on the right side of the chart were returns are lowest. In Q2, the picture on that front was mixed. We were only neutral some of the biggest outperformers like UK Gilts (+312bps in USD-hedged duration-matched total return terms) and investment grade credit in the US (+430bps) and UK (+231bps). Our relative value allocation within EM, overweight corporates (+430bps) versus sovereigns (+527bps), also underperformed during Q2. We remained overweight government debt markets in the euro area which were the worst performers during the quarter (Germany: -25bps, Spain: -59bps, Italy: -67bps, and France: -83bps). The news was better on the credit side, where our significant overweight to US high-yield (+146bps) was a big positive contributor, as were overweights to US CMBS (+137bps) and euro area high-yield (+92bps). Bottom Line: Our model bond portfolio slightly underperformed its benchmark index in the second quarter of the year by -6bps – a negative result mainly driven by our underweight allocation to the US Treasury market but with an overweight to US high-yield providing a meaningful offset. Future Drivers Of Portfolio Returns & Scenario Analysis Looking ahead, the performance of the model bond portfolio will continue to be driven primarily by swings in global government bond yields, most notably US Treasuries. Our most favored cyclical indicators for global bond yields are still, in aggregate, signaling more upside potential over at least the next six months, although the nature of the signal is changing (Chart 5). Our Global Duration Indicator, comprised of leading economic indicators and measures of future economic sentiment, remains elevated but appears to have peaked. At the same time, the global manufacturing PMI, which typically leads global real bond yields by around six months, continues to climb to new cyclical highs. This suggests that the recent downdraft in global real bond yields could prove to be short-lived. Our Global Central Bank Monitor is climbing steadily, indicating greater upward pressure on bond yields from the combination of strong growth, rising inflation and loose financial conditions. Admittedly, bond yields are lagging the upward trajectory implied by the Monitor with central banks deliberately responding far more slowly to the cyclical pressures that would have triggered bond-bearish monetary tightening in the past. Nonetheless, the Monitor, the Global Duration Indicator and the global manufacturing PMI and all sending the same message – global bond yields remain too low, suggesting a below-benchmark overall portfolio duration stance remains appropriate. With regards to country allocation within the government bond side of our model portfolio, we continue to overweight countries where central banks are less likely to begin normalizing pandemic-era monetary policy quickly (Germany, France, Italy, Spain, Japan, Australia), while underweighting countries where normalization is expected to begin within the next 6-12 months (the US and Canada). We remain neutral the UK, although we have them on “downgrade watch” until there is greater clarity on how severely the spread of the Delta variant is impacting UK growth. The US remains the biggest underweight. The modestly hawkish turn by the Fed at the June FOMC meeting likely marked the end of the cyclical bear-steepening trend of the US Treasury curve. A full-blown turn to a bear-flattening of the US curve will be slow to develop, but we fully expect the cyclical pressures that drove the underperformance of longer-maturity US Treasuries over the past year to begin leaking into shorter-maturity bonds. That trend already appears to be underway with 5-year US yields starting to drift upward at a faster pace compared to other developed market peers (Chart 6). Chart 5Cyclical Indicators Suggest Global Yields Still Have More Upside

Cyclical Indicators Suggest Global Yields Still Have More Upside

Cyclical Indicators Suggest Global Yields Still Have More Upside

Chart 6UST Underperformance Will Shift To Shorter Maturities

UST Underperformance Will Shift To Shorter Maturities

UST Underperformance Will Shift To Shorter Maturities

This leads us to make a change to our model portfolio allocations this week, reducing the exposure to the belly of the US Treasury curve (the 3-5 year and 5-7 year maturity buckets), while modestly increasing the allocation to the 7-10 year bucket. To neutralize the duration-extending implication of that marginal shift, we added a new allocation to US Treasury bills, thus turning this US Treasury shift into a “butterfly” trade, essentially selling the 5-year bullet for a cash/10-year barbell. Longer-term Treasury yields, however, are still in the process of working off an oversold condition that developed in Q1 (Chart 7). Duration positioning remains quite short, according to the JP Morgan survey of bond investors, while speculators are still working off a huge net short position in 30-year Treasury futures according to data from the CFTC. We anticipate that it will take another month or two to work off such an extreme oversold condition for US Treasuries, based on similar episodes over the past two decades. After that, longer-maturity Treasury yields will begin to begin climbing again, to the benefit of the US underweight (and below-benchmark duration stance) in our model portfolio. Chart 7Longer-Maturity USTs Working Off Oversold Condition

Longer-Maturity USTs Working Off Oversold Condition

Longer-Maturity USTs Working Off Oversold Condition

Chart 8A Sharply Diminished Impulse From Global QE

A Sharply Diminished Impulse From Global QE

A Sharply Diminished Impulse From Global QE

Outside the US, the bond-friendly impact of quantitative easing programs is fading, on the margin, with the growth of central bank balance sheets slowing (Chart 8). While outright tapering of bond buying has only occurred in Canada and the UK (within our model bond portfolio universe), we expect the Fed to begin tapering in early 2022. Financial stability concerns are expected to play an increasingly important role in future tapering decisions, with house prices booming in many countries, most notably Canada which supports our underweight stance on Canadian government debt. Australia is the notable exception to this trend towards slowing balance sheet growth, with the Reserve Bank of Australia (RBA) maintaining a healthy pace of bond buying given underwhelming realized inflation. The recent wave of COVID-19 cases, which has left half of Australia under lockdowns that were largely avoided in 2020, will ensure that the RBA stays dovish for longer, to the benefit of our overweight stance on Australian government bonds. We continue to see the overall dovish stance of global central bankers as being conducive to the outperformance of inflation-linked bonds versus nominal government debt. However, inflation breakevens in most countries have largely completed the rebound from the depressed levels reached during the 2020 COVID-19 global recession. Our Comprehensive Breakeven Indicators combine three measures to determine the upside potential for 10-year inflation breakevens: the distance from fair value based on our models, the spread between headline inflation and central bank target inflation, and the gap between market-based and survey-based measures of inflation expectations. Those indicators suggest that the most attractive markets to position for further upside potential for breakevens are in Italy and France, with breakevens looking more stretched in the US, Canada and Australia (Chart 9). On the back of this, we are maintaining our allocations to inflation-linked bonds in the euro area in our model portfolio. Chart 9Less Scope For Wider Global Inflation Breakevens

Less Scope For Wider Global Inflation Breakevens

Less Scope For Wider Global Inflation Breakevens

Chart 10Fading Support For Credit Markets From Global QE

Fading Support For Credit Markets From Global QE

Fading Support For Credit Markets From Global QE

Moving our attention to the credit side of our model portfolio, we feel that a moderate overweight stance on overall global corporates versus governments remains appropriate. However, the slowing trend in developed market central bank balance sheets, as an indicator of the incremental shift away from the COVID-era monetary policies from 2020, is flashing a warning sign for the performance of global spread product. The annual growth rate of the combined balance sheets of the Fed, ECB, Bank of Japan and Bank of England has been an excellent leading indicator of the excess returns of both global investment grade and high-yield corporates over the past decade (Chart 10). That growth rate peaked back in February of this year, suggesting a peak of global corporate bond excess returns around February 2022 Although given the current tight level of global corporate bond spreads, both for investment grade and high-yield, we expect future return outperformance from corporates versus government debt to come from carry rather than spread compression. Our preferred measure of the attractiveness of credit spreads is the historical percentile ranking of 12-month breakeven spreads, which measure how much spreads would need to widen to eliminate the carry advantage over duration-matched government bonds on a one-year horizon. Currently, only the lower-rated high-yield credit tiers in the US and euro area offer 12-month breakeven spreads above the bottom quartile of their history, within the credit sectors of our model portfolio (Chart 11). Chart 11Lower-Rated High-Yield Offers Relatively Attractive Spreads

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

Given the sharply reduced default risks on both sides of the Atlantic, and with nominal growth in good shape amid low borrowing rates, we are maintaining our overweights to high-yield bonds in both the US and euro area. At the same time, we are sticking with only a neutral stance on investment grade corporates in the US, euro area and the UK. We do anticipate starting to reduce the overall corporate bond exposure later this year, however, based on the ominous leading signal from the growth of central bank balance sheets – and what that signals about the future path for global monetary policy. Within the euro area, we continue to prefer owning Italian government bonds (and to a lesser extent, Spanish government debt) over investment grade corporates, given the more explicit support for the sovereigns through ECB quantitative easing (Chart 12). We expect the ECB to be the most accommodative central bank within our model portfolio universe over at least the next year, with even tapering of any kind unlikely in 2022. Chart 12Favor Italian BTPs Over Euro Area Investment Grade

Favor Italian BTPs Over Euro Area Investment Grade

Favor Italian BTPs Over Euro Area Investment Grade

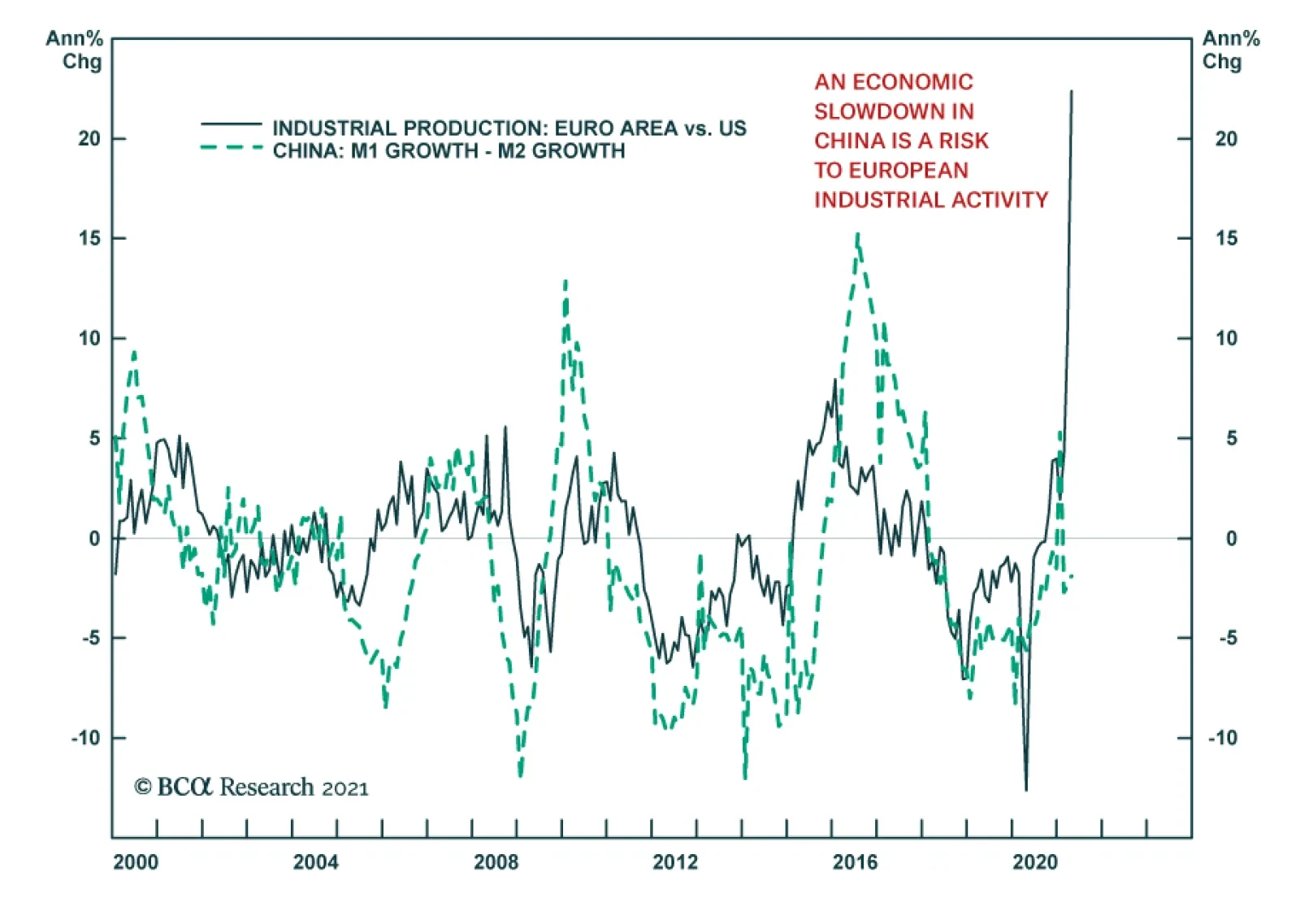

One area of the spread product universe where we are starting to reduce risk in the model portfolio is EM USD-denominated credit. EM debt has benefited from a bullish combination of global policy stimulus, a weakening US dollar and rising commodity prices over the past year. We have positioned for that in our model portfolio through an overall overweight stance on EM USD-denominated debt, but one that favors investment grade corporates over sovereigns. Now, all of those supportive factors for EM credit are fading. Chinese policymakers have reigned in both credit stimulus and fiscal stimulus this year, with the combined impulse suggesting a slower pace of Chinese economic growth in the latter half of 2021 (Chart 13). Given China’s huge share of the global consumption of industrial commodities, slowing Chinese growth should cool the momentum of commodity prices over the next few quarters. A slowing liquidity impulse from global central bank asset purchases is also a negative for EM debt performance, on the margin. The same can be said for the US dollar, which is no longer depreciating as markets start to pull forward the expected future path for US interest rates (Chart 14). A stronger US dollar typically correlates with softer commodity prices and wider EM credit spreads. Chart 13Major EM Risks: China Tightening & Global QE Tapering

Major EM Risks: China Tightening & Global QE Tapering

Major EM Risks: China Tightening & Global QE Tapering

Chart 14EM Supportive USD Weakness Is Fading

EM Supportive USD Weakness Is Fading

EM Supportive USD Weakness Is Fading

In response to these growing risks to the bullish EM backdrop - including the rapid spread of the Delta variant made worse by the less-effective vaccines available in those countries - we are downgrading our overall EM USD credit exposure in the model bond portfolio to underweight from neutral. We are doing this by cutting the EM corporate exposure from overweight to neutral, while maintaining an underweight tilt on EM USD sovereigns. We expect to further cut the EM exposure in the coming months by moving to a full underweight on EM corporates. Summing it all up, our overall allocations and risks in our model portfolio leading into Q3/2021 look like this: An overall below-benchmark stance on global duration, equal to nearly one full year versus the custom index (Chart 15) A moderate overweight stance on global spread product versus government debt, equal to five percentage points of the portfolio (Chart 16). This overweight comes almost entirely from overweight allocations to US and euro area high-yield corporate debt. Chart 15Overall Portfolio Duration: Stay Below Benchmark

Overall Portfolio Duration: Stay Below Benchmark

Overall Portfolio Duration: Stay Below Benchmark

Chart 16Overall Portfolio Allocation: Small Spread Product Overweight

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

After the changes made to our US Treasury and EM positions, the tracking error of the portfolio, or its expected volatility versus that of the benchmark index, is quite low at 34bps (Chart 17). The main reason for this is that our positioning remains focused heavily on the US (Treasury underweight, high-yield overweight), with much of the other positioning close to neutral or largely offsetting other positions in a relative value sense (overweight Australia vs underweight Canada, overweight US CMBS versus underweight US Agency MBS). This fits with our desire to maintain only a moderate level of overall portfolio risk. The yield of the portfolio is now slightly higher than that of the benchmark, with a small “positive carry”, hedged into USD, of 13bps (Chart 18). Chart 17Overall Portfolio Risk: Moderate

Overall Portfolio Risk: Moderate

Overall Portfolio Risk: Moderate

Chart 18Overall Portfolio Yield: Small Positive Carry Vs. Benchmark

Overall Portfolio Yield: Small Positive Carry Vs. Benchmark

Overall Portfolio Yield: Small Positive Carry Vs. Benchmark

Scenario Analysis & Return Forecasts After making the shifts to our model bond portfolio allocations in the US and EM, we now turn to scenario analysis to determine the return expectations for the portfolio for the next six months. On the credit side of the portfolio, we use risk-factor-based regression models to forecast future yield changes for global spread product sectors as a function of four major factors - the VIX, oil prices, the US dollar and the fed funds rate (Table 2A). For the government bond side of the portfolio, we avoid using regression models and instead use a yield-beta driven framework, taking forecasts for changes in US Treasury yields and translating those in changes in non-US bond yields by applying a historical yield beta (Table 2B). For our scenario analysis over the next six months, we use a base case scenario plus two alternate “tail risk” scenarios. We see global growth momentum and the Fed monetary policy outlook as the two most important factors for fixed income markets in the second half of 2021, thus our scenarios are defined along those lines. Table 2AFactor Regressions Used To Estimate Spread Product Yield Changes

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

Table 2BEstimated Government Bond Yield Betas To US Treasuries

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

Base Case Global growth stays above-trend in both Q3 and Q4, putting downward pressure on unemployment rates and keeping realized inflation elevated. Ongoing global vaccinations lead to more of the global economy fully reopening, with the Delta variant not having serious widespread impact on economic confidence outside of parts of the emerging world. Excess savings built up during the pandemic are run down by both consumers and businesses as optimism stays ebullient within the developed economies. China credit tightening slows growth enough to cool off upward commodity price momentum. At the same time, falling US unemployment and surprisingly “sticky” domestic US realized inflation embolden the Fed to signal a move to begin tapering its bond purchases starting in January 2022. Real bond yields globally bottom out, while inflation expectations recover some of the pullback seen in Q2/2021. The entire US Treasury curve shifts higher, led by the 10-year reaching 1.65% and a modest bear-flattening of the 5-year/30-year curve. The VIX stays near 15, the US dollar rises +3%, the Brent oil price goes nowhere and the fed funds rate is unchanged at 0% Upside Growth Surprise The Delta variant proves to be far less deadly than feared. A rapid pace of global vaccinations leads to booming growth led by the US but including a fully reopened euro area. Chinese policymakers begin to reverse some of the H1/2021 credit tightening. Unemployment rates rapidly fall worldwide, while supply bottlenecks persist, keeping upward pressure on realized inflation. Markets pull forward the timing and pace of future central bank interest rate hikes, most notably in the US when the Fed begins tapering bond purchases sooner than expected before year-end. Real bond yields drift higher globally, but inflation breakevens stay elevated with the earlier surge in realized inflation proving not to be “transitory”. The US Treasury curve modestly bear-flattens, with the 10-year reaching 1.9% and the 5-year/30-year spread narrowing by 25bps. The VIX rises to 25 as risk assets struggle in response to rising bond yields even with faster growth. The US dollar falls -5% on the back of improving global growth expectations, the Brent oil price climbs +5% and the fed funds rate stays unchanged. Downside Growth Surprise The global economy gets hit on multiple fronts: the rapid spread of the Delta variant overwhelms the positive momentum on vaccinations, most notably in EM countries; Europe struggles to fully reopen; China policy tightening results in a larger-than-expected drag on global growth; and US households are reluctant to draw down on excess savings after government income support measures expire in September. Diminished economic optimism leads to a pullback in global equity values, lower government bond yields and wider global credit spreads. The US Treasury curve bull flattens as longer-maturity yields fall in a risk-off move, with the 10-year yield moving back down to 1.25% alongside lower inflation breakevens. The VIX rises to 30, the safe-haven US dollar rises +5%, the Brent oil price falls -10% and the fed funds rate stays at 0%. Chart 19Risk Factor Assumptions For The Scenario Analysis

Risk Factor Assumptions For The Scenario Analysis

Risk Factor Assumptions For The Scenario Analysis

Chart 20US Treasury Yield Assumptions For The Scenario Analysis

US Treasury Yield Assumptions For The Scenario Analysis

US Treasury Yield Assumptions For The Scenario Analysis

The inputs into the scenario analysis are shown in Chart 19 (for the USD, VIX, oil and the fed funds rate), while the US Treasury yield scenarios are in Chart 20. The excess return scenarios for the model bond portfolio, using the above inputs in our simple quantitative return forecast framework, are shown in Table 3A (the scenarios for the changes in US Treasury yields are shown in Table 3B). Table 3AGFIS Model Bond Portfolio Scenario Analysis For The Next Six Months

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

Table 3BUS Treasury Yield Assumptions For The 6-Month Forward Scenario Analysis

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

The model bond portfolio is expected to deliver a positive excess return over the next six months of +46bps in the base case scenario and +28bps in the optimistic growth scenario, but is projected to underperform by -36bps in the pessimistic growth scenario. Bottom Line: We are maintaining an overall below-benchmark portfolio duration stance, against a backdrop of persistent above-trend global growth and a highly stimulative fiscal/monetary policy mix. We are maintaining a moderate overweight to global spread product versus government debt, concentrated on an overweight to US high-yield where valuations look the least stretched. We are making two changes to the portfolio allocations heading into Q3: shifting the Treasury curve exposure to have more of a flattening bias, while downgrading EM USD-denominated corporates to neutral. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Ray Park, CFA Research Analyst ray@bcaresearch.com Footnotes 1 The GFIS model bond portfolio custom benchmark index is the Bloomberg Barclays Global Aggregate Index, but with allocations to global high-yield corporate debt replacing very high-quality spread product (i.e. AA-rated). We believe this to be more indicative of the typical internal benchmark used by global multi-sector fixed income managers. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

GFIS Model Bond Portfolio Q2/2021 Performance Review & Current Allocations: Hitting A Few Roadblocks

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

The French presidential election is nine months away, and it is already starting to catch investors’ attention as one of the main political events in Europe in 2022. According to BCA Research’s European Investment Strategy & Geopolitical Strategy…

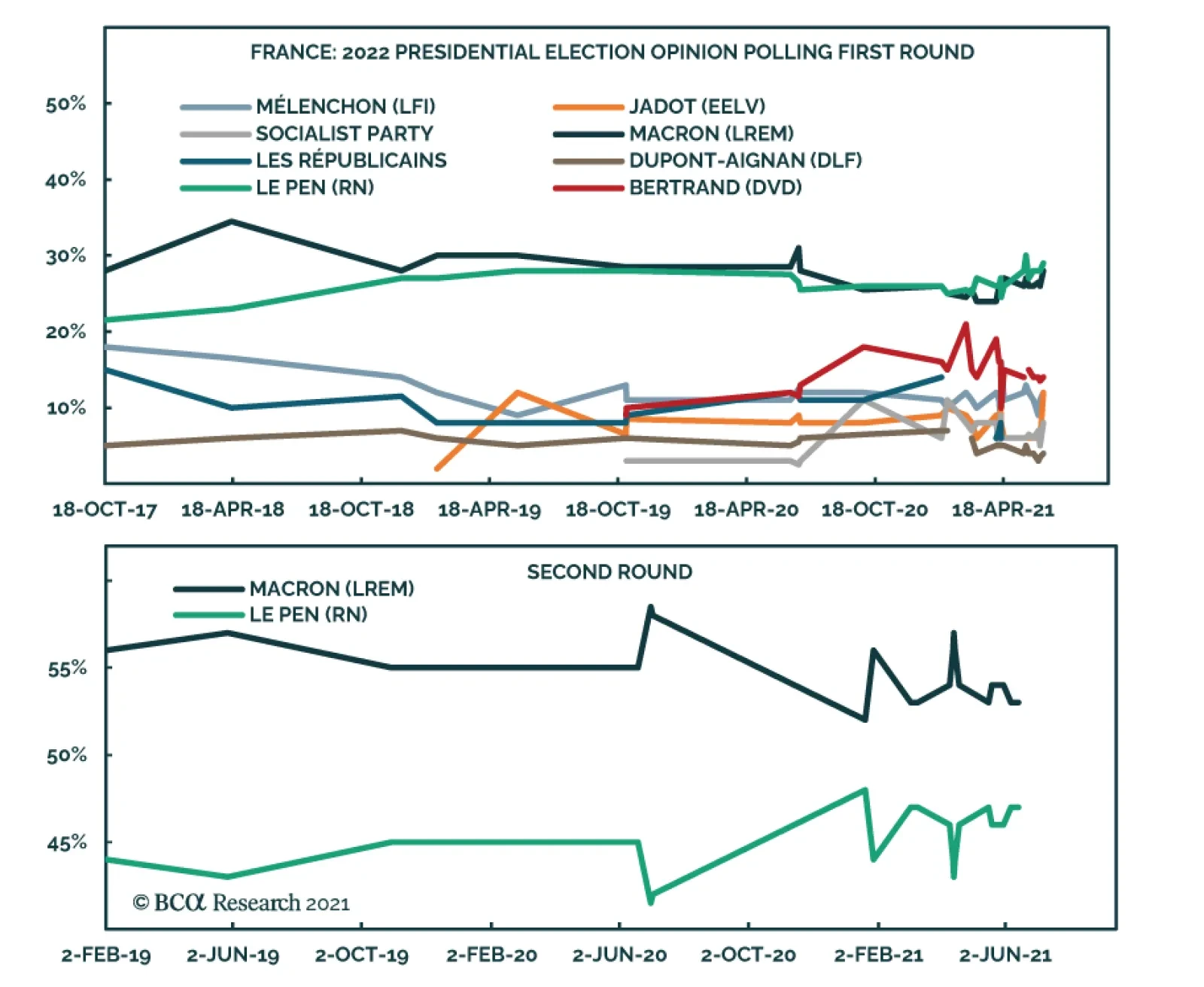

Highlights Barring major surprises, President Macron will be re-elected in 2022. Any dramatic reversal in the pandemic that leads to a new recession would benefit the opposition candidate. Otherwise, Macron will remain the frontrunner. A second term for President Macron would see a continuation of the structural reforms started in 2017, but with a longer process for coalition-building in the National Assembly. This is bullish for France. Reducing the size of the state will go a long way to improve France’s economic competitiveness over the long run. Tactically, favor the more defensive Spanish market over the highly cyclical French market. Underweight French consumer discretionary equities relative to their European and global peers. Longer term, overweight French industrials equities relative to German ones, and overweight French tech equities relative to European ones. Ahead of the election, buy the dip on any euro weakness and French OAT/German bund spread widening. Feature The French presidential election is nine months away, and it is already starting to catch investors’ attention as one of the main political events in Europe in 2022. In talks with clients, we’ve been asked repeatedly about the odds we assign to a Marine Le Pen victory and the market implications. Those concerns are understandable but overrated. Le Pen’s personal approval rating is on the rise, and, in most polls, the far-right candidate beats President Emmanuel Macron in the first round vote, although not the critical second round. Although the same polls see Macron being re-elected, the gap between the two has narrowed considerably since the 2017 election, which Macron won by 66 percent of the vote. Still, Macron is favored for re-election. He has several strong advantages over Le Pen, and it is unlikely she will be able to close the gap further before the election. Macron’s first term has been eventful. Neoliberal structural reforms started with drums beating in the first 18 months of his term. But the pace and breadth of reform eventually became too ambitious or painful for France to bear, and protests erupted in 2018. First came the “Yellow Vest Movement,” and then came protests against pension reform. Macron tried to compromise and continue with his agenda, but COVID-19 forced his hand. Since then, Macron has focused on crisis management, benefiting from the large state sector’s role as an automatic stabilizer amid the downturn. A second term under President Macron would see a reboot of the structural reforms started in 2017, albeit without single-party rule in the National Assembly. Reforms aimed at reducing the size of the state, and its cost, would go a long way to improve France’s economic competitiveness over the long run. Therefore, the prospect of Macron’s reelection is bullish for France, even though the reality of his second term would be more complex. 2017 All Over Again? Yes And No At first glance, the 2022 election seems to be a repeat of 2017. Le Pen and Macron are likely to face off in the second round and the latter, the Europhile centrist candidate, is likely to win once more. However, everything surrounding this election has changed. The Incumbency Effect One of the major changes is favorable for Macron: he is the incumbent running for re-election. Macron had been part of President Francois Hollande’s government since 2014, so he was still viewed in 2017 as a political neophyte and dark horse candidate. His rapid rise to power, along with that of his upstart party, La République En Marche (LREM), was astounding. Chart 1Pro-Incumbency Effect Favors Macron

France: More Than Just A Déjà-Vu

France: More Than Just A Déjà-Vu

There is a strong pro-incumbency effect in French presidential elections, especially in the first round (Chart 1). Since 1965, five incumbents have run for re-election, and all have made it to the second round. Importantly, four won first place in the first round, with a six percentage-point margin on average. The chief exception is Nicolas Sarkozy in 2012. The reason for Sarkozy’s loss, however, is well known: he attempted to pass an unpopular pension reform in the teeth of the Euro debt crisis, 12 months before facing re-election. The only other incumbent who failed at re-election was Valerie Giscard d’Estaing, who lost to Francois Mitterrand in 1981, when the whole world was in stagflation and upheaval. The incumbency effect is not as pronounced in the second round (Chart 1, bottom panel). However, when facing a far-right candidate, incumbents win by a wide margin. This was the case in 2002 and 2017. Today, Macron still has a 12-point lead on Le Pen. Macron compares well to his predecessors. Chart 2 shows the approval rating for all presidents sitting in office over the past 40 years. The number of people who intend to vote for Macron has increased, the first time this has happened for an incumbent president since 1988. Only three presidents had a higher approval rating at this stage of their term, albeit from a higher starting point. Macron’s approval rating has increased by 10% since February 2020, when the COVID-19 pandemic hit Europe. Chart 2Macron Compares Well To His Predecessors

France: More Than Just A Déjà-Vu

France: More Than Just A Déjà-Vu

Table 1Incumbency And Recessions Under The Fifth Republic

France: More Than Just A Déjà-Vu

France: More Than Just A Déjà-Vu

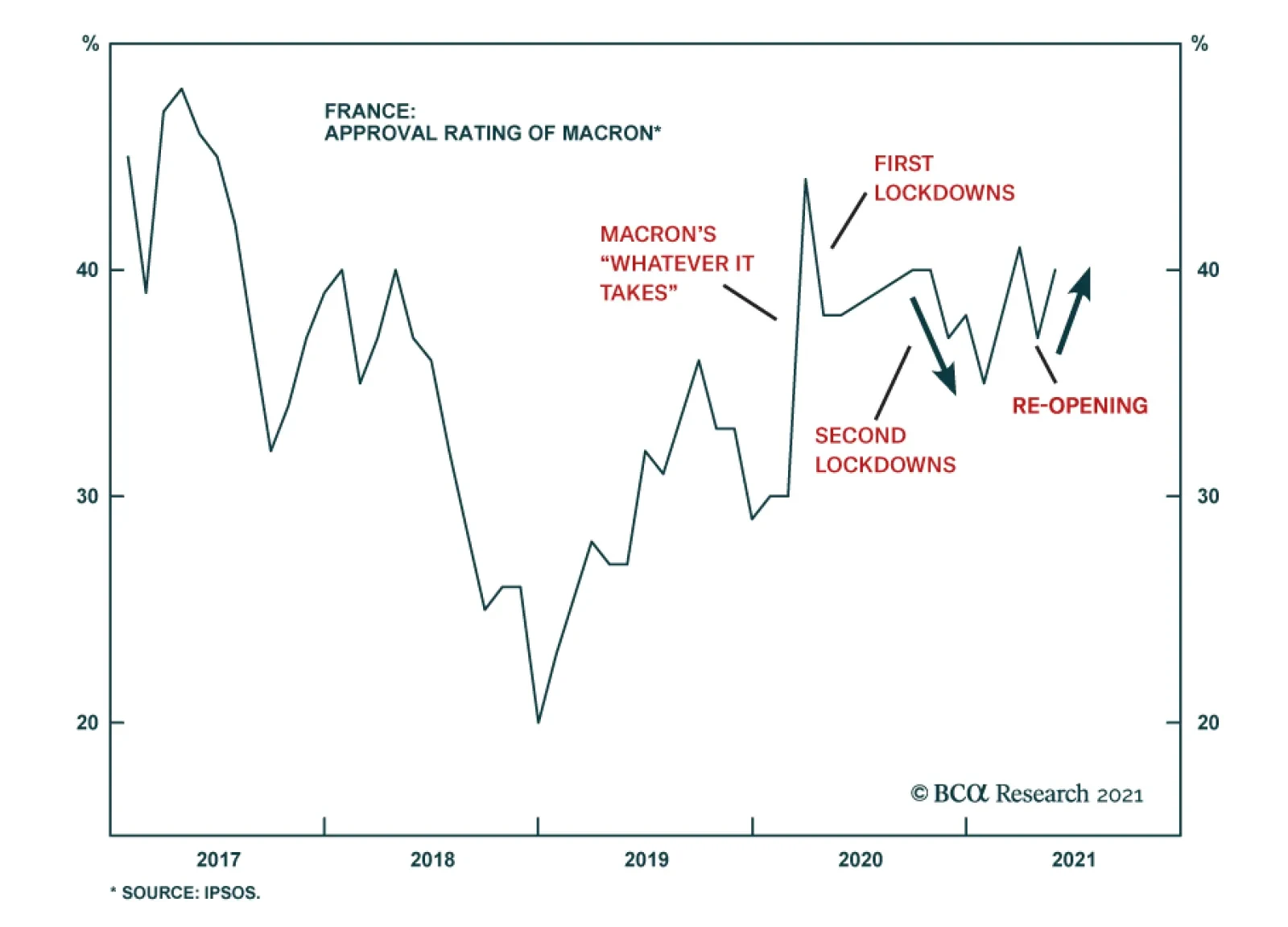

The shock of the pandemic and recession is the greatest change since 2017, and the biggest challenge facing Macron. Four incumbents have made a bid for re-election that was preceded by a recession within 12-24 months (Table 1). The results are mixed, and it is hard to establish a clear anti-incumbency effect. If anything, the timing and nature of this crisis are likely to help Macron rather than hurt him, since the vaccination campaign and easing of lockdown measures will enable the economy to normalize and improve ahead of April 10-24, 2022, when voters cast their first ballots. Nonetheless, another major shock (of any kind) could undermine the incumbent advantage. Economic Recovery Is The Top Priority While the Macron administration’s handling of the pandemic was questioned, public opinion was never aggressively hostile toward his handling of the economy. Macron was instrumental in securing a major European fiscal stimulus package (and joint debt issuance) with the German Chancellor, Angela Merkel. He enthusiastically adopted the crisis mentality of “whatever it takes” to wage war against COVID-19, enabling the oversized French state to deploy the most generous furlough scheme in Europe, shielding millions of workers and preventing businesses from going under. This will be one of his winning cards. Chart 3The Handling Of The Pandemic Dictates Macron's Popularity

The Handling Of The Pandemic Dictates Macron's Popularity

The Handling Of The Pandemic Dictates Macron's Popularity

His approval rating began to rebound following the end of lockdowns (Chart 3). This trend should strengthen as the French economy reopens, supported by a government that will play an accommodative and reflationary economic role until the election. Public opinion wants him to focus on the labor market and the economic recovery in the months to come, and he will be happy to oblige. Public opinion also views Macron as the most qualified candidate when it comes to economic matters (Table 2). 42% of respondents think that Le Pen is not qualified “at all” on economic matters, her Achilles’ heel, a perception that was already entrenched when Macron crushed her in a televised debate before the second round of the 2017 election. Table 2Macron Is Perceived As The Most Qualified To Oversee The Economic Recovery

France: More Than Just A Déjà-Vu

France: More Than Just A Déjà-Vu

Europhile Versus Eurosceptic? The central issue of the 2017 election was Europe and France’s role in it. Following the UK’s disruptive Brexit referendum in 2016, and a long tradition of Euroscepticism within her party, Le Pen campaigned on “Frexit” and the abandonment of the euro. Conversely, Macron embraced the EU and the monetary union as he ran for president and committed to having France play a more important role within the bloc if he won. Chart 4Le Pen And The EU: Not The Divorce We Expected

Le Pen And The EU: Not The Divorce We Expected

Le Pen And The EU: Not The Divorce We Expected

Since then, Le Pen has drastically shifted her stance on the EU. She now claims that the benefits of the common currency and single market outweigh the costs. After all, 70% of the French public support the euro and EU membership (Chart 4). Like clockwork, her personal approval ratings have steadily gone up. This strategic shift aligns her with the median voter, and combined with the Covid crisis, it is the only reason to take her candidacy remotely seriously in 2022, despite Macron’s clear advantages. Nevertheless, Le Pen has not yet risen above her 2012 peak in popular support. She failed to do so between 2014 and 2015, when the lingering European debt crisis, the Syrian refugee crisis, multiple terrorist attacks in France, and sluggish economic growth should have boosted her popularity. Her shifting perspective on the euro was therefore necessary and might be just what she needs to break through her 37% ceiling of popular support. Le Pen’s policy agenda is now focusing on protectionism, immigration, and national security. It is a Trumpian mix. However, while her new stance is more mainstream, it also differentiates her less from the other center-right politicians in France, namely Xavier Bertrand, who recently made local electoral gains in Le Pen’s northern industrial base. Macron is as strong an advocate for Europe as ever. He convinced Germany to break the taboo on joint fiscal policy during the pandemic. Now, he is also mounting a bid to become the natural leader of Europe, given that Merkel is stepping down, and her party is likely to lose standing in the German election in September. France is set to take over the rotating EU Council Presidency in the first half of 2022, under the theme “Recovery, power, belonging,” which provides Macron with a golden opportunity to pitch himself as Europe’s premier statesman and economic steward in the final months of the election campaign. One Thing Hasn’t Changed: The Outcome Of A Macron/Le Pen Duel Most opinion polls give Macron a 10-12 point lead on Le Pen in the second round of the election. This gap is wide enough to reassure investors that it is not a polling error. However, in 2017, Macron’s average lead over Le Pen was 22%, and he won the election with 66% of votes. It is the narrowing of that gap that raises eyebrows among investors. Table 3Ideological Blocs Also Favor Macron

France: More Than Just A Déjà-Vu

France: More Than Just A Déjà-Vu

Still, Le Pen’s chances at closing the gap are overrated. She is not a political “unknown” anymore and has very little ability to “surprise” voters into rallying around her next year. She will have trouble persuading those who know all about her. Grouping French voters according to ideological blocs, that is, presidential preference by party affiliation, suggests that the biggest threat to Macron is a strong center-right candidate who can beat Le Pen, especially if this should coincide with a revival of the center-left (Table 3). Otherwise, as in 2017, Macron will be able to count on voters from other parties in the second round of the election (Table 4). While both candidates appeal to right-wing constituents and would have to share their ballots, Macron can count on the green EELV party, as well as left-wing voters, to join center-right voters to elect him. Macron has made environmental issues a part of his mandate, which should help him confront a green neophyte such as Le Pen. Table 4Voting Against Le Pen Implies Voting For Macron

France: More Than Just A Déjà-Vu

France: More Than Just A Déjà-Vu

The results of the regional elections held last month confirm this analysis. The motivation to keep Le Pen and her Rassemblement National (National Rally) party out of power is still strong (see Box 1). The poor showing of the National Rally means she won’t be able to maintain her current momentum in her personal approval ratings. Box 1 2021 Regional Elections: Bad Omen For Marine Le Pen In Revival Of The Center-Right? The regional elections took place on June 20 and 27. While limited in relevance for the 2022 presidential race, the result of extremely low voter turnout, regional elections offer a gauge of how constituents feel about the political offerings from anti-establishment parties. Le Pen’s party suffered a heavy blow. It had hoped to consolidate power and build momentum ahead of the presidential election, but it failed even to win in its stronghold of Southern France. Meanwhile, Macron’s party (La République En Marche!) also disappointed. This outcome is not surprising; the local elections last year yielded similar results, highlighting the lack of presence at the local and regional levels for the four-year-old party. The surprise came from the center-right. It managed to win seven of the thirteen regions, beating far-right candidates by wide margins. Importantly, Xavier Bertand, Valérie Pécresse, and Laurent Wauquiez, all predicted to run for president next year, held onto their seats. Chart 5Strong Demographic Base In The Second Round

France: More Than Just A Déjà-Vu

France: More Than Just A Déjà-Vu

Both candidates’ demographic bases have remained the same. Macron is still popular among Millennials, white collar workers, and the elderly (Chart 5). He also has a strong base in Paris (and the suburbs) as opposed to Le Pen, and he still outperforms Le Pen among rural voters in today’s polls. Macron also scores high among the employees of the public sector—even though he is in favor of a smaller public sector. Furthermore, the unemployed mostly favor him, which reinforces the perception that he is the best candidate to improve the French economy and cut the unemployment rate. What if Le Pen fails to make it into the second round of the election? We discuss this possibility in the next section. Risks To The Base Case Scenario The greatest risks to our view are a setback in the economic recovery, an outperformance from the center-right, and the emergence of a dark horse. The latest developments in the UK and Israel, where a large share of the population is fully vaccinated, suggest that the “Delta” variant of COVID-19 remains a threat, with the potential to send economies back into lockdowns. The consequences would be dire for Macron. His chances at re-election would likely evaporate if his government imposed new lockdown measures. What about presidential candidates other than Le Pen? Our base case scenario that Macron will win is based on two assumptions: (1) the center-left Socialist Party will remain in shambles, and (2) the center-right remains scattered under different banners and will therefore lack unity. There is very little chance that the center-left will make a comeback in time, but the results from the regional elections suggest that the center-right could surprise to the upside (see Box 1), especially if it decides to rally behind a single candidate ahead of the first round. Could this candidate be a dark horse? Former Prime Minister Edouard Philippe or outsider candidate Xavier Bertrand could make formidable opponents to both Macron and Le Pen. Philippe’s personal approval rating currently stands at 50%, the highest among French politicians. He also appeals to constituents of all political leanings (Chart 6). This scenario could reshuffle the likely outcomes of both the first and second round of the election. Both Bertand and Philippe could win over voters who decided to side with Le Pen in 2017, while Philippe can compete with Macron over LREM voters. Additionally, Xavier Bertrand cuts into Le Pen’s support since he has made blue collar workers and the middle-class a priority. However, Macron and Le Pen each enjoy a strong voters’ base. It is necessary to monitor whether Valérie Pécresse (Soyons libres) and Laurent Wauquiez (Les Républicains) can be brought to endorse Xavier Bertrand ahead of the first round in 2022. Chart 6Edouard Philippe: From Ally To Outcast To Challenger?

France: More Than Just A Déjà-Vu

France: More Than Just A Déjà-Vu

Beyond The Election Aside from the presidency, the outstanding question is the makeup of the National Assembly in 2022. Macron is not likely to enjoy the strong single-party legislative majority of his first term or to gain control of the Senate. Consequently, he will be more constrained in the legislature in a second term. Nonetheless, the demand for a better economy and a healthier job market requires pro-productivity reforms, which the public knows, and Macron has made reform his banner. Other conventional parties will come under pressure to support Macron’s reform agenda, even though that agenda will be less ambitious than it was in his first term. Chart 7Strong Presence Of Right-Leaning Forces

Strong Presence Of Right-Leaning Forces

Strong Presence Of Right-Leaning Forces

Efforts at cutting back the size of the state are still likely, even though the pandemic has helped rather than hurt statism. This is because the French median voter, who never witnessed the degree of neoliberal reform that took place in the Anglo-Saxon world, has grown weary of the economy’s inefficiencies, just as the Anglo-Saxons have grown weary of laissez-faire neoliberalism. Before the pandemic, the French people understood the need to reduce the size of the state. After all, a larger state implies a larger cost burden borne by both households and corporations. When faced with the choice between paying the bill for the government’s fiscal response to COVID-19 (through higher taxes), or undertaking reforms aiming at reducing the size of the state, the French people will pick the former. Moreover, centrist forces will hold sway in the legislature (Chart 7); hence, some kind of budget normalization is expected in 2023 or thereafter. Other structural reforms If Macron wins would include pension reforms. We should also expect measures to push French companies to bring activities back to France, as well as a greater focus on leading France on the green path. Bottom Line: Barring major surprises, President Macron will be re-elected in 2022. There is a risk to our view if a center-right candidate defeats Le Pen to make it to the second round of the election. Either Macron or a center-right presidency would see a continuation of the structural reforms started in 2017, but with a longer process for coalition-building in the National Assembly. Investment Implications The French economy is currently experiencing an economic upswing. Three factors explain this pick-up: ultra-accommodative monetary conditions in Europe, fiscal largesse, and considerable pent-up demand. In 2021, GDP is projected to expand by 5.75% in annual average terms, higher than the Euro Area average of 4.6%. It should then grow by 4% in 2022 and by 2% in 2023. We remain bullish on French equities on a secular basis, as long as the elections result in further incremental structural reforms over time. As the election draws nearer, investors should treat any French OAT/German Bund spread widening as a buying opportunity and purchase the euro on any election-related dip. French Equities The CAC40 and French equities have had a good run since the beginning of the year. In absolute terms, the CAC40 is one of the best performers year-to-date, up +17%, driven by the outperformance of French consumer discretionary and financials equities, both in absolute and relative terms. However, a period of turbulence is appearing on the horizon; the shift in global growth drivers, the beginning of the global liquidity withdrawal, and lingering COVID worries are creating headwinds for the cyclicals-to-defensives ratio this summer. As such, we recently recommended investors downgrade cyclical equities tactically in Europe from overweight to neutral. With 66% in cyclicals, the French MSCI equity index will underperform in this environment, especially relative to the more defensive Spanish market (Table 5). Table 5Cyclicals Versus Defensives In European Markets

France: More Than Just A Déjà-Vu

France: More Than Just A Déjà-Vu

Chart 8Three Trade Ideas

Three Trade Ideas

Three Trade Ideas

In fact, our Combined Mechanical Valuation Indicator (CMVI) shows that French consumer discretionary equities are expensive relative to both their European and global peers (Chart 8). Regarding the reform theme, we stick with our long French industrial equities / short German industrial equities on a long-term horizon (Chart 8, second and third panel). The idea is that French reforms should suppress unit labor costs and make French exports more competitive vis-à-vis their main competitor, Germany. The latter faces a leftward shift in policy in elections this September. Finally, we recommend investors go long French tech stocks relative to their European counterparts. This sector is cheap (Chart 8, bottom panel), and the French tech sector will be supported by additional government spending of EUR7 billion on digital investments over the next two years. Bond Markets & FX A dovish ECB is consistent with a continued overweight in European peripheral bonds and an underweight stance on French government bonds. Chart 9Just Buy The Dip

Just Buy The Dip

Just Buy The Dip

What is more relevant with respect to the French election is the OAT/Bund spread. In the past, unusually wide spreads between the two represented a euro breakup premium. In early 2017, spreads widened when the approval rating of Le Pen increased (Chart 9). However, since “Frexit” and the abandonment of the euro are no longer part of Le Pen’s agenda, investors should view spread widening as a buying opportunity. Similarly, investors should buy the euro on any election-related dip, particularly following the first round. “Frexit” has been removed from the equation, hence the euro should not weaken on breakup risk this time around. Bottom Line: We remain bullish on French equities within a European portfolio on a secular basis. If our views on the cyclicals-to-defensives ratio materialize in the near-term, highly cyclical French equities will temporarily underperform, unlike the more defensive Spanish market. On a 3- to 12-month horizon, investors should short French consumer discretionary equities relative to both their European and global counterparts. Current valuations suggest that betting on the booming French tech sector at the expense of its European neighbors will be profitable. Once the election draws nearer, investors should treat any French OAT/German Bund spread widening as a buying opportunity and purchase the euro on any election-related dip. Jeremie Peloso, Associate Editor JeremieP@bcaresearch.com

This week, we present the third edition of the BCA Research Global Fixed Income Strategy (GFIS) Global Credit Conditions Chartbook—a review of central bank surveys of bank lending standards and loan demand. The data from lending surveys during the first quarter of 2021 point towards easing standards in developed markets (Chart 1). Credit standards for business loans eased outright in most regions except for the euro area and New Zealand where the pace of tightening slowed significantly. On the whole, banks expected the easing trend to continue into Q2. Chart 1Credit Standards Moving Towards Or Deeper Into Easy Territory

Credit Standards Moving Towards Or Deeper Into Easy Territory

Credit Standards Moving Towards Or Deeper Into Easy Territory

With credit spreads at historical tights, banks across the board cited increased competition from other lenders as a reason behind easing standards, confirming that easy financial conditions are not limited solely to booming financial markets. This will help maintain a market-friendly economic growth backdrop as developed economies put pandemic restrictions behind them. At the same time, an absence of tightening lending standards by commercial banks puts incremental pressure on central banks to move towards bond-bearish tightenings of monetary policy. An Overview Of Global Credit Conditions Surveys Chart 2Credit Standards And Spreads Are Correlated

Credit Standards And Spreads Are Correlated

Credit Standards And Spreads Are Correlated

After every quarter, major central banks compile surveys to assess prevailing credit conditions. The purpose is to obtain from banks an assessment of how their lending standards and demand for loans, for both firms and consumers, changed over the previous quarter. Most surveys also ask questions about the key factors driving these changes and expectations for the next quarter.1 For fixed income investors, these surveys are valuable for a few reasons. Firstly, data on consumer lending is a window into consumer health while business loan demand sheds light on the investment picture. These help derive a view on the path of future economic growth and interest rates and, thus, the appropriate duration stance of a bond portfolio. Also, credit standards can tell us about the pass-through from fiscal and monetary policy measures to realized financial conditions (i.e. corporate borrowing rates). Most importantly, credit standards exhibit a direct correlation with corporate bond spreads (Chart 2). As loan officers have access to detailed, non-public information on a large number of borrowers, they are uniquely positioned to evaluate corporate health. When banks are tightening standards, they see an issue with the credit quality of current or future loans, which impacts borrowing costs in the corporate bond market. Tightening standards indicate a worsening borrowing backdrop and weaker growth, which then pushes up corporate spreads. Vice versa, easing standards imply a favorable backdrop and plentiful liquidity—both bullish signs for spread product. US In the US, a net percentage of domestic respondents to the Fed’s Senior Loan Officer Survey, reported easing standards for commercial and industrial (C&I) loans to firms of all sizes over Q1/2021 (Chart 3). Nearly 20% of respondents cited an improving or less uncertain economic outlook as a very important factor behind the decision to ease standards, while roughly one-third cited increased competition from other lenders. Chart 3US Credit Conditions

US Credit Conditions

US Credit Conditions

Chart 4High-yield Borrowers Are Exposed To A Widening In Spreads

High-yield Borrowers Are Exposed To A Widening In Spreads

High-yield Borrowers Are Exposed To A Widening In Spreads

Although it did not strengthen on net, C&I loan demand did weaken at a much slower pace in Q1. The factors driving loan demand suggest a buoyant economic backdrop—about a quarter of banks reporting increased demand cited merger and acquisition needs and increased investment as very important reasons. Meanwhile, weaker loan demand was attributed to less precautionary demand for cash and an increase in internally generated funds among customers. On the consumer side, loan demand improved slightly on the whole, driven largely by a significant improvement in auto loan demand. While consumer loan demand has historically correlated well with the year-over-year growth in personal consumption expenditures, those two series diverged remarkably in Q1, with spending growth far outpacing loan growth. This divergence reflects the tremendous impact of pandemic-related transfer payments and benefits. We expect a continued recovery in consumer lending demand as unemployment benefits are withdrawn and consumers once again have to borrow to finance spending. As part of the special ad-hoc questions in this edition of the survey, respondents were asked about how lending standards had changed compared to the pre-pandemic period by borrower risk rating. Interestingly, large banks actually eased their standards for investment grade borrowers, reflecting the impact of Fed’s massive liquidity injections (Chart 4). However, despite spreads on high-yield having tightened to post-GFC lows, credit standards for below-investment grade borrowers remain much tighter than before the pandemic. So far, lower-quality borrowers have been able to go to public debt markets for financing, but this highlights a downside risk—if there is an event which causes corporate bond spreads to widen, high-yield borrowers may be starved of cheap financing options with banks still holding purse strings taut. Euro Area In the euro area, banks continued to tighten standards to enterprises, albeit at a much-reduced pace, in Q1/2021 (Chart 5). The tightening, however, was lower than expected in the previous quarter, possibly reflecting prolonged policy support and improving risk sentiment. Deteriorating risk perceptions related to the general economic and firm-specific situation were the primary contributing factor to tightening. But this was partly offset by increased competition from other lenders. The reduced pace of tightening does confirm the signal from the high-yield default rate, which is rolling over. Going forward, banks expect the pace of tightening to slow very slightly going into Q2. Chart 5Euro Area Credit Conditions

Euro Area Credit Conditions

Euro Area Credit Conditions

Chart 6Credit Standards For Major Euro Area Economies

Credit Standards For Major Euro Area Economies

Credit Standards For Major Euro Area Economies

Business credit demand continued to weaken at a faster pace in Q1, marking three consecutive quarters of deterioration. Weak fixed investment continued to be the biggest drag on demand, while the previous positive contribution from inventory and working capital needs has disappeared entirely. As we highlighted in the last edition of this chartbook, the continued drag on demand for investment reflects a lingering uncertainty regarding the pandemic which could possibly lower potential long-term growth in the euro area.2 As in the US, however, the reduction in demand also reflected already built-up liquidity buffers and the availability of internal and market-based financing. In Q2, banks expect a strong rebound in enterprise loan demand, especially from small and medium-sized enterprises (SMEs). Consumer credit demand continued to decline at a stronger pace in Q1, reflecting the continued pandemic-related restrictions in Europe over the quarter. The key drivers were lower durable goods spending and weakening consumer confidence. Banks also reported increased use of internally-generated funds, which is consistent with accumulated savings and pent-up demand during the lockdown. Assuming that the emerging Delta variant does not sidetrack the European return to normalcy, we will likely see the expected consumer credit demand rebound come to fruition. This would be consistent with recent strong consumer confidence prints out of the region. Looking individually at the four major euro area economies, credit standards for enterprises tightened in Germany, Italy, and Spain but were unchanged in France (Chart 6). In countries where standards tightened, worsening risk perceptions were the primary factor. In France, increased competition from other lenders contributed to easing on the margin. Going into Q2, standards are expected to tighten very modestly in the two core European economies while diverging in peripheral Europe—Spanish banks expect an increased pace of tightening while Italian ones expect standards to remain unchanged. UK In the UK, overall corporate credit standards, measured as an average of standards for medium and large non-financial firms, eased slightly in Q1/2021 (Chart 7A). This increase in credit availability was driven primarily by an improving economic outlook and sector-specific risk picture. As in the US and euro area, competition from capital markets also played a role and is expected to contribute to the further easing expected in Q2. Chart 7AUK Credit Conditions

UK Credit Conditions

UK Credit Conditions

Chart 7BInvestment And Inventory Financing Expected To Pick Up In The UK

GFIS Credit Conditions Chartbook Q2/2021: Easing Up

GFIS Credit Conditions Chartbook Q2/2021: Easing Up

Meanwhile, corporate loan demand is picking up at a pace not seen since Brexit, excluding the 2020 spike driven by emergency funding needs, signaling a buoyant picture. In particular, the surge in demand was driven by large non-financial firms which are also expected to drive the demand pick-up in Q2. Household loan demand fell slightly in the first quarter but is expected to rebound. Consumer confidence, which had initially lagged behind loan demand, appears to have caught up as the UK’s “Freedom Day” from pandemic restrictions approaches in July. Lenders are also expected to ease availability for unsecured household loans, primarily on the back of market share objectives. This should create the ideal backdrop for a consumption boom if the Delta variant does not further limit the UK government’s ability to deliver on its promise of a full reopening. Delving into the factors behind booming corporate loan demand, there are promising signs for the broader UK economy (Chart 7B). In a Special Report published earlier this year, we argued that UK real interest rates were depressed because the country suffered from a series of rolling economic and political shocks, the effects of which were now expected to fade.3 There are already some signs of this in the credit data, with capital investment and inventory financing demand expected to rebound in Q2. Despite work-from-home effects dampening the need for office space, on the margin, UK commercial real estate demand is strong and expected to further strengthen. Japan Chart 8Japan Credit Conditions

Japan Credit Conditions

Japan Credit Conditions

In Japan, credit standards to firms and households eased at a slower pace in Q1/2021 (Chart 8). The vast majority of respondents indicated that standards were basically unchanged, with none of the firms reporting any tightening, and a small number reporting some degree of easing. The most important factors driving easing were aggressive competition from other bank and non-bank lenders, as well as strengthened efforts to grow the business. Going into Q2, the pace of easing is expected to continue to slow. Business loan demand, which behaves somewhat counter-cyclically in Japan, increased over Q1. The entirety of this pickup can be attributed to small firms; large and medium-sized firms on the whole decreased their loan demand. Counter to trends in other regions, firms in Japan actually saw a decrease in internally-generated funds, which was the most important factor contributing to increased loan demand. Consumer loan demand fell slightly on balance but was mostly unchanged from the previous quarter. Respondents reporting weaker demand saw a decrease in household consumption as the most important factor. Sentiment remains subdued and has lagged the recovery in loan demand seen last year. Our colleagues at BCA Research Foreign Exchange Strategy are eyeing a recovery for the Japanese economy as the government turns around its vaccination campaign and the Olympics jumpstart consumption.4 On that basis, the very modest recovery in loan demand expected by Japanese banks appears too pessimistic. Canada And New Zealand In Canada, business lending standards continued to ease at a faster pace in Q1/2021, coinciding with rebounding business confidence which is now back to pre-pandemic levels (Chart 9). This is in line with a remarkable vaccine rollout—68% of the population has already received its first dose and the pace of daily vaccinations is showing no signs of rolling over. Chart 9Canada Credit Conditions

Canada Credit Conditions

Canada Credit Conditions

Chart 10New Zealand Credit Conditions

New Zealand Credit Conditions

New Zealand Credit Conditions

However, housing is a major concern for Canadian policymakers. In a recent Special Report, co-authored with our colleagues at The Bank Credit Analyst, we highlighted both Canada and New Zealand as “higher risk” countries more exposed to ballooning house prices.5 In addition to low rates, mortgage lending standards, which have been easing since Q3/2020, have undoubtedly contributed to this issue. However, the Bank of Canada (BoC), with its hawkish messaging, has signaled that it will not idly stand by; there is also popular support behind raising rates to tamp down house prices. Expect mortgage standards to tighten and a pick-up in mortgage rates as the BoC nears liftoff, most likely in 2022. Credit standards in New Zealand were mostly unchanged in Q1/2021, reversing the tightening trend of previous quarters (Chart 10). Over the next six months, standards are expected to ease considerably. Business loan demand was unchanged on net, with corporates decreasing and SMEs increasing demand. SMEs are also expected to increase demand slightly over the next six months. Tepid loan demand is consistent with business confidence hovering around the neutral zero line. As in Canada, soaring house prices are a major issue for the New Zealand economy. Data on household lending is alarming on that front. Although consumer loan demand continued to weaken, demand for residential mortgages spiked to an all-time high in Q1. While demand is expected to normalize going forward, the Q1 datapoint indicates froth in the market. The Reserve Bank of New Zealand is considering a variety of macroprudential measures but will have to raise rates sooner rather than later to effectively cool down the housing market. Appendix: Where To Find The Bank Lending Surveys A number of central banks publish regular surveys of bank lending conditions in their domestic economies. The surveys, and the details on how they are conducted, can be found on the websites of the central banks: US Federal Reserve: https://www.federalreserve.gov/data/sloos.htm European Central Bank: https://www.ecb.europa.eu/stats/ecb_surveys/bank_lending_survey/ Bank of England: https://www.bankofengland.co.uk/credit-conditions-survey/2021/2021-q1 Bank of Japan: https://www.boj.or.jp/en/statistics/dl/loan/loos/index.htm/ Bank of Canada: https://www.bankofcanada.ca/publications/slos/ Reserve Bank of New Zealand: https://www.rbnz.govt.nz/statistics/c60-credit-conditions-survey Shakti Sharma Senior Analyst ShaktiS@bcaresearch.com Footnotes 1 The weblinks to each individual survey for the US, euro area, UK, Japan, Canada and New Zealand can be found in the Appendix on page 12. 2 Please see BCA Research Global Fixed Income Strategy Report, "GFIS Global Credit Conditions Chartbook Q1/2021: A Tentative Recovery", dated February 16, 2021, available at gfis.bcaresearch.com. 3 Please see BCA Research Global Fixed Income Strategy Special Report, "Why Are UK Interest Rates Still So Low?", dated March 10, 2021, available at gfis.bcaresearch.com. 4 Please see BCA Research Foreign Exchange Strategy Report, "The Case For Japan", dated June 11, 2021, available at fes.bcaresearch.com. 5 Please see BCA Research Global Fixed Income Strategy Special Report, "Global House Prices: A New Threat For Policymakers", dated May 28, 2021, available at gfis.bcaresearch.com.

Highlights The US is withdrawing from the Middle East and South Asia and making a strategic pivot to Asia Pacific. The third quarter will see risks flare around Iran and the US rejoin the 2015 Iranian nuclear deal. The result is briefly negative for oil prices but the rise of Iran is a new geopolitical trend that will increase Middle Eastern risk over the long run. The geopolitical outlook is dollar bullish, while the macroeconomic outlook is getting less dollar-bearish due to China’s risk of over-tightening policy. Stay neutral USD and be wary of commodities and emerging markets in the third quarter. European political risk is bottoming. The German and French elections are at best minor risks. However, the continent is ripe for negative black swans, especially due to Russian aggression. Go tactically long global large caps and defensives. Feature Chart 1Three Key Views On Track (So Far)

Three Key Views On Track (So Far)

Three Key Views On Track (So Far)

We chose “No Return To Normalcy” as the theme of our 2021 outlook. While the COVID-19 vaccine promised economic recovery, we argued that normalization would create complacency regarding fundamental changes that have taken place in the geopolitical environment. A contradiction between an improving macroeconomic backdrop and a foreboding geopolitical backdrop would develop in 2021 and beyond. The “reflation trade” has begun to lose steam as we go to press. However, global recovery will still be the dominant story in the second half of the year as vaccination spreads. The question for the third quarter and the rest of the year is whether reflation will continue. As a matter of forecasting, we think it will. But as a matter of investment strategy, we are taking a more defensive stance until China relaxes economic policy. In our annual outlook we highlighted three key geopolitical views: (1) China’s headwinds, both at home and abroad (2) US détente with Iran and pivot to Asia (3) Europe’s opportunity. All three trends are broadly on track and can be illustrated by looking at equity performance in the relevant regions for the year so far: Chinese stocks sold off, UAE stocks rallied, and European stocks rallied (Chart 1). However, these trends are not exclusively tied to absolute equity performance. The most important question is what happens to global growth and the US dollar as these three key views continue. Stay Neutral On The Dollar It paid off for us to maintain a neutral stance on the dollar. True, the global recovery and exorbitant US trade and budget deficits are bearish for the dollar and bullish for other currencies. But the greenback’s “counter-trend bounce” is proving more formidable than many investors expected. The fundamentals of the American economy and global position remain strong. Since the outbreak of COVID-19, the US has secured its recovery with fiscal policy, maintained rule of law amid a contested election, innovated and distributed vaccines, benefited from more flexible social restrictions, refurbished global alliances, and put pressure on its geopolitical rivals. In essence, the combined effect of President Trump’s and Biden’s policies has been to make America “great again” (Chart 2). From a geopolitical perspective, the dollar is appealing. Chart 2Trump-Biden Make America Great Again?

Trump-Biden Make America Great Again?

Trump-Biden Make America Great Again?

In addition, the first two geopolitical views mentioned above – China’s headwinds and the US-Iran détente – imply a negative environment for China and the renminbi. The reason for the US to do a suboptimal deal with Iran, both in 2015 and 2021, is to reduce the risk of war and buy time to enable a strategic pivot to Asia Pacific. Three US presidents have been elected on the pledge to conclude the “forever wars” in the Middle East and South Asia. Biden is withdrawing US troops from Afghanistan in September. There can be little doubt Biden is committed to an Iran deal, which is supposed to free up the US’s hands (Chart 3). Meanwhile the US public and Congress are unified in their desire to better defend US interests against China’s economic and military rise. There has not yet been a stabilization of US-China policies. Biden is not likely to hold a summit with Chinese President Xi Jinping until late October at earliest – and that is a guess, not a confirmed summit. The Biden administration has completed its review of China policy and is maintaining the Trump administration’s hawkish posture, as predicted. The US and China may resume their strategic and economic dialogue at some point but it is impossible to go back to the status quo ante 2015. That was the year the US adopted a more confrontational stance toward China – a stance later supercharged by Trump’s election and trade tariffs. The hawkish consensus on China is one of the rare unifying factors in a deeply divided America. The Biden administration explicitly says the US-China relationship is now defined by “competition” instead of “engagement.”1 One exception to this neutral view on the dollar has been our decision to go long the Japanese yen and Swiss franc, which has not panned out so far. Our reasoning is that geopolitical risk will boost these currencies but otherwise the reduction of geopolitical risk will weigh on the dollar in the context of global growth recovery. So far geopolitical risk has remained subdued while the US dollar has outperformed. We are still sympathetic to these safe-haven currencies, however, as they are attractively valued as long as one expects geopolitical risks to materialize (Chart 4). Chart 3US Pivot To Asia Runs Through Iran

US Pivot To Asia Runs Through Iran

US Pivot To Asia Runs Through Iran

Our third key view, that EU was the real winner of the US election last year, remains on track. This is marginally positive for the euro at the expense of the dollar. Given the above points, we favor an equal-weighted basket of the euro and the dollar relative to the renminbi (Chart 5). Chart 4Safe-Haven Currencies Attractive

Safe-Haven Currencies Attractive

Safe-Haven Currencies Attractive

Chart 5Favor Euro And Dollar Over Renminbi

Favor Euro And Dollar Over Renminbi

Favor Euro And Dollar Over Renminbi