Euro Area

Weak Euro Area sentiment data and tight financial conditions support the case for a tactical US outperformance over Europe. July monetary data came in slightly below expectations, with M3 growth only edging up to 3.4% y/y from 3.3%. Household loan growth…

Although Euro area PMIs beat expectations in August, the growth outlook remains weak. The composite index rose to 51.1, driven by manufacturing returning to expansion at 50.5 from 49.8. Meanwhile the services PMI slipped 0.3 points to 50.7. The readings…

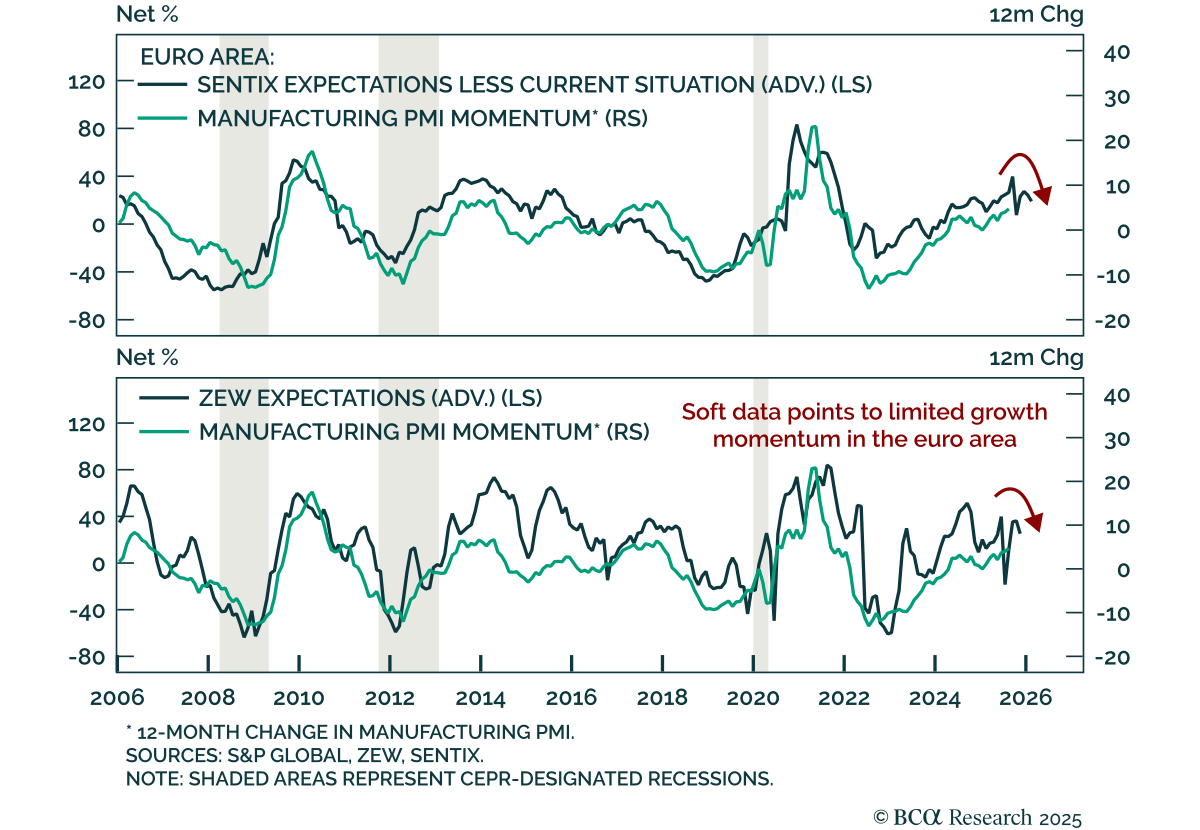

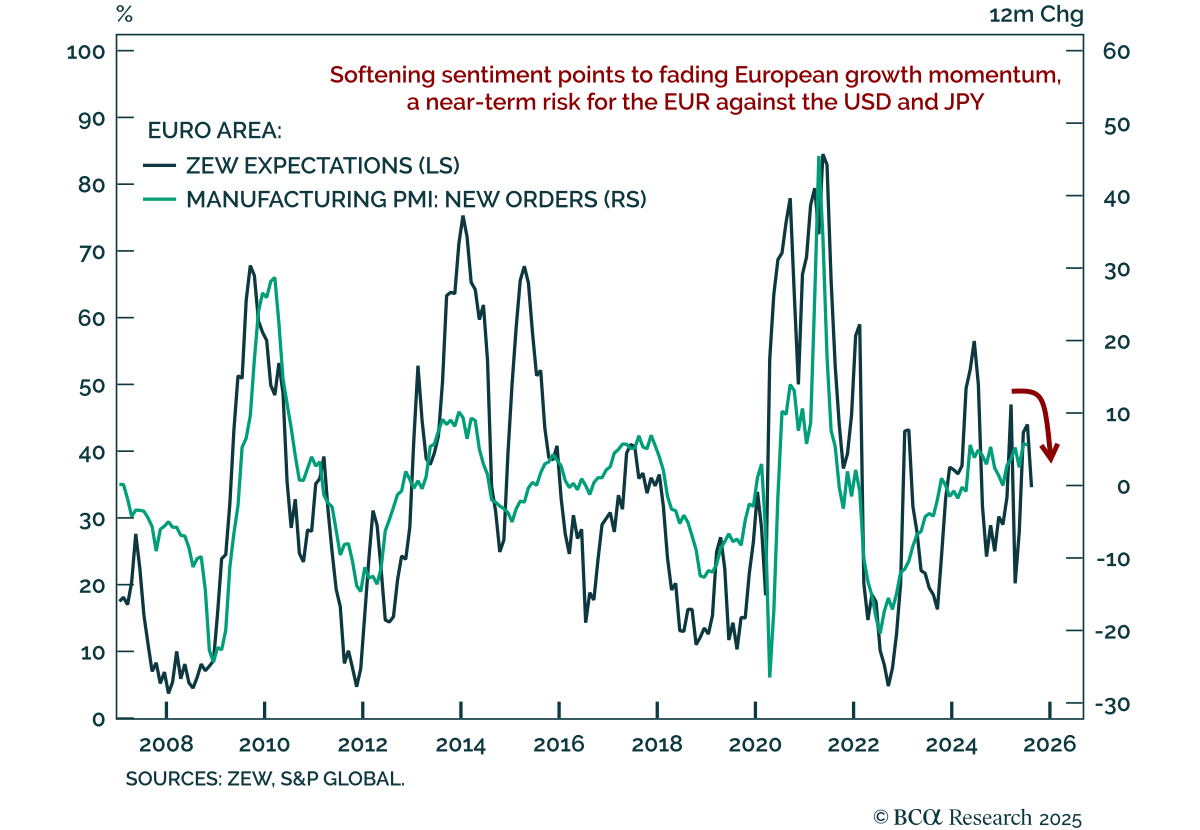

European sentiment has moderated, pointing to near-term downside risk for a technically-stretched Euro. The August Eurozone ZEW Expectations index fell to 25.1 from 36.1, with Germany’s reading missing estimates, dropping sharply to 34.7 from 52.7. The German…

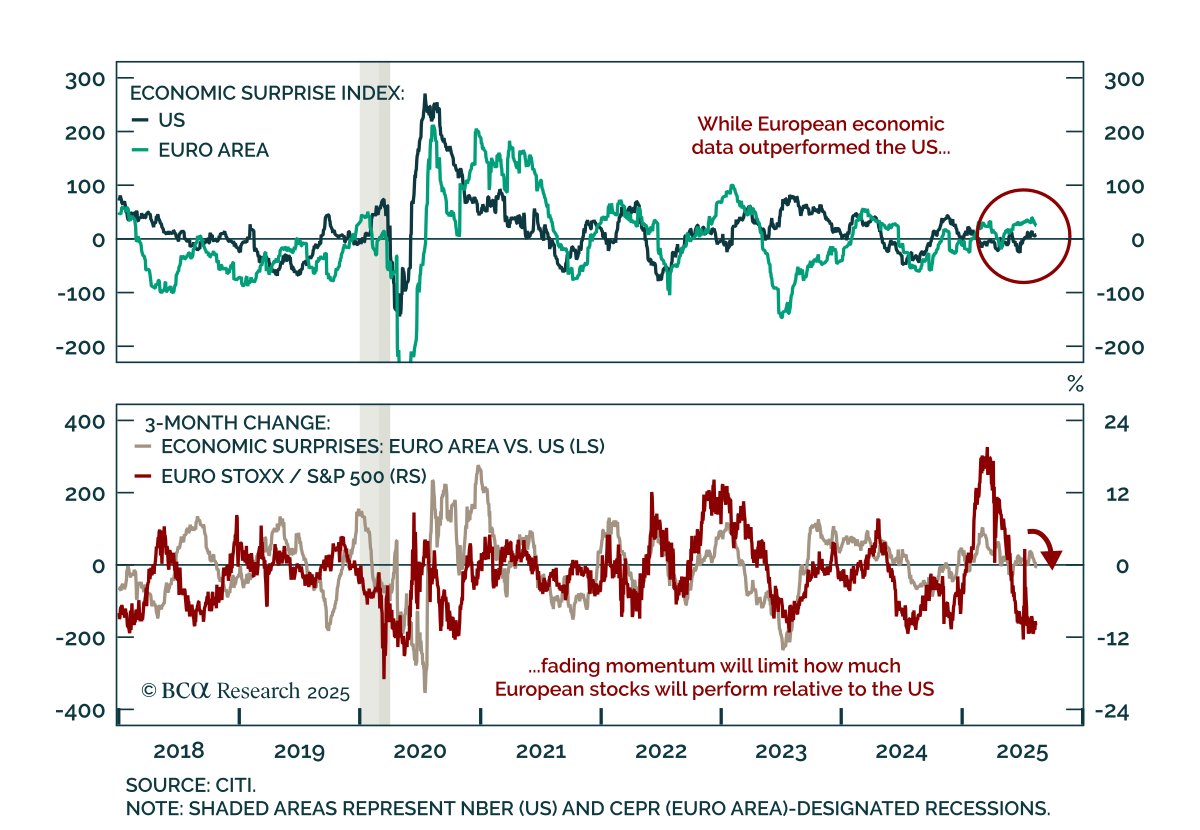

US equities are set for tactical outperformance versus Europe, but dips or underperformance in European assets remain entry points for long-term investors. European stocks have stalled below prior highs, while the S&P 500 has rebounded to record levels…

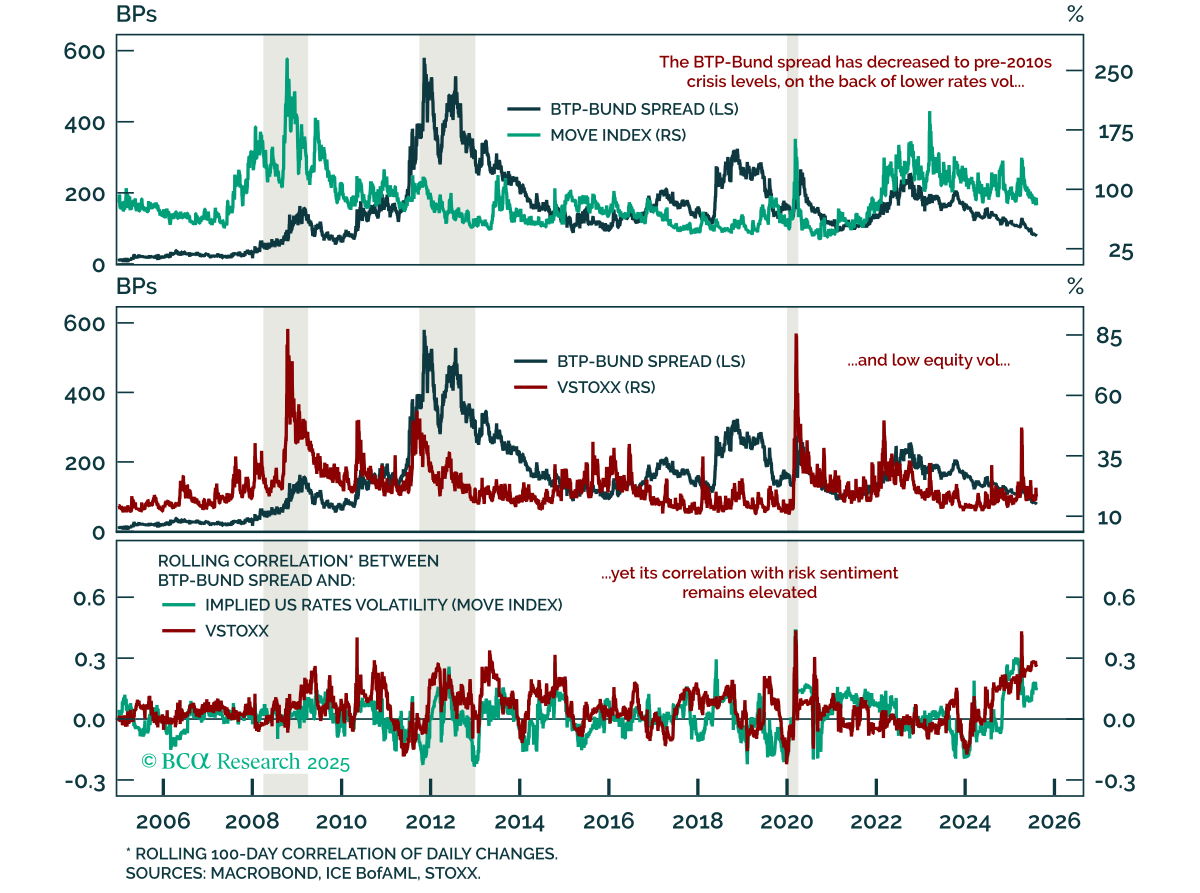

The BTP-Bund spread has tightened to pre-2010s levels, but with global growth risks we favor Gilts over Bunds and prefer BTPs over credit. While the EURO STOXX 50 remains rangebound since the Liberation Day recovery, European financial stress remains low. The…

Euro area inflation held steady in July, but near-term risks remain. Long-term investors should buy on dips. Headline and core HICP came in at 2.0% and 2.3% y/y, roughly in line with expectations. The ECB held its deposit rate at 2% at its last meeting…

EUR/USD has broken below key support, and near-term risks justify a tactical bearish stance while longer-term investors should buy dips. The pair fell through its 50-day moving average, which, along with the 20-day, had provided steady support since…

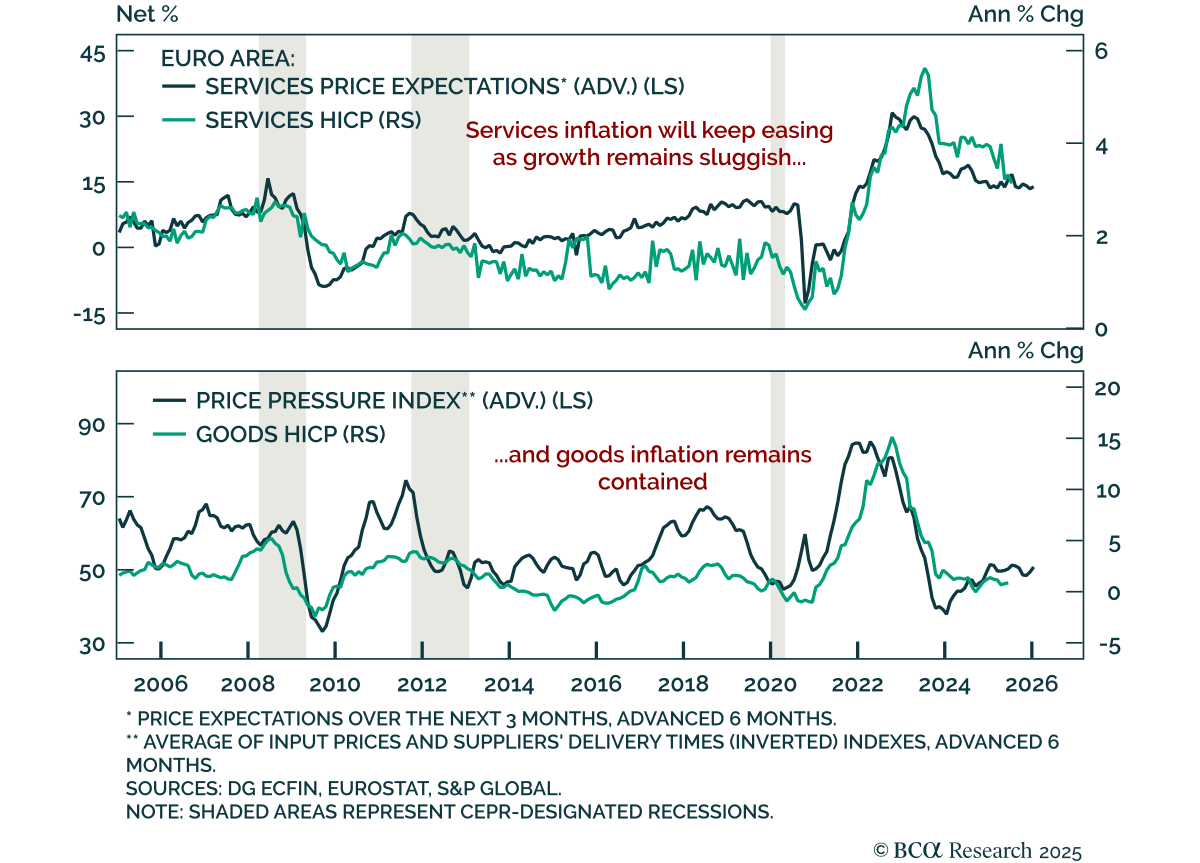

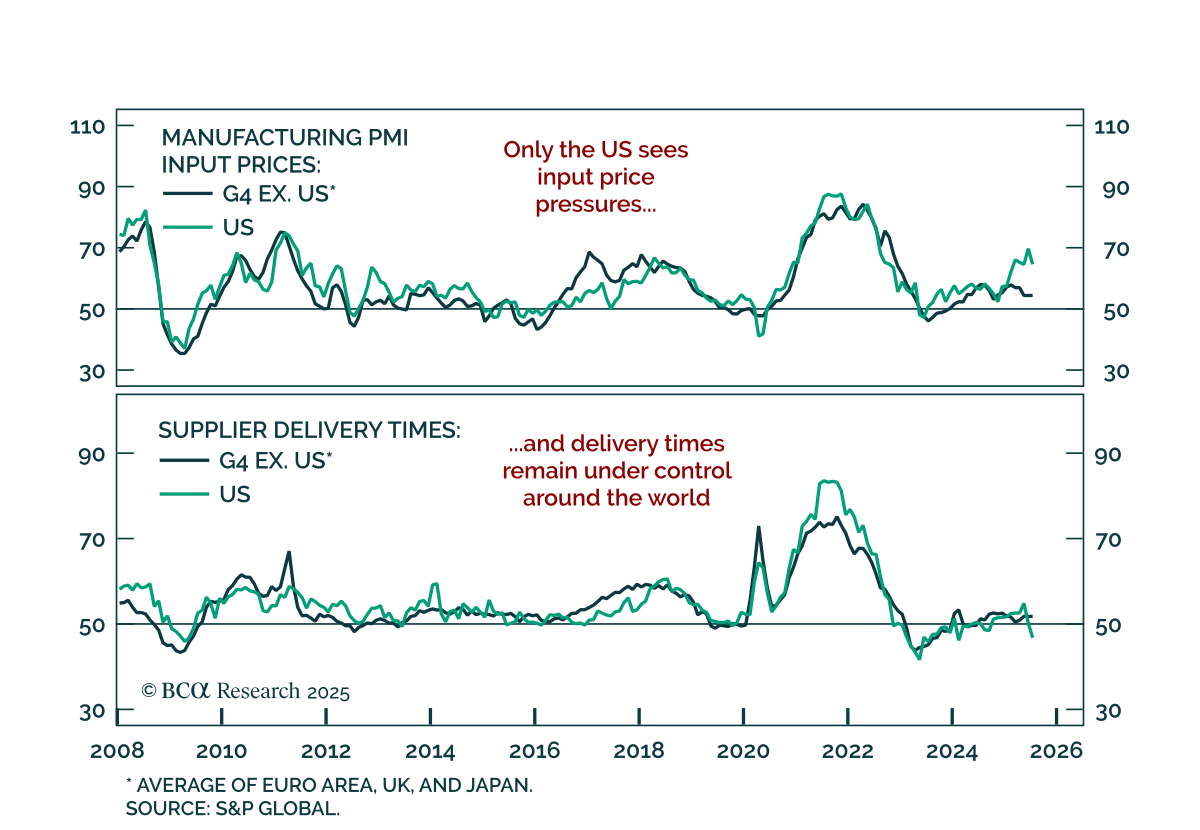

Cresting price pressures and weak global growth reinforce our long duration stance, with labor market slack limiting inflation upside across most major economies. Our price pressure indexes show moderate input inflation outside the US and stable global…

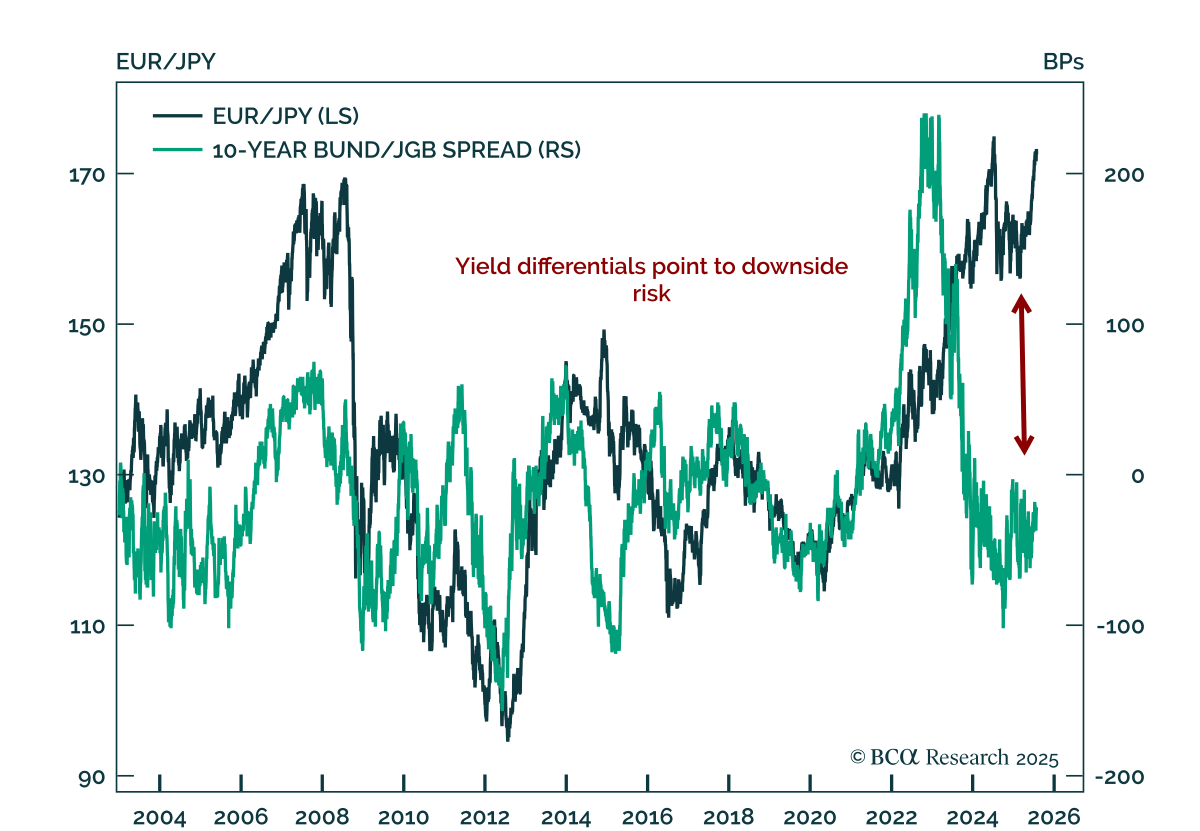

Our strategists recommend shorting EUR/JPY, citing stretched valuations and rising reversal risks. The cross has surged more than 6% since late May, triggering new short positions from the Counterpoint, European Investment Strategy, and Global Investment…

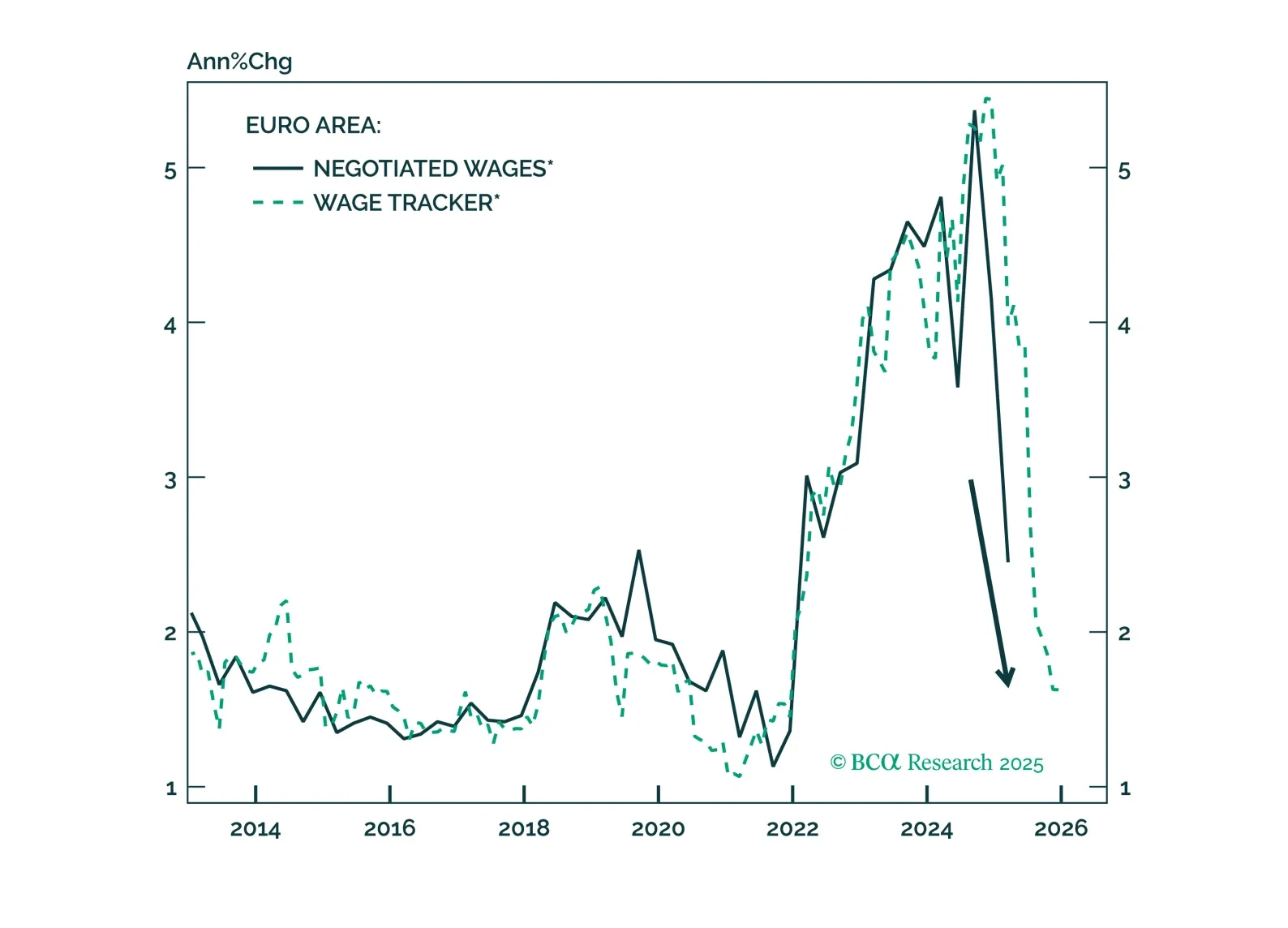

Consensus sees one final ECB cut; we argue two are coming as deflationary forces are building in Europe. Dive in for the trade map: falling Bund yields, tighter peripheral spreads, and a euro primed for a 2026 rebound.