Euro Area

Highlights Sweden’s economic recovery is robust and will deepen. Policy is accommodative. Very few advanced economies will benefit as much from the global economic rebound. The labor market will tighten, capacity utilization will increase, and inflation will rise faster than the Riksbank forecasts. On a one- to two-year investment horizon, the SEK is a buy against both the USD and the EUR. Despite their pronounced outperformance, Swedish stocks possess significantly more upside against both Eurozone and US equities over the remainder of the cycle. Swedish industrials will beat their competitors in both these markets. Nonetheless, China’s policy tightening creates a meaningful tactical risk, which selling Norwegian stocks can hedge. Italy’s fiscal plan constitutes a new salvo in Europe’s efforts to avoid last decade’s mistakes. Feature Last week, the Swedish Riksbank did not follow in the footsteps of the Norges Bank. The Swedish central bank acknowledged that the economy is performing better than anticipated and that the housing market is gaining in strength; yet, it refrained from hinting at any forthcoming adjustment to its policy rate or the pace of its asset purchase program. The positive outlook for the Swedish economy will force the Riksbank to tighten policy significantly before the ECB. As a result, we expect the Swedish Krona to outperform the euro and the US dollar. Moreover, investors should continue to overweight Swedish equities due to their large exposure to industrials and financials, even if they have already significantly outperformed the Euro Area. Sweden’s Economic Outlook The Swedish economy will accelerate, which will put pressure on resource utilization and fan inflationary risk in the years ahead. The degree of stimulus supporting Sweden is consequential. Chart 1A Dual Labor Market

A Dual Labor Market

A Dual Labor Market

On the fiscal front, the government support measures that have been announced since the beginning of the COVID-19 crisis currently amount to SEK420bn, or SEK197bn for 2020 (4% of GDP), and SEK223bn for 2021 (4.5% of GDP). Moreover, generous labor market protection and part-time employment schemes meant that the number of employees in permanent employment contracts remained stable during the pandemic (Chart 1). Thus, the bulk of the rise in Swedish unemployment came from workers on fixed-term contracts. Monetary policy remains very accommodative as well. The Riksbank left its repo rate unchanged at 0% through the crisis, but cut its lending rate from 0.75% to 0.1%. More importantly, the Swedish central bank is aggressively injecting liquidity into the economy. It set up a SEK500bn funding-for-lending facility in order to incentivize bank lending to the nonfinancial private sector, and started a SEK700bn QE program, which as of Q1 2021 had purchased SEK380bn securities and which will purchase another SEK120bn in Q2, with covered bonds issued by banks accounting for 70% of it. As a result, the amount of securities held on the Riksbank balance sheet will nearly triple by year end (Chart 2). Chart 2The Riksbank Is Open For Business

Take A Chance On Sweden

Take A Chance On Sweden

Beyond the monetary and fiscal stimulus, many factors point to greater economic strength for Sweden. Despite a slow start to the process, as of last week, nearly 30% of the Swedish population had received at least one vaccine dose, which is broadly in line with vaccination rates prevalent in France or Germany. Crucially, the pace of vaccination is accelerating at a rate of 13% per week. Even if this second derivative slows, more than 70% of the population will have received at least one dose by this summer. Thus, greater mobility is in the cards during the second quarter, which will boost household spending. Chart 3The Wealth Effect

The Wealth Effect

The Wealth Effect

The housing market also favors a pick-up in consumption. The HOX housing price index is growing at a 15% annual rate, its fastest expansion in over 5 years. As a result of the wealth effect, this rapid appreciation is consistent with a swift improvement in the growth rate of household expenditures (Chart 3). Moreover, spending on durable goods now stands 1.3% above its pre-pandemic levels, while spending on non-durables is back to pre-pandemic levels. This context suggests that increased mobility translates into greater spending. The industrial sector remains a particularly bright spot in the Swedish economy. Sweden is extremely sensitive to the global industrial and trade cycle, because exports represent 45% of GDP. Moreover, the highly cyclical intermediate and capital goods comprise 56% of the country’s foreign shipments, which accentuates the beta of the Swedish economy. BCA Research remains optimistic about the global industrial cycle. Sweden will reap a significant dividend. Already the Swedish PMI points to stronger industrial production, and the index’s exports component is roaring ahead (Chart 4). The potential for a greater uptake in consumption, capex, and durable goods spending in the rest of the EU (Sweden’s largest trading partner) bodes well for the Swedish manufacturing sector. Additionally, if the collapse in the US inventory-to-sales ratio is any indication for the rest of the world, a global restocking cycle is forthcoming, which will further boost Swedish industrial activity (Chart 4, bottom panels). Finally, global public infrastructure plans are on the rise, which will also help Sweden. Chart 4Sweden Is well Placed

Sweden Is well Placed

Sweden Is well Placed

Chart 5Brightening Labor Market Prospects

Brightening Labor Market Prospects

Brightening Labor Market Prospects

In this context, the Swedish labor market should tighten significantly in the approaching quarters. Already, job vacancies are rebounding, and redundancy notices have normalized, which matches both the GDP growth surprise in Q1 and the continued rise in the NIER Sweden Economic Tendency Indicator. Furthermore, the employment component of the PMIs stands at 58.9 and is consistent with a sharp improvement in job growth over the coming year (Chart 5). The expected labor market growth will contribute to an increase in capacity utilization, which will place upward pressure on wages and inflation. When the 12-month moving average of US and Eurozone imports rises, so does the Riksbank Resource Utilization Indicator, because global trade has such a pronounced effect on the Swedish economy (Chart 6). Meanwhile, greater resource utilization leads to accelerated inflation, greater labor shortages, and rising unit labor costs (Chart 7). Chart 6CAPU Will Rise

CAPU Will Rise

CAPU Will Rise

Chart 7The Coming Pressure Buildup

The Coming Pressure Buildup

The Coming Pressure Buildup

Bottom Line: As a result of generous stimulus and the global economic recovery, the Swedish economy is set to continue its rebound. Consequently, employment and capacity utilization will improve meaningfully, which will lead to a resurgence of inflation and wages in the coming 24 months. Investment Implications On a 12 to 24 months horizon, we remain positive on the Swedish krona and Swedish equities. Fixed Income And FX Chart 8Three Hikes By 2025

Three Hikes By 2025

Three Hikes By 2025

The backend of the Swedish OIS curve only discounts 75bps of hikes by 2025. This pricing is too modest (Chart 8). The Swedish economy will rebound further as the vaccination campaign advances, and rising house prices and household indebtedness will fan growing long-term risk to financial stability, both of which suggest that the Riksbank will have to change its tack in 2022. The great likelihood that the Fed will start tapering off its asset purchase toward the end this year, that the ECB will follow sometime in 2022, and that the Norges Bank will be increasing interest rates next year will give more leeway to the Swedish central bank. A wider Sweden/Germany 10-year government bond spread is not an appealing vehicle to play a more hawkish Riksbank down the road. This spread hit a 23-year high in March and now rests at 62bps or its 98th percentile since 2000. Moreover, the terminal rate proxy embedded in the German money market curve is currently so low that the spread between Sweden’s and the Eurozone’s terminal rate proxy stands near a record high. Hence, German yields already embed much more pessimism than Swedish ones. Nonetheless, BCA recommends a below benchmark duration exposure within the Swedish fixed-income space, as we do for other government bond markets around the world.1 A bullish bias toward the SEK is a bet on the Riksbank that offers a very appealing risk/reward ratio, according to BCA Research’s Foreign Exchange Strategy strategists.2 The krona is very cheap against both the euro and the US dollar, trading at 9% and 29% discounts to purchasing power parity, respectively. Moreover, the Swedish current account stands at 5.2% of GDP, compared to 2.3% and -3.1% for the Euro Area and the US, creating a natural underpinning under the SEK. Chart 9The SEK Loves Growth

The SEK Loves Growth

The SEK Loves Growth

Over the coming 12 to 24 months, cyclical forces favor selling EUR/SEK and USD/SEK on any strength. The SEK is one of the most cyclical G-10 currencies and has one of the strongest sensitivities to the US dollar. Hence, our positive global economic outlook and our FX strategists negative view on the greenback are synonymous with a weak USD/SEK. These same factors also mean that the krona will appreciate more than the euro, as the negative correlation between EUR/SEK and our Boom/Bust Indicator and global earnings growth illustrate (Chart 9). Equities We also like Swedish equities, but the state of the Swedish economy and the evolution of the Riksbank policy surprise have a limited impact on Swedish equities. The Swedish bourse is mostly about the evolution of the global business cycle. The Swedish benchmark heightened sensitivity to the global business cycle reflects its massive overweight in deep cyclicals, with industrials, financials, consumer discretionary, and materials accounting for 38.4%, 26.1%, 9.7% and 3.7% of the MSCI index respectively, or 78% altogether (Table 1). As a result, BCA’s preference for global cyclicals at the expense of defensives and this publication’s fondness for the recovery laggards like the industrial and financial sectors automatically translate into a favorable bias toward Sweden’s stocks.3 Table 1Mamma Mia! That’s A Lot Of Cyclicals

Take A Chance On Sweden

Take A Chance On Sweden

Valuations offer a more complex picture, but they do not diminish our predilection for Sweden. Swedish equities trade at a discount to US stocks but at a premium to Euro Area ones (Chart 10). However, Swedish stocks offer higher RoEs and profit margins than both the US and the Euro Area, while also sporting lower leverage (Chart 11). Thus, their valuation premium to Euro Area stocks is warranted and their discount to US ones is excessive, especially when rising yields hurt the relative performance of the growth stocks that dominate US indexes. Chart 10Swedish Discounts And Premia

Swedish Discounts And Premia

Swedish Discounts And Premia

Chart 11Profitable Sweden

Profitable Sweden

Profitable Sweden

The outlook for Swedish earnings is appealing, both in absolute and relative terms. The Swedish market’s extreme sensitivity to global economic activity means that Sweden’s EPS increase and beat US profits when the Riksbank Resource Utilization Indicator expands (Chart 12). These relationships are artefacts of the Swedish economy’s pro-cyclicality, which causes capacity utilization to interweave tightly with the global business cycle (Chart 6). Chart 12The Winner Takes It All

The Winner Takes It All

The Winner Takes It All

Chart 13Better Capex Play Than You

Better Capex Play Than You

Better Capex Play Than You

Global capex and infrastructure spending favor Swedish equities compared to Euro Area ones. Over the past thirty years, Sweden’s stocks have outperformed those of the Eurozone when capital goods orders in the advanced economies have expanded (Chart 13). This reflects the Swedish benchmark’s large overweight in industrials, a sector that is the prime beneficiary of global capex. Capital goods orders are recovering well, and their growth rate can climb higher, especially as western multinationals announce capex plans and as governments from the US to Italy intend to ramp up infrastructure spending. Moreover, the large pent-up demand for durable goods in the Eurozone further enhances the potential of industrial firms, and thus, of Swedish equities.4 Chart 14Another Sign Of Pro-Cyclicality

Another Sign Of Pro-Cyclicality

Another Sign Of Pro-Cyclicality

BCA Research’s positive cyclical stance on commodities offers another reason to overweight Sweden’s market relative to that of the US and the Euro Area. Our Commodity and Energy Strategy sister service anticipates significant further upside for natural resources, especially base metals, over the remainder of the business cycle.5 Commodity prices still have room to rally, because demand will grow as the global economy continues to recover and because the supply of natural resources has been constrained by a decade of low investment. As a result, rising metal prices will symptomatize strong economic activity around the world and will incentivize capex in commodity extraction, both of which will boost the revenue of industrial firms. Furthermore, commodity price inflation often corresponds with rising yields, which boosts financials as well. These relationships explain the Swedish stocks’ outperformance of US and Eurozone stocks, when natural resource prices rally, despite the former’s low exposure to materials (Chart 14). At the sector level, the appeal of Swedish industrials relative to those of the Eurozone and the US completes the rationale to favor Swedish equities in a global portfolio. Swedish industrials are just as profitable as US ones and are more so than Euro Area ones, while having significantly lower leverage than either of them (Chart 15). Additionally, for the past two years, the EPS growth of Swedish industrials has bested that of US and Eurozone ones. Yet, their forward P/E ratio trades in line with the US and the Euro Area, while the sell-side’s long-term relative earnings growth estimate is too depressed (Chart 16). The same observations are valid when comparing Swedish industrials to French or German ones. Hence, in the context of a global business cycle upswing, buying Swedish industrials while selling their US and Euro Area competitors is an appealing pair trade, especially since it also involves short USD/SEK and short EUR/SEK bets. Chart 15Attractive Swedish Industrials...

Attractive Swedish Industrials...

Attractive Swedish Industrials...

Chart 16...And Not Expensive

...And Not Expensive

...And Not Expensive

Despite our optimism toward Swedish stocks on a 12 to 24 months basis, investors must hedge a near-term risk. Chinese authorities are aiming to contain financial excesses and trying to restrain credit growth. As we showed four weeks ago, China’s excess reserve ratio is contracting, which points toward a slowdown in the Chinese credit impulse.6 Historically, such a development can hurt global cyclicals, and thus, also Swedish equities. However, BCA Research’s China strategists believe that Beijing will not kill off the Chinese business cycle; thus, the recent disappointment in the Chinese PMI is transitory.7 Chart 17Industrials vs Materials: Europe vs China

Industrials vs Materials: Europe vs China

Industrials vs Materials: Europe vs China

Materials more than industrials will suffer the brunt of a China slowdown, as the re-opening trade and capex cycle among advanced economies will create a buffer for the latter. Indeed, the performance of global industrials relative to materials stocks correlates with the evolution of the spread between the Euro Area and Chinese PMI (Chart 17). Thus, we recommend selling Norwegian equities to hedge the tactical risk inherent in an overweight on Sweden. As Table 1 above shows, Norway overweighs materials and energy (two sectors greatly exposed to China), hence, a temporary pullback in commodity prices should hurt Norwegian stocks more than Swedish ones. Bottom Line: The SEK is an inexpensive and attractive vehicle to bet on both the global business cycle strength and the Swedish economic recovery. Thus, investors should use any rebound in EUR/SEK and USD/SEK to sell these pairs. Moreover, Swedish stocks greatly overweight cyclical sectors, particularly industrials and materials. This sectoral profile renders Swedish equities as attractive bets on the global economy. Additionally, Swedish shares display alluring operating metrics. As a result, we recommend investors go long Swedish industrials relative to those of the US and Euro Area. They should also overweight Swedish equities against the US and the Eurozone. Consequent to some China-related tactical risks, an underweight stance on Norwegian stocks constitutes an attractive hedge to this Swedish exposure. A Few Words On Italy’s National Recovery And Resilience Plan Mario Draghi’s plan to revive the Italian economy, announced last week, is an important marker of Europe’s changing relationship with fiscal policy. Last decade, excessive austerity contributed to subpar growth, ultimately firing up concerns about debt sustainability in many peripheral economies, and fueled risk premia in Italy and Spain. Under the cover of the current crisis, and in the face of the changing political winds in Brussel and Berlin where fiscal rectitude is not the mantra it once was, national European governments are beginning to propose ambitious fiscal stimulus plans. The National Recovery and Resilience program illustrates these dynamics. The EUR248bn plan is a testament to the importance of the NGEU recovery program as well as the REACT EU recovery fund. Through these facilities, the EU will contribute EUR191.5bn to the fiscal plan via grants and loans. Italy will contribute the remainder of the funds. While the total amount disbursed over the next six years corresponds to 14% of Italy’s 2019 GDP, the Draghi government estimates that the program will add 3.2 percentage points to GDP between 2024 and 2026. Importantly, markets are not rebelling. Despite expectations that Italy would continue to run an accommodative fiscal policy, the BTP/Bund spreads remain stable. We can expect this trend of greater stimulus to be mimicked around the EU. Spain is another large recipient of the NGEU program, and it too is likely to increase stimulus beyond what the EU will fund. France will hold an election in May 2022, and President Macron has all the incentives to stimulate the economy between now and then. If, as we wrote last week, Germany shifts to the left in September, then this outcome will be guaranteed. Bottom Line: The Draghi plan is the first salvo of greater fiscal stimulus in the EU. This trend will help Eurozone growth improve relative to the US over the coming few years. Despite a loose fiscal policy, BTPs and other peripheral bonds will continue to outperform on the back of declining risk premia. Mathieu Savary, Chief European Investment Strategist Mathieu@bcaresearch.com Footnotes 1Please see Global Fixed Income Strategy “GFIS Model Bond Portfolio Q1/2021 Performance Review & Current Allocations: Grand Reopening,” dated April 6, 2021, available at gfis.bcaresearch.com 2Please see Foreign Exchange Strategy “2021 Key Views: Tradeable Themes,” dated December 4, 2020, available at fes.bcaresearch.com 3Please see European Investment Strategy “Summer Of ‘21,” dated March 22, 2021, available at eis.bcaresearch.com 4Please see European Investment Strategy “Winds Of Change: Germany Goes Green,” dated April 23, 2021, available at eis.bcaresearch.com 5Please see Commodity & Energy Strategy “Industrial Commodities Super-Cycle Or Bull Market?” dated March 4, 2021, available at ces.bcaresearch.com 6Please see European Investment Strategy “The Euro Dance: One Step Back, Two Steps Forward,” dated March 29, 2021, available at eis.bcaresearch.com 7Please see China Investment Strategy “National People’s Congress Sets Tone For 2021 Growth,” dated March 17, 2021, available at cis.bcaresearch.com Cyclical Recommendations Structural Recommendations Currency Performance

Take A Chance On Sweden

Take A Chance On Sweden

Fixed Income Performance Government Bonds

Take A Chance On Sweden

Take A Chance On Sweden

Corporate Bonds

Take A Chance On Sweden

Take A Chance On Sweden

Equity Performance Major Stock Indices

Take A Chance On Sweden

Take A Chance On Sweden

Geographic Performance

Take A Chance On Sweden

Take A Chance On Sweden

Sector Performance

Take A Chance On Sweden

Take A Chance On Sweden

Closed Trades

Highlights The Greens are likely to win control of Germany’s government in the September 26 federal elections. At least they will be very influential in the new coalition. Germany has achieved may of its long-term geopolitical goals within the EU. There is consensus on dovish monetary and fiscal policy and hawkish environmental policy. The biggest changes will come from the outside. The US and Germany have a more difficult relationship. While they both oppose Russian and Chinese aggression, Germany will resist American aggression. The Christian Democrats have a 65% chance of remaining in government which would limit the Greens’ controversial and ambitious tax agenda. The 35% chance of a left-wing coalition will frontload fiscal stimulus for the sake of recovery. The economy is looking up and a Green-led fiscal easing would supercharge the recovery. However, coalition politics will likely fail to address Germany’s poor demography, deteriorating productivity, and large excess savings. On a cyclical basis, overweight peripheral European bonds relative to bunds; EUR/USD; and Italian and Spanish stocks relative to German stocks. Feature Chart 1Germans Turn To A Young Woman And A Green

Winds Of Change: Germany Goes Green

Winds Of Change: Germany Goes Green

Germany is set to become the first major country to be led by a green party. At very least the German election on September 26 will see an upset in which the ruling party under-performs and the Greens over-perform (Chart 1). At 30%, online betting markets are underrating the odds that Annalena Baerbock will become the first Green chancellor in 2022 – and the first elected chancellor to hail from a third party (Chart 2). The “German question” – the problem of how to unify Germany yet keep peace with the neighbors – lay at the heart of Europe for the past two centuries but today it appears substantially resolved: a peaceful and unified Germany stands at the center of a peaceful and mostly unified Europe. There are a range of risks on the horizon but this positive backdrop should be acknowledged. Chart 2Market Waking Up To Baerbock’s Bid For Chancellorship

Winds Of Change: Germany Goes Green

Winds Of Change: Germany Goes Green

All of the likeliest scenarios for the German election will reinforce the current situation by perpetuating policies that aim for Euro Area solidarity. Even the green shift is already well underway, though a Green-led government would supercharge it. Nevertheless this year’s election is important because it heralds a leftward shift in Germany and will shape fiscal, energy, industrial, and trade policy for at least the coming four years. A left-wing sweep would generate equity market excitement in the short run – a positive fiscal surprise to supercharge the post-pandemic rebound – but over the long run it would bring greater policy uncertainty because it would cause a break with the past and possibly a structural economic shift (Chart 3). The Greens are in favor of substantial increases in taxation and regulation as well as big changes in industrial and energy policy. In the absence of a left-wing sweep, coalition politics will be a muddle and Germany’s existing policies will continue. Chart 3German Policy Uncertainty On The Rise

German Policy Uncertainty On The Rise

German Policy Uncertainty On The Rise

Regardless of what happens within Germany, the geopolitical environment is increasingly dangerous. Germany will try to avoid getting drawn into the US’s great power struggles with Russia and China but it may not have a choice. Germany’s Geopolitics The difficulty of German unification stands at the center of modern European history. Because of the large and productive German-speaking population, unification in 1871 posed a security threat to the neighbors, culminating in the world wars. The peaceful German reunification after the Cold War created the potential for the EU to succeed and establish peace and prosperity on the continent. This arrangement has survived recent challenges. Germany’s relationship with the EU came under threat from the financial crisis, the Arab Spring and immigration influx, Brexit, and President Trump’s trade tariffs. But in the end these events cemented the reality that German and Europe are strengthening their bonds in the face of foreign pressures. Germany achieved what it had long sought – preeminence on the continent – by eschewing a military role, sticking to France economically, and avoiding conflict with Russia. Since Germany has achieved many of its long-sought strategic objectives it has not fallen victim to a nationalist backlash over the past ten years like the US and United Kingdom. However, Germany is not immune to populism or anti-establishment sentiment. The two main political blocs, the Christian Democrats and the Democratic Socialists, have suffered a loss of popular support in recent elections, forcing them into a grand coalition together. Anti-establishment feeling in Germany has moved the electorate to the left, in favor of the Greens. The Greens have risen inexorably over the past decade and have now seized the momentum only five months before an election (Chart 4). Yet the Greens in Germany are basically an establishment political party. They participate in 11 out of 16 state governments and currently hold the top position in Baden-Württemberg, Germany’s third most populous and productive state. From 1998-2005 they participated in government, getting their hands dirty with neoliberal structural reforms and overseas military deployments. Moreover the Greens cannot rule alone but will have to rule within a coalition, which will mediate their more controversial policies. Chart 4Greens Surge, Christian Democrats Falter

Greens Surge, Christian Democrats Falter

Greens Surge, Christian Democrats Falter

Today Germany is in lock step with France and the EU by meeting three key conditions: full monetary accommodation (the German constitutional court’s challenges to the European Central Bank are ineffectual), full fiscal accommodation (Chancellor Angela Merkel agreed to joint debt issuance and loose deficit controls amid the COVID-19 crisis as well as robust green energy policies), and full security accommodation (German rearmament exists within the context of NATO and European security aspirations are undertaken in lock-step with the French). These conditions will not change in the 2021 election even assuming that the Greens take power at the head of a left-wing coalition. Bottom Line: Germany has virtually achieved its grand strategic aims of unifying and ruling Europe. No German government will challenge this situation and every German government will strive to solidify it. The greatest risks to this setup stem from abroad rather than at home. The Return Of The German Question? Germany’s geopolitical position can be summarized by Chart 5, which shows popular views toward different countries and institutions. The Germans look positively upon the EU and global institutions like the United Nations and less so NATO. They look unfavorably upon everything else. They take an unfavorable view toward Russia, but not dramatically so, which shows their lack of interest in conflict with Russia – they do not want to be the battleground or the ramparts of another major European war. They dislike the United States and China even more, and equally. Even if attitudes toward the US have improved since the 2020 election the net unfavorability is telling. Chart 5Germany More Favorable Toward Russia Than US?

Winds Of Change: Germany Goes Green

Winds Of Change: Germany Goes Green

Since the global financial crisis, and especially Russia’s invasion of Ukraine in 2014, Germany has built up its military. This buildup is taking place under the prodding of the United States and in step with NATO allies, who are reacting to Russia’s military action to restore its sphere of influence in the former Soviet space (Chart 6). Germany’s military spending still falls short of NATO’s 2% of GDP target, however. It will not be seen as a threat to its neighbors as long as it remains integrated with France and Europe and geared toward deterring Russia. Chart 6Germany And NATO Increase Military Spending

Winds Of Change: Germany Goes Green

Winds Of Change: Germany Goes Green

Chart 7Watch Russo-German Relations For Cracks In Europe’s Edifice

Winds Of Change: Germany Goes Green

Winds Of Change: Germany Goes Green

Russia’s aggressiveness should continue to drive the Germans and Europeans into each other’s arms. This could change if Putin pursues diplomacy over military coercion, for then he could split Germany from eastern Europe. The possibility is clear from Russia’s and Germany’s current insistence on completing the Nord Stream 2 pipeline despite American and eastern European objections. The pipeline is set to be completed by September, right in time for the elections – in no small part because the Greens oppose it. If the US insists on halting the pipeline then a crisis will erupt with Russia that will humiliate Merkel and the Christian Democrats. But the US may refrain from doing so in the face of Russian military threats (odds are 50/50). The Russian positioning over 100,000 troops on the border with Ukraine this year – and now reportedly ordering them to return to base by May 1 – amounts to a test of Russo-German relations. Putin can easily expand the Russian footprint in Ukraine and tensions will remain elevated at least through the Russian legislative elections in September. Germans would respond to another invasion with sanctions, albeit likely watering down tougher sanctions proposed by the Americans. What would truly change the game would be a Russian conquest of all of Ukraine. This is unlikely – precisely because it would unite Germany, the Europeans, and the Americans solidly against Russia, to its economic loss as well as strategic disadvantage (Chart 7). China’s rise should also keep Germany bound up with Europe. The Germans fear China’s technological and manufacturing advancement, including Chinese involvement in digital infrastructure and networks. The Greens are critical of the way that carbon-heavy Chinese goods undercut the prices of carbon-lite German goods. Baerbock favors carbon adjustment fees, a pretty word for tariffs. However, the Germans want to maintain business with China and are not very afraid of China’s military. Hence there is a risk of a US-German split over the question of China. If Germany should consistently side with Russia and China over US objections then it risks attracting hostile attention from the US as well as from fellow Europeans, who will eventually fear that German power is becoming exorbitant by forming relations with giants outside the EU. But this is not the leading risk today. The US is courting Germany and seeking to renew the trans-Atlantic alliance. Meanwhile Germany needs US support against Russia’s military and China’s trade practices. US-German relations will improve unless the US forces Germany into an outright conflict with the autocratic powers. Bottom Line: The US and Germany have a more difficult relationship now than in the past but they share an interest in deterring Russian aggression and Chinese technological and trade ambitions. Biden’s attempt to confront these powers multilaterally is limited by Germany’s risk-aversion. Scenarios For The 2021 Election There are several realistic scenarios for the German election outcome. Our expectation that the Greens will form a government stems from a series of fundamental factors. Opinion polling has now clearly shifted in favor of our view, with the Greens gaining the momentum with only five months to go. Grouping the political parties into ideological blocs shows that the race is a dead heat. Our bet is that momentum will break in favor of the opposition Greens, which we explain below. Meanwhile the Free Democrats should perform well, stealing votes from the Christian Democrats. The right-wing Alternative für Deutschland (AfD), while not performing well, is persistent enough to poach some votes from the Christian Democrats. These are “lost” votes to the conservatives as none of the parties will join it in a coalition (Chart 8). Chart 8Germany's Median Voters Shifts To the Left

Germany's Median Voters Shifts To the Left

Germany's Median Voters Shifts To the Left

The Christian Democrats bear all the signs of a stale and vulnerable government. They have been in power for 16 years and their performance in state and federal elections has eroded recently, including this year (Table 1). The public is susceptible to the powerful idea that it is time for a change. Chancellor Merkel’s approval rating is still around 60%, but in freefall, and her successful legacy is not enough to save her party, which is showing all the signs of panic: succession issues, indecision, infighting, corruption scandals. The Greens will be “tax-and-spend” lefties but the coalition matters in terms of what can actually be legislated (Table 2).1 Table 1AChristian Democrats Fall, Greens Rise, In Recent State Elections

Winds Of Change: Germany Goes Green

Winds Of Change: Germany Goes Green

Table 1BChristian Democrats Fall, Greens Rise, In Recent State Elections

Winds Of Change: Germany Goes Green

Winds Of Change: Germany Goes Green

Table 2Policy Platforms Of The Green Party

Winds Of Change: Germany Goes Green

Winds Of Change: Germany Goes Green

The fact that Christian Democrats and their Bavarian sister party, the Christian Social Union, saw such a tough race for chancellor candidate is an ill omen. Moreover the party’s elites went for the safe choice of Merkel’s handpicked successor, Armin Laschet, over the more popular Markus Soeder (Chart 9), in a division that will likely haunt the party later this year. Chart 9Christian Democrats And Christian Social Union Divided Ahead Of Election

Winds Of Change: Germany Goes Green

Winds Of Change: Germany Goes Green

Laschet has received a bounce in polls with the nomination but it will be temporary. He has not cut a major figure in any polling prior to now. Chart 10Dissatisfaction Points To Government Change

Winds Of Change: Germany Goes Green

Winds Of Change: Germany Goes Green

He has quarreled openly with Merkel and the coalition over pandemic management. He was not her first choice of successor anyway – that was Annagret Kramp-Karrenbauer, who fell from grace due to controversy over the faintest hint of cooperation with the AfD. There is a manifest problem filling Merkel’s shoes. Even more important than coalition infighting is the fact that Germany, like the rest of the world, has suffered a historic shock to its economy and society. The pandemic and recession were then aggravated by a botched vaccine rollout. General dissatisfaction is high, another negative sign for the incumbent party (Chart 10). Of course, the election is still five months away. The vaccine will make its way around, the economy will reopen, and consumers will look up – see below for the very positive macro upturn that Germany should expect between now and the election. Voters have largely favored strict pandemic measures and Merkel will have long coattails. This Christian Democrats and Christian Social Union have ruled modern Germany for all but 15 years and have not fallen beneath 33% of the popular vote since reunification. The Greens have frequently aroused more energy in opinion polling than at the voting booth. With these points in mind, we offer the following election scenarios with our subjective probabilities: Green-Red-Red Coalition – Greens rule without Christian Democrats – 35% odds. Green-Black Coalition – Greens rule with Christian Democrats – 30% odds. Black-Green Coalition – Christian Democrats rule with Greens – 25% odds. Grand Coalition (Status Quo) – Christian Democrats rule without Greens – 10% odds. Our subjective probabilities are based on the opinion polls and online betting cited above but adjusted for the Greens’ momentum, the Christian Democrats’ internal divisions, the “time for change” factor, and the presence of a historic exogenous economic and social shock. Geopolitical surprises could occur before the election but they would most likely reinforce the Greens, since they have taken a hawkish line against Russia and China. Bottom Line: The Greens are likely to lead the next German government but at very least they will have a powerful influence. Policy Impacts Of Election Scenarios The makeup of the ruling coalition will determine the parameters of new policy. Fiscal policy will change based on the election outcome – both spending and taxes. The Greens will be “tax-and-spend” lefties but the coalition matters in terms of what can actually be legislated.2 The Greens’ idea is to “steer” the rebuilding process through environmental policy. But if the left lacks a strong majority then the Greens’ more controversial and punitive measures will not get through. Transformative policies will weigh heavily on the lower classes (Chart 11). Chart 11Ambitious Climate Policy Will Face Resistance

Winds Of Change: Germany Goes Green

Winds Of Change: Germany Goes Green

The policy dispositions of the various chancellor candidates help to illustrate Germany’s high degree of policy consensus. Table 3 looks at the candidates based on whether they are “hawkish” (active or offensive) or “dovish” (passive or defensive) on a given policy area. What stands out is the agreement among the different candidates despite party differences. Nobody is a fiscal or monetary hawk. Only Baerbock can be classified as a hawk on trade.3 Nobody is a hawk on immigration. Nearly everyone is a hawk on fighting climate change. And attitudes are turning more skeptical of Russia and China, though not outright hawkish. Table 3Policy Consensus Among German Chancellor Candidates

Winds Of Change: Germany Goes Green

Winds Of Change: Germany Goes Green

Germany will not abandon its green initiatives even if the Greens underperform. The current grand coalition pursued a climate package due to popular pressure even with the Greens in opposition. Germans are considerably more pro-environment even than other Europeans (Chart 12). The green shift is also happening across the world. The US is now joining the green race while China is doubling down for its own reasons. See the Appendix for current green targets and measures, which have been updated in the wake of a slew of announcements before Biden’s Earth Day climate summit on April 22-23. Chart 12Germans Care Even More About Environment Than Other Europeans

Winds Of Change: Germany Goes Green

Winds Of Change: Germany Goes Green

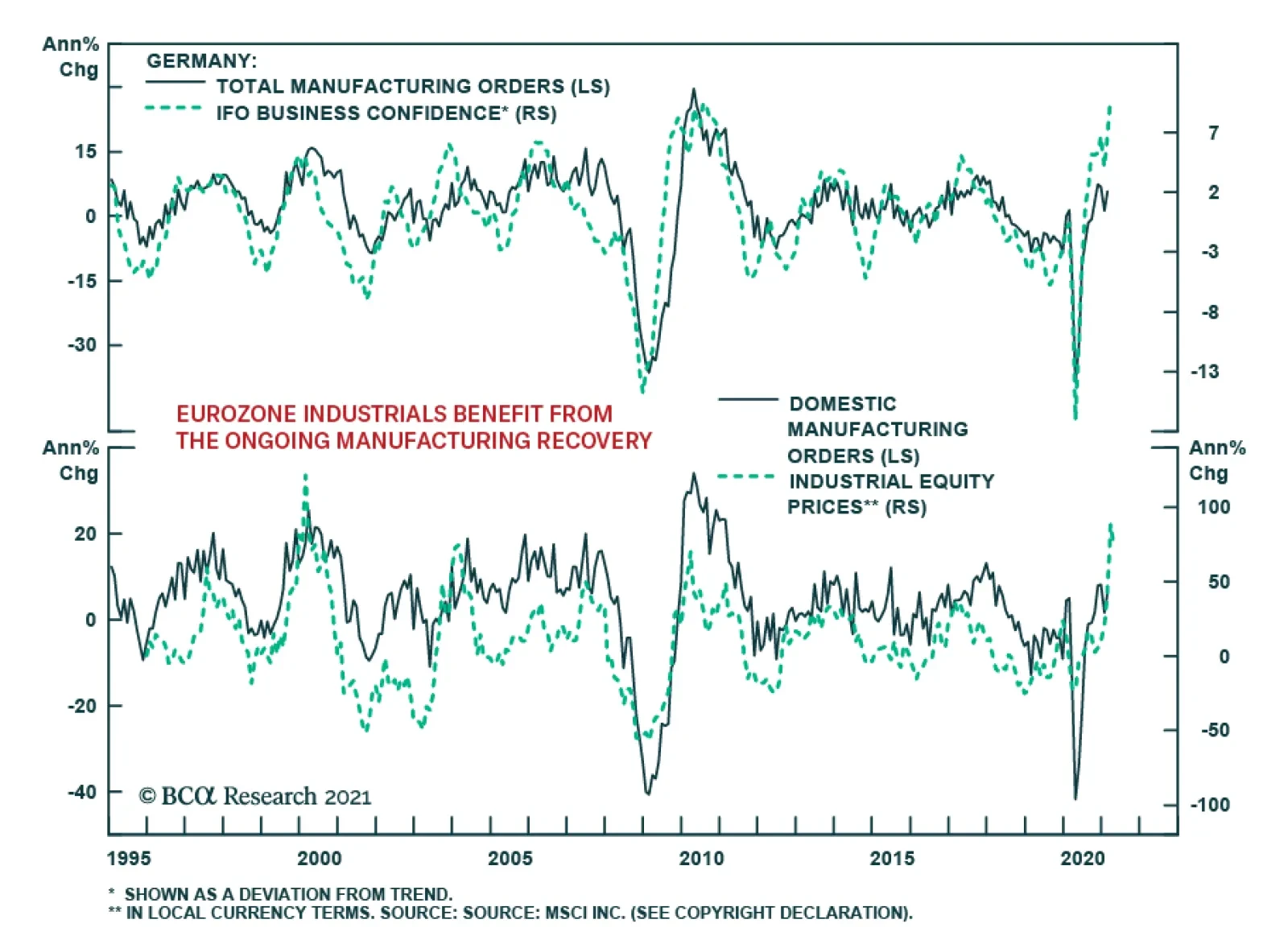

Any coalition will raise spending more than taxes since it will be focused on post-COVID economic recovery. There has been a long prelude to Germany’s proactive fiscal shift – it has staying power and is not to be dismissed. A Christian Democratic coalition would try to restore fiscal discipline sooner than otherwise but there is only a 5% chance that it will have the power to do so according to the scenarios given above. The rest of Europe will be motivated to spend aggressively while EU fiscal caps are on hold in 2022, especially if the German government is taking a more dovish turn. Even more than the US and UK, Germany is turning away from the neoliberal Washington Consensus. But Germans are not experiencing any kind of US-style surge of polarization and populism. At least not yet. It may be a risk over the long run, depending on the fate of the Christian Democrats, the AfD, and various internal and external developments. Bottom Line: Germany has a national consensus that consists of dovish monetary, fiscal, trade, and immigration policies and hawkish (pro-green) environmental policy. Germany is turning less dovish on geopolitical conflicts with Russia and China. Given that a coalition government is likely, this consensus is likely to determine actual policy in the wake of this year’s election. A few things are clear regardless of the ruling coalition. First, Germany is seeking domestic demand as a new source of growth, to rebalance its economy and deepen EU integration. Second, Germany is accelerating its green energy drive. Third, Germany cannot accept being in the middle of a new cold war with Russia. Fourth, Germany has an ambivalent policy on China. Germany’s Macro Outlook Even before considering the broader fiscal picture, the outlook for German economic activity over the course of the coming 12 to 24 months was already positive. Our base case scenario for the September election, which foresees a coalition government led by the Green Party, only confirms this optimistic view. However, Germany is still facing significant long-term challenges, and, so far, there has not been a political consensus to address these structural headwinds adequately. The Greens offer some solutions but not all of their proposals are constructive and much will depend on their parliamentary strength. Peering Into The Near-Term… Germany’s economy is set to benefit from the continued recovery of the global business cycle, which is a view at the core of BCA Research’s current outlook.4 Germany remains a trading and manufacturing powerhouse, and thus, it will reap a significant dividend from the continued global manufacturing upswing. Manufacturing and trade amount to 20% and 88% of Germany’s GDP, the highest percentage of any major economy. Alternatively, according to the OECD, foreign demand for German goods accounts for nearly 30% of domestic value added, a share even greater than that for a smaller economy like Korea (Chart 13). Moreover, road vehicles, machinery and other transport equipment, as well as chemicals and related products, account for 53% of Germany’s exports. These products are all particularly sensitive to the global business cycle. They will therefore enhance the performance of the German economy over the next two years. Trade with the rest of Europe constitutes another boost to Germany’s economy going forward. Shipments to the euro area and the rest of the EU account for 34% and 23% of Germany’s exports, or 57% overall. Right now, the lagging economy of Europe is a handicap for Germany; however, Europe has more pent-up demand than the US, and the consumption of durable goods will surge once the vaccination campaign progresses further (Chart 14). This will create a significant boon for Germany, since we expect European consumption to pick up meaningfully over the coming 12 to 18 months.5 Chart 13Germany Depends On Global Trade

Winds Of Change: Germany Goes Green

Winds Of Change: Germany Goes Green

Chart 14Europe Has More Pent-Up Demand Than The US

Europe Has More Pent-Up Demand Than The US

Europe Has More Pent-Up Demand Than The US

Chart 15Vaccination Progress

Vaccination Progress

Vaccination Progress

Domestic forces also point toward a strong Germany economy, not just foreign factors. The pace of vaccination is rapidly accelerating in Germany (Chart 15). The recent announcement of 50 million additional doses purchases for the quarter and up to 1.8 billion more doses over the next two years by the EU points to further improvements. A more broad-based vaccination effort will catalyze underlying tailwinds to consumption. German household income will also progress significantly. The Kurzarbeit program was instrumental in containing the unemployment rate during the crisis, which only peaked at 6.4% from 5% in early 2020. However, the program could not prevent a sharp decline in total hours worked of 7%, since by definition, it forced six million employees to work reduced hours (Chart 16). One of the great benefits of the program is that it prevents a rupture of the link between workers and employers. Thus, the economy suffers less frictional unemployment as activity recovers and household income does not suffer long lasting damage. Meanwhile, the German government is likely to extend the support for households and businesses as a result of the delayed use of the debt-brake. The Greens propose revising the debt brake rather than restoring it in 2022 like the conservatives pledge to do. Chart 16Kurtzarbeit Saved The Day

Kurtzarbeit Saved The Day

Kurtzarbeit Saved The Day

The balance-sheet strength of German households means that they will have the wherewithal to spend these growing incomes. Residential real estate prices are rising at an 8% annual pace, which is pushing the asset-to-disposable income ratio to record highs. Meanwhile, the debt-to-assets ratio, and the level of interest rates are also very low, which means that the burden of serving existing liabilities is minimal (Chart 17). In this context, durable goods spending will accelerate, which will lift overall cyclical spending, even if German households do not spend much of the EUR120 billion in excess savings built up over the past year. As Chart 18 shows, while US durable goods spending has already overtaken its pre-COVID highs, Germany’s continues to linger near its long-term trend. Thus, as the economy re-opens this summer, and income and employment increase, the concurrent surge in consumer confidence will allow for a recovery in cyclical spending. Chart 17Strong Household Balance Sheets

Strong Household Balance Sheets

Strong Household Balance Sheets

Chart 18Germany Too Has More Pent-up Demand Than The US

Germany Too Has More Pent-up Demand Than The US

Germany Too Has More Pent-up Demand Than The US

Chart 19Positive Message From Many Indicators

Positive Message From Many Indicators

Positive Message From Many Indicators

Various economic indicators are already pointing toward the coming German economic boom.Manufacturing orders are strong, and economic sentiment confidence is rising across most sectors. Meanwhile, consumer optimism is forming a trough, and new car registrations are climbing rapidly. Most positively, the stocks of finished goods have collapsed, which suggests that production will be ramped up to fulfill future demand (Chart 19). Bottom Line: The German economy is set to accelerate in the second half of the year and into 2022. As usual, Germany will enjoy a healthy dividend from robust global growth, but the expanding vaccination program, as well durable employee-employer relations, strong household balance sheets, and significant pent-up demand for durable goods will also fuel the domestic economy. Our base case scenario that fiscal policy will remain accommodative in the wake of a political shift to the left in Berlin in September will only supercharge this inevitable recovery. … And The Long-Term In contrast to the bright near-term perspective, the long-term outlook for the German economy remains poor. The policies of any new ruling coalition are unlikely to address the problems of Germany’s poor demography, deteriorating productivity, and large excess savings. There is potential for a productivity boost in the context of a global green energy and high-tech race but for now that remains a matter of speculation. The most obvious issue facing Germany is its ageing population, counterbalanced by its fertility rate of only 1.6. Over the course of the next three decades, Germany’s dependency ratio will surge to 80%, driven by an increase in the elderly dependency ratio of 20% (Chart 20). The working age population is set to decline by 18% by 2050, which will curtail potential GDP growth. The outlook for German productivity growth is also poor. Germany’s productivity growth has been in a long-term decline, falling from 5% in 1975 to less than 1% in 2019. Contrary to commonly-held ideas, from 1999 to 2007, German labor productivity growth has only matched that of France or Spain; since 2008, it has lagged behind these two nations, although it has bested Italy. One crucial reason for Germany’s uninspiring productivity performance is a lack of investment. Some of this reflects the country’s austere fiscal policy. For example, in 2019, Germany’s public investment stood at 2.4% of GDP, which compares poorly to the OECD’s average of 3.8%, or even to that of the US, where public investment stood at 3.6% of GDP. This poor statistic does not even account for the depreciation of the German public capital stock. Since the introduction of the euro, net public investment has averaged 0.03% of GDP. The biggest problem remains at the municipal level. From 2012 to 2019, federal and state level net investment averaged 0.2% of GDP, while municipal net investment subtracted 0.2% of GDP on average. Hopefully, the new government will be able to address this deficiency of the German economy. The Greens are most proactive but they will face obstacles. The bigger problem for German productivity is corporate capex. Corporate investments have been low in this country. Since the introduction of the euro, the contribution of capital intensity to productivity in Germany has equaled that of Italy and has underperformed France and Spain. As a result, the age of the German capital stock is at a record high and stands well above the US or Eurozone average (Chart 21). Chart 20Germany Has Poor Demographics

Germany Has Poor Demographics

Germany Has Poor Demographics

Chart 21Germany's Capital Stock Is Ageing

Germany's Capital Stock Is Ageing

Germany's Capital Stock Is Ageing

The make-up of Germany’s capex aggravates the productivity-handicap. According to a Bundesbank study, the contribution to labor productivity from information and communication technology (ICT) capital spending has averaged 0.05 percentage points annually from 2008 to 2012. On this metric, Germany lagged behind France and the US, but still bested Italy. From 2013 to 2017, the contribution of ICT investment to productivity fell to 0.02 percentage points, still below France and the US, but in line with Italy. Looking at the absolute level of ICT or knowledge-based capital (KBC) investment further highlights Germany’s challenge. In 2016, total investment in ICT equipment, software and database, R&D and intellectual property products, and other KBC assets (which include organizational capital and training) represented less than 8% of GDP. In France, the US, or Sweden, these outlays accounted for 11%, 12%, and 13% of GDP, respectively (Chart 22, top panel). This lack of investment directly hurts Germany’s capacity to innovate. The bottom panel of Chart 22 shows that, for the eight most important categories of ICT patents (accounting for 80% of total ICT patents), Germany remarkably lags behind the US, Japan, Korea, or China. Chart 22Germany Lags In ICT investment

Winds Of Change: Germany Goes Green

Winds Of Change: Germany Goes Green

A major source of Germany’s handicap in ICT and KBC investment comes from small businesses, which have been particularly reluctant to deploy capital. A study by the OECD shows that, between 2010 and 2019, the gap of ICT tools and activities adoption between Germany’s small and large companies deteriorated relative to the OECD average (Chart 23). The lack of venture capital investing probably exacerbates these problems. In 2019, venture capital investing accounted for 0.06% of Germany’s GDP. This is below the level of venture investing in France or the UK (0.08% and 0.1% of GDP, respectively), let alone South Korea, Canada, Israel, or the US (0.16%, 0.2%, 0.4% and 0.65%, respectively). The Greens claim they will create new venture capital funds but their capability in this domain is questionable. Chart 23The Lagging ICT Capabilities Of Small German Businesses

Winds Of Change: Germany Goes Green

Winds Of Change: Germany Goes Green

Since Germany’s productivity growth is likely to remain sub-par compared to rest of the OECD and to lag behind even that of France or the UK, the only way for Germany to protect its competitiveness will be to control costs. This means that Germany cannot allow its recent loss of competitiveness to continue much further (Chart 24). Thus, low productivity growth will limit Germany’s real wages. Chart 24Germany's Competitiveness Is Declining

Germany's Competitiveness Is Declining

Germany's Competitiveness Is Declining

This wage constraint will negatively impact consumption. Beyond a pop over the coming 12 to 24 months, German consumption is likely to remain depressed, as it was in the first decade and a half of the century, following the Hartz IV labor market reforms that also hurt real wages. The Greens for their part aim to boost welfare payments, raise the minimum wage, and reduce enforcement of Hartz IV. Bottom Line: German excess savings will remain wide on a structural basis. Without a meaningful pick-up in capex, German nonfinancial businesses will remain net lenders. Meanwhile, households that were worried about their financial future in a world of low real-wage growth will also continue to save a significant share of their income. Consequently, the excess savings Germany developed since the turn of the millennia are here to stay (Chart 25). In other words, Germany will continue to sport a large current account surplus and exert a deflationary influence on Europe and the rest of the world. The policy prescribed by the various parties contesting the September election will not necessarily result in new laws that will reverse the issues of low capex and low ICT investment. The Greens will worsen the over-regulation of the economy. Barring a policy revolution that succeeds in all its aims (a tall order), we can expect more of the same for Germany – that is, a slowly declining economy. Chart 25Too Much Savings, Not Enough Investments

Too Much Savings, Not Enough Investments

Too Much Savings, Not Enough Investments

Chart 26Germany Scores Well On Renewable Power

Winds Of Change: Germany Goes Green

Winds Of Change: Germany Goes Green

That being said, some bright spots exist. Germany is becoming a leader in renewable energy, and it can capitalize on the broadening of this trend to enlarge its export market (Chart 26). Investment Implications Bond Markets The economic outlook for Germany and the euro area at large is consistent with the underweighting of German bunds within European fixed-income portfolios. Bunds rank among the most expensive bond markets in the world, which will make them extremely vulnerable to positive economic surprise in Europe later this year, especially if Germany’s fiscal policy loosens up further in the wake of the September election (Chart 27). Moreover, easier German fiscal policy should help European peripheral bonds, especially the inexpensive Italian BTPs that the ECB currently buys aggressively. Thus, we continue to overweight BTPs, and add Greek and Portuguese bonds to the list. Chart 27German Bunds Are Expensive

Winds Of Change: Germany Goes Green

Winds Of Change: Germany Goes Green

Chart 28German Yields Already Embed Plenty Pessimism About Europe

German Yields Already Embed Plenty Pessimism About Europe

German Yields Already Embed Plenty Pessimism About Europe

Relative to US Treasurys, the outlook for Bunds is more complex. On the one hand, the ECB will not tighten policy as much as the Fed later this cycle; moreover, European inflation is likely to remain below US levels this year, as well as through the business cycle. On the other hand, Bunds already embed a significantly lower real terminal rate proxy and term premium than Treasury Notes (Chart 28). Netting it all out, BCA Research Global Fixed Income Strategy service believes Bunds should outperform Treasurys this year, because they have a lower beta, which is a valuable feature in a rising yield environment.6 We will closely monitor risks around this view, because it is likely that the European economic recovery will be the catalyst for the next up leg in global yields, in which case German bunds could temporarily underperform. On a structural basis, as long as Germany’s productivity issues are not addressed by Berlin, German Bunds are likely to remain an anchor for global yields. Germany will remain awash in excess savings, which will act as a deflationary anchor, while also limiting the long-term upside for European real rates. Excess savings results in a large current account surplus; thus, Germany will continue to export its savings abroad and act as a containing factor for global yields. The Euro The medium-term outlook points to significant euro upside. Our expectation of a European and German positive growth surprise over the coming 12 months is consistent with an outperformance of the euro. The fact that investors have been moving funds out of the Eurozone and into the US at an almost constant rate for the past 10 years only lends credence to this argument (Chart 29). Our view on Germany’s fiscal policy contributes to the euro’s luster. Greater German budget deficits help European economic activity and curtail risk premia across the Eurozone. This process is doubly positive for the euro. First, lower risk premia in the periphery invite inflows into the euro area, especially since Greek, Portuguese, Italian, or Spanish yields offer better value than alternatives. Second, stronger growth and lower risk premia relieve pressure on the ECB as the sole reflator for the Eurozone. At the margin, this process should boost the extremely depressed terminal rate proxy for Europe and help EUR/USD. Robust global economic activity adds to the euro’s appeal, beyond the positive domestic forces at play in Europe. The dollar is a countercyclical currency; thus, global business cycle upswings coincide with a weak USD, which increases EUR/USD’s appeal. Nonetheless, if the boost to global activity emanates from the US, then the dollar can strengthen. This phenomenon was at play in the first quarter of 2021. However, the global growth leadership is set to move away from the US over the next 12 months, which implies that the normal inverse relationship between the dollar and global growth will reassert itself to the euro’s benefit. The European balance of payments dynamics will consolidate the attraction of the euro. Germany’s and the Eurozone’s current account surplus will remain wide, especially in comparison to the expanding twin deficit plaguing the US. Beyond the next 12 to 24 months, the lack of structural vigor of Germany’s and Europe’s economy is likely to shift the euro into a safe-haven currency, like the yen and the Swiss franc. A strong balance of payments and low interest rates (all symptoms of excess savings) are the defining features of funding currencies, and will be permanent attributes of the euro area if reforms do not address its productivity malaise. The Eurozone’s net international position is already rising and its low inflation will put a structural upward bias to the Euro’s purchasing power parity estimates (Chart 30). Those developments have all been evident in Japan and Switzerland, and will likely extinguish the euro’s pro-cyclicality as time passes. Chart 29Investors Already Underweight European Assets

Investors Already Underweight European Assets

Investors Already Underweight European Assets

Chart 30Upward Bias In The Euro's Fair Value

Upward Bias In The Euro's Fair Value

Upward Bias In The Euro's Fair Value

Chart 31Germany Has Not Outperformed The Rest Of The Eurozone

Germany Has Not Outperformed The Rest Of The Eurozone

Germany Has Not Outperformed The Rest Of The Eurozone

German Equities In absolute terms, the DAX and German equities still possess ample upside over the next 12 to 24 months. BCA Research is assuming a positive stance on equities, and a high beta market like Germany stands to benefit.7 Moreover, the elevated sensitivity to global economic activity of German equities accentuate their appeal. BCA Research likes European stocks, and German ones are no exception.8 The more complex question is how to position German equities within a European stock portfolio. After massively outperforming from 2003 to 2012, German equities have moved in line with the rest of the Eurozone ever since (Chart 31). Moreover, German equities now trade at a discount on all the major valuation metrics relative to the rest of the Eurozone (Chart 31, bottom panel). The global macro forces that dictate the outlook for German equities relative to the rest of the Eurozone are currently sending conflicting messages. On the one hand, German equities normally outperform when commodity prices rally or when the euro appreciates (Chart 32). On the other hand, however, German equities also underperform when global yields rise, or following periods when Chinese excess reserves fall, such as what we are witnessing today. With this lack of clarity from global forces, the answer to Germany’s relative performance question lies within European economic dynamics. Germany is losing competitiveness relative to the rest of the Eurozone (Chart 24 page 22) which suggests that German stocks will benefit less than their peers from a stronger euro in comparison to their performance in the last decade. Moreover, German equities outperform when the German manufacturing PMI increases relative to that of the broad euro area. The gap between the German and euro area manufacturing PMI stands near record highs and is likely to narrow as the rest of the Eurozone catches up. This should have a bearing on the performance of German stocks (Chart 33). Chart 32Mixed Global Backdrop For Germany's Relative Performance

Mixed Global Backdrop For Germany's Relative Performance

Mixed Global Backdrop For Germany's Relative Performance

Chart 33A European Economic Catch-Up Would Hurt German Equities

A European Economic Catch-Up Would Hurt German Equities

A European Economic Catch-Up Would Hurt German Equities

Finally, sectoral dynamics may prove to be the ultimate arbiter. Table 4 highlights the limited difference in sectoral weightings between Germany and the rest of the Eurozone, which helps explain the stability in the relative performance over the past nine years. However, the variance is greater between Germany and specific European nations. In this approach, BCA’s negative stance on growth stocks correlates with an overweight of Germany relative to the Netherlands. Moreover, our positive outlook on financials and bond yields suggests that Germany should underperform Italian and Spanish stocks. Table 4Sectoral Breakdown Across Europe Major Bourses

Winds Of Change: Germany Goes Green

Winds Of Change: Germany Goes Green

Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Mathieu Savary, Chief European Investment Strategist Mathieu@bcaresearch.com Appendix: Global Climate Policy Commitments

Winds Of Change: Germany Goes Green

Winds Of Change: Germany Goes Green

Winds Of Change: Germany Goes Green

Winds Of Change: Germany Goes Green

Footnotes 1 See Matthew Karnitschnig, "German Conservatives Mired In ‘The Swamp,’" Politico, March 24, 2021, politico.eu. 2 The Greens are interested in a range of taxes, including a carbon tax, a digital services tax, and a financial transactions tax. They are also interested in industrial quotas requiring steel and car makers to sell a certain proportion of carbon-neutral steel and electric vehicles. See an excellent interview with Ms. Baerbock in Ileana Grabitz and Katharina Schuler, "I don’t have to convert the SUV driver in Prenzlauer Berg," Zeit Online, January 2, 2020, zeit.de. 3 See her comments to Zeit Online. 4 Please see BCA Research Global Investment Strategy Strategy Outlook "Second Quarter 2021 Strategy Outlook: Inflation Cometh?", dated March 26, 2021, available at gis.bcareseach.com. 5 Please see BCA Research European Investment Strategy Special Report "A Temporary Decoupling", dated April 5, 2021, available at eis.bcareseach.com. 6 Please see BCA Research Global Fixed Income Strategy Strategy Report "Harder, Better, Faster, Stronger", dated March 16, 2021, available at gfis.bcareseach.com. 7 Please see BCA Research Global Income Strategy Strategy Outlook "Second Quarter 2021 Strategy Outlook: Inflation Cometh?", dated March 26, 2021, available at gis.bcareseach.com. 8 Please see BCA Research European Income Strategy Strategy Report "Time And Attraction", dated April 12, 2021, available at eis.bcareseach.com.

Highlights Stronger global growth in the wake of continued and expected fiscal and monetary stimulus, and progress against COVID-19 are boosting oil demand assumptions by the major data suppliers for this year. We lifted our 2021 global demand estimate by 640k b/d to 98.25mm b/d, and assume OPEC 2.0 will make the necessary adjustments to keep Brent prices closer to $60/bbl than not, so as not to disrupt a fragile recovery. We are maintaining our 2022 and 2023 Brent forecasts at $65/bbl and $75/bbl. Commodity markets are ignoring the rising odds of armed conflict involving the US, Russia and China and their clients and allies. Russia has massed troops on Ukraine’s border and warned the US not to interfere. China has massed warships off the coast of the Philippines, and continues its incursions in Taiwan’s air-defense zone, keeping US forces on alert. Intentional or accidental engagement would spike oil prices. Two-way price risk abounds. In addition to the risk of armed hostilities, faster distribution of vaccines would accelerate recovery and boost prices above our forecasts. Downside risk of a resurgence in COVID-19-induced lockdowns remains, as rising death and hospitalization rates in Brazil, India and Europe attest (Chart of the Week). Feature Oil-demand estimates – ours included – are reviving in the wake of measurable progress in combating the COVID-19 pandemic in major economies, and an abundance of fiscal and monetary stimulus, particularly out of the US.1 On the back of higher IMF GDP projections, we lifted our 2021 global demand estimate by 640k b/d to 98.25mm b/d in this month’s balances. In our modeling, we assume OPEC 2.0 will make the necessary adjustments to keep Brent prices closer to $60/bbl than not, so as not to disrupt a fragile recovery. In an unusual turn of events, the early stages of the recovery in oil demand will be led by DM markets, which we proxy using OECD oil consumption (Chart 2). Thereafter, EM economies, re-take the growth lead next year and into 2023. Chart of the WeekCOVID-19 Deaths, Hospitalizations Threaten Global Recovery

Upside Oil Price Risks Are Increasing

Upside Oil Price Risks Are Increasing

Chart 2DM Demand Surges This Year

DM Demand Surges This Year

DM Demand Surges This Year

Absorbing OPEC 2.0 Spare Capacity We continue to model OPEC 2.0, the producer coalition led by the Kingdom of Saudi Arabia (KSA) and Russia, as the dominant producer in the market. The growth we are expecting this year will absorb a significant share of OPEC 2.0’s spare capacity, most of which – ~ 6mm b/d of the ~ 8mm b/d – is to be found in KSA (Chart 3). The core producers’ spare capacity allows them to meet recovering demand faster than the US shale producers can mobilize rigs and crews and get new supply into gathering lines and on to main lines. We model the US shale producers as a price-taking cohort, who will produce whatever the market allows them to produce. After falling to 9.22mm b/d in 2020, we expect US production to recover to 9.56mm b/d this year, 10.65mm b/d in 2022, and 11.18mm in 2023 (Chart 4). Lower 48 production growth in the US will be led by the shales, which will account for ~ 80% of total US output each year. Chart 3Core OPEC 2.0 Spare Capacity Will Respond First To Higher Demand

Core OPEC 2.0 Spare Capacity Will Respond First To Higher Demand

Core OPEC 2.0 Spare Capacity Will Respond First To Higher Demand

Chart 4Shale Is The Marginal Barrel In The Price Taking Cohort

Shale Is The Marginal Barrel In The Price Taking Cohort

Shale Is The Marginal Barrel In The Price Taking Cohort

OPEC 2.0’s dominant position on the supply side allows it to capture economic rents before non-coalition producers, which will remain a disincentive to them until the spare capacity is exhausted. Thereafter, the price-taking cohort likely will fund much of its E+P activities out of retained earnings, given their limited ability to attract capital. Equity investors will continue to demand dividends that can be maintained and grown, or return of capital via share buybacks. This will restrain production growth to those firms that are profitable. We expect the OPEC 2.0 coalition’s production discipline will keep supply levels just below demand so that inventories continue to fall, just as they have done during the COVID-19 pandemic, despite the demand destruction it caused (Chart 5). These modeling assumptions lead us to continue to expect supply and demand will continue to move toward balance into 2023 (Table 1). Chart 5Supply-Demand Balances in 2021

Supply-Demand Balances in 2021

Supply-Demand Balances in 2021

Table 1BCA Global Oil Supply - Demand Balances (MMb/d, Base Case Balances)

Upside Oil Price Risks Are Increasing

Upside Oil Price Risks Are Increasing

We continue to expect this balancing to induce persistent physical deficits, which will keep inventories falling into 2023 (Chart 6). As inventories are drawn, OPEC 2.0’s dominant-producer position will allow it to will keep the Brent and WTI forward curves backwardated (Chart 7).2 We are maintaining our 2022 and 2023 Brent forecasts at $65/bbl and $75/bbl (Chart 8). Chart 6OPEC 2.0 Policy Continues To Keep Supply Below Demand...

OPEC 2.0 Policy Continues To Keep Supply Below Demand...

OPEC 2.0 Policy Continues To Keep Supply Below Demand...

Chart 7OECD Inventories Fall to 2023

OECD Inventories Fall to 2023

OECD Inventories Fall to 2023

Chart 8Brent Forecasts Rise As Global Economy Recovers

Brent Forecasts Rise As Global Economy Recovers

Brent Forecasts Rise As Global Economy Recovers

Two-Way Price Risk Abounds Risks to our views abound on the upside and the downside. To the upside, the example of the UK and the US in mobilizing its distribution of vaccines is instructive. Both states got off to a rough start, particularly the US, which did not seem to have a strategy in place as recently as January. After the US kicked its procurement and distribution into high gear its vaccination rates soared and now appear to be on track to deliver a “normal” Fourth of July holiday in the US. The UK has begun its reopening this week. Both states are expected to achieve herd immunity in 3Q21.3 The EU, which mishandled its procurement and distribution likely benefits from lessons learned in the UK and US and achieves herd immunity in 4Q21, according to McKinsey’s research. Any acceleration in this timetable likely would lead to stronger growth and higher oil prices. The next big task for the global community will be making vaccines available to EM economies, particularly those in which the pandemic is accelerating and providing the ideal setting for mutations and the spread of variants that could become difficult to contain. The risk of a resurgence in large-scale COVID-19-induced lockdowns remains, as rising death and hospitalization rates in Brazil, India and Europe attest. Cry Havoc The other big upside risk we see is armed conflict involving the US, Russia, China and their clients and allies. Commodity markets are ignoring these risks at present. Even though they do not rise to the level of war, the odds of kinetic engagement – planes being shot down or ships engaging in battle in the South China Sea – are rising on a daily basis. This is not unexpected, as our colleagues in BCA Research’s Geopolitical Strategy pointed out recently.4 Indeed, our GPS service, led by Matt Gertken, warned the Biden administration would be tested in this manner by Russia and China from the get-go. Russia has massed troops on Ukraine’s border and warned the US not to interfere. China has massed warships off the coast of the Philippines, and continues its incursions in Taiwan’s air-defense zone, keeping US forces on alert. Political dialogue between the US and Russia and the US and China is increasingly vitriolic, with no sign of any leavening in the near future. Intentional or accidental engagement could let slip the dogs of war and spike oil prices briefly. Finally, OPEC 2.0 is going to have to accommodate the “official” return of Iran as a bona fide oil exporter, if, as we expect, it is able to reinstate its nuclear deal – i.e., the Joint Comprehensive Plan of Action (JCPOA) – with Western states, which was abrogated by then-President Donald Trump in 2018. This may prove difficult, given our view that the oil-price collapse of 2014-16 was the result of the Saudis engineering a market-share war to tank prices, in an effort to deny Iran $100+ per-barrel prices that had prevailed between end-2010 and mid-2014. OPEC 2.0, particularly KSA, has not publicly involved itself in the US-Iran negotiations. However, it is worthwhile recalling that following the disastrous market-share war launched in 2014, KSA and the rest of OPEC 2.0 did accommodate Iran’s return to markets post-JCPOA. Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Ashwin Shyam Research Associate Commodity & Energy Strategy ashwin.shyam@bcaresearch.com Commodities Round-Up Energy: Bullish Brent and WTI prices rallied sharply following the release of the EIA’s Weekly Petroleum Status Report showing a 9.1mm-barrel decline in US crude and product stocks for the week ended 9 April 2021. This was led by a huge draw in commercial crude and distillate inventories (5.9mm barrels and 2.1mm barrels, respectively). These draws came on the back of generally bullish global demand upgrades by the major data services (EIA, IEA and OPEC) over the past week. These assessments were supported by EIA data showing refined-product demand – i.e., “product supplied” – jumped 1.1mm b/d for the week ended 9 April. With vaccine distributions picking up steam, despite setbacks on the Johnson & Johnson jab, the storage draws and improved demand appear to have catalyze the move higher. Continued weakness in the USD also provided a tailwind, as did falling real interest rates in the US. Base Metals: Bullish Nickel prices fell earlier this week, as China’s official Xinhua news agency reported that Chinese Premier, Li Keqiang stressed the need to strengthen raw materials’ market regulation, amidst rising commodities prices, which been pressuring corporate financial performance (Chart 9). This statement came after China’s top economic advisor, Liu He also called for authorities to track commodities prices last week. Nickel prices fell by around $500/ ton earlier this week on this news, and were trading at $16,114.5/MT on the London Metals exchange as of Tuesday’s close. Other base metals were not affected by this news. Precious Metals: Bullish The US dollar and 10-year treasury yields fell after March US inflation data was released earlier this week. US consumer prices rose by the most in nearly nine years. The demand for an inflation hedge, coupled with the falling US dollar and treasury yields, which reduce the opportunity cost of purchasing gold, caused gold prices to rise (Chart 10). This uncertainty, coupled with the increasing inflationary pressures due to the US fiscal stimulus will increase demand for gold. Spot COMEX gold prices were trading at $1,746.20/oz as of Tuesday’s close. Ags/Softs: Neutral The USDA reported ending stocks of corn in the US stood at 1.35 billion bushels, well below market estimates of 1.39 billion and the 1.50 billion-bushel estimate by the Department last month, according to agriculture.com’s tally. Global corn stocks ended at 283.9mm MT vs a market estimate of 284.5mm MT and a Department estimate of 287.6mm MT. Chart 9Base Metals Are Being Bullish

Base Metals Are Being Bullish

Base Metals Are Being Bullish

Chart 10Gold Prices To Rise

Gold Prices To Rise

Gold Prices To Rise

Footnotes 1 Please see US-Russia Pipeline Standoff Could Push LNG Prices Higher, which we published on 8 April 2021 re the IMF’s latest forecast for global growth. Briefly, the Fund raised its growth expectations for this year and next to 6% and 4.4%, respectively, nearly a full percentage-point increase versus its January forecast update for 2021 2 A backwardated forward curve – prompt prices trading in excess of deferred prices – is the market’s way of signaling tightness. It means refiners of crude oil value crude availability right now over availability a year from now. This is exactly the same dynamic that drives an investor to pay $1 today for a dollar bill delivered tomorrow than for that same dollar bill delivered a year from now (that might only fetch 98 cents today, e.g.). 3 Please see When will the COVID-19 pandemic end?, published 26 March 2021 by McKinsey & Co. 4 Please see The Arsenal Of Democracy, a prescient analysis published 2 April 2021 by BCA’s Geopolitical Strategy. The report notes the Biden administration “still faces early stress-tests on China/Taiwan, Russia, Iran, and even North Korea. Game theory helps explain why financial markets cannot ignore the 60% chance of a crisis in the Taiwan Strait. A full-fledged war is still low-probability, but Taiwan remains the world’s preeminent geopolitical risk.” Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades Commodity Prices and Plays Reference Table Trades Closed in 2021 Summary of Closed Trades

Higher Inflation On The Way

Higher Inflation On The Way