Euro Area

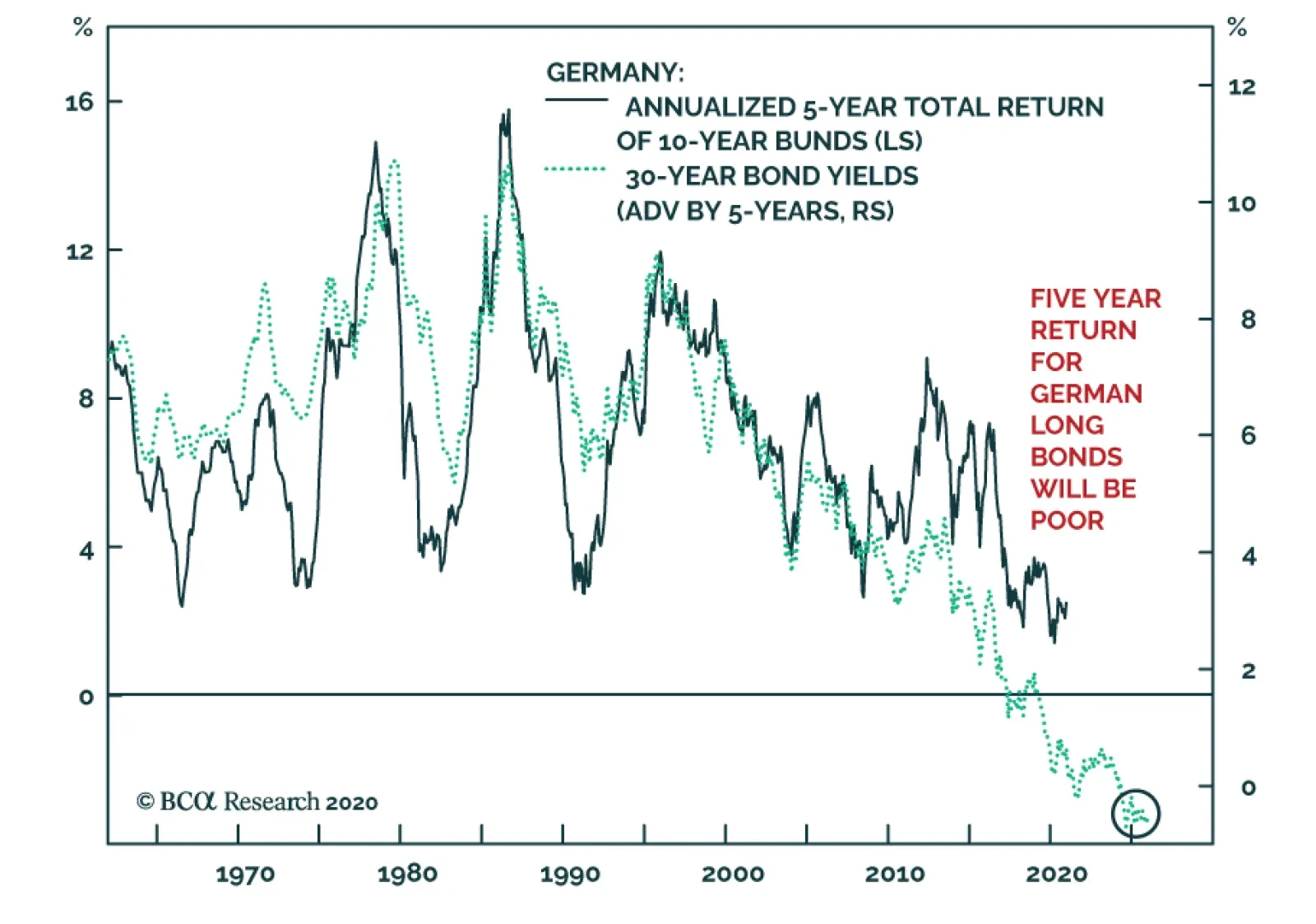

Empirically, the current yield to maturity gives a robust sense of the returns of 30-year German government bonds over the coming five years. At the present juncture, the yield of -0.2% suggests that over the next five years, the German long bond could…

Highlights With a vaccine already rolling out in the UK and soon in the US, investors have reason to be optimistic about next year. Government bond yields are rising, cyclical equities are outperforming defensives, international stocks hinting at outperforming American, and value stocks are starting to beat growth stocks (Chart 1). Feature President Trump’s defeat in the US election also reduces the risk of a global trade war, or a real war with Iran. European, Chinese, and Emirati stocks have rallied since the election, at least partly due to the reduction in these risks (Chart 2). However, geopolitical risk and global policy uncertainty have been rising on a secular, not just cyclical, basis (Chart 3). Geopolitical tensions have escalated with each crisis since the financial meltdown of 2008. Chart 1A New Global Business Cycle

A New Global Business Cycle

A New Global Business Cycle

Chart 2Biden: No Trade War Or War With Iran?

Biden: No Trade War Or War With Iran?

Biden: No Trade War Or War With Iran?

Chart 3Geopolitical Risk And Global Policy Uncertainty

Geopolitical Risk And Global Policy Uncertainty

Geopolitical Risk And Global Policy Uncertainty

Chart 4The Decline Of The Liberal Democracies?

The Decline Of The Liberal Democracies?

The Decline Of The Liberal Democracies?

Trump was a symptom, not a cause, of what ails the world. The cause is the relative decline of the liberal democracies in political, economic, and military strength relative to that of other global players (Chart 4). This relative decline has emboldened Chinese and Russian challenges to the US-led global order, as well as aggressive and unpredictable moves by middle and small powers. Moreover the aftershocks of the pandemic and recession will create social and political instability in various parts of the world, particularly emerging markets (Chart 5). Chart 5EM Troubles Await

EM Troubles Await

EM Troubles Await

Chart 6Global Arms Build-Up Continues

Global Arms Build-Up Continues

Global Arms Build-Up Continues

We are bullish on risk assets next year, but our view is driven largely from the birth of a new economic cycle, not from geopolitics. Geopolitical risk is rapidly becoming underrated, judging by the steep drop-off in measured risk. There is no going back to a pre-Trump, pre-Xi Jinping, pre-2008, pre-Putin, pre-9/11, pre-historical golden age in which nations were enlightened, benign, and focused exclusively on peace and prosperity. Hard data, such as military spending, show the world moving in the opposite direction (Chart 6). So while stock markets will grind higher next year, investors should not expect that Biden and the vaccine truly portend a “return to normalcy.” Key View #1: China’s Communist Party Turns 100, With Rising Headwinds Investors should ignore the hype about the Chinese Communist Party’s one hundredth birthday in 2021. Since 1997, the Chinese leadership has laid great emphasis on this “first centenary” as an occasion by which China should become a moderately prosperous society. This has been achieved. China is deep into a structural economic transition that holds out a much more difficult economic, social, and political future. Chart 7China: Less Money, More Problems

China: Less Money, More Problems

China: Less Money, More Problems

The big day, July 1, will be celebrated with a speech by General Secretary Xi Jinping in which he reiterates the development goals of the five-year plan. This plan – which doubles down on import substitution and the aggressive tech acquisition campaign – will be finalized in March, along with Xi’s yet-to-be released vision for 2035, which marks the halfway point to the “second centenary,” 2049, the hundredth birthday of the regime. Xi’s 2035 goals may contain some surprises but the Communist Party’s policy frameworks should be seen as “best laid plans” that are likely to be overturned by economic and geopolitical realities. It was easier for the country to meet its political development targets during the period of rapid industrialization from 1979-2008. Now China is deep into a structural economic transition that holds out a much more difficult economic, social, and political future. Potential growth is slowing with the graying of society and the country is making a frantic dash, primarily through technology acquisition, to boost productivity and keep from falling into the “middle income trap” (Chart 7). Total debt levels have surged as Beijing attempts to make this transition smoothly, without upsetting social stability. Households and the government are taking on a greater debt load to maintain aggregate demand while the government tries to force the corporate sector to deleverage in fits and starts (Chart 8). The deleveraging process is painful and coincides with a structural transition away from export-led manufacturing. Beijing likely believes it has already led de-industrialization proceed too quickly, given the huge long-term political risks of this process, as witnessed in the US and UK. The fourteenth five-year plan hints that the authorities will give manufacturing a reprieve from structural reform efforts (Chart 9). Chart 8China Struggles To Dismount Debt Bubble

China Struggles To Dismount Debt Bubble

China Struggles To Dismount Debt Bubble

Chart 9China Will Slow De-Industrialization, Stoking Protectionism

China Will Slow De-Industrialization, Stoking Protectionism

China Will Slow De-Industrialization, Stoking Protectionism

Chart 10China Already Reining In Stimulus

China Already Reining In Stimulus

China Already Reining In Stimulus

A premature resumption of deleveraging heightens domestic economic risks. The trade war and then the pandemic forced the Xi administration to abandon its structural reform plans temporarily and drastically ease monetary, fiscal, and credit policy to prevent a recession. Almost immediately the danger of asset bubbles reared its head again. Because the regime is focused on containing systemic financial risk, it has already begun tightening monetary policy as the nation heads into 2021 – even though the rest of the world has not fully recovered from the pandemic (Chart 10). The risk of over-tightening is likely to be contained, since Beijing has no interest in undermining its own recovery. But the risk is understated in financial markets at the moment and, combined with American fiscal risks due to gridlock, this familiar Chinese policy tug-of-war poses a clear risk to the global recovery and emerging market assets next year. Far more important than the first centenary, or even General Secretary Xi’s 2035 vision, is the impending leadership rotation in 2022. Xi was originally supposed to step down at this time – instead he is likely to take on the title of party chairman, like Mao, and aims to stay in power till 2035 or thereabouts. He will consolidate power once again through a range of crackdowns – on political rivals and corruption, on high-flying tech and financial companies, on outdated high-polluting industries, and on ideological dissenters. Beijing must have a stable economy going into its five-year national party congresses, and 2022 is no different. But that goal has largely been achieved through this year’s massive stimulus and the discovery of a global vaccine. In a risk-on environment, the need for economic stability poses a downside risk for financial assets since it implies macro-prudential actions to curb bubbles. The 2017 party congress revealed that Xi sees policy tightening as a key part of his policy agenda and power consolidation. In short, the critical twentieth congress in 2022 offers no promise of plentiful monetary and credit stimulus (Chart 11). All investors can count on is the minimum required for stability. This is positive for emerging markets at the moment, but less so as the lagged effects of this year’s stimulus dissipate. Chart 11No Promise Of Major New Stimulus For Party Congress 2022

No Promise Of Major New Stimulus For Party Congress 2022

No Promise Of Major New Stimulus For Party Congress 2022

Not only will Chinese domestic policy uncertainty remain underestimated, but geopolitical risk will also do so. Superficially, Beijing had a banner year in 2020. It handled the coronavirus better than other countries, especially the US, thus advertising Xi Jinping’s centralized and statist governance model. President Trump lost the election. Regardless of why Trump lost, his trade war precipitated a manufacturing slowdown that hit the Rust Belt in 2019, before the virus, and his loss will warn future presidents against assaulting China’s economy head-on, at least in their first term. All of this is worth gold in Chinese domestic politics. Chart 12China’s Image Suffered In Spite Of Trump

2021 Key Views: No Return To Normalcy

2021 Key Views: No Return To Normalcy

Internationally, however, China’s image has collapsed – and this is in spite of Trump’s erratic and belligerent behavior, which alienated most of the world and the US’s allies (Chart 12). Moreover, despite being the origin of COVID-19, China’s is one of the few economies that thrived this year. Its global manufacturing share rose. While delaying and denying transparency regarding the virus, China accused other countries of originating the virus, and unleashed a virulent “wolf warrior” diplomacy, a military standoff with India, and a trade war with Australia. The rest of Asia will be increasingly willing to take calculated risks to counterbalance China’s growing regional clout, and international protectionist headwinds will persist. The United States will play a leading part in this process. Sino-American strategic tensions have grown relentlessly for more than a decade, especially since Xi Jinping rose to power, as is evident from Chinese treasury holdings (Chart 13). The Biden administration will naturally seek a diplomatic “reset” and a new strategic and economic dialogue with China. But Biden has already indicated that he intends to insist on China’s commitments under Trump’s “phase one” trade deal. He says he will keep Trump’s sweeping Section 301 tariffs in place, presumably until China demonstrates improvement on the intellectual property and tech transfer practices that provided the rationale for the tariffs. Biden’s victory in the Rust Belt ensures that he cannot revert to the pre-Trump status quo. Indeed Biden amplifies the US strategic challenge to China’s rise because he is much more likely to assemble a “grand alliance” or “coalition of the willing” focused on constraining China’s illiberal and mercantilist policies. Even the combined economic might of a western coalition is not enough to force China to abandon its statist development model, but it would make negotiations more likely to be successful on the West’s more limited and transactional demands (Chart 14). Chart 13The US-China Divorce Pre-Dates And Post-Dates Trump

The US-China Divorce Pre-Dates And Post-Dates Trump

The US-China Divorce Pre-Dates And Post-Dates Trump

Chart 14Biden's Grand Alliance A Danger To China

Biden's Grand Alliance A Danger To China

Biden's Grand Alliance A Danger To China

The Taiwan Strait is ground zero for US-China geopolitical tensions. The US is reviving its right to arm Taiwan for the sake of its self-defense, but the US commitment is questionable at best – and it is this very uncertainty that makes a miscalculation more likely and hence conflict a major tail risk (Chart 15). True, Beijing has enormous economic leverage over Taiwan, and it is fresh off a triumph of imposing its will over Hong Kong, which vindicates playing the long game rather than taking any preemptive military actions that could prove disastrous. Nevertheless, Xi Jinping’s reassertion of Beijing and communism is driving Taiwanese popular opinion away from the mainland, resulting in a polarizing dynamic that will be extremely difficult to bridge (Chart 16). If China comes to believe that the Biden administration is pursuing a technological blockade just as rapidly and resolutely as the Trump administration, then it could conclude that Taiwan should be brought to heel sooner rather than later. Chart 15US Boosts Arms Sales To Taiwan

2021 Key Views: No Return To Normalcy

2021 Key Views: No Return To Normalcy

Chart 16Taiwan Strait Risk Will Explode If Biden Seeks Tech Blockade

2021 Key Views: No Return To Normalcy

2021 Key Views: No Return To Normalcy

Bottom Line: On a secular basis, China faces rising domestic economic risks and rising geopolitical risk. Given the rally in Chinese currency and equities in 2021, the downside risk is greater than the upside risk of any fleeting “diplomatic reset” with the United States. Emerging markets will benefit from China’s stimulus this year but will suffer from its policy tightening over time. Key View #2: The US “Pivot To Asia” Is Back On … And Runs Through Iran Most likely President-elect Biden will face gridlock at home. His domestic agenda largely frustrated, he will focus on foreign policy. Given his old age, he may also be a one-term president, which reinforces the need to focus on the achievable. He will aim to restore the Obama administration’s foreign policy, the chief features of which were the 2015 nuclear deal with Iran and the “Pivot to Asia.” The US is limited by the need to pivot to Asia, while Iran is limited by the risk of regime failure. A deal should be agreed. The purpose of the Iranian deal was to limit Iran’s nuclear and regional ambitions, stabilize Iraq, create a semblance of regional balance, and thus enable American military withdrawal. The US could have simply abandoned the region, but Iran’s ensuing supremacy would have destabilized the region and quickly sucked the US back in. The newly energy independent US needed a durable deal. Then it could turn its attention to Asia Pacific, where it needed to rebuild its strategic influence in the face of a challenger that made Iran look like a joke (Chart 17). Chart 17The "Pivot To Asia" In A Nutshell

The "Pivot To Asia" In A Nutshell

The "Pivot To Asia" In A Nutshell

It is possible for Biden to revive the Iranian deal, given that the other five members of the agreement have kept it afloat during the Trump years. Moreover, since it was always an executive deal that lacked Senate approval, Biden can rejoin unilaterally. However, the deal largely expires in 2025 – and the Trump administration accurately criticized the deal’s failure to contain Iran’s missile development and regional ambitions. Therefore Biden is proposing a renegotiation. This could lead to an even greater US-Iran engagement, but it is not clear that a robust new deal is feasible. Iran can also recommit to the old deal, having taken only incremental steps to violate the deal after the US’s departure – manifestly as leverage for future negotiations. Of course, the Iranians are not likely to give up their nuclear program in the long run, as nuclear weapons are the golden ticket to regime survival. Libya gave up its nuclear program and was toppled by NATO; North Korea developed its program into deliverable nuclear weapons and saw an increase in stature. Iran will continue to maintain a nuclear program that someday could be weaponized. Nevertheless, Tehran will be inclined to deal with Biden. President Hassan Rouhani is a lame duck, his legacy in tatters due to Trump, but his final act in office could be to salvage his legacy (and his faction’s hopes) by overseeing a return to the agreement prior to Iran’s presidential election in June. From Supreme Leader Ali Khamenei’s point of view, this would be beneficial. He also needs to secure his legacy, but as he tries to lay the groundwork for his power succession, Iran faces economic collapse, widespread social unrest, and a potentially explosive division between the Iranian Revolutionary Guard Corps and the more pragmatic political faction hoping for economic opening and reform. Iran needs a reprieve from US maximum pressure, so Khamenei will ultimately rejoin a limited nuclear agreement if it enables the regime to live to fight another day. In short, the US is limited by the need to pivot to Asia, while Iran is limited by the risk of regime failure. A deal should be agreed. But this is precisely why conflict could erupt in 2021. First, either in Trump’s final days in office or in the early days of the Biden administration, Israel could take military action – as it has likely done several times this year already – to set back the Iranian nuclear program and try to reinforce its own long-term security. Second, the Biden administration could decide to utilize the immense leverage that President Trump has bequeathed, resulting in a surprisingly confrontational stance that would push Iran to the brink. This is unlikely but it may be necessary due to the following point. Third, China and Russia could refuse to cooperate with the US, eliminating the prospect of a robust renegotiation of the deal, and forcing Biden to choose between accepting the shabby old deal or adopting something similar to Trump’s maximum pressure. China will probably cooperate; Russia is far less certain. Beijing knows that the US intention in Iran is to free up strategic resources to revive the US position in Asia, but it has offered limited cooperation on Iran and North Korea because it does not have an interest in their acquiring nuclear weapons and it needs to mitigate US hostility. Biden has a much stronger political mandate to confront China than he does to confront Iran. Assuming that the Israelis and Saudis can no more prevent Biden’s détente with Iran than they could Obama’s, the next question will be whether Biden effectively shifts from a restored Iranian deal to shoring up these allies and partners. He can possibly build on the Abraham Accords negotiated by the Trump administration smooth Israeli ties with the Arab world. The Middle East could conceivably see a semblance of balance. But not in 2021. The coming year will be the rocky transition phase in which the US-Iran détente succeeds or fails. Chart 18Oil Market Share War Preceded The Last US-Iran Deal

Oil Market Share War Preceded The Last US-Iran Deal

Oil Market Share War Preceded The Last US-Iran Deal

Chart 19Still, Base Case Is For Rising Oil Prices

Still, Base Case Is For Rising Oil Prices

Still, Base Case Is For Rising Oil Prices

Chart 20Biden Needs A Credible Threat

Biden Needs A Credible Threat

Biden Needs A Credible Threat

The lead-up to the 2015 Iranian deal saw a huge collapse in global oil prices due to a market share war with Saudi Arabia, Russia, and the US triggered by US shale production and Iranian sanctions relief (Chart 18). This was despite rising global demand and the emergence of the Islamic State in Iraq. In 2021, global demand will also be reviving and Iraq, though not in the midst of full-scale war, is still unstable. OPEC 2.0 could buckle once again, though Moscow and Riyadh already confirmed this year that they understand the devastating consequences of not cooperating on production discipline. Our Commodity and Energy Strategy projects that the cartel will continue to operate, thus drawing down inventories (Chart 19). The US and/or Israel will have to establish a credible military threat to ensure that Iran is in check, and that will create fireworks and geopolitical risks first before it produces any Middle Eastern balance (Chart 20). Bottom Line: The US and Iran are both driven to revive the 2015 nuclear deal by strategic needs. Whether a better deal can be negotiated is less likely. The return to US-Iran détente is a source of geopolitical risk in 2021 though it should ultimately succeed. The lower risk of full-scale war is negative for global oil prices but OPEC 2.0 cartel behavior will be the key determiner. The cartel flirted with disaster in 2020 and will most likely hang together in 2021 for the sake of its members’ domestic stability. Key View #3: Europe Wins The US Election Chart 21Europe Won The US Election

Europe Won The US Election

Europe Won The US Election

The European Union has not seen as monumental of a challenge from anti-establishment politicians over the past decade as have Britain and America. The establishment has doubled down on integration and solidarity. Now Europe is the big winner of the US election. Brussels and Berlin no longer face a tariff onslaught from Trump, a US-instigated global trade war, or as high of a risk of a major war in the Middle East. Biden’s first order of business will be reviving the trans-Atlantic alliance. Financial markets recognize that Europe is the winner and the euro has finally taken off against the dollar over the past year. European industrials and small caps outperformed during the trade war as well as COVID-19, a bullish signal (Chart 21). Reinforcing this trend is the fact that China is looking to court Europe and reduce momentum for an anti-China coalition. The center of gravity in Europe is Germany and 2021 faces a major transition in German politics. Chancellor Angela Merkel will step down at long last. Her Christian Democratic Union is favored to retain power after receiving a much-needed boost for its handling of this year’s crisis (Chart 22), although the risk of an upset and change of ruling party is much greater than consensus holds. Chart 22German Election Poses Political Risk, Not Investment Risk

German Election Poses Political Risk, Not Investment Risk

German Election Poses Political Risk, Not Investment Risk

However, from an investment point of view, an upset in the German election is not very concerning. A left-wing coalition would take power that would merely reinforce the shift toward more dovish fiscal policy and European solidarity. Either way Germany will affirm what France affirmed in 2017, and what France is on track to reaffirm in 2022: that the European project is intact, despite Brexit, and evolving to address various challenges. The European project is intact, despite Brexit, and evolving to address various challenges. This is not to say that European elections pose no risk. In fact, there will be upsets as a result of this year’s crisis and the troubled aftermath. The countries with upcoming elections – or likely snap elections in the not-too-distant future, like Spain and Italy – show various levels of vulnerability to opposition parties (Chart 23). Chart 23Post-COVID EU Elections Will Not Be A Cakewalk

Post-COVID EU Elections Will Not Be A Cakewalk

Post-COVID EU Elections Will Not Be A Cakewalk

Chart 24Immigration Tailwind For Populism Subsided

Immigration Tailwind For Populism Subsided

Immigration Tailwind For Populism Subsided

The chief risks to Europe stem from fiscal normalization and instability abroad. Regime failures in the Middle East and Africa could send new waves of immigration, and high levels of immigration have fueled anti-establishment politics over the past decade. Yet this is not a problem at the moment (Chart 24). And even more so than the US, the EU has tightened border enforcement and control over immigration (Chart 25). This has enabled the political establishment to save itself from populist discontent. The other danger for Europe is posed by Russian instability. In general, Moscow is focusing on maintaining domestic stability amid the pandemic and ongoing economic austerity, as well as eventual succession concerns. However, Vladimir Putin’s low approval rating has often served as a warning that Russia might take an external action to achieve some limited national objective and instigate opposition from the West, which increases government support at home (Chart 26). Chart 25Europe Tough On Immigration Like US

Europe Tough On Immigration Like US

Europe Tough On Immigration Like US

Chart 26Warning Sign That Russia May Lash Out

Warning Sign That Russia May Lash Out

Warning Sign That Russia May Lash Out

Chart 27Russian Geopolitical Risk Premium Rising

Russian Geopolitical Risk Premium Rising

Russian Geopolitical Risk Premium Rising

The US Democratic Party is also losing faith in engagement with Russia, so while it will need to negotiate on Iran and arms reduction, it will also seek to use sanctions and democracy promotion to undermine Putin’s regime and his leverage over Europe. The Russian geopolitical risk premium will rise, upsetting an otherwise fairly attractive opportunity relative to other emerging markets (Chart 27). Bottom Line: The European democracies have passed a major “stress test” over the past decade. The dollar will fall relative to the euro, in keeping with macro fundamentals, though it will not be supplanted as the leading reserve currency. Europe and the euro will benefit from the change of power in Washington, and a rise in European political risks will still be minor from a global point of view. Russia and the ruble will suffer from a persistent risk premium. Investment Takeaways As the “Year of the Rat” draws to a close, geopolitical risk and global policy uncertainty have come off the boil and safe haven assets have sold off. Yet geopolitical risk will remain elevated in 2021. The secular drivers of the dramatic rise in this risk since 2008 have not been resolved. To play the above themes and views, we are initiating the following strategic investment recommendations: Long developed market equities ex-US – US outperformance over DM has reached extreme levels and the global economic cycle and post-pandemic revival will favor DM-ex-US. Long emerging market equities ex-China – Emerging markets will benefit from a falling dollar and commodity recovery. China has seen the good news but now faces the headwinds outlined above. Long European industrials relative to global – European equities stand to benefit from the change of power in Washington, US-China decoupling, and the global recovery. Long Mexican industrials versus emerging markets – Mexico witnessed the rise of an American protectionist and a landslide election in favor of a populist left-winger. Now it has a new trade deal with the US and the US is diversifying from China, while its ruling party faces a check on its power via midterm elections, and, regardless, has maintained orthodox economic policy. Long Indian equities versus Chinese – Prime Minister Narendra Modi has a single party majority, four years on his political clock, and has recommitted to pro-productivity structural reforms. The nation is taking more concerted action in pursuit of economic development since strategic objectives in South Asia cannot be met without greater dynamism. The US, Japan, Australia, and other countries are looking to develop relations as they diversify from China. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com

The European Central Bank (ECB) followed through on messaging that it would “recalibrate its instruments” in order to stimulate further amid renewed weakness in Europe. As expected, the central bank expanded the PEPP by 500 billion euros to 1.85 trillion…

The euro area is likely to experience a contraction in economic activity in the 4th quarter of 2020, but there is hope this deterioration is already passing. The decline in activity highlighted by the Google Mobility Trend data is a direct…

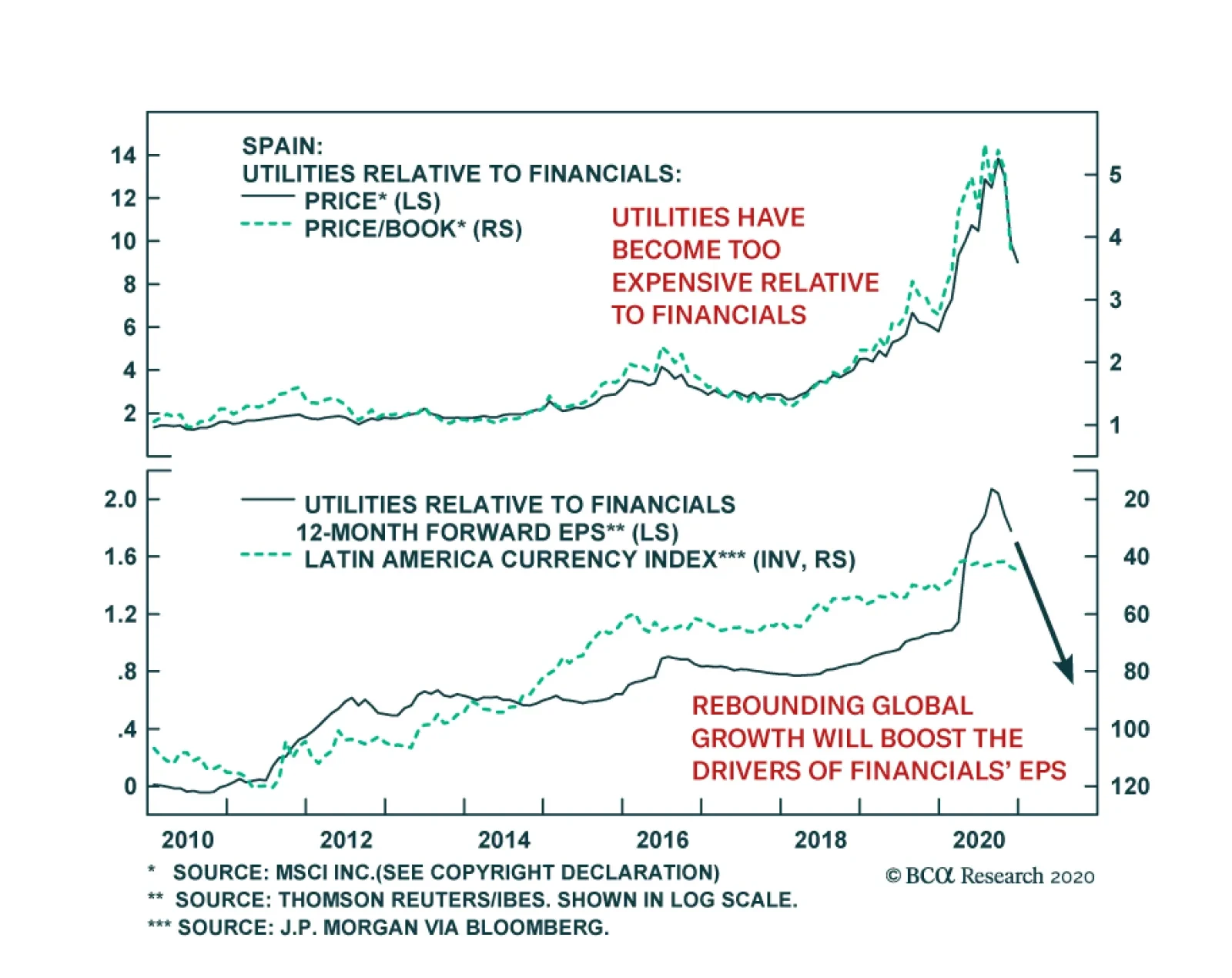

Spanish utilities surged 13-folds relative to Spanish financials between 2009 and October 2020. This incredible outperformance was rooted in many factors. Over this period, relative forward earnings increased 6-folds. Utilities were able to grow their…

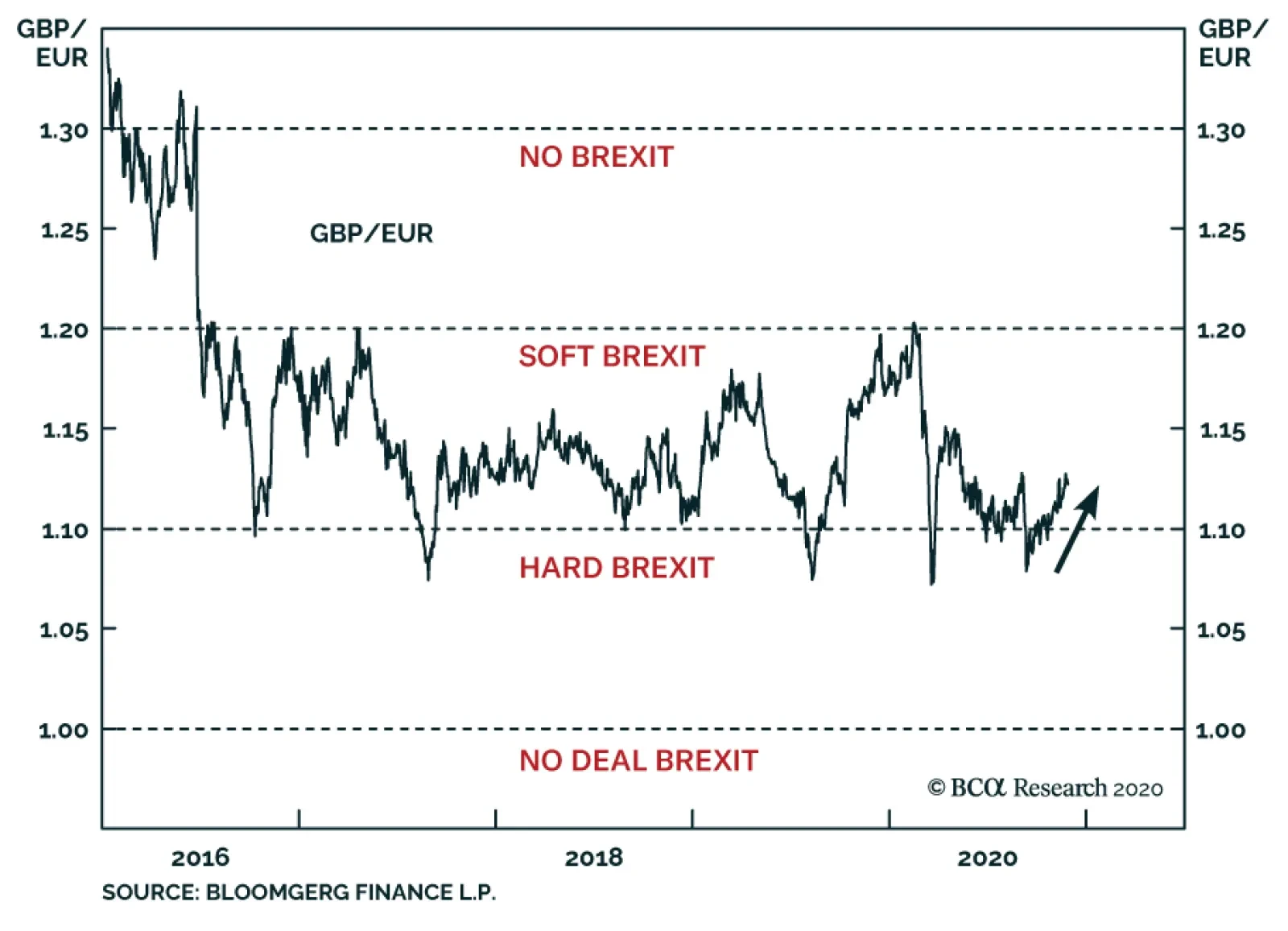

According to BCA Research's Geopolitical Strategy service, it is not too late to go long GBP-EUR. A near-term global risk-off move would work against this trade, but it is a strategic opportunity. The Brexit finale is approaching as the UK and EU enter the…

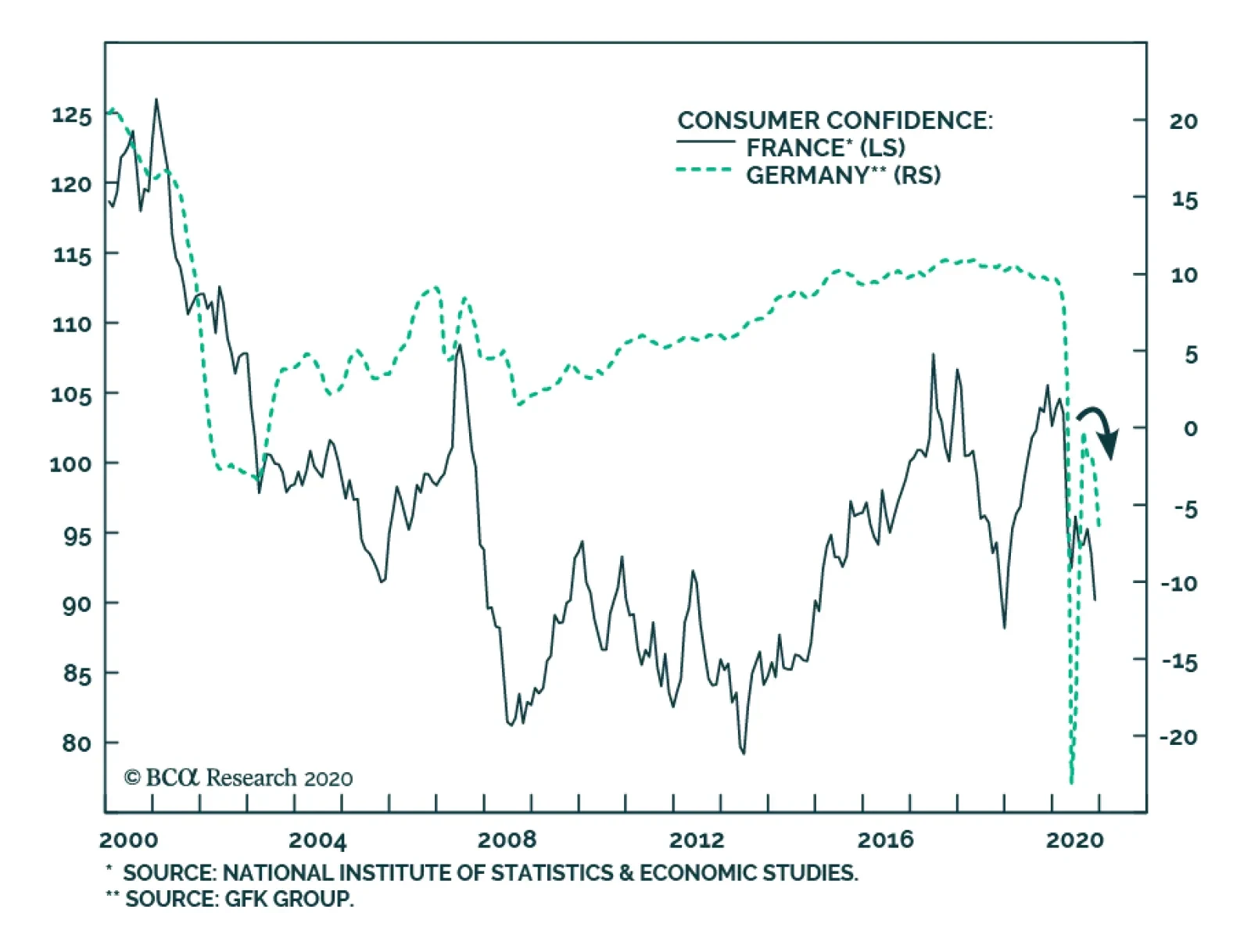

Consumer sentiment in the euro area’s two largest economies is souring amid the institution of renewed measures to control the pandemic. Germany’s GfK consumer confidence survey slipped to -6.7 from -3.2, missing expectations of a decline to -4.9. Similarly,…

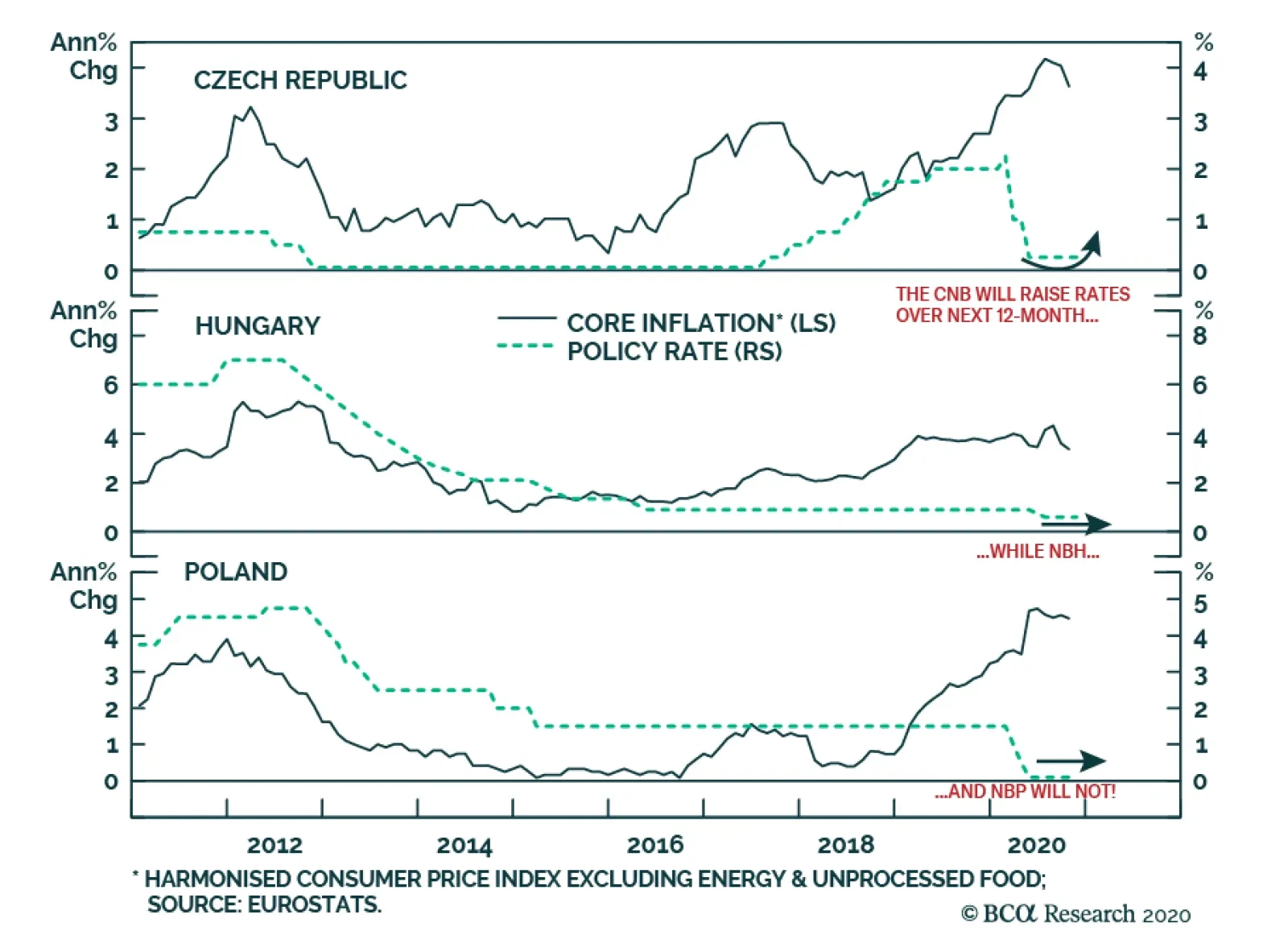

Among Central European (CE) currencies, BCA Research's Emerging Markets Strategy service remains upbeat on the Czech koruna (CZK) due to a relatively hawkish central bank. Meanwhile, the Hungarian forint and Polish zloty are bound to continue underperforming…

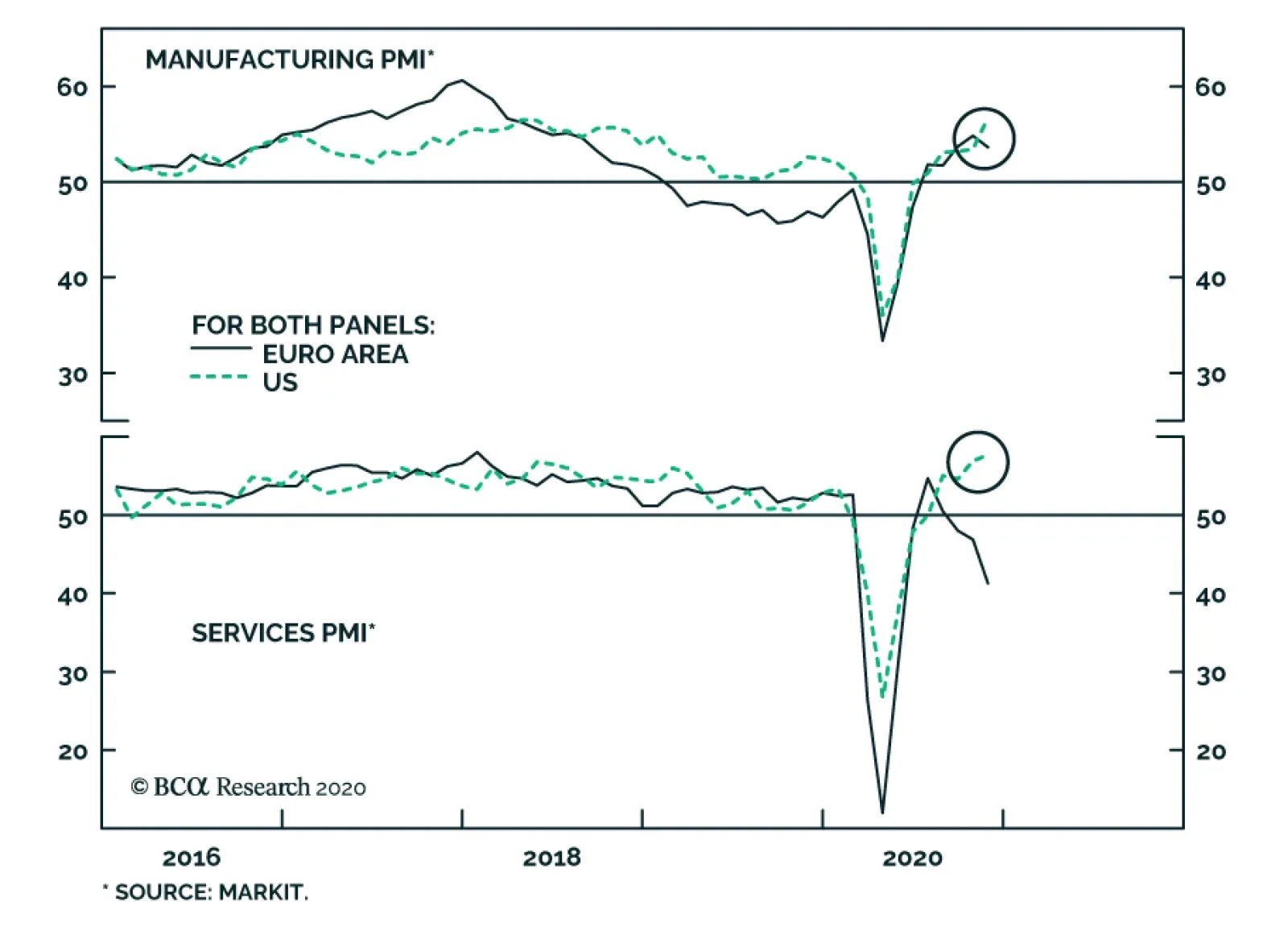

The Eurozone Flash Composite PMI in November fell from 50 to 45.1, the lowest reading since May. The collapse in services led the overall index lower. It fell to 41.3 from 46.9, slightly below expectations of 42 and reflecting the impact of the lockdown…

Highlights There is some evidence that the euro could gravitate to 1.50 over the next few years. The key assumption is that the equilibrium rate of interest will rise in the euro area relative to that in the US. Our bias is that fair value for the euro is closer to 1.35, or 15% above current levels. Over the very near term, the risks are tilted towards the downside. But while EUR/USD could punch below 1.15, an undershoot towards parity is highly unlikely. In our FX portfolio, we are long EUR/CHF and short EUR/GBP. We would buy the euro outright below 1.15. Feature The markets have rejoiced at the success of a few vaccine trials and are looking forward to a return to normalcy in 2021. Around the world, equity markets have rallied in symphony. Even secular dogs such as the Japanese Nikkei, which has been in a relative bear market for many decades, broke to fresh 21-year highs. Copper prices are rising fervently, and measures of risk, such as the VIX index or high-yield corporate spreads, are collapsing to pre-pandemic levels both in the US and Europe. As a procyclical currency, the euro has also been quite cheerful. Bullish sentiment on the euro is at a decade high and the currency has rallied 11% from the lows, commensurate with the drop in the DXY index (Chart 1). As a share of total open interest, 80% of speculators are bullish on the euro. Historically, sentiment at this level has been usually associated with the euro being closer to 1.50. Chart 1Sentiment On The Euro Is Elevated

Sentiment On The Euro Is Elevated

Sentiment On The Euro Is Elevated

Chart 2The Euro Is Lagging Copper Prices

The Euro Is Lagging Copper Prices

The Euro Is Lagging Copper Prices

The juxtaposition of much welcomed good news and elevated sentiment sets the euro in a very precarious tug of war. Standard theory suggests that the post-pandemic trade may already be priced into the common currency, given bullish sentiment. This augurs for a reversal. On the other hand, other measures also suggest that the rally in the euro has more room to run. For example, copper prices and the euro have tended to move together, and the red metal suggests EUR/USD should be above 1.20 (Chart 2). Similarly, EUR/JPY has lagged the stellar performance of global equity prices. Is the lagging performance of EUR/USD sending the right signal, suggesting caution? Or is the common-currency a coiled spring ready to head much higher in 2021? How To Forecast The Euro According to Bloomberg forecasts, the euro will be at 1.25 by the end of 2022 (Chart 3). By our reckoning, these forecasts are much too pessimistic. The key driver of the EUR/USD exchange rate is the relative growth profile between the euro area and the US, how that profile is likely to evolve in the future, and the implication for relative monetary policies. Anything else that tries to predict the euro is a subset of this much bigger question. How is growth in the euro area likely to evolve compared to the US? There are many ways to approach this issue, with surprisingly similar results. The key driver of the EUR/USD exchange rate is the relative growth profile between the euro area and the US. The first is just to take the IMF growth estimates at face value. According to the Fund, the euro area economy is projected to contract by 8.3% this year, almost double that of the US, which is 4.3%. But by next year, the economy is expected to bounce back more fervently. Euro area growth is expected to advance by 5.2% compared to 3.1% in the US. Much of the rise will be due to a surge in investment within the euro area, especially driven by pent-up demand in the peripheral countries. This growth acceleration is projected to continue well into 2023. Back-of-the envelope calculations suggest that this will pin EUR/USD around 1.35 (Chart 4) Chart 3Few Expect The Euro Above 1.25

Few Expect The Euro Above 1.25

Few Expect The Euro Above 1.25

Chart 4EUR/USD And Relative Growth

EUR/USD And Relative Growth

EUR/USD And Relative Growth

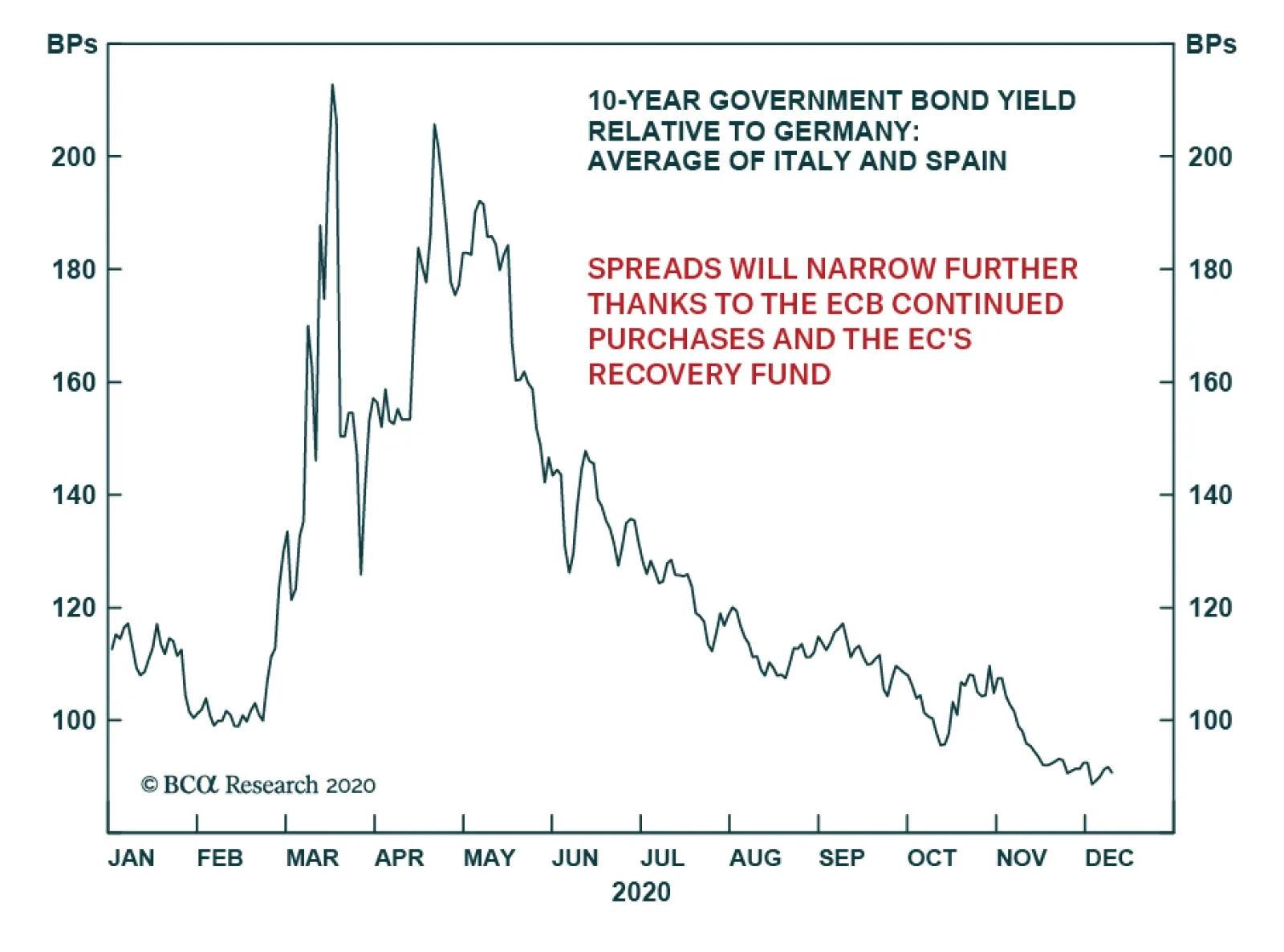

The Case For European Growth We tend to side with the IMF’s forecasts and even argue that this might actually be on the conservative side for the euro area. There are two major reasons for this, both of which are bilaterally important. First, the neutral rate of interest in the euro area may have moved a step function higher relative to the US. The standard dilemma for the euro zone is that interest rates have always been too low for the most productive nation, Germany, but too expensive for others, such as Spain and Italy. The silver lining is that the European Central Bank (ECB) has now lowered domestic interest rates and eased policy to the point where they are accommodative for all euro zone countries.1 Bond yields in peripheral Europe are collapsing relative to those in Germany and France (Chart 5). This makes it much easier for the less-productive, peripheral countries to borrow and invest. This will boost productivity, lifting the neutral rate. Chart 5The Neutral Rate In The Euro Area

The Neutral Rate In The Euro Area

The Neutral Rate In The Euro Area

Second and equally important, the periphery has become as competitive as the core. Through labor market reforms, internal devaluation, and recurring recessions throughout the last decade, unit labor costs in Greece, Ireland, Portugal, and Spain have converged with that in Germany and France. This has effectively eliminated the competitiveness gap that had accumulated over the past two decades (Chart 6). Even Italy, which remained saddled with a rigid and less productive workforce, has seen unit labor costs begin to crest. Chart 6Southern Europe Is Competitive Again

Southern Europe Is Competitive Again

Southern Europe Is Competitive Again

According to the Holston-Laubach-Williams estimates at the NY Fed, the natural rate of interest in the euro area is now higher than in the US, something that has rarely occurred over the 20-year history of the common currency. Based on these estimates, the euro could gravitate towards 1.50 (Chart 7). Chart 7EUR/USD And The Neutral Rate

EUR/USD And The Neutral Rate

EUR/USD And The Neutral Rate

US Versus Europe Chart 8Productivity In Europe Has Lagged

Productivity In Europe Has Lagged

Productivity In Europe Has Lagged

In today’s world, 1.50 for the euro is certainly very high and will surely stir up some action from the ECB well before we approach these levels. As most of my colleagues would argue, no central bank wants a strong currency.2 But how can we gauge the above premise that the neutral rate of interest should be higher in the euro area due to the tectonic shifts over the last few years? One way is to look at trend productivity growth. Since the 1960s, up until the Great Financial Crisis, trend productivity growth was around 2.2% in the US and 2.8% in the euro area. However, since 2009, productivity growth has been 0.6% per year in the euro area and 1.1% in the US (Chart 8). In other words, the European debt crisis has substantially subdued productivity growth in the euro area. If indeed the crisis is behind us, and we assume European productivity growth returns back to trend over the next 10 years, while making up for the shortfall relative to the US, this will pin it at roughly 1.6% higher in Europe relative to the US. Cumulatively, that is a rise of around 20%. Meanwhile, we highlighted last week that the euro was undervalued by over 10%.3 This pins the euro above 1.50. The Euro At Parity And Inflation Chart 9US Versus Euro Area Inflation

US Versus Euro Area Inflation

US Versus Euro Area Inflation

While the euro might gravitate higher in the next few years, it is unlikely to do so in a straight line. Meanwhile, deflation is a key near-term threat for the euro (Chart 9). With the ECB clearly telegraphing that it will do more easing in December, the relative monetary policy stance is not favorable. That said, there are three key points to consider about inflation. First, most G10 central banks were unable to meet their inflation mandate when output gaps were closing and the economy was at full employment. This makes it less likely they will meet their mandate anytime soon. This is not just an ECB problem, but one for the Fed, BoJ, and even the RBA. Second, inflation tends to be a global phenomenon in the developed world, meaning desynchronized cycles in inflation dynamics are quite rare. Finally, with balance sheets expanding everywhere in the G10, the potential for higher inflation once output gaps close will be universal. European productivity growth will have to outpace that in the US by roughly 1.6%, to play catch up. Going forward, an agreement on the mutualization of European debt means we can begin to expect more synchronized business cycles as fiscal stabilizers kick in. The reason is that both fiscal and monetary policy can now be synchronized across member states. This makes shortfalls in inflation less likely. Finally, while deflation can be a sign of an expensive currency, there is little evidence that this is the case for the euro. The euro area continues to sport very healthy trade and current account surpluses, a sign that the euro remains very competitive among its trading partners. Intra-European trade represents a large share of cross-border transactions in Europe, meaning currency considerations are less important. In 2019, most member states had a share of intra-EU exports of between 50% and 75%. The bottom line is that disappointing inflation dynamics could lead to a knee-jerk selloff in the euro, but this should be an opportunity to accumulate long positions. The Cyclical Catalyst Ultimately, European growth is cyclically tied to export growth. And with a huge concentration of cyclical sectors, such as financials, industrials, materials and energy, in European bourses, the euro tends to be largely driven by pro-cyclical flows. Earnings revisions between the euro area and the US have generally led the EUR/USD exchange rate by about 9-12 months (Chart 10). Chart 10EUR/USD Tracks Relative Profits

EUR/USD Tracks Relative Profits

EUR/USD Tracks Relative Profits

So far, the signs are positive. The impulse from Chinese credit is providing a release valve for European exports (Chart 11). So even if social distancing remains in place for longer than people expect, it still allows economies that are geared more towards manufacturing such as Europe, Japan, and China to keep churning higher. This could boost European earnings in a meaningful way. Chart 11Chinese Demand For European Goods

Chinese Demand For European Goods

Chinese Demand For European Goods

Fortunately for investors, European equities, especially those in the periphery, remain unloved, given that they are trading at some of the cheapest cyclically adjusted price-to-earnings multiples in the developed world (Chart 12A). Over the next decade, it would be surprising if some of these “old economy” stocks did not unwind their discount via both rising earnings and multiples. Many emerging markets, including China, still depend on “old-economy” materials such as oil, and industrial machinery, that Europe sells. The impulse from Chinese credit is providing a release valve for European exports. Even in the commodity space, cyclical metals like copper are still massively underperforming safe havens like gold. This has largely tracked the discount between European stocks and US stocks. A bet on a reversal could prove very profitable (Chart 12B). Chart 12AEuro Stocks Are Cheap

Euro Stocks Are Cheap

Euro Stocks Are Cheap

Chart 12BEuro Stocks Could Rerate

Euro Stocks Could Rerate

Euro Stocks Could Rerate

Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Footnotes 1 Please see Foreign Exchange Strategy Weekly Report, "EUR/USD And The Neutral Rate Of Interest," dated June 14, 2019, available at fes.bcaresearch.com 2 Please see Global Fixed Income Strategy Weekly Report, "Nobody Wants A Strong Currency," dated November 17, 2020, gfis.bcaresearch.com 3 Please see Foreign Exchange Strategy Weekly Report, "Updating Our PPP Models," dated November 13, 2020. fes.bcaresearch.com Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Limit Orders Closed Trades