Euro Area

Dear clients, This week we are sending you a Research Note on balance of payments across the G10, authored by my colleague Kelly Zhong. With unprecedented monetary and fiscal stimulus, balance-of-payment dynamics will become an even more important driver of currencies over the next few years. That said, while the US current account is in deficit, the short dollar narrative is beginning to capture investor imagination, suggesting the call is rapidly becoming consensus. We are in the consensus camp, but are going short GBP today, as a bet on a short-term reversal. As for cable, the recent rally has gotten ahead of potential volatility in the coming months, even though it is cheap. Finally, we are lowering our target on the short gold/silver trade to 65, but tightening the stop-loss to 75. I hope you find the report insightful. Chester Ntonifor, Vice President Foreign Exchange Strategy Highlights COVID-19 has turned the world upside down this year, and severely impaired global trade. Global trade values plunged by 5% quarter-on-quarter in the first quarter, and are forecasted to have slumped by 27% in the second quarter. Most countries have also seen negative foreign direct investment (FDI) growth in the first few months of 2020. Global FDI inflows are forecasted to fall by 40% this year and drop by an additional 5-10% next. While all countries have been hit by COVID-19, the economic damage appears particularly pronounced in countries heavily reliant on foreign funding. Feature COVID-19 has turned the world upside down in 2020. The global economy headed into recession following a decade-long expansion. While many economies are starting to ease restriction measures, the possibility of a second wave remains a big downside risk to the global economy. If history is any guide, the Spanish flu during the early 1900s came in three waves, the second of which brought the most severe damage. Undoubtedly, international trade has been under severe pressure this year. Global trade volumes plunged by 5% in the first quarter, and are expected to be down 27% in the second quarter from their levels in the final three months of 2019. Moreover, the path of recovery remains uncertain as the pandemic continues to disrupt global supply chains and weaken consumer confidence. According to the United Nations Conference on Trade and Development (UNCTAD), it may take until late 2021/early 2022 for global trade to recover to pre-pandemic levels (Chart 1). As reinvested earnings make up more than half of total FDI, squeezed earnings this year will have a direct impact on FDI in the aftermath of COVID-19. Global FDI inflows rebounded in 2019, reaching a total of $1.5 trillion, as the effect of the 2017 US tax reforms waned and US repatriation declined. This year, however, most countries have seen negative FDI growth rates in the first few months in 2020. According to UNCTAD, global FDI inflows are forecast to plunge by 40%, bringing total FDI inflows below the US$1 trillion level for the first time since 2005 (Chart 2). Unfortunately, as reinvested earnings make up more than half of total FDI, squeezed earnings this year will have a direct impact on FDI in the aftermath of COVID-19. Typically, FDI flows bottom only six to 18 months after the end of a recession. FDI inflows are forecast to decline further by another 5-10% in 2021. Chart 1Steep Decline In Trade Volumes In 1H'20

Steep Decline In Trade Volumes In 1H'20

Steep Decline In Trade Volumes In 1H'20

Chart 2Global FDI Projected To Fall Through 2021

Global FDI Projected To Fall Through 2021

Global FDI Projected To Fall Through 2021

While all economies have been hit by COVID-19, the impact varies by region. Emerging market countries, particularly those linked to commodities and manufacturing-intensive industries, appear to be have been hit harder by the crisis. This makes sense, given trade is much more volatile than services or consumption. Chart 3 shows that while exports make up less than 30% of GDP in the US, they amount to over 130% of GDP in Thailand and Malaysia, and over 300% of GDP in Singapore and Hong Kong. Chart 3Reliance On Trade Differ Across Countries

Balance Of Payments Beyond COVID-19

Balance Of Payments Beyond COVID-19

Going forward, the recoveries might be uneven as well. Prior to COVID-19, global trade flows were already facing many challenges, including trade disputes, geopolitical tensions and rising protectionism. COVID-19 may have just supercharged two megatrends: Technology and Innovation: The pool of investments concentrated on exploiting raw materials and cheap labor is shrinking, while those promoting technology and ESG are becoming crucial. De-globalization: Policymakers in many countries are promoting more regulation and intervention, especially in key industries related to national security and health care. This suggests COVID-19 might represent a tipping point, making balance of payments all the more important for currencies, as investors become more discerning between countries and sectors with a high return on capital and those without. The euro area, Switzerland, Australia and Sweden sport the best basic balance surpluses. In this report, we look at the balance-of-payment dynamics in the G10. The most important measure for us is the basic balance, which takes the sum of the current account and net long-term capital inflows. Our rationale is that these tend to measure the underlying competitiveness of a currency more accurately than other balance of payment measures. On this basis, the euro area, Switzerland, Australia and Sweden sport the best basic balance surpluses. The US is the worst (Chart 4). Below, we visit some of key drivers behind these trends. Chart 4Basic Balances Across G10

Balance Of Payments Beyond COVID-19

Balance Of Payments Beyond COVID-19

United States Chart 5US Balance Of Payments

US Balance Of Payments

US Balance Of Payments

The US basic balance is deteriorating again (Chart 5). The key driver has been a decline in foreign direct investment. If this trend continues, this could further undermine the US currency. The US remains the world’s largest FDI recipient, attracting US$261 billion in 2019, which is almost double the size of FDI inflows into the second largest FDI recipient – China – with US$141 billion of inflows last year. However, cross-border flows have since fallen off a cliff after the waning effect of the one-time tax dividend introduced at the end of 2017. The lack of mega-M&A deals has also been a contributing factor. The trends in the trade balance have been flat, despite a push by the Trump Administration to reduce the US trade deficit and rejuvenate the US economy. The most recent second-quarter data show a deterioration from -2.3% of GDP to -2.8%. The trade deficit with China did drop by 21% to $345 billion in 2019, however, US companies quickly found alternatives from countries that are not affected by newly imposed tariffs, particularly from Southeast Asia: The US trade deficit with Vietnam jumped by 30%, or $16.3 billion, in 2019. More recently, exports have plunged much faster than imports, further widening the US trade deficit. On portfolio flows, the most recent TIC data show that US Treasurys continued to be shunned by foreigners in May. In short, the US balance-of-payment dynamics are consistent with our bearish dollar view. Euro Area Chart 6Euro Area Balance Of Payments

Euro Area Balance Of Payments

Euro Area Balance Of Payments

A rising basic balance surplus has been one of the key pillars underpinning a bullish euro thesis. Of course, an apex in globalization will hurt this thesis, but the starting point for the euro area is much better than many of its trading partners. The trade surplus in the euro area was not spared from COVID-19 – it plunged to €9.4 billion in May from €20.7 billion the same month last year, as the pandemic hit global demand and disrupted supply chains. Exports tumbled by 29.5% year-on-year to €143.3 billion while imports declined by 26.7% to €133.9 billion. Even in this dire scenario, the trade surplus still remains a “healthy” 1.8% of GDP, buffeting the current account (Chart 6). Foreign direct investment inflows have regained some ground in recent years, with the improvement accelerating in recent months. FDI inflows surged by 18% in 2019, reaching US$429 billion. Outflows also rose by 13% in 2019, led by a large increase in investment by multinationals based in the Netherlands and Germany. Going forward, FDI is sure to drop, but this will not be a European-centric problem. Portfolio flows have started to reverse, but have not been the key driver of the basic balance. This is because ever since the European Central Bank introduced negative interest rates in 2014, portfolio outflows have been persisted. This also makes sense since Europeans need to recycle their excess savings abroad. In sum, despite the headwinds to global trade and investment, the basic balance remains at a healthy 2.9% of GDP, which bodes well for the euro. Japan Chart 7Japan Balance Of Payments

Japan Balance Of Payments

Japan Balance Of Payments

A key pillar for the basic balance in Japan has been the current account balance, which has been buffeted over the years by income receipts from Japan’s large investment positions abroad. Going forward, this could make the yen very attractive in a world less reliant on global trade. Japanese exports tumbled by 26.2% year-on-year in June, led by lower sales in transport equipment, motor vehicles and manufactured goods. However, the slowing export trend was well in place before the pandemic. Exports had been declining for 18 consecutive months before COVID-19 dealt the final blow. Imports also fell by 14% year-on-year in June, led by lower energy prices. On the service side of the income equation, foreign visitors to Japan dropped by 99.9% from over 2.5 million in January to less than 2,000 in May. That equates to about 2% of the Japanese population. Despite all this, Japan still sports a healthy current account surplus, at 4% of GDP (Chart 7). In 2019, Japan remained the largest investor in the world, heavily recycling its current account surplus. FDI outflows from Japanese multinationals surged by 58% to a record US$227 billion, including US$104 billion in cross-border M&A deals. Notable mentions include Takeda acquiring Shire (Ireland) for US$60 billion, and SoftBank Group acquiring a stake in WeWork (the US) for US$6 billion. In terms of portfolio investments, foreign bond purchases have eased of late as global interest rates approach zero. Higher real rates are now being found in safe-haven currencies like the Swiss franc and the Japanese yen, which is supportive for the yen. Overall, the basic balance in Japan is at nil, in perfect balance between domestic savings and external investments. United Kingdom Chart 8UK Balance Of Payments

UK Balance Of Payments

UK Balance Of Payments

The key development in the UK’s balance-of-payment dynamics is that a cheap pound combined with the pandemic appear to have stemmed the decline in the trade balance. The UK has run a current account deficit each year since 1983. This has kept the basic balance mostly negative (Chart 8). That could change if the marginal improvement in trade is durable and meaningful. The current account deficit further widened to £21.1 billion, or 3.8% of GDP, in the first quarter, of which the goods trade balance was more volatile than usual. Since May, the goods trade balance has been slowly recovering to £2.8 billion, but has been offset by the services trade deficit. The primary income deficit also widened in the first quarter as offshore businesses rushed to preserve cash buffers. Foreign direct investment in the UK has been improving of late, currently sitting at 3.7% of GDP. This is encouraging, given the steep post-Brexit drop. Going forward, we continue to favor the British pound over the long term due to its cheap valuation. However, we are going short today, as a play on a tactical dollar bounce. More on this next week. Canada Chart 9Canada Balance Of Payments

Canada Balance Of Payments

Canada Balance Of Payments

The Canadian basic balance has been flat for over a decade, as the persistent current account deficit has continuously been financed by FDI inflows and portfolio investment (Chart 9). This is a vote of confidence by investors over longer-term returns on Canadian assets. Canada is one of the largest exporters of crude oil, meaning the fall in resource prices generated a big dent in export incomes. However, the country is slowly on a recovery path. Exports increased 6.7% month-on-month in May, helping narrow the trade deficit to C$0.7 billion. More importantly, a positive net international investment position means that positive income flows into Canada are buffeting the current account balance. In 2019, Canada was the 10th largest FDI recipient in the world, with FDI inflows increasing to US$50 billion. Today, the basic balance stands at a surplus of 1% of GDP. Australia Chart 10Australia Balance Of Payments

Australia Balance Of Payments

Australia Balance Of Payments

Australia’s trade balance has been rapidly improving since the 2016 bottom, and has been the primary driver of an improving basic balance. While exports fell as the pandemic hit a nadir, imports fell more deeply. This allowed the trade surplus to widen in the first six months of the year compared to last year. Australia has long had a current account deficit, as import requirements to help drive investment opportunities were not met by domestic savings. With those projects now bearing fruit, the funding requirement has greatly eased. This has buffeted the current account balance, which turned positive for the first time last year following a 35-year-long deficit, and continues to rocket higher (Chart 10). Going forward, Australia’s trade balance and current account balance are likely to continue increasing as Australia has a comparative advantage in exports of resources, especially LNG, which is consistent with the ESG megatrend. Australia is also introducing major reforms to its foreign investment framework to protect national interests and local assets from acquisitions. Meanwhile, net portfolio investment remains negative, suggesting the current account surplus is being recycled abroad. In short, we believe the Aussie dollar has a large amount of running room, based on its healthy basic balance surplus of 4% of GDP. New Zealand Chart 11New Zealand Balance Of Payments

New Zealand Balance Of Payments

New Zealand Balance Of Payments

Compared to its antipodean neighbour, the New Zealand basic balance has been flat for many years, but has seen recent improvement (Chart 11). The trade balance was boosted by goods exports, which were up NZ$261 million, while imports were down NZ$352 million in the first quarter of this year. The rise in goods exports was led by an increase in fruit (mainly kiwifruit), milk, powder, butter and cheese. More recently, due to the ease of lockdown measures, exports increased by 2.2% year-on-year in June while imports marginally rose by 0.2%, further enhancing New Zealand’s trade balance. The primary income deficit widened to NZ$2.2 billion in the first quarter due to less earnings on foreign investment. Moreover, the secondary income deficit also widened, driven by a smaller inflow of non-resident withholding tax. Despite this, the current account deficit narrowed to NZ$1.6 billion in the first quarter, or 2% of GDP, the smallest deficit since 2016. New Zealand received $5.4 billion in FDI flows in 2019, rising from only $2 billion in 2018. Most FDI inflows arrived from Canada, Australia, Hong Kong and Japan. Impressively, according to the World Bank’s 2020 Doing Business Report, New Zealand ranked first out of 190 countries due to its openness and business-friendly economy, low levels of corruption, good protection of property rights, political stability and favorable tax policies. Portfolio investment inflows also increased by NZ$11.8 billion. The improvement in the backdrop of New Zealand’s basic balance will allow it to outperform the US dollar. As a tactical trade, however, we are short the kiwi versus the CAD. The basis is that relative terms of trade favor the CAD for now. Switzerland Chart 12Switzerland Balance Of Payments

Switzerland Balance Of Payments

Switzerland Balance Of Payments

Switzerland’s basic balance is almost always in surplus, driven by a structural uptrend in the trade balance (Chart 12). This has allowed the trade-weighted Swiss franc to outperform on a structural basis. We expect this trend to continue. As a country consistently running high surpluses, Switzerland also tends to invest more in foreign assets. Over the years, these smart investments have helped buffet the current account. Overall, in the first three months of this year, the current account balance stood at CHF 17.4 billion, or 11.2% of GDP. In terms of the net international investment position, both stocks of assets and liabilities fell by CHF 110 billion and CHF 42 billion, respectively in the first quarter, due to falling equity prices globally. The net international investment position fell by CHF 67 billion to CHF 745 billion in the January-March period. That said, Switzerland continued to deploy capital abroad in the first quarter, which should help buffet the current account going forward. The positive balance-of-payment backdrop has created a headache for the Swiss National Bank. As such, the SNB will likely continue to intervene in the foreign exchange markets to calm appreciation in the franc. We believe the franc will continue to outperform the USD in the near term, but underperform the euro. Norway Chart 13Norway Balance Of Payments

Norway Balance Of Payments

Norway Balance Of Payments

Norway has a very open economy, with trade representing over 70% of GDP, and it has been hit quite hard by COVID-19 this year. The trade surplus started to plunge sharply due to falling energy prices at the beginning of the lockdown (Chart 13). More recently, Norway posted its first trade deficit in May since last September, which carried over to June, as exports fell more than imports. Thanks to increases in income receipts from abroad, the current account balance remained flat at NOK 66.1 billion in the first quarter. With persistent current account surpluses, Norway has long been a capital exporter. However, the FDI outflow and inflow gap is gradually closing. In 2019, net FDI was -3.5% of GDP. In the first quarter of this year, it was -3.3%. Portfolio outflows have also softened over the years, as the current account balance has narrowed. There was, however, a trend change in the first three months of this year - Norway’s purchases of foreign bonds, surged as investors switched to safer assets. Ultimately, we remain NOK bulls due to its cheap valuation. As economies gradually reopen and ease lockdown measures, the recovery in energy prices will push the Norwegian krone back toward its fair value. Sweden Chart 14Sweden Balance Of Payments

Sweden Balance Of Payments

Sweden Balance Of Payments

Sweden maintained its trade surplus with the rest of the world throughout the first few months of 2020 (Chart 14). Imports fell more than exports amid the pandemic. The goods trade balance almost doubled from the fourth quarter of 2019 to SEK 68.8 billion in the first quarter of 2020. The primary income surplus also increased by SEK 10 billion to SEK 42.2, further strengthening the current account and bringing the total current account surplus to SEK 80.6 billion, or 4% of GDP. Both FDI inflows and outflows have been increasing in Sweden, but the net number was slightly negative. In the first quarter of 2020, FDI inflows rose by SEK 51.6 billion while FDI outflows increased by SEK 100.6 billion. In terms of portfolio investment, Swedish investors reduced their portfolio investment abroad by SEK 141 billion in the first quarter, while foreigners decreased their portfolio investment in Sweden by SEK 45.8 billion. In conclusion, the Swedish krona remains one of our favorite longs due to its increasing basic balance surplus (4% of GDP) and its cheap valuation. We are long the Nordic basket (NOK and SEK) against both the euro and the US dollar. Kelly Zhong Research Analyst kellyz@bcaresearch.com Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Footnotes Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Limit Orders Closed Trades

Please note that we will be on our summer holidays next week. Our next report will come out on August 20. Highlights The 30-year bond yield is the puppet master pulling the strings of all other investments. Where 30-year bond yields are still far from the lower bound, they will ultimately get a lot closer. Continue to overweight 30-year bonds in the US and periphery Europe versus 30-year bonds in core Europe. Continue to overweight the US stock market versus the European stock market. An expected near-term setback to stocks versus bonds will briefly pause the European currency rally. The gold rally is also due a pause, given that it is overstretched relative to the decline in the real bond yield. Fractal trade: Long USD/PLN. Feature Chart I-1AThe Collapsed 30-Year Bond Yield Explains The Collapse Of Banks...

The Collapsed 30-Year Bond Yield Explains The Collapse Of Banks...

The Collapsed 30-Year Bond Yield Explains The Collapse Of Banks...

Chart I-1B...And The Collapsed Earnings Yield (Surging Valuation) Of Tech And Healthcare

...And The Collapsed Earnings Yield (Surging Valuation) Of Tech And Healthcare

...And The Collapsed Earnings Yield (Surging Valuation) Of Tech And Healthcare

The abiding mantra of this publication is that investment is complex, but it is not complicated. By complex, we mean that the financial markets are not fully predictable or analysable. By not complicated, we mean that the relative prices of everything are inextricably connected, rather like the movements of a puppet. All you need to do is find the puppet master pulling the strings. Right now, the puppet master is the 30-year bond. The Real Action Is In 30-Year Bonds While most people are focussing on the 10-year bond yield, the real action has been at the ultra-long 30-year maturity. In the US and periphery Europe, 30-year yields are within a whisker of all-time lows. Yet these ultra-long bond yields are still well above those in core Europe which are much closer to the lower bound. The upshot is that while all yields have equal scope to rise, yields have more scope to fall further in the US and periphery Europe than in core Europe (Chart I-2 and Chart I-3). Chart I-230-Year Yields In The US And Periphery Europe...

30-Year Yields In The US And Periphery Europe...

30-Year Yields In The US And Periphery Europe...

Chart I-3...Are Still Well Above Those In ##br##Core Europe

...Are Still Well Above Those In Core Europe

...Are Still Well Above Those In Core Europe

This simple asymmetry has created a winning relative value strategy that will keep on winning. Overweight 30-year bonds in the US and periphery Europe versus 30-year bonds in core Europe. Our preferred expression is to overweight 30-year bonds in the US and Spain versus Germany and France. Bond yields have more scope to fall further in the US and periphery Europe than in core Europe. Remarkably, in the US, the 10-year real yield is also tightly tracking the 30-year nominal yield (minus a constant 2.2 percent) (Chart I-4). Using a little algebra, this means that the market’s 10-year inflation expectation is just a steady-state value of 2.2 percent minus a shortfall equalling the shortfall in the 10-year nominal yield versus the 30-year nominal yield (Chart I-5). Chart I-4The 10-Year Real Yield Is Just ##br##Tracking The 30-Year Nominal ##br##Yield

The 10-Year Real Yield Is Just Tracking The 30-Year Nominal Yield

The 10-Year Real Yield Is Just Tracking The 30-Year Nominal Yield

Chart I-5The 10-Year Inflation Expectation Can Be Derived From The 30-Year And 10-Year Nominal Yields

The 10-Year Inflation Expectation Can Be Derived From The 30-Year And 10-Year Nominal Yields

The 10-Year Inflation Expectation Can Be Derived From The 30-Year And 10-Year Nominal Yields

10-year inflation expectation = 2.2 – (30-year nominal yield – 10-year nominal yield) The reason that this is remarkable is we can explain the trend in inflation expectations from just the 30-year and 10-year nominal yields, and nothing more. In turn, gold is tightly tracking the inverted real yield, as it theoretically should. Gold, which generates no yield, becomes relatively more valuable as the real yield on other assets diminishes (Chart I-6). Having said that, the most recent surge in the gold price is stretched relative to its relationship with the real bond yield, suggesting that the strong rally in gold is due a pause (Chart I-7). Chart I-6Gold Is Just Tracking The (Inverted) Real Yield...

Gold Is Just Tracking The (Inverted) Real Yield...

Gold Is Just Tracking The (Inverted) Real Yield...

Chart I-7...But Gold's Most Recent Surge Is ##br##Stretched

...But Gold's Most Recent Surge Is Stretched

...But Gold's Most Recent Surge Is Stretched

The 30-Year Bond Is Driving Stock Markets Moving to the stock market, bank relative performance has closely tracked the collapse in the 30-year yield, because the collapsed bond yield signals both weaker bank credit growth and a likely increase in banks’ non-performing loans (Chart of the Week, left panel). Banks and other ‘value cyclicals’ whose cashflows are in terminal decline are highly sensitive to the prospects for near-term cashflows, which are under severe pressure in the pandemic era. At the same time, as the distant cashflows are small, the banks’ share prices are less sensitive to the uplifted net present values of these distant cashflows that come from lower bond yields. In contrast, technology, healthcare and other ‘growth defensives’ generate a growing stream of cashflows. Making their net present values highly sensitive to a change in the bond yield used to discount those large distant cashflows. The profits of the tech and healthcare sectors are proving to be highly resilient in the pandemic era. Through 2018, the 30-year yield went up by 1 percent, so the forward earnings yield of growth defensives went up by 1 percent (their valuations fell). Subsequently, the 30-year yield has collapsed by 2 percent, so unsurprisingly the forward earnings yield of growth defensives has also collapsed by 2 percent (their valuations have surged). To repeat, financial markets are not complicated (Chart of the Week, right panel). Moreover, the profits of the growth defensives are proving to be highly resilient in the pandemic era, holding up well in the worst shock to demand since the Great Depression. The combination of resilient profits with higher valuations explains why the technology and healthcare sectors are reaching new highs, while the rest of the stock market is going nowhere (Chart I-8). Chart I-8Tech And Healthcare At New Highs While The Rest Of The Market Languishes

Tech And Healthcare At New Highs While The Rest Of The Market Languishes

Tech And Healthcare At New Highs While The Rest Of The Market Languishes

Meanwhile, the relative performance of stock markets is also uncomplicated. It just stems from the relative exposure to the high-flying growth defensive sectors. Compared with Europe, the US has a 20 percent larger exposure to technology and healthcare (Chart I-9). Which is all you need to explain the consistent outperformance of the US versus Europe (Chart I-10). Chart I-9The US Is 20 Percent Over-Exposed To Tech And Healthcare...

The US Is 20 Percent Over-Exposed To Tech And Healthcare...

The US Is 20 Percent Over-Exposed To Tech And Healthcare...

Chart I-10...Which Explains Its Consistent Outperformance Versus Europe

...Which Explains Its Consistent Outperformance Versus Europe

...Which Explains Its Consistent Outperformance Versus Europe

A Quick Comment On European Currencies And The Dollar Turning to the foreign exchange market, the recent rally in European currencies can at least partly be explained as a sell-off in the dollar. Begging the question, what is behind the dollar’s recent weakness? The dollar has moved as a mirror-image of the global stock market. For the broad dollar index, the explanation is quite straightforward. True to its traditional role as a haven currency, the dollar has moved as a mirror-image of the global stock market, measured by the MSCI All Country World Index (in local currencies). Simply put, as the stock market has shaken off its year-to-date losses, the dollar has shaken off its year-to-date gains (Chart I-11). Chart I-11The Dollar Has Just Tracked The (Inverted) Stock Market

The Dollar Has Just Tracked The (Inverted) Stock Market

The Dollar Has Just Tracked The (Inverted) Stock Market

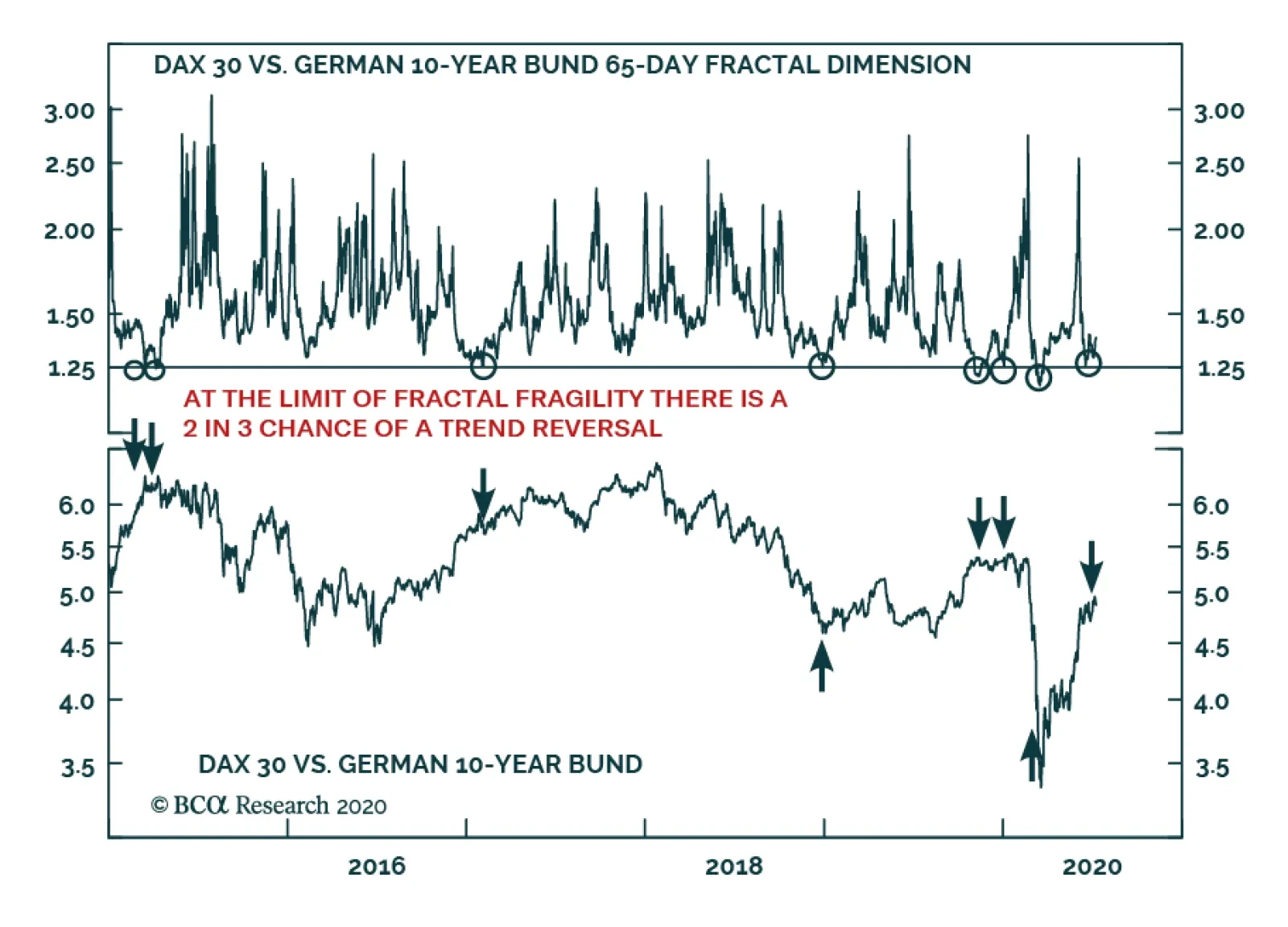

Looking ahead, we can link the prospects of currencies to the outlook for 30-year bond yields. A further compression in yields will weaken the dollar, and help European currencies, in two ways. First, as already mentioned, yields have more scope to decline in the US than in core Europe, and a fading US yield premium will weigh on the dollar. Second, to the extent that the lower yields can prevent a protracted bear market in stocks and other risk-assets, non-haven currencies can perform well versus the haven dollar. Having said that, an expected near-term setback to stocks versus bonds will briefly pause the European currency rally. Concluding Remarks The charts in this report should leave you in no doubt that the 30-year bond yield – particularly in the US – is the puppet master pulling the strings of all investments: bond market relative performance, real bond yields, gold, banks, growth defensives, equity market relative performance, and major currencies. Which raises the crucial question, can the downtrend in 30-year bond yields continue? Yes, absent an imminent vaccine or treatment for Covid-19, the downtrend in yields can continue. As we explained last week in An Economy Without Mouths And Noses Will Lose 10 Percent Of Jobs, the spectre of mass unemployment is looming large. Specifically, the major threat to the jobs market lies in the coming months when government lifelines to employers – such as state-subsidised furlough schemes – are cut or weakened. Where 30-year bond yields are still far from the lower bound, they will ultimately get a lot closer. Hence, it is inevitable that those central banks that can become more dovish will become more dovish. Given the political difficulties of using fiscal policy bullets, the lessons from Japan and Europe are that the monetary policy bullets get fully expended first. In practical terms, this means that where 30-year bond yields are still far from the lower bound, they will ultimately get a lot closer. The upshot is that core European bonds will continue to underperform US bonds, and that the European stock market will continue to underperform the US stock market. European currencies will trend higher versus the dollar, albeit a setback to stocks versus bonds is a near-term risk to the European currency uptrend. Fractal Trading System* This week’s recommended trade is to play a potential countertrend move in the dollar via long USD/PLN. The profit target and symmetrical stop-loss is set at 4 percent. The rolling 1-year win ratio now stands at 57 percent. Chart I-12USD/PLN

USD/PLN

USD/PLN

When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com. Dhaval Joshi Chief European Investment Strategist dhaval@bcaresearch.com Fractal Trading System Cyclical Recommendations Structural Recommendations Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights Global Bond Yields: The growing divide between falling negative real bond yields and rising inflation expectations in the US and other major developed economies may be a sign of investors pricing in slower long-run potential economic growth in the aftermath of the COVID-19 recession – and, thus, lower equilibrium real interest rates. Stay overweight inflation-linked bonds versus nominal equivalents. Currency-hedged spread product: A broad ranking of currency-hedged global spread product yields, adjusted for volatility and credit quality, shows that the most attractive yields (hedged into USD, EUR, GBP and JPY) are on offer in emerging market USD-denominated investment grade corporates and high-yield company debt in the US and UK. Feature Global bond yields are testing the downside of the narrow trading ranges that have persisted since May. As of last Friday, the yield on the Bloomberg Barclays Global Treasury index was at 0.41%, only 3 basis points (bps) above the 2020 low seen back in March. The 10-year US Treasury yield closed yesterday at 0.56%, only 6bps above the year-to-date low. Chart of the Week

A Massive Shock To Growth ... And Interest Rates

A Massive Shock To Growth ... And Interest Rates

Concerns about global growth, with the number of new COVID-19 cases still surging in the US and new breakouts occurring in countries like Spain and Australia, would seem to be the logical culprit for the decline in yields. The first reads on global GDP data for the 2nd quarter released last week were historically miserable, with declines of -33% (annualized) in the US and -10% in the euro area (non-annualized). That represents a very deep hole of lost output, literally wiping out several years of growth. Even with the sharp improvements seen recently in cyclical indicators like global manufacturing PMIs, especially in China and Europe, a return to pre-pandemic levels of global economic output is many years away. Central banks will have no choice but to keep policy rates near 0% for at last the next couple of years, as is the current forward guidance provided by the Fed, ECB and others. Lower global bond yields may simply be reflecting the reality that it will take a long time to heal the economic wounds from the pandemic. However, there may be a more insidious reason why bond yields are falling. Investors may be permanently marking down their expectations for long-term potential economic growth, and equilibrium interest rates, in response to the devastation caused by the COVID-19 recession. Last week, Fitch Ratings lowered its estimates for long-term potential GDP growth, used to determine sovereign credit ratings, by 0.5 percentage points for the US (now 1.4%), 0.5 percentage points for the euro area (now 0.7%) and 0.7 percentage points in the UK (now 0.7%).1 These are declines similar in magnitude to the plunge in the OECD’s potential growth rate estimates seen after the 2009 Great Recession (Chart of the Week). Bond yields in the US and Europe witnessed a fundamental repricing in response, with nominal 5-year yields, 5-years forward breaking 200bps below the 4-6% range that prevailed in the US and Europe during the decade prior to the Great Recession. A similar re-rating of global bond yields to structurally lower levels may now be happening, with investors now believing that central banks will have difficulty raising rates much (if at all) in the future - even after the pandemic has ended. The Message From Declining Negative Real Bond Yields Chart 2The Real Rate/Breakevens Divergence Continues

The Real Rate/Breakevens Divergence Continues

The Real Rate/Breakevens Divergence Continues

The typical signals about economic growth from government bond yields are now less clear because of the aggressive policy responses to the COVID-19 crisis. 0% policy rates, dovish forward guidance on the timing of any future rate increases, large scale asset purchases (QE), and more extreme measures like yield curve control to peg bond yields, have all acted to suppress the level and volatility of nominal global bond yields. Within those calm nominal yields, however, the dynamic that has been in place since May - rising inflation breakevens and falling real bond yields – is growing in intensity. The 10-year US TIPS real yield is now at a new all-time low of -1.02%, while the 10-year TIPS breakeven is now up to 1.58%, the highest since February before the pandemic began to roil financial markets (Chart 2). Similar trends are evident in most other major developed economy bond markets, with the gap between falling real yields and widening breakevens growing at a notably faster pace in Canada and Australia. More often than not, longer-term real yields tend to move in the same direction as inflation expectations when economic growth is improving. The former responds to faster economic activity, often with an associated pick up in private sector credit demand. At the same time, rising inflation expectations discount higher economic resource utilization (i.e. lower unemployment) and confidence that inflation will start to pick up. A deeply negative correlation between longer-term real yields and inflation expectations is unusual, but not unprecedented. A deeply negative correlation between longer-term real yields and inflation expectations is unusual, but not unprecedented. In Chart 3, we show the range of rolling three-year correlations between 10-year inflation-linked (real) government bond yields and 10-year inflation breakevens in the US, Germany, France, Italy, the UK, Japan, Canada and Australia for the post-crisis period. The triangles in the chart are the latest three-year correlation, while the diamonds are a more recent measure showing the 13-week correlation. There are a few key takeaways from this chart: Chart 3Negative Real Yield/Breakevens Correlations Are Not Unprecedented

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

All countries shown have experienced a sustained period of negative correlation between real yields and inflation breakevens; The correlation has mostly been positive in Australia and has always been negative in Japan; Most importantly, the deeply negative correlations seen over the past three months – with rising breakevens all but fully offsetting falling real yields – are at or below the range of historical experience for all countries shown. Chart 4TIPS Yields May Stay Negative For Some Time

TIPS Yields May Stay Negative For Some Time

TIPS Yields May Stay Negative For Some Time

In the current virus-stricken world, where many businesses that have closed during the pandemic may never reopen, there will be abundant spare global economic capacity for several years. In the US, measures of spare capacity like the unemployment gap (the unemployment rate minus the full-employment NAIRU rate) have been a reliable leading directional indicator of the long-run correlation between real TIPS yields and TIPS breakevens over the past decade (Chart 4). The surge in US unemployment seen since the spring, which has pushed the jobless rate into double-digit territory, suggests that the current deeply negative correlation between US real yields and inflation breakevens can persist over the next 6-12 months. Given the large increases in unemployment seen in other countries, the negative correlations between real yields and inflation breakevens should also continue outside the US. As for inflation expectations, those remain correlated in the short-run to changes in oil prices and exchange rates in all countries. On that front, there is still some room for breakevens to widen to reach the fair value levels implied by our models.2 A good conceptual way to think about inflation breakevens on a more fundamental level, however, is as a “vote of confidence” in a central bank’s monetary policy stance. If investors perceive policy settings to be too tight, markets will price in slower growth and lower inflation expectations, and vice versa. Every developed market central bank is now setting policy rates near or below 0% - and promising to keep them there until at least the end of 2022. Thus, the trend of rising global inflation breakevens can continue as a reflection of very dovish central banks that will be more tolerant of increases in inflation and not tighten policy pre-emptively. Currently, real 10-year inflation-linked bond yields are below the New York Fed’s estimates of the neutral real short-term rate, or “r-star”, in the US and the UK (Chart 5), as well as in the euro area and Canada (Chart 6).3 In the US and euro area, real yields have followed the broad trend of r-star, but the gap between the two is relatively moderate with r-star estimated to be only 0.5% in the US and 0.2% in the euro zone (where the ECB is setting a negative nominal interest rate on European bank deposits at the central bank – a policy choice that the Fed has been very reluctant to consider). Chart 5Negative Real Bond Yields Are Below R* In The US & UK ...

Negative Real Bond Yields Are Below R* In The US & UK ...

Negative Real Bond Yields Are Below R* In The US & UK ...

Chart 6... As Well As In The Euro Area & Canada

... As Well As In The Euro Area & Canada

... As Well As In The Euro Area & Canada

A more interesting study is in the UK where 10yr inflation-linked Gilt yields have fallen below -2.5%, but without the Bank of England implementing any negative nominal policy rates. In the UK, inflation expectations have been relatively high – running in the 2.5-3% range prior to the COVID-19 recession – as the Bank of England has consistently kept overnight interest rates below actual CPI inflation since the 2008 financial crisis. Thus, nominal Gilt yields have stayed relatively low for longer, as real yields and inflation expectations have remained negatively correlated for a long period with the Bank of England maintaining a consistently negative real policy rate. Chart 7Spillovers From Negative TIPS Yields Into Other Assets

Spillovers From Negative TIPS Yields Into Other Assets

Spillovers From Negative TIPS Yields Into Other Assets

If the Fed were to do the same in the US, keeping the funds rate very low even as inflation rises, then a similar dynamic could take place where real TIPS yields continue to fall and TIPS breakevens continue to rise as the market prices in a sustained negative real fed funds rate. That may already be happening, with Fed Chair Jerome Powell hinting last week that the Fed is in the process of completing its inflation strategy review – with a shift towards rate hikes occurring only after realized inflation has sustainably increased to the Fed’s 2% target. A forecast of inflation heading to 2% because of falling unemployment will no longer be enough.4 Other factors may be at work depressing real bond yields while boosting inflation expectations, such as the massive QE bond buying programs of the Fed, ECB and other central banks. Yet even QE programs are essentially an aggressive form of forward guidance designed to drive down longer-term bond yields by lowering expectations of future interest rates. In sum, it is increasingly likely that the current phase of negative global real bond yields may become longer lasting if markets believe that equilibrium real policy rates are now negative. Bond investors will expect central banks to sit on their hands and do nothing in that environment, even if inflation starts to increase. This not only has implications for bond markets, but other asset classes as well based on what is happening in the US. The steady decline in the in the 10-year US TIPS yield has boosted the valuation of assets that typically have been considered inflation hedges, like equities and gold (Chart 7). The fall in TIPS yields also suggests that more weakness in the US dollar is likely to come over the next 6-12 months – another reflationary factor that should help lift global inflation expectations and boost the attractiveness of inflation-linked bonds. The current phase of negative global real bond yields may become longer lasting if markets believe that equilibrium real policy rates are now negative. Bottom Line: The growing divide between falling negative real bond yields and rising inflation expectations in the US and other major developed economies may be a sign of investors pricing in slower long-run potential economic growth in the aftermath of the COVID-19 recession – and, thus, lower equilibrium real interest rates. Stay overweight inflation-linked bonds versus nominal equivalents. Searching For Value In Global Spread Product Last week, we looked at the impact of currency hedging on the attractiveness of government bond yields across the developed markets.5 We concluded that US Treasuries still offered superior yields to most other countries’ sovereign bonds, even with the US dollar in a weakening trend and after hedging out currency risk. We also presented a cursory look at the relative attractiveness of the major global spread product categories in that report, but without factoring in any considerations on the relative credit quality or volatility between sectors. This week, we will look at the relative value of global spread products hedged into USD, GBP, EUR and JPY, but after controlling for those credit and volatility risks. We conducted a similar analysis in early 2018,6 ranking the currency-hedged yields for a wide variety of global spread products by the ratio of yields to trailing volatility. This time, instead of looking at the just that simple valuation metric, we use regression models to make a judgment on how under- or over-valued spread products are relative to their “fair value”. To recap the methodology of this analysis, we take the Bloomberg Barclays index yield-to-maturity (YTM) for each spread product category, hedged into the four currencies used in this analysis, and divide it by the annualized trailing volatility of those yields over both short-term (1-year) and long-term (3-year) windows. In order to hedge the yields into each currency, we used the annualized differentials between spot and 3-month forward exchange rates, which is the all-in cost of hedging. We then compare those currency-hedged, volatility-adjusted yields to two measures of risk: the index credit rating and duration times spread (DTS) for each spread product. Table 1 summarizes the attractiveness of each product when hedged into different currencies. The rank is based on the average of four different valuation measures.7 The higher the rank, the more attractive the sector is in terms of yield relative to risk measures such as both short-term and long-term volatilities, credit ratings, and DTS. Table 1Ranking Currency-Hedged, Risk-Adjusted Global Spread Product Yields

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

A few interesting points come from the table: Emerging market (EM) USD-denominated investment grade (IG) corporate debt ranks at or near the top of the rankings, for all currencies; the opposite holds true for EM USD-denominated sovereign bonds Almost all European spread products rank poorly for non-euro denominated investors US & UK high-yield (HY) rank highly for all currencies US real estate related assets (MBS and CMBS) also rank well for all investor groups In general, US products are more attractive than European credit sectors. This is mainly because US spread products offer higher yields than European ones even after accounting for volatility and the weakening US dollar. Almost all European spread products rank poorly for non-euro denominated investors. Chart 8 shows the unhedged YTM on the x-axis and the option-adjusted spread (OAS) on the y-axis (Table 2 contains the abbreviations used in this chart and all remaining charts in this report). Unsurprisingly, the YTM and OAS follow a very tight linear relationship. However, when yields are hedged into different currencies and risk measures are factored in, the result changes. Chart 8Global Spread Product Yields & Spreads

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Charts 9A to 12B show the details of spread product analysis with different currency hedges and risk factors. To limit the number of charts shown, we show only currency-hedged yields adjusted by long-term trailing volatility (the rankings do not change significantly when using a shorter-term volatility measure). The y-axis in all charts shows the volatility-adjusted yields, while the x-axis shows credit ratings and DTS. Sectors that are close to upper-right in each chart are more attractive (undervalued), while spread products that are close to bottom-left are less attractive (overvalued). Chart 9AGlobal Spread Product Yields, Hedged Into USD, Adjusted For Credit Quality

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Chart 9BGlobal Spread Product Yields, Hedged Into USD, Adjusted For Duration-Times-Spread

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Chart 10AGlobal Spread Product Yields, Hedged Into EUR, Adjusted For Credit Quality

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Chart 10BGlobal Spread Product Yields, Hedged Into EUR, Adjusted For Duration-Times-Spread

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Chart 11AGlobal Spread Product Yields, Hedged Into GBP, Adjusted For Credit Quality

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Chart 11BGlobal Spread Product Yields, Hedged Into GBP, Adjusted For Duration-Times-Spread

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Chart 12AGlobal Spread Product Yields, Hedged Into JPY, Adjusted For Credit Quality

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Chart 12BGlobal Spread Product Yields, Hedged Into JPY, Adjusted For Duration-Times-Spread

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Table 2Global Spread Products In Our Analysis

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

An interesting result is that when comparing the three major high-yield products (US-HY, EMU-HY and UK-HY), US-HY is the most attractive in USD terms, but UK-HY is more attractive when hedged into GBP, EUR, and JPY. Another observation is that higher quality bonds such as government-related and agency debt in the US and euro area are overvalued and less attractive given how low their yields are, regardless of their low volatility. The results from this analysis may differ from our current recommendations. For example, we currently only have a neutral recommendation on EM corporates, but based on this analysis, EM corporates offer the most attractive return in USD terms. This analysis is purely based on YTM and traditional risk factors without considering other concerns that could make EM assets riskier such as the spread of COVID-19 in major EM countries. However, these rankings do line up with our major spread product call of overweighting US IG and HY corporate debt versus euro area equivalents. Based on this analysis, EM corporates offer the most attractive return in USD terms. Bottom Line: A broad ranking of currency-hedged global spread product yields, adjusted for volatility and credit quality, shows that the most attractive yields (hedged into USD, EUR, GBP and JPY) are on offer in emerging market USD-denominated investment grade corporates and high-yield company debt in the US and UK. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Ray Park, CFA Research Analyst ray@bcaresearch.com Footnotes 1https://www.fitchratings.com/research/sovereigns/coronavirus-impact-on-gdp-will-be-felt-for-years-to-come-27-07-2020 2 Please see BCA Global Fixed Income Strategy Weekly Report, "How To Play The Revival Of Global Inflation Expectations", dated June 23, 2020, available at gfis.bcaresarch.com. 3 We use the French 10-year inflation-linked bond as the proxy for the entire euro area, as this is the oldest inflation-linked bond market in the region and thus has the most data history. 4https://www.wsj.com/articles/fed-weighs-abandoning-pre-emptive-rate-moves-to-curb-inflation-11596360600?mod=hp_lead_pos6 5 Please see BCA Research Weekly Report, “What A Weaker US Dollar Means For Global Bond Investors”, dated July 28, 2020, available at gfis.bcaresarch.com. 6 Please see BCA Global Fixed Income Strategy Weekly Report, "Policymakers Are Now Selling Put Options On Volatility, Not Asset Prices", dated March 6, 2018, available at gfis.bcareseach.com. 7 Hedged YTM/Short-term trailing volatility vs. Credit Rating; Hedged YTM/Long-term trailing volatility vs. Credit Rating; Hedged YTM/Long-term trailing volatility vs. Duration; Hedged YTM/Long-term trailing volatility vs. Duration. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Are Bond Markets Throwing In The Towel On Long-Term Growth?

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

Markets have shrugged off the rise in COVID-19 cases in the US and new clusters in other places such as Spain, Hong Kong, Melbourne, and Tokyo (Chart 1). The MSCI All-Country World Index is now only 4% off its all-time high in February. We don’t see the markets ignoring reality for much longer. Economic activity remains very subdued (Chart 2), which will eventually cause a significant rise in bankruptcies and problems for banks. Nevertheless, the unprecedented monetary and fiscal stimulus will be increased further in coming weeks, which should prevent a big shift towards pessimism for a while. The crunch time will come in the northern-hemisphere winter, when COVID cases in North America and Europe are likely to rise sharply again. Risk assets at their current levels are not pricing in those risks. Recommended Allocation

Monthly Portfolio Update: Winter Is Coming – But Maybe Not Yet

Monthly Portfolio Update: Winter Is Coming – But Maybe Not Yet

Chart 1COVID Cases Are Still On The Rise

COVID Cases Are Still On The Rise

COVID Cases Are Still On The Rise

Chart 2Activity Remains Subdued

Monthly Portfolio Update: Winter Is Coming – But Maybe Not Yet

Monthly Portfolio Update: Winter Is Coming – But Maybe Not Yet

Markets are driven by the second derivative of growth. It is not surprising, then, that equities began to rally in March, exactly when economic data stopped deteriorating, even though it remained atrocious (Chart 3). Real interest rates have also continued to fall, even as risk assets rallied; this further fueled the rally, since the theoretical value of equities rises as the rate at which they are discounted falls (Chart 4). Chart 3Data Stopped Deteriorating In March

Data Stopped Deteriorating In March

Data Stopped Deteriorating In March

Chart 4Real Interest Rates Have Continued To Fall

Real Interest Rates Have Continued To Fall

Real Interest Rates Have Continued To Fall

But the question now is: Can the data continue to improve? PMIs will fall back towards 50, and economic releases are unlikely to surprise so strongly on the upside. In the US, as a result of the rise in COVID-19 cases and renewed (albeit mostly moderate) government restrictions on activity, consumer confidence has started to weaken again and initial unemployment claims to pick up (Charts 5 and 6). Even though the Fed will remain ultra-dovish, real rates will not fall much further from their current level, which is the lowest since TIPS started trading in the late 1990s. Chart 5Consumer Confidence Is Weakening Again

Consumer Confidence Is Weakening Again

Consumer Confidence Is Weakening Again

Chart 6The Jobs Market Has Stopped Improving

The Jobs Market Has Stopped Improving

The Jobs Market Has Stopped Improving

Chart 7Will Money Supply Growth Peak?

Will Money Supply Growth Peak?

Will Money Supply Growth Peak?

Money supply growth has grown rapidly, as a result of the increase in central-bank balance-sheets and the rush of companies to borrow to shore up their cash positions (Chart 7). The increase in excess liquidity has also been a force behind the rise in risk assets. But money supply growth is likely to slow from now. At least partly offsetting these risks will be further fiscal stimulus. BCA Research’s Geopolitical strategists see Congress approving a big new package of around $2.5 trillion, mainly because of widespread popular support for an extension of more generous unemployment benefits (Table 1). Agreement should come before the scheduled recess on August 10 (if it doesn’t, this would trigger a market selloff). The recent agreement between European Union leaders on a EUR750 billion fiscal package was a major breakthrough, since it represented joint borrowing backed by the rich northern European countries to provide transfers to the poorer periphery. Table 1There Is Much Public Support For Fiscal Stimulus

Monthly Portfolio Update: Winter Is Coming – But Maybe Not Yet

Monthly Portfolio Update: Winter Is Coming – But Maybe Not Yet

Further upside may come as the many investors who have missed the rally since March capitulate and buy risk assets. Investor sentiment is currently unusually polarized. Speculative individuals and hedge funds are very bullish (Chart 8). But more conservative pension funds, wealth managers, and individual investors, mostly remain cautious, as evidenced by the AAII weekly survey, in which many more investors say they expect the stock market to fall over the next six months than to rise (Chart 9). Cash levels remain high by historical standards (Chart 10). Although only a minority of investors turned positive in March, a recent academic study demonstrated how hedge funds and small active institutions have a disproportionate influence on price movements (Chart 11). A downside risk, then, would be if these investors decided to take profits or turned more bearish. Chart 8Hedge Funds Are Bullish...

Hedge Funds Are Bullish...

Hedge Funds Are Bullish...

Chart 9...But Retail Investors Very Cautious

...But Retail Investors Very Cautious

...But Retail Investors Very Cautious

Chart 10Cash Holdings Remain Elevated

Cash Holdings Remain Elevated

Cash Holdings Remain Elevated

Chart 11Some Smaller Investors Have A Big Impact

Monthly Portfolio Update: Winter Is Coming – But Maybe Not Yet

Monthly Portfolio Update: Winter Is Coming – But Maybe Not Yet

We have argued, since the pandemic began, that investors should not take high-conviction bets in such an uncertain environment. They should, rather, design portfolios which are robust under various scenarios. After the 43% rise in global equities since March, we cannot recommend an above-benchmark weighting, since downside risks are not priced in. We remain neutral on global equities. However, fixed-income instruments look even more unattractive at the current low level of rates; we remain underweight. We recommend hedging via a large overweight in cash, which leaves dry powder for when a better buying opportunity arises. Currencies: A key (as always) to the macro view is what happens to the US dollar. Many of the drivers of the dollar – interest-rate differentials, valuation, momentum, and relative money-supply growth – point to it weakening further (Chart 12). The trade-weighted dollar is already off 9% from its March peak. We turned bearish on the USD in our Quarterly published at the beginning of July. It is too early, however, to declare that the dollar bull market, which began in 2012, is definitely over. Chart 12Dollar Indicators Are Bearish...

Dollar Indicators Are Bearish...

Dollar Indicators Are Bearish...

Chart 13…But Short USD Is Now A Consensus

Monthly Portfolio Update: Winter Is Coming – But Maybe Not Yet

Monthly Portfolio Update: Winter Is Coming – But Maybe Not Yet

A new downturn in the global economy would push the dollar back up again, since it is a safe-haven currency. Shorting the dollar, especially against the euro, is now a consensus position, and so a near-term reversal is quite likely (Chart 13). But, over the next 12-18 months, a move above 1.22 for the euro and towards 100 for the yen is possible. We will continue to analyze whether the dollar could be entering a bear market, since this would necessarily make us more structurally positive on commodities and emerging markets. Equities: A pickup in global growth and a weakening US dollar might prove positive for cyclicals and value stocks in the long run, which would cause European and EM equities to outperform. Given the current uncertainty, however, we cannot recommend that stance and therefore continue to prefer “growth defensives” such as Health Care and Technology, which implies an overweight on the overall US market. Valuations in the Health Care sector remain attractive (Chart 14). Companies in the (broadly defined) Tech sector are beneficiaries of the pandemic, generally have robust balance-sheets, and should continue to see strong earnings growth for some years. And, while Technology is clearly expensive, valuations are still nowhere as excessive as in 2000 (Chart 15). For Tech to crash would require either that it go ex-growth, or that there is significant regulatory action. Chart 14Health Care Still Attractively Valued

Health Care Still Attractively Valued

Health Care Still Attractively Valued

Chart 15Tech Still Way Below Bubble Levels

Tech Still Way Below Bubble Levels

Tech Still Way Below Bubble Levels

Chart 16Europe No Longer So Dominated By Financials

Europe No Longer So Dominated By Financials

Europe No Longer So Dominated By Financials

Neither of these seems likely for now. Euro zone equities are less dominated than they were by Financials, but remain more cyclical than the US, with very few internet-related names (Chart 16). Fixed Income: Central banks will remain very dovish and, as Fed chair Jerome Powell has emphasized, are not even thinking about thinking about tightening policy. This suggests that nominal rates will rise only moderately, even if growth continues to pick up. The Fed still has plenty of room to ease further if needed, since the programs it rolled out in March have barely been taken up yet (Table 2). We thus recommend a neutral position on duration. We find TIPS attractive as a hedge against an eventual spike in inflation. The 10-year breakeven inflation rate implied in TIPS remains around 100 basis points below being compatible with the Fed achieving its 2% PCE inflation target in the long run (Chart 17). The announcement in September of the results of the Fed’s 18-month review of its policy framework, which is likely to intensify its efforts to achieve the inflation target, could push breakevens up a bit further. In credit, we continue to recommend buying whatever central banks are buying, mostly investment-grade corporate bonds and the top end of the US junk bond market. Though spreads have fallen a long way, they are still well above end-2019 levels, and look attractive in a world of such low government bond yields (Chart 18). Table 2Usage Of The 2020 Federal Reserve Emergency Lending Facilities

Monthly Portfolio Update: Winter Is Coming – But Maybe Not Yet

Monthly Portfolio Update: Winter Is Coming – But Maybe Not Yet

Chart 17TIPS Still Pricing Low Inflation For A Decade

TIPS Still Pricing Low Inflation For A Decade

TIPS Still Pricing Low Inflation For A Decade

Chart 18Credit Spreads Could Fall Further

Credit Spreads Could Fall Further

Credit Spreads Could Fall Further

Commodities: The weakening US dollar and continued expansion of Chinese stimulus (Chart 19) should be positive for industrial metals prices over the next six to nine months. Oil prices also have some further upside, since the OPEC 2.0 agreement to restrict supply is being adhered to, and demand will gradually pick up (although air travel will remain depressed, more commuters are using their cars as they avoid public transport). BCA Research’s Energy Service forecasts Brent crude to average $44 in the second half of this year, and $65 in 2021 (up from the current $43). Gold has already run up a lot and is now close to a record high price in real terms, with sentiment very optimistic (Chart 20). Chart 19China Stimulus Positive For Metals

China Stimulus Positive For Metals

China Stimulus Positive For Metals

Nonetheless, in an environment of very low real rates, it represents a good hedge against extreme tail risks, and therefore we continue to recommend a moderate position as an insurance. Chart 20Gold Looking Rather Toppish

Gold Looking Rather Toppish

Gold Looking Rather Toppish

Garry Evans, Senior Vice President Global Asset Allocation garry@bcaresearch.com Recommended Asset Allocation

Dear Client, In lieu of our regular report next week, we will be sending you a Special Report from my colleague Garry Evans, Chief Global Asset Allocation Strategist. Garry will be discussing the social and industrial changes that will remain in place even after the COVID-19 pandemic is over, and how investors should tilt their portfolios to take advantage of them. I hope you find his report insightful. Best regards, Peter Berezin, Chief Global Strategist Highlights The number of coronavirus cases in the US appears to have peaked. Negotiations to avert a fiscal cliff continue in Washington. While we expect a deal to be reached, markets could tread nervously until this happens. The US dollar will weaken further over the next 12 months. Narrowing interest rate differentials, a revival in global growth, deteriorating momentum, and pricey valuations all bode poorly for the greenback. Global equities in general, and non-US stocks in particular, tend to fare well in a weak dollar environment. Small cap and value stocks usually outperform when the dollar weakens. Bank shares should start to do better as yield curves steepen and faster economic growth reduces concerns over non-performing loans. US Virus Wave Cresting, But Fiscal Risks Intensifying Chart 1US: Number Of New Cases Seems To Be Peaking

The Stock Market Implications Of A Weaker Dollar

The Stock Market Implications Of A Weaker Dollar

Last week, we argued that the two biggest near-term threats to stocks and other risky assets were the rising number of coronavirus cases in parts of the US and the looming fiscal cliff.1 Since then, the news on the virus has been broadly positive, while developments on the fiscal front have been mixed. Chart 1 shows that the number of new cases seems to have peaked in the US. In Texas, Florida, California, and Arizona, the share of doctor visits linked to suspected Covid infections is trending lower. This metric leads diagnoses by about one-to-two weeks (Chart 2). Chart 2Doctor Visits, Which Lead Diagnoses, Are Trending Lower

The Stock Market Implications Of A Weaker Dollar

The Stock Market Implications Of A Weaker Dollar

Over half the US population lives in states that have either suspended or reversed reopening plans (Chart 3). Assuming the number of infections keeps falling and fiscal policy is not unduly tightened, household spending and employment growth – which appear to have stalled out in the second half of July – should begin to pick up. Chart 3Not So Fast

The Stock Market Implications Of A Weaker Dollar

The Stock Market Implications Of A Weaker Dollar

Unfortunately, the assumption that fiscal policy will remain stimulative looks somewhat shaky. Expanded unemployment benefits for 30 million Americans, consisting mainly of an additional $600 per week for unemployed workers, are set to expire at the end of July. Congressional Republicans have suggested trimming benefits to $200 per week. However, even that would represent a fiscal tightening of nearly 3% of GDP. A Question Of Incentives The Republican position is understandable, given that two-thirds of unemployed workers are currently receiving more in unemployment benefits than they earned while working. Thus, some scaling back of benefits is not only inevitable, but desirable. The question is one of timing. While job openings have risen from their lows, they are still 23% below where they were at the start of the year. According to the NFIB survey, the share of small businesses reporting difficulty in finding qualified workers has also fallen from year-ago levels. When the binding constraint on employment is a shortage of jobs rather than a shortage of workers, higher unemployment benefits will likely boost hiring. This is because increased benefits will increase spending on goods and services across the economy, thus augmenting the demand for labor. Debt, Gold, And The Dollar Chart 4Gold Prices Have Risen On The Back Of Falling Real Yields

Gold Prices Have Risen On The Back Of Falling Real Yields

Gold Prices Have Risen On The Back Of Falling Real Yields

Does the inevitable increase in government debt due to ongoing fiscal stimulus portend disaster down the road? According to many commentators, the recent drop in the dollar and the surge in gold prices is surely telling us that it does. While it is a compelling story, it is mainly false. The yield on the 30-year Treasury bond currently stands at 1.20%, down from 1.5% in mid-June and 2.33% at the start of the year. Bondholders may be many things, but masochistic is not one of them. If they really thought a fiscal crisis was around the corner, yields would be a lot higher. So why is the dollar falling and gold rallying? The answer is inflation expectations have risen off very low levels, which has pushed down real yields. Gold prices are almost perfectly correlated with real interest rates (Chart 4). The Real Reason The Dollar Has Fallen Going into this year, US real yields had a lot more room to decline than rates abroad. For example, at the start of 2019, US real 2-year yields were 221 bps above comparable euro area yields. Today, US real rates are 35 bps lower – a swing of 256 bps. Yield differentials have narrowed against other economies as well, which has pushed down the value of the dollar (Chart 5). In addition, relative growth dynamics have hurt the greenback. The US economy tends to be less cyclical than most of its trading partners. While the US benefits from faster global growth, the rest of the world benefits even more. This causes capital to flow from the US to other countries, leading to a weaker dollar (Chart 6). Chart 5The Greenback Has Been Losing Interest Rate Support

The Greenback Has Been Losing Interest Rate Support

The Greenback Has Been Losing Interest Rate Support

Chart 6The Dollar Usually Weakens When Global Growth Accelerates

The Dollar Usually Weakens When Global Growth Accelerates

The Dollar Usually Weakens When Global Growth Accelerates

Chart 7The Dollar And Cycles

The Stock Market Implications Of A Weaker Dollar

The Stock Market Implications Of A Weaker Dollar

BCA Research’s Foreign Exchange Strategist, Chester Ntonifor, has stressed that the dollar typically fares worst in the initial stages of business cycle recoveries (Chart 7). That is the stage we are in today. Indeed, the gap in growth between the US and the rest of the world is likely to be larger than usual over the next few quarters because the pandemic has hit the US harder than most other developed economies. Momentum is also working against the dollar. Being a contrarian is usually a smart investment strategy. That is not the case when it comes to trading the dollar. With the dollar, you want to follow the herd. This is because the dollar is a high momentum currency (Chart 8). A simple trading rule that buys the dollar when it is trading above its 50-day or 200-day moving average, and sells the dollar when it is trading below its respective moving averages, has historically made a lot of money. Likewise, the dollar performs best prospectively when sentiment is bullish and improving (Chart 9). Currently, the dollar is trading below its various moving averages. Sentiment is also poor and deteriorating (Chart 10). Chart 8USD Is A High Momentum Currency

The Stock Market Implications Of A Weaker Dollar

The Stock Market Implications Of A Weaker Dollar

Chart 9Trading The Dollar: The Trend Is Your Friend

The Stock Market Implications Of A Weaker Dollar

The Stock Market Implications Of A Weaker Dollar

Chart 10The Dollar Has Started Breaking Down

The Dollar Has Started Breaking Down

The Dollar Has Started Breaking Down

Chart 11The Dollar Is Still Fairly Expensive

The Stock Market Implications Of A Weaker Dollar

The Stock Market Implications Of A Weaker Dollar

If the dollar were cheap, all the factors discussed above could be overlooked. But the dollar is not cheap. It is still pricey based on purchasing power parity measures which compare the common-currency cost of identical consumption bundles from one country to the next (Chart 11). A Weaker Dollar is Bullish For Stocks, Especially Non-US Stocks Global equities in general, and non-US stocks in particular, tend to perform well when the dollar is weakening (Chart 12). Chart 12A Weaker Dollar Should Help Global Equities

A Weaker Dollar Should Help Global Equities

A Weaker Dollar Should Help Global Equities

Chart 13Cyclicals Tend To Outperform Defensives In A Falling Dollar Environment

Cyclicals Tend To Outperform Defensives In A Falling Dollar Environment

Cyclicals Tend To Outperform Defensives In A Falling Dollar Environment

Cyclical sectors such as industrials, energy, and materials normally outperform defensives in a weak dollar environment (Chart 13). Relative profit growth in these sectors tends to rise when the dollar depreciates (Chart 14). To the extent that cyclicals are overrepresented in stock market indices outside the US, this gives non-US equities a leg up. Chart 14Relative Profit Growth In Cyclical Sectors Tend To Rise When The USD Depreciates

Relative Profit Growth In Cyclical Sectors Tend To Rise When The USD Depreciates

Relative Profit Growth In Cyclical Sectors Tend To Rise When The USD Depreciates

EM Is The Big Winner From Dollar Weakness A weaker dollar is particularly beneficial to emerging markets. Commodity prices usually rise when the dollar drops (Chart 15). Rising resource prices are good news for many emerging markets. EM debt dynamics also tend to improve when the dollar weakens. EM external debt has grown in recent years (Chart 16). About 80% of EM foreign currency denominated debt is in dollars. A falling dollar reduces the local-currency value of US dollar-denominated liabilities, thus strengthening the balance sheets of many EM companies and governments. Emerging markets with large current account deficits and significant dollar liabilities such as Brazil, Indonesia, Turkey, and Mexico will outperform EMs that generally run current account surpluses and have little in the way of foreign-currency debt. Chart 15Commodity Prices Usually Rise When The Dollar Falls

Commodity Prices Usually Rise When The Dollar Falls

Commodity Prices Usually Rise When The Dollar Falls

Chart 16EM External Debt Has Grown In Recent Years

EM External Debt Has Grown In Recent Years

EM External Debt Has Grown In Recent Years

The Federal Reserve today is trying to engineer an easing in US financial conditions. A weaker dollar is facilitating that goal. Historically, EM stocks have been almost perfectly inversely correlated with US financial conditions (Chart 17). Chart 17EM Equities Benefit From Easier US Financial Conditions

EM Equities Benefit From Easier US Financial Conditions

EM Equities Benefit From Easier US Financial Conditions