Euro Area

Highlights ECB: The ECB disappointed markets last week who expected an increase in the size of its asset purchase schemes given the recent increase of Italian bond yields. For now, the central bank remains focused on preventing a European credit crunch through increased use of bank funding measures like TLTROs – although a renewed selloff in BTPs would likely change the minds of the “Italy hawks” on the ECB Governing Council. Euro Area High-Yield: Valuations for euro area junk bonds improved somewhat during the COVID-19 selloff, but spreads do not offer much protection from the coming surge in default losses. Remain underweight euro area high-yield corporates in global fixed income portfolios. Feature Chart 1Will Growth Trump Liquidity For Euro Area Junk Bonds?

Will Growth Trump Liquidity For Euro Area Junk Bonds?

Will Growth Trump Liquidity For Euro Area Junk Bonds?

Over the past week, investors heard from the three major developed market central banks – the Federal Reserve, the European Central Bank (ECB) and the Bank of Japan (BoJ). The Fed and BoJ did little to seriously impact financial markets, offering only strengthened forward guidance on already hyper-easy policy settings along with some expansion of existing asset purchase programs (involving municipal bonds for the Fed, JGBs and Japanese corporate bonds for the BoJ). The ECB was the most interesting of the three, because of what was NOT done – namely, an increase in the amount of asset purchases – and what it implies about the policy debate within the central bank on how to deal with Italy. The hit to the euro area economy from the COVID-19 lockdowns has been sharp and brutal, pushing the entire region quickly into deep recession (Chart 1). Given such a severe hit to growth, and with policy interest rates already at zero (or even negative), the only avenue for the ECB to deliver more stimulus is through expanding its balance sheet through asset purchases and liquidity provision to banks. This makes the ECB’s next moves on its balance sheet critical for determining the future path of European risk assets like equities and high-yield corporate bonds – the latter of which we discuss later in this report. A Cautious Next Step From The ECB Chart 2An Unprecedented Economic Collapse

An Unprecedented Economic Collapse

An Unprecedented Economic Collapse

The need for the ECB to do something at last week’s monetary policy meeting was obvious. Real GDP for the entire region is estimated to have contracted -3.8% on a year-over-year basis in the first quarter of the year. At the country level, large declines occurred in France (-5.8%), Italy (-4.7%) and Spain (-5.2%) that were far greater than seen during the 2009 recession. The decline was broad-based across industries as well, with the European Commission’s (EC) business confidence indices collapsing in April for manufacturing, services, retail and construction (Chart 2). The bottom has also fallen out on the EC price expectations indices, suggesting that outright deflation across the euro area is just around the corner. The ECB last week provided what were called “alternative scenarios” for the impact of COVID-19 on euro area growth. We presume these are meant to be an alternative to the most recent set of ECB economic projections that were published in March that now look wildly optimistic given the COVID-19 lockdowns. The revised scenarios now call for a real GDP contraction in 2020 of anywhere from -5% to -12%, with only a partial recovery of those losses in 2021.1 The central bank also provided an estimate of the output loss by industry from COVID-19 related lockdowns (Table 1) – a staggering -60% for retail, transportation, accommodation and food services and -40% for manufacturing and construction. Table 1The Lockdown Has Been Painful For Europe

The ECB Will Do Whatever It Takes … Eventually

The ECB Will Do Whatever It Takes … Eventually

Against this horrendous growth and inflation backdrop, with forecasts being slashed, the expectation was that the ECB would ramp up the size of its bond buying programs to try and ease financial conditions further. That would help cushion the growth downturn and attempt to put a floor under collapsing inflation expectations (Chart 3). Yet at last week’s monetary policy meeting, the ECB announced the following: No changes in policy interest rates No increase in the size of the Asset Purchase Program (APP) from the existing €120bn or Pandemic Emergency Purchase Program (PEPP) from the existing €750bn For existing targeted long-term refinancing operations (TLTROs) between June 2020 and June 2021, interest rates were lowered by -25bps A new long-term refinancing operation for euro area banks was introduced called the Pandemic Emergency Long Term Refinancing Operation (PELTRO), which would offer liquidity to euro area banks on a monthly basis until December, at an interest rate of -0.25%. The increased use of LTROs was an easier way for the ECB Governing Council to avoid a potential credit crunch if euro area banks become more risk averse. The ECB clearly wants to take no chances on banks reining in loan activity. The latest ECB Bank Lending Survey, released just two days before last week’s policy meeting, showed a modest tightening of standards for bank loans to businesses in the first quarter of 2020. This was most visible in Germany and Italy, with France actually showing a slight decline in the net percentage of banks tightening lending standards (Chart 4). The survey also showed that euro area banks expected a significant net easing of lending standards in response to the loan guarantees and liquidity support measures announced by European governments to mitigate the impact of COVID-19 lockdowns. Chart 3Expanding The Balance Sheet Is The Only Tool The ECB Has Left

Expanding The Balance Sheet Is The Only Tool The ECB Has Left

Expanding The Balance Sheet Is The Only Tool The ECB Has Left

Chart 4The ECB Wants To Avoid A Credit Crunch

The ECB Wants To Avoid A Credit Crunch

The ECB Wants To Avoid A Credit Crunch

With bank lending growth across the entire euro area having already increased to 4.9% on a year-over-year basis in March, the fastest pace in two years, the ECB clearly wants to take no chances on banks reining in loan activity - even if those loans are merely for stressed companies tapping existing credit lines, or taking advantage of government loan guarantees to minimize layoffs in a deep recession. Another surge in Italian bond yields in the next few months would likely trigger an increase in the size of the PEPP. However, there was likely an additional reason why the ECB chose the LTRO route over ramping up asset purchases – internal political divisions over Italy. Chart 5Italian Financial Stability Remains Critical For The ECB

Italian Financial Stability Remains Critical For The ECB

Italian Financial Stability Remains Critical For The ECB

There remain some on the ECB Governing Council that do not wish to keep buying more BTPs, thus giving Italy a blank check to run even larger budget deficits. The unique nature of the COVID-19 outbreak has somewhat loosened those biases against the highly indebted countries of southern Europe, as evidenced by the inclusion of Greek bonds in the PEPP shopping list. Yet there are still many within the ECB, and within the governments of the “hard money” countries of the euro area, who would prefer to see Italy get monetary support for greater deficit spending through ECB vehicles with conditionality like Outright Monetary Transactions (OMT). Given these internal divisions over Italy, an increase in the size of the existing asset purchase schemes will only take place if there is a major increase in Italian risk premiums that threatens the financial stability of the entire euro area. On that front, risk indicators like the BTP-Bund spread and credit default spreads on Italian banks have risen over the past month, but remain well below the stressed levels witnessed during the Global Financial Crisis and the European Debt Crisis (Chart 5). Additionally, Italian bank stocks have actually been outperforming their euro area peers since early 2019, while the Italy-Germany spread curve is not inverted (2-year spreads higher than 10yr spreads) as occurred in 2011 when investors feared Italy would crash out of the euro. With Italian government yields still at relatively low and manageable levels, even as the highly-indebted Italian government has stated that its budget deficit will surge to -10% of GDP to provide stimulus to a virus-ravaged economy, there is no pressure on the ECB to increase the size of the PEPP that was just announced less than two months ago. Yet even with all the internal divisions, another surge in Italian bond yields in the next few months would likely trigger an increase in the size of the PEPP to prevent a broader tightening of euro area financial conditions. For this reason, we continue to recommend a strategic (6-12 months) overweight stance on Italian government bonds within global fixed income portfolios. Bottom Line: The ECB disappointed markets last week who expected an increase in the size of its asset purchase schemes given the recent increase of Italian bond yields. For now, the central bank remains focused on preventing a European credit crunch through increased use of bank funding measures like TLTROs – although a renewed selloff in BTPs would likely change the minds of the “Italy hawks” on the ECB Governing Council. A Quick Look At Euro Area High-Yield Valuation We recently upgraded our recommended investment stance on euro area investment grade corporate bonds to neutral.2 This shift was based on the ECB increasing the amount of its corporate bond purchases as part of its COVID-19 monetary easing measures, coming after the Fed announced its own new programs to buy US investment grade corporates. With the major central banks providing direct support to higher quality corporates, the left side of the return distribution for those bonds eligible for these purchase programs has effectively been reduced. This warrants a higher weighting for those bonds in investor portfolios. For high-yield corporates, the story is more nuanced. Both the Fed and ECB have announced that investment grade bonds purchased in their bond buying programs, which are then subsequently downgraded to below investment grade, can stay on the balance sheet of those programs. This makes Ba-rated junk bonds – the highest credit tier below investment grade – a relatively more attractive bet within the overall high-yield universe, both in the US and Europe. Although the lack of a direct central bank bid still makes high-yield corporates a riskier bet in a recessionary environment where default losses will surely increase. This means rather than just “buying what the central banks are buying”, we must rely on more traditional metrics to determine if high-yield bonds offer value. To evaluate the attractiveness of euro area high-yield corporates, we use three different approaches that use relative value to other credit markets, or more intrinsic value based on potential credit losses. Relative spreads vs. euro area investment grade One way to assess the value of euro area high-yield is to compare its credit spread to that of higher-rated euro area investment grade corporate bonds. Since movements in both spreads are highly correlated, as they both benefit from accelerating euro area economic growth (and vice versa), any change in spreads between the two could represent a relative value opportunity. Currently, the option-adjusted spread (OAS) of the euro area high-yield benchmark index (635bps) is 449bps over that of the investment grade index (186bps), using Bloomberg Barclays index data (Chart 6). While this is a relatively wide spread differential for the years since the 2008 financial crisis, it is not a particularly large gap during a recession that is likely to be deeper than the 2009 downturn. The same argument holds when looking at the ratio of the euro area high-yield OAS to the investment grade OAS, which is only at average levels for the post crisis period (3rd panel). 12-month breakeven spreads One of our favorite credit valuation tools is the 12-month breakeven spread, which measures the amount of spread widening over a one-year horizon that would make the total return of a corporate bond equal to that of a duration-matched government bond. We apply that calculation to data for an entire spread product sector, like investment grade or high-yield, to determine a breakeven spread for that sector. We then look at the percentile ranks of the breakeven spread versus its own history to determine if that particular fixed income sector looks relatively attractive. Rather than just “buying what the central banks are buying”, we must rely on more traditional metrics to determine if high-yield bonds offer value. On that basis, euro area high-yield corporates, across all credit tiers, offer somewhat attractive spreads, with 12-month breakevens in the upper half of the historical distribution (Chart 7). US high-yield, by comparison, offers far more attractive spreads with 12-month breakevens in the upper quartile of their historical distribution across all credit tiers. Only the riskiest Caa-rated bonds are in the top 25% of the distribution in the euro area (Chart 8). Chart 6In The Euro Area, HY Is Not That Cheap Versus IG

In The Euro Area, HY Is Not That Cheap Versus IG

In The Euro Area, HY Is Not That Cheap Versus IG

Chart 712-Month Breakeven Spreads For Euro Area HY Are Now More Attractive ...

12-Month Breakeven Spreads For Euro Area HY Are Now More Attractive ...

12-Month Breakeven Spreads For Euro Area HY Are Now More Attractive ...

Chart 8… But Not Versus US High-Yield

The ECB Will Do Whatever It Takes … Eventually

The ECB Will Do Whatever It Takes … Eventually

The overall attractiveness of US high-yield versus euro area equivalents can also be seen when comparing the benchmark index yields in common currency terms. For the overall indices, euro area junk bond yields, hedged into USD dollars, offer a yield of 7.8%, virtually equal to the 8.0% yield in the US (Chart 9), although more material differences do exist within credit tiers. Chart 9A Comparison Of Junk Bond Yields In The Euro Area & The US

The ECB Will Do Whatever It Takes … Eventually

The ECB Will Do Whatever It Takes … Eventually

Default-adjusted spreads The other metric that we use to assess the value of high-yield corporate bonds is default-adjusted spreads. This measure takes the high-yield index OAS and subtracts credit losses to determine an “excess” spread. We look at the current default-adjusted spread versus its long-run average to determine if high-yield spreads offer an attractive valuation cushion relative to expected credit losses. To determine the credit losses, we need the default rate, and the recovery rate given default, for the overall high-yield market. For defaults, we will use the output of our euro area default rate model (Chart 10). The model uses four variables: lending standards for businesses from the ECB bank lending survey, high-yield ratings downgrades as a share of all rating actions, euro area real GDP growth, and the median debt-to-equity ratio for a sample of issuers in the euro area high-yield space. All the variables are advanced such that the model produces a one-year-ahead forecast of expected high-yield defaults.3 Our high-yield model is projecting that the euro area default rate will climb to 11% by the end of 2020, before declining to 8% mid-2021 as the euro area economy recovers from the 2020 recession. For the euro recovery rate, we are using a range based on the historical experience during recessions (30%) and recoveries (45%). Using our default rate model projection, and that range of recovery rates, we can produce a range of euro area default-adjusted spreads. Euro area high-yield spreads do not offer much of a spread cushion to absorb expected default losses over the next year. Thus, euro area junk bonds are expensive. In Chart 11, we show the history of the euro area default adjusted spread. We have added the long run average (358bps) and the +/1 standard deviation of the spread. Spreads at or lower than -1 standard deviation are considered expensive (i.e. the high-yield index spread is too low relative to credit losses), and vice versa. The shaded box in the bottom right corner of the chart represents our forecasted default-adjusted spread for the next year. Chart 10Our Model Says The Euro Area Default Rate Will Surpass 10%

Our Model Says The Euro Area Default Rate Will Surpass 10%

Our Model Says The Euro Area Default Rate Will Surpass 10%

Chart 11Euro Area HY Default-Adjusted Spreads Do Not Offer Compelling Value

Euro Area HY Default-Adjusted Spreads Do Not Offer Compelling Value

Euro Area HY Default-Adjusted Spreads Do Not Offer Compelling Value

Chart 12An Aggressive Overweight Stance On Risk Assets Is Still Not Warranted

An Aggressive Overweight Stance On Risk Assets Is Still Not Warranted

An Aggressive Overweight Stance On Risk Assets Is Still Not Warranted

Our projected spread range over the next twelve months is 218bps to -112bps, well below the long-run average and at the low end of the historical distribution. We conclude from this analysis that current euro area high-yield spreads do not offer much of a spread cushion to absorb expected default losses over the next year. Thus, euro area junk bonds are expensive. Given the lack of a compelling valuation argument under all our metrics, we are leaving our recommended investment stance on euro area high-yield bonds at underweight. We continue to focus our recommended global spread product allocations on overweights in markets where there is direct and explicit support from policymaker purchase programs: US investment grade bonds with maturity of less than five years, US Ba-rated high-yield bonds, and UK investment grade corporates. This selectively overweight investment stance on global credit is warranted from a risk management perspective, as well. Our “Pro-Risk Checklist” of indicators that would lead us to recommend a more aggressive stance on risk assets in general, and spread product in particular, is still flashing a cautious message (Chart 12). The US dollar continues to strengthen (exacerbating global deflation and dollar funding pressures); the VIX index of US equity volatility has fallen below our threshold of 40, but not by much; and the number of new global (ex-China) COVID-19 cases is showing mixed results, falling in the US and Italy but increasing elsewhere. Bottom Line: Valuations for euro area junk bonds improved somewhat during the COVID-19 selloff, but spreads do not offer much protection from the coming surge in default losses. Remain underweight euro area high-yield corporates in global fixed income portfolios. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 The alternative ECB growth forecasts can be found here: https://www.ecb.europa.eu/pub/economic-bulletin/focus/2020/html/ecb.ebbox202003_01~767f86ae95.en.html 2 Please see BCA Research Global Fixed Income Strategy Weekly Report, "Buy What The Central Banks Are Buying", dated April 14, 2020, available at gfis.bcaresearch.com. 3 For real GDP growth, we use Bloomberg consensus forecasts for the next four quarters in the model. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

The ECB Will Do Whatever It Takes … Eventually

The ECB Will Do Whatever It Takes … Eventually

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

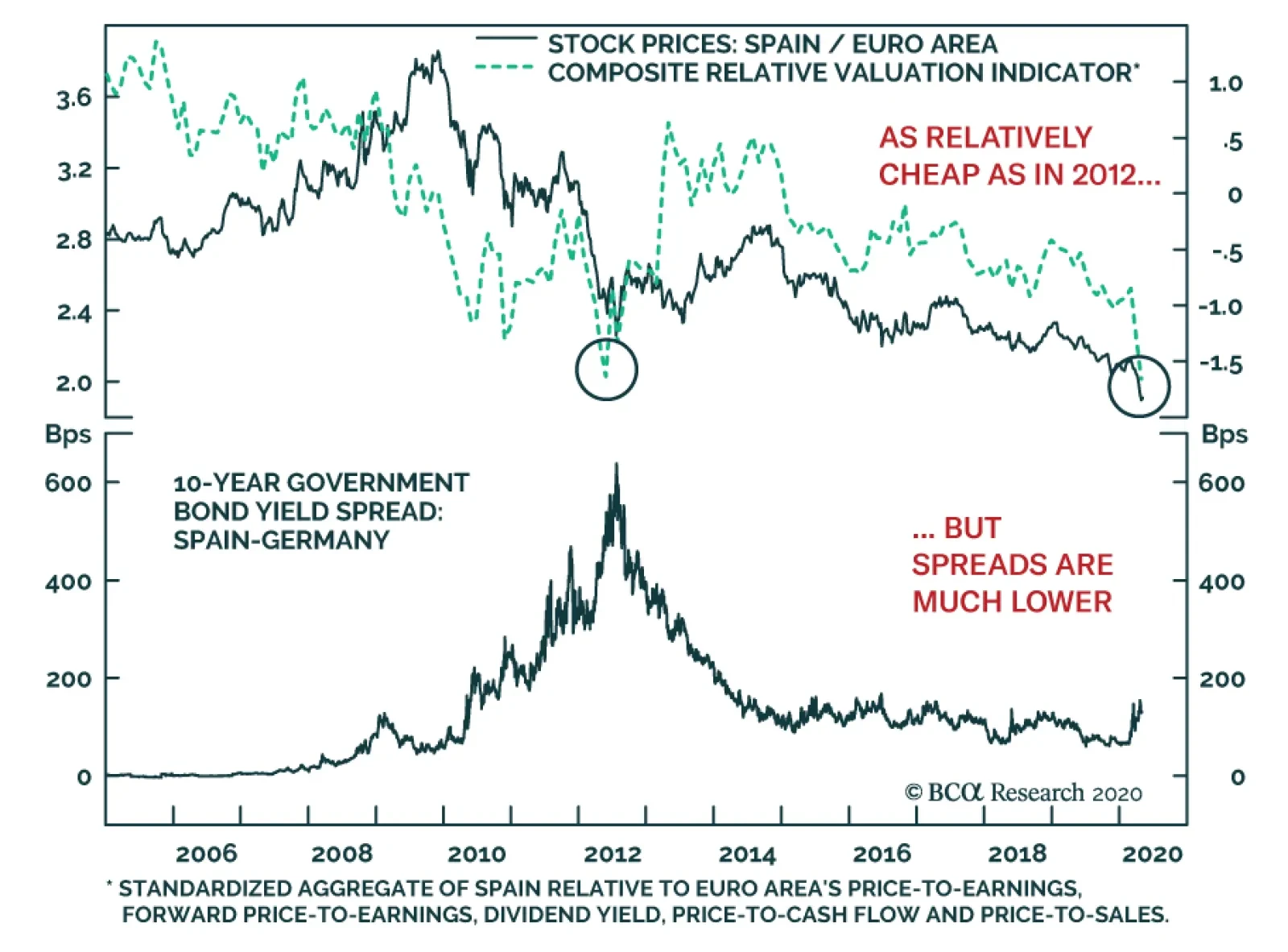

Spanish stocks stand at their lowest level relative to the overall Eurozone since late 1996. Additionally, a composite valuation indicator currently shows that Spanish equities trade at their cheapest relative to European stocks since the apex of the euro…

Highlights In this Special Report we explore in detail the fiscal response amongst advanced economies, with the goal of judging whether the response is large enough to prevent an “L-shaped” recession. The crisis remains in its early days and new information about the size and character of the response, as well as the magnitude of the economic shock, continues to emerge on a near-daily basis. As such, our conclusions may change over the coming weeks in line with incoming data. Even when narrowly-defined, the announced (or likely) fiscal response of the US, China, and Germany is quite large and appears to be adequate to prevent the direct and indirect effects of the lockdowns from causing an “L-shaped” event. This is not the case, however, in other euro area economies (France, Italy, and Spain), or in emerging markets. Our analysis also suggests that the global fiscal response will need to increase if the global economy faces a W-shaped shock caused by another round of aggressive containment measures later this year. This underscores the importance of ensuring that the “Great Lockdown” succeeds at reducing the spread of the disease to a point that does not necessitate widespread renewed restrictions on economic activity. Feature The global economic expansion that began in 2009 has come to an abrupt end due to the COVID-19 pandemic. Aggressive containment measures necessary to control the spread of the disease and prevent the collapse in health care systems around the world have caused a large and sudden stop in global economic activity, which has prompted unprecedented responses from governments around the world. In this Special Report we explore in detail the fiscal response amongst advanced economies, with the goal of judging whether the response is large enough to prevent an “L-shaped” recession (characterized by a very prolonged return to trend growth). The crisis remains in its early days and new information about the size and character of the response, as well as the magnitude of the economic shock, continues to emerge on a near-daily basis. As such, our conclusions may change over the coming weeks in line with incoming data. But for now, we (tentatively) conclude that the fiscal response appears to be adequate to prevent the direct and indirect effects of the lockdowns from causing an “L-shaped” event. However, there are two important caveats. First, while Germany has provided among the strongest fiscal responses globally, measures in France, Italy, and Spain are still lacking and must be stepped up. Second, the announced fiscal measures will not be sufficient if the global economy faces a W-shaped shock caused by another round of aggressive containment measures later this year – more will have to be done. For policymakers, this underscores the importance of ensuring that the “Great Lockdown” succeeds at reducing the spread of the disease to a point that does not necessitate widespread renewed restrictions on economic activity. In this regard, the gradual re-opening of several US states by early-May, while positive for economic activity in the short-run, is a non-trivial risk to the US and global economic outlooks over the coming 6-12 months. This risk must be closely watched by investors. The Global Fiscal Response: Comparing Across Countries And Across Measures The flurry of policy announcements from national governments over the past six weeks has led to a great degree of confusion about the size and disposition of the global COVID-19 fiscal response. Our analysis is based heavily on the IMF’s tracking of these measures, albeit with a few adjustments. We also rely on analysis from Bruegel, a prominent European macroeconomic think-tank, as well as our own Geopolitical Strategy team and a variety of news reports. Chart II-1 presents the IMF’s estimate of the total fiscal response to the crisis across major countries, as of April 23rd, broken down into “above-the-line” and “below-the-line” measures. Above-the-line measures are those that directly impact government budget balances (direct fiscal spending and revenue measures, usually tax deferrals), whereas below-the-line measures typically involve balance sheet measures to backstop businesses through capital injections and loan guarantees. Chart II-1The Global Fiscal Response Is Huge When Including All Measures

May 2020

May 2020

Chart II-1 makes it clear that the fiscal response of advanced economies is enormous when including both above- and below-the-line measures. By this metric, the response of most developed economies is on the order of 10% of GDP, and well above 30% in the case of Italy and Germany. However, using the sum of above- and below-the-line measures to gauge the fiscal response of any country may not be the ideal approach, given that below-the-line measures are contingent either on the triggering of certain conditions or on the provision of credit to households and firms from the financial system. Below-the-line measures also likely increase the liability position of the private sector, thus raising the odds of negative second-round effects. Instead, Chart II-2 compares the countries shown in Chart 1 based only on the IMF’s estimate of above-the-line measures, and with a 4% downward adjustment to Japan’s reported spending to account for previously announced measures.8 The chart shows that countries fall into roughly three categories in terms of the magnitude of their above-the-line response: in excess of 4% of GDP (Australia, the US, Japan, Canada, and Germany), 2-3% (the UK, Brazil, and China), and sub-2% (all other countries shown in the chart, including Spain, Italy, and France). Chart II-2The Picture Changes When Excluding Below-The-Line Measures

May 2020

May 2020

Analysis by Bruegel provides somewhat different estimates of the global COVID-19 fiscal response for select European countries as well as the US (Table II-1). Bruegel breaks down discretionary fiscal measures that have been announced into three categories: those involving an immediate fiscal impulse (new spending and foregone revenues), those related to deferred payments, and other liquidity provisions and guarantees. Bruegel distinguishes between the first and second categories because of their differing impact on government budget balances. Deferrals improve the liquidity positions of individuals and companies but do not cancel their obligations, meaning that they result only in a temporary deterioration in budget balances. Table II-1The Type Of Fiscal Response Varies Significantly Across Countries

May 2020

May 2020

Table II-1 highlights that Bruegel’s estimates of the sum of above- and below-the-line measures are similar to the IMF’s estimates for the US, the UK, and Spain, but are smaller for Italy and larger for France and Germany (particularly the latter). These differences underscore the extreme uncertainty facing investors, who have to contend not only with varying estimates of the magnitude of government policies but also a torrent of news concerning the evolution of the pandemic itself. Chart II-3 presents our best current estimate of the above-the-line fiscal response of several countries (the measure we deem to be most likely to result in an immediate fiscal impulse), by excluding loans, guarantees, and non-specified revenue deferrals to the best of our ability.2 Chart II-3 is based on a combination of data from the IMF, Bruegel analysis, and BCA estimates and news analysis. Chart II-3When Narrowly Defined, Several Countries Are Responding Forcefully, But Many Countries Are Not

May 2020

May 2020

Overall, investors can draw the following conclusions from Charts II-1 – II-3 and Table II-1: When measured as the total of above- and below-the-line measures, nearly all large developed market countries have responded with sizeable measures. Emerging market economies are the clear laggards. Excluding below-the-line measures and using our approach, Australia, the US, China, Germany, Japan, and Canada appear to be spending the most relative to the size of their economies. While Japan’s “headline” fiscal number was inflated by including previously-announced spending, it is still decently-sized after adjustment. Outside of Germany, the rest of Europe appears to be providing a middling or poor above-the-line fiscal response. The UK appears to be providing between 4-5% of GDP as a fiscal impulse, whereas the fiscal response in Italy, Spain, and France looks more like that of emerging markets than of advanced economies. Measuring The Stimulus Against The Shock Despite the substantial amount of new information over the past six weeks concerning the evolution of the pandemic and the attendant policy response, it remains extremely difficult to judge what the balance between shock and stimulus will be and what that means for the profile of growth. Nonetheless, below we present a framework that investors can use to approach the question, and that can be updated as new information emerges concerning the impact of the shutdowns and the extent of the response. Our approach involves analyzing four specific questions: What is the size of the initial shock? What are the likely second-round effects on growth? What is the likely multiplier on fiscal spending? Will the composition of fiscal spending alter its effectiveness? The Size Of The Initial Shock Chart II-4 presents the OECD’s estimates of the initial impact of partial or complete shutdowns on economic activity in several countries. The OECD first used a sectoral approach to estimating the impact on activity while lockdowns are in effect, assuming a 100% shutdown for manufacturing of transportation equipment and other personal services, a 50% decline in activity for construction and professional services, and a 75% decline for retail trade, wholesale trade, hotels, restaurants, and air travel. Chart II-4 illustrates the total impact of this approach for key developed and emerging economies. Chart II-4Annual GDP Will Be 1.5%-2.5% Lower For Each Month Lockdowns Are In Effect

May 2020

May 2020

The OECD’s approach provides a credible estimate of the impact of aggressive containment policies, and implies that annual real GDP is likely to be 1.5-2.5% lower for major countries for each month that lockdown policies are in effect. This implies that output in major economies is likely to fall 3.5% - 6% for the year from the initial shock alone, assuming an aggressive 10-week lockdown followed by a complete return to normal. Estimating Potential Second Round Effects Chart II-5 presents projections from the Bank for International Settlements on the spillover and spillback potential of a 5% initial shock to the level of global GDP from the COVID-19 pandemic (equivalent to a 20% impact on an annualized basis). Chart II-5Additional Lockdown Events Are A Greater Risk Than First Wave After-Effects

May 2020

May 2020

The chart shows that the cumulative impact of the initial shock rises to 7-8% by the end of this year for the US, euro area, and emerging markets, and 6% for other advanced economies. These estimates account for both domestic second round effects of the initial shock, as well as the reverberating impact of the shock on global trade. Chart II-5 also shows the devastating effect that a second wave of COVID-19 emerging in the second half of the year would have after including spillover and spillback effects, assuming that only partial lockdowns would be required. In this scenario, the level of GDP would be 10-12% lower at the end of the year depending on the region, suggesting that investors should be more concerned about the possibility of additional lockdown events than they should be about the after-effects of the first wave of infections (more on this below). Will Fiscal Multipliers Be High Or Low? When examining the academic literature on fiscal multipliers, the first impression is that multipliers are likely to be extremely large in the current environment. Tables II-2 and II-3 present a range of academic multiplier estimates aggregated by the IMF, categorized by the stage of the business cycle and whether the zero lower bound is in effect. Table II-2Fiscal Multipliers Are Much Larger During Recessions Than Expansions

May 2020

May 2020

Table II-3Models Suggest The Multiplier Is Quite High At The Zero Lower Bound

May 2020

May 2020

The tables tell a clear story: multipliers are typically meaningfully larger during recessions than during expansions, and extremely large when the zero lower bound (ZLB) is in effect. However, there are at least two reasons to expect that the fiscal multiplier during this crisis will not be as large as Tables II-2 and II-3 suggest. First, it is obviously the case that the multiplier will be low while full or even partial lockdowns are in effect, as consumers will not have the ability to fully act in response to stimulative measures. This will be partially offset by a burst of spending once lockdowns are removed, but the empirical multiplier estimates during recessions shown in Table II-2 have not been measured during a period when constraints to spending have been in effect, and we suspect that this will have at least somewhat of a dampening effect on the efficacy of fiscal spending relative to previous recessions (even once regulations concerning store closures are removed). Second, Table II-3 likely overestimates the multiplier at the ZLB. These estimates have been based on models rather than empirical analysis, and appear to be in reference to the prevention of large subsequent declines in output following an initial shock. The modeled finding of a large multiplier at the ZLB occurs because increased deficit spending will not lead to higher policy rates in a scenario where the neutral rate has fallen below zero. But it seems difficult to believe that the fiscal multiplier during ZLB episodes, defined as the impact of fiscal spending on the path of output relative to the initial shock (not relative to a counterfactual additional shock), is larger than the highest empirical estimates of the multiplier during recessions. The only circumstance in which we can envision this being the case is an environment where long-term bond yields are capped and remain at zero, alongside short-term interest rates, as the economy improves. The IMF has provided a simple rule of thumb approach to estimating the fiscal multiplier for a given country. The IMF’s approach involves first estimating the multiplier under normal circumstances based on a series of key structural characteristics that have been shown to influence the economy’s response to fiscal shocks. Then, the “normal” multiplier is adjusted higher or lower depending on the stage of the business cycle, and whether monetary policy is constrained by the ZLB. For the US, the IMF’s approach suggests that a multiplier range of 1.1 – 1.6 is reasonable, assuming the highest cyclical adjustment but no ZLB adjustment (see Box II-1 for a description of the calculation). Given the unprecedented nature of this crisis, we are inclined to use the low end of this range (1.1) as a conservative assumption when judging whether fiscal responses to the crisis are sufficient. For investors, this means that governments should be aiming, at a minimum, for fiscal packages that are roughly 90% of the size of the expected shock of their economies, using our US fiscal multiplier assumption as a guide. Box II-1 The “Bucket” Approach To Estimating Fiscal Multipliers The IMF “bucket” approach to estimating fiscal multiplier involves determining the multiplier that is likely to apply to a given country during “normal” circumstances, based on a set of structural characteristics associated with larger multipliers. This “normal” multiplier is then adjusted based on the following formula: M = MNT * (1+Cycle) * (1+Mon) Where M is the final multiplier estimate, MNT is the “normal times” multiplier derived from structural characteristics, Cycle is the cyclical factor ranging from −0.4 to +0.6, and Mon is the monetary policy stance factor ranging from 0 to 0.3. The Cycle factor is higher the more a country’s output gap is negative, and the Mon factor is higher the closer the economy is to the zero lower bound. Table II-B1 applies the IMF’s approach to the US, using the same structural score as the IMF presented in the note that described the approach. The table highlights that the approach suggests a US fiscal multiplier range of 1.1 – 1.6 given the maximum cycle adjustment proscribed by the rule, which we feel is reasonable given the unprecedented rise in US unemployment. We make no adjustment to the range for the zero lower bound. Table II-B1A Multiplier Estimate Of 1.1 – 1.6 Seems Reasonable For The US

May 2020

May 2020

The Composition Of The Response: Helping Or Hurting? The last of our four questions deals with the issue of composition and whether the form of a country’s fiscal response is likely to alter its effectiveness. We implicitly addressed the first element of composition, whether measures are above-the-line or below-the-line, by comparing Charts II-1 - II-3 on pages 28-31. Our view is that above-the-line measures are far more important than below-the-line measures, as the former provides direct income and liquidity support. Below-the-line measures are also important, as they are likely to help reduce business failure and household bankruptcies. The fiscal multiplier on these measures has to be above zero, but it is likely to be much lower than that of an above-the-line response. The second element of composition concerns the appropriate distribution of aid among households, businesses, and local governments. On this particular question, it remains extremely challenging to analyze the issue on a global basis, owing to a frequent lack of an explicit breakdown of fiscal measures by recipient. Chart II-6Much Of The US Fiscal Response Is Going To Households And Small Businesses

May 2020

May 2020

For now, we limit our distributional analysis to the US, and hope to expand our approach to other countries in future research. Chart II-6 presents a breakdown of the US fiscal response by recipient, which informs the following observations. Households: Chart II-6 highlights that US households will receive approximately $600 billion as part of the CARES Act, roughly half of which will occur through direct payments (i.e. “stimulus checks”) and another 40% from expanded unemployment benefits. In cases where the federal household response has been criticized by members of the public as inadequate, it has often been compared to income support programs of other countries. The Canada Emergency Response Benefit (“CERB”) is a good example of a program that seems, at first blush, to be superior: it provides $2,000 CAD in direct payments to individuals for a 4 week period, for up to 16 weeks (i.e. a maximum of $8,000 CAD), which seems better than a $1,200 USD stimulus check. However, Table II-4 highlights that this comparison is mostly spurious. First, the CERB is not universal, in that it is only available to those who have stopped or will stop working due to COVID-19. At a projected cost of $35 billion CAD, the CERB program represents 1.5% of Canadian GDP. By comparison, $600 billion USD in overall household support represents 2.75% of US GDP; this number drops to 1.75% when only considering support to those who have lost their jobs, but this is still higher as a share of the economy than in Canada. Moreover, there is little question that Congress is prepared to pass more stimulus for additional weeks of required assistance. The discrepancy between the perception and reality of US household sector support appears to be rooted in the speed of payments. Speed is the one area where Canada’s household sector response appears to have legitimately outperformed the US; CERB payments are received by applicants within three business days for those registered for electronic payment, and in some cases they are received the following day. By contrast, it has taken some time for US States to start paying out the additional $600 USD per week in expanded unemployment benefits, but as of the middle of last week nearly all states had started making these payments. Table II-4US Household Relief Is Just As Generous As Seemingly Better Programs

May 2020

May 2020

Firms: On April 16th the Small Business Administration announced that the Paycheck Protection Program (“PPP”) had expended its initial budget of $350 billion. While additional funds of $320 billion have subsequently been approved (plus $60 billion in small business emergency loans and grants), the run on PPP funds was, to some investors, an implicit sign that the CARES Act was inadequately structured. However, the fact that the initial funds ran out in mid-April simply reflects the reality that social distancing measures had been in place for 3-4 weeks by the time that the program began taking applications. Table II-5 highlights that $350 billion was large enough to replace nearly 90% of lost small business income for one month, assuming that overall small business revenue has fallen by 50% and that small businesses account for 44% of total GDP. The Table also shows that a combined total of $730 billion is enough to replace almost 80% of lost small business income for 10 weeks, given these assumptions. With loan forgiveness at least partially tied to small businesses retaining employees on payroll for an 8-week period, the PPP is also essentially an indirect form of household income support. Table II-5Help For Small Businesses Will Replace A Significant Amount Of Lost Income

May 2020

May 2020

Chart II-7Persistent State & Local Austerity Must Be Avoided This Time

Persistent State & Local Austerity Must Be Avoided This Time

Persistent State & Local Austerity Must Be Avoided This Time

State & Local Governments: The magnitude of support for state & local (S&L) governments appears to be the least-well designed element of the US fiscal response. The CARES Act provides for $170 billion in support to S&L, which at first blush seems large as it is approximately 25% of S&L current receipts in Q4 2019 (i.e. it stands to cover a 25% loss in revenue for one quarter). However, this does not account for the significant reported increase in S&L costs to combat the pandemic, nor does it provide S&L governments with any revenue certainty beyond June 30th when most of the assistance from CARES must be spent. Unlike households or firms, who also face significant uncertainty, nearly all US states are subject to balanced budget requirements, which prevent them from spending more than they collect in revenue. When faced even with projected revenue losses in the second half of this year and into 2021, states are likely to aggressively and immediately cut costs in order to avoid budgetary shortfalls. Chart II-7 highlights that S&L austerity was a significant element of the persistent drag on real GDP growth from overall government expenditure and investment in the first 3-4 years of the post-GFC economic expansion. A repeat of this episode would significantly raise the odds of an “L-type” recession (and thus should certainly be avoided). This is why Congress is moving to pass larger state and local aid. Our Geopolitical Strategy team argues that neither President Trump nor Senate Majority Leader Mitch McConnell will prevent the additional financial assistance that US states will require, despite their rhetoric about states going bankrupt.3 A near-term, temporary standoff may occur, but Washington will almost certainly act to provide at least additional short-term funding if state employment starts to fall due to budget pressure. So while we recognize that the state & local component of the US fiscal response is currently lacking, it does not seem likely to represent a serious threat to an eventual economic recovery in the US. Putting It All Together: Will It Be Enough? Chart II-8 reproduces Chart II-3 with an assumed fiscal multiplier of 1.1, and with shaded regions denoting the likely initial and total impact on GDP from aggressive containment measures (based on the OECD and BIS’ estimates). Based on our analysis of the US fiscal response, we make no adjustments for the composition of the measures beyond defining the fiscal response on a narrow basis (i.e. excluding loans, guarantees, and non-specified revenue deferrals). The chart highlights that the narrowly-defined fiscal response of three key economies driving global demand, the US, China, and Germany, is either at the upper end or above the total impact range. Thus, for now, we tentatively conclude that the fiscal response that has or will happen appears to be adequate to prevent the direct and indirect effects of the lockdowns from causing an “L-shaped” event, especially since Chart II-8 explicitly excludes below-the-line measures. However, there are two important caveats to this conclusion. First, Chart II-8 makes it clear that measures in France, Italy, and Spain are still lacking and must be stepped up. Italy and France have provided a substantial below-the-line response, but it is far from clear that a debt-based response or one that only temporarily improves access to cash for households and businesses will be enough to prevent a prolonged fallout from the sudden stop in economic activity and income. Chart II-8Several Important Countries Seem To Be Doing Enough, But More Is Needed In Europe Ex-Germany

May 2020

May 2020

Second, our analysis suggests that the announced fiscal measures will not be sufficient if the global economy faces a W-shaped shock caused by another round of aggressive containment measures later this year or if these measures remain in place at half-strength for many months. This underscores how sensitive the adequacy of announced fiscal measures are to the amount of time economies remain under full or partial lockdown. As such, it is crucial for investors to have some sense of when advanced economies may be able to sustainably end aggressive containment measures. When Can The Lockdowns Sustainably End? Several countries and US states have already announced some reductions in their restrictions, but the question of how comprehensive these measures can be without risking a second period of prolonged stay-at-home orders looms large. Table II-6 presents two different methods of estimating sustainable lockdown end dates for several advanced economies. First, we use the “70-day rule” that appears to have succeeded in ending the outbreak in Wuhan, calculated from the first day that either school or work closures took effect in each country.4 Second, using a linear trend from the peak 5-day moving average of confirmed cases and fatalities, we calculate when confirmed cases and fatalities may reach zero. Table II-6By Re-Opening Soon, The US May Be Risking A Damaging Second Wave

May 2020

May 2020

The table highlights that these methods generally prescribe a reopening date of May 31st or earlier, with a few exceptions. The UK’s confirmed case count and fatality trends are still too shallow to suggest an end of May re-opening, as is the case in Canada. In the case of Sweden, no projections can truly be made based on the 70-day rule because closures never formally occurred. But the most problematic point highlighted in Table II-6 is that US newly confirmed cases are only currently projected to fall to zero as of February 2021. Chart II-9 highlights that while new cases per capita in New York state are much higher than in the rest of the country, they are declining whereas they have yet to clearly peak elsewhere. Cross-country case comparisons can be problematic due to differences in testing, but with several US states having already begun the gradual re-opening process, this underscores that US policymakers may be allowing a dangerous rise in the odds of a secondary infection wave. Chart II-9No Clear Downtrend Yet Outside Of New York State

May 2020

May 2020

Investment Conclusions Our core conclusion that an “L-shaped” global recession is likely to be avoided is generally bullish for equities on a 12-month horizon. However, uncertainty remains extremely elevated, and the recent rise in stock prices in the US (and globally) has been at least partially based on the expectation that lockdowns will sustainably end soon, which at least in the case of the US appears to be a premature conclusion given the current lack of large-scale virus testing capacity. As such, we are less optimistic towards risky assets tactically, and would recommend a neutral stance over a 0-3 month horizon. As noted above, our cross-country comparison of narrowly-defined fiscal measures suggested that euro area countries (excluding Germany) will likely have to do more in order to prevent a long period of below-trend growth. In the case of highly-indebted countries like Italy, this raises the additional question of whether a significantly increased debt-to-GDP ratio stemming from an aggressive fiscal impulse will cause another euro area sovereign debt crisis similar to what occurred from 2010-2014. Chart II-10Italy's Debt Sustainability Hurdle Is Lower Than It Used To Be

Italy's Debt Sustainability Hurdle Is Lower Than It Used To Be

Italy's Debt Sustainability Hurdle Is Lower Than It Used To Be

Government debts are sustainable as long as interest rates remain below economic growth, and from this vantage point Italy should spend as much as needed in order to ensure that nominal growth remains above current long-term government bond yields. Chart II-10 highlights that, despite a widening spread versus German bunds, Italian 10-year yields are much lower today than they were during the worst of the euro area crisis, meaning that the debt sustainability hurdle is technically lower. However, we have also noted in previous reports that high-debt countries often face multiple government debt equilibria; if global investors become fearful that that high-debt countries may not be able to repay their obligations without defaulting or devaluing, then a self-fulfilling prophecy will occur via sharply higher interest rates (Chart II-11). Chart II-11Multiple Equilibria In Debt Markets Are Possible Without A Lender Of Last Resort

May 2020

May 2020

Chart II-12Italy's Structural Budget Balance Has Improved

Italy's Structural Budget Balance Has Improved

Italy's Structural Budget Balance Has Improved

For now, we view the risk of a renewed Italian debt crisis from significantly increased spending related to COVID-19 as minimal, and it is certainly lower than the status quo as the latter risks causing a sharp gap between nominal growth and bond yields like what occurred from 2010 – 2014. First, Chart II-12 highlights that Italy has succeeded in somewhat reducing its structural balance, which averaged -4% for many years prior to the euro area crisis. Assuming an adequate global response to the crisis and that economic recovery ensues, it is not clear why global bond investors would be concerned that Italian structural deficits would persistently widen. Second, the ECB is purchasing Italian government bonds as part of its new Pandemic Emergency Purchase Program, which will help cap the level of Italian yields. Chart II-13Italy's Debt Service Ratio Won't Go Up Much, If Yields Are Unchanged

Italy's Debt Service Ratio Won't Go Up Much, If Yields Are Unchanged

Italy's Debt Service Ratio Won't Go Up Much, If Yields Are Unchanged

Third, Chart II-13 shows what will occur to Italy’s government debt service ratio (general government net interest payments as a percent of GDP) in a scenario where Italy’s gross debt to GDP rises a full 20 percentage points and the ratio of net interest payments to debt remains unchanged. The chart shows that while debt service will rise, it will still be lower than at any point prior to 2015. So not only should Italy spend significantly more to combat the severely damaging nature of the pandemic, we would expect that Italian spreads would fall, not rise, in such an outcome. Jonathan LaBerge, CFA Vice President Special Reports Footnotes 1 Skeptical economists call Japan’s largest-ever stimulus package ‘puffed-up’, Keita Nakamura, The Japan Times, April 8, 2020. 2 Please note that Chart II-3 differs somewhat from a chart that has been frequently shown by our Geopolitical Strategy service. Both charts are accurate; they simply employ different definitions of the fiscal response to the pandemic. 3 Indeed, McConnell has already walked back his comments that states should consider bankruptcy. President Trump is constrained by the election, as are Senate Republicans, and the House Democrats control the purse strings. Hence more state and local funding is forthcoming. At best for the Republicans, there may be provisions to ensure it goes to the COVID-19 crisis rather than states’ unfunded pension obligations. See Geopolitical Strategy, “Drowning In Oil (GeoRisk Update),” April 24, 2020, www.bcaresearch.com. 4 School and work closure dates have been sources from the Oxford COVID-19 Government Response Tracker.

Highlights The global economy will contract at its fastest pace since the early 1930s, but will not slump into a depression. Easy monetary conditions, an extremely expansive fiscal policy, and solid bank and household balance sheets are crucial to the economic outlook. Risk assets remain attractive. The dollar and bonds will soon move from bull to bear markets. The credit market offers some attractive opportunities. Stocks are vulnerable to short-term profit-taking, but the cyclical outlook remains bright. Favor energy and consumer discretionary equities. Feature What a difference a month makes. US and global equities have rallied by 31.4% and 28.3% from their March lows, respectively. Last month we recommended investors shift the weighting of their portfolios to stocks over bonds. April’s dramatic turnaround has not altered our positive view of equities on a 12- to 24-month basis, especially relative to government bonds. However, the probability of near-term profit taking is significant. The spectacular dislocation in the oil market also has grabbed headlines. This was a capitulation event. Hence, assets linked to oil are now cyclically attractive, even if they remain volatile in the coming weeks. It is time to buy energy equities, especially firms with solid balance sheets and proven dividend records. Under the IMF’s base case, the resulting output loss will total $9 trillion. Finally, the Federal Reserve’s large liquidity injections have dulled the dollar’s strength. While the USD still has some upside risk in the near term, investors should continue to transfer capital into foreign currencies. A weaker dollar will be the catalyst to lift Treasury yields and will contribute to the outperformance of energy stocks. Dismal Growth Versus Vigorous Policy Responses Chart I-1Consumer Spending Is In Freefall

Consumer Spending Is In Freefall

Consumer Spending Is In Freefall

The economic lockdowns and the collapse in consumer confidence continue to take their toll on the US and global economies (Chart I-1). The eventual end of the shelter-at-home orders and the progressive re-opening of the economy will halt this trend. The rapid monetary and fiscal easing worldwide will allow growth to recover smartly in the second half of the year, but only after authorities loosen extreme social distancing measures. The Economy Is In Freefall… First-quarter US growth is already as weak as it was at the depth of the recession that followed the Great Financial Crisis. The second quarter will be even more anemic. Our Live-Trackers for both the US and global economies either continue to collapse or have flat-lined at rock-bottom levels (Chart I-2). US industrial production is falling at a 21% quarterly annualized rate and the weakness in the PMI manufacturing survey warns that the worst is yet to come. In March, retail sales contracted by 8.7% compared with February, which was the poorest reading on record, and year-on-year comparisons will only deteriorate further. Annual GDP growth could fall below -11% next quarter with both the industrial and consumer sectors in shock, according to the New York Fed Weekly Economic Index (Chart I-3). Chart I-2No Hope From The Live Trackers

May 2020

May 2020

Chart I-3Real GDP Growth Is Melting

Real GDP Growth Is Melting

Real GDP Growth Is Melting

The IMF expects the recession to eclipse the post GFC-slump, in both advanced and emerging economies. Its most recent World Economic Outlook describes base-case 2020 growth of -5.9%, -7.5%, and -1.0% in the US, Eurozone and emerging markets, respectively. This compares with -2.5%, -4.5% and 2.8% each in 2009. If a second wave of infections forces renewed lockdowns in the fall, then 2020 growth could be 5.12% and 4.49% lower than baseline in developed markets and emerging markets, respectively. Under the IMF’s base case, the resulting output loss will total $9 trillion in the coming 3 years (Chart I-4). Chart I-4An Enormous Output Gap Is Forming

May 2020

May 2020

Chart I-5Disinflation Build-Up

Disinflation Build-Up

Disinflation Build-Up

An output gap of the magnitude depicted by the IMF will dampen inflation for the next 12 to 24 months. In addition to the shortfall in aggregate demand, imploding economic confidence and the lag effect of the Fed’s monetary tightening in 2018 will pull down the velocity of money even further. This combination will reduce US inflation to 1.5% or lower (Chart I-5, top panel). The Price Paid component of both the Philly Fed and Empire State Manufacturing Surveys already captures this impact. The return of producer price deflation in China guarantees that weak US import prices will add to domestic deflationary pressures (Chart I-5 third panel). The recent strength in the dollar will only amplify imported deflation (Chart I-5, bottom panel). A deflationary shock is an immediate problem for businesses and creates a huge risk for household incomes because it exacerbates the already violent contraction in aggregate demand. In the coming months, the weakest nominal GDP growth since the Great Depression will depress profits. BCA Research’s US Equity Strategy team expects S&P 500 operating earnings per share to drop from $162 in 2019 to no further than $104 in 2020.1 The profits of small businesses will suffer even more. Cash flow shortfalls will also cause corporate defaults to spike because many firms will not be able to service their debt (Chart I-6). Currently, 86% of the job losses since the onset of the COVID-19 crisis are temporary. However, if corporate bankruptcies spike too fast and too high, then these job losses will become permanent and household incomes will not recover quickly. A sharp but brief recession would turn into a long depression. Chart I-6Defaults Can Only Rise

Defaults Can Only Rise

Defaults Can Only Rise

…But The Liquidity Crisis Will Not Morph Into A Solvency Crisis… In response to the aggregate demand shock caused by COVID-19, global central banks are supporting lending. These policies are an essential ingredient to flatten the default curve and minimize the permanent hit to employment and household income. The US Fed is acting as the central banker to the world. The US Fed is acting as the central banker to the world. Its new quantitative easing program has already added $1.36 trillion in excess reserves this quarter. Moreover, the Fed’s decision to loosen supplementary liquidity ratios and capital adequacy ratios allows the interbank and offshore markets to normalize. Meanwhile, the Fed’s swap lines with global central banks have surged by $432 billion since the crisis began. Its FIMA facility also permits central banks to pledge Treasurys as collateral to receive US dollars. These two programs let global central banks provide dollar funding to the private sector outside the US. Chart I-7Easing Liquidity Stress

Easing Liquidity Stress

Easing Liquidity Stress

The Fed is also supporting the credit market directly. The $250 billion Secondary Market Corporate Facility, the $500 billion Primary Market Corporate Facility and the $600 billion Main Street New Loan and Expanded Loan Facilities, all mean that firms with a credit rating above Baa or a debt-to-EBITDA ratio below 4x can still get funding. Together with the $100 billion Term-Asset-backed Securities Loan Facility, these measures will prevent a liquidity crisis from morphing into a solvency crisis in which healthier borrowers cannot roll over their debt. Such a crisis would magnify the inevitable increase in defaults manyfold. The market is already reflecting the impact of the Fed’s programs. Corporate spreads for credit tiers affected by the Fed’s support are narrowing (Chart I-7). Spreads reflective of liquidity conditions, such as the FRA-OIS gap, the Commercial paper-OIS spread and cross-currency basis-swap spreads, have also begun to normalize. The narrowing of bank CDS spreads demonstrates that unlike the GFC, the current crisis does not threaten the viability of major commercial banks (Chart I-7, bottom panel). Other central banks are doing their share. The Bank of Canada is buying provincial debt to ensure that the authorities directly tasked with managing the pandemic have the ability to do so. The European Central Bank has enacted a QE program of at least EUR1.1 trillion and enlarged the TLTRO facility while decreasing its interest rate, which cheapens the cost of financing for commercial banks. Moreover, the ECB has also eased liquidity and capital adequacy ratios for commercial banks. Last week, it announced that it would also accept junk bonds as collateral, as long as these bonds were rated as investment grade prior to April 7, 2020. …And Governments Are Pulling Levers… Chart I-8Record Fiscal Easing

May 2020

May 2020

Governments, too, are ensuring that private-sector default rates do not spike uncontrollably and doom the economy to a repeat of the 1930s. Policymakers in the G-10 and China have announced larger stimulus packages than the programs implemented in the wake of the GFC (Chart I-8). The US’s programs already total $2.89 trillion or 13% of 2020 GDP. Germany is abandoning fiscal discipline and has declared stimulus measures totaling 12% of GDP. Italy’s package is more modest at 3% of GDP. Even powerhouse China is not taking chances. In addition to a larger fiscal package than in 2008, the reserve requirement ratio stands at 9.5%, the lowest level in 13 years, and the People’s Bank of China cut the rate of interest on excess reserves by 37 basis points to 0.35% (Chart I-9). The last cut to the IOER was in November 2008 and was of 27 basis points. This interest rate easing preceded a CNY4 trillion increase in the stock of credit, which played a major role in the global recovery that began in 2009. Hence, the recent IOER reduction, in light of the decline in loan prime rates and MLF rates, suggests that China is getting ready to boost its economy by as much as in 2008. Chart I-9China Is Pressing On The Gas Pedal

China Is Pressing On The Gas Pedal

China Is Pressing On The Gas Pedal

Among the advanced economies, loan guarantees supplement growing deficits. So far, this protection totals at least $1.3 trillion. While guarantees do not directly boost the income and spending of the private sector, they address the risk of an uncontrolled spike in defaults. Therefore, they minimize the odds that rocketing temporary layoffs will morph into permanent unemployment. Section II, written by BCA’s Jonathan Laberge, addresses the question of fiscal policy and whether the packages announced so far are large enough to fill the hole created by COVID-19. While a deep recession is unavoidable, governments will provide more stimulus if activity does not soon stabilize. … While Banks And Household Balance Sheets Compare Favorably To 2008 Banks and the household sector, the largest agent in the private sector, entered 2020 on stronger footing than prior to the GFC. Otherwise, all the fiscal and monetary easing in the world would do little to support the global economy. If banks were as weak as when they entered the GFC, then monetary stimulus would have remained trapped in the banking system in the form of excess reserves. Both in the US and in the euro area, banks now possess higher capital adequacy ratios than in 2008 (Chart I-10). Moreover, as BCA Research’s US Investment Strategy service has demonstrated, the large cash holdings and low loan-to-deposit ratio of the US banking system reinforces its strength (Chart I-11).2 Thus, banks are unlikely to tighten credit standards for as long as they did after the GFC. Broad money expansion should outpace the post-GFC experience, as the surge in US M2 growth to a post-war record of 16% indicates. Chart I-10Banks Have More Capital Than In 2008…

May 2020

May 2020

Chart I-11...And Have More Cash And Secure Funding

...And Have More Cash And Secure Funding

...And Have More Cash And Secure Funding

Consumers are also in better shape than in 2008. Last December, US household debt stood at 99.7% of disposable income compared with a peak of 136% in 2008. More importantly, financial obligations represented only 15.1% of disposable income, a near-record low. Limited financial obligations suggest that consumer bankruptcies should remain manageable as long as governments help households weather the current period of temporary unemployment (Chart I-12). Meanwhile, household indebtedness in Spain and Ireland has collapsed from 137% to 94% and from 183% to 85% of disposable income, respectively. Italy, despite its structural economic weakness, always sported a low private-sector debt load. A precautionary rise in the savings rate is unavoidable, but it will not match the magnitude of the increase that followed the GFC. The economy will recover quicker than it did following the GFC. The deep recession engulfing the world should not evolve into a prolonged depression because banks and household balance sheets are in a better state than in 2008. While the recovery will be chaotic, the velocity of money will not remain as depressed for as long as it stayed after 2008, which will allow nominal GDP to recover faster than after the GFC. Banks and households will be quicker to lend and borrow from each other than they were after the GFC. Consequently, the collapse in the consumption of durable goods (e.g. cars) has created pent-up demand, but not a permanent downshift in the demand curve (Chart I-13). Chart I-12Robust Household Finances

Robust Household Finances

Robust Household Finances

Chart I-13Households' Pent-Up Demand

Households' Pent-Up Demand

Households' Pent-Up Demand

Bottom Line: The global economy is on track to suffer its worst contraction since the 1930s. However, the combination of aggressive monetary and fiscal stimulus will prevent a rising wave of defaults from swelling to a crippling tsunami that permanently curtails household income. Given that banks and households have stronger balance sheets than in 2008, when governments ease lockdowns, the economy will recover quicker than it did following the GFC. The evolution of any second wave of infection is the crucial risk to this view. The IMF’s forecast indicates that growth will suffer substantial downside relative to its baseline scenario if the second wave is strong and forces renewed lockdowns. In this scenario, the current package of stimulus must be augmented to avoid a depression-like outcome. A big problem for forecasters, is that we do not have a good sense of how the second wave of infections will evolve. Moreover, the ability to test the population and engage in contact tracing will determine how aggressive lockdowns will be. Therefore, we currently have very little visibility to handicap the odds of each path. Investment Implications Low inflation for the next 18 months will allow monetary conditions to stay extremely accommodative. Growth will recover in the second half of 2020, so the window to own risk assets remains fully open as long as we can avoid a second wave of complete lockdowns. The Dollar’s Last Hurrah The US dollar has become dangerously expensive. According to a simple model, the dollar trades at a premium to its purchasing-parity equilibrium against major currencies, which is comparable to 1985 or 2002 when it attained its most recent cyclical tops (Chart I-14). The dollar may not trade as richly against our Behavioral Effective Exchange Rate model, but this fair value estimate has rolled over (Chart I-14, bottom panel). A peak in global policy uncertainty may be the key to timing the start of the dollar’s decline. Policy will prompt downside risk created by the dollar’s overvaluation. The US twin deficit, which is the sum of the fiscal and current account deficits, is set to explode because Washington will expand the fiscal gap by 15~20% of GDP while the private sector will not increase its savings rate at the same pace. If US real interest rates are high and rising, then foreign investors will snap up US liabilities and finance the twin deficit. If real rates are low and falling, then foreigners will demand a much cheapened dollar (which would embed higher long-term expected returns) to buy US liabilities (Chart I-15). Chart I-14The Dollar Is Pricey

The Dollar Is Pricey

The Dollar Is Pricey

Chart I-15Bulging Twin Deficits Are A Worry

Bulging Twin Deficits Are A Worry

Bulging Twin Deficits Are A Worry

Real interest rates probably will not climb, hence the twin deficit will become an insurmountable burden for the dollar. The Fed has not hit its symmetric 2% inflation target since the GFC and will not do so in the next one to two years. As a result, the Fed will not lift nominal interest rates until inflation expectations, currently at 1.14%, return to the 2.3% to 2.5% zone consistent with investors believing that the Fed is achieving its mandate. Thus, real interest rates will decline, which will drag down the USD. Relative money supply trends also point to a weaker dollar in the coming 12 months (Chart I-16). The Fed is easing policy more aggressively than other central banks and US banks are better capitalized than European or Japanese ones. Therefore, US money supply growth should continue to outpace foreign money supply. The inevitable slippage of dollars out of the US economy, especially if the current account deficit widens, will boost the supply of dollars globally relative to other currencies. Without any real interest rate advantage, the USD will lose value against other currencies. China’s policy easing is also negative for the dollar. China’s large-scale stimulus will allow the global industrial cycle to recover smartly in the second half of 2020, especially if the increase in pent-up demand fuels realized demand in the fall. The US economy’s closed nature and low exposure to both trade and manufacturing will weigh on US internal rates of return relative to the rest of the world, and invite outflows (Chart I-17). This selling will accentuate downward pressure created by the aforementioned balance of payments and policy dynamics. Chart I-16Money Supply Trends Will Hurt The Dollar

Money Supply Trends Will Hurt The Dollar

Money Supply Trends Will Hurt The Dollar

Chart I-17The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

The dollar is also vulnerable from a technical perspective. A record share of currencies is more than one-standard deviation oversold against the USD (Chart I-18). According to the Institute of International Finance (IIF), outflows from EM economies have already eclipsed their 2008 records, and the underperformance of DM assets suggests that portfolio managers have aggressively abandoned non-USD assets. These developments imply that investors who wanted to move money back into the US have already done so. Chart I-18The Dollar Is Becoming Overbought

The Dollar Is Becoming Overbought

The Dollar Is Becoming Overbought

Chart I-19The Dollar Is A Momentum Currency

May 2020

May 2020

Investors should move funds out of the dollar, but not aggressively. The outlook for the dollar in the next year or two is poor, but the USD’s most important tailwind is intact: the global economy will recover, but for the time being, it remains in freefall. Moreover, among the G-10 currencies, the dollar responds most positively to the momentum factor (Chart I-19), which remains another tailwind. The greenback will remain volatile in the coming weeks. EM currencies offer a particularly tricky dilemma. They have cheapened to levels where historically they offer very compelling long-term returns (Chart I-20). However, EM firms have large amounts of dollar-denominated debt. The fall in EM FX and collapse in domestic cash flows will likely cause some large-scale bankruptcies. If a large, famous EM company defaults, then the headline risk would probably trigger a broad-based selling of EM currencies. For now, our Emerging Market Strategy service recommends that, within the EM FX space, investors favor the currencies with the lowest funding needs, such as the RUB, KRW and THB.3 Chart I-20EM FX Is Decisively Cheap

EM FX Is Decisively Cheap

EM FX Is Decisively Cheap

For tactical investors, a peak in global policy uncertainty may be the key to timing the start of the dollar’s decline (Chart I-21). This implies that if a second wave of infections force severe lockdowns, the dollar rally may not be done. Chart I-21Uncertainty Must Recede For The Dollar To Weaken

Uncertainty Must Recede For The Dollar To Weaken

Uncertainty Must Recede For The Dollar To Weaken

Fixed Income Government bonds have not yet depreciated and the exact timing of a price decline remains uncertain. However, Treasurys and Bunds offer an increasingly poor cyclical risk-reward ratio. Bond valuations continue to deteriorate. Our time-tested BCA Bond Valuation model shows that G-10 bonds, in general, and US Treasurys, in particular, are at their most expensive levels since December 2008 and March 1985, two periods that preceded major increases in yields (Chart I-22). Buy inflation-protected securities at the expense of nominal bonds. Liquidity conditions also represent a threat for safe-haven bonds. The wave of liquidity unleashed by global central banks is meeting record fiscal thrust. Thus, not only is the supply of government bonds increasing, but a larger proportion of the money injected by central banks will actually make its way into the real economy than after 2008. Record-low yields are vulnerable because the increase in the global money supply should prevent nominal GDP growth from slumping permanently as in the 1930s and after the GFC. Additionally, the sharp escalation in liquid assets on the balance sheets of commercial banks also creates an additional risk for bond prices (Chart I-23). Chart I-22Bonds Are Furiously Expensive

Bonds Are Furiously Expensive

Bonds Are Furiously Expensive

Chart I-23Liquidity Injections Point To Higher Yields

Liquidity Injections Point To Higher Yields

Liquidity Injections Point To Higher Yields

QE also threatens government fixed income. After the GFC, real interest rates fell because investors understood that US short rates would remain at zero for a long time. Yet, 10-year Treasury yields rose sharply in 2009 as inflation breakevens increased more than the decline in TIPS yields. This pattern repeated itself following each QE wave (Chart I-24). In essence, if the Fed provides enough liquidity to allow markets to function well, then the chance of cyclical deflation decreases, which warrants higher inflation expectations. A lower dollar will be fundamental to the rise in inflation breakeven and yields. A soft dollar will confirm that the Fed is providing enough liquidity to satiate dollar demand and it will favor risk-taking around the world. Moreover, it will boost commodity prices and help realize inflation increases down the line. Chart I-24QE Lifts Breakevens And Yields

QE Lifts Breakevens And Yields

QE Lifts Breakevens And Yields

Technical considerations also point to the end of the bond bull market, at least for the next 12 to 18 months. Investors remain bullish toward bonds, which is a contrarian signal. Our Composite Momentum Indicator has reached levels last achieved at the end of 2008, which suggested at that time that bond-buying was long in the tooth. Chart I-25Inflation Will Drive US/German Spreads

Inflation Will Drive US/German Spreads

Inflation Will Drive US/German Spreads

In this context, investors with a cyclical investment horizon should consider bringing duration below benchmark. In the short term, this position still carries significant risks because the outlook for yields depends on the dollar. Another dollar spike caused by renewed lockdowns would also pin yields near current levels for longer. A lower-risk version of this bet would be to buy inflation-protected securities at the expense of nominal bonds, a position recommended by our US Bond Strategy service.4 Investors should be careful when betting that US yields will further converge toward German ones. The 10-year yield spread between US Treasurys and German Bunds has quickly narrowed, falling by 170 basis points from a high of 279 basis points in November 2018. Despite this sharp contraction, the spread remains elevated by historical standards. So far, the declining yield gap reflects the fall in policy rates in the US relative to Europe. Given that both the Fed and the ECB are at the lower bounds of their policy rates, short-rate differentials are unlikely to compress further. Instead, inflation differentials between the US and Europe must decline (Chart I-25). The inflation gap between the US and Europe probably will not narrow significantly this year. The IMF forecasts that Europe’s economy will underperform the US. Therefore, slack in Europe will expand faster than in the US. Moreover, monetary and fiscal support in the US is more aggressive than in Europe. Consequently, a weaker dollar, which will increase US inflation expectations relative to Europe, will put upward pressure on the US/German 10-year spread. However, if the European fiscal policy response starts to match the size of the US stimulus, then the spread between the US and Germany would narrow further. Ample liquidity also continues to underpin equity prices. Finally, for credit investors, our US Bond Strategy service recommends buying securities with abnormally large spreads and which the various Fed programs target. These include agency CMBS, consumer ABS, municipal bonds, and corporates rated Ba and above.5 Equities Chart I-26Investors Are Not Exuberant About Stocks

Investors Are Not Exuberant About Stocks

Investors Are Not Exuberant About Stocks