Euro Area

Highlights US Corporates: The Fed continues to expand the reach of its extraordinary monetary policies designed to combat the COVID-19 recession, now giving itself the ability to hold BB-rated US high-yield bonds within its corporate bond buying programs. Raise allocations to US BB-rated corporates to overweight, within a neutral overall strategic (6-12 months) allocation to US high-yield. Euro Area Corporates: European investment grade corporate debt has seen significant spread widening over the past month, but spreads have stabilized with the ECB introducing a new asset purchase program with fewer restrictions. Upgrade euro area investment grade corporates to neutral from underweight on both a tactical (0-6 months) and strategic (6-12 months) basis. Favor debt from beaten-up sectors that are already priced for severe economic weakness like Energy, Transportation and non-bank Financials. Central Banks Are A Corporate Bond Investor’s Best Friend Right Now Chart of the WeekThe Fed & ECB Are Supporting Bond Markets

The Fed & ECB Are Supporting Bond Markets

The Fed & ECB Are Supporting Bond Markets

The actions of policymakers worldwide to help mitigate the severe economic shock from the COVID-19 recession have helped boost global risk assets over the past couple of weeks. This is particularly notable in US corporate bond markets, where credit spreads have tightened for both shorter-maturity investment grade bonds and Ba-rated high-yield (Chart of the Week). It is not a coincidence that those are the parts of the US corporate bond market that the Fed is now explicitly backstopping through its off-balance-sheet investment programs. Last week, the Fed unveiled yet another “bazooka” to help ease US financial conditions, broadening the scope of its previously investment grade-only corporate bond purchase programs to include Ba-rated high-yield corporate bonds and high-yield ETFs. In Europe, meanwhile, the European Central Bank (ECB) is also providing additional monetary support through increased asset purchases of both government and corporate debt. Those purchases are focused more on the weakest links in the euro area financial and economic chain like Italian sovereign bonds. This has helped to stabilize credit spreads for both Italian government bonds and euro area investment grade corporate debt. This support from policymakers is critical to prevent a further tightening of financial conditions during a severe global recession (Chart 2). The excess return (over government bonds) for the Bloomberg Barclays global high-yield bond index is now down 15% on a year-over-year basis. High-yield corporate bond spreads are well above the lows seen earlier this year on both sides of the Atlantic, across all credit quality tiers. In the US, spreads between credit quality tiers had widened to levels not seen in several years. Within the US investment grade universe, the gap between Baa-rated and Aa-rated spreads had widened from 20bps to 60bps (Chart 3), a level last seen in September 2011, but now sits at 39bps. Chart 2Junk Bonds Already Discount A Big Recession

Junk Bonds Already Discount A Big Recession

Junk Bonds Already Discount A Big Recession

Chart 3The Fed Wants These Spreads To Tighten

The Fed Wants These Spreads To Tighten

The Fed Wants These Spreads To Tighten

Looking in the other direction of the credit quality spectrum, the spread between Baa-rated and Ba-rated corporates – the line of demarcation between investment grade and high-yield bonds – had blown out from 132bps in February to 556bps, but is now at 360bps. This is the market pricing in the growing risk of fallen angels being downgraded from investment grade to junk. In our view, the Ba-Baa spread is the best indicator to follow to see if the Fed’s extension of its bond purchase program to high-yield is working to reduce borrowing costs for lower-rated US companies. Both in the US and Europe, we continue to recommend a credit investment strategy that favors the parts of the markets that the Fed and ECB are most directly involved in now. That means staying overweight US investment grade corporate bonds with maturities of less than five years (the Fed’s maturity limit for its bond buying program). It also means staying overweight Italian government debt versus core European equivalents. The Fed’s new extension into high-yield corporates within its buying programs means we need to upgrade our recommendation on US BB-rated high-yield to overweight within our recommended neutral strategic (6-12 months) allocation to US junk bonds. We are making that change on a tactical basis in our model bond portfolio, as well, as can be seen on pages 14-15. As the title of this Weekly Report suggests, buy what the central banks are buying. The Fed’s new extension into high-yield corporates within its buying programs means we need to upgrade our recommendation on US BB-rated high-yield to overweight within our recommended neutral strategic (6-12 months) allocation to US junk bonds. In Europe, there is now scope to also raise allocations to euro area corporate bonds, as well, as we discuss over the remainder of this report. Bottom Line: The Fed continues to expand the reach of its extraordinary monetary policies designed to combat the COVID-19 recession, now giving itself the ability to hold BB-rated US high-yield bonds within its corporate bond buying programs. Raise allocations to US BB-rated corporates to overweight within a neutral overall strategic (6-12 months) allocation to US high-yield. Looking For Value In Euro Area Investment Grade Bonds The outlook for euro area spread product does not have as clean-cut a story as is the case for US credit. The ECB is not explicitly supporting European corporate credit markets to the same degree as the Fed is with its open-ended off-balance sheet investment vehicles. While the ECB has introduced a new large €750bn asset purchase program, the Pandemic Emergency Purchase Program (PEPP), to help ease financial conditions in the euro area, no specific details have yet been provided specifying how much of the PEPP will go towards corporate debt versus sovereign bonds. The ECB has already loosened the country and issuer limit restrictions it has imposed on its existing Asset Purchase Program (APP), however, which means that the central bank will be very flexible with the PEPP purchases. That means helping reduce sovereign risk premiums in Peripheral Europe by buying greater amounts of Italian, Spanish and even Greek government debt. That also likely means buying more corporate debt in the most stressed sectors of the euro area economy, as needed. Greater ECB bond purchases would make euro area investment grade credit – which has seen some value restored after the recent bout of spread widening - more attractive over both tactical and strategic investment horizons. This is true even with much of the euro area now in a deep recession because of COVID-19 lockdowns, which has already been discounted in the poor investment performance of euro area corporates. Greater ECB bond purchases would make euro area investment grade credit – which has seen some value restored after the recent bout of spread widening - more attractive over both tactical and strategic investment horizons. Year-to-date, euro area corporate credit markets have been hit hard by the global credit selloff (Table 1). In total return terms denominated in euros, the Bloomberg Barclays euro area investment grade corporate bond index is down -5.0% so far in 2020. The numbers are slightly better relative to duration-matched euro area government bonds (the pure credit component), with the index excess return down -5.5% year-to-date. At the broad sector level, the laggards so far in 2020 have been the sectors most exposed to the sharp downturn in European (and global) economic growth. In excess return terms, the worst performing sectors year-to-date within the eleven major groupings shown in Table 1 have been Consumer Cyclicals (-8.5%), Transportation (-8.1%), Energy (-7.2%). The best performing sectors are those that would be categorized as less cyclical and more “defensive”, like Utilities (-4.3%), Technology (-4.3%) and Financials (-4.7%). In many ways, this is a mirror image of 2019, when Consumer Cyclicals and Transportation were among the top performers while Technology was the worst performer. Table 1Euro Area Investment Grade Corporate Bond Returns

Buy What The Central Banks Are Buying

Buy What The Central Banks Are Buying

Chart 4Euro Area Corporate Spreads Are Relatively Subdued Vs. Past Credit Cycles

Euro Area Corporate Spreads Are Relatively Subdued Vs. Past Credit Cycles

Euro Area Corporate Spreads Are Relatively Subdued Vs. Past Credit Cycles

When looking at the differences in spreads between credit tiers in the euro area, the gaps are not as wide as in the US (Chart 4). The index spread on Baa-rated euro area corporates is only 44bps above that of Aa-rated credit, far below the 100bps gap seen at the peak of the 2001 and 2011 spread widening episodes and well below the 200bps witnessed in 2008. Looking at the difference between Ba-rated and Baa-rated euro area spreads paints a similar picture, with the gap between the highest high-yield credit tier and lowest investment grade credit tier now sitting at 297bps after getting as wide as 431bps in late March – close to the 500bps peak seen in 2011 but far below the 1000bps levels seen in 2001 and 2007 The broad conclusion looking strictly at credit tiers is that euro area corporates have cheapened up a bit during the COVID-19 selloff, but on a more modest scale compared to previous euro area credit cycles. A similar conclusion is reached when looking at industry-level credit spreads. The broad conclusion looking strictly at credit tiers is that euro area corporates have cheapened up a bit during the COVID-19 selloff, but on a more modest scale compared to previous euro area credit cycles. A similar conclusion is reached when looking at industry-level credit spreads. In Charts 5 & 6, we show the history of option-adjusted spreads (OAS) for the major industrial sub-groupings of the Bloomberg Barclays euro area investment grade corporate indices. Unsurprisingly, spreads look relatively wide for the biggest underperforming sectors like Energy, Consumer Cyclicals and Transportation. The spread widening has been more contained in the better performing sectors like Technology. Chart 5A Mixed Performance For Euro Area Investment Grade Spreads By Industry …

A Mixed Performance For Euro Area Investment Grade Spreads By Industry ...

A Mixed Performance For Euro Area Investment Grade Spreads By Industry ...

Chart 6…. With Spreads Well Below 2001 And 2008 Credit Cycle Peaks

... With Spreads Well Below 2001 And 2008 Credit Cycle Peaks

... With Spreads Well Below 2001 And 2008 Credit Cycle Peaks

When looking at the individual country corporate bond indices within the euro area, the current levels of spreads do not look particularly wide in an historical context. In Chart 7, we show a bar chart of the range of index OAS for the six largest euro area countries (Germany, France, Italy, Spain, the Netherlands, Belgium and Austria). The current OAS is shown within that historical range. The chart shows that current spreads are in the middle of that range for most countries, suggesting some better value has been restored by the COVID-19 selloff but with spreads remaining relatively subdued compared to past euro area credit cycles.1 Chart 7Euro Area Investment Grade Corporate Spreads By Country

Buy What The Central Banks Are Buying

Buy What The Central Banks Are Buying

On a relative basis, investment grade spreads are tightest in France (203bps), the Netherlands (202bps) and Belgium (226bps), and widest in Germany (255bps), Italy (255bps), Austria (251bps) and Spain (234bps). With the ECB already promising greater flexibility in the country allocations of its sovereign bond purchases within the PEPP, Italian corporates may offer the best value within the major euro area countries. With the ECB already promising greater flexibility in the country allocations of its sovereign bond purchases within the PEPP, Italian corporates may offer the best value within the major euro area countries. We can get a better sense of relative corporate bond spread valuation at the country level by looking at the 12-month breakeven spread percentile rankings of those spreads. This is one of the tools we use to assess value in global credit spreads, as measured by historical “spread cushions”. Specifically, we calculate how much spread widening is required over a one-year horizon to eliminate the yield advantage of owning corporate bonds versus duration-matched government debt. We then show those breakeven spreads as a percentile ranking versus its own history, to allow comparisons over periods with differing underlying spread volatility. In Charts 8 & 9, we show the 12-month breakeven spread percentile rankings for Germany, France, Italy, Spain, Belgium and Austria. On this basis, the current level of spreads looks most historically attractive in Germany, Italy and France, with the breakeven spread in the upper quartile versus its history dating back to the year 2000. Spreads in Spain, Belgium and Austria also look relatively wide versus their own history, but to a lesser extent than in Germany, France and Italy. Chart 8German, Italian & French Investment Grade Corporates Offer Better Value On A Breakeven Spread Basis ….

German, Italian & French Investment Grade Corporates Offer Better Value On A Breakeven Spread Basis ...

German, Italian & French Investment Grade Corporates Offer Better Value On A Breakeven Spread Basis ...

Chart 9… Than Spanish, Belgian & Austrian Investment Grade Corporates

Buy What The Central Banks Are Buying

Buy What The Central Banks Are Buying

Chart 10Euro Area Investment Grade Corporate Spreads Are Relatively Wide Across All Credit Tiers

Euro Area Investment Grade Corporate Spreads Are Relatively Wide Across All Credit Tiers

Euro Area Investment Grade Corporate Spreads Are Relatively Wide Across All Credit Tiers

So while there are some modest differences in value to exploit within the euro area investment grade corporate bond universe at the country level, there is less to choose from across credit tiers. The 12-month breakeven spreads for Aaa-rated, Aa-rated, A-rated and Baa-rated euro area corporates are all within the upper quartiles of their own history (Chart 10). One other tool we can use to assess value across euro area investment grade corporates is our sector relative value framework. Borrowing from the methodology used by our colleagues at BCA Research US Bond Strategy to assess US investment grade corporates, the sector relative value framework determines “fair value” spreads for each of the major and minor industry level sub-indices of the overall euro area investment grade universe. The methodology takes each sector's individual OAS and regresses it in a cross-sectional regression with all other sectors. The independent variables in the model are each sector's duration, trailing 12-month spread volatility, and credit rating - the primary risk factors for any corporate bond. Using the common coefficients from that regression, a risk-adjusted "fair value" spread is calculated. The difference between the actual OAS and fair value OAS is our valuation metric used to inform our sector allocation ranking. The latest output from the euro area relative value spread model can be found in Table 2. We also show the duration-times-spread (DTS) for each sector in those tables, which we use as the primary way to measure the riskiness (volatility) of each sector. The scatterplot in Chart 11 shows the tradeoff between the valuation residual from our model and each sector's DTS. Table 2Euro Area Investment Grade Corporate Sector Valuation & Recommended Allocation

Buy What The Central Banks Are Buying

Buy What The Central Banks Are Buying

We can then apply individual sector weights based on the model output and our desired level of overall spread risk to come up with a recommended credit portfolio. The weights are determined at our discretion and are not the output from any quantitative portfolio optimization process. The only constraints are that all sector weights must add to 100% (i.e. the portfolio is fully invested with no use of leverage) and the overall level of spread risk (DTS) must equal our desired target. The strongest overweight candidates (a DTS score equal to or greater than that of the overall index with the highest positive valuation residual) are the following euro area investment grade sectors: Packaging, Tobacco, Other Industrials, Media Entertainment, Supermarkets, Integrated Energy, Consumer Cyclical Services and all non-bank Financials (Insurance, REITs, Brokerages and Finance Companies). Against the current backdrop of euro area corporate spreads offering relatively wide spreads on a breakeven spread basis, and with the ECB providing a highly accommodative monetary backdrop that includes more purchases of both government and corporate debt, we think targeting an overall portfolio DTS greater than that of the euro area investment grade corporate bond index is reasonable. On that basis, we are looking to go overweight sectors with relatively higher DTS and positive risk-adjusted spread residuals from our relative value model (and vice versa). Those overweight candidates would ideally be located in the upper right quadrant of Chart 11. Chart 11Euro Area Investment Grade Corporate Sectors: Valuation Versus Risk

Buy What The Central Banks Are Buying

Buy What The Central Banks Are Buying

Based on the latest output from the relative value model, the strongest overweight candidates (a DTS score equal to or greater than that of the overall index with the highest positive valuation residual) are the following euro area investment grade sectors: Packaging, Tobacco, Other Industrials, Media Entertainment, Supermarkets, Integrated Energy, Consumer Cyclical Services and all non-bank Financials (Insurance, REITs, Brokerages and Finance Companies). The least attractive sectors within this framework (negative risk-adjusted valuations) are: Senior Bank Debt, Natural Gas, Other Utilities, Metals and Mining, Chemicals, Construction Machinery, Lodging, Cable and Satellite, Restaurants, Food/Beverage, Health Care, Oil Field Services, Building Materials and Aerospace/Defense. Bottom Line: European investment grade corporate debt has seen significant spread widening over the past month, but spreads should stabilize with the ECB introducing a new asset purchase program with fewer restrictions. Upgrade euro area investment grade corporates to neutral from underweight on both a tactical (0-6 months) and strategic (6-12 months) basis. Favor debt from beaten-up sectors that are already priced for severe economic weakness like Energy, Transportation and non-bank Financials. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 For the Netherlands, there is a much shorter history of corporate bond index data available from Bloomberg Barclays than the other euro area countries shown in Chart 7. The OAS range only encompasses about seven years of data, while the other countries go back as far as the early 2000s. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Buy What The Central Banks Are Buying

Buy What The Central Banks Are Buying

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

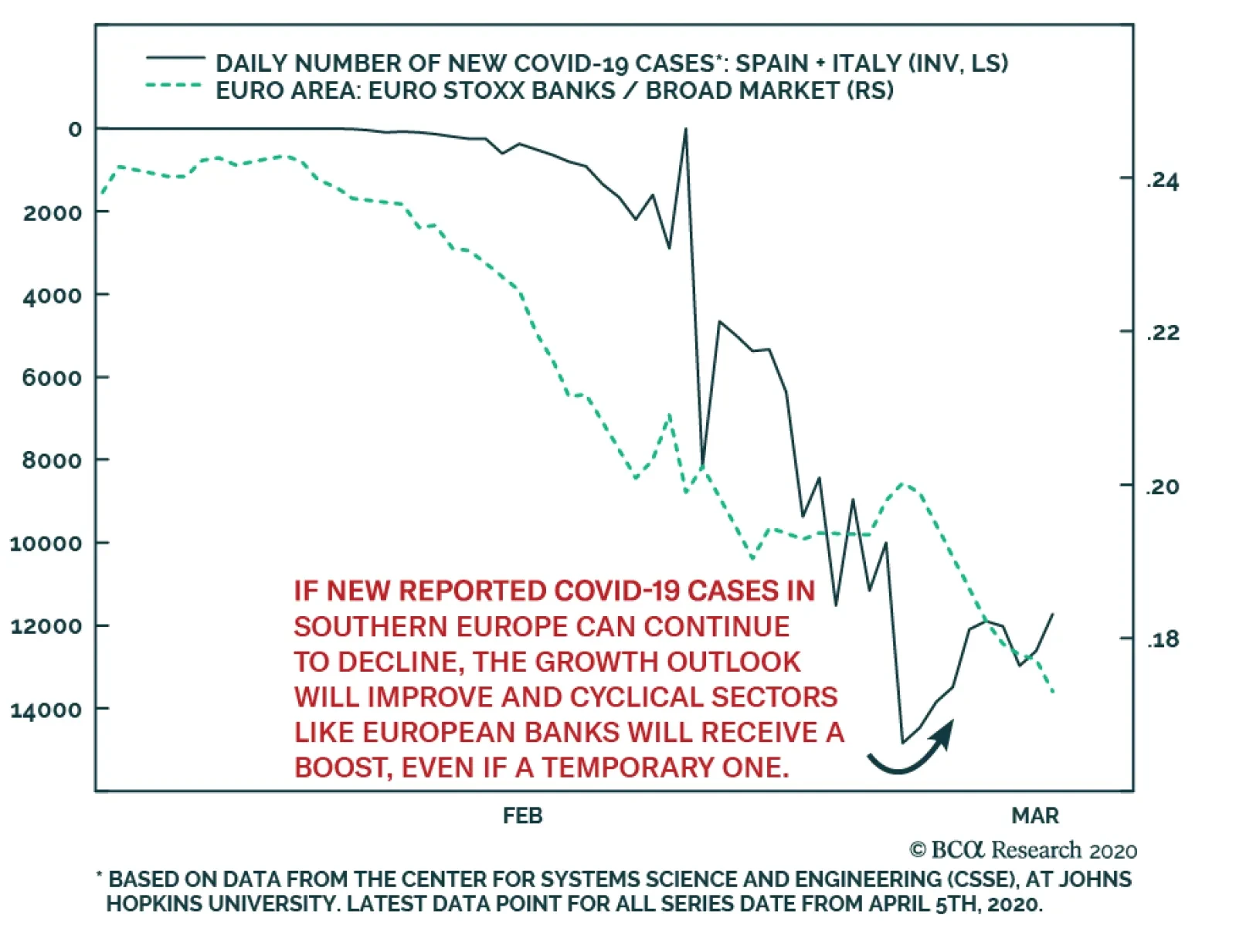

Highlights The near-term is fraught with risk for US equities and global risk assets. Investors concerned over uncertainty, a slow recovery, and economic aftershocks must also guard against geopolitics. COVID-19 is not a victory for dictatorship over democracies. Democracies face voters and will ultimately improve government effectiveness. President Trump is likely to lose the US election. As this becomes increasingly likely, his policy will turn more aggressive, increasing geopolitical risks – particularly in US-China relations. Stay short CNY-USD. Stay long defense stocks. Feature Chart 1Another Downdraft Is Likely

Geopolitics Is The Next Shoe To Drop

Geopolitics Is The Next Shoe To Drop

US equity prices have risen 26% since their March 23 low point, but our review of systemic global crises suggests that a re-test of the bottom would not be surprising (Chart 1). A range of mitigating health policies – plus still-growing policy stimulus – will most likely prevent a depression. But a longer than expected economic trough, due to some persistent level of social distancing pre-vaccine, and negative second-order effects, such as emerging market crises, could trigger another wave of selling. Moreover we expect another shoe to drop: geopolitics. A Light At The End Of The Tunnel Governments are starting to get a handle on the COVID-19 pandemic. The number of daily new cases in the European Union, which is most clearly correlated with global equities, has subsided (Chart 2). Chart 2Any Setbacks Will Hit Equity Market Hard

Any Setbacks Will Hit Equity Market Hard

Any Setbacks Will Hit Equity Market Hard

The US is also seeing new cases crest. To be safe one should count on a subsidiary spike that could easily set back US equities after a notable stock market rally (Chart 2, second panel). But Europe has shown that social distancing works, which US investors will recognize. Italy’s Prime Minister Giuseppe Conte is expected to begin the gradual loosening of social controls to restart the economy. Since Italy is the hardest hit of the western nations (second only to Spain), its leaders will not relax lockdown measures unless they are sure they can do so safely (Chart 2, bottom panel). Still, if governments loosen controls too soon, they may have to tighten them again. Uncertainty will therefore persist regarding the pace of economic normalization, which is bound to be slow due to the fact that discretionary spending will remain suppressed, as it is today in China, and the special precautions that at-risk populations like the elderly will have to take. Economic stimulus measures are still growing in size. Japan’s stimulus, which we count at 16% of GDP, is smaller than the headline 20% but still very large. We have long argued that Japan was on the forefront of the move toward debt monetization among developed markets, but COVID-19 has accelerated the paradigm shift. The United Kingdom has now explicitly stated that the Bank of England will directly finance government debt. The Spanish government is proposing Universal Basic Income (UBI), which it hopes to make permanent, rather than merely for the duration of the pandemic. The jury is still out on whether the weak Pedro Sanchez government will be able to pass it but the current is in favor of “whatever it takes.” Italy’s Five Star Movement has long advocated universal basic income and is part of a ruling coalition that has received a wave of popular support to combat the crisis. At present only a more limited “income of emergency” is being legislated, in keeping with the more centrist Democratic Party, a coalition partner. But Italy’s devastation creates the impetus for bolder moves, either by this government or a subsequent government in 2021 or after. The European institutions are backstopping these states, at least for now, so any deeper disagreements about climbing down from stimulus will have to wait until the coming years. The EU itself is likely to announce additional fiscal measures, via the European Stability Mechanism, whose austerity requirements will be waived, and the European Investment Bank. We can see a token agreement on “coronabonds” (joint debt issuance by the Euro Area), but investors should not fixate on the eurobond debate. These would require a new mechanism, which is inexpedient, whereas the existing mechanisms are already sufficient to bankroll the huge deficit spending plans that the member states are already rolling out. The United States is negotiating an additional “phase four” package that could range between $500 billion and $2 trillion, meaning anywhere from 2.5% to 10% of GDP in new measures (Chart 3). Our estimate would err on the high side because it will largely consist of the same key elements as the “phase three” $2.3 trillion package: unemployment benefits and cash to households, plus a larger dollop for local governments than in the last package. Chart 3Fiscal Tsunami Is Still Building

Geopolitics Is The Next Shoe To Drop

Geopolitics Is The Next Shoe To Drop

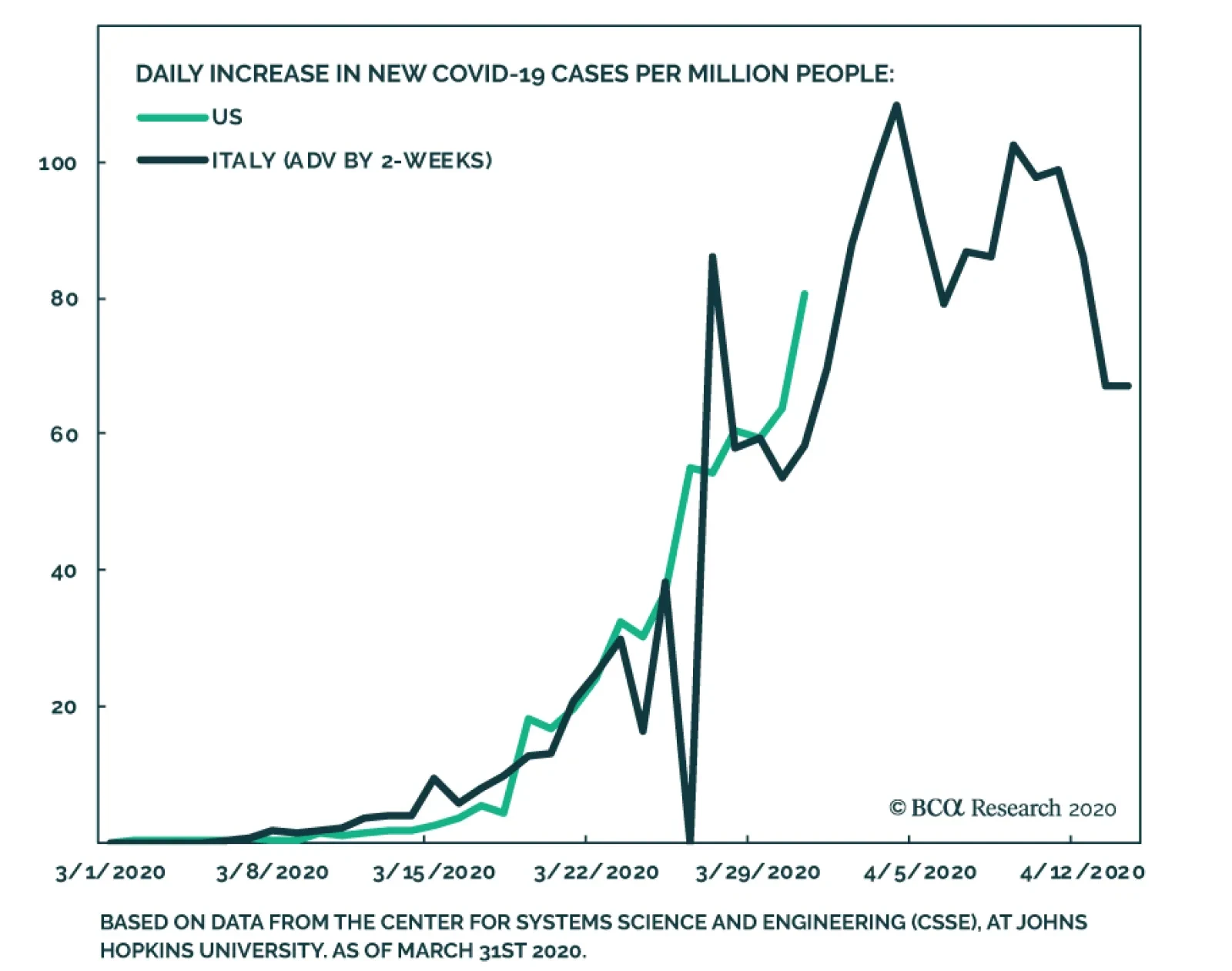

Congress is scheduled to return to vote the week of April 20, but an early return is entirely possible if the pandemic worsens. If the infection curve is flattening, then Republican Senators may hold out longer in negotiations. Squabbling would cause temporary agitation in equity markets. The Democrats and the Republicans still have a mutual interest in spending profusely: the Republicans to try to salvage their seats through economic improvement by November; the Democrats to prove their election proposition that a larger role for government is necessary. Finally, China is preparing to announce more stimulus. So far Chinese measures amount to only 3% of GDP but this is insufficient given the weakness in China’s economic rebound thus far. The expansion in quasi-fiscal spending (government-controlled credit expansion) is an open question, but we would guesstimate a minimum of 3% of GDP. Dramatic measures should be expected because China is undergoing the first recessionary environment since the Cultural Revolution and President Xi Jinping risks a monumental economic destabilization if he hesitates to shore up aggregate demand, which would ultimately threaten single-party rule. We see little chance of him making this mistake. The problem is that animal spirits and external demand will remain weak regardless, an occasion for disappointments among bullish equity investors. Moreover US-China geopolitical risks are rising again, as discussed below. Our updated list of fiscal measures for 25 countries can be found in the Appendix. Bottom Line: The pandemic is peaking in the US and EU, while more stimulus is coming. This is positive for equity investors with a 12-month time frame but the near-term remains vulnerable to another selloff. Democracies Are Not Less Effective Than Dictatorships The pandemic has given rise to wildly misleading narratives in the financial community and mainstream media about the political ramifications for different nations. Getting these narratives right is important for one’s investment strategy. The most popular is that China “won” – is expanding its global influence – while the United States “lost” – is failing at global leadership. More broadly the authoritarian eastern model is said to be triumphing over the western democratic model. The real distinction among states is whether they were familiar with pandemics emanating from China, the unreliability of China’s transparency and communications, and the need to track and trace infections from the beginning. Thus South Korea, Taiwan, Singapore, Vietnam, and Japan have all had relatively benign experiences and all but Vietnam are democracies, with varying degrees of representation and contestation. Nor is COVID-19 an “eastern” versus “western” thing. Germany did an effective job testing, tracking, and tracing infections as well. Germans are relatively law-abiding and trust Chancellor Angela Merkel and the state governments to “do the right thing.” Canada, with its experience of SARS, has also reacted effectively. Denmark, Austria, and the Czech Republic are already tentatively reopening their economies. Yet the number of new confirmed cases per million people shows that Germany is not wildly different from the US and Italy (Chart 4). The truth is that Italy’s bad fortune alerted the US and G7 states to take the threat more seriously – the US has had good outcomes in Washington State but bad outcomes in highly populated New York. Nor is it true that the American health care system is uniquely terrible in treating patients, as is so widely claimed. US deaths per million are worse than Germany but better than Italy (Chart 5) – and Italy’s health system is also not to blame. Failure of ruling parties to spring into decisive action is the main differentiator. Chart 4US In Line With Italy In New Cases …

Geopolitics Is The Next Shoe To Drop

Geopolitics Is The Next Shoe To Drop

Chart 5… But Better In Limiting Deaths

Geopolitics Is The Next Shoe To Drop

Geopolitics Is The Next Shoe To Drop

Chart 6Dictatorships Good At Halting Freedoms

Geopolitics Is The Next Shoe To Drop

Geopolitics Is The Next Shoe To Drop

Dictatorships have had fewer cases and deaths, if their statistics can be trusted – which is a big if.1 This does not suggest that their governance model is better, but rather that they are better at halting freedoms, such as free movement (Chart 6). North Korea has zero cases of COVID-19. People were already under lockdown. Variation within the dictatorships stems from their policy responses and experience fighting pandemics. China, the origin of several recent outbreaks, has extensive experience. It also has a functional health system, fiscal resources, and a heavily centralized power structure. Iran, however, has less experience and capability. The question now is Russia, which was slow to react and has a growing outbreak, yet has a heavily centralized power structure to flatten the curve. Incidentally domestic risk is an important reason for Russia to cooperate with OPEC on oil production cuts, as we have argued. These points can be demonstrated by comparing COVID-19 deaths per million to each nation’s health capabilities and underlying vulnerability to the disease. Note that our intention is to highlight the role of policy in outcomes, not to attempt a full explanation of an epidemiological phenomenon. In Chart 7A, we judge health capacity by health spending per head and life expectancy at the age of 60. Nations that spend a lot per person, and whose people live longer, have better health systems. Yet many of these states are seeing the highest number of deaths because they are European and Europe was the epicenter of the outbreak. Chart 7ARich, Healthy Countries Got Hit Hardest Because Unprepared

Geopolitics Is The Next Shoe To Drop

Geopolitics Is The Next Shoe To Drop

The US ranks right along with Germany and Sweden.2 Policy responses – early testing, tracking, and tracing – explain why South Korea has far fewer deaths than Italy and Spain on a population-weighted basis. However, the underlying conditions still matter, as the US’s health system, travel bans, and distance from the crisis produced better outcomes than its other policy responses would have implied. These data will be more accurate once the infection curve has flattened across the world. The situation is changing rapidly. If the US rises up in deaths per capita, it will be because of its slow responses, or subsequent policies. The same goes for emerging market economies that are ranking low in deaths but either have not seen the full effect of the pandemic, or had more time to adjust policy due to the crisis in Europe. Emerging market economies have lower health capacity, but also younger and hence healthier populations. The older the society, and the higher proportion of severe illnesses like heart and lung disease, the more susceptible to COVID-19 deaths, as Chart 7B shows. But yet again, the policy response still proves decisive. China has more deaths than some countries that are more vulnerable, because it got hit first. If Brazil and Turkey rise higher and higher above China in deaths, as is likely, it is because of policy failure, not basic vulnerability. Chart 7BEurope And US: Vulnerable Populations, Governments Slow To React

Geopolitics Is The Next Shoe To Drop

Geopolitics Is The Next Shoe To Drop

Russia stands out as especially vulnerable in this Chart 7B. Here is where authoritarian measures may pay off, as with China, but only in the short term – since Russia will still be left with an elderly population highly prone to severe illness and a creaking health system. As mentioned above, the risk to Russian stability is a factor pushing for geopolitical cooperation in oil market cartel behavior to push prices up and improve the fiscal outlook to enable better domestic stability management. Bottom Line: Government policy, particularly preparedness and rapid action, have been the decisive factors in containing COVID-19, not dictatorial or democratic government types. The richest countries have the most freedoms and the most vulnerable elderly demographics. Within the rich countries, southern Europe reacted slowly and got hit hardest, with some exceptions. The US’s incompetence has been overrated, based on deaths, probably because of President Trump’s general unpopularity. These results are preliminary but they suggest that the US and EU will experience political change to address their lack of rapid action. Non-democracies will still have to deal with the recession and the consequences on social stability. Democracies Face Voter Blowback Democracies will face the wrath of voters once the immediate crisis dies down. The crisis has driven people to rally around the flag, creating polling bounces for national leaders and ruling parties. In some cases the trough-to-peak increase in popular support is remarkable – President Trump's approval reached 10 percentage points briefly, and he rose over 50% approval in some polls for the first time in his presidency (Chart 8A). Yet these initial bounces are already subsiding, as in Trump’s case (Chart 8B). Chart 8ADemocracies Are Accountable To Voters

Geopolitics Is The Next Shoe To Drop

Geopolitics Is The Next Shoe To Drop

Chart 8BAnd Polling Bounces Are Fading

Geopolitics Is The Next Shoe To Drop

Geopolitics Is The Next Shoe To Drop

By this measure, the US, Italy, France, and Spain all face serious political reckonings going forward. Trump is the first in the firing line. Our quantitative election model relies on state-level leading economic indicators that are lagging and show him still winning with 273 Electoral College votes (Chart 9A). However, if we introduce a 2008-magnitude economic shock to these indexes, the Democrats flip Michigan, Wisconsin, Pennsylvania, and New Hampshire, yielding 334 Electoral College votes for former Vice President Joe Biden (Chart 9B). This is assuming Trump’s approval rating stays the same, which, at 46%, is strong relative to the whole term in office. Chart 9AOur Quant Election Model Will Turn Against Trump When Data Catches Up

Geopolitics Is The Next Shoe To Drop

Geopolitics Is The Next Shoe To Drop

Chart 9BA 2008-Style Shock To States Gives Democrats The White House

Geopolitics Is The Next Shoe To Drop

Geopolitics Is The Next Shoe To Drop

Our qualitative judgement reinforces our election model. Historically, US elections are referendums on the ruling party. An incumbent president helps the party win reelection. But a recession is usually insurmountable. George Bush Sr lost in 1992 despite a shallow recession that ended the year before. While Joe Biden is a flawed candidate in numerous ways, the question voters face in November is whether they are better off than they were four years ago. With thousands of deaths and an unemployment rate at or above 20%, it is hard to see swing state voters answering “yes.” Not impossible, but we subjectively put the odds at 35%, and that could easily be revised downward if Trump’s polling falls back down to the 42% range. Trump will also be responsible for the handling of the pandemic itself. His administration obviously made several policy mistakes. A paper trail will highlight intelligence warnings as early as November, and warnings from his inner circle as early as January, that will hurt him.3 Objectively, the Republican Party’s greatest policy flaw, prior to COVID-19, was health care – and this will connect with COVID-19 even if the Affordable Care Act (Obamacare) has little to do with crisis response. Bottom Line: The first and most important political casualty of the pandemic will be Trump’s presidency. Not because the US is uniquely incompetent in the face of the pandemic – although it obviously could have done better, judging by several of the other democracies – but because this year happens to be an election year and democracies hold governments accountable. Major Risk Of Clash With China Chart 10China Likely To Depreciate The Renminbi

China Likely To Depreciate The Renminbi

China Likely To Depreciate The Renminbi

There are two downside geopolitical risks that follow directly from the above. First, while the Democratic candidate Joe Biden is a “centrist,” his position will move to the left of the political spectrum. This is to energize the progressive faction of the party – which is already energized. The market will be taken aback if Biden produces major leftward shifts, in the direction of Senator Bernie Sanders, on taxes, regulation, health care, pharmaceuticals, banks, energy, or tech. This is not a problem when the market is down 36%, but as the market rallies, it becomes more relevant. While US taxes and regulation will go up, Biden will still have to win over the Midwestern Rust Belt voter through trade protectionism, a la Trump and Bernie. This will be exacerbated by the pandemic, which has supercharged American popular enmity toward China and fear of supply chain vulnerability toward China. When Biden reveals that he is protectionist too, US equities will react negatively. Second, more immediately, the clash with China may happen much sooner. As President Trump comes to realize he is losing his grip on power, he will have an incentive to retaliate against China for its mishandling of the pandemic, shift the blame, and achieve long-term strategic objectives as well. This makes Trump’s approval rating a critical indicator – not only of his reelection odds, but of whether he determines he has lost and therefore adopts more belligerent foreign or trade policy. We view the danger zone as anything less than 43%. If Trump becomes a lame duck, he could target China, or other countries, such as Venezuela. The advantage of the latter is that it could have the desired political effect without threatening the economic restart. A conflict with Iran would have bigger consequences – particularly negative for Europe. But in the COVID-19 context, Venezuela and Iran are not relevant to American voters. A conflict with North Korea, however, is part of the strategic conflict with China and would be hard to keep separate from broader tensions. This is only likely if Kim Jong Un stages a major provocation. At present, Washington and Beijing are keeping a lid on tensions. Presidents Trump and Xi are in communication. Beijing has rebuked the foreign minister who accused the US military of bringing COVID-19 to Wuhan. Trump has stopped using inflammatory rhetoric about the “Chinese virus.” China is not depreciating the renminbi, it is upholding other aspects of the trade deal, and it is sending face masks and ventilators to assist the US with the health crisis. But this could change. With its economy under extreme pressure, Beijing must take greater moves to stimulate. An obvious victim will be the renminbi, which is arguably stronger than it should be, especially if China cuts interest rates further, no doubt in great part because of the “phase one” trade deal with the United States (Chart 10). If and when Beijing decides that it must ease the downward pressure on exports and the economy, the renminbi will slide. This will provoke Trump. If he is convinced he cannot salvage the economy anyway, then he has an incentive to channel American anger toward China into new punitive measures over currency manipulation. Finally, the ingredients for our “Taiwan black swan” scenario are falling into place. Taiwan has long attempted to gain representation in the World Health Organization but has been blocked by Beijing’s assertion of the One China principle. However, Taiwan is now caught in an escalating tussle with the WHO leadership that involves both Washington and Beijing. Taipei warned the WHO as early as December that COVID-19 could be transmitted by humans and that the pandemic risk was high.4 Both China and the WHO leadership are simultaneously under pressure from the Trump administration for failing to share information and sound the alarm to prepare other nations. Bottom Line: If President Trump decides to prosecute China for its handling of the virus, and/or promote US-Taiwan relations in a way that aggravates China, then the trigger for a major geopolitical incident will have arrived. Investment Implications It is impossible to predict the precise catalyst or timing of such a crisis. We observe that the US and China are each experiencing historic economic dislocation, their strategic relationship has broken down over the past decade, and their populations are incensed at each other over grievances relating to the trade war, COVID-19, and various disinformation campaigns. Taiwan is at the epicenter of this conflict, due to its defense relationship with the United States and renewed political tensions with China under Xi Jinping. But the Chinese tech sector, North Korea, the South and East China Seas, Xinjiang, and Iran are also potential catalysts. Geopolitics is the other shoe to drop in the wake of COVID-19. Presidents Trump and Xi Jinping are the biggest sources of geopolitical risk, as we outlined in our 2020 forecast. They are cooperating in the immediate crisis, but in the aftermath there will be recriminations. A worsening domestic situation, a loss of prestige for either leader, or a foreign policy provocation could trigger punitive measures, saber rattling, or even military incidents. Risk assets are rallying on the light at the end of the tunnel. We are reaching and in some countries passing the peak intensity of the (first wave of the) pandemic. But the economic aftermath is extremely uncertain and the political fallout has hardly begun. In the US, the implication is clearly negative for Trump. But if that implication is realized, it points to much higher geopolitical risks within 2020 than are currently being considered as the world focuses on the virus. If President Trump chooses to wag the dog with Venezuela, that is obviously a much more positive outcome for global risk assets than if he attempts to achieve American strategic objectives of curbing China’s global assertiveness. Tactically, we remain defensive and recommend defensive US equity sectors and the Japanese yen. On a 12-month and beyond time frame we are more bullish on global growth and are long gold and oil. We remain strategically short CNY-USD and short Taiwanese equities relative to Korean. Matt Gertken Vice President Geopolitical Strategist mattg@bcaresearch.com Appendix Appendix TableThe Global Fiscal Stimulus Response To COVID-19

Geopolitics Is The Next Shoe To Drop

Geopolitics Is The Next Shoe To Drop

Footnotes 1 Given that one of Iran’s top health officials has criticized China for its questionable data and lack of transparency, one does not need to trust the US Intelligence Community’s assessment that China misled the world in the early days of the outbreak. See Matthew Petti, "Even Iran Doesn't Believe China's Coronavirus Stats," April 6, 2020. 2 Readers accustomed to the apocalyptic view of the US health system may wonder that the US comes out looking very well on health capacity. This is because we combine and standardize the scores for per capita spending and longevity. However our data also show that the US is inefficient on health: its life expectancy scores are slightly lower than those of the Europeans, yet it spends more per head. 3 See Josh Margolin and James Gordon Meek, "Intelligence report warned of coronavirus crisis as early as November: Sources," ABC News, April 8, 2020, and Maggie Haberman, "Trade Adviser Warned White House in January of Risks of a Pandemic," New York Times, April 6, 2020. 4 See "Taiwan says WHO failed to act on coronavirus transmission warning," Financial Times, March 19, 2020.

Highlights Europe’s dirty little secret: Euro area debt is already mutualised. Investment implication: Overweight Italian BTPs, underweight German bunds, and overweight the euro on a structural (2-year plus) horizon. ESM plus ECB plus OMT equals a compromise solution to fund stimulus at a mutualised euro area interest rate. Investment implication: Overweight Italian BTPs, underweight German bunds on a cyclical (6-12 month) horizon. Spain’s high early peak in morbidity means that it has taken its pain upfront, at least compared to other countries. Investment implication: upgrade Spain’s IBEX to a tactical overweight – and remove it from the cyclical underweight basket. Feature Chart of the WeekThe Underperformances Of China, Italy And Spain Were A Mirror-Image Of Their Covid-19 Morbidity Curves

The Underperformances Of China, Italy And Spain Were A Mirror-Image Of Their Covid-19 Morbidity Curves

The Underperformances Of China, Italy And Spain Were A Mirror-Image Of Their Covid-19 Morbidity Curves

More About Morbidity Curves Most analyses of the pandemic tend to focus on the grim daily mortality statistics. Yet the key to the pandemic’s evolution is not its mortality rate, but rather its morbidity (severe illness) rate. This is because, without a vaccine, the total area underneath the morbidity curve is fixed. The cumulative number of people who will fall severely ill is pre-determined at the outset (Figures 1-3). Figure I-1The Area Under The Morbidity Curve Is Fixed, A High First Peak Means A Low Second Peak

Will Europe Unite Or Split?

Will Europe Unite Or Split?

Figure I-2A Low First Peak Means An Extended First Peak…

Will Europe Unite Or Split?

Will Europe Unite Or Split?

Figure I-3…Or A High Second Peak

Will Europe Unite Or Split?

Will Europe Unite Or Split?

Very optimistically assuming a Covid-19 morbidity rate of 1 percent, and that 65 percent of the population must get infected to exhaust the pandemic, we know that Covid-19 will ultimately make 0.65 percent of the population severely ill. Absent a vaccine, this number is set in stone. But the number of deaths is not set in stone. It depends on the availability of emergency medical treatment for those that are severely ill. For Covid-19 this means access to ventilation in an intensive care unit (ICU). Yet even the best equipped countries only have ICUs for 0.03 percent of the population. Therefore, the emergency treatment must be rationed either by supply or by demand. Without a Covid-19 vaccine, we cannot change the cumulative number of people who will become severely ill. Rationing by supply means that we must deny emergency treatment to the severely ill – not just Covid-19 patients but victims of, say, heart attacks or car crashes. Accept more deaths. Rationing by demand means that we must flatten the demand (morbidity) curve so that demand is always satisfied by the limited ICU supply. During the pandemics of 1918-19 and 1957, countries could ration emergency medical treatment by supply. Not in 2020. In an era of universal healthcare, everybody is entitled to, and expects to get, emergency medical care. Which means we must ration emergency medical treatment by demand. As such, we must analyse the 2020 response differently to the responses in 1918-19 and 1957. To repeat, without a vaccine, we cannot change the area under the morbidity curve. There is no way of escaping this truth. A low first peak requires a very elongated peak or a high second peak (Chart I-2). Conversely, countries that have suffered a high first peak will need a shorter peak and small (or no) second peak. Chart I-2Japan's Early Stabilisation Was A False Dawn

Japan's Early Stabilisation Was A False Dawn

Japan's Early Stabilisation Was A False Dawn

Turning to an equity market implication, the underperformances of highly cyclical and domestically exposed Spain and Italy have closely tracked their morbidity curves (Chart I-1). Given that both countries have suffered very high first peaks in morbidity, the strong implication is that they have taken their pain upfront – at least compared to other countries. In the case of Spain, the market is also technically oversold (see Fractal Trading System). Investment implication: upgrade Spain’s IBEX to a tactical overweight – and remove it from the cyclical underweight basket. How Europe Could Unite Europe is dithering on its fiscal response to the pandemic. Specifically, Germany and the Netherlands are pushing back against the concept of mutualised euro area debt in the form of ‘corona-bonds’. But a pandemic is an act of nature, an indiscriminate exogenous shock. What is the point of the economic and monetary union if Italy must fund its response to an act of nature at the Italian 10-year yield of 1.5 percent rather than the euro area 10-year yield of 0 percent? (Chart I-3 and Chart I-4) Chart I-3To Fight An Act Of Nature Why Should Italy Borrow At A Higher Rate...

To Fight An Act Of Nature Why Should Italy Borrow At A Higher Rate...

To Fight An Act Of Nature Why Should Italy Borrow At A Higher Rate...

Chart I-4...When It Could Borrow At A Lower Mutualised Rate?

...When It Could Borrow At A Lower Mutualised Rate?

...When It Could Borrow At A Lower Mutualised Rate?

The good news is there is a compromise solution to fund stimulus at a mutualised interest rate. It uses the euro area’s €500 billion bailout fund, the European Stability Mechanism (ESM). But the compromise solution carries two problems which need mitigation. First, ESM credit lines come with conditionality. Italy would rightly balk if it were shackled like Greece, Portugal, and Ireland were after the euro debt crisis. Luckily, the ESM is likely to regard the current ‘act of nature’ crisis very differently to the debt crisis and impose only minimum and appropriate conditionality – for example, that credit lines should be used for healthcare and social welfare spending. Second, ESM credit lines come with a stigma. Taking fright that Italy is tapping the ESM, the bond market might drive up the yields on Italian BTPs. If this pushed up Italy’s overall funding rate, it would defeat the purpose of using the ESM in the first place. ESM plus ECB plus OMT equals a compromise solution to borrow at a mutualised interest rate. The hope is that the bond market, realising that Italy is using the bailout facility to counter an act of nature, would not drive up BTP yields. But if it did, the ECB could counter this by buying BTPs. One option would be to use its Outright Monetary Transactions (OMT) facility. Set up during the euro debt crisis, the OMT’s specific function is to counter bond market attacks when they are not justified by the economic fundamentals. In other words, to prevent a liquidity crisis escalating into a solvency crisis. Thereby, ESM plus ECB plus OMT equals a compromise solution to fund stimulus at a mutualised euro area interest rate. Investment implication: Overweight Italian BTPs, underweight German bunds on a cyclical (6-12 month) horizon. Europe’s Dirty Little Secret Outwardly, Germany and the Netherlands are reluctant to go down the slippery slope to mutualised euro area debt. But here’s the dirty little secret they don’t want you to know. Euro area debt is already mutualised. The stealth mutualisation has happened via the Target2 banking imbalance which now stands at €1.5 trillion. This imbalance is an accounting identity showing that Italy is owed ‘German euros’ via its large quantity of bank deposits in German banks while Germany is symmetrically owed ‘Italian euros’ via its large effective holding of Italian government bonds. The imbalance is irrelevant if a German euro equals an Italian euro. But if Italy defaulted on its bonds – by repaying them in a reinstated and devalued lira – then Target2 means that Germany must pick up the bill (Chart I-5). Chart I-5Target2 Means That If Italy Defaults, Germany Picks Up The Bill

Will Europe Unite Or Split?

Will Europe Unite Or Split?

The Target2 imbalance is the result of the ECB’s QE program, in which the central bank has bought hundreds of billions of Italian bonds. If Italy repaid those bonds in a devalued lira, then the ECB would become insolvent, and the central bank’s remaining shareholders would have to plug the hole. The biggest shareholder would be Germany. Could Germany force Italy to repay its bonds in euros? No. According to a legal principle called ‘lex monetae’ Italy can repay its debt in its sovereign currency, whatever that is. Meanwhile, because of the fragility of the Italian banking system, the Italians who sold the bonds to the ECB deposited the cash in German banks. Legally, these depositors must be paid back in whatever is the German currency. Euro area debt is already mutualised. If euro area debt is already mutualised, why do policymakers continue to pretend that it isn’t? There are three reasons. First no policymaker would want to publicise that Germany is now on the hook if Italy left the euro. Second, no policymaker would want to publicise that the ECB has put Germany in this position (Chart I-6). Chart I-6ECB QE Has Created The Target2 Imbalance

ECB QE Has Created The Target2 Imbalance

ECB QE Has Created The Target2 Imbalance

Third, and most important, policymakers would point out that the mutualisation of debt only happens if the euro breaks up. They would argue that because the euro is irreversible, the debt is not mutualised. In fact, their argument is completely back to front. The truth is: Because euro area debt is now mutualised, the euro has become irreversible. Investment implication: Overweight Italian BTPs, underweight German bunds, and overweight the euro on a structural (2-year plus) horizon. Fractal Trading System* As already discussed, this week’s recommended trade is long Spain’s IBEX 35 versus the Euro Stoxx 600. The profit target is 3 percent with a symmetrical stop-loss. Meanwhile our other trade, long Australia versus New Zealand has moved into a 2 percent profit. The rolling 12-month win ratio now stands at 66 percent. Chart I-7IBEX 35 Vs. EUROSTOXX 600

IBEX 35 Vs. EUROSTOXX 600

IBEX 35 Vs. EUROSTOXX 600

When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com. Dhaval Joshi Chief European Investment Strategist dhaval@bcaresearch.com Fractal Trading System Cyclical Recommendations Structural Recommendations Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights Bond Yield Differentials: The deepening global recession has prompted aggressive monetary easing measures by virtually every developed economy central bank. With policy rates now near zero everywhere, government bond yield differentials between countries have been reduced substantially. Currency Hedged vs Unhedged Yields: Opportunities still exist in some countries to create synthetically “higher” yields relative to low local rates by hedging the currency exposure of foreign bonds. Country Allocation: Italy and Spain government bonds offer the most attractive yields, hedged into any of the major currencies (USD, EUR, GBP, JPY). Among the lower yielders, Canadian, Australian, French and Japanese government bonds offer the most attractive yield pickups, on a currency-hedged basis, versus yields in the US, Germany, and the UK. Feature Chart 1A Synchronized Collapse

A Synchronized Collapse

A Synchronized Collapse

The COVID-19 economic downturn is already shaping up to be one of the deepest global recessions in history. While there have been worldwide industrial slowdowns and manufacturing recessions in the past, what is happening now is different in that all countries are suffering sharp contractions in activity in the much larger services sectors that employ far more workers. The result will be massive increases in unemployment, as is already happening in the US where a staggering 10 million workers have filed for jobless benefits over just the past two weeks. Central bankers have responded to the shock to growth by following essentially the same playbook: cutting interest rates to zero as rapidly as possible, followed up with quantitative easing and other programs to support financial markets. With a synchronized economic collapse leading to policy convergence, government bond yields have plunged worldwide, but yield differentials between countries have also fallen sharply as a result (Chart of the Week). In this report, we will present the case for using currency hedging more actively than usual to create more attractive global bond yields. What can a global government bond investor do in this environment of tiny-but-highly-correlated bond yields to squeeze out some incremental additional return? In this report, we will present the case for using currency hedging more actively than usual to create more attractive global bond yields. A Fundamentally Driven Yield Convergence Chart 2Yields Are Low Everywhere

Yields Are Low Everywhere

Yields Are Low Everywhere

As a simple starting point, just looking at the level of government bond yields in the developed economies is a good indication of how little there is to choose from between countries right now. For example, a 10-year government bond in the US was yielding 0.67% yesterday, compared to a 10-year yield in Australia, Canada and the UK of 0.82%, 0.75%, and 0.33% respectively (Chart 2). Not only are those low absolute yields, but those spreads versus US Treasuries are very narrow in an historical context. Another way to see how similar interest rate structures have become within the major developed markets is by looking at market expectations of future policy rates. Our proxy for the market’s pricing of the terminal nominal policy rate – the 5-year overnight index swap (OIS) rate, 5-years forward – shows that interest rate markets are expecting policy rates to stay very low over the next few years. The fall in the terminal rate estimate has been the largest in the US and Canada, where the markets were still pricing in a “peak” policy rate level around 2% as late as December – the figure is now 0.6% in the US and 1.1% in Canada (Chart 3). Chart 3Global Policy Rate Convergence

Global Policy Rate Convergence

Global Policy Rate Convergence

So if the bond markets now believe that the current levels of bond yields will be sustained for longer, is that a realistic belief? There is already a considerable amount of both monetary and fiscal stimulus that has been introduced by policymakers. At some point, this stimulus should begin to stabilize and boost economic growth, but only after the immediate public health crisis of the COVID-19 outbreak has begun to subside. That will eventually help put a floor under developed market government bond yields. Chart 4The Backdrop Remains Conducive To Global Bond Yields Staying Low

The Backdrop Remains Conducive To Global Bond Yields Staying Low

The Backdrop Remains Conducive To Global Bond Yields Staying Low

As we discussed in a recent weekly report, three elements must all happen before a true and lasting bottom for both risk assets and bond yields can begin to take place (Chart 4):1 The net number of new COVID-19 cases must begin to slow in critical countries like the US and Italy, a first step before the lockdown restrictions can start to be lifted; The US dollar (USD) must peak out and begin to roll over, taking stress off non-US borrowers of USD-denominated debt; The VIX must sustainably fall back from the levels above 40 that imply very volatile markets and continued investor nervousness about the future. Global government bond yields are likely to remain relatively range bound over the next month or two, at least. Out of this list, the slowing in the number of new cases of the virus in Italy is a positive sign, as is the VIX falling back to the mid-40s. The sticky USD is still a major issue, however, particularly for borrowers with major dollar debts in the emerging world. There is not yet an “all clear” from this checklist, suggesting that global government bond yields are likely to remain relatively range bound over the next month or two, at least. This means bond investors need to consider alternative strategies to boost the yield of their government bond portfolios. Bottom Line: The deepening global recession has prompted similar monetary easing measures by virtually every developed economy central bank. With policy rates near zero everywhere, government bond yield differentials between countries have been largely eliminated. Searching For More Attractive Yields - With Currency Hedging When discussing our country allocation strategy, we have always looked at the yields and relative returns of government bonds in each country in hedged currency terms rather than in local currency terms. This is to remove the significant return volatility coming from currency exposure, while also making an appropriate “apples-to-apples” comparison of the yields on offer in each country. We have chosen the USD as the “base currency” for all these comparisons. In Chart 5, we show a static snapshot of the government bond yield curves, in local currency terms, for the US, Germany, France, Italy, the UK, Japan, Canada and Australia. The US, Canada and Australia remain the relative high-yielders within the major developed markets, although the “riskier” credits of Italy and Spain offer the highest outright yields. Unhedged German yields look particularly unattractive here, with the entire yield curve offering yields below 0%. Chart 5Currency-Unhedged Global Government Bond Yield Curves

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Chart 6USD-Hedged Global Government Bond Yield Curves

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

In Chart 6, we show those same yield curves, but with the non-US yields all shown on a USD-hedged basis. The yields include the net gain/cost of hedging foreign currency back into US dollars using 3-month currency forwards. Shown this way, the non-US yield curves can be more directly compared to the “base” US Treasury curve. Looking at those yields shows that there is a much tighter convergence of yields with the US for most countries, but in a relative narrower range between 0.5% and 1.25% across the full maturity spectrum. The Fed’s rapid easing cycle, which started with the 75bps of rate cuts in the summer of 2019 and continued with the rapid move to a near-zero funds rate during the COVID-19 crisis, has dramatically altered the calculus for both global bond country allocation and currency hedging. Chart 7Fed Rate Cuts Have Reduced The Yield Advantage of USTs

Fed Rate Cuts Have Reduced The Yield Advantage of USTs

Fed Rate Cuts Have Reduced The Yield Advantage of USTs

Chart 8Fed Rate Cuts Have Taken The Carry Out Of The USD

Fed Rate Cuts Have Taken The Carry Out Of The USD

Fed Rate Cuts Have Taken The Carry Out Of The USD

First, the Fed’s easing cycle triggered a major decline in US Treasury yields that was not matched in other countries, eliminating much of the unhedged yield advantage of Treasuries over non-US peers (Chart 7). At the same time, the Fed’s rate cuts eliminated much of the interest rate “carry” of owning US dollars versus other currencies. The amount of that reduction was significant, with the gain of hedging a euro or yen currency exposure into dollars reduced from nearly around 250bps in the spring of 2019 to just over 100bps today (Chart 8). That dramatically alters the attractiveness of even negative-yielding German and Japanese government bonds, whose yields could once have been transformed into a relatively high USD-based yield via currency hedging. The Fed’s easing cycle triggered a major decline in US Treasury yields that was not matched in other countries, eliminating much of the unhedged yield advantage of Treasuries over non-US peers. At the same time, the Fed’s rate cuts eliminated much of the interest rate “carry” of owning US dollars versus other currencies. Country Allocation Strategy Implications For dedicated global government bond investors, the only way to earn meaningfully higher yields in the current environment is to consider selective currency hedging of bond exposures. In Tables 1-4, we show 2-year, 5-year, 10-year and 30-year government bond yields for the major developed economy bond markets. The yields are hedged into USD, EUR, GBP and JPY, to allow comparisons of foreign yields for investors with those four base currencies. Table 1Currency-Hedged 2-Year Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Table 2Currency-Hedged 5-Year Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Table 3Currency-Hedged 10-Year Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Table 4Currency-Hedged 30-Year Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

For USD-based investors, there are still some interesting opportunities available to find a USD-hedged foreign yield that can exceed that of US Treasuries. The higher-yielding European markets like Italy and Spain are the obvious places to find yield, and we continue to recommend those bonds with the ECB now buying more of the riskier euro area government bonds as part of its new Pandemic Emergency Purchase Program. However, Canadian, Australian and French bonds – hedged into USD – all offer intriguing yield pickups over US Treasuries. Even the negative yields available in Japan and Switzerland look interesting when expressed in USD terms, although that is not the case for negative yielding German bonds. Canadian, Australian and French bonds – hedged into USD – all offer intriguing yield pickups over US Treasuries. Even the negative yields available in Japan and Switzerland look interesting when expressed in USD terms, although that is not the case for negative yielding German bonds. In Tables 5-8, the currency-hedged yields for each country are shown as a spread to the relevant “base” bond yield for each currency. For example, under the “EUR” column in Table 6, the cells show the yield spread between 5-year government bonds hedged into euros and 5-year German bonds. Here, we can see that there are far fewer opportunities for euro-based bond investors to find non-European yields that offer adequate yield pickups versus German yields. The pickings are even less slim for Japanese investors, with many non-Japanese yields trading below Japanese yields on a JPY-hedged basis. Table 5Currency-Hedged 2-Year Govt. Bond Yield Spreads Versus The

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Table 6Currency-Hedged 5-Year Govt. Bond Yield Spreads Versus The

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Table 7Currency-Hedged 10-Year Govt. Bond Yield Spreads Versus The

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Table 8Currency-Hedged 30-Year Govt. Bond Yield Spreads Versus The

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

In sum, looking across all eight tables shown, the most consistently attractive yields, across all currencies and maturities, can be found in Australia, Canada, France, Italy and Spain. Bottom Line: Opportunities still exist in some countries to create synthetically “higher” yields relative to low local rates by hedging the currency exposure of foreign bonds. Italy and Spain government bonds offer the most attractive yields, hedged into any of the major currencies (USD, EUR, GBP, JPY). Among the lower yielders, Canadian, Australian, French and Japanese government bonds offer the most attractive yield pickups, on a currency-hedged basis, versus yields in the US, Germany, and the UK. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 Please see BCA Global Fixed Income Strategy Weekly Report, "Central Banks To Markets: Redefining "Whatever It Takes"", dated March 24, 2020, available at gfis.bcaresearch.com. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Get Out The Magnifying Glass: Finding Value In Government Bond Yields

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

The number of newly reported cases of COVID-19 in Italy and Spain seems to have peaked 13 days ago. This by no means indicates that an end of the lockdowns is imminent, but if China’s experience is any guide, it suggests that we are finally getting closer to…

We have been closely monitoring the dynamics of the COVID-19 outbreak in Italy. If the containment of the virus can gather momentum, it could fuel the prospect that other Western countries can also gain control of the epidemic. The data on new infections…

Highlights The economic shutdown needed to exhaust the coronavirus pandemic must last much longer than is anticipated. For example, in Italy it must last 24 weeks. If the economy is reopened too soon, the pandemic will reignite in a second wave later this year, just as in 1918. Take the 12 percent profit in the tactical overweight to equities versus bonds and go neutral. Stay underweight European equities and euro area banks given their high sensitivity to the economy. Stay overweight US T-bonds versus German bunds and Swiss bonds. All high-quality bond yields will eventually reach the lower bound of -1 percent, making US T-bonds the most attractive in class. The euro is a structural overweight but a tactical neutral – because in equity market corrections the repatriation of foreign investments into domestic cash boosts the demand for dollars relative to the euro. Fractal trades: Go long Australia versus New Zealand. Short palladium versus nickel was closed at 32 percent profit. Feature “You’ve got to understand that you don’t make the timeline, the virus makes the timeline” – Dr. Anthony Fauci, Director of the National Institute of Allergy and Infectious Diseases It’s A Biological Crisis The coronavirus crisis is first and foremost a biological crisis. This makes it fundamentally different to the 2008 global financial crisis, the 2000 dot com bust, the 1990 Japanese crash, and the 1930s Great Depression – all of which were financial crises needing financial and economic cures. As such, the current crisis needs to be analysed very differently. Crucially, the financial and economic policy responses to the coronavirus crisis are only a palliative, not a cure. The cure is to exhaust the coronavirus pandemic. But to exhaust the pandemic without overburdening stretched healthcare systems will require shutting the economy for months. If the economy is reopened too soon, then the pandemic will reignite in a second and a possible third wave just as in 1918-19 (Chart of the Week). Chart I-1If The Economy Is Reopened Too Soon The Pandemic Will Reignite, Just As In 1918-19

If The Economy Is Reopened Too Soon The Pandemic Will Reignite, Just As In 1918-19

If The Economy Is Reopened Too Soon The Pandemic Will Reignite, Just As In 1918-19

The US fiscal stimulus package amounts to 10 percent of annual GDP. But if exhausting the pandemic requires a third of the economy to be shut for a third of the year, then the economy would lose one ninth, or 11 percent, of its annual output. Hence, despite the biggest fiscal boost of all time, the economy would end up shrinking (Chart I-2). Chart I-2Fiscal Stimulus Is Massive, But Might Not Be Enough

The Economy Must Shut For 24 Weeks

The Economy Must Shut For 24 Weeks

Meanwhile, Germany’s willingness to remove the ‘debt brake’ that limits its structural federal deficit to 0.35 percent of GDP, the willingness to issue euro ‘corona-bonds’, and the ECB’s willingness to increase the size and breath of its asset-purchase program are minor details in a much bigger story. Rather like rearranging the deckchairs on the Titanic. Ignore the minor details and concentrate on the bigger story. How long must the economy stay shut to exhaust the pandemic? The Crucial Metric Is Not Mortality, It Is Morbidity Some people counter that in shutting the economy, “the cure is worse than the disease”. They argue that most coronavirus victims suffer mild or no illness. Moreover, the mortality rate is low and might not be much higher than that of the flu. Even if this turns out to be true, the argument misses the point. Death requires very little medical intervention and resource, whereas severe illness requires massive medical intervention and resource. Moreover, when the severe illness is a respiratory illness, it leaves the sufferer struggling to breathe and needing ventilation in an intensive care unit (ICU). No civilized society can deny an ICU to somebody who is struggling to breathe. Therefore, the most important metric for the coronavirus crisis is not its mortality rate, but rather its morbidity (severe illness) rate. Or more specifically, the morbidity rate versus the economy’s ICU capacity. How long must the economy stay shut to exhaust the pandemic? Enter the Diamond Princess. The cruise ship turned into a laboratory for the coronavirus because all 3700 passengers and crew were quarantined and tested for the infection. Of the 700 people who tested positive, 11 have subsequently died. But the more important point is that 45 people needed ICU treatment, meaning the coronavirus morbidity rate was four times its mortality rate (Table I-1). Table I-1On The Diamond Princess, The COVID-19 Morbidity Rate Was Four Times Its Mortality Rate

The Economy Must Shut For 24 Weeks

The Economy Must Shut For 24 Weeks

A separate study by the Intensive Care National Audit & Research Centre in the UK corroborates this, suggesting that the coronavirus morbidity rate is around three times the mortality rate and that the average time in an ICU for a coronavirus patient is half a week.1 Let’s be optimistic and assume that the coronavirus mortality rate is around 0.3 percent and that its morbidity rate is around three times higher at 1 percent. This means that if a hundred thousand people get infected, one thousand will need ICU treatment. But even advanced economies have only a dozen or so ICU beds per hundred thousand people. For example, Italy has 12.5 (Chart I-3). Chart I-3Advanced Economies Have Only A Dozen Or So ICU Beds Per Hundred Thousand People

The Economy Must Shut For 24 Weeks

The Economy Must Shut For 24 Weeks