Europe

The dollar's retreat is creating the most compelling window for euro internationalisation since Maastricht, but Europe is missing the one instrument that would make it real. In this report, we make the case for the Eurobond, assess which model is most likely to prevail, and explain why the trade is long euro on dips and overweight Central and Eastern European sovereign spreads.

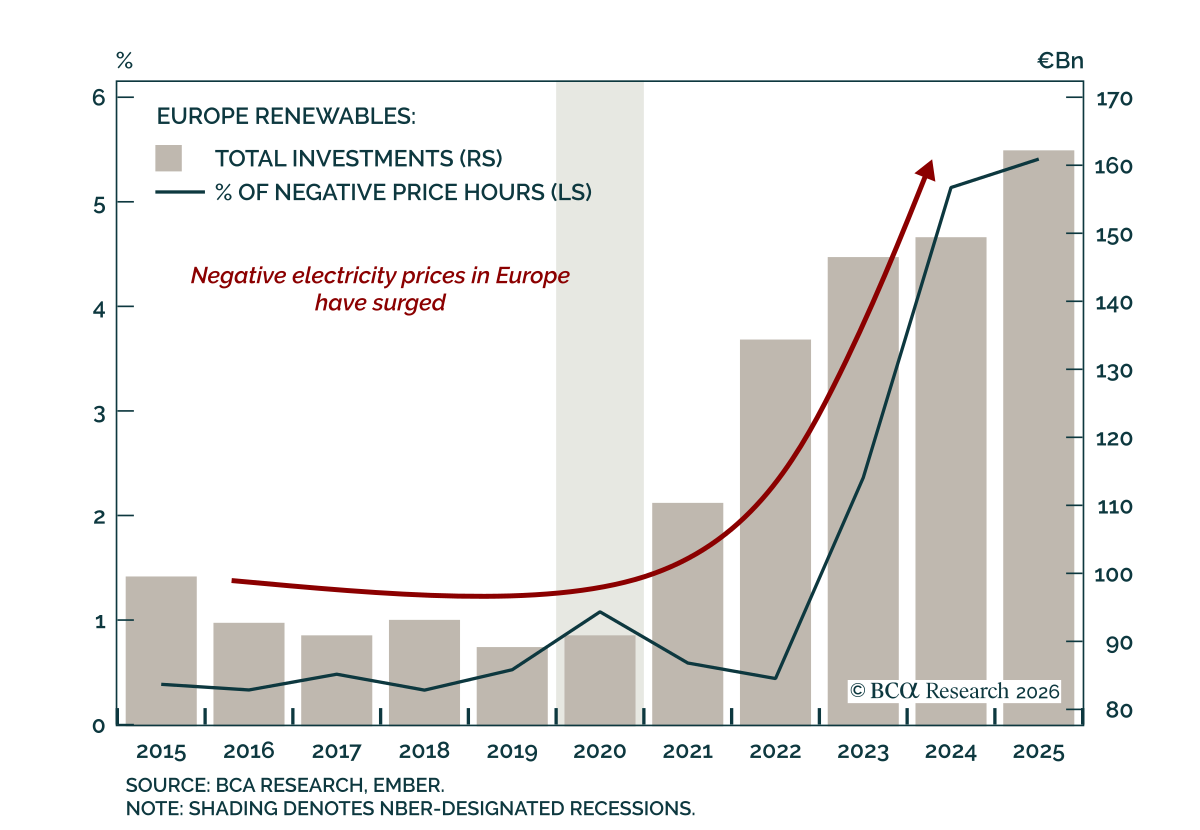

Europe has been too ambitious with Renewables. Oversupply, volatility, and rising contract risk are compressing revenues and returns. The space is now crowded yet markets have not fully repriced the risk. New opportunities are emerging: Power Storage and Data Centers have upside.

Volatility is high, but the path for yields is clearer than it looks. Across three oil scenarios, we show how policy responses shape fixed income markets and why the balance of risks still points to lower yields.

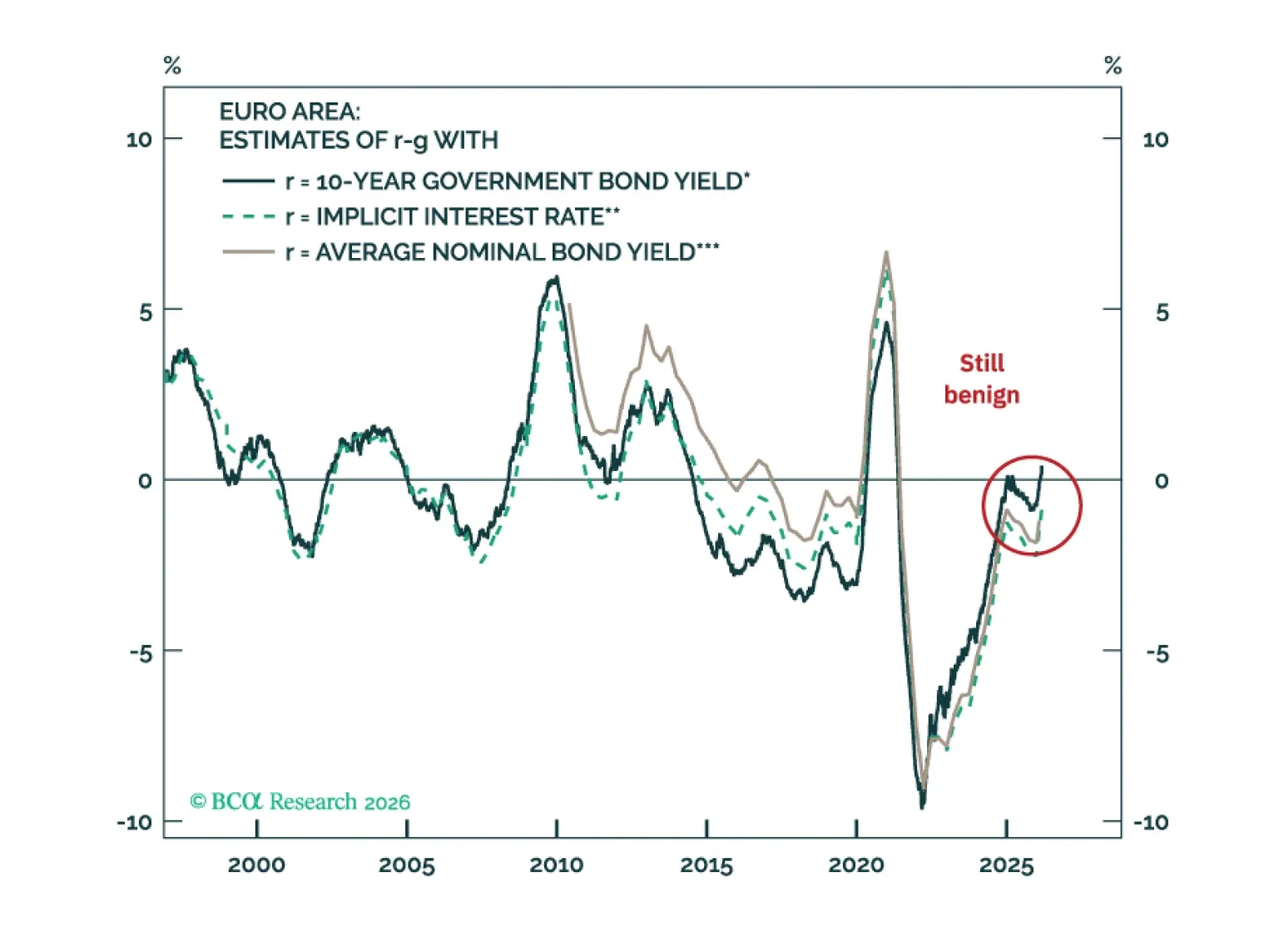

Europe’s fiscal debate has resurfaced as interest rates normalize and new spending pressures emerge. Yet alarmism is misplaced. Aggregate debt levels are high but broadly stable, servicing costs remain historically low, and r–g dynamics are broadly benign. Fiscal space matters less as the ECB and EU backstop growth and spreads. Structural reforms—not wanton fiscal spending—is Europe’s real opportunity.

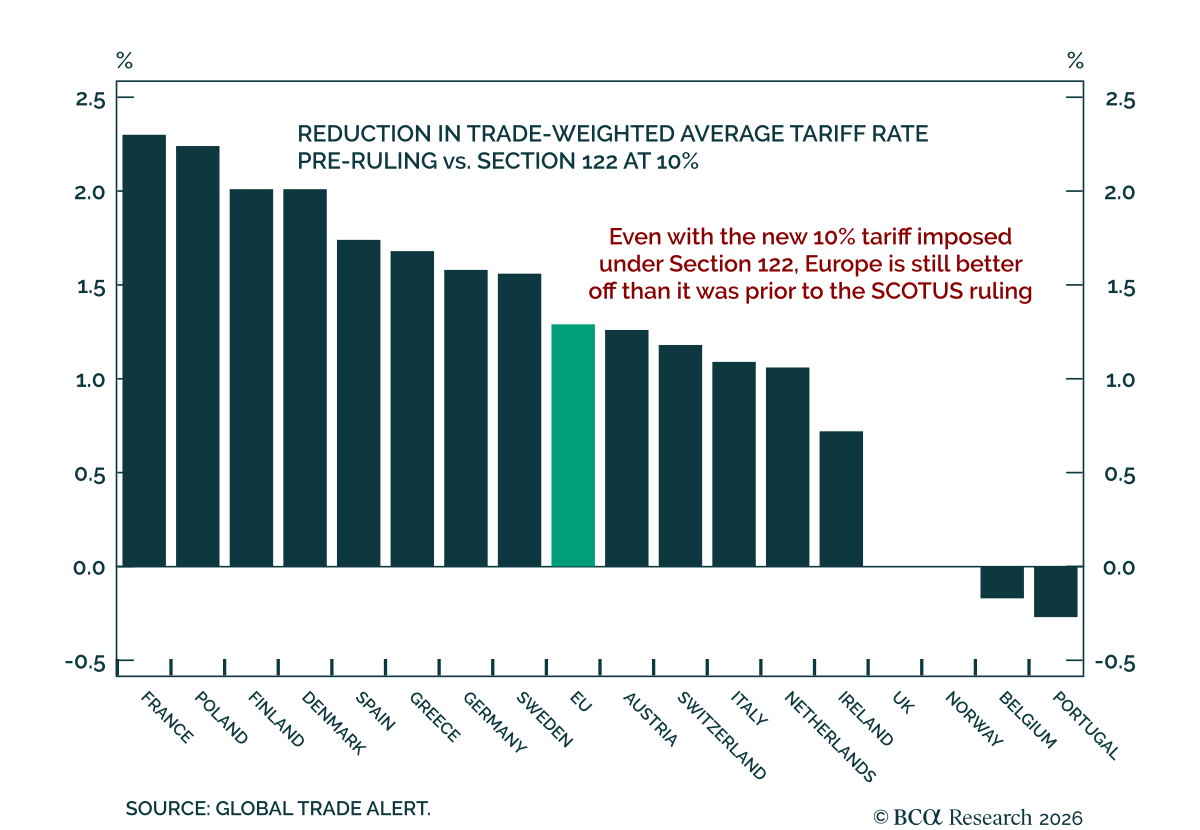

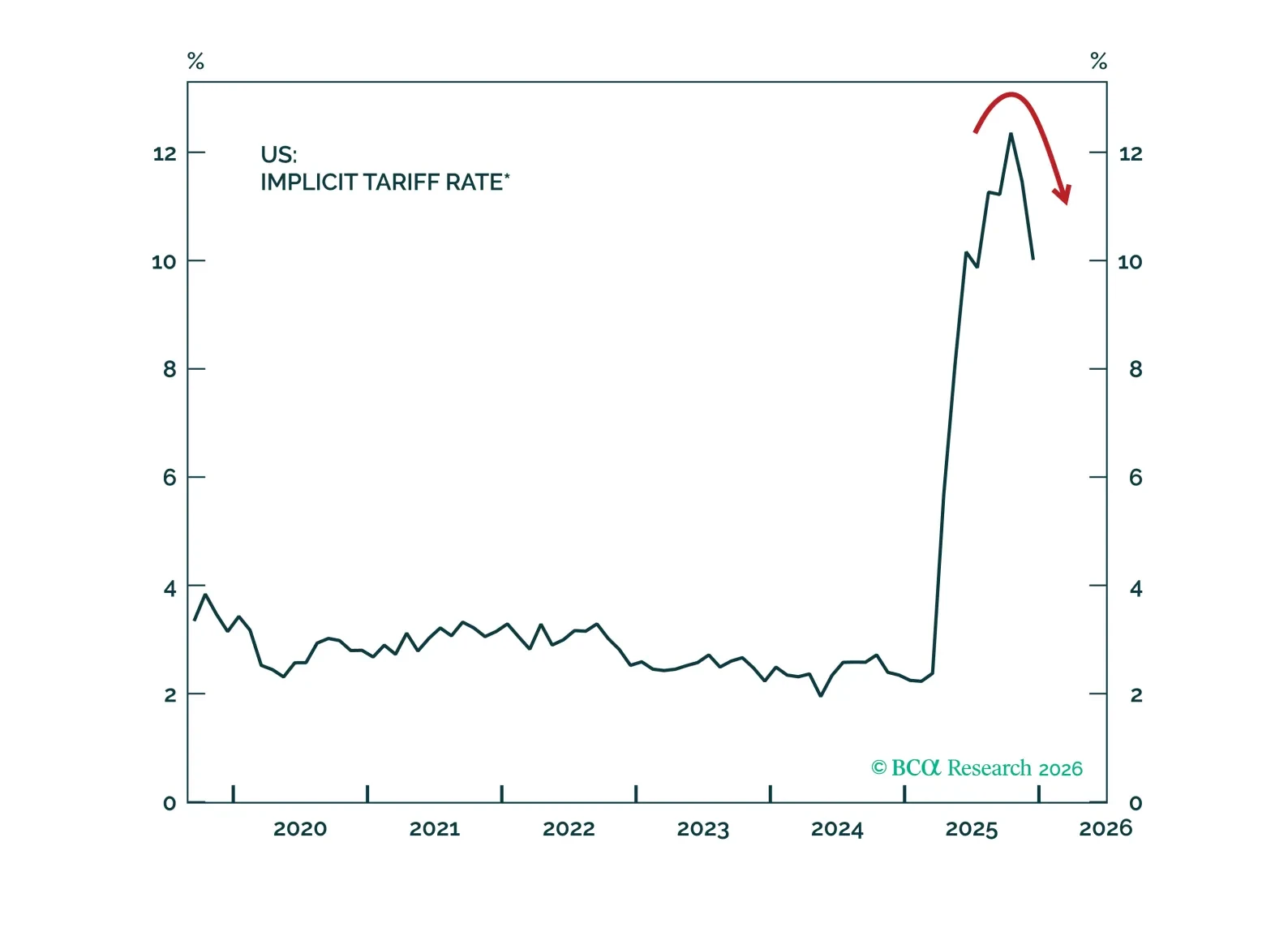

The Section 122 tariffs under the US Trade Act of 1974 are more favorable to Europe; the trade-weighted tariff rate falls to 10.45%, from 11.74% pre-ruling. This positive development does not change our overall views on Europe, as we expected lower tariffs ahead of the US midterms.