Europe

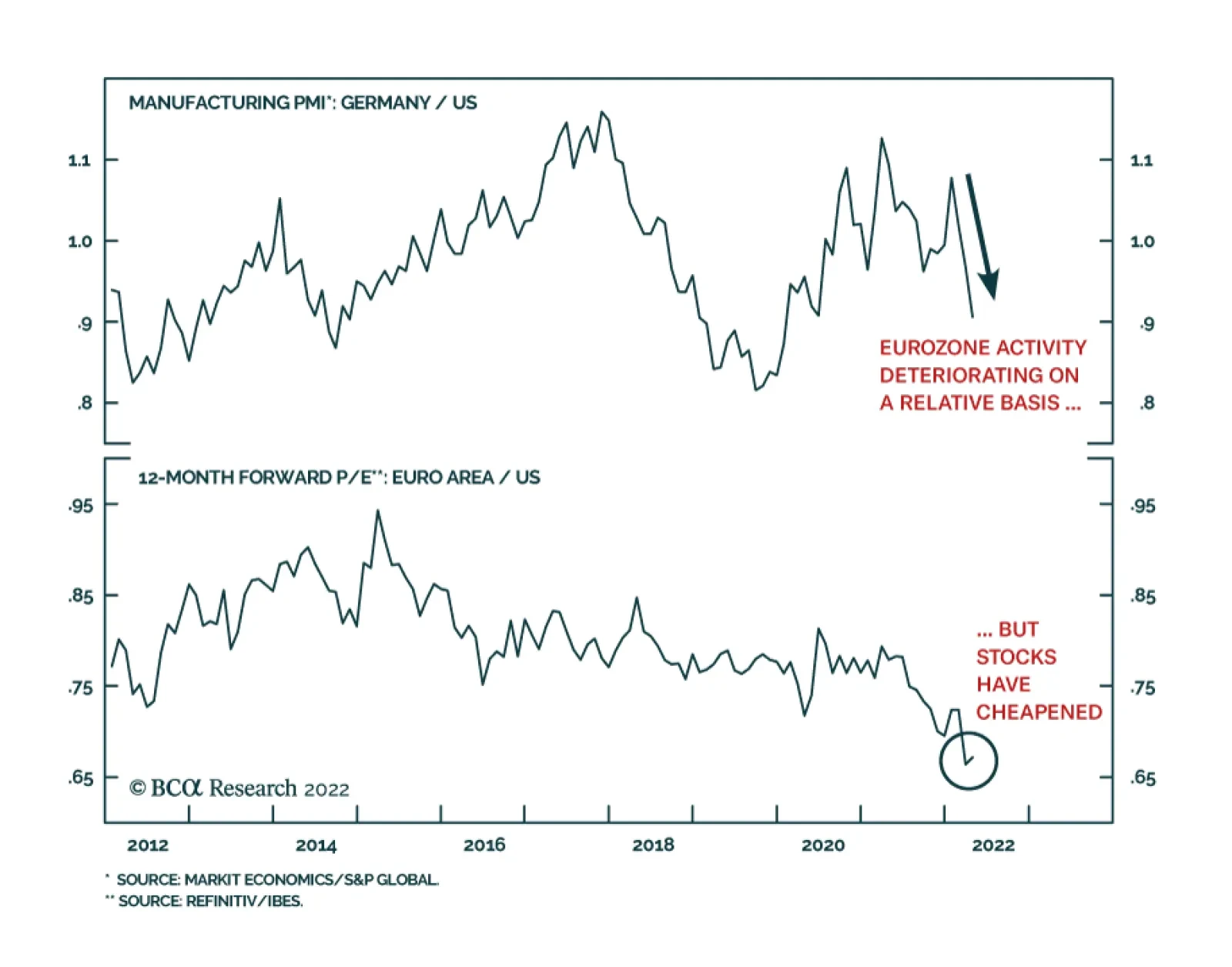

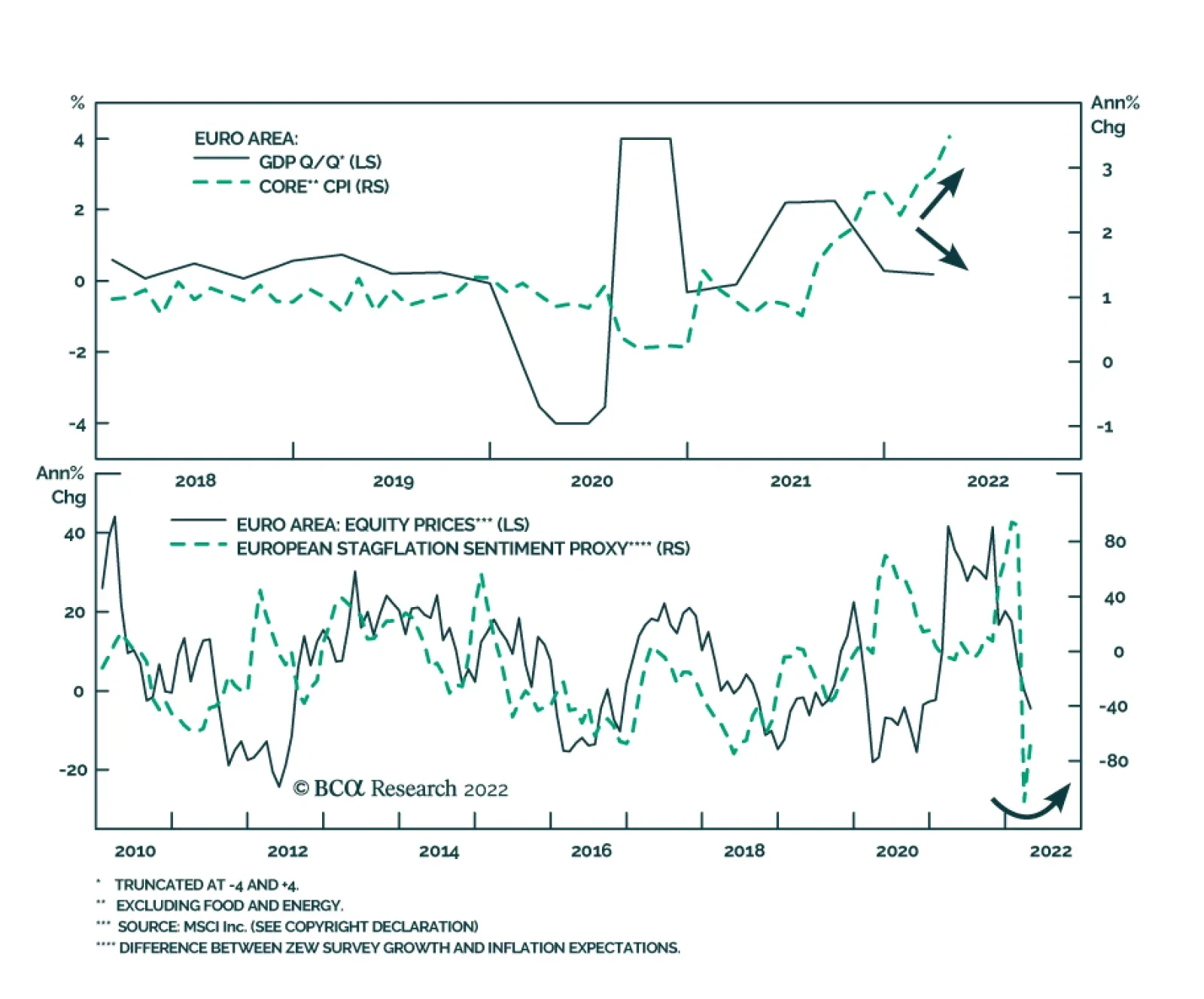

The German Manufacturing PMI has been declining relative to its US counterpart since January, underscoring that the Eurozone economy is facing stronger headwinds. Hard data corroborates this dynamic. The Euro Area’s Q1 GDP and CPI releases suggest that the…

As expected, economic activity slowed in the Euro Area: GDP growth eased from 0.3% q/q in Q4 2021 to 0.2% q/q in Q1 2022. Meanwhile, core CPI inflation rose to a 29-year high of 3.5% y/y and headline inflation hit an all-time high of 7.5% y/y in April.…

Listen to a short summary of this report. Executive Summary The Number Of Babies Born In China Has Fallen By Close To 30% Since 2019

The Number Of Babies Born In China Has Fallen By Close To 30% Since 2019

The Number Of Babies Born In China Has Fallen By Close To 30% Since 2019

The number of births collapsed during the pandemic. While the preliminary evidence suggests that fertility rates are starting to recover in most developed economies, they remain well below the level necessary to maintain a stable population. Aging populations are putting strain on pension and health care systems. They are also threatening to undermine geopolitical influence. The conventional wisdom is that there is not much that can be done to lift fertility rates. While it is true that government subsidies to encourage parents to have more children are not especially effective, other policies, such as cheaper child care, are more promising. Rather than discouraging property investment, China is likely to increase housing supply in order to make family formation more affordable. This could boost commodity demand. More contentiously, the use of IVF technologies to select for certain traits such as higher intelligence in children could open up a new front on the geopolitical battlefield that few analysts are expecting. Regardless of government policy, birth rates will eventually rise of their own accord because both cultural and genetic evolution will select for families that wish to have more children. In the long run, faster population growth will lead to stronger corporate sales, which is a plus for equities. Over a shorter-term horizon, however, the global dependency ratio could end up increasing, as the number of retirees rises while the number of children that parents need to support goes up. This could put upward pressure on interest rates and bond yields. Bottom Line: Contrary to popular opinion, global fertility rates may be bottoming and could rise significantly over the long run. While this trend will eventually benefit stocks, it is likely to come at the expense of higher bond yields. Dear Client, We tactically downgraded global equities from overweight to neutral on February 28th. As we discussed last week in our report entitled “Here Comes Goldilocks,” we see a more fortuitous environment emerging in the second half of the year, which suggests that stocks will likely be higher over a 12-month horizon. This week, we step back from recent market action to focus on a long-term investment theme of great importance: demographic change. Contrary to the conventional wisdom that sees birth rates continuing to fall over the next few decades, we argue that developed economies may be on the cusp of a strong and sustained baby boom. I will be visiting clients in the San Francisco Bay Area next week. Instead of our regular report, we will be sending you a Special Report written by Irene Tunkel, BCA’s Chief US Equity Strategist. Irene will discuss inflation regimes and their implications for US equities. Best regards, Peter Berezin, Chief Global Strategist Baby Bust At the start of the pandemic, some speculated that with little else to do, couples would spend more time in bed, leading to a mini baby boom. As it turned out, the exact opposite happened: Birth rates plunged around the world. In the US, the number of babies born in January 2021 was about 10% lower than one would have expected based on the pre-pandemic trend. Similar shortfalls were observed in the UK, France, Italy, Spain, and Japan (Chart 1). In China, the number of births fell by almost 30% between 2019 and 2021 to the lowest level since 1949 (Chart 2). Chart 1The Birth Rate Has Recovered Since The Start Of The Pandemic But Remains Below Levels Consistent With A Stable Population

The Coming Stork Wars

The Coming Stork Wars

Chart 2The Number Of Babies Born In China Has Fallen By Close To 30% Since 2019

The Number Of Babies Born In China Has Fallen By Close To 30% Since 2019

The Number Of Babies Born In China Has Fallen By Close To 30% Since 2019

While the pandemic continues to restrain fertility in China, the latest data from developed economies suggest births have rebounded. Nevertheless, birth rates remain far below the level necessary to maintain stable populations. A recent study in The Lancet estimated that more than three-quarters of countries would have below-replacement fertility rates by the end of the century. The study estimated that the global population would peak at 9.7 billion in 2064 and decline to 8.8 billion by 2100. Alarm Over Low Birth Rates Low birth rates have become a major cause of concern for policymakers. Aging populations are putting strain on pension and health care systems. The OECD expects the old-age dependency ratio to double from 30% to 60% by 2075 (Chart 3). Pension spending in the OECD is projected to rise by 1.4% of GDP over the next 40 years. Chart 3Conventional Forecasts Expect The Population To Grey Over The Coming Decade

The Coming Stork Wars

The Coming Stork Wars

Chart 4The UN Projects China's Working-Age Population Will Shrink By 400 Million Over The Remainder Of The Century

The UN Projects China's Working-Age Population Will Shrink By 400 Million Over The Remainder Of The Century

The UN Projects China's Working-Age Population Will Shrink By 400 Million Over The Remainder Of The Century

Health care spending is likely to grow at an even faster pace. In the US, the Congressional Budget Office sees federal government-financed health care spending rising from 5.7% of GDP to 9.4% of GDP by 2050. As has been the case in Japan and Russia, and could be the case in China, a shrinking population threatens to undermine geopolitical influence. The UN estimates that China’s working-age population will decline from about 1 billion to less than 600 million by the end of the century. By 2100, Nigeria’s working-age population is projected to approach China’s (Chart 4). It is difficult to be an economic and military superpower if you do not have enough workers and soldiers. Pro-Natal Subsidies: Little Bang for the Buck Governments are responding by adopting increasingly aggressive pro-natal policies. According to the UN, more than 50 countries have officially declared their intention to increase fertility rates (Chart 5). Chart 5Governments Are Actively Trying To Raise Fertility Rates

The Coming Stork Wars

The Coming Stork Wars

Chart 6Fertility Rates Keep Dropping In OECD Countries Amid Rising Government Incentives

Fertility Rates Keep Dropping In OECD Countries Amid Rising Government Incentives

Fertility Rates Keep Dropping In OECD Countries Amid Rising Government Incentives

Various European countries, ranging from Estonia, Germany, Greece, Finland, France, Italy, and Lithuania to the UK offer varying bonus payments to new parents. Japan and Singapore both have baby bonus schemes. South Korea, which has the lowest fertility rate in the world, recently increased the reward it pays to mothers from US$500 to US$1,700. The most significant pro-natal shift has come from China. After having officially abandoned its one-child policy in 2016, China announced last year that it will allow couples to have up to three children. We expect China to introduce generous subsidies to encourage childbirth over the next few years. Will such policies arrest the decline in birth rates? There are certainly reasons to be skeptical. Chart 6 shows that spending on family benefits in OECD economies rose from 1.5% to 2.1% of GDP over the past 40 years. Yet, the fertility rate fell from 2.25 to 1.66 over this period. Can Anything Turn the Tide? A number of structural forces have contributed to lower fertility rates. These include increased female labor market participation, readily available birth control, falling child mortality, and rising housing and educational costs. The availability of government-provided income support and health care has also arguably reduced the historic role that children have played in supporting their parents in old age. The conventional wisdom is that these forces will only strengthen in the future, ensuring that fertility rates keep dropping. I am not so sure. Are Children Inferior, Normal, or Veblen goods? While it is rather awkward to think of the decision to have children in economic terms, there is some logic to this approach. Economists tend to distinguish between substitution and income effects. The substitution effect for children is negative: As wages rise, the opportunity cost of having children goes up. In contrast, a number of studies have documented that the income effect is positive: Give a couple an extra $1 million, no strings attached, and that could push them over the line in deciding to have an additional child (in economic parlance, children are “normal” rather than “inferior”). Economists have long known that labor supply curves tend to be “backward bending” (Charts 7A & B). The classic example is that of leisure. As wages initially rise from low levels, people may seek to work more (and hence, consume less leisure). Eventually, however, if wages rise enough, people will cut back on work in order to enjoy the fruits of their labor. Chart 7ABackward-Bending Demand Curves May Also Apply To Children

The Coming Stork Wars

The Coming Stork Wars

Chart 7BLower Child-Rearing Costs Would Improve The Demographic Problem

The Coming Stork Wars

The Coming Stork Wars

The same sort of backward-bending demand curve may apply to children. As wages rise above a certain threshold, parents may decide that they can afford to have more children. Chart 8 shows that the correlation between per capita income and realized fertility has turned positive in developed economies. Chart 8Correlation Between Incomes And Realized Fertility Has Turned Positive In Developed Countries

The Coming Stork Wars

The Coming Stork Wars

Looking out, it is possible that children will become “Veblen” goods, named after nineteenth-century economist Thorstein Veblen, who coined the term “conspicuous consumption.” With many luxury goods now available to the masses, what better way to signal that one has made it to the top than to have five kids in Manhattan or Beverly Hills? How Expensive Are Children, Really? Across most developed economies, women tend to end up having fewer children than they would like (Chart 9). While difficulty in finding a suitable spouse is sometimes cited as a reason, the financial hardship associated with parenting usually ranks higher. Chart 9Most Women Are Having Fewer Children Than They Desire

The Coming Stork Wars

The Coming Stork Wars

Chart 10Depression Rates Among Children And Teenagers Have Been Increasing Over The Past Decade

The Coming Stork Wars

The Coming Stork Wars

According to one recent estimate, it costs nearly $300,000, excluding college tuition, to raise a child in the US. This number, however, is conditional on what society currently deems appropriate for rearing children. If the incremental cost of a child were to decline, the slope of the budget constraint in Chart 7B would become flatter, implying that both the income and substitution effects would reinforce each other in the direction of having more children. Could society eventually conclude that the cost of having a child is not as large as widely perceived? The idea is not as far-fetched as it sounds. Having turned 50 this week, I find it interesting to look back at how much cultural norms towards kids have changed over the past few decades. Growing up in Hamilton Ontario, I remember taking the public bus alone at the age of 10 to school, the pool, or anywhere else I wanted to go. Are kids even allowed to leave the house unattended anymore? As Derek Thompson points out in a recent article in The Atlantic, American parents have nearly doubled the amount of time spent raising their kids. And what has the advent of helicopter parenting achieved? It is difficult to point to any concrete benefits. Depression rates among children and teenagers have soared (Chart 10). While the proliferation of social media has exacerbated childhood angst, the tendency for parents to try to shield their children from hardship and failure has probably only made things worse. Does Schooling Matter Much? Sticking with the issue of schooling, to what extent does the modern parental preoccupation with education actually benefit children? Probably a lot less than parents realize. IQ is highly correlated with educational achievement and many other favorable life outcomes (Chart 11). IQ scores are by far the best predictors of job performance, much better than fashionable concepts such as “emotional intelligence” (Chart 12). Chart 11IQ Tests Don’t Just Measure How Well You Can Do On An IQ Test

The Coming Stork Wars

The Coming Stork Wars

Chart 12Cognitive Ability Matters A Lot For Job Performance

The Coming Stork Wars

The Coming Stork Wars

In healthy, well-nourished populations, genetics explains about 50% of IQ variation at age ten and 80% in adulthood (Chart 13). In fact, IQ is almost as heritable as height (Chart 14). Chart 13The Heritability Of IQ Reaches 80% By Adulthood

The Coming Stork Wars

The Coming Stork Wars

Chart 14IQ Is Almost As Heritable As Height

The Coming Stork Wars

The Coming Stork Wars

When a child suffers from economic or social deprivation, improvements to their environment can have a large positive impact on their cognitive performance. However, beyond a certain environmental threshold, there is not much that parents can do. A recent study concluded that “there is only a marginal and inconsistent influence of parenting on offspring IQ in adolescence and young adulthood.” Table 1A Poisoned Chalice? Genetic Screening Can Raise IQ

The Coming Stork Wars

The Coming Stork Wars

Even musical training, which parents often spend a fortune on, does not appear to generate any knock-on benefits for math or language skills. As much as I hate to say it, the evidence suggests that the most reliable way to enhance a child’s educational prospects is to endow them with high IQ genes. I will not speak to the questionable ethics of doing so, but as I discussed in my report on the rise and fall of human intelligence a few years ago, the technology is coming. Carl Shulman and Nick Bostrom estimate that genetic screening could boost average IQs by up to 65 points in five generations (Table 1). The Stork Wars The ability to engineer high-IQ children through IVF technologies could open up a front on the geopolitical battlefield that few analysts are expecting. Such a battlefield for geopolitical supremacy will take place at a time when China and Russia, on the one side, and much of the West, on the other side, are moving in polar opposite directions on a variety of cultural issues. The empirical evidence suggests that there is a U-shaped relationship between gender equality and fertility rates. Both patriarchal societies, such as those in parts of the Middle East, and egalitarian societies, such as those in Scandinavia, have been able to maintain relatively high fertility levels. Between these two extremes, fertility rates are typically well below replacement. Whereas most Western nationals have sought to promote gender equality in recent years, China and Russia have shifted in a more traditionalist direction. Last April, China’s government shut down a number of feminist social media groups. This followed a statement by China's Education Ministry that the government would seek to “cultivate masculinity.” Boys were becoming “delicate, timid and effeminate,” a key government advisor declared. Ironically, both the traditionalist and egalitarian approaches could lift fertility rates, but at the cost of an ever-wider cleavage in the global culture wars. The Long-Term Outlook for Fertility Rates: Up, Up, and Away? In a world of abundant material resources, a steady or declining population is not an evolutionary stable equilibrium. As long as there are some selection pressures towards having more offspring, in the absence of offsetting forces, evolution will push up fertility rates. In the pre-industrial era, parents with many children often struggled to keep enough food on the table. The correlation between parent and child fertility was close to zero, meaning that children who came from big families did not have more surviving offspring than children from small families. After the Industrial Revolution, the correlation turned positive, and by most indications, has been rising over the past few decades. Were it not for the positive correlation between parent and child fertility, global population levels would be even lower today. How high could birth rates climb if the cultural forces, which have suppressed fertility over the past century, abate? The natural tendency is to think that evolution works too slowly to matter. However, this represents a misreading of the evidence. When there are evolutionary disequilibria – that is, when the environment changes in ways that renders existing reproductivity strategies suboptimal – natural selection can work surprisingly fast. Contrary to the widespread notion that human evolution stopped before the Agricultural Revolution, a recent study in Nature found that 88% of physiological traits have undergone polygenic change during the past 2,000 to 3,000 years. Using plausible estimates of intergenerational fertility correlations, Jason Collins and Lionel Page calibrate a model of global population growth. In contrast to more conventional demographic models, they conclude that global population growth, rather than turning negative later this century, will accelerate. In their baseline model without any heritability effects, the global total fertility rate falls to 1.82 by the end of the century. Once heritability effects are included, the projected total fertility rate rises to 2.21 (Chart 15). The largest effects are for Europe and North America, the first two regions to undertake a demographic transition to (temporarily) low birth rates. The authors see the European median total fertility rate rising to 2.46 by the end of the century, with the North American rate increasing to 2.67. Chart 15Natural Selection Could End Up Boosting Fertility Rates Over The Long Run

The Coming Stork Wars

The Coming Stork Wars

Notably, the support ratio – the ratio of workers-to-consumers – continues to fall in their model over the remainder of the century. They conclude: “Once the increase in number of children is taken into consideration, the higher number of children in the heritability model merely shifts the nature of the burden rather than ameliorating it.” Investment Conclusions The world is at a demographic inflection point. After rising steadily for four decades, the global support ratio has peaked (Chart 16). Baby boomers are beginning to leave the labor market en masse. While they were working, they accumulated a lot of assets. In the US, baby boomers hold more than half of all household wealth (Chart 17). Chart 16Less Workers And More Consumers Over The Next Decades

Less Workers And More Consumers Over The Next Decades

Less Workers And More Consumers Over The Next Decades

Chart 17Baby Boomers Hold More Than Half Of Wealth In The US

The Coming Stork Wars

The Coming Stork Wars

Going forward, rather than working and saving, baby boomers will spend down their wealth. The global pool of savings will shrink, putting upward pressure on equilibrium real interest rates and bond yields. Faced with the prospect of shrinking work forces, strained social security systems, and declining geopolitical influence, countries with low or negative population growth will offer increasingly generous subsidies to encourage couples to have more children. The resulting bigger budget deficits will further drain national savings. In and of themselves, government subsides are unlikely to significantly boost birth rates. More holistic policies will be needed, including steps to reduce the cost of child care and housing. Rather than discouraging property investment, China is likely to increase housing supply in order to make family formation more affordable. This could help support commodity demand. Governments will try to influence the social and cultural narrative on family matters.In some cases, the impact could be quite innocuous, such as China’s decision to ban for-profit tutoring companies in order to ease pressure on students and parents. In other cases, the impact could be very contentious, leading to an escalation in the so-called culture wars. Regardless of the policy measures that governments adopt, birth rates will eventually rise of their own accord because both cultural and genetic evolution will select for families that wish to have more children. In the long run, faster population growth will lead to stronger corporate sales, which is a plus for equities. Over a shorter-term horizon, however, the global dependency ratio could end up increasing, as the number of retirees rises while the number of children that parents need to support goes up. On balance, therefore, we see demographic trends as being somewhat negative for stocks over the next one-or-two decades. Peter Berezin Chief Global Strategist peterb@bcaresearch.com Follow me on LinkedIn Twitter View Matrix

The Coming Stork Wars

The Coming Stork Wars

Special Trade Recommendations Current MacroQuant Model Scores

The Coming Stork Wars

The Coming Stork Wars

Executive Summary German GeoRisk Indicator

German GeoRisk Indicator

German GeoRisk Indicator

Russia and Germany have begun cutting off each other’s energy in a major escalation of strategic tensions. The odds of Finland and Sweden joining NATO have shot up. A halt to NATO enlargement, particularly on Russia’s borders, is Russia’s chief demand. Tensions will skyrocket. China’s reversion to autocracy and de facto alliance with Russia are reinforcing the historic confluence of internal and external risk, weighing on Chinese assets. Geopolitical risk is rising in South Korea and Hong Kong, rising in Spain and Italy, and flat in South Africa. France’s election will lower domestic political risk but the EU as a whole faces a higher risk premium. The Biden administration is doubling down on its defense of Ukraine, calling for $33 billion in additional aid and telling Russia that it will not dominate its neighbor. However, the Putin regime cannot afford to lose in Ukraine and will threaten to widen the conflict to intimidate and divide the West. Trade Recommendation Inception Date Return LONG GLOBAL DEFENSIVES / CYCLICALS EQUITIES 2022-01-20 14.2% Bottom Line: Stay long global defensives over cyclicals. Feature Chart 1Geopolitical Risk And Policy Uncertainty Drive Up Dollar

Geopolitical Risk And Policy Uncertainty Drive Up Dollar

Geopolitical Risk And Policy Uncertainty Drive Up Dollar

The dollar (DXY) is breaking above the psychological threshold of 100 on the back of monetary tightening and safe-haven demand. Geopolitical risk does not always drive up the dollar – other macroeconomic factors may prevail. But in today’s situation macro and geopolitics are converging to boost the greenback (Chart 1). Global economic policy uncertainty is also rising sharply. It is highly correlated with the broader trade-weighted dollar. The latter is nowhere near 2020 peaks but could rise to that level if current trends hold. A strong dollar reflects slowing global growth and also tightens global financial conditions, with negative implications for cyclical and emerging market equities. Bottom Line: Tactically favor US equities and the US dollar to guard against greater energy shock, policy uncertainty, and risk-aversion. Energy Cutoff Points To European Recession Chart 2Escalation With Russia Weighs Further On EU Assets

Escalation With Russia Weighs Further On EU Assets

Escalation With Russia Weighs Further On EU Assets

Russia is reducing natural gas flows to Poland and Bulgaria and threatening other countries, Germany is now embracing an oil embargo against Russia, while Finland and Sweden are considering joining NATO. These three factors are leading to a major escalation of strategic tensions on the continent that will get worse before they get better, driving up our European GeoRisk indicators and weighing on European assets (Chart 2). Russia’s ultimatum in December 2021 stressed that NATO enlargement should cease and that NATO forces and weapons should not be positioned east of the May 1997 status quo. Russia invaded Ukraine to ensure its military neutrality over the long run.1 Finland and Sweden, seeing Ukraine’s isolation amid Russian invasion, are now reviewing whether to change their historic neutrality and join NATO. Public opinion polls now show Finnish support for joining at 61% and Swedish support at 57%. The scheduling of a joint conference between the country’s leaders on May 13 looks like it could be a joint declaration of their intention to join. The US and other NATO members will have to provide mutual defense guarantees for the interim period if that is the case, lest Russia attack. The odds that Finland and Sweden remain neutral are higher than the consensus holds (given the 97% odds that they join NATO on Predictit.org). But the latest developments suggest they are moving toward applying for membership. They fear being left in the cold like Ukraine in the event of an attack. Russia’s response will be critical. If Russia deploys nuclear weapons to Kaliningrad, as former President Dmitri Medvedev warned, then Moscow will be making a menacing show but not necessarily changing the reality of Russia’s nuclear strike capabilities. That is equivalent to a pass and could mark the peak of the entire crisis. The geopolitical risk premium would begin to subside after that. Related Report Geopolitical StrategyLe Pen And Other Hurdles (GeoRisk Update) However, Russia has also threatened “military-political repercussions” if the Nordics join NATO. Russia’s capabilities are manifestly limited, judging by Ukraine today and the Winter War of 1939, but a broader war cannot entirely be ruled out. Global financial markets will still need to adjust for a larger tail risk of a war in Finland/Sweden in the very near term. Most likely Russia will retaliate by cutting off Europe’s natural gas. Clearly this is the threat on the table, after the cutoff to Poland and Bulgaria and the warnings to other countries. In the near term, several companies are gratifying Russia and paying for gas in rubles. But these payments violate EU sanctions against Russia and the intention is to wean off Russian imports as soon as possible. Germany says it can reduce gas imports starting next year after inking a deal with Qatar. Hence Russia might take the initiative and start reducing the flow earlier. Bottom Line: If Europe plunges into recession as a result of an immediate natural gas cutoff, then strategic stability between Russia and the West will become less certain. The tail risk of a broader war goes up. Stay cyclically long US equities over global equities and tactically long US treasuries. Stay long defense stocks and gold. Stay Short CNY At the end of last year we argued that Beijing would double down on “Zero Covid” policy in 2022, at least until the twentieth national party congress this fall. Social restrictions serve a dual purpose of disease suppression and dissent repression. Now that the state is doubling down, what will happen next? The economy will deteriorate: imports are already contracting at a rate of 0.1% YoY. The manufacturing PMI has fallen to 48.1 and the service sector PMI to 42.0, indicating contraction. Furthermore, social unrest could emerge, as lockdowns serve as a catalyst to ignite underlying socioeconomic disparities. Hence the national party congress is less likely to go smoothly, implying that investors will catch a glimpse of political instability under the surface in China as the year progresses. The political risk premium will remain high (Chart 3). Chart 3China's Confluence Of Domestic And Foreign Risk Weighs On Stocks And Currency

China's Confluence Of Domestic And Foreign Risk Weighs On Stocks And Currency

China's Confluence Of Domestic And Foreign Risk Weighs On Stocks And Currency

While Chairman Xi Jinping is still likely to clinch another ten years in power, it will not be auspicious amid an economic crash and any social unrest. Xi could be forced into some compromises on either Politburo personnel or policy adjustments. A notable indicator of compromise would be if he nominated a successor, though this would not provide any real long-term assurance to investors given the lack of formal mechanisms for power transfer. After the party congress we expect Xi to “let 100 flowers bloom,” meaning that he will ease fiscal, regulatory, and social policy so that today’s monetary and fiscal stimulus can work effectively. Right now monetary and fiscal easing has limited impact because private sector actors are averse to taking risk. Easing policy to boost the economy could also entail a diplomatic charm offensive to try to convince the US and EU to avoid imposing any significant sanctions on trade and investment flows, whether due to Russia or human rights violations. Such a diplomatic initiative would only succeed, if at all, in the short run. The US cannot allow a deep re-engagement with China since that would serve to strengthen the de facto Russo-Chinese strategic alliance. In other words, an eruption of instability threatens to weaken Xi’s hand and jeopardize his power retention. While it is extremely unlikely that Xi will fall from power, he could have his image of supremacy besmirched. It is likely that China will be forced to ease a range of policies, including lockdowns and regulations of key sectors, that will be marginally positive for economic growth. There may also be schemes to attract foreign investment. Bottom Line: If China expands the range of its policy easing the result could be received positively by global investors in 2023. But the short-term outlook is still negative and deteriorating due to China’s reversion to autocracy and confluence of political and geopolitical risk. Stay short CNY and neutral Chinese stocks. Stay Short KRW South Koreans went to the polls on March 9 to elect their new president for a five-year term. The two top candidates for the job were Yoon Suk-yeol and Lee Jae-myung. Yoon, a former public prosecutor, was the candidate for the People Power Party, a conservative party that can be traced back to the Saenuri and the Grand National Party, which was in power from 2007 to 2017 under President Lee Myung-bak and President Park Geun-hye. Lee, the governor of the largest province in Korea, was the candidate for the Democratic Party, the party of the incumbent President Moon Jae-in. Yoon won by a whisker, garnering 48.6% of the votes versus 47.8% for Lee. The margin of victory for Yoon is the lowest since Korea started directly electing its presidents. President-elect Yoon will be inaugurated in May. He will not have control of the National Assembly, as his party only holds 34% of the seats. The Democratic Party holds the majority, with 172 out of 300 seats. The next legislative election will be in 2024, which means that President Yoon will have to work with the opposition for a good two years before his party has a chance to pass laws on its own. President-elect Yoon was the more pro-business and fiscally restrained candidate. His nomination of Han Duck-soo as his prime minister suggests that, insofar as any domestic policy change is possible, he will be pragmatic, as Han served under two liberal administrations. Yoon’s lack of a majority and nomination of a left-leaning prime minister suggest that domestic policy will not be a source of uncertainty for investors through 2024. Foreign policy, by contrast, will be the biggest source of risk for investors. Yoon rejects the dovish “Moonshine” policy of his predecessor and favors a strong hand in dealing with North Korea. “War can be avoided only when we acquire an ability to launch pre-emptive strikes and show our willingness to use them,” he has argued. North Korea responded by expanding its nuclear doctrine and resuming tests of intercontinental ballistic missiles with the launch of the Hwasong-17 on March 24 – the first ICBM launch since 2017. In a significant upgrade of North Korea’s deterrence strategy, Kim Yo Jong, the sister of Kim Jong Un, warned on April 4 that North Korea would use nuclear weapons to “eliminate” South Korea if attacked (implying an overwhelming nuclear retaliation to any attack whatsoever). Kim Jong Un himself claimed on April 26 that North Korea’s nuclear weapons are no longer merely about deterrence but would be deployed if the country is attacked. President-elect Yoon welcomes the possibility of deploying of US strategic assets to strengthen deterrence against the North. The hawkish turn is not surprising considering that North-South relations failed to make any substantive improvements during President Moon’s five-year tenure as a pro-engagement president. South Koreans, especially Yoon’s supporters, are split on whether inter-Korean dialogue should be continued. They are becoming more interested in developing their own nuclear weapons or at the very least deploying US nuclear weapons in South Korea. Half of South Korean voters support security through alliance with the US, while a third support security through the development of independent nuclear weapons. The nuclear debate will raise tensions on the peninsula. An even bigger change in South Korea’s foreign policy is its policy towards China. President-elect Yoon has accused President Moon of succumbing to China’s economic extortion. Moon had established a policy of “three No’s,” meaning no to additional THAAD missiles in South Korea, no to hosting other US missile defense systems, and no to joining an alliance with Japan and the United States. By contrast, Yoon’s electoral promises include deploying more THAAD and joining the Quadrilateral Dialogue (US, Japan, Australia, India). Polls show that South Koreans hold a low opinion of all of their neighbors but that China has slipped slightly beneath Japan and North Korea in favorability. Even Democratic Party voters feel more negative towards China. While negative attitudes towards China are not unique to Korea, there is an important difference from other countries: the Korean youth dislike China the most, not the older generations. Negative sentiment is less tied to old wounds from the Korean war and more related to ideology and today’s grievances. Younger Koreans, growing up in a liberal democracy and proud of their economic and cultural success, have been involved in campus clashes against Chinese students over Korean support for Hong Kong democrats. Negative attitudes towards China among the youth should alarm investors, as young people provide the voting base for elections to come, and China is the largest trading partner for Korea. Korea’s foreign policy will hew to the American side, at risk to its economy (Chart 4). Chart 4South Korean Geopolitical Risk Rising Under The Radar

South Korean Geopolitical Risk Rising Under The Radar

South Korean Geopolitical Risk Rising Under The Radar

President-elect Yoon’s policies towards North Korea and China will increase geopolitical risk in East Asia. The biggest beneficiary will be India. Both Korea and Japan need to find a substitute to Chinese markets and labor, which have become less reliable in recent years. South Korea’s newly elected president is aligned with the US and West and less friendly toward China and Russia. He faces a rampant North Korea that feels emboldened by its position of an arsenal of 40-50 deliverable nuclear weapons. The North Koreans now claim that they will respond to any military attack with nuclear force and are testing intercontinental ballistic missiles and possibly a nuclear weapon. The US currently has three aircraft carriers around Korea, despite its urgent foreign policy challenges in Europe and the Middle East. Bottom Line: Stay long JPY-KRW. South Korea’s geopolitical risk premium will remain high. But favor Korean stocks over Taiwanese stocks. Stay Neutral On Hong Kong Stocks Hong Kong’s leadership change will trigger a new bout of unrest (Chart 5). Chart 5Hong Kong: More Turbulence Ahead

Hong Kong: More Turbulence Ahead

Hong Kong: More Turbulence Ahead

On April 4, Hong Kong’s incumbent Chief Executive, Carrie Lam, confirmed that she would not seek a second term but would step down on June 30. John Lee, the current chief secretary of Hong Kong, became the only candidate approved to run for election, which is scheduled to be held on May 8. With the backing of the pro-Beijing members in the Election Committee, Lee is expected to secure enough nominations to win the race. Lee served as security secretary from when Carrie Lam took office in 2017 until June 2021. He firmly supported the Hong Kong extradition bill in 2019 and National Security Law in 2020, which provoked historic social unrest in those years. He insisted on taking a tough security stance towards pro-democracy protests. With Lee in power, Hong Kong will face more unrest and tougher crackdowns in the coming years, which will likely bring more social instability. Lee will provoke pro-democracy activists with his policy stances and adherence to Beijing’s party line. For example, his various statements to the news media suggest a dogmatic approach to censorship and political dissent. With the adoption of the National Security Law, Hong Kong’s pro-democracy faction is already deeply disaffected. Carrie Lam was originally elected as a popular leader, with notable support from women, but her popularity fell sharply after the passage of the extradition bill and National Security Law, as well as her mishandling of the Covid-19 outbreak. Her failure to handle the clashes between the Hong Kong people and Beijing damaged public trust in government. Trust never fully recovered when it took another hit recently from the latest wave of the pandemic. Putting another pro-Beijing hardliner in power will exacerbate the trend. Hong Kong equities are vulnerable not merely because of social unrest. During the era of US-China engagement, Hong Kong benefited as the middleman and the symbol that the Communist Party could cooperate within a liberal, democratic, capitalist global order. Hence US-China power struggle removes this special status and causes Hong Kong financial assets to contract mainland Chinese geopolitical risk. As a result of the 2019-2020 crackdown, John Lee and Carrie Lam were among a list of Hong Kong officials sanctioned by the US Treasury Department and State Department in 2020. Now, after the Ukraine war, the US will be on the lookout for any Hong Kong role in helping Russia circumvent sanctions, as well as any other ways in which China might further its strategic aims by means of Hong Kong. Bottom Line: Stay neutral on Hong Kong equities. Favor France Within European Equities French political risk will fall after the presidential election, which recommits the country to geopolitical unity with the US and NATO and potentially pro-productivity structural reforms (Chart 6). France is already a geopolitically secure country so the reduction of domestic political risk should be doubly positive for French assets, though they have already outperformed. And the Russia-West conflict is fueling a risk premium regardless of France’s positive developments. Chart 6France's Domestic Political Risk Will Subside But Russian War Will Keep Geopolitical Risk Elevated

France's Domestic Political Risk Will Subside But Russian War Will Keep Geopolitical Risk Elevated

France's Domestic Political Risk Will Subside But Russian War Will Keep Geopolitical Risk Elevated

The French election ended with a solid victory for the political establishment as we expected. President Emmanuel Macron gaining 58% of the vote to Marine Le Pen’s 42%. Macron beat his opinion polling by 4.5pp while Le Pen underperformed her polls by 4.5pp. A large number of voters abstained, at 28%, compared to 25.5% in 2017. The regional results showed a stark divergence between overseas or peripheral France (where Marine Le Pen even managed to get over half of the vote in several cases) and the core cities of France (where Macron won handily). Macron had won an outright majority in every region in 2017. Macron did best among the young and the old, while Le Pen did best among middle-aged voters. But Macron won every age group except the 50 year-olds, who want to retire early. Macron did well among business executives, managers, and retired people, but Le Pen won among the working classes, as expected. Le Pen won the lowest paid income group, while Macron’s margin of victory rises with each step up the income ladder. Macron’s performance was strong, especially considering the global context. The pandemic knocked several incumbent parties out of power (US, Germany) and required leadership changes in others (Japan, Italy). The subsequent inflation shock now threatens to cause another major political rotation in rapid succession, leaving various political leaders and parties vulnerable in the coming months and years (Australia, the UK, Spain). Only Canada and now France marked exceptions, where post-pandemic elections confirmed the country’s leader. The Ukraine war constitutes yet another shock but it helped Macron, as Le Pen had objective links and sympathies with Russian President Vladimir Putin. Macron’s timing was lucky but his message of structural reform for the sake of economic efficiency still resonates in contemporary France, where change is long overdue – at least compared with Le Pen’s proposal of doubling down on statism, protectionism, and fiscal largesse. The French middle class was never as susceptible to populism as the US, UK, and Italy because it had been better protected from the ravages of globalization. Populism is still a force to be reckoned with, especially if left-wing populists do well in the National Assembly, or if right-wing populists find a fresher face than the Le Pen dynasty. But the failure of populism in the context of pandemic, inflation, and war suggests that France’s political establishment remains well fortified by the economic structure and the electoral system. Whether Macron can sustain his structural reforms depends on legislative elections to be held on June 12-19. Early projections are positive for his party, which should keep a majority. Macron’s new mandate will help. Le Pen’s National Rally and its predecessors may perform better than in the past but that is not saying much as their presence in the National Assembly has been weak. Bottom Line: France is geopolitically secure and has seen a resounding public vote for structural reform that could improve productivity depending on legislative elections. French equities can continue to outperform their European peers over the long run. Our European Investment Strategy recommends French equities ex-consumer stocks, French small caps over large caps, and French aerospace and defense. Favor Spanish Over Italian Stocks Chart 7Italian And Spanish Political Risk Will Rise But Favor Spanish Stocks

Italian And Spanish Political Risk Will Rise But Favor Spanish Stocks

Italian And Spanish Political Risk Will Rise But Favor Spanish Stocks

What about Spain? It is still a “divided nation” susceptible to a rise in political risk ahead of the general election due by December 10, 2023 (Chart 7). In the past few months, a series of strategic mistakes and internal power struggles have led to a significant decline in the popularity of Spain’s largest opposition party, the People’s Party. Due to public infighting and power struggle, Pablo Casado was forced to step down as the leader of the People’s Party on February 23, as requested by 16 of the party’s 17 regional leaders. It is yet to be seen if the new party leader, Alberto Nunez Feijoo, can reboot People’s Party. The far-right VOX party will benefit from the People Party’s setback. The latter’s misstep in a regional election (Castile & Leon) gave VOX a chance to participate in a regional government for the very first time. Hence VOX’s influence will spread and it will receive greater recognition as an important political force. Meanwhile the ruling Socialist Worker’s Party (PSOE) faces anger from the public amid inflation and high energy prices. However, Spanish Prime Minister Pedro Sanchez’s decision to send offensive military weapons to Ukraine is widely supported among major parties, including even his reluctant coalition partner, Unidas Podemos. The People’s Party’s recent infighting gives temporary relief to the ruling party. The Russia-Ukraine issue caused some minor divisions within the government but they are not yet leading to any major political crisis, as nationwide pro-Ukraine sentiment is largely unified. The Andalusia regional election, which is expected this November, will be a check point for Feijoo and a pre-test for next year’s general election. Andalusia is the most populous autonomous community in Spain, consisting about 17% of the seats in the congress (the lower house). The problem for Sanchez and the Socialists is that the stagflationary backdrop will weigh on their support over time. Bottom Line: Spanish political risk is likely to spike sooner rather than later, though Spanish domestic risk it is limited in nature. Madrid faces low geopolitical risk, low energy vulnerability, and is not susceptible to trying to leave the EU or Euro Area. Favor Spanish over Italian stocks. Stay Constructive On South Africa The political and economic status quo is largely unchanged in South Africa and will remain so going into the 2024 national elections. Fiscal discipline will weaken ahead of the election, which should be negative for the rand, but the global commodity shortage and geopolitical risks in Russia and China will probably overwhelm any negative effects from South Africa’s domestic policies. Rising commodity prices have propped up the local equity market and will bring in much-needed revenue into the local economy and government coffers. But structural issues persist. Low growth outcomes amid weak productivity and high unemployment levels will remain the norm. The median voter is increasingly constrained with fewer economic opportunities on the horizon. Pressure will mount on the ruling African National Congress (ANC), fueling civil unrest and adding to overall political risk (Chart 8). Chart 8South Africa's Political Status Quo Is Tactically Positive For Equities And Currency

South Africa's Political Status Quo Is Tactically Positive For Equities And Currency

South Africa's Political Status Quo Is Tactically Positive For Equities And Currency

Almost a year has passed since the civil unrest episode of 2021. Covid-19 lockdowns have lifted and the national state of disaster has ended, reducing social tensions. This is evident in the decline of our South Africa GeoRisk indicator from 2021 highs. While we recently argued that fiscal austerity is under way in South Africa, we also noted that fiscal policy will reverse course in time for the 2024 election. In this year’s fiscal budget, the budget deficit is projected to narrow from -6% to -4.2% over the next two years. Government has increased tax revenue collection through structural reforms that are rooting out corruption and wasteful expenditure. But the ANC will have to tap into government spending to shore up lost support come 2024. Already, the ANC have committed to maintaining a special Covid-19 social-grant payment, first introduced in 2020, for another year. This grant, along with other government support, will feature in 2024 and possibly beyond. Unemployment is at 34.3%, its highest level ever recorded. The ANC cannot leave it unchecked. The most prevalent and immediate recourse is to increase social payments and transfers. Given the increasing number of social dependents that higher unemployment creates, government spending will have to increase to address rising unemployment. President Cyril Ramaphosa is still a positive figurehead for the ANC, but the 2021 local elections showed that the ANC cannot rely on the Ramaphosa effect alone. The ANC is also dealing with intra-party fighting. Ramaphosa has yet to assert total control over the party elites, distracting the ANC from achieving its policy objectives. To correct course, Ramaphosa will have to relax fiscal discipline. To this outcome, investors should expect our GeoRisk indicator to register steady increases in political risk moving into 2024. The only reason to be mildly optimistic is that South Africa is distant from geopolitical risk and can continue to benefit from the global bull market in metals. Bottom Line: Maintain a cyclically constructive outlook on South African currency and assets. Tight global commodity markets will support this emerging market, which stands to benefit from developments in Russia and China. Investment Takeaways Stay strategically long gold on geopolitical and inflation risk, despite the dollar rally. Stay long US equities relative to global and UK equities relative to DM-ex-US. Favor global defensives over cyclicals and large caps over small caps. Stay short CNY, TWD, and KRW-JPY. Stay short CZK-GBP. Favor Mexico within emerging markets. Stay long defense and cyber security stocks. We are booking a 5% stop loss on our long Canada / short Saudi Arabia equity trade. We still expect Middle Eastern tensions to escalate and trigger a Saudi selloff. Matt Gertken Chief Geopolitical Strategist mattg@bcaresearch.com Jesse Anak Kuri Associate Editor Jesse.Kuri@bcaresearch.com Yushu Ma Research Analyst yushu.ma@bcaresearch.com Guy Russell Senior Analyst GuyR@bcaresearch.com Footnotes 1 The campaign in the south suggests that Ukraine will be partitioned, landlocked, and susceptible to blockade in the coming years. If Russia achieves its military objectives, then Ukraine will accept neutrality in a ceasefire to avoid losing more territory. If Russia fails, then it faces humiliation and its attempts to save face will become unpredictable and aggressive. Strategic Themes Open Tactical Positions (0-6 Months) Open Cyclical Recommendations (6-18 Months) Regional Geopolitical Risk Matrix Geopolitical Calendar

Dear Client, This week, we present our inaugural report on ESG investing and the global energy transition. Henceforth, we will be publishing this research on the last Thursday of every month. Our principal ESG focus will be on the Environmental aspects of climate change, and the policies and actions undertaken to arrest the rise in the Earth's temperature via decarbonization. To date, the goal of Environmental policy in many jurisdictions – e.g., the US and EU – has been to disincentivize exploration, production, refining and transportation investment in hydrocarbons. At the same time, it has strongly incentivized investment in renewable-power generation. This has produced volatile marginal effects, forcing commodity markets to allocate increasingly scarce energy and metals supplies against a backdrop of increasing demand. It is at this nexus where investment opportunities will emerge. ESG's Social and Governance pillars are slower-moving change agents, with long-duration effects. Human-rights failures can destroy lives and lead to social unrest. Failed corporate governance and national governance can sharply alter firms' abilities and willingness to invest in environmentally responsible resource development. Failure in both dimensions can profoundly affect commodity supply-demand balances, and imperil the energy transition. Much of what passes for ESG measurement and compliance is self-reported – when data are available – and differs little from PR or virtue signaling. This is starting to change. Over the next 2-3 years, we expect a continued increase in government involvement in standardizing ESG reporting – cf, the SEC's recent proposal for reporting Scope 1, 2 and 3 emissions, and an increased focus on carbon pricing, which we believe will require a global carbon tax or carbon-price floor. This will be needed to incentivize investment in renewables and carbon-reduction and -capture technology, given the near-impossibility of harmonizing local and regional carbon-trading schemes. Otherwise climate clubs – i.e., trading blocs comprising states with shared ESG goals – will emerge, which will further fragment global trade. We are hopeful you will find this research useful in your decision making and investing. Bob Ryan Managing Editor, Commodity & ESG Strategy Executive Summary Fossil Fuels Dominate Global Energy Mix

Fossil Fuels Dominate Global Energy Mix

Fossil Fuels Dominate Global Energy Mix

Whether or not the SEC's proposal to disclose Scope 1, 2 and 3 emissions and other risk factors by firms it regulates will be adopted in whole or in part, we are confident it foreshadows deeper government involvement in the ESG arena in the near term in the US and EU. Carbon pricing will become increasingly important in global climate-change policy. We believe this will require a global carbon tax or carbon-price floor to incentivize investment in renewables and carbon-reduction and -capture technology. Failure to agree on at least a carbon price floor over the next 2-3 years almost surely will lead to the formation of climate clubs. In such clubs, like-minded states with similarly rigorous carbon-pricing and ESG disclosure requirements will allow trade among each other, but will levy tariffs against firms in states lacking such policies. Bottom Line: Governments are approaching a reckoning on their commitments to reduce or slow CO2 and greenhouse-gas (GHG) emissions. These are meant to hold the rise in the Earth's temperature to less than 2° C, or to approach the 1.5° C goal of the Paris Agreement. Reporting mandates like the EU's and the SEC's proposed CO2/GHG reports will help, as will increased subsidies and tax support for carbon-capture and hydrogen technology. However, a global carbon tax or carbon-price floor will be required to incentivize the investment needed to meet climate-change goals. Feature Voluntary programs and self-reporting are not reducing the concentration of CO2 and other GHGs fast enough to stay on track to meet Paris Agreement targets of holding the rise in the Earth's temperature to less than 2° C vs, pre-industrial levels, or preferably to 1.5° C. Over the next couple of years, we believe states will have to mandate additional ESG reporting – particularly on CO2 and other GHG emissions – and will require audits of programs and reports connected to GHG emissions, given the scope of what they are trying to accomplish. The EU got the ball rolling on reporting emissions, and now the US SEC is proposing new regulations as well. These will require the firms it regulates to disclose Scope 1, 2 and 3 emissions and other climate-related factors that constitute material risks to revenues and profits.1 Regardless of whether this proposal makes it through the legislative process, firms with operations in the EU will have to comply with similar reporting requirements if similar proposals are approved. Growing Energy Demand Fuels Higher CO2 Emissions World electricity demand – the principal focus of the global energy transition – grew 6% last year, on the back of strong GDP growth and weather-related demand. 2021 saw the highest electricity demand growth recorded by the IEA in the post-GFC recovery that began in 2010, amounting to 1,500 Twh year-on-year. Coal covered more than half of the growth in global electricity demand last year, and has constituted a major chunk of the electricity mix over a longer historical sample. Based on data starting in 2000, the world – primarily EM – has been net positive coal-fired power capacity (Chart 1) which reached an all-time high in 2021 as well, rising 9% y/y, while gas-fired generation grew 2%. The increase in fossil fuel generation pushed CO2 emissions globally up almost 6% to record highs. Renewable generation grew by 6% last year and is expected to meet most of the increase in electricity demand over the 2022-24 period with 8% p.a. growth, according to the IEA. Coal demand surged on the back of robust economic growth and weather-related factors, which helped propel global CO2 emissions to a record high at just over 36 billion MT in 2021, according to the IEA. This reversed the downturn in 2020 caused by the COVID-19 pandemic (Chart 2). Higher methane and nitrous oxide emissions, plus CO2 released by oil and gas flaring, lifted total energy-related GHG emissions to record levels last year as well. Chart 1Coal-Fired Power Has Been A Constant

Looking Through ESG Virtue Signaling

Looking Through ESG Virtue Signaling

Chart 2Fossil Fuels Dominate Global Energy Mix

Fossil Fuels Dominate Global Energy Mix

Fossil Fuels Dominate Global Energy Mix

We find evidence of a long-run relationship between real GDP and carbon dioxide emissions (Chart 3). This likely plays out through cointegration between oil consumption with real GDP, a relationship we exploit when estimating our monthly oil balances. While the income elasticity for emerging economies reliant on manufacturing – e.g., India and China – is positive, for the EU, a bloc of developed nations, that elasticity turns negative. This is consistent with the hypothesis of the Environmental Kuznets Curve, which states that initial increases in GDP per capita are associated with environmental degradation, however, beyond a point, income increases are associated with lower environmental damage.2 Interesting, as well, is the lack of any cointegration between GDP and US CO2 emissions. That may be due to the increased use of natgas vs. coal, and the fact that the energy intensity of US GDP continues to fall. Energy demand levels, including electricity, continues to exceed renewables supply. So even though renewable-energy generation growth is expected to meet 90% of energy demand growth from 2022 to 2024, the accumulation of CO2 and other GHGs will continue keeping the level of pollutants rising over that period. Chart 3CO2 Closely Tied To GDP

CO2 Closely Tied To GDP

CO2 Closely Tied To GDP

Recent research on global CO2 emissions growth for different countries based on historical values for population, GDP per capita and carbon intensity (measured as CO2 emissions per unit of GDP) projects median annual CO2 emissions in 2100 will be 34 Gigatons (Chart 4).3 This is significantly higher than the emissions required to keep temperature increases under 2° C by the end of the forecast period. The forecast is accompanied by four other CO2 emission scenarios provided by the Intergovernmental Panel on Climate Change (IPCC). Chart 4CO2 Projected Increases Overshoot Paris Agreement Targets

Looking Through ESG Virtue Signaling

Looking Through ESG Virtue Signaling

Carbon Tax Needed One of our high-conviction views is governments worldwide need to agree a global carbon tax that can be applied directly to CO2 emissions.4 If a global carbon tax cannot be agreed, a global carbon-price floor also could be used to incentivize the investment needed to meet climate-change goals. An IMF analysis entitled "Five Things To Know About Carbon Pricing" published in September notes: "An international carbon price floor can be strikingly effective. A 2030 price floor of $75 a ton for advanced economies, $50 for high-income emerging market economies such as China, and $25 for lower-income emerging markets such as India would keep warming below 2°C with just six participants (Canada, China, European Union, India, United Kingdom, United States) and other G20 countries meeting their Paris pledges." There may be legitimate grounds for arguing over the point at which the tax is collected – i.e., at the production or consumption stages – but, in our view, this would be far superior (and quicker to implement) than trying to harmonize the different carbon-trading schemes worldwide. In addition, the revenues generated by the tax would allow governments to protect the interests of lower-income constituencies, which are most adversely affected by such regressive taxes. We also have maintained failure to agree a carbon tax of some form over the next 2-3 years almost surely will lead to the formation of climate clubs, a notion pioneered by William Nordhaus, the 2018 Nobel Laurate.5 In Nordhaus's clubs, like-minded states with similarly rigorous carbon-pricing and ESG disclosure requirements will allow trade among each other, but will levy tariffs against firms in states lacking such measures. There is some evidence China already is preparing for this eventuality by limiting the export of high-carbon products to consumer states with strong climate-protection laws. For example, the EU last year rolled out a Carbon Border Adjustment Mechanism (CBAM), which it describes as "a climate measure that should prevent the risk of carbon leakage and supports the EU's increased ambition on climate mitigation, while ensuring WTO compatibility."6 Investment Implications Governments are moving quickly to address shortcoming in existing CO2 and GHG reduction policies. Among other things, the EU and US are proposing mandatory reporting on these emissions covering Scope 1, 2 and 3 emissions. In addition, China is refining its five-year plan to limit high-carbon exports, so that it does not run afoul of the EU's CBAM. We expect more of such measures going forward, as CO2 and GHG emissions continue to accumulate in the atmosphere at a rate that cannot be offset by existing policy. Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Ashwin Shyam Research Analyst Commodity & Energy Strategy ashwin.shyam@bcaresearch.com Paula Struk Research Associate Commodity & Energy Strategy paula.struk@bcaresearch.com Footnotes 1 Scope 1 covers GHG emissions firms directly generate on their own; Scope 2 applies to emissions indirectly created a purchasing electricity and other forms of energy; and Scope 3 covers indirect emissions produced up and down the firms' supply chain. These are deemed to be material risks that could impact firms' revenues and profitability, hence necessary information for investors and market participants generally. Please see SEC Proposes Rules to Enhance and Standardize Climate-Related Disclosures for Investors, published by the SEC on March 21, 2022. 2 For more information on this, please see ScienceDirect’s page on the Environmental Kuznets Curve. 3 Please see Country-based rate of emissions reductions should increase by 80% beyond nationally determined contributions to meet the 2 degree Celsius target (Liu and Rafter, 2021), published in Nature. 4 Please see Surging Metals Prices And The Case For Carbon-Capture, which we published on May 13, 2021. It is available at ces.bcaresearch.com. 5 Please see Nordhaus, William (2015), "Climate Clubs: Overcoming Free-riding in International Climate Policy," American Economic Review 105:4, pp. 1339–1370. 6 Please see Carbon Border Adjustment Mechanism: Questions and Answers, published by the European Commission on July 14, 2021. See also China issues guidelines under 14th 5-year plan to limit high-carbon product exports, published by S&P Global Platts on April 7, 2022. Platts notes this likely will be China's first FYP to include limits on "high-carbon products from the (refining and petrochemical) industry amid China's carbon neutrality journey. This comes amid expectations that foreign countries may levy tariffs like the EU's Cross Border Adjustment Mechanism, or CBAM, on such products in the future." Investment Views and Themes Recommendations Strategic Recommendations Trades Closed in 2022

Image

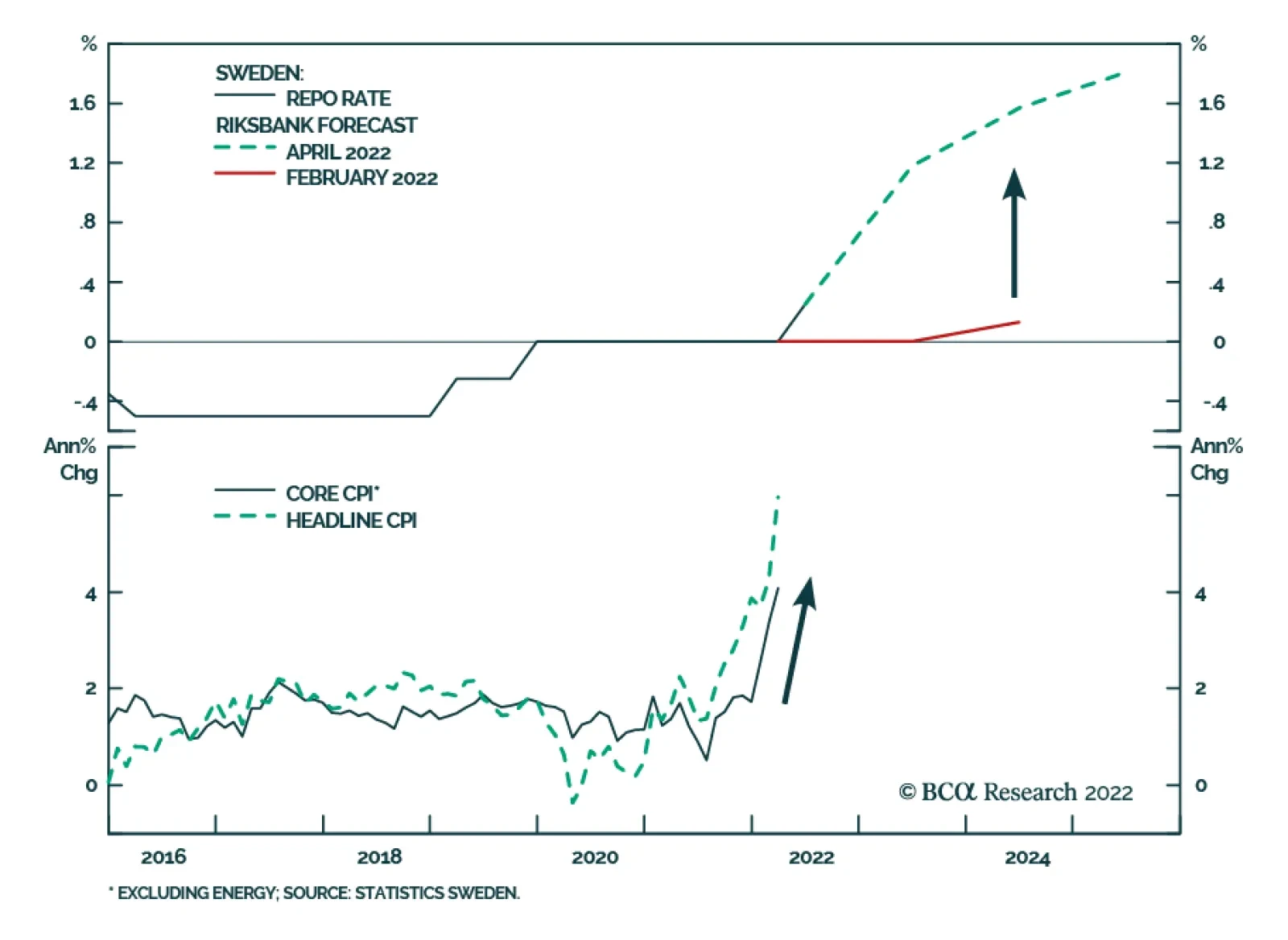

Sweden’s Riksbank unexpectedly lifted its policy rate from zero to 0.25% on Thursday – marking an earlier-than-anticipated start to the tightening cycle. The central bank also announced plans to reduce the pace of asset purchases in the second half of the…

Highlights All four of our US Equity indicators are currently pointing in a bearish direction. Our Monetary Indicator has fallen to a three decade low, our Technical Indicator has broken into negative territory, our Valuation Indicator still signals extreme equity pricing, and our Speculation Indicator does not yet support a contrarian buy signal. Still, we do not expect a US recession over the coming year, which implies that S&P 500 revenue growth will stay positive. Nonrecessionary earnings contractions are rare, and are almost always associated with a significant contraction in profit margins. Our new profit margin warning indicator currently suggests the odds of falling margins are low, although the risks may rise later this year. Stocks are extremely expensive, but rich valuations are being driven by extremely low real bond yields, rather than investor exuberance. Valuation is unlikely to impact US stock market performance significantly over the coming year unless long-maturity bond yields rise substantially further. Technical analysis of stock prices has a long and successful history at boosting investment performance, which ostensibly suggests that investors should be paying more attention to technical conditions in the current environment. However, technical trading rules have been less helpful in expansionary environments when inflation is above average and when stock prices and bond yields are less likely to be positively correlated (as is currently the case). As such, the recent technical breakdown of the US equity market may simply reflect a reduced signal-to-noise ratio associated with these economic and financial market regimes. For now, we see our indicators as supportive of a cautious, minimally-overweight stance toward stocks within a multi-asset portfolio over the coming 6 to 12 months. Rising odds of a recession, declining profit margins, and a large increase in investor or Fed expectations for the neutral rate of interest are the most significant threats to the equity market, the risks of which should be monitored closely by investors. Feature In Section 1 of our report, we reviewed why a recession in the US is unlikely over the coming 6 to 12 months. However, we also highlighted that the risks to the economic outlook are meaningful and that an aggressively overweight stance toward risky assets is currently unwarranted. During times of significant uncertainty, investors should pay relatively more attention to long-term economic and financial market indicators with a reliable track record. In this report we begin by briefly reviewing the message from our US Equity Indicators, and then turn to a deeper examination of the top-down outlook for earnings, the determinants of rich valuation in the US stock market, and whether investors should rely on technical indicators in the current environment. We conclude that, while an indicator-based approach is providing mixed signals about the US equity market, we generally see our indicators as supportive of a cautious, minimally-overweight stance toward stocks within a multi-asset portfolio. Aside from tracking the risk of a recession, investors should be closely attuned to signs of a contraction in profit margins or shifting neutral rate expectations as a basis to reduce equity exposure to below-benchmark levels. A Brief Review Of Our US Equity Indicators Chart II-1Our Equity Indicators Are Pointing In A Bearish Direction

Our Equity Indicators Are Pointing In A Bearish Direction

Our Equity Indicators Are Pointing In A Bearish Direction

Chart II-1 presents our US Equity Indicators, which we update each month in Section 3 of our report. We highlight our observations below: Chart II-1 shows that our Monetary Indicator has fallen to its lowest level since 1995, when the Fed surprised investors and shifted rapidly in a hawkish direction. The indicator is most acutely impacted by the speed of the rise in 10-year Treasury yields and a massive surge in the BCA Short Rate Indicator to levels that have not prevailed since the late 1970s (Chart II-2). Our Technical Indicator has recently broken into negative territory, which we have traditionally interpreted as a sign to sell stocks. The indicator has been dragged lower by a deterioration in stock market breadth across several tracked measures and by weak sentiment (Chart II-3). The momentum component of the indicator is fractionally positive but is exhibiting clear weakness. Our Valuation Indicator continues to highlight that US equities are extremely overvalued relative to their history, despite the recent sell-off in stock prices. Our Speculation Indicator arguably provides the least negative signal of our four indicators, at least from a contrarian perspective. In Q1 2021, the indicator nearly reached the all-time high set in March 2000, but it has since retreated significantly and has exited extremely speculative territory. While this may eventually provide a positive signal for stocks, equity returns have historically been below average during months when the indicator declines. Thus, the downtrend in the Speculation Indicator still points to weakness in stock prices, at least over the nearer term. Chart II-2Our Monetary Indicator Is Falling In Part Because Of Surging Interest Rate Expectations

Our Monetary Indicator Is Falling In Part Because Of Surging Interest Rate Expectations

Our Monetary Indicator Is Falling In Part Because Of Surging Interest Rate Expectations

Chart II-3All Three Components Of Our Technical Indicator Are Falling

All Three Components Of Our Technical Indicator Are Falling

All Three Components Of Our Technical Indicator Are Falling

In summary, all four of our US Equity indicators are currently pointing in a bearish direction, which clearly argues against an aggressively overweight stance favoring equities within a multi-asset portfolio. At the same time, we reviewed the odds of a US recession over the coming year in Section 1 of our report and argued that a recession is not likely over the coming 12 months. Thus, one key question for investors is whether a nonrecessionary contraction in earnings is likely over the coming year. We address this question in the next section of our report, before turning to a deeper examination of the relative importance of equity valuation and technical indicators. Gauging The Risk Of A Nonrecessionary Earnings Contraction Chart II-4Nonrecessionary Earnings Declines Usually Occur Due To Falling Margins

Nonrecessionary Earnings Declines Usually Occur Due To Falling Margins

Nonrecessionary Earnings Declines Usually Occur Due To Falling Margins

Based on S&P data, there have been five cases since 1960 when 12-month trailing earnings per share fell year-over-year, while the economy continued to expand (Chart II-4). Sales per share growth remained positive in four of these cases (panel 2), underscoring that falling profit margins have been mostly responsible for these nonrecessionary earnings declines. We have noted our concern about how elevated US profit margins have become and have argued that a significant further expansion is not likely to occur over the coming 12-24 months.1 To gauge the risk of a sizeable decline in margins over the coming year, we construct a new indicator based on the seven instances when S&P 500 margins fell outside the context of a recession. This includes two cases when margins fell but earnings did not (because of buoyant revenue growth). We based the indicator on these five factors: Changes in unit labor cost growth to measure the impact of wage costs on firm profitability; Lagging changes in commodity prices as a proxy for material costs; The level of real short-term interest rates as a proxy for borrowing costs; Changes in a sales growth proxy to measure the impact of operating leverage on margins; And changes in the ISM manufacturing index to capture any residual impact on margins from the business cycle. Chart II-5The Odds Of A Nonrecessionary Profit Margin Contraction Are Currently Low

The Odds Of A Nonrecessionary Profit Margin Contraction Are Currently Low

The Odds Of A Nonrecessionary Profit Margin Contraction Are Currently Low

Chart II-5 presents the indicator, which is shaded both for recessionary periods and the seven nonrecessionary margin contraction episodes we identified. While the indicator does not perfectly predict margin contractions outside of recessions, it did signal 50% or greater odds of a margin contraction in four of the seven episodes we examined, and signals high odds of a contraction in margins during recessions. Among the three cases in which the indicator failed to indicate falling margins during an expansion, two of those failures were episodes when earnings growth did not ultimately contract. The inability to explain the 1997-1998 margin contraction is the most relevant failure of the indicator, in addition to two false signals in 1963 and 1988. Still, the approach provides a useful framework to gauge the risk of falling profit margins, and the results provide an interesting and somewhat surprising message about the relative importance of the factors we included. We would have expected that accelerating wages would have been the most significant factor explaining nonrecessionary profit margin declines. Wages were highly significant, but they were the second most important factor behind our sales growth proxy. Lagged commodity prices were the third most significant factor, followed by real short-term interest rates. Changes in the ISM manufacturing index were least significant, underscoring that our sales growth proxy already captures most of the effect of the business cycle on profit margins. This suggests that operating leverage is an important determinant of margins during economic expansions, and that investors should be most concerned about declining profit margins when both revenue growth is slowing significantly and wage growth is accelerating. The indicator currently points to low odds of a nonrecessionary margin contraction, but this is likely to change over the coming year. We expect that all five of the factors will evolve in a fashion that is negative for margins over the coming twelve months: While the pace of its increase is slowing, median wage growth continues to accelerate, even when adjusting for the fact that 1st quartile wage growth is growing at an above-average rate (Chart II-6). Combining the latter with higher odds of at or below-trend growth this year implies that unit labor costs may rise further over the coming twelve months. Analysts expect S&P 500 revenue growth to slow nontrivially over the coming year (Chart II-7). Current expectations point to growth slowing to a level that would still be quite strong relative to what has prevailed over the past decade; however, accelerating wage costs in lockstep with decelerating revenue growth is exactly the type of combination that has historically been associated with falling margins during economic expansions. Chart II-6Wage Growth Is Accelerating...

Wage Growth Is Accelerating...

Wage Growth Is Accelerating...

Chart II-7...And Revenue Growth Is Set To Slow

...And Revenue Growth Is Set To Slow

...And Revenue Growth Is Set To Slow

Although these are less impactful factors, the lagged effect of the recent surge in commodity prices will also weigh on margins over the coming year, as will rising real interest rates and a likely slowdown in manufacturing activity in response to slower goods spending. In addition to our new indicator, we have two other tools at our disposal to track the odds of a decline in profit margins over the coming year. First, Chart II-8 illustrates that an industry operating margin diffusion index does a decent job at leading turning points in S&P 500 profit margins, despite its volatility. And second, Chart II-9 highlights that changes in the sales and profit margin diffusion indexes sourced from the Atlanta Fed’s Business Inflation Expectations Survey have predicted turning points in operating sales per share and margins over the past decade. Chart II-9 does suggest that profit margins may not rise further, but flat margins are not likely to be a threat to earnings growth over the coming year if a recession is avoided (as we expect). Chart II-8Sector Diffusion Indexes Are Not Signaling A Major Warning Sign For Margins...

Sector Diffusion Indexes Are Not Signaling A Major Warning Sign For Margins...

Sector Diffusion Indexes Are Not Signaling A Major Warning Sign For Margins...

Chart II-9...Neither Are The Atlanta Fed Business Sales And Margin Diffusion Indexes

...Neither Are The Atlanta Fed Business Sales And Margin Diffusion Indexes

...Neither Are The Atlanta Fed Business Sales And Margin Diffusion Indexes