Europe

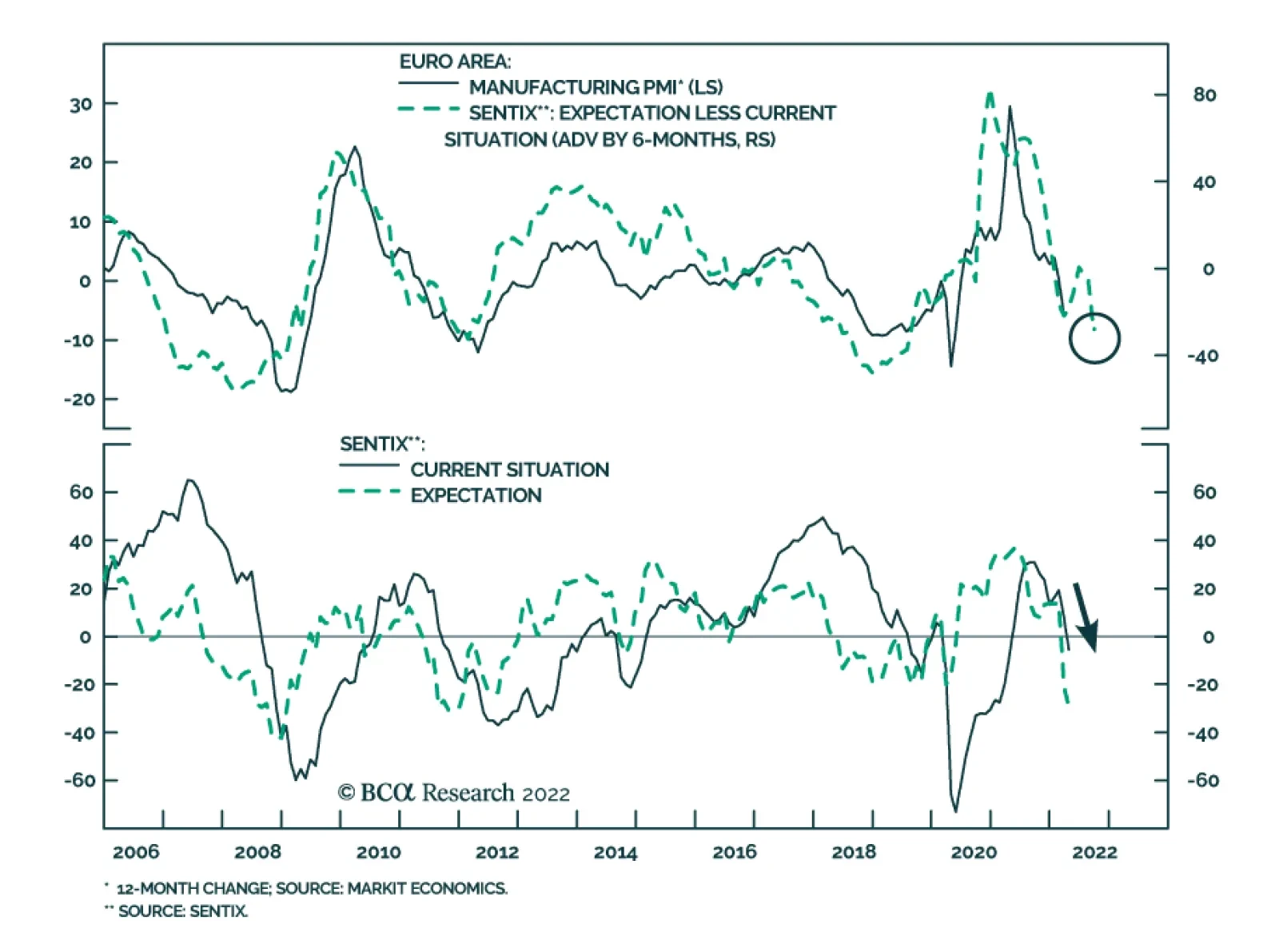

The April Sentix Economic Index sent a negative signal about investor morale. The overall index for the Eurozone collapsed 11 points to -18 – the lowest since July 2020 and a negative surprise to expectations of -9.4. The sharp decline reflects a…

Executive Summary Cheap Or Expensive?

Cheap Or Expensive?

Cheap Or Expensive?

President Emmanuel Macron will be re-elected.French growth will slow in the coming quarters but will also remain solid beyond that horizon.France’s reform push will continue, particularly pension reforms and efforts to reduce inefficiencies. However, austerity is unlikely to materialize.French stocks will underperform once energy inflation peaks. Consumer discretionary and staples have run ahead of themselves relative to the broad market and to their European peers. French small-cap stocks and aerospace and defense equities are attractive.RecommendationsINCEPTIONDATERETURN (%)COMMENTBuy French Small-Caps Equities / Sell French Large-Caps Equities (*)04/04/2022 CyclicalSell French Consumer Equities Relative to French Benchmark (*)04/04/2022 CyclicalOverweight French Aerospace & Defense**04/04/2022 Structural Bottom Line: A second Macron presidency will not boost the appeal of French large-cap equities, even if it helps French long-term growth. Investors should underweight the French market in Europe via a large underweight in French consumer discretionary and consumer staple stocks. However, investors should overweight French defense names as well as small-cap equities.FeatureThe French presidential election is upon us. President Emmanuel Macron ambitious pro-growth and pro-business reform agenda in 2017 tackled the roots of the French malaise of the past decades. Our conviction that Macron would win a second mandate has survived challenges such as the “Yellow Vest Movement” in 2019 and then COVID-19. Now, with the shock of the Ukraine war, the evidence still suggests he will win the upcoming election. Chart 1Five More Years Of Macron

France: Macron And Macro

France: Macron And Macro

Macron is the favorite with 53% of voting intentions against Marine Le Pen in the second round of the election (Chart 1). Even a potential Russian interference in the French election wouldn’t change the outcome of such a duel, which we discussed at length last summer. Since then, Macron’s advantages over Le Pen have only strengthened, boosted by his handling of Omicron and the Ukraine/Russia crisis while the center-right and the far-right battle each other (Chart 1, bottom panel).Macron also took the unofficial leadership of Europe after Angela Merkel exited the stage. He managed to breathe new life into the European Union (EU), bringing forth greater unity. As a result, the current war in Ukraine and elevated energy prices have made this political rendez-vous more relevant. Chart 2Less Euroscepticism Helps Macron

Less Euroscepticism Helps Macron

Less Euroscepticism Helps Macron

The main axis of Macron’s next term is to make France a more independent nation within a stronger Europe. This is a paradox, but what it means is that he is capitalizing on the current geopolitical climate of great power struggle and hypo-globalization. France is breaking with its tradition of Euroscepticism to secure its national interests within a closer European bloc (Chart 2).True, the French economy will not be spared from the current stagflation episode and growth will slow in the near term. However, France is in a better position to withstand the energy shock than most of its European peers.After Macron is re-elected, his political capital will be replenished and his structural reform effort will continue, albeit with modifications to deal with the post-pandemic and post-Ukraine environment. Fiscal and monetary policies remain very accommodative. As a result, Macron has a favorable chance of reforming France further. Pension reform as well as the green and digital transitions will improve France’s economic competitiveness over the long run.2017 vs. 2022: One Pandemic, One Recession, And One War Later Chart 3The French Economy Will Surprise To The Upside

France: Macron And Macro

France: Macron And Macro

France was badly hit by COVID-19. However, appropriate fiscal policy and strong domestic demand are driving the recovery (Chart 3). While most sectors are expected to recover fully by 2023, a few sectors, such as automotive, aeronautics, and tourism, still lag behind pre-pandemic levels (Chart 3, panel 2). On the upside, France appears to be doing better than the other major European economies (Chart 3, bottom panel). Moreover, about 1.5% of GDP worth of leftover funds from emergency measures and the recovery plan are to be deployed in 2022.The Ukrainian conflict challenges this positive backdrop. Growth forecasts for 2022 were revised to 2.8% from 4%. The impact from elevated energy prices is projected to reduce annual GDP growth by 0.7% and to trim an additional 0.2% once international spillovers are factored in (Table 1). Nonetheless, France is not as vulnerable to Russian energy as Germany and Italy (Chart 4). For now, Russia-EU energy flow continues, although the threats are rising. Germany once again rejected an energy boycott when Biden visited Europe two weeks ago, but it is also preparing for the eventuality that gas flows may dry up, which highlights the fluidity of the situation. Table 1Impact Of High Energy Prices

France: Macron And Macro

France: Macron And Macro

Chart 4Low Vulnerability To Russian Energy…

France: Macron And Macro

France: Macron And Macro

The direct consequences of the conflict on French exports are limited. Russia, Ukraine, and Belarus represent 1.2% of French exports, or EUR12 billion, most of which comes from transport equipment and other manufactured goods (Table 2). Table 2… And Low Trade Exposure

France: Macron And Macro

France: Macron And Macro

The evolution of the Chinese economy is another major external influence on French growth. France is exposed to the deceleration of the Chinese manufacturing PMI induced by the slowdown in Chinese credit growth. The recent closing of cities like Shanghai or Shenzhen because of the spread of the Omicron variant will accentuate near-term risks. However, Chinese policymakers want to stabilize growth by the time the Communist Party reshuffles this fall and the credit impulse is trying to bottom, which will help French exports to China improve later this year or next (Chart 5).Higher inflation is another consequence of supply disruptions and elevated energy prices caused by the Ukrainian war. For now, this is not a pressing concern in France. Headline inflation came in at 5.1%, well below the European average (Table 3). The government intervened to shield consumers from rising energy prices by handing out energy vouchers, freezing gas prices until the end of the year, and cutting electricity taxes. Chart 5France Is Sensitive To The Chinese Economy

France Is Sensitive To The Chinese Economy

France Is Sensitive To The Chinese Economy

Table 3Lower Inflation In France

France: Macron And Macro

France: Macron And Macro

Chart 6French Households Accumulated Plenty Of Excess Savings

France: Macron And Macro

France: Macron And Macro

This is good news for French households, as it preserves some of their purchasing power, especially when compared to Spanish households that suffer an inflation rate of 9.8%. However, it is not enough to prevent consumer confidence from crumbling. From Table 1, consumer spending is projected to fall by 1%. Yet, French consumers benefit from their large savings, accumulated during the pandemic (Chart 6). Unlike the US, where the household savings rate has already gone back to pre-pandemic levels, the savings rate in France is still high. Households can use those excess savings to mitigate elevated energy prices.With respect to employment, the generous French furlough scheme contributed to this accumulation of savings by limiting the rise in unemployment (Chart 7). Therefore, the French labor market was resilient throughout the crisis and has recovered quickly. Labor force participation exceeds its pre-crisis level by about 0.5%. Youth unemployment reached its lowest level since the 1980s, at 14.8 %, in part because of the 2017 labor and vocational reforms. Moreover, labor market conditions are now tighter than they were pre-pandemic and firms are increasingly complaining about labor shortages (Chart 8). The business sector still expects employment growth to remain as robust as it was in 2018. As a result, French wage growth will firm up before the year-end. Chart 7The French Labor Market Has Recovered...

The French Labor Market Has Recovered...

The French Labor Market Has Recovered...

Chart 8...And Is Showing Signs Of Tightening

...And Is Showing Signs Of Tightening

...And Is Showing Signs Of Tightening

The corporate sector has several reasons to be optimistic (Chart 9). The emergency measures prevented widespread corporate defaults and bank lending remained supportive through the crisis. Profit margins are high. Additionally, conducting business in France is becoming easier. Business creation has continued to rise (Chart 9, bottom panel) and FDI projects were up 32% in 2021, making France the largest investment destination in Europe. Nonetheless, the rise in non-financial gross corporate debt is concerning, even though the increase in net debt was limited by the jump in bank deposits during the crisis (Chart 10). Chart 9France Is Becoming More Business Friendly

France Is Becoming More Business Friendly

France Is Becoming More Business Friendly

Chart 10Corporate Debt Is A Concern

France: Macron And Macro

France: Macron And Macro

Bottom Line: French growth will decelerate in the coming quarter in response to the Ukrainian crisis, but it will remain stronger than that of its European peers. In the second half of the year, stronger demand recovery in hard-hit sectors, Chinese stimulus, European fiscal support, pent-up demand, and a declining energy drag will allow growth to recover markedly.Reforms: Take 2(022)The series of recent crises highlight several weaknesses in the French economy. The pandemic revealed how vulnerable and underfunded the French health sector is. It also underscored that digitalization is inadequate in French firms. The Ukraine/Russia conflict is mixed: it underscores the energy dependence of European countries and highlights the need for greater defense spending, even if France is already less dependent than others and manufactures state of the art military equipment.Related ReportEuropean Investment StrategyFrance: More Than Just A Déjà-VuIn both crises, the French social welfare state played a crucial role as an automatic stabilizer. The IMF estimates that stabilizers absorbed about 80% of the household income shock during the pandemic, while government spending to contain high energy prices amounted to €15.5 billion since last fall.The fiscal response to these crises caused a large addition to the public debt, which already stands at 115% of GDP. Furthermore, at 55% of GDP before COVID, France’s public expenditure ratio was already one of the highest in the Eurozone (Chart 11). For now, the debt burden is manageable because low interest rates make France’s debt arithmetic benign. However, such an elevated share of output controlled by the government increases resource misallocation and hurts productivity, meaning it weighs on potential GDP growth.Low interest rates are not guaranteed in the future. Putting France’s debt on a sustainable path requires structural reforms (Chart 12). Already, the OECD estimates that the 2017-2018 labor-market and tax reforms have generated positive economic spillovers across all income levels (Chart 12, bottom panel). Chart 11Public Debt Just Got Bigger

France: Macron And Macro

France: Macron And Macro

Chart 12Structural Reforms & Pubic Debt

France: Macron And Macro

France: Macron And Macro

Going forward, reducing debt and cutting spending will be hard considering France’s energy and defense structural goals. Macron’s political party, En Marche!, may perform well in this year’s legislative election, but it is unlikely to achieve the sweeping victory that it saw in 2017. Macron will therefore be forced to compromise to build a coalition in favor of structural reform. His strength in the Assembly will be the chief uncertainty and critical determinant of his ability to achieve his key reform goals in the coming five years. As a result, Macron will focus on lifting French trend growth further by encouraging digital and green transitions. Beyond pension reforms, fiscal austerity will be limited to ensure the social acceptability of structural reforms.In the rest of this section, we focus on the two most important reforms proposed by Macron for his second mandate: pensions and economic competitiveness plans. Reducing public spending is needed to alleviate the burden on resources created by the massive size of the French government, but France’s strategic needs outstrip Macron’s ability to slash spending.French Pension System: Too Generous Table 4Public Spending Comparison

France: Macron And Macro

France: Macron And Macro

Pension represents 14% of GDP compared with 10% in Germany (Table 4). Expenditures on pension explains 35% of the difference on total public spending between France and the Euro Area.Reforming the pension system is a sensitive topic in France. It arguably cost Nicolas Sarkozy his re-election bid in 2012. Yet, pension reforms are essential. The current system is complex and fragmented, with 42 different types of coexisting pensions, each with its own calculation rules. Chart 13Pension Reform Is Long Overdue

France: Macron And Macro

France: Macron And Macro

Additionally, it does not reflect the ageing of the population (Chart 13). Employment among the 55-64 age cohort is only 56% in France, compared to 62% in the OECD average. Also, the effective retirement age in France is 60.8, compared with an average of 65 in Europe. Furthermore, replacement rates (pension / last salaries) are high, which puts an unsustainable burden on the state’s finances.According to the French think tank Institut Montaigne, progressively pushing the retirement age to 65 would save €7.7 billion per year by 2027 and €18 billion per year by 2032. Overall, the government would save around €50 billion per year through such pension adjustments and simplification reforms as well as by operating cost reductions. This would largely finance Macron’s investment to improve competitiveness, digitalization, the green transition, and national defense.Transitioning To Reduce InefficienciesTo boost long-term growth, an important prong of Macron’s project is the €100 billion “France Relance” recovery plan. It is part of the NGEU pandemic relief funds and includes €30 billion for green transition (including measures to improve energy performance of buildings, to increase rail freight, and to support businesses to make the transition). It also includes €34 billion for competitiveness and innovation (tax cuts and support for digitalization). Chart 14French Handicap: Productivity

France: Macron And Macro

France: Macron And Macro

This plan is a band-aid if the many inefficiencies undermining France’s productivity are not tackled (Chart 14). The uptake of digital technologies is uneven and lags far behind other developed nations with respect to cloud computing and the internet of things. Small businesses perform particularly poorly (Chart 15). As a result, the French tech sector has become a priority of Macron’s government. The “France 2030” investment plan unveiled in October 2021, worth €30 billion over five years, aims to foster industrial and tech “champions of the future.” It intends to lift business creation in the tech sector. Nonetheless, this is easier said than done; picking low-hanging fruits will help productivity but matching the prowess of the US is highly unlikely.Another problem is the inefficiency of French R&D. Government support for business R&D is elevated but does not translate into high R&D intensity (Chart 16). This problem is not unique to France: R&D returns across the EU do not match those of the US. Addressing France’s bureaucratic and extremely centralized management structure could tackle some of this hindrance (Chart 16, bottom panel). Chart 15France Is Digitally Lagging …

France: Macron And Macro

France: Macron And Macro

Chart 16… And Full Of Inefficiencies

France: Macron And Macro

France: Macron And Macro

When it comes to the green transition, Macron focuses on three axes: renewable energies, energy efficiency, and electric vehicles.Macron wants a “massive deployment” of renewable energies. A new plan for the construction of additional nuclear reactors will be implemented, since it is the only solution that allows France to reduce its carbon emissions quickly. Alongside this plan for electricity generation, a strategy will be put in place to increase energy efficiency. This is where the support to electric vehicle production and adoption comes in (Chart 17).Reforming energy taxes is another avenue to generate greater revenues, such as from higher carbon pricing, and this would help finance more green investments. Eliminating fossil fuel subsidies, for which France spends significantly more than its peers, and streamlining tax collectioncould yield 1% in annual savings by 2027 (Chart 18). Moreover, increasing carbon prices to EUR65 per ton by 2030 would contribute to France’s environmental goals and provide additional revenue. Chart 17French EV-olution

France: Macron And Macro

France: Macron And Macro

Chart 18More Green Taxes

France: Macron And Macro

France: Macron And Macro

Bottom Line: The re-election of President Macron portends another reform push in France. The large public debt load threatens national long-term economic prospects. Hence, increasing potential GDP growth is paramount. True, Macron’s majority in the Assemblée Nationale will decrease, which will limit the scope of the next reform round. Nonetheless, France will implement pension reforms that can both increase the size of the labor force and finance further initiatives. Moreover, France will push forward with efforts to streamline tech investment, increase spending in the nuclear electricity production, and boost energy efficiency.Investment ImplicationsThe investment implications of a second Macron mandate are manifold. First, investors should remain overweight the French tech sector compared to that of the rest of the Eurozone because of the boost to earnings from greater public investment. Chart 19Small-Caps, Big Upside

Small-Caps, Big Upside

Small-Caps, Big Upside

French small-cap stocks will also benefit from reforms. French small-cap equities have become oversold relative to their large-cap counterparts, falling 30% in relative terms since their late 2017 peak (Chart 19). Part of that underperformance anticipated the drag on French households from spiking energy prices. However, French households are more insulated from the impact of high inflation than their US or European counterparts. Moreover, the previous set of reforms boosted lower- and middle-class income (Chart 12 on page 9). Consequently, French consumer confidence will grow compared to that in the US and China, which helps the relative performance of French small-cap shares (Chart 19, panel 2). Rising German yields and an eventual stabilization in the euro will also buoy these stocks (Chart 19, bottom two panels).French industrials equities will be another sector to enjoy a dividend from Macron’s policy initiatives. The “France 2030” plan involves an increase in capex. The build-up in nuclear power under the green transition plan is also positive for industrial earnings. These policies will favor domestic spending, which bolsters French industrial stocks.Last week, we described the tailwinds for European aerospace and defense equities. The same logic holds true for French aerospace and defense names, which are our favorite plays within the French industrial complex. Chart 3 on page 3 highlighted that the aerospace sector is among the major areas of the economy for which gross value added has yet to recoup its pandemic losses. The gradual re-opening of the global economy will create an important tailwind for the sector. Moreover, France is the fourth-largest global defense exporter. Thus, the French defense industry will profit from the upside in global military spending.Related ReportGeopolitical StrategyFrance: Macron (And Structural Reforms) Still Favored In 2022In this context, French aerospace and defense stocks should outperform not only the overall French market, but also their industrial peers (Chart 20). Since we already favor aerospace and defense equities within the Euro Area, the overweight of French aerospace and defense shares does not translate into an overweight compared to their European competitors. The position of French large-cap stocks within a European portfolio is more complex. They are unlikely to exhibit any significant net impact from Macron’s reform push. French equities have outperformed the rest of Europe already. Most of this outperformance reflected sectoral biases; the French market overweights industrial and consumer stocks. However, the country effect explains the recent outperformance of French equities (Chart 21). The country effect can be approximated by comparing French stocks to the rest of the European market on a sector-neutral basis. Chart 20Favor French Aerospace & Defense

Favor French Aerospace & Defense

Favor French Aerospace & Defense

Chart 21Country Effect Explains The Recent Outperformance Of French Equities

Country Effect Explains The Recent Outperformance Of French Equities

Country Effect Explains The Recent Outperformance Of French Equities

The lower vulnerability of the French economy to higher energy prices compared to the rest of Europe explains this outcome (see Chart 4 on page 4). The outperformance of French consumer stocks (which account for nearly a third of the index) relative to their European competitors added to the country effect as well.An end to the energy spike is likely to arrest the outperformance of French equities. Over the past six years, Brent crude oil prices expressed in euros as well as oil and gas inflation have supported the performance of French equities relative to German ones much better than core inflation or bond yields (Chart 22). The forward earnings of French equities compared to those of the Eurozone market closely track energy markets (Chart 23). Essentially, the French market biases and the country’s low reliance on imported energy are valuable hedges when stagflation fears are rampant (Chart 24). Chart 22The End Of The French Reign Draws Near

The End Of The French Reign Draws Near

The End Of The French Reign Draws Near

Chart 23Supply Shock Lifted French Earnings

Supply Shock Lifted French Earnings

Supply Shock Lifted French Earnings

The best vehicle to underweight French large-cap stocks is to underweight French consumer stocks compared to the Euro Area MSCI benchmark. French equities outperformed the rest of Europe by a greater extent than relative earnings would have implied, which resulted in a small P/E expansion (Chart 25). However, when consumer stocks are excluded, French stocks have performed in line with the rest of the Euro Area and have underperformed relative earnings, which has caused a derating of the French market excluding consumer stocks (Chart 25, bottom two panels). Chart 24French Equities Thrive When Stagflation Fears Are High

French Equities Thrive When Stagflation Fears Are High

French Equities Thrive When Stagflation Fears Are High

Chart 25Cheap Or Expensive?

Cheap Or Expensive?

Cheap Or Expensive?

French consumer equities have become very expensive. Their relative performance has completely decoupled from earnings compared to their Eurozone competitors and their relative valuation has expanded to two sigma above its past 20 years average (Chart 26). Measured against the French broad equity market, the same dynamics can be observed (Chart 26, bottom two panels). These divergences are unsustainable and the most likely catalyst for their correction is the rapid decline in global consumer confidence (Chart 27). Chart 26French Consumer Equities Are Expensive

Beware French Consumer Stocks

Beware French Consumer Stocks

Chart 27Crumbling Consumer Confidence Does Not Bode Well For French Consumer Stocks

French Consumer Equities Are Expensive

French Consumer Equities Are Expensive

Bottom Line: The best direct bets on President Macron’s re-election are to overweight French small-cap stocks compared to large-cap ones and to favor aerospace and defense stocks within the French market. Investors should also underweight French stocks in Europe. However, to do so, investors should underweight French consumer stocks and maintain a benchmark weight for the other French sectors compared to their allocation in the Eurozone benchmark. Traders should buy Euro Area consumer staples and consumer discretionary stocks and sell French ones. Jeremie Peloso,Associate EditorJeremieP@bcaresearch.comMathieu Savary,Chief European StrategistMathieu@bcaresearch.comFootnotes

Executive Summary Equities Are Still Attractive Versus Bonds

Equities Are Still Attractive Versus Bonds

Equities Are Still Attractive Versus Bonds

Macroeconomic Outlook: Global growth will reaccelerate in the second half of this year provided a ceasefire in Ukraine is reached. Inflation will temporarily come down as the dislocations caused by the war and the pandemic subside, before moving up again in late 2023. Equities: Maintain a modest overweight in stocks over a 12-month horizon, favoring non-US equities, small caps, and value stocks. Look to turn more defensive in the second half of 2023 in advance of another wave of inflation. Fixed income: The neutral rate of interest in the US is around 3.5%-to-4%, which is substantially higher than the consensus view. Bond yields will move sideways this year but will rise over the long haul. Overweight Germany, France, Japan, and Australia while underweighting the US and the UK in a global bond portfolio. Credit: Corporate debt will outperform high-quality government bonds over the next 12 months. Favor HY over IG and Europe over the US. Spreads will widen again in late 2023. Currencies: As a countercyclical currency, the US dollar will weaken later this year, with EUR/USD rising to 1.18. We are upgrading our view on the yen from bearish to neutral due to improved valuations. The CNY will strengthen as the Chinese authorities take steps to boost domestic demand. Commodities: Oil prices will dip in the second half of 2022 as the geopolitical premium in crude declines and more OPEC supply comes to market. However, oil and other commodity prices will start moving higher by mid-2023. Bottom Line: The cyclical bull market in stocks that began in 2009 is running long in the tooth, but the combination of faster global growth later this year and a temporary lull in inflation should pave the way for one final hurrah for equities. Dear Client, Instead of our regular report this week, we are sending you our Quarterly Strategy Outlook, where we explore the major trends that are set to drive financial markets in the rest of 2022 and beyond. Next week, please join me for a webcast on Monday, April 11 at 9:00 AM EDT (2:00 PM BST, 3:00 PM CEST, 9:00 PM HKT) where I will discuss the outlook. Best regards, Peter Berezin, Chief Global Strategist P.S. You can now follow me on LinkedIn and Twitter. I. Overview We continue to recommend overweighting global equities over a 12-month horizon. However, we see downside risks to stocks both in the near term (next 3 months) and long term (2-to-5 years). In the near term, stocks will weaken anew if Russia’s stated intentions to scale back operations in Ukraine turn out to be a ruse. There is also a risk that China will need to temporarily shutter large parts of its economy to combat the spread of the highly contagious BA.2 Omicron variant. While stocks could suffer a period of indigestion in response to monetary tightening by the Fed and a number of other central banks, we doubt that rates will rise enough over the next 12 months to undermine the global economy. This reflects our view that the neutral rate of interest in the US and most other countries is higher than widely believed. If the neutral rate ends up being between 3.5% and 4% in the US, as we expect, the odds are low that the Fed will induce a recession by raising rates to 2.75%, as the latest dot plot implies (Chart 1). Chart 1The Market Sees The Fed Raising Rates To Around 3% And Then Backing Off

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

The downside of a higher neutral rate is that eventually, investors will need to value stocks using a higher real discount rate. How fast markets mark up their estimate of neutral depends on the trajectory of inflation. We were warning about inflation before it was cool to warn about inflation (see, for example, our January 2021 report, Stagflation in a Few Months?; or our February 2021 report, 1970s-Style Inflation: Yes, It Could Happen Again). Our view has been that inflation will follow a “two steps up, one step down” pattern. We are currently near the top of those two steps: US inflation will temporarily decline in the second half of this year, as goods inflation drops but service inflation is slow to rise. The decline in inflation will provide some breathing room for the Fed, allowing it to raise rates by no more than what markets are already discounting over the next 12 months. Unfortunately, the respite in inflation will not last long. By the end of 2023, inflation will start to pick up again, forcing the Fed to resume hiking rates in 2024. This second round of Fed tightening is not priced by the markets, and so when it happens, it could be quite disruptive for stocks and other risk assets. Investors should overweight equities on a 12-month horizon but look to turn more defensive in the second half of 2023. II. The Global Economy War and Pestilence Are Near-Term Risks BCA’s geopolitical team, led by Matt Gertken, was ringing the alarm bell about Ukraine well before Russia’s invasion. Recent indications from Russia that it will scale back operations in Ukraine could pave the way for a ceasefire; or they could turn out to be a ruse, giving Russia time to restock supply lines and fortify its army in advance of a new summertime campaign against Kyiv. It is too early to tell, but either way, our geopolitical team expects more fighting in the near term. The West is not keen to give Putin an easy off-ramp, and even if it were, it is doubtful he would take it. The only way that Putin can salvage his legacy among his fan base in Russia is to decisively win the war in order to ensure Ukraine’s military neutrality. For his part, Zelensky cannot simply agree to Russia’s pre-war demands that Ukraine demilitarize and swear off joining NATO unless Russian forces first withdraw. To give in to such demands without any concrete security guarantees would raise the question of why Ukraine fought the war to begin with. The Impact of the Ukraine War on the Global Economy The direct effect of the war on the global economy is likely to be small. Together, Russia and Ukraine account for 3.5% of global GDP in PPP terms and 1.9% in dollar terms. Exports to Russia and Ukraine amount to only 0.2% of G7 GDP (Chart 2). Most corporations have little direct exposure to Russia, although there are a few notable exceptions (Chart 3). Chart 2Little Direct Trade Exposure To Russia And Ukraine

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

In contrast to the direct effects, the indirect effects have the potential to be sizable. Russia is the world’s second largest oil producer, accounting for 12% of annual global output (Chart 4). It is the world’s top exporter of natural gas. About half of European natural gas imports come from Russia. Russia is also a significant producer of nickel, copper, aluminum, steel, and palladium. Chart 3Only A Handful Of Firms Have Significant Sales Exposure To Russia

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

Chart 4Russia is The World's Second Largest Oil Producer

Russia is The World's Second Largest Oil Producer

Russia is The World's Second Largest Oil Producer

Russia and Ukraine are major agricultural producers. Together, they account for a quarter of global wheat exports, with much of it going to the Middle East and North Africa (Chart 5). They are also significant producers of potatoes, corn, sugar beets, and seed oils. In addition, Russia produces two-thirds of all ammonium nitrate, the main source of nitrogen-based fertilizers. Largely as a result of higher commodity prices and other supply disruptions, the OECD estimates that the war could shave about 1% off of global growth this year, with Europe taking the brunt of the hit (Chart 6). At present, the futures curves for most commodities are highly backwardated (Chart 7). While one cannot look to the futures as unbiased predictors of where spot prices are heading, it is fair to say that commodity markets are discounting some easing in prices over the next two years. If that does not occur, global growth could weaken more than the OECD expects. Chart 5Developing Economies Buy The Bulk Of Russian And Ukrainian Wheat

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

Chart 6The War In Ukraine Could Shave One Percentage Point Off Of Global Growth

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

Chart 7Futures Curves For Most Commodities Are Backwardated

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

Another Covid Wave Two years after “two weeks to flatten the curve,” the world continues to underappreciate the power of exponential growth. Suppose that it takes five days for someone with Covid to infect someone else. If everyone with Covid infects an average of six people, the cumulative number of Covid cases would rise from 1,000 to 10 million in around four weeks. Suppose you could cut the number of new infections in half to three per person. In that case, it would take about six weeks for 10 million people to be infected. In other words, mitigation measures that cut the infection rate by half would only extend how long it takes for 10 million people to be infected by two weeks. That’s not a lot. The point is that any infection rate above one will generate an explosive rise in cases. In the pre-Omicron days, keeping the infection rate below one was difficult, but not impossible for countries with the means and motivation to do so. As the virus has become more contagious, however, keeping it at bay has grown more difficult. The latest strain of Omicron, BA.2, appears to be 40% more contagious than the original Omicron strain, which itself was about 4-times more contagious than Delta. BA.2 is quickly spreading around the world. The number of cases has spiked across much of Europe, parts of Asia, and has begun to rise in North America (Chart 8). In China, the authorities have locked down Shanghai, home to 25 million people. Chart 8Covid Cases Are On The Rise Again

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

The success that China has had in suppressing the virus has left its population with little natural immunity; and given the questionable efficacy of its vaccines, with little artificial immunity as well. Moreover, as is the case in Hong Kong, a large share of mainland China’s elderly population remains completely unvaccinated. Chart 9New Covid Drugs Are Set To Hit The Market

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

This presents the Chinese authorities with a difficult dilemma: Impose severe lockdowns over much of the population, or let the virus run rampant. As the logic of exponential change described above suggests, there is not much of a middle ground. Our guess is that the Chinese government will choose the former option. China has already signed a deal to commercialize Pfizer’s Paxlovid. The drug is highly effective at preventing hospitalization if taken within five days from the onset of symptoms. Fortunately, Paxlovid production is starting to ramp up (Chart 9). China will probably wait until it has sufficient supply of the drug before relaxing its zero-Covid policy. While beneficial to growth later this year, this strategy could have a negative near-term impact on activity, as the authorities continue to play whack-a-mole with Covid. Chart 10Inflation Is Running High, Especially In The US

Inflation Is Running High, Especially In The US

Inflation Is Running High, Especially In The US

Central Banks in a Bind Standard economic theory says that central banks should adjust interest rates in response to permanent shocks, while ignoring transitory ones. This is especially true if the shock in question emanates from the supply side of the economy. After all, higher rates cool aggregate demand; they do not raise aggregate supply. The lone exception to this rule is when a supply shock threatens to dislodge long-term inflation expectations. If long-term inflation expectations become unanchored, what began as a transitory shock could morph into a semi-permanent one. The problem for central banks is that the dislocations caused by the Ukraine war are coming at a time when inflation is already running high. Headline CPI inflation reached 7.9% in the US in February, while core CPI inflation clocked in at 6.4%. Trimmed-mean inflation has increased in most economies (Chart 10). Fortunately, while short-term inflation expectations have moved up, long-term expectations have been more stable. Expected US inflation 5-to-10 years out in the University of Michigan survey stood at 3.0% in March, down a notch from 3.1% in January, and broadly in line with the average reading between 2010 and 2015 (Chart 11). Survey-based measures of long-term inflation expectations are even more subdued in the euro area and Japan (Chart 12). Market-based inflation expectations have risen, although this partly reflects higher oil prices. Even then, the widely-watched 5-year, 5-year forward TIPS inflation breakeven rate remains near the bottom of the Fed’s comfort range of 2.3%-to-2.5% (Chart 13).1 Chart 11Long-Term Inflation Expectations Remain Contained In The US...

Long-Term Inflation Expectations Remain Contained In The US...

Long-Term Inflation Expectations Remain Contained In The US...

Chart 12... And In The Euro Area And Japan

... And In The Euro Area And Japan

... And In The Euro Area And Japan

Chart 13The Market's Long-Term Inflation Expectations Are Near The Bottom Of The Fed's Comfort Zone

The Market's Long-Term Inflation Expectations Are Near The Bottom Of The Fed's Comfort Zone

The Market's Long-Term Inflation Expectations Are Near The Bottom Of The Fed's Comfort Zone

Goods versus Services Inflation Most of the increase in consumer prices has been concentrated in goods rather than services (Chart 14). This is rather unusual in that goods prices usually fall over time; but in the context of the pandemic, it is entirely understandable. Chart 14Goods Prices Have Been A Major Driver Of Overall Inflation

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

The pandemic caused spending to shift from services to goods (Chart 15). This occurred at the same time as the supply of goods was being adversely affected by various pandemic-disruptions, most notably the semiconductor shortage that is still curtailing automobile production. Chart 15AGoods Inflation Should Fade As Consumption Shifts Back Towards Services (I)

Goods Inflation Should Fade Goods Inflation Should Fade As Consumption Shifts Back Towards Services (I)

Goods Inflation Should Fade Goods Inflation Should Fade As Consumption Shifts Back Towards Services (I)

Chart 15BGoods Inflation Should Fade As Consumption Shifts Back Towards Services (II)

Goods Inflation Should Fade Goods Inflation Should Fade As Consumption Shifts Back Towards Services (II)

Goods Inflation Should Fade Goods Inflation Should Fade As Consumption Shifts Back Towards Services (II)

Looking out, the composition of consumer spending will shift back towards services. Supply chain bottlenecks should also abate, especially if the situation in Ukraine stabilizes. It is worth noting that the number of ships on anchor off the coast of Los Angeles and Long Beach has already fallen by half (Chart 16). The supplier delivery components of both the manufacturing and nonmanufacturing ISM indices have also come off their highs (Chart 17). Even used car prices appear to have finally peaked (Chart 18). Chart 16Shipping Delays Are Abating

Shipping Delays Are Abating

Shipping Delays Are Abating

Chart 17Delivery Times Are Slowly Coming Down

Delivery Times Are Slowly Coming Down

Delivery Times Are Slowly Coming Down

Chart 18Used Car Prices May Have Finally Peaked

Used Car Prices May Have Finally Peaked

Used Car Prices May Have Finally Peaked

On the Lookout for a Wage-Price Spiral Could rising services inflation offset any decline in goods inflation this year? It is possible, but for that to happen, wage growth would have to accelerate further. For now, much of the acceleration in US wage growth has occurred at the bottom end of the income distribution (Chart 19). It is easy to see why. Chart 20 shows that low-paid workers have not returned to the labor market to the same degree as higher-paid workers. However, now that extended unemployment benefits have lapsed and savings deposits are being drawn down, the incentive to resume work will strengthen. Chart 19Wage Growth Has Picked Up, But Mostly At The Bottom End Of The Income Distribution

Wage Growth Has Picked Up, But Mostly At The Bottom End Of The Income Distribution

Wage Growth Has Picked Up, But Mostly At The Bottom End Of The Income Distribution

Chart 20More Low-Wage Employees Should Return To Work

More Low-Wage Employees Should Return To Work

More Low-Wage Employees Should Return To Work

Chart 21More Workers Will Return To Their Jobs Once The Pandemic Ends

More Workers Will Return To Their Jobs Once The Pandemic Ends

More Workers Will Return To Their Jobs Once The Pandemic Ends

The end of the pandemic should allow more workers to remain at their jobs. In January, during the height of the Omicron wave, 8.75 million US workers (5% of the total workforce) were absent from work due to the virus (Chart 21). How High Will Interest Rates Eventually Rise? If goods inflation comes down swiftly later this year, and services inflation is slow to rise, then overall inflation will decline. This should allow the Fed to pause tightening in early 2023. Whether the Fed will remain on hold beyond then depends on where the neutral rate of interest resides. Chart 22The Yield Curve Inverted in Mid-2019 But Growth Accelerated

The Yield Curve Inverted in Mid-2019 But Growth Accelerated

The Yield Curve Inverted in Mid-2019 But Growth Accelerated

The neutral rate, or equilibrium rate as it is sometimes called, is the interest rate consistent with full employment and stable inflation. If the Fed pauses hiking before interest rates have reached neutral, the economy will eventually overheat, forcing the Fed to resume hiking. In contrast, if the Fed inadvertently raises rates above neutral, unemployment will start rising, requiring the Fed to cut rates. Markets are clearly worried about the latter scenario. The 2/10 yield curve inverted earlier this week. With the term premium much lower than in the past, an inversion in the yield curve is not the powerful harbinger of recession that it once was. After all, the 2/10 curve inverted in August 2019 and the economy actually strengthened over the subsequent six months before the pandemic came along (Chart 22). Nevertheless, an inverted yield curve is consistent with markets expectations that the Fed will raise rates above neutral. That is always a dangerous undertaking. Raising rates above neutral would likely push up the unemployment rate. There has never been a case in the post-war era where the 3-month moving average of the unemployment rate has risen by more than 30 basis points without a recession occurring (Chart 23). Chart 23When Unemployment Starts Rising, It Usually Keeps Rising

When Unemployment Starts Rising, It Usually Keeps Rising

When Unemployment Starts Rising, It Usually Keeps Rising

As discussed in the Feature Section below, the neutral rate of interest is probably between 3.5% and 4% in the US. This is good news in the short term because it lowers the odds that the Fed will raise rates above neutral during the next 12 months. It is bad news in the long run because it means that the Fed will find itself even more behind the curve than it is now, making a recession almost inevitable. The Feature Section builds on our report from two weeks ago. Readers familiar with that report should feel free to skip ahead to the next section. III. Feature: A Higher Neutral Rate Conceptually, the neutral rate is the interest rate that equates the amount of investment a country wants to undertake at full employment with the amount of savings that it has at its disposal.2 Anything that reduces savings or increases investment would raise the neutral rate (Chart 24). Chart 24The Savings-Investment Balance Determines The Neutral Rate Of Interest

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

A number of factors are likely to lower desired savings in the US over the next few years: Households will spend down their accumulated pandemic savings. US households are sitting on $2.3 trillion (10% of GDP) in excess savings, the result of both decreased spending on services during the pandemic and the receipt of generous government transfer payments (Chart 25). Household wealth has soared since the start of the pandemic (Chart 26). Conservatively assuming that households spend three cents of every additional dollar in wealth, the resulting wealth effect could boost consumption by 4% of GDP. Chart 25Plenty Of Pent-Up Demand

Plenty Of Pent-Up Demand

Plenty Of Pent-Up Demand

Chart 26Net Worth Has Soared Since The Pandemic

Net Worth Has Soared Since The Pandemic

Net Worth Has Soared Since The Pandemic

The household deleveraging cycle has ended (Chart 27). Household balance sheets are in good shape. After falling during the initial stages of the pandemic, consumer credit has begun to rebound. For the first time since the housing boom, mortgage equity withdrawals are rising. Banks are easing lending standards on consumer loans across the board. Chart 27US Household Deleveraging Pressures Have Abated

US Household Deleveraging Pressures Have Abated

US Household Deleveraging Pressures Have Abated

Chart 28Baby Boomers Have Amassed A Lot Of Wealth

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

Baby boomers are retiring. They hold over half of US household wealth, considerably more than younger generations (Chart 28). As baby boomers transition from being savers to dissavers, national savings will decline. Government budget deficits will stay elevated. Fiscal deficits subtract from national savings. While the US budget deficit will come down over the next few years, the IMF estimates that the structural budget deficit will still average 4.9% of GDP between 2022 and 2026 compared to 2.0% of GDP between 2014 and 2019 (Chart 29).Chart 29Fiscal Policy: Tighter But Not Tight

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

On the investment front: The deceleration in trend GDP growth, which depressed investment spending, has largely run its course.3 According to the Congressional Budget Office, real potential GDP growth fell from over 3% in the early 1980s to about 1.9% today. The CBO expects potential growth to edge down only slightly to 1.7% over the next few decades (Chart 30). After moving broadly sideways for two decades, core capital goods orders – a leading indicator for capital spending – have broken out to the upside (Chart 31). Capex intention surveys remain upbeat (Chart 32). The average age of the nonresidential capital stock currently stands at 16.3 years, the highest since 1965 (Chart 33). Chart 30Much Of The Deceleration In Potential Growth Has Already Happened

Much Of The Deceleration In Potential Growth Has Already Happened

Much Of The Deceleration In Potential Growth Has Already Happened

Chart 31Positive Signs For Capex (I)

Positive Signs For Capex (I)

Positive Signs For Capex (I)

Chart 32Positive Signs For Capex (II)

Positive Signs For Capex (II)

Positive Signs For Capex (II)

Chart 33An Aging Capital Stock

An Aging Capital Stock

An Aging Capital Stock

Similar to nonresidential investment, the US has been underinvesting in residential real estate (Chart 34). The average age of the housing stock has risen to a 71-year high of 31 years. The homeowner vacancy rate has plunged to the lowest level on record. The number of newly finished homes for sale is half of what it was prior to the pandemic. Chart 34US Housing Is In Short Supply

US Housing Is In Short Supply

US Housing Is In Short Supply

The New ESG: Energy Security and Guns The war in Ukraine will put further upward pressure on the neutral rate, especially outside of the United States. After staging a plodding recovery following the euro debt crisis, European capital spending received a sizable boost from the launch of the NextGenerationEU Recovery Fund (Chart 35). As Mathieu Savary points out in his latest must-read report on Europe, capital spending will rise further in the years ahead as European governments accelerate efforts to make their economies less reliant on Russian energy. Germany has already announced plans to construct three new LNG terminals. The push to build out Europe’s energy infrastructure is coming at a time when businesses are looking to ramp up capital spending. As in the US, Europe’s capital stock has aged rapidly over the past decade (Chart 36). Chart 35European Capex Should Recover

European Capex Should Recover

European Capex Should Recover

Chart 36European Machines Need More Than Just An Oil Change

European Machines Need More Than Just An Oil Change

European Machines Need More Than Just An Oil Change

Chart 37The War In Ukraine Calls For More Spending Across Europe

The War In Ukraine Calls For More Spending Across Europe

The War In Ukraine Calls For More Spending Across Europe

Meanwhile, European governments are trying to ease the burden from rising energy costs. For example, France has introduced a rebate on fuel. It is part of a EUR 20 billion package aimed at cutting heating and electricity bills. European military spending will rise. Military spending currently amounts to 1.5% of GDP, well below NATO’s threshold of 2% (Chart 37). Germany has announced that it will spend EUR 100 billion more on defense. European governments will also need to boost spending to accommodate Ukrainian refugees. The UN estimates that four million refugees have left Ukraine, with the vast majority settling in the EU. A Smaller Chinese Current Account Surplus? The difference between what a country saves and invests equals its current account balance. Historically, China has been a major exporter of savings, which has helped depress interest rates abroad. While China’s current account surplus has declined as a share of its own GDP, it has remained very large as a share of global ex-China GDP, reflecting China’s growing weight in the global economy (Chart 38). Many analysts assume that China will double down on efforts to boost exports in order to offset the drag from falling property investment. However, there is a major geopolitical snag with that thesis: A country that runs a current account surplus must, by definition, accumulate assets from the rest of the world. As the freezing of Russia’s foreign exchange reserves demonstrates, that is a risky proposition for a country such as China. Rather than increasing its current account surplus, China may seek to bolster its economy by raising domestic demand. This could be achieved by either boosting domestic infrastructure spending or raising household consumption. Notably, China’s credit impulse appears to have bottomed and is set to increase in the second half of the year. This is good news not just for Chinese growth but growth abroad (Chart 39). Chart 38Will China Be A Source Of Excess Savings?

Will China Be A Source Of Excess Savings?

Will China Be A Source Of Excess Savings?

Chart 39China's Credit Impulse Appears To Have Bottomed

China's Credit Impulse Appears To Have Bottomed

China's Credit Impulse Appears To Have Bottomed

The IMF’s latest projections foresee China’s current account surplus falling by more than half between 2021 and 2026 as a share of global ex-China GDP. If this were to happen, the neutral rate in China and elsewhere would rise. IV. Financial Markets A. Portfolio Strategy Chart 40The Markets Wobbled And Then Recovered After The Beginning Of The Last Four Fed Rate Cycles

The Markets Wobbled And Then Recovered After The Beginning Of The Last Four Fed Rate Cycles

The Markets Wobbled And Then Recovered After The Beginning Of The Last Four Fed Rate Cycles

As noted in the overview, if the neutral rate turns out to be higher than currently perceived, the Fed is unlikely to induce a recession by raising rates over the next 12 months. That is good news for equities. A look back at the past four Fed tightening cycles shows that stocks often wobble when the Fed starts hiking rates, but then usually rise as long as rates do not move into restrictive territory (Chart 40). Unfortunately, a higher neutral rate also means that investors will eventually need to value stocks using a higher discount rate. It also means that any decline in inflation this year will not last. The US economy will probably start to overheat again in the second half of 2023. This will set the stage for a second, and more painful, tightening cycle in 2024. Admittedly, there is a lot of uncertainty over our “two steps up, one step down” forecast for inflation. It is certainly possible that the “one step down” phase does not last long and that the resurgence in inflation we are expecting in the second half of next year occurs earlier. It is also possible that investors will react negatively to rising rates, even if the economy is ultimately able to withstand them. As such, only a modest overweight to equities is justified over the next 12 months, with risks tilted to the downside in the near term. More conservative asset allocators should consider moving to a neutral stance on equities already, as my colleague Garry Evans advised clients to do in his latest Global Asset Allocation Quarterly Portfolio Outlook. B. Fixed Income Stay Underweight Duration Over a 2-to-5 Year Horizon Our recommendation to maintain below-benchmark duration in fixed-income portfolios panned out since the publication of our Annual Outlook in December, with the US 10-year Treasury yield rising from 1.43% to 2.38%. We continue to expect bond yields in the US to rise over the long haul. Conceptually, the yield on a government bond equals the expected path of policy rates over the duration of the bond plus a term premium. The term premium is the difference between the return investors can expect from buying a long-term bond that pays a fixed interest rate, and the return from rolling over a short-term bill. The term premium has been negative in recent years. Investors have been willing to sacrifice return to own long-term bonds because bond prices usually rise when the odds of a recession go up. The fact that monthly stock returns and changes in bond yields have been positively correlated since 2001 underscores the benefits that investors have received from owning long-term bonds as a hedge against unfavorable economic news (Chart 41). However, now that inflation has emerged as an increasingly important macroeconomic risk, the correlation between stock returns and changes in bond yields could turn negative again. Unlike weak economic growth, which is bad for only stocks, high inflation is bad for both bonds and stocks. Chart 41Correlation Between Stock Returns And Bond Yields Could Turn Negative

Correlation Between Stock Returns And Bond Yields Could Turn Negative

Correlation Between Stock Returns And Bond Yields Could Turn Negative

If bond yields start to rise whenever stock prices fall, the incentive to own long-term bonds will decline. This will cause the term premium to increase. Assuming the term premium rises to about 0.5%, and a neutral rate of 3.5%-to-4%, the long-term fair value for the 10-year US Treasury yield is 4%-to-4.5%. This is well above the 5-year/5-year forward yield of 2.20%. Move from Underweight to Neutral Duration Over a 12-Month Horizon Below benchmark duration positions usually do well when the Fed hikes rates by more than expected over the subsequent 12 months (Chart 42). Chart 42The Golden Rule Of Bond Investing

The Golden Rule Of Bond Investing

The Golden Rule Of Bond Investing

Given our view that US inflation will temporarily decline later this year, the Fed will probably not need to raise rates over the next 12 months by more than the 249 basis points that markets are already discounting. Thus, while a below-benchmark duration position is advisable over a 2-to-5-year time frame, it could struggle over a horizon of less than 12 months. Our end-2022 target range for the US 10-year Treasury yield is 2.25%-to-2.5%. Chart 43Bond Sentiment And Positioning Are Bearish

Bond Sentiment And Positioning Are Bearish

Bond Sentiment And Positioning Are Bearish

Supporting our decision to move to a neutral benchmark duration stance over a 12-month horizon is that investor positioning and sentiment are both bond bearish (Chart 43). From a contrarian point of view, this is supportive of bonds. Global Bond Allocation BCA’s global fixed-income strategists recommend overweighting German, French, Australian, and Japanese government bonds, while underweighting those of the US and the UK. They are neutral on Italy and Spain given that the ECB is set to slow the pace of bond buying. The neutral rate of interest has risen in the euro area, partly on the back of more expansionary fiscal policy across the region. In absolute terms, however, the neutral rate in the euro area is still quite low, and possibly negative. Unlike in the US, where inflation has risen to uncomfortably high levels, much of Europe would benefit from higher inflation expectations, as this would depress real rates across the region, giving growth a boost. This implies that the ECB is unlikely to raise rates much over the next two years. As with the euro area, Japan would benefit from lower real rates. The Bank of Japan’s yield curve control policy has been put to the test in recent weeks. To its credit, the BoJ has stuck to its guns, buying bonds in unlimited quantities to prevent yields from rising. We expect the BoJ to stay the course. Unlike in the euro area and Japan, inflation expectations are quite elevated in the UK and wage growth is rising quickly there. This justifies an underweight stance on UK gilts. Although job vacancies in Australia have climbed to record levels, wage growth is still not strong enough from the RBA’s point of view to justify rapid rate hikes. As a result, BCA’s global fixed-income strategists remain overweight Australian bonds. Finally, our fixed-income strategists are underweight Canadian bonds but are contemplating upgrading them given that markets have already priced in 238 basis points in tightening over the next 12 months. Unlike in the US, high levels of consumer debt will also limit the Bank of Canada’s ability to raise rates. Modest Upside in High-Yield Corporate Bonds Credit spreads have narrowed in recent days but remain above where they were prior to Russia’s invasion of Ukraine. Since the start of the year, US investment-grade bonds have underperformed duration-matched Treasurys by 154 basis points, while high-yield bonds have underperformed by 96 basis points (Chart 44). The outperformance of high-yield relative to investment-grade debt can be explained by the fact that the former has more exposure to the energy sector, which has benefited from rising oil prices. Looking out, falling inflation and a rebound in global growth later this year should provide a modestly supportive backdrop for corporate credit. High-yield spreads are still pricing in a default rate of 3.8% over the next 12 months (Chart 45). This is well above the trailing 12-month default rate of 1.3%. Our fixed-income strategists continue to prefer US high-yield over US investment-grade. Chart 44Spreads Have Narrowed Over The Past Two Weeks But Remain Above Pre-War Levels

Spreads Have Narrowed Over The Past Two Weeks But Remain Above Pre-War Levels

Spreads Have Narrowed Over The Past Two Weeks But Remain Above Pre-War Levels

Chart 45Spread-Implied Default Rate Is Too High

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

European credit is attractively priced and should benefit from any stabilization in the situation in Ukraine. Our fixed-income strategists prefer both European high-yield and investment-grade bonds over their US counterparts. As with equities, the bull market in corporate credit will end in late 2023 as the Fed is forced to resume raising rates in 2024 in the face of an overheated economy. C. Currencies Chart 46Widening Interest Rate Differentials Have Supported The Dollar

Widening Interest Rate Differentials Have Supported The Dollar

Widening Interest Rate Differentials Have Supported The Dollar

The US Dollar Will Weaken Starting in the Second Half of 2022 Since bottoming last May, the US dollar has been trending higher. While the dollar could strengthen further in the near term if the war in Ukraine escalates, the fundamental backdrop supporting the greenback is starting to fray. If US inflation comes down later this year, the Fed is unlikely to raise rates by more than what markets are already discounting over the next 12 months. Thus, widening rate differentials will no longer support the dollar (Chart 46). The dollar is a countercyclical currency: It usually weakens when global growth is strengthening and strengthens when global growth is weakening (Chart 47). The dollar tends to be particularly vulnerable when growth expectations are rising more outside the US than in the US (Chart 48). Chart 47The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

Chart 48Better Growth Prospects Abroad Will Weigh On The US Dollar

Better Growth Prospects Abroad Will Weigh On The US Dollar

Better Growth Prospects Abroad Will Weigh On The US Dollar

Global growth should rebound in the second half of the year once the pandemic finally ends and the situation in Ukraine stabilizes. Growth is especially likely to recover in Europe. This will support the euro, a dovish ECB notwithstanding. Chester Ntonifor, BCA’s Foreign Exchange Strategist, expects EUR/USD to end the year at 1.18. The Dollar is Overvalued The dollar’s ascent has left it overvalued by more than 20% on a Purchasing Power Parity (PPP) basis (Chart 49). The PPP exchange rate equalizes the price of a representative basket of goods and services between the US and other economies. PPP deviations from fair value have done a reasonably good job of predicting dollar movements over the long run (Chart 50). Chart 49USD Remains Overvalued

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

Chart 50Valuations Matter For FX Long-Term Returns

Valuations Matter For FX Long-Term Returns

Valuations Matter For FX Long-Term Returns

Reflecting the dollar’s overvaluation, the US trade deficit has widened sharply (Chart 51). Excluding energy exports, the US trade deficit as a share of GDP is now the largest on record. Equity inflows have helped finance America’s burgeoning current account deficit (Chart 52). However, these inflows have ebbed significantly as foreign investors have lost their infatuation with US tech stocks. Chart 51The US Trade Deficit Has Widened

The US Trade Deficit Has Widened

The US Trade Deficit Has Widened

Chart 52Net Inflows Into US Equities Have Dried Up

Net Inflows Into US Equities Have Dried Up

Net Inflows Into US Equities Have Dried Up

Dollar positioning remains stretched on the long side (Chart 53). That is not necessarily an obstacle in the short run, given that the dollar tends to be a momentum currency, but it does suggest that the greenback could weaken over a 12-month horizon as more dollar bulls jump ship. The Yen: Cheaper but Few Catalysts for a Bounce The trade-weighted yen has depreciated by 6.4% since the start of the year. The yen is 31% undervalued relative to the dollar on a PPP basis (Chart 54). In a nod to these improved valuations, we are upgrading our 12-month and long-term view on the yen from bearish to neutral. Chart 53Still A Lot of Dollar Bulls

Still A Lot of Dollar Bulls

Still A Lot of Dollar Bulls

Chart 54The Yen Has Gotten Cheaper

The Yen Has Gotten Cheaper

The Yen Has Gotten Cheaper

While the yen is unlikely to weaken much from current levels, it is unlikely to strengthen. As noted above, the Bank of Japan has no incentive to abandon its yield curve control strategy. Yes, the recent rapid decline in the yen is a shock to the economy, but it is a “good” shock in the sense that it could finally jolt inflation expectations towards the BoJ’s target of 2%. If inflation expectations rise, real rates would fall, which would be bearish for the currency. Favor the RMB and other EM Currencies The Chinese RMB has been resilient so far this year, rising slightly against the dollar, even as the greenback has rallied against most other currencies. Real rates are much higher in China than in the US, and this has supported the RMB (Chart 55). Chart 55Higher Real Rates In China Have Supported The RMB

Higher Real Rates In China Have Supported The RMB

Higher Real Rates In China Have Supported The RMB

Chart 56The RMB Is Undervalued Based On PPP

The RMB Is Undervalued Based On PPP

The RMB Is Undervalued Based On PPP

Despite the RMB’s strength, it is still undervalued by 10.5% relative to its PPP exchange rate (Chart 56). While productivity growth has slowed in China, it remains higher than in most other countries. The real exchange rates of countries that benefit from fast productivity growth typically appreciates over time. China holds about half of its foreign exchange reserves in US dollars, a number that has not changed much since 2012 (Chart 57). We expect China to diversify away from dollars over the coming years. Moreover, as discussed earlier in the report, the incentive for China to run large current account surpluses may fade, which will result in slower reserve accumulation. Both factors could curb the demand for dollars in international markets. Chart 57Half Of Chinese FX Reserves Are Held In USD Assets

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

A resilient RMB will provide a tailwind for other EM currencies. Many EM central banks began to raise rates well before their developed market counterparts. In Brazil, for example, the policy rate has risen to 11.75% from 2% last April. With inflation in EMs likely to come down later this year as pandemic and war-related dislocations subside, real policy rates will rise, giving EM currencies a boost. D. Commodities Longer-Term Bullish Thesis on Commodities Remains Intact BCA’s commodity team, led by Bob Ryan, expects crude prices to fall in the second half of the year, before moving higher again in 2023. Their forecast is for Brent to dip to $88/bbl by end-2022, which is below the current futures price of $97/bbl. Chart 58Dearth Of Oil Capex Will Put A Floor Under Oil Prices

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

The risk to their end-2022 forecast is tilted to the upside. The relationship between the Saudis and the US has become increasingly strained. This could hamper efforts to bring more oil to market. Hopes that Iranian crude will reach global markets could also be dashed if, as BCA’s geopolitical strategists expect, the US-Iran nuclear deal falls through. A cut-off of Russian oil could also cause prices to rise. While Urals crude is being sold at a heavy discount of $30/bbl to Brent (compared to a discount of around $2/bbl prior to the invasion), it is still leaving the country. In fact, Russian oil production actually rose in March over February. An escalation of the war would make it more difficult for Russia to divert enough oil to China, India, and other countries in order to evade Western sanctions. Looking beyond this year, Bob and his team see upside to oil prices. They expect Brent to finish 2023 at $96/bbl, above the futures price of $89/bbl. Years of underinvestment in crude oil production have led to tight supply conditions (Chart 58). Proven global oil reserves increased by only 6% between 2010 and 2020, having risen by 26% over the preceding decade. Stay Positive on Metals As with oil, there has been little investment in mining capacity in recent years. While a weaker property market in China will weigh on metals prices, this will be partly offset by increased infrastructure spending. The shift towards green energy will also boost metals prices. The typical electric vehicle requires about four times as much copper as a typical gasoline-powered vehicle. Huge amounts of copper will also be necessary to expand electrical grids. Favor Gold Over Cryptos After breaking above $2,000/oz, the price of gold has retreated to $1,926/oz. In the near term, gold prices will be swayed by geopolitical developments. Longer term, real rates will dictate the direction of gold prices. Chart 59 shows that there is a very strong correlation between the price of gold and TIPS yields. If we are correct that the neutral rate of interest is 3.5%-to-4% in the US, real bond yields will eventually need to rise from current levels. Gold prices are quite expensive by historic standards, which represents a long-term risk (Chart 60). Chart 59Strong Correlation Between Real Rates And Gold

Strong Correlation Between Real Rates And Gold

Strong Correlation Between Real Rates And Gold

Chart 60Gold Is Quite Pricey From A Historical Perspective

Gold Is Quite Pricey From A Historical Perspective

Gold Is Quite Pricey From A Historical Perspective

That said, we expect the bulk of the increase in real bond yields to occur only after mid-2023. As mentioned earlier, the Fed will probably not have to deliver more tightening that what markets are already discounting over the next 12 months. Thus, gold prices are unlikely to fall much in the near term. In any case, we continue to regard gold as a safer play than cryptocurrencies. As we discussed in Who Pays for Cryptos?, the long-term outlook for cryptocurrencies remains daunting. Many of the most hyped blockchain applications, from DeFi to NFTs, will turn out to be duds. Concerns that cryptocurrencies are harming the environment, contributing to crime, and enriching a small group of early investors at the expense of everyone else will lead to increased regulatory scrutiny. Our long-term target for Bitcoin is $5,000. E. Equities Equities Are Still Attractively Priced Relative to Bonds Corporate earnings are highly correlated with the state of the business cycle (Chart 61). A recovery in global growth later this year will bolster revenue, while easing supply-chain pressures should help contain costs in the face of rising wages. It is worth noting that despite all the shocks to the global economy, EPS estimates in the US and abroad have actually risen this year (Chart 62). Chart 61The Business Cycle Drives Earnings

The Business Cycle Drives Earnings

The Business Cycle Drives Earnings

Chart 62Global EPS Estimates Have Held Up Reasonably Well

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

Chart 63Equities Are Still Attractive Versus Bonds

Equities Are Still Attractive Versus Bonds

Equities Are Still Attractive Versus Bonds

As Doug Peta, BCA’s Chief US Strategist has pointed out, the bar for positive earnings surprises for Q1 is quite low: According to Refinitiv/IBES, S&P 500 earnings are expected to fall by 4.5% in Q1 over Q4 levels. Global equities currently trade at 18-times forward earnings. Relative to real bond yields, stocks continue to look reasonably cheap (Chart 63). Even in the US, where valuations are more stretched, the earnings yield on stocks exceeds the real bond yield by 570 basis points. At the peak of the market in 2000, the gap between earnings yields and real bond yields was close to zero. Favor Non-US Markets, Small Caps, and Value Valuations are especially attractive outside the US. Non-US equities trade at 13.7-times forward earnings. Emerging markets trade at a forward P/E of only 12.1. Correspondingly, the gap between earnings yields and real bond yields is about 200 basis points higher outside the US. In general, non-US markets fare best in a setting of accelerating growth and a weakening dollar – precisely the sort of environment we expect to prevail in the second half of the year (Chart 64). US small caps also perform best when growth is strengthening and the dollar is weakening (Chart 65). In contrast to the period between 2003 and 2020, small caps now trade at a discount to their large cap brethren. The S&P 600 currently trades at 14.4-times forward earnings compared to 19.7-times for the S&P 500, despite the fact that small cap earnings are projected to grow more quickly both over the next 12-months and over the long haul (Chart 66). Chart 64A Weaker Dollar And Stronger Global Economy Are Tailwinds For Non-US Stocks

A Weaker Dollar And Stronger Global Economy Are Tailwinds For Non-US Stocks

A Weaker Dollar And Stronger Global Economy Are Tailwinds For Non-US Stocks

Chart 65US Small Caps Usually Fare Well When The Economy Is Strengthening And The Dollar Is Weakening

US Small Caps Usually Fare Well When The Economy Is Strengthening And The Dollar Is Weakening

US Small Caps Usually Fare Well When The Economy Is Strengthening And The Dollar Is Weakening

Globally, growth stocks have outperformed value stocks by 60% since 2017. However, only one-tenth of that outperformance has come from faster earnings growth (Chart 67). This has left value trading nearly two standard deviations cheap relative to growth. Chart 66Small Caps Look Attractive Relative To Large Caps

Small Caps Look Attractive Relative To Large Caps

Small Caps Look Attractive Relative To Large Caps

Chart 67Value Remains Cheap

Value Remains Cheap

Value Remains Cheap

Chart 68Higher Yields Tend To Flatter Bank Stocks And Usually Weigh On Tech

Higher Yields Tend To Flatter Bank Stocks And Usually Weigh On Tech

Higher Yields Tend To Flatter Bank Stocks And Usually Weigh On Tech

Tech stocks are overrepresented in growth indices, while banks are overrepresented in value indices. US banks have held up relatively well since the start of the year but have not gained as much as one would have expected based on the significant increase in bond yields (Chart 68). With the deleveraging cycle in the US coming to an end, US banks sport both attractive valuations and the potential for better-than-expected earnings growth. European banks should also recover as the situation in Ukraine stabilizes. They trade at only 7.9-times forward earnings and 0.6-times book. On the flipside, structurally higher bond yields will weigh on tech shares. Moreover, as we discussed in our recent report entitled The Disruptor Delusion, a cooling in pandemic-related tech spending, increasing market saturation, and concerns about Big Tech’s excessive power will all hurt tech returns. Peter Berezin Chief Global Strategist peterb@bcaresearch.com Footnotes 1 The Federal Reserve targets an average inflation rate of 2% for the personal consumption expenditures (PCE) index. The TIPS breakeven is based on the CPI index. Due to compositional differences between the two indices, CPI inflation has historically averaged 30-to-50 basis points higher than PCE inflation. This is why the Fed effectively targets a CPI inflation rate of about 2.3%-to-2.5%. 2 These savings can either by generated domestically or imported from abroad via a current account deficit. 3 Theoretically, there is a close relationship between trend growth and the equilibrium investment-to-GDP ratio. For example, if real trend growth is 3% and the capital stock-to-GDP ratio is 200%, a country would need to invest 6% of GDP net of depreciation to maintain the existing capital stock-to-GDP ratio. In contrast, if trend growth were to fall to 2%, the country would only need to invest 4% of GDP. Global Investment Strategy View Matrix

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral

Special Trade Recommendations Current MacroQuant Model Scores

2022 Second Quarter Strategy Outlook – The New Neutral

2022 Second Quarter Strategy Outlook – The New Neutral