Europe

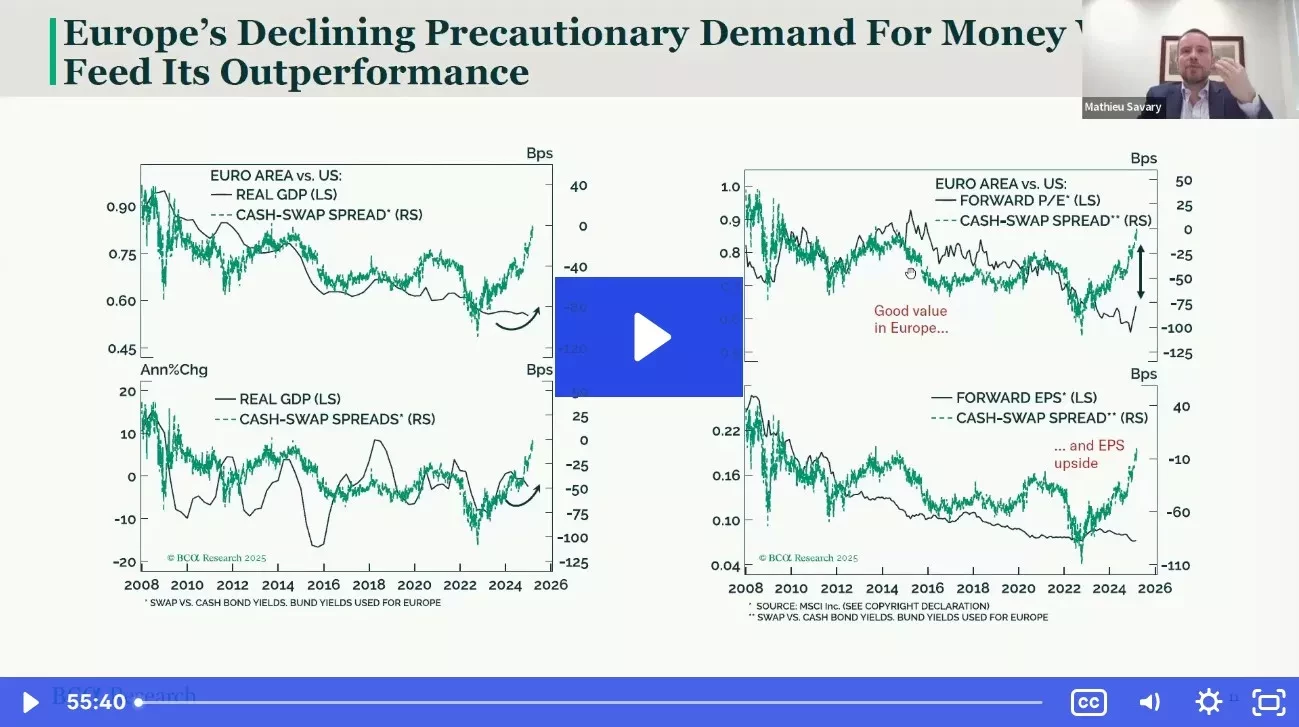

Our Chart Of The Week comes from Mathieu Savary, Chief Strategist of our European Investment Strategy service. Mathieu believes the recent outperformance of European over US risk assets is unlikely to last over the next 3-6 months. Markets are…

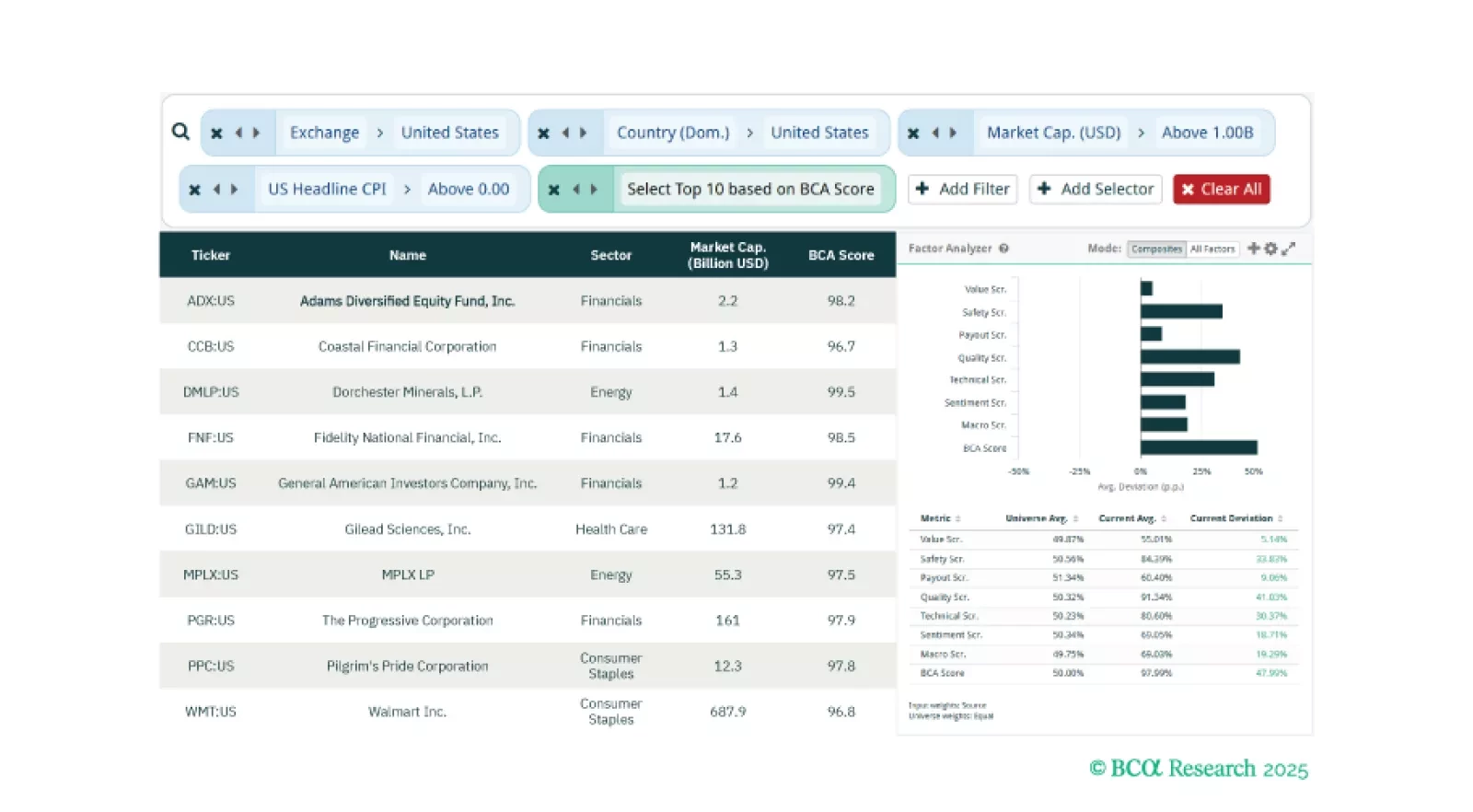

Weekly Screeners: “Transitory” Inflation 2.0, European Aerospace & Defense, And Buffett’s Philosophy

This week, our three screeners cover equity plays for “transitory” inflation impacts from US tariffs, a correction in sentiment within the European Aerospace and Defense industry, and Value Investor, Warren Buffett’s Philosophy.

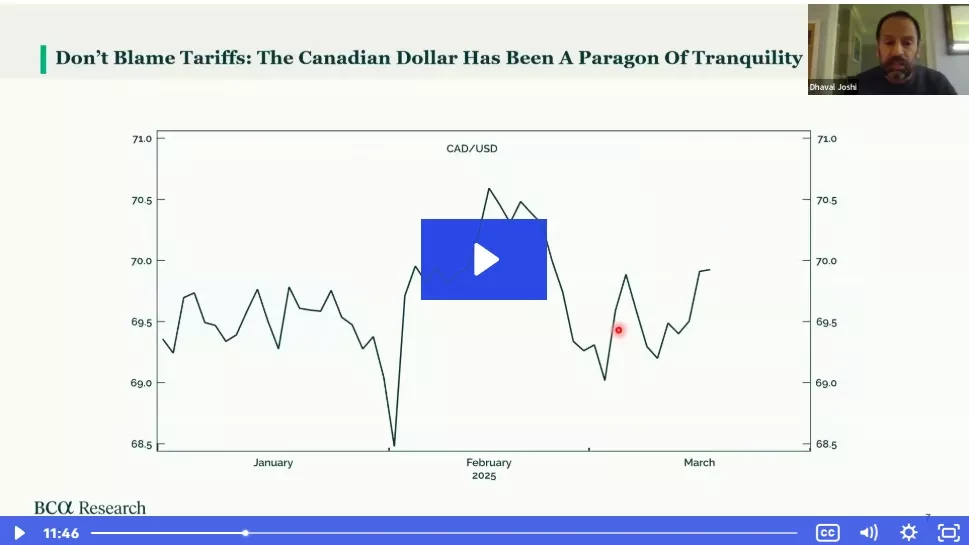

In this webcast, Dhaval discussed how investors should interpret, and react to, the recent selloff in stocks.

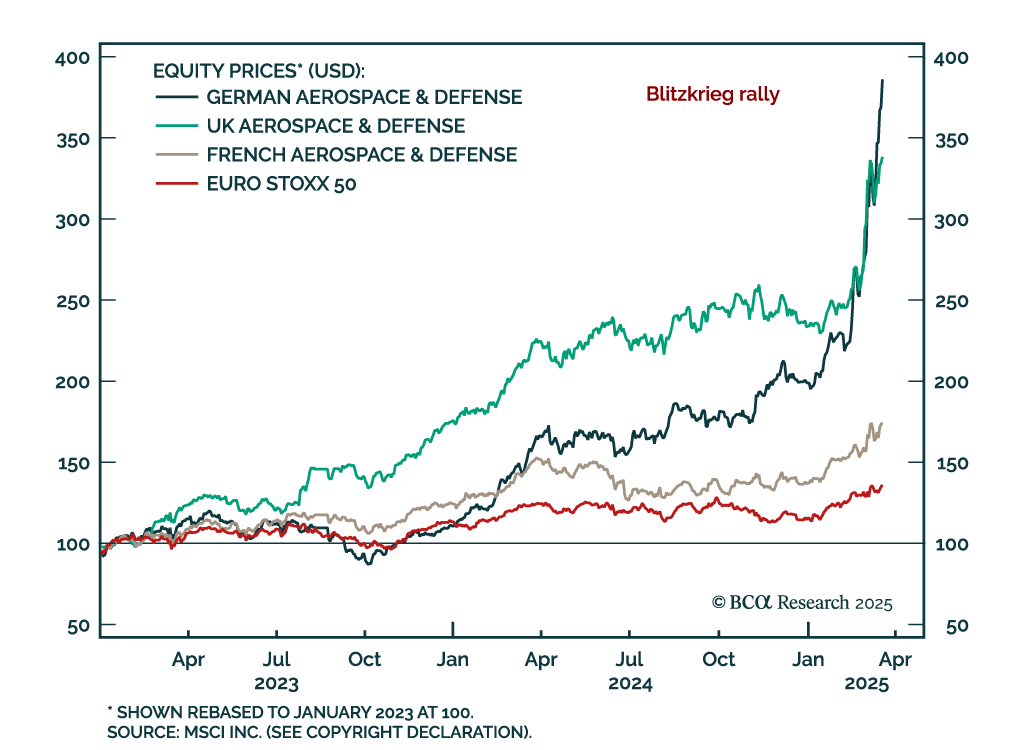

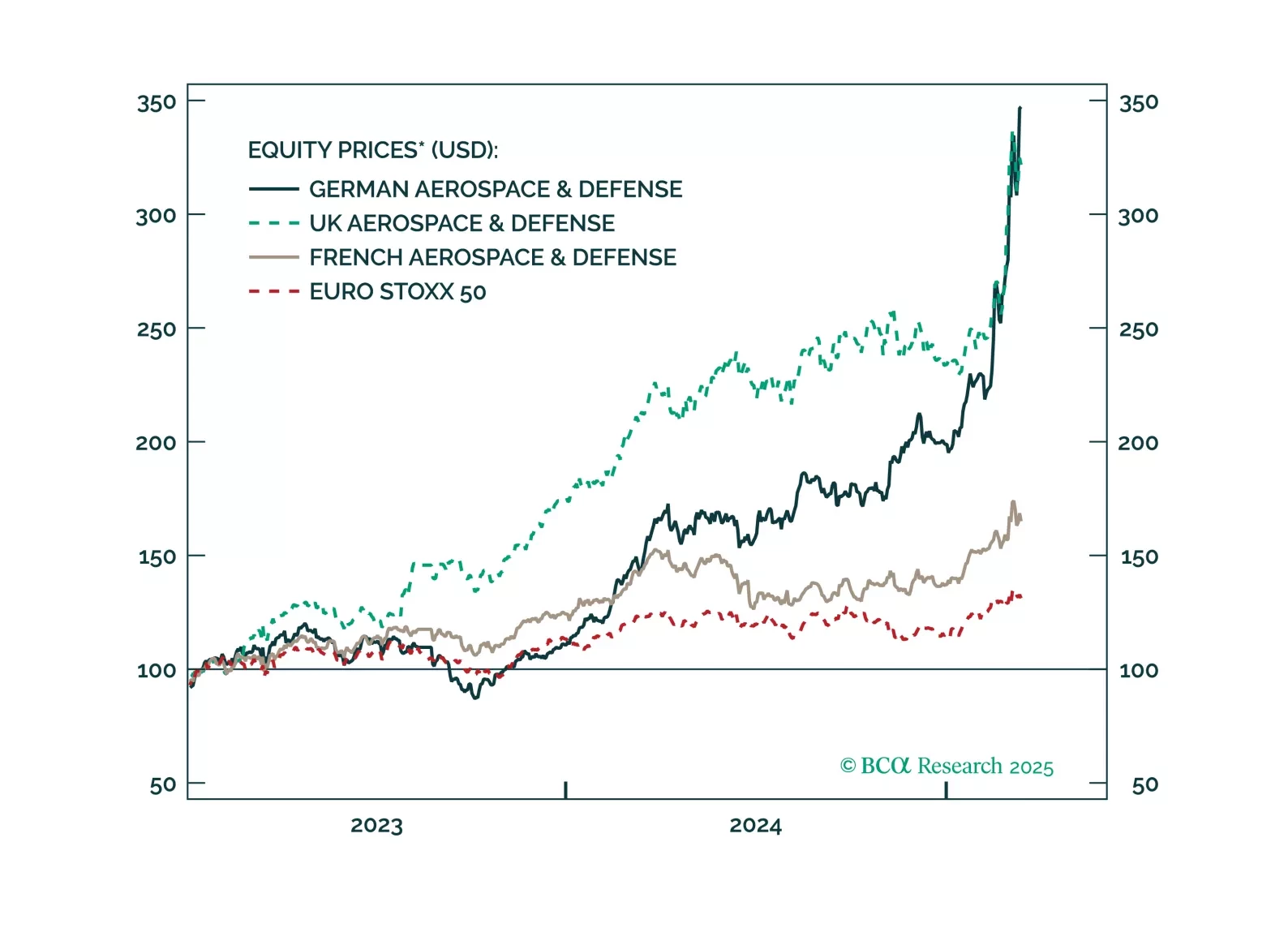

Our European strategists looked at the European defense sector after the massive rally following Germany’s fiscal turnaround. The rally in European defense stocks, up over 100% since their March 2023 recommendation, is overextended. While the long-term…

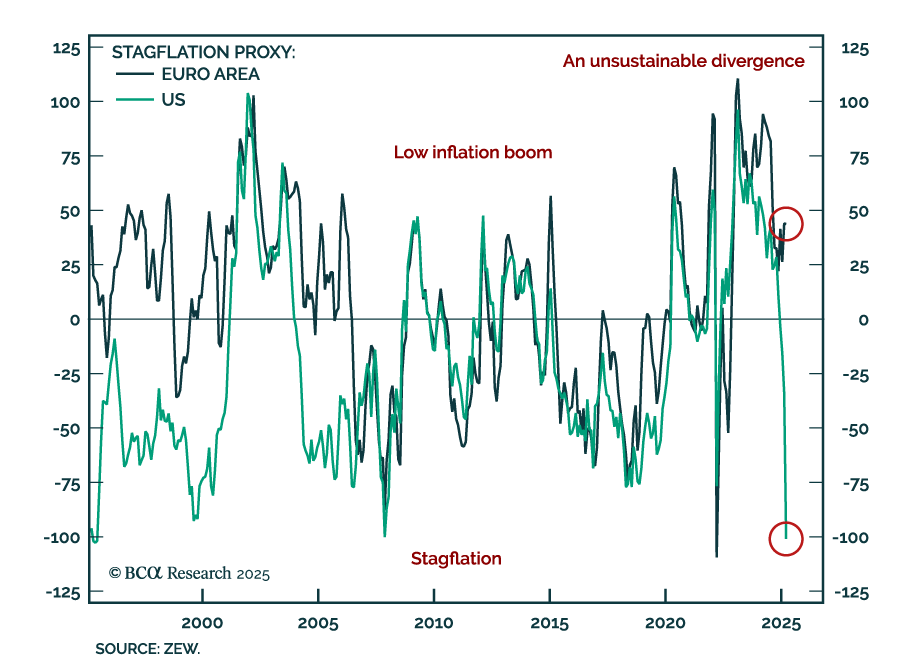

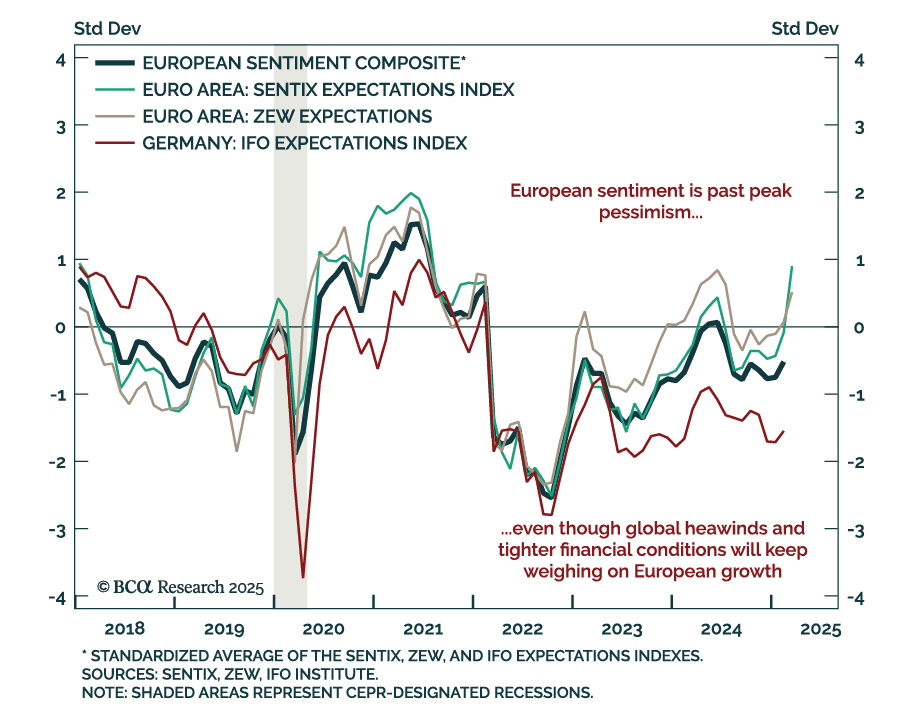

The March ZEW index for Germany and the eurozone beat estimates, with the expectations component rising to 51.6 from 26.0 in February. The current situation assessment only marginally improved yet remains deeply negative at -87.6. The March data shows…

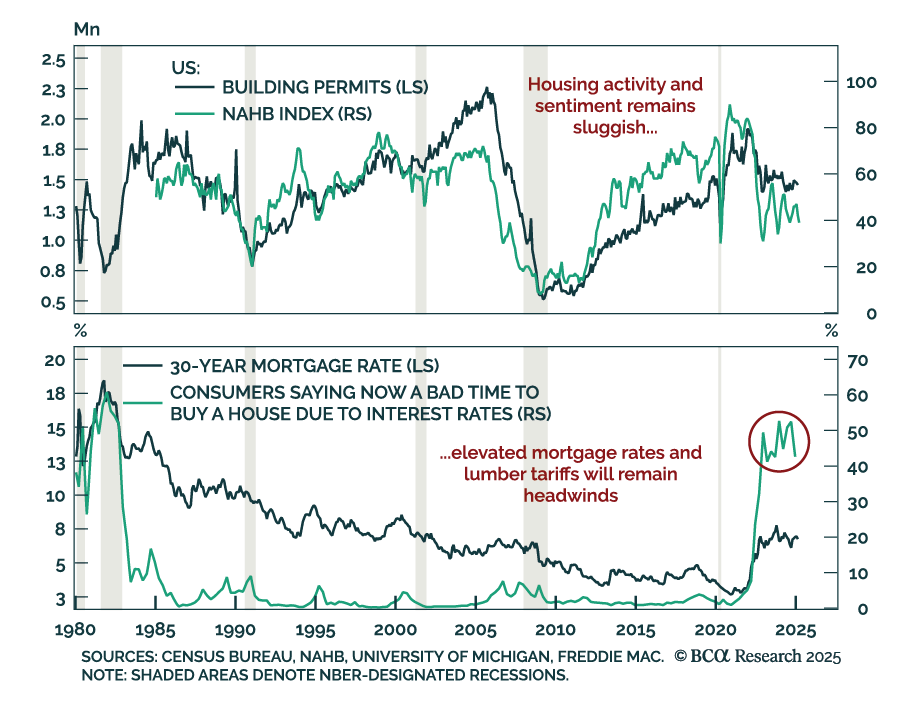

US February housing data was relatively strong, with housing starts rising 11.2% m/m after falling 9.8% in January. While they fell less than expected, building permits still declined at a faster pace than in January. The March NAHB Housing Market Index also…

Join our webcast as we break down what’s next for European vs. U.S. equities—and where the best opportunities lie.

Investors should not chase the rally in European defense names any further. Too much good news has been priced in too quickly.

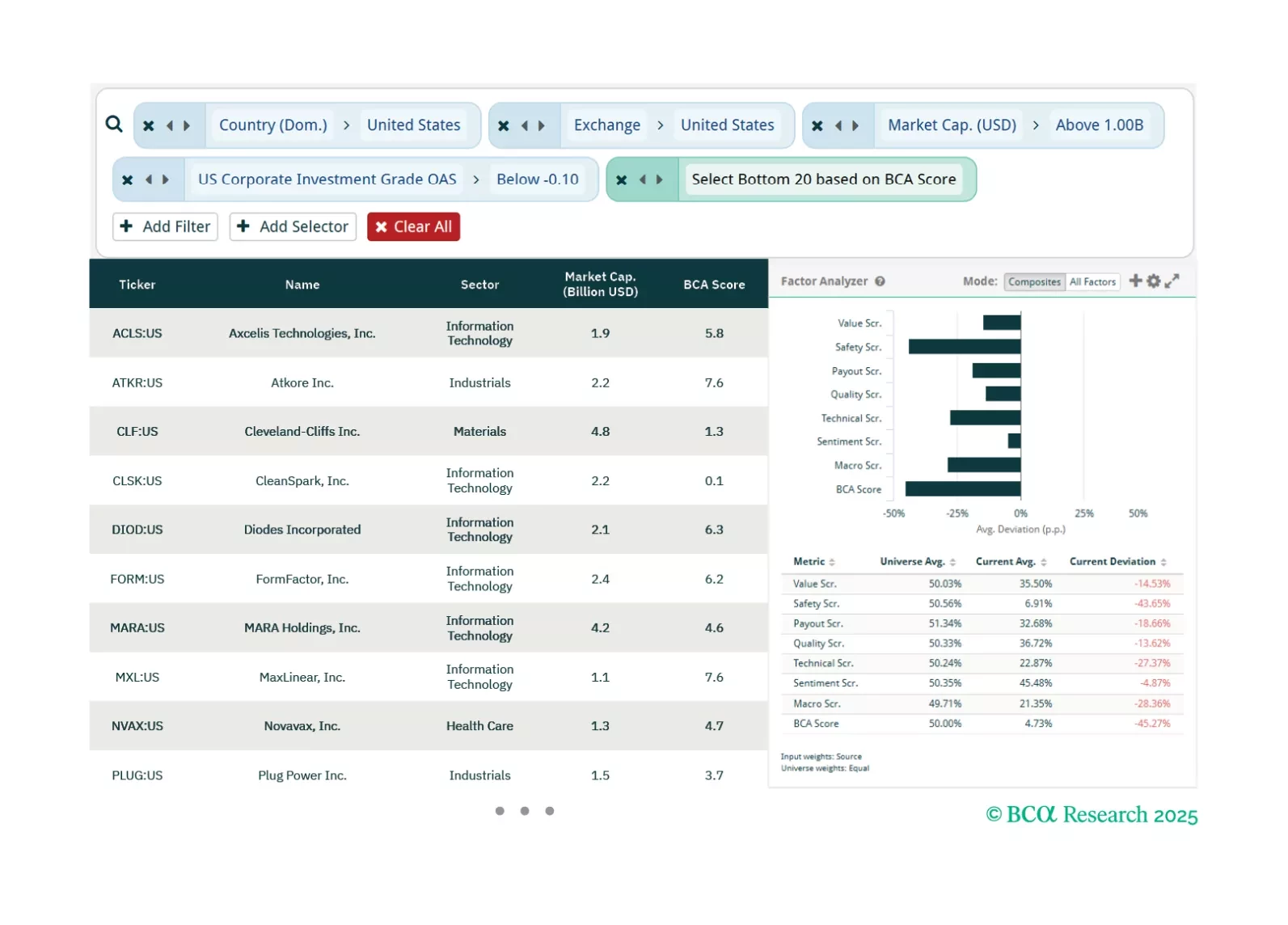

This week, our three screeners cover equity plays in US OAS Spreads, US Exceptionalism, and “DIVE”.

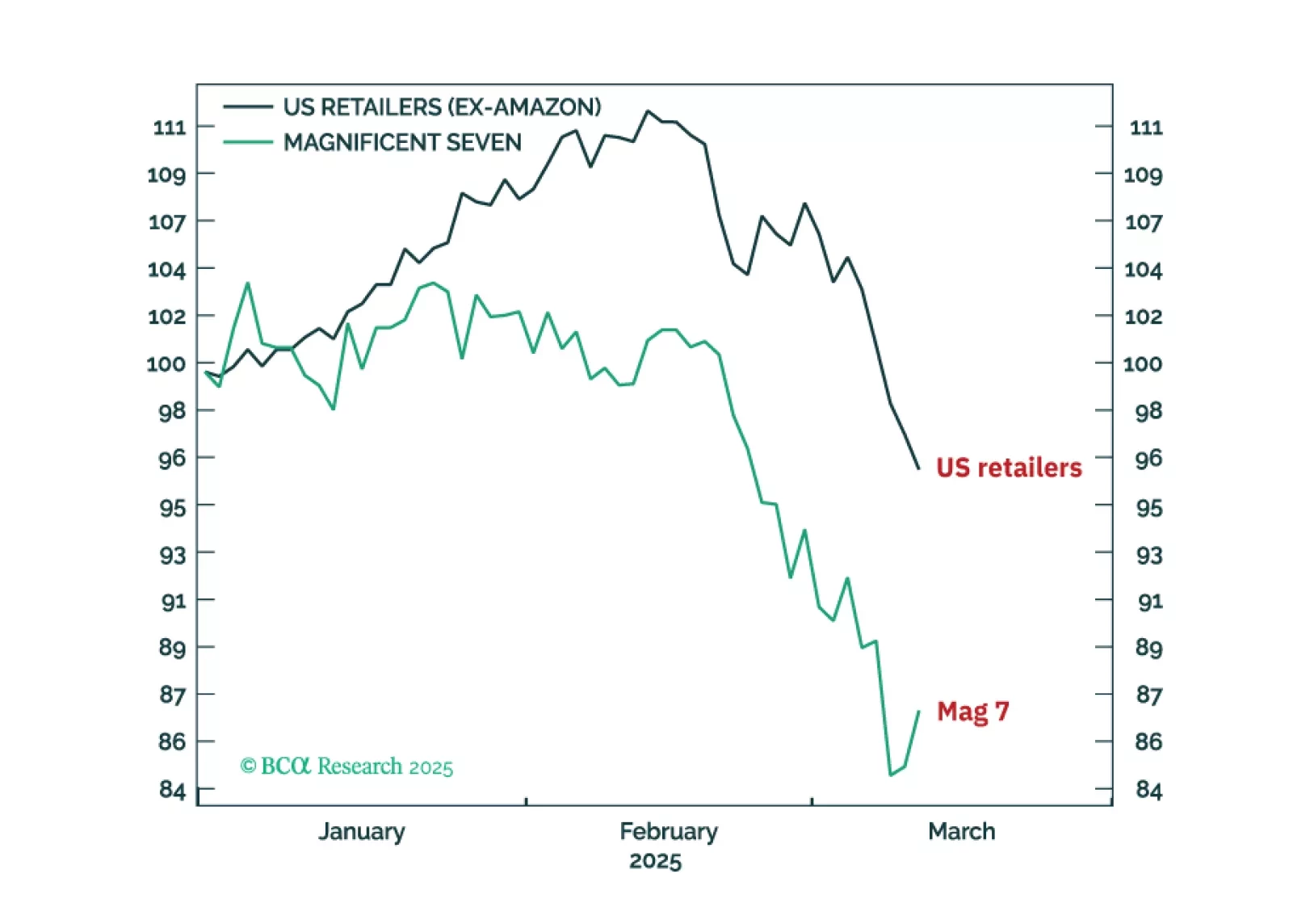

The Trump slump is nearing a temporary reprieve, with a playable countertrend rally in stocks and a tactical rebound in the dollar. Go tactically long USD/SEK. For long-term investors though, the AI bubble still has a lot of air to come out.