Europe

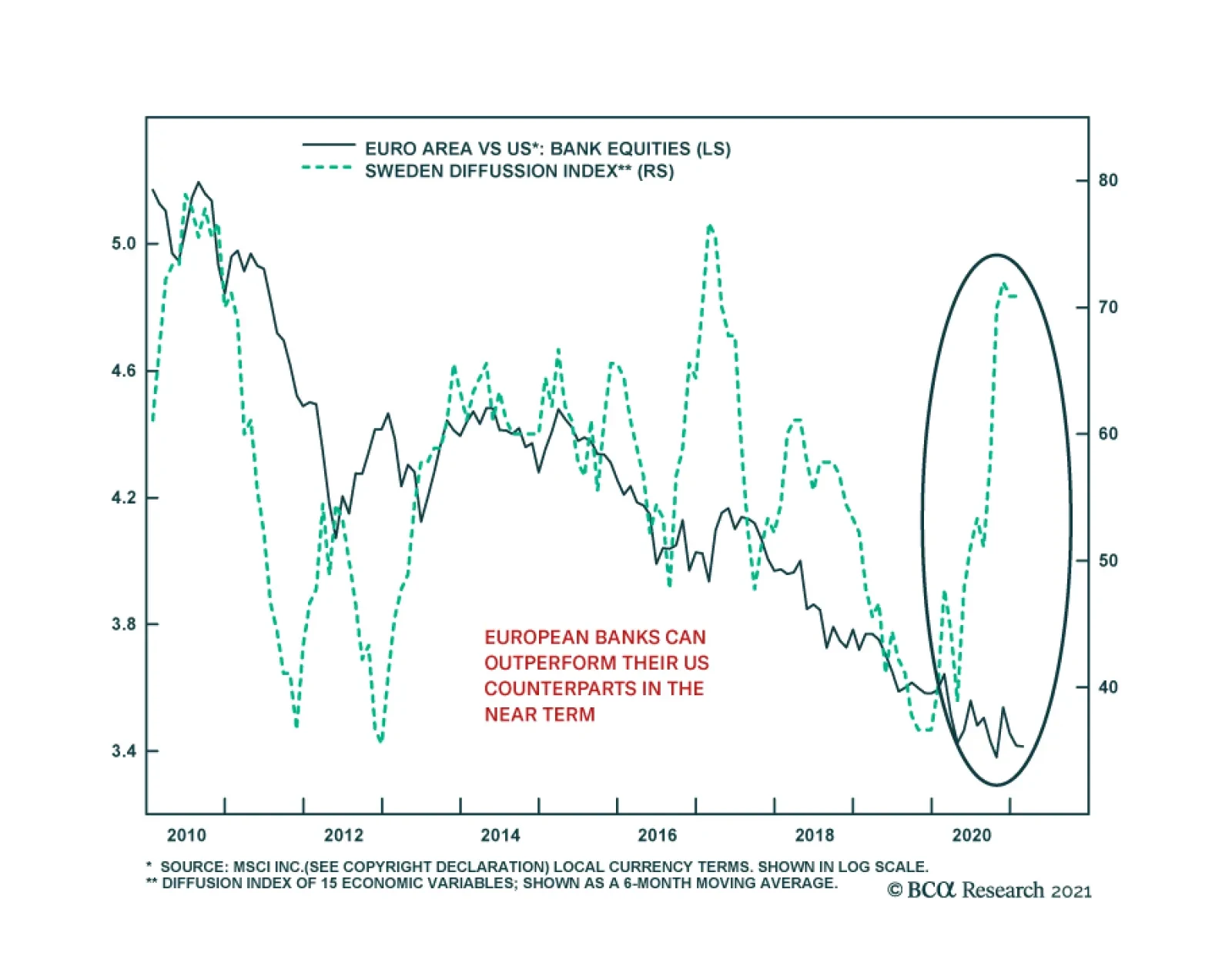

European banks face structural hurdles against their US counterparts. The return on equity of European banks stands well below that of the US, and the lower neutral rate of interest in Europe suggests that European banks will continue to face narrower net…

Highlights For the month of February, our trading model recommends shorting the US dollar versus the euro and Swiss franc. While we agree a barbell strategy makes sense, we would rather hold the yen and the Scandinavian currencies. In the near term, we recommend trades at the crosses, given the potential for the dollar rally to run further. An opportunity has opened up to short the AUD/MXN cross. We are tightening the stop on our short EUR/GBP position to protect profits. We believe EUR/CHF still has upside. While the US has been labelling Switzerland a currency manipulator, the real culprit is Europe. Precious metals remain a buy. We are placing a limit sell on the gold/silver ratio at 70, after our initial target of 65 was touched. Platinum should also outperform in 2021. Remain long AUD/NZD, as the key drivers (relative terms of trade and cheap valuation) remain intact. Feature Currency markets are at a crossroads. On the one hand, news on the vaccine front continues to progress, raising the specter that we might return to normalcy sometime in the second half of this year. On the other hand, the current lockdowns are slowing down economic activity across the developed world, which is bullish for the dollar. With the DXY index up 1.4% this year, it appears near-term economic weakness is dominating the currency market narrative. Our long-term trade basket is centered on a dollar-bearish theme, but we have been shifting much focus in the near term to non-US dollar opportunities. Central to this has been our conviction that the dollar is due for a countertrend bounce, in an order of magnitude of 2%-4%.1 It appears we are already halfway there (Chart I-1). For the month of January, our trade recommendations outperformed the model allocation. Notable trades were being short gold versus silver and being short EUR/GBP. Silver in particular was a big winner in January (Chart I-2). Most emerging market currencies saw weakness, especially the Korean won, Russian ruble, and Brazilian real Chart I-1The Dollar Has Been Strong In 2021

Portfolio And Model Review

Portfolio And Model Review

Chart I-2Our FX Portfolio Did Well In January

Portfolio And Model Review

Portfolio And Model Review

For the month of February, our trading model recommends shorting the US dollar, mostly versus the euro and Swiss franc (Chart I-3 and Chart I-4). The model gets its signal from three variables: Relative interest rates (both levels and rates of change), valuation, and sentiment.2 While some of these variables have moved in favor the dollar, the magnitude of these moves has not been sufficient to trigger a model shift. We agree a barbell strategy makes sense. That said, we would rather hold the yen (as the safe haven, compared to the CHF) and the Scandinavian currencies (compared to the EUR). These are our two strategic positions, and we made the case for yen long positions last week. Chart I-3Our FX Model Remains ##br##Short USD...

Our FX Model Remains Short USD...

Our FX Model Remains Short USD...

Chart I-4...Especially Versus The Euro And Swiss Franc

...Especially Versus The Euro And Swiss Franc

...Especially Versus The Euro And Swiss Franc

Circling back to our trades at the crosses, we maintain that they should continue to perform well in February and beyond. We revisit the rationale behind these trades, as well as introduce a new idea: Short the AUD/MXN cross. Go Short AUD/MXN A tactical opportunity has opened up to go short the AUD/MXN cross. Central to this thesis are three catalysts: relative economic activity, valuation, and sentiment. The Australian PMI has rebounded quite strongly relative to that in Mexico, driven by the performance of the Chinese economy, versus that of the US economy. Australia exports mostly to China, while Mexico is heavily tied to the US economy. With the Chinese credit impulse rolling over, the US economy has been outperforming of late. If past is prologue, this will herald a lower AUD/MXN exchange rate (Chart I-5). Correspondingly, oil prices are outperforming metals prices. China is the biggest consumer of metals, while the US is the biggest consumer of oil. A higher oil-to-metal ratio is negative for AUD/MXN. Terms of trade between Australia and Mexico have been an important driver of the exchange rate (Chart I-5). China had a massive restocking of metals last year, much more than oil and natural gas. This implies that the destocking phase (should it occur) will be most acute among metal inventories (Chart I-6), suggesting oil imports into China could fare better than metals. On a real effective exchange rate basis, the Aussie is expensive relative to the Mexican peso. Historically, this has heralded a lower exchange rate (Chart I-7). Chart I-5AUD/MXN And Terms Of Trade

Portfolio And Model Review

Portfolio And Model Review

Chart I-6Chinese Destocking: From Crude Oil To Metals?

Chinese Destocking: From Crude Oil To Metals?

Chinese Destocking: From Crude Oil To Metals?

Chart I-7AUD/MXN Is ##br##Expensive

AUD/MXN Is Expensive

AUD/MXN Is Expensive

Back in 2020, when everyone was short the Aussie and long the MXN, being a contrarian paid off handsomely. Now, speculators are roughly neutral both crosses. Should the trends we are highlighting carry on into the next few months, this will be a powerful catalyst for speculators to jump on the bandwagon. We recommend opening a short AUD/MXN trade today, with a stop loss at 16.50 and an initial target of 13. Stay Short EUR/GBP Chart I-8An Asymmetry In Pricing

An Asymmetry In Pricing

An Asymmetry In Pricing

Our short EUR/GBP position is performing well, amidst a more hawkish Bank of England this week. Technically, there remains room for much downside on the cross. Real interest rates in the UK are rising relative to those in the euro area. The Brexit discount has not been fully priced out of the EUR/GBP cross, whereas broad US dollar weakness has eroded the discount in cable (Chart I-8). From a technical perspective, speculators are still very long the EUR/GBP, even though our intermediate-term indicator is nearing bombed-out levels (Chart I-9). Chart I-9EUR/GBP Still Has Downside

EUR/GBP Still Has Downside

EUR/GBP Still Has Downside

Finally, short EUR/GBP tends to benefit from an outperformance of oil prices. We will be revisiting the fair value of the pound in upcoming reports given the fundamental shifts that are happening in the post-EU relationship. For now, we are tightening stops on our short EUR/GBP position to 0.89, in order to protect profits. Remain Long NOK And SEK Chart I-10NOK Follows Oil Prices

NOK Follows Oil Prices

NOK Follows Oil Prices

The Scandinavian currencies are extremely cheap and an attractive bet for 2021. As such, we believe the recent relapse in their performance provides an opportunity for fresh long positions. For the NOK, a rising oil price is bullish, both against the EUR and USD (Chart I-10). Meanwhile, superior handling of the pandemic has buoyed domestic economic data in Norway. Both retail sales and domestic inflation have been perking up, pushing the Norges Bank to dial forward expectations of a rate lift-off. Sweden is also holding up relatively well this year. Part of the reason for this is that over the years, the drop in the Swedish krona, both against the US dollar and euro, has made Sweden very competitive. With our models showing the Swedish krona as undervalued by 13% versus the USD, there is much room for currency appreciation before financial conditions tighten significantly. The bottom line is that both Norway and Sweden are well positioned to benefit from a global economic recovery, with much undervalued currencies that will bolster their basic balances. We expect both the SEK and NOK to remain the best performers versus the USD in the coming year. Stay Long EUR/CHF While the US has been labelling Switzerland a currency manipulator, the real culprit is the euro area. To be clear, the SNB has been actively intervening in the currency markets. However, when one looks at relative monetary policy, the expansion in the ECB’s balance sheet far outpaces that of the SNB (Chart I-11). With the correlation between balance sheet policy and the exchange rate shifting, it may embolden Switzerland to intervene even more strongly in currency markets. Historically, the Swiss franc was buffeted by the global environment (improving global trade) and rising productivity in Switzerland. As a result, the SNB had no alternative but to try to recycle those excess savings abroad by lifting its FX reserves, or see even stronger appreciation of its currency. With global trade much more muted, intervention in the FX market could be a more potent headwind for the franc. Chart I-11The SNB Is More Hawkish Than The ECB

The SNB Is More Hawkish Than The ECB

The SNB Is More Hawkish Than The ECB

Chart I-12EUR/CHF And The Global Cycle

EUR/CHF And The Global Cycle

EUR/CHF And The Global Cycle

In the near-term, the risk to this trade is that safe-haven flows reaccelerate, as investors re-price risk. However, this will be a short-term hiccup. EUR/CHF is a procyclical cross and will benefit from improvement in the Eurozone economy relative to the rest of the world (Chart I-12). Meanwhile, by many measures, the Swiss franc remains expensive versus the euro. Stay Long AUD/NZD Chart I-13RBA QE Will Hurt AUD/NZD

RBA QE Will Hurt AUD/NZD

RBA QE Will Hurt AUD/NZD

The rally in the kiwi has provided an exploitable opportunity to lean against it. We remain long the AUD/NZD cross, despite the RBA stepping up the pace of QE at its latest meeting. The rationale is as follows: The balance sheet of the RBA was already lagging that of the RBNZ, so the latest move is simply catch up (Chart I-13). It has no doubt been negative for the cross, as Australia-New Zealand rates have compressed. However, when the program expires, the AUD will be subject to external forces once again. The Australian bourse is heavy in cyclical stocks, notably banks and commodity plays, while the New Zealand stock market is the most defensive in the G10. Should value outperform growth, this will favor the AUD/NZD cross. The kiwi has benefited from rising terms of trade, as agricultural prices have catapulted higher. Should a correction ensue, as we expect, this will favor NZD short positions. Our conviction on long AUD/NZD has clearly been hit with the RBA’s latest move. As such, we are tightening stops to 1.05 for risk management purposes. Stay Long Precious Metals, Especially Silver And Platinum We are placing a limit sell on the gold/silver ratio at 70, after our initial 65 target was hit. The rationale for the trade remains intact: In a world of ample liquidity and a falling US dollar, gold and precious metals are bound to benefit. However, silver has underperformed the rise in gold. The long-term mean for the gold/silver ratio is 50, providing ample alpha for this trade (Chart I-14). Chart I-14The Case For Short Gold Versus Silver

The Case For Short Gold Versus Silver

The Case For Short Gold Versus Silver

Silver is heavily used in the electronics and renewable energy industries, which are capturing the new manufacturing landscape. Silver faced resistance near $30/oz. However, this will be a temporary hiccup. The next important level for silver will be the 2012 highs near $35/oz. After this, silver could take out its 2011 highs that were close to $50/oz, just as gold did. Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Footnotes 1 Please see our Foreign Exchange Strategy report, "Sizing A Potential Dollar Bounce," dated January 15, 2021. 2 Please see our Foreign Exchange Strategy report, "Introducing An FX Trading Model," dated April 24, 2020. Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Limit Orders Closed Trades

Highlights Italy looks like it will form a national unity coalition under Super Mario Draghi – though it is not yet a done deal. A snap election is still our base case, whether in 2021 or 2022, but the ECB will do “whatever it takes,” as will Draghi if he becomes Italy’s prime minister. Even if the right-wing populist parties win power in a snap election, their goal is to expand fiscal spending, not exit the Euro Area. And they would rule in a world where even Germany and Brussels concede the need for soft budgets. Go long BTPs versus German bunds, and Italian stocks versus Spanish stocks, on a tactical 3-6 month horizon. The structural outlook for Italy is still bearish until Italy can secure its recovery and launch structural reforms. Feature In 2016-17 we wrote two special reports on Italy under the heading of “Europe’s Divine Comedy.” In “Inferno” we focused on Italy’s structural flaws and in “Purgatorio” we explained why Italy would stay in the European Union. We have long awaited the chance to write the third installment, which must be called “Paradiso” in honor of Dante Alighieri. But the tragedy of the pandemic makes this title sadly inappropriate. The new government that is tentatively taking shape is not the solution to the country’s long-term problems either. Former European Central Bank President Mario Draghi is an excellent policymaker and would ensure that Italy does not add political chaos to its pandemic woes this year. A unity government under Draghi – which is not yet a done deal as we go to press – would be a tactical and even cyclical positive for Italian equity and bond prices but not a structural positive. The paradise of national revival will have to wait for a later date. In the meantime Italy’s performance will be dictated by its surroundings. The Black Death Italy suffered worse than the rest of Europe from COVID-19, judging both by deaths and the economic slump (Chart 1). It was the first western country to suffer a major outbreak. Outgoing Prime Minister Giuseppe Conte was the first western leader to impose a Chinese-style lockdown – which came as a shock for democratic populations unfamiliar with such draconian measures. Few will forget the terrifying moment in March when the military was deployed in Bergamo to help dispose of the bodies.1 Chart 1Italy's National Crisis

Italy's National Crisis

Italy's National Crisis

Chart 2Italy’s Unemployment Problem – Especially In The South

Europe's Divine Comedy III: Paradiso? Or Paradise Lost?

Europe's Divine Comedy III: Paradiso? Or Paradise Lost?

The crisis struck at an awkward time in Italian politics as well. Like the US and UK, Italy saw a surge of populism in the 2010s. Hostility toward the political elite arose largely in reaction to hyper-globalization, the adoption of the euro, and deep structural flaws that have engendered a sluggish and unequal economy: Poor demographics: Italy’s population peaked in 2017 and is expected to fall from 61 million to 31 million by the year 2100. Its fertility rate is 1.3, the lowest in the OECD except South Korea. It has the third smallest youth share of population (13%) and stands second only to Japan in elderly share of population (23%).2 North-South division: Southern Italy, the Mezzogiorno, is poorer, less educated, less efficient, and less well governed than northern Italy. Unemployment is 7 percentage points higher in the south than in Italy on average (Chart 2). In our “Inferno” report we concluded that regional divisions discourage exiting the Eurozone and EU, since southern Italy benefits from EU transfers and northern Italy would refuse to subsidize southern Italy without EU support (Chart 3). Chart 3EU Budget Allocations Favor Italy

Europe's Divine Comedy III: Paradiso? Or Paradise Lost?

Europe's Divine Comedy III: Paradiso? Or Paradise Lost?

Low productivity: Italy’s real output per hour has lagged that of its European peers as the country has struggled to adjust to globalization, digitization, aging, and emerging technologies (Chart 4). Chart 4Italy's Lagging Productivity

Italy's Lagging Productivity

Italy's Lagging Productivity

High debt: Italy’s debt-to-GDP ratio is expected to rise from to 134.8% to 152.6% by the year 2025, putting it on a higher-debt trajectory than even the worst case projections prior to the pandemic (Chart 5). Normally Italy runs a current account surplus and primary budget surplus, although the pandemic has pushed the country down the road of budget deficits (Chart 6). The debt problem is manageable as long as inflation is low and the ECB purchases Italian government bonds – which it will do in the interest of financial stability. But it sucks away growth and investment over time, a problem that will revive whenever the EU Commission tries to return to semi-normal fiscal policy restraints. Chart 5Italy’s Debt Pile

Europe's Divine Comedy III: Paradiso? Or Paradise Lost?

Europe's Divine Comedy III: Paradiso? Or Paradise Lost?

Chart 6Italy’s Budget Surplus Destroyed By COVID-19

Europe's Divine Comedy III: Paradiso? Or Paradise Lost?

Europe's Divine Comedy III: Paradiso? Or Paradise Lost?

Italy’s predicament can be illustrated simply by comparing the growth of GDP per capita over the past decade to that of Spain, which is a structurally comparable Mediterranean European economy and yet has generated a lot more wealth for its people after having slashed government spending and reformed the labor market and pension system in the wake of the debt crisis (Chart 7). Chart 7Spain Reformed, Italy Didn't

Spain Reformed, Italy Didn't

Spain Reformed, Italy Didn't

Structural reforms undertaken by the technocratic Mario Monti government in the wake of the sovereign debt crisis proved insufficient. Subsequent reform efforts went up in a puff of smoke when Matteo Renzi’s pro-reform constitutional referendum failed in 2016. Italy’s government is congenitally gridlocked because the lower and upper houses of the legislature have equal powers, like in the US, but its parliamentary governments can be easily toppled by either house. The 2016 constitutional reforms would have given the central government historic new powers to force through painful yet necessary structural changes – but centrist voters of different stripes hesitated to grant these new powers since they looked likely to go to populist parties on the brink of victory in the looming 2017 elections. The populists – the right-wing League in the north and the left-wing Five Star Movement in the south – did indeed come to power in 2017 but Italian’s political establishment subsequently restrained them from pursuing either serious euroskepticism or massive fiscal spending. Pro-establishment President Sergio Mattarella rejected any cabinet members who would attack the monetary union. Subsequent battles with Brussels and Germany prevented Italy from passing a blowout stimulus that challenged EU fiscal orthodoxy and threatened to precipitate a solvency crisis in the banking system. In 2019 the ambitious League broke with the Five Star Movement, which collaborated with the center-left Democratic Party to form a new coalition. But the resulting compromise government, its populism diluted, only managed one structural reform – to reduce the size of parliament – plus a moderate increase in government spending. The populist parties ended up being right about the need for more proactive fiscal policy, as Germany conceded in late 2019 and as COVID-19 lockdowns made absolutely necessary in early 2020. French President Emmanuel Macron and German Chancellor Angela Merkel agreed to launch a €750 billion EU Recovery Fund that enabled jointly issued debt for EU members, solidifying a proactive fiscal turn in the bloc. Italy now has €209 billion coming its way. This is a boon for the recovery, though it is also the origin of the politicking that brought down the ruling coalition last month. With central banks monumentally dovish, European and American fiscal engines firing on all cylinders, and China’s 2020 stimulus still coursing through the world’s veins, the macro backdrop is positive for Italy. But with Italy’s economy still shackled by fundamental flaws, it will not be a lead actor or an endogenous growth story. Bottom Line: Italy missed the chance in the 2010s to undertake structural reforms that could lift productivity and potential growth. Now it is struggling to maintain political order in the wake of a devastating pandemic and recession. The vaccine and global recovery will lift Italian assets but the future remains extremely uncertain, given the eventual need to climb down from extreme stimulus and impose painful structural reforms. Paradiso? Or Paradiso Perduto? The latest political turmoil arose over the EU Recovery Fund and how Italy will spend the €209 billion allotted to it, as well as the €38.6 billion allotted to the country under the EU’s structural budget for 2021-28. Ostensibly Matteo Renzi pulled his Italia Viva party out of the ruling coalition because he feared that former Prime Minister Conte, together with his economy and industry ministers, would spend the funds on short-term vote-winning handouts rather than long-term structural fixes in health, education, and culture. But Renzi was not appeased when Conte offered to spend more on health and education as requested. Renzi’s party fares poorly in opinion polls and the recent electoral reforms were not favorable to it, so he can hardly have wanted a new election. He wanted Italy to tap €36 billion from the European Stability Mechanism in addition to taking EU recovery funds, since this would come with strings attached in the form of structural reform. He apparently wanted to precipitate a new pro-establishment coalition. President Mattarella’s appointment of Mario Draghi to lead a national unity coalition is the solution. But as we go to press it is not certain that Draghi will be able to command a majority in parliament. Chart 8Salvini's League Lost Steam But Populist Right Still Powerful

Salvini's League Lost Steam But Populist Right Still Powerful

Salvini's League Lost Steam But Populist Right Still Powerful

Matteo Salvini and the League are the pivotal players now. Salvini and his party suffered loss of popular support in 2019 as a result of his ambitious attempt to break from the government, force new elections, and rule on its own. The party especially suffered from the pandemic, which hit its base of voters in Lombardy hard and sent voters in support of the central government as well as the political establishment (Chart 8). Salvini must now decide whether to try to rebuild his status by joining Draghi in the national interest, to show he can be a team player, albeit at risk of being seen as an institutional politician. If so, he would cede the right-wing anti-establishment space to his partner Giorgia Meloni, who leads the Brothers of Italy, which has eaten up all the support Salvini has lost since the European parliament election of 2019. What is clear is that his current strategy is not working, and he played ball with the big boys during the 2017-19 period, so we would not rule him out of a Draghi government. If Draghi does not win over Salvini and the League, he would need to win the support of the Five Star Movement to form a coalition. The party’s leaders initially said they would not join Draghi, who epitomizes the establishment of which they are sworn enemies. Yet Five Star has not lost any popular support for working with the conventional Democratic Party, in stark contrast with the League, which stayed ideologically pure but lost supporters. Some Five Star members, including Foreign Minister Luigi Di Maio, former leader of the party, want to work with Draghi and stay in government. Hence the party could still join Draghi, or it could break apart with some members defecting. It would require 33% of Five Star members in the Chamber of Deputies and 28% of Five Star members in the Senate to join Draghi to give him a majority, assuming the League and Brothers of Italy refuse to cooperate (Table 1). Interestingly, if the League is absent from the vote, and all parties other than the Brothers and Five Star join Draghi, then he could also form a government. This would give cover to the League under the pretense of COVID vigilance, without being seen as actively preventing a government formation. Table 1'Whatever It Takes' To Build A National Unity Coalition Under Super Mario Draghi

Europe's Divine Comedy III: Paradiso? Or Paradise Lost?

Europe's Divine Comedy III: Paradiso? Or Paradise Lost?

We have favored an early election and this could still occur. If there is an election it will happen before June because an election cannot happen within the last six months of the current president’s term, as per Article 88 of the Constitution. If Italy avoids a snap election till June, political stability is ensured at least till January. The pandemic was the justification for avoiding a snap election but the pandemic did not prevent the regional elections or constitutional referendum in September. The referendum was a hurdle that needed to be cleared before the next election, so now the way is open. All of the parties are greedily eying the presidency, with President Mattarella’s seven-year term set to expire next January. Mattarella has emerged as a staunch defender of the establishment and a check on anti-establishment parties. If the populists gain a plurality prior to January, then they can try to get a more sympathetic or neutral policymaker in that position. By contrast, the pro-establishment parties are hoping that a Draghi coalition can last long enough to ensure that one of their own holds that post. Since the latter need either the League or Five Star to govern, they would have to compromise on the next president – which is a very big concession. In distributing EU recovery funds, there is little doubt that a unity government under Draghi would be a credible way of proceeding. Draghi has joined other central bankers, like the Fed’s Janet Yellen, in voicing strong support for fiscal policy to get the developed democracies out of their current low-growth morass. He would have the authority and expertise to direct spending to productivity-enhancing projects at home while working with Brussels to allow Italy the greatest possible flexibility. Italy’s portion of EU recovery funds is shown in Chart 9, with the black bar indicating the part consisting of loans. The sector breakdown of total EU recovery fund is shown in Table 2. Chart 9Italy’s Fiscal Stimulus To Receive EU Top-Up

Europe's Divine Comedy III: Paradiso? Or Paradise Lost?

Europe's Divine Comedy III: Paradiso? Or Paradise Lost?

Table 2Composition Of EU Recovery Fund By Economic Sector

Europe's Divine Comedy III: Paradiso? Or Paradise Lost?

Europe's Divine Comedy III: Paradiso? Or Paradise Lost?

Yet a Draghi government is not a permanent solution to Italy’s political crisis or its economic malaise. Currently the political parties are squabbling over how to distribute a windfall of special funds – Italy is benefiting from a more pragmatic EU policy as it emerges from a crisis. But in future the parties will be fighting over what to do when the funds are spent. Even if the EU continues to be generous the stimulus will decelerate, while structural reforms will have to be attempted yet again. A technocratic Draghi government would be well positioned to institute the reforms that Italy needs but the economic medicine could sow the seeds for another voter backlash – in which case the anti-establishment right would be in prime position. This would set up a giant clash with Germany and Brussels. Italy, The EU, And Global Power Politics Geopolitically, Italy matters because it is a test of whether the European Union will continue consolidating power within its sphere of influence. If Draghi can form a unity government, oversee economic recovery and long-delayed structural reforms, and survive to reap the benefits at the voting booth, it would mark a historic victory for the EU as it lurches from crisis to crisis in pursuit of deeper integration and ever closer union. The Italian question would effectively be resolved and the EU would have the capacity to handle other challenges elsewhere. Europe’s geopolitical coherence is critical for global geopolitics as well. Europe is the prime beneficiary of US-China competition – at least until such time as it is forced to choose sides. Since Europe is a great power, it can remain neutral for a long time, using America as a stick against Chinese technology theft while expanding market share in China as it diversifies away from the United States (Chart 10). Chancellor Merkel has already signaled to Biden that she is not eager to join any “bloc” against China. Biden will have to devote a massive diplomatic effort to convince the Europeans, who are not as concerned about China’s military and strategic threat, that it is necessary to form a grand alliance toward containing China’s rise. Chart 10EU Balances Between US And China

Europe's Divine Comedy III: Paradiso? Or Paradise Lost?

Europe's Divine Comedy III: Paradiso? Or Paradise Lost?

The EU’s efforts to carve out a sphere of influence have momentum. The German and EU approach to fiscal policy has become more dovish and proactive, a concession to the southern European economies that will improve their support for the European project. Across the Atlantic the EU states see President Trump’s rise and fall as a story of America’s declining influence, which improves the EU’s authority over its own populace, and yet has not resulted in an American-imposed trade war that would undermine the recovery. To the east, EU states see Russian authoritarianism and its discontents, which reinforce the public’s commitment to democratic values and the single market. To the north, they see the negative example of Brexit, which continues to plague the UK, with Scotland pushing for independence again. To the south, Europeans have become less concerned about illegal immigration, having watched the inflow of migrants from Turkey, the Middle East, and North Africa fall sharply – at least until the next major regime failure in these regions causes a new wave of refugees (Chart 11). These events have encouraged various countries to fall in line behind the consensus of European solidarity and geopolitical independence. A technocratic government in Italy would reinforce these trends but a populist government would not be able to avoid or override them. Chart 11Europe Less Concerned About Refugees (For Now)

Europe Less Concerned About Refugees (For Now)

Europe Less Concerned About Refugees (For Now)

Chart 12Italian Euroskeptics Constrained By Public Opinion

Europe's Divine Comedy III: Paradiso? Or Paradise Lost?

Europe's Divine Comedy III: Paradiso? Or Paradise Lost?

The Italian populist parties are still in the ascent but they do not seek to exit the EU or monetary union (Chart 12). We fully expect Italy to see snap elections in 2022 if not 2023, given the fragility of any new coalition to emerge today. If the right-wing League and Brothers should win control of government, and clash with Germany and Brussels, they would still operate within an environment circumscribed by these geopolitical limitations. Otherwise greater solidarity gives the EU greater room for maneuver among the US, China, and Russia. Investment Takeaways In the short run, the Draghi government is bullish for Italian assets. If Draghi fails and snap elections are called, the downside to European equities and the euro is limited, since any risk of an Italian exit from the EU dissipated back in 2016-18. Past turmoil resulted in higher Italian bond yields and wider spreads between BTPs and German bunds because markets had to price in the risk that the Euro Area would break up. We have long highlighted that this risk was overstated and markets are well aware of that by now. The market’s muted reaction to this latest kerfuffle proves the point (Chart 13). Chart 13Markets Unimpressed By Italian Political Turmoil

Markets Unimpressed By Italian Political Turmoil

Markets Unimpressed By Italian Political Turmoil

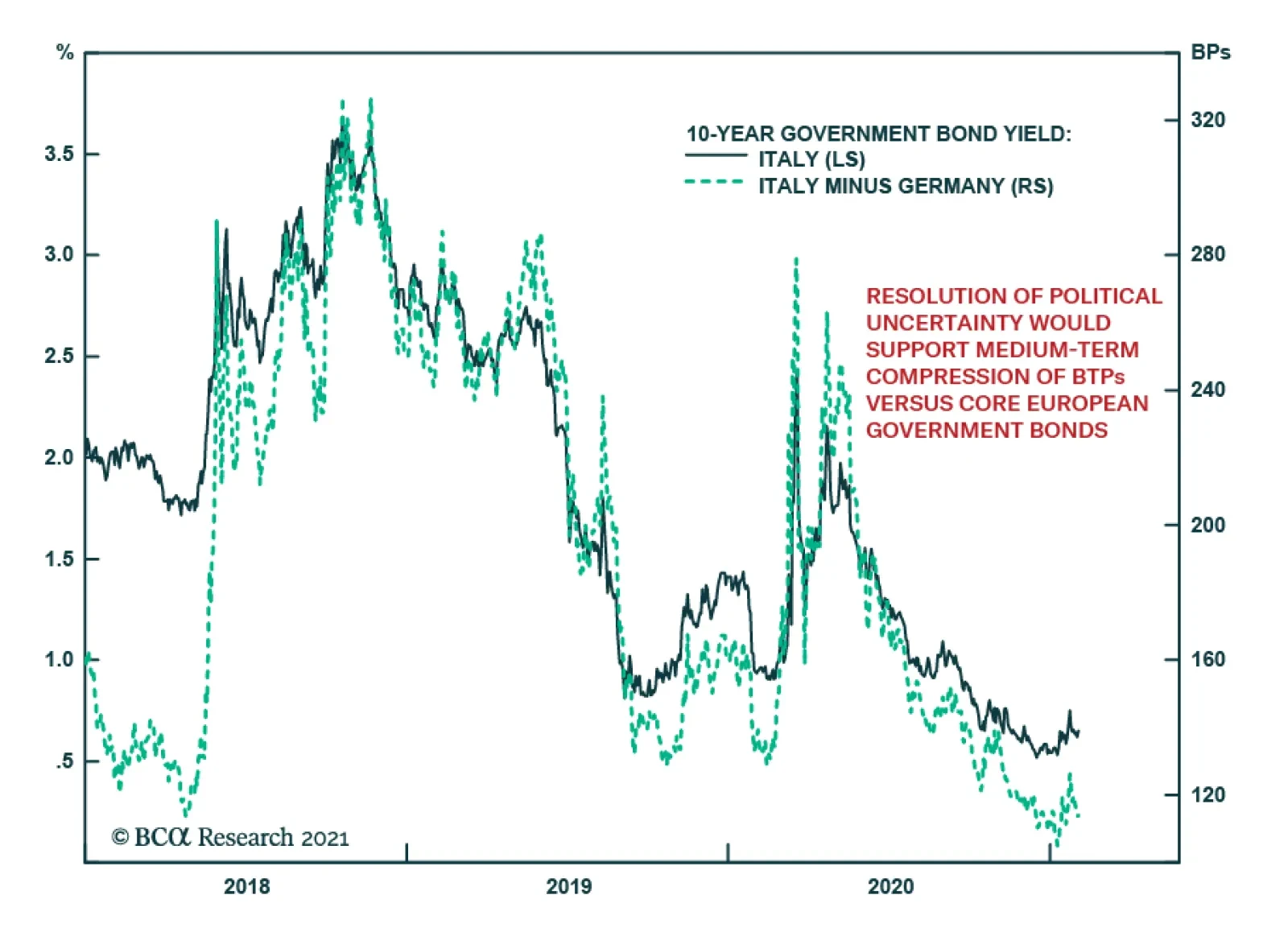

On overweight stance toward Italian government bonds has been one of the highest conviction calls of our fixed income strategist, Rob Robis, over the past year. He expects that Italian bond yields (and spreads over German debt) will converge to Spanish levels, thus restoring a relationship last seen sustainably in 2016. He also notes that the ECB is willing to use quantitative easing to support Italy when its politics inject a risk premium into government bonds and spreads widen. The central bank is also providing additional support to Italy via cheap bank funding (TLTROs) that helps limit Italian risk premia at a time when underlying credit growth is exceedingly weak. During the height of the COVID lockdowns last year, the ECB increased its buying of Italian bonds higher than levels implied by its Capital Key weighting scheme, which officially governs bond purchases. Once Italian yields fell back to pre-pandemic levels, the ECB slowed the pace of purchases to levels at or below the Capital Key weights. As long as the pandemic lingers, the ECB will have the ability and pretext to ensure that Italian spreads do not rise too high (Chart 14). Chart 14Overweight Italian Government Bonds

Overweight Italian Government Bonds

Overweight Italian Government Bonds

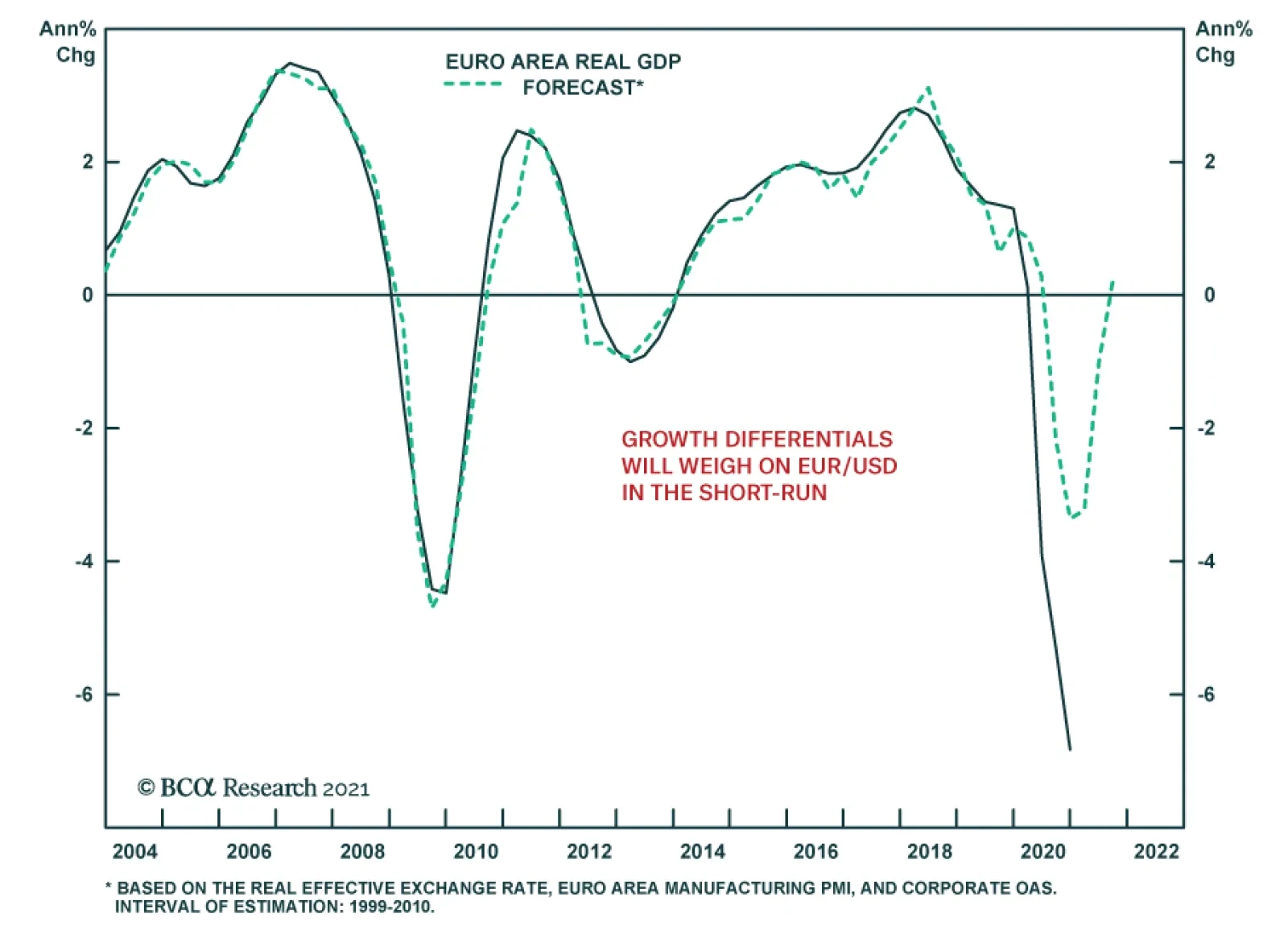

True, investors may be more reluctant to drive Italian yields and spreads to new lows as long as there is a risk of elections this year or next that could bring anti-establishment leaders to power and trigger an increase in Italian political risk premia. But this trap between politics and QE still justifies an overweight stance within global bond portfolios, as Italian yields will remain too attractive for investors to ignore given the puny levels of alternative sovereign bond yields available elsewhere in the Euro Area. Go tactically long Italian BTPs relative to German bunds. Italian stocks have seen a long and dreary downtrend versus global stocks, whether relative to developed or emerging markets, including or excluding the US and China. However, they are trading at a heavy discount in terms of price-to-book and price-to-sales metrics and a Draghi government to direct stimulus funding is doubly good news. Italian stocks have rebounded against Spanish equities since 2017 – as have Italian banks versus Spanish banks. Italian non-performing loans declined from a peak of €178 billion in 2015 to €63 billion in 2020. The banks raised enough equity capital to cover these NPLs. Since banks form a significant part of the Italian bourse, an improvement in bank balance sheets would be positive for the overall market. A Draghi government would reinvigorate this tendency, especially if it credibly commits to structural reforms that elevate potential growth. Spain’s structural reforms are priced in and it is next in line for a post-COVID political shakeup (Chart 15). Go tactically long Italian stocks relative to Spanish. While a Draghi coalition is marginally positive for the euro there are several factors motivating the dollar’s counter-trend bounce in the near term (Chart 16). US and Eurozone growth are diverging, with the EU struggling to roll out its COVID vaccine while the US prepares to pile a new $1.5-$1.9 trillion fiscal stimulus on top of the unspent $900 billion stimulus passed at the end of last year. Chart 15Italian Stocks Have Upside Versus Spanish

Italian Stocks Have Upside Versus Spanish

Italian Stocks Have Upside Versus Spanish

Chart 16Wait For Geopolitical Risk To Clear Before Shorting USD-EUR

Wait For Geopolitical Risk To Clear Before Shorting USD-EUR

Wait For Geopolitical Risk To Clear Before Shorting USD-EUR

Over the long run, a Draghi government provides limited upside with regard to Italian assets. The new coalition serves to avoid an election, not enable structural reform. An unstable ruling coalition will lose support over time in what will be a difficult post-pandemic environment. An early election and anti-establishment victory are not unlikely, if not in 2021 then in 2022 when Italy faces a falling stimulus impulse and the need for painful reforms. For now the truly bullish development is Germany’s dovish shift on fiscal policy rather than any temporary sign of Italian political functionality. Dysfunction can return to Italy fairly quickly but an accommodative Germany is hard to be gotten. Hence Italy’s biggest political risks will come if populist parties win full control of government in the next election while Germany and Brussels seek to normalize fiscal policy and impose some semblance of restraint in the wake of the crisis. It is also possible that a new economic shock or wave of immigration could bring Italy’s populists not only to take power but to rediscover their original euroskepticism. Thus any preference for Italian assets should be seen as a cyclical play on global growth and European solidarity and reflation – not a structural play on Italy’s endogenous strengths. Last week we shifted to the sidelines of the stock rally due to our concern that political and geopolitical risks have fallen too much off the radar. The Biden administration faces tests over China/Taiwan and Iran/Israel. Biden’s tax hikes will come into view soon. Chinese policy tightening is also a concern, even for those of us who do not expect overtightening. These factors pose downside risk to bubbly global stock markets in the near term. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1 Angela Giuffrida and Lorenzo Tondo, "‘A generation has died’: Italian province struggles to bury its coronavirus dead," The Guardian, March 19, 2020, theguardian.com. 2 See Stein Emil Vollset et al, "Fertility, mortality, migration, and population scenarios for 195 countries and territories from 2017 to 2100: a forecasting analysis for the Global Burden of Disease Study," The Lancet, July 14, 2020, thelancet.com.

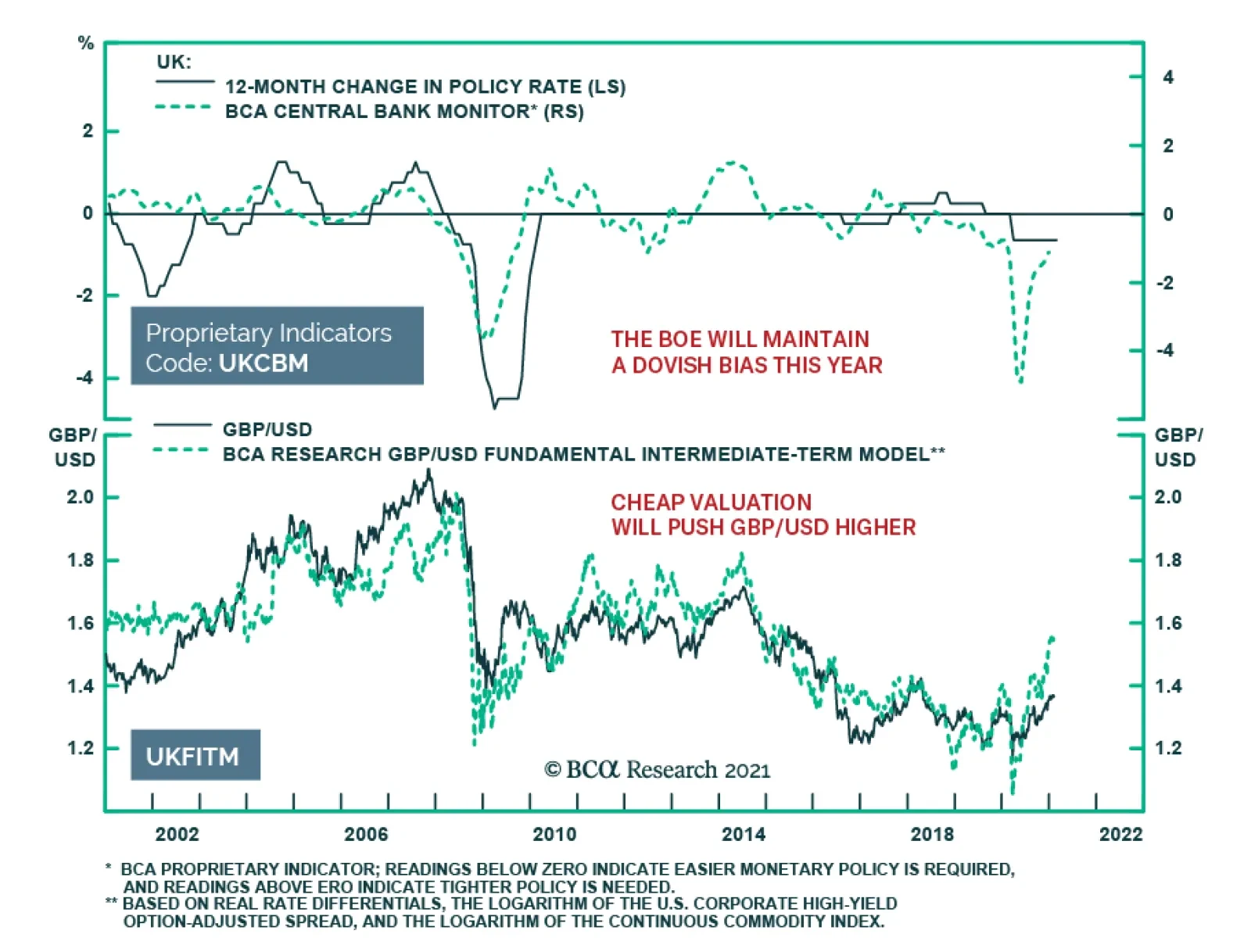

The Bank of England did not adjust monetary policy at the conclusion of its meeting on Thursday. The Bank Rate was maintained at 0.1% and its target stock of asset purchases was held at GBP 895 billion. Although the BoE revised down its Q1 growth forecast to…

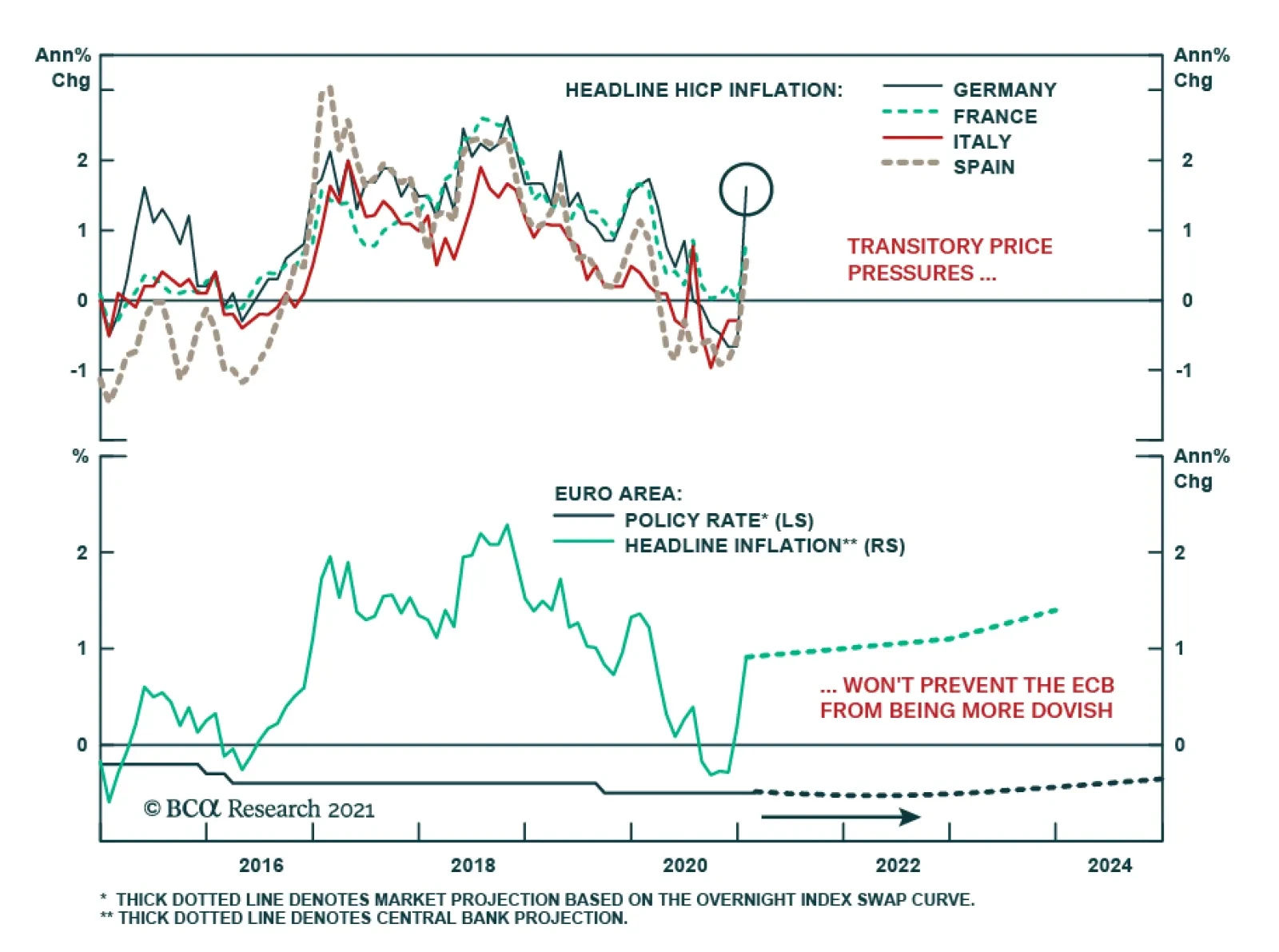

Euro area inflation surprised to the upside in January. The flash headline measure jumped to 0.9% y/y, marking the first annual price increase since July and surpassing expectations of a 0.6% y/y acceleration. Similarly, core CPI accelerated by 1.4% y/y…

Italian markets are cheering Mario Draghi’s acceptance of President Mattarella’s request to form a national unity government. If the former ECB head succeeds, it would eliminate the political uncertainty accompanying snap elections amid a pandemic. It would…

Euro area GDP deteriorated in Q4 on the back of a violent resurgence in the pandemic. On an annualized basis, the economy contracted 0.7% q/q following a 12.4% expansion in Q3. This translates to a 5.1% y/y decline in Q4, bringing the drop in output in 2020…

Highlights GameStop & Bond Yields: The reflationary conditions that helped create a backdrop highly conducive to the wild stock market speculation on display last week – namely, aggressive monetary and fiscal policy stimulus to fight the pandemic – remain bearish for global government bonds and bullish for risk assets like global corporate credit. Remain overweight the latter versus the former. Italy: The latest bout of political uncertainty in Italy has only paused the medium-term spread compression story for BTPs versus core European government bonds, for two reasons: a) this political battle has, to date, had far less of the fiscal populism and anti-Europe flavor of past conflicts; and b) the ECB has shown that it will aggressively use its balance sheet to prevent a spike in Italian bond yields. Maintain an overweight stance on Italy in global bond portfolios, even with early elections likely later this year. Feature Dear Client, The next Global Fixed Income Strategy publication will be a Special Report on Canada, jointly published with our colleagues at Foreign Exchange Strategy on Friday, February 12. We will return to our regular publishing schedule on Tuesday, February 16. Rob Robis, Chief Global Fixed Income Strategist Chart of the WeekExpect More Bubbles & GameStop-Like Silliness

Expect More Bubbles & GameStop-Like Silliness

Expect More Bubbles & GameStop-Like Silliness

The “Reddit Retail Revolution” has exposed the dangers of staying too long in crowded short positions for equities like GameStop, but bond markets were unfazed by the wild moves in stocks last week. US Treasury yields actually crept upwards as the mother of all short squeezes became the top news story in America. Corporate credit spreads worldwide were essentially unchanged, despite the pickup in US equity volatility measures like the VIX. Bond investors recognize that, while the sideshow of rebel traders taking on mighty hedge funds makes for great theater, the underlying reflationary global policy backdrop remains the main driver of global bond yields and credit risk premia (Chart of the Week). Global fiscal policy risks are increasingly tilted towards more stimulus than currently projected, even as the pace of new COVID-19 cases is starting to slow in the US and much of Europe. Vaccine rollouts in many countries are going far slower than expected, which has forced global central banks to commit to maintaining highly accommodative policies - zero interest rates, quantitative easing (QE) and cheap bank funding – for longer. As Fed Chair Jerome Powell noted in his press conference following last week’s FOMC meeting, “There’s nothing more important to the economy now than people getting vaccinated.” Chart 2Vaccine Rollout Critical For Fed/ECB/BoE Policy

The Revolution Will Be Monetized

The Revolution Will Be Monetized

On that front, the largest economies on both sides of the Atlantic continue to perform poorly. According to data from the Duke Global Health Innovation Center, vaccination coverage (defined as actual vaccination doses acquired on a per person basis) in the US, UK and European Union remains low relative to the intensity of COVID-19 cases within the population (Chart 2) – especially compared to the experience of other major Western countries.1 As we discussed in last week’s report, it is far too soon for investors to fear a hawkish move by global central banks towards tapering asset purchases and signaling future interest rate hikes.2 The GameStop episode may cause some policymakers to worry about the financial stability risks resulting from cheap money policies, but not before the greater risks to global growth from the COVID-19 pandemic are contained. Until vaccination rates rise to levels where there is the potential for herd immunity to be reached, central banks will have little choice by to maintain 0% (or lower) policy rates for longer with continued expansion of their balance sheets (Chart 3). Policy makers will even likely respond with more QE in the event of broad financial market turmoil occurring before inflation expectations return to central bank targets (Chart 4). Chart 3Expect More Global QE ...

The Revolution Will Be Monetized

The Revolution Will Be Monetized

Chart 4...To Moderate Reflationary Pressure On Bond Yields

...To Moderate Reflationary Pressure On Bond Yields

...To Moderate Reflationary Pressure On Bond Yields

We continue to recommend the following medium-term positioning for reflation-based themes in global fixed income markets: below-benchmark overall duration exposure, favoring lower-quality corporate bonds versus government debt, and underweighting US Treasuries within global government bond portfolios. Bottom Line: The reflationary conditions that have helped create a backdrop highly conducive to the wild stock market speculation on display last week – namely, aggressive monetary and fiscal policy stimulus to fight the pandemic – remain bearish for global government bonds and bullish for risk assets like global corporate credit. Italy: ECB Policy Trumps Political Uncertainty One of our highest conviction fixed income investment recommendations over the past year has been to overweight Italian government bonds (BTPs). We have maintained that bullish stance with an expectation that Italian bond yields (and spreads over German debt) would converge to the levels of Spain, restoring a relationship last seen sustainably in 2016 (Chart 5). Chart 5A Small Response To Italian Political Uncertainty

A Small Response To Italian Political Uncertainty

A Small Response To Italian Political Uncertainty

The recent collapse of the coalition government of Prime Minister Giuseppe Conte would, in a more “normal” time, represent a serious threat to the stability of the Italian bond market and our bullish view. Yet the response so far has been muted, with the spread between 10-year BTPs and German Bunds up only 11bps from the mid-January lows. The current political drama stemmed from a disagreement within the ruling coalition over how the government was planning to use Italy’s share of the €750bn EU Recovery Fund. As we go to press, the survival of the current government hangs in the balance, with President Sergio Mattarella testing whether the political parties can form a government with a majority. The initial announcement of that Recovery Fund was considered to be a major reason for a reduced risk premium on Italian government bonds, as it represented a potential step towards greater fiscal integration within Europe. Unfortunately, it took the COVID-19 crisis to get the rest of Europe to offer help to the more economically fragile countries like Italy. The country suffered one of the world’s worst initial waves of the virus and the late-2020 surge has also hit hard – although, more recently, Italy has fared far better than Southern European neighbors Spain and Portugal with a slower pace of new cases and hospitalizations (Chart 6). Italy’s economy has struggled under the weight of some of the most stringent restrictions on activity within Europe to stop the spread of the virus, according to the Oxford COVID-19 database (Chart 7). Domestic spending on retail and recreation activities is estimated to be down nearly 50% from the start of the pandemic, a hit to the economy made worse by the collapse of tourism revenue that will take years to fully recover. In other words, Italy desperately needs the money from the EU Recovery Fund. Chart 6Italy's COVID-19 Situation Is Slowly Improving

Italy's COVID-19 Situation Is Slowly Improving

Italy's COVID-19 Situation Is Slowly Improving

Chart 7A Big Economic Hit To Italy From COVID-19

A Big Economic Hit To Italy From COVID-19

A Big Economic Hit To Italy From COVID-19

Former Prime Minister Matteo Renzi and his Italia Viva party precipitated the crisis by withdrawing their support from Conte’s coalition, but are in a weak position electorally. They claim that the funds should be handled by parliament, rather than a technocratic council overseen by Conte, and devoted to long-term structural reform rather than short-term fixes. Renzi’s withdrawal from the ruling coalition, however, is not grounded in substantial disagreements over fiscal spending: First, the EU recovery fund requires all member states to use 30% of the funds on climate change initiatives and 25% on digitizing the economy, and none of the major parties oppose this use of the €209 billion coming their way. Second, Prime Minister Conte adjusted his spending plans, nearly doubling the allocations for health, education, and culture, in response to Renzi’s criticisms that not enough spending focused on structural needs. Third, Renzi wants to tap €36 billion from the European Stability Mechanism in addition to taking recovery funds, but this would come with austerity measures attached (which is self-defeating) and would be opposed by the left-wing populist Five Star Movement, a linchpin in the ruling coalition. Even if the immediate political turmoil passes, there will still be an elevated risk of an early election as the various parties jockey for power in the wake of the cataclysmic pandemic, and as they eye control of the presidency, which is up for grabs in 2022. The only real change on the fiscal front would come if the populist League and Brothers of Italy ended up winning a majority and control of government in the eventual elections, as they favor much greater fiscal largesse. It is possible that Conte will survive as his personal support has increased throughout the crisis. Otherwise, former ECB President Mario Draghi could replace him, although he is now less popular than Conte. President Mattarella is not eager to dissolve parliament given that the combined strength of right-wing anti-establishment parties is greater than that of the centrist and left-wing parties in the ruling coalition judging by public opinion polls (Chart 8). Yet sooner rather than later, a new election looms. The country already completed an electoral reform via a referendum in September 2020 that cleared the way for a new election to be held. Chart 8Unstable Coalition Wants To Delay Election As Populist Right Slightly Ahead

Unstable Coalition Wants To Delay Election As Populist Right Slightly Ahead

Unstable Coalition Wants To Delay Election As Populist Right Slightly Ahead

Chart 9Waning Immigration Undercuts Italian Populists (For Now)

The Revolution Will Be Monetized

The Revolution Will Be Monetized

The current crisis is different than past bouts of Italian political uncertainty as there is less of a question over Italy’s commitment to the euro - which in the past has resulted in higher Italian bond yields and wider BTP-Bund spreads as markets had to price in euro breakup risk. The current coalition, and any new coalition cobbled out of the current morass to prevent a snap election, are united in their opposition to the populist League and the Brothers of Italy. They will strive to remain in power to distribute the EU recovery funds and secure the Italian presidency for an establishment political elite – one, like Mattarella, who will act as a check on the power of any future populist government and its cabinet choices, just as Mattarella himself hobbled the League’s most radical proposals from 2018-19. Chart 10Italian Support For EU & The Euro Sufficient But Not Ironclad

The Revolution Will Be Monetized

The Revolution Will Be Monetized

While the right-wing “sovereigntist” parties lead in the opinion polls, the League has lost support since its leader Matteo Salvini’s failed bid to trigger an election in August 2019 and especially since the COVID-19 outbreak has boosted the establishment parties and coalition members. Anti-immigration sentiment, a key support of this faction, has subsided as the EU has cut down the influx of immigrants (Chart 9). Salvini and his supporters have also compromised their euroskepticism to appeal to a broader audience as 60% of the populace still approves of the euro – although this support is falling again and bears monitoring (Chart 10). Another economic shock or a new wave of immigration could put the right-wing populists into power. Moreover, an unstable ruling coalition will lose support over time in what will be a difficult post-pandemic environment. Thus, the risk of euroskepticism and fiscal populism will persist over the coming two years, even though they are most likely contained at the moment. Has The ECB Removed The Tail Risk Of BTPs? The ECB has shown they are willing to use their balance sheet via QE and cheap bank funding tools like TLTROs to support the euro area’s weakest link – Italy. Thus, any upward pressure on Italian bond yields/spreads from the current political fracas will almost certainly be met by a more aggressive ECB response (more QE for longer, new TLTROs), limiting the damage to the Italian bond market. Chart 11What Would Italian Loan Growth Be WITHOUT ECB Support?

What Would Italian Loan Growth Be WITHOUT ECB Support?

What Would Italian Loan Growth Be WITHOUT ECB Support?

The ECB’s TLTROs appear to have been helpful for Italy, whose LTRO allotments represent 14.7% of total bank lending (Chart 11). Yet Spanish banks have relied on cheap ECB funding to a similar degree, while the growth of bank lending in Italy has substantially lagged that of Spain since the start of the pandemic in 2020 – even with Italy having less restrictive lending standards according to the ECB’s Bank Lending Survey. The ECB has also helped Italy by being more flexible with its purchases of Italian government bonds within both the Public Sector Purchase Program (PSPP) and the Pandemic Emergency Purchase Program (PEPP) that began in response to COVID-19. ECB data show that, after the worst days of the COVID-19 market rout last spring when the 10-year Italian bond yield soared from 1% to 2.4% over just three weeks, the ECB increased the Italy share of its bond buying to levels well above the Capital Key weighting scheme that “officially” governs the bond purchases. This was true within both the PSPP (Chart 12) and the PSPP (Chart 13). Chart 12ECB Paying Less Attention To The Capital Key In The PSPP ...

The Revolution Will Be Monetized

The Revolution Will Be Monetized

Chart 13… And The PEPP

The Revolution Will Be Monetized

The Revolution Will Be Monetized

Chart 14Stay Overweight Italian Government Bonds

Stay Overweight Italian Government Bonds

Stay Overweight Italian Government Bonds

The ECB’s actions helped stabilize Italian bond yields, sowing the seeds of the major decline in yields that took place between April and September. Once Italian bond yields fell back to pre-pandemic levels, the ECB slowed the pace of its purchases of Italian bonds to levels at or below the Capital Key weights. Thus, the ECB was willing to deviate from its own self-imposed rules for its bond purchase schemes in order to ease financial conditions in Italy during a pandemic. There is no reason to believe that would not occur again if yields rise because of a growing political risk premium while the pandemic was still raging. A prolonged period of political uncertainty in Italy, especially one that ends with fresh elections, could even force the ECB to maintain or extend its full current mix of policies and not just QE. For example, a new TLTRO could be initiated later this year, or the subsidized cost of banks borrowing from existing TLTROs could be reduced further, all in an effort to help boost Italian lending activity. More likely, the PEPP could be expanded in size or extended beyond the current March 2022 expiration, or the PSPP could be upsized to allow for more purchases of Italian debt (Chart 14). From an investment strategy perspective, there is still a strong case for overweighting Italian government bonds in global fixed income portfolios, even with the current political uncertainty. The weight of ECB policy actions removes much of the usual upside risk to BTP yields. However, investors will likely be more reluctant to drive Italian yields (and spreads versus Germany) to fresh lows if there is a risk of early elections, as we expect. Italian bonds are now more of a pure carry with yields trapped between politics and QE, but that still justifies an overweight stance - especially given the puny levels of alternative sovereign bond yields available elsewhere in the euro area. Bottom Line: The latest bout of political uncertainty in Italy has only paused the medium-term spread compression story for BTPs versus core European government bonds, for two reasons: a) this political battle has, to date, had far less of the fiscal populism and anti-Europe flavor of past conflicts; and b) the ECB has shown that it will aggressively use its balance sheet to prevent a spike in Italian bond yields. Maintain an overweight stance on Italy in global bond portfolios, even with early elections likely later this year. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1 The Duke Global Health Innovation Center data on COVID-19 can be found here: https://launchandscalefaster.org/COVID-19. 2 Please see BCA Research Global Fixed Income Strategy Report, "A Pause, Not A Peak, In Global Bond Yields", dated January 26, 2021, available at gfis.bcaresearch.com. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

The Revolution Will Be Monetized

The Revolution Will Be Monetized

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

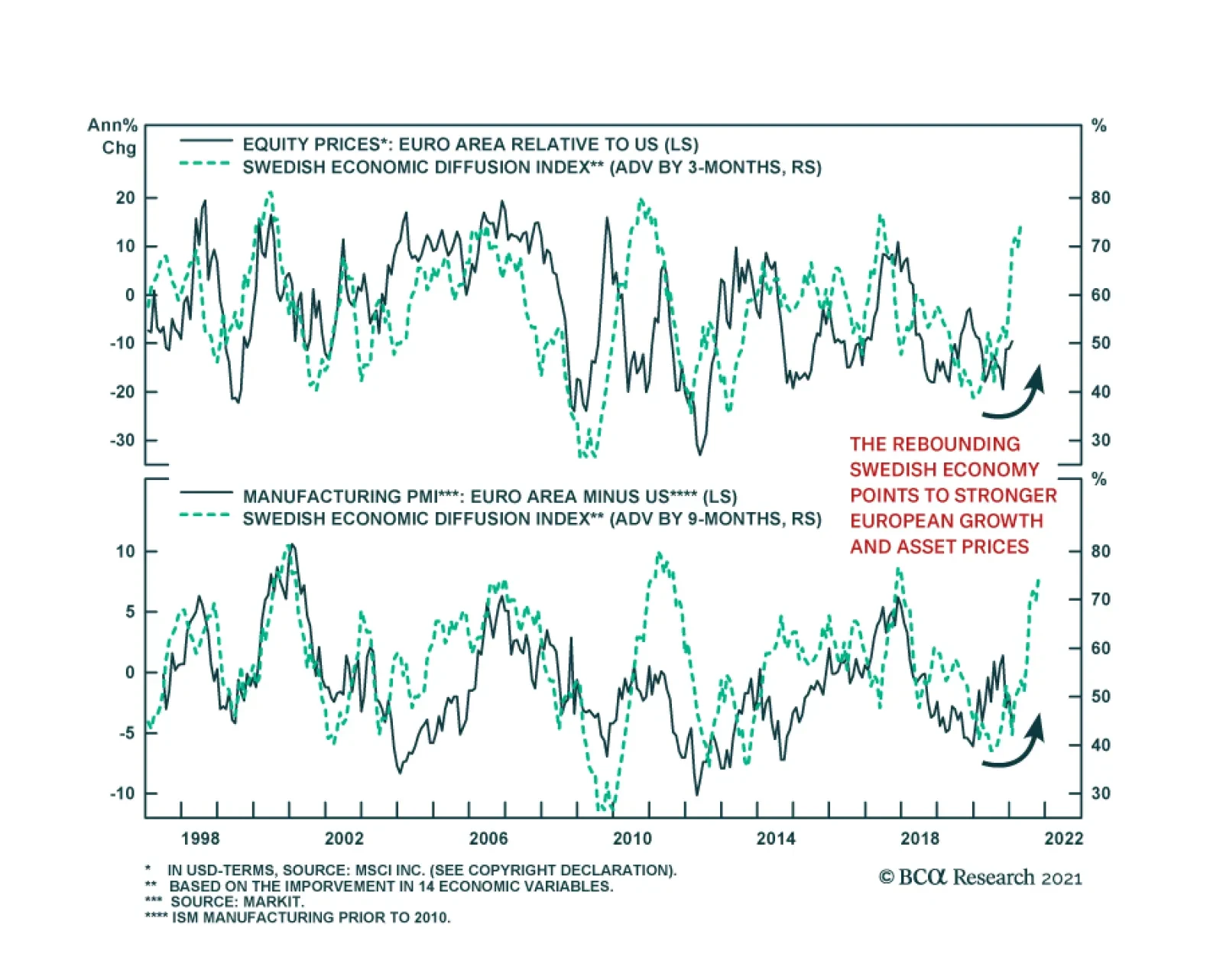

Sweden has a small open economy that specializes in the exports of intermediate industrial goods. This property not only makes Sweden extremely sensitive to the global business cycle, but also, Sweden is among the first advanced economies to respond to pick…

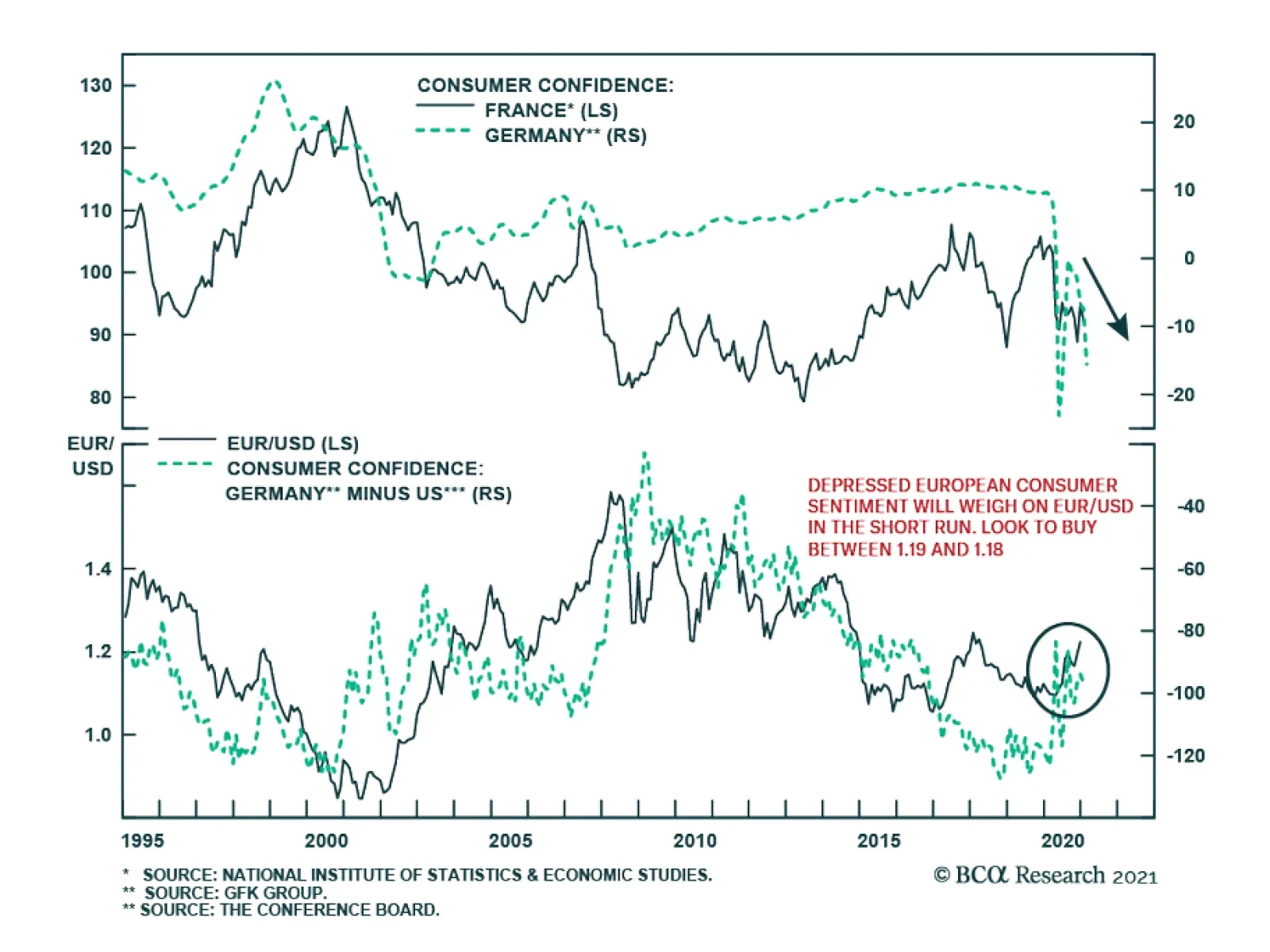

Consumer confidence is collapsing in Europe amid widespread lockdowns to contain the latest wave of infections. Germany’s GfK survey dropped to -15.6 for February, marking the lowest reading since July, the third-lowest reading in the history of the…