Europe

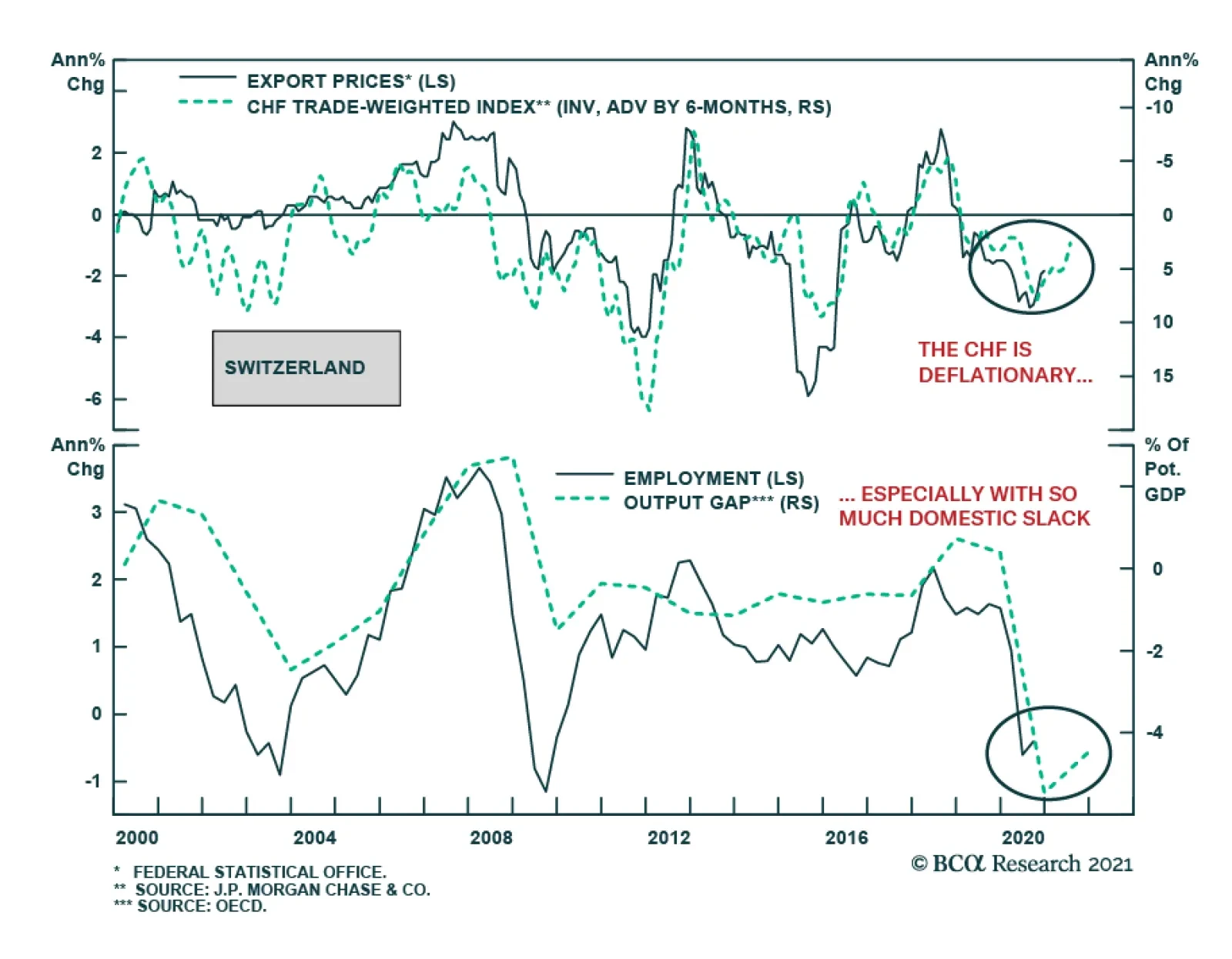

Switzerland has been named a currency manipulator, yet, the SNB will persevere with its aggressive balance sheet policy because it has no choice. The Swiss economy remains under the threat of deflationary pressures, with headline and core inflation…

Highlights Global Yields: The fall in global bond yields over the past two weeks represents a corrective pullback from an overly rapid rise in inflation expectations, especially in the US. The underlying reflationary themes that drove yields higher, however, remain intact, even with uncertainty over COVID-19 vaccine distribution and mixed messages on future central bank policy moves. Duration Strategy: We maintain our broad core recommendations on global government bonds: stay below-benchmark on overall duration exposure, overweighting non-US markets versus US Treasuries, while favoring inflation-linked debt over nominal bonds. Australia vs. US: Following from the conclusions of our Special Report on Australia published last week, we are initiating a new cross-country spread trade in our Tactical Overlay portfolio: long 10-year Australian government bond futures versus short 10-year US Treasury futures. Feature Chart of the WeekCentral Banks Will Stay Very Dovish

Central Banks Will Stay Very Dovish

Central Banks Will Stay Very Dovish

The benchmark 10-year US Treasury yield fell to 1.04% yesterday as this report went to press, after reaching a high of 1.18% on January 12th. 10-year government bond yields have also fallen over the same period, but by lesser amounts ranging between 5-10bps, in Germany, France, the UK and Australia. We view these moves as a consolidation before the next upleg in global yields, and not the start of a new bullish cyclical phase for government bond markets. Our Central Bank Monitors for the major developed economies are all showing diminished pressure for easier monetary policies, but are not yet signaling a need for tightening to slow overheating economies (Chart of the Week). Realized inflation and breakevens from inflation-linked bond markets remain below levels consistent with central bank policy targets, even in the US after the big run-up in TIPS breakevens. Reflationary, pro-growth monetary (and fiscal) policies are still necessary. Policymakers can talk all they want about optimism on future global growth with COVID-19 vaccines now being rolled out in more countries, but it is far too soon to expect any shift away from a maximum dovish monetary policy stance that is bearish for bonds and bullish for risk assets. We continue to recommend a below-benchmark overall stance on global cyclical duration exposure, with a country allocation focused most intensely on underweighting US Treasuries. The Global Backdrop Remains Bond Bearish Optimism over a potential boom in global economic growth in the second half of 2021 - fueled by the rollout of COVID-19 vaccines, massive pandemic income support programs and other increased government spending measures, and ongoing easy monetary policies – has become an increasingly consensus view among investors. As evidence of this, the latest edition of the widely-followed Bank of America Fund Managers’ Survey highlighted that the biggest tail risks for financial markets all relate to that bullish narrative: a disappointing vaccine rollout, a “Tantrum” in bond markets, a bursting of the US equity bubble and rising inflation expectations.1 We can understand why investors would be most worried about the success of the COVID-19 vaccine distribution which has started with mixed results. According to the Oxford University COVID-19 database, the UK has now delivered 10.38 vaccinations per 100 people, while the US has given out 6.6 shots per 100 people (Chart 2). By comparison, the pace of the vaccine rollout has been far slower in Germany, France, Italy and China. Note that this data shows total vaccine shots administered and does not represent a count of the total number of inoculated citizens, as a full dose requires two shots. Chart 2Vaccine Rollout So Far: Operation Impulse Power

A Pause, Not A Peak, In Global Bond Yields

A Pause, Not A Peak, In Global Bond Yields

Success on the vaccine front is what is needed for investors to envision an eventual end to the pandemic … or at least an end to the growth-damaging lockdowns related to the pandemic. So a slower-than-expected rollout does justify somewhat lower bond yields, all else equal. However, the news on the spread of the virus itself has turned more encouraging during this “dark winter” of COVID-19. The latest data on new cases of the virus shows that the severe surge in the US and UK appears to have peaked (Chart 3). In the euro area, the overall number of new cases is at best stabilizing with more divergence between countries: cases are continuing to explode higher in Italy and Spain but slowing in large economies like Germany and the Netherlands (and stabilizing in France). The growth in new virus-related hospitalizations, however, has clearly slowed across those major economies, including in places with surging new case numbers like Italy. Chart 3Lockdowns Will Not Last Forever

Lockdowns Will Not Last Forever

Lockdowns Will Not Last Forever

Chart 4European Lockdowns Taking A Bite Out Of Growth

European Lockdowns Taking A Bite Out Of Growth

European Lockdowns Taking A Bite Out Of Growth

A reduction in the strain on hospital bed capacity gives hope that the current severe economic restrictions seen in Europe and parts of the US can soon begin to be lifted. This can help sustain the cyclical upturn in global economic growth, especially in countries where lockdowns have been most onerous like the UK, which saw a sharp plunge in the preliminary Markit PMI data for January (Chart 4). So on the COVID-19 front, we interpret the overall backdrop as more positive for global growth expectations, and hence more supportive of higher global bond yields. Chart 5Reflationary Expectations Remain Well Entrenched

Reflationary Expectations Remain Well Entrenched

Reflationary Expectations Remain Well Entrenched

Expectations are still tilted towards rising yields, judging by the ZEW survey of global financial market professionals (Chart 5). The survey shows that the bias continues to lean towards expectations of both higher long-term interest rates and inflation, but without any expected increase in short-term interest rates. This fits with the overall yield curve steepening theme that has driven global bond markets since last summer, which has been consistent with the dovish messaging from central banks. The Fed, ECB and other major central banks continue to project a very slow recovery of labor markets from the COVID-19 shock, with no return to pre-pandemic levels until at least 2024 (Chart 6). This is forcing central banks to maintain as dovish a policy mix as possible, including projecting stable policy rates over the next several years supported by ongoing quantitative easing (QE). These policies have helped support the rise in global inflation expectations and helped fuel the “Everything Rally” that has stretched the valuations of risk assets worldwide. So it is also not surprising that worries about a bond “Tantrum”, rising inflation expectations and a bursting of equity bubbles would also top the tail risks highlighted in that Bank of America investor survey. All are connected to the next moves of the major global central banks. Chart 6Central Banks Must Stay Easy For A Long Time

Central Banks Must Stay Easy For A Long Time

Central Banks Must Stay Easy For A Long Time

On that front, we are not worried about any premature shift to a less dovish stance, given the lingering uncertainties over COVID-19 and with actual inflation – and inflation expectations - remaining below central bank targets. Several officials from the world’s most important central bank, the US Federal Reserve, have made comments in recent weeks discussing the outlook for US monetary policy. A few FOMC members raised the possibility of a potential discussion of slower bond purchases by year-end, if the US economy grows faster than expected and the vaccine rollout goes smoothly. Although the majority of FOMC members, including Fed Chair Jerome Powell and Vice-Chairman Richard Clarida, noted that any such discussion was premature and would not take place until 2022 at the earliest. In our view, the Fed will not begin to signal any shift to a less dovish policy stance before US inflation and inflation expectations have all sustainably returned to levels consistent with the Fed’s 2% target (Chart 7). That means seeing TIPS breakevens rise to the 2.3-2.5% range that has prevailed during previous periods when headline PCE inflation as at or above 2%. Chart 7US Inflation Still Justifies Maximum Fed Dovishness

US Inflation Still Justifies Maximum Fed Dovishness

US Inflation Still Justifies Maximum Fed Dovishness

Chart 8The Fed Is Not Yet Worried About Overly Easy Financial Conditions

The Fed Is Not Yet Worried About Overly Easy Financial Conditions

The Fed Is Not Yet Worried About Overly Easy Financial Conditions

Such a shift by the Fed could happen by year-end, but only if there was also concern within the FOMC that financial conditions in the US had become overly stimulative and risked future instability of overvalued asset prices (Chart 8). At the present time, however, the Fed will continue to focus on policy reflation and worry about any negative spillover effects on financial markets at a later date. Financial conditions are also a potential issue for other central banks, but from a different perspective – currencies. Financial conditions in more export-focused economies like the euro area and Australia are more heavily influenced by the impact on competitiveness from currency values (Chart 9). Chart 9Currencies Dictate Financial Conditions Outside The US

Currencies Dictate Financial Conditions Outside The US

Currencies Dictate Financial Conditions Outside The US

Chart 10Projected Relative QE Favors UST Underperformance

Projected Relative QE Favors UST Underperformance

Projected Relative QE Favors UST Underperformance

The combination of the Fed’s lingering dovish policy bias and the improving global growth backdrop should keep the US dollar under cyclical downward pressure. The weaker greenback means that non-US central banks must try to maintain an even more dovish bias than the Fed to limit the upward pressure on their own currencies. A desire to fight unwanted currency appreciation via a more rapid pace of QE relative to the Fed – at a time when US Treasury yields are likely to remain under upward pressure from rising inflation expectations – should support a narrowing of non-US vs US bond spreads over the next 6-12 months (Chart 10). Bottom Line: The underlying reflationary themes that drove global bond yields higher over the past several months remain intact, even with uncertainty over COVID-19 vaccine distribution and mixed messages on future central bank policy moves. Stay below-benchmark on overall global duration exposure, overweighting non-US government bond markets versus US Treasuries, while also favoring global inflation-linked debt over nominal bonds. A New Cross-Country Spread Trade: Long Australian Government Bonds Vs. US Treasuries In last week’s Special Report on Australia, which we co-authored jointly with BCA Research Foreign Exchange Strategy, we concluded that a neutral exposure to Australian government debt within global bond portfolios was still warranted.2 Uncertainty over the Reserve Bank of Australia (RBA) reaction function and the future path of Australia’s yield beta, which measures the sensitivity of Australian yields to global yields and remains elevated, justified a neutral stance. We do, however, have a higher conviction view that Australian government debt will outperform US Treasuries – especially given our expectation that US yields have more cyclical upside – given that the yield beta of the former to the latter has declined (Chart 11). Chart 11Australian Government Bonds Are "Defensive" When US Yields Are Rising

Australian Government Bonds Are "Defensive" When US Yields Are Rising

Australian Government Bonds Are "Defensive" When US Yields Are Rising

This week, we translate that view into a new tactical trade—going long 10-year Australian government bonds versus shorting 10-year US Treasuries. This trade will be implemented through bond futures (details of the trade can be seen in our trade table on page 15). In addition to the yield beta argument, the Australia-US 10-year spread looks attractive on a fair value basis. Chart 12 presents our new Australia-US 10-year spread valuation model, based on fundamental factors such as relative policy interest rates, inflation and unemployment. The model also accounts for the impact from the massive bond buying by the Fed and Reserve Bank of Australia (RBA); we include as an independent variable the relative central bank balance sheets as a share of respective nominal GDP. Although the Australia-US spread has converged somewhat towards fair value since the blow out in March 2020, it is still at attractive levels at 13bps or 0.8 standard deviations above fair value. The model-implied fair value of the Australia-US spread could also fall further, thereby creating a lower anchor point for spreads to gravitate towards. While the policy rate differential will likely remain unchanged until 2023, other factors will move to drag down the spread fair value (Chart 13). The gap in relative headline inflation should, much to the RBA’s chagrin, move further into negative territory given the relatively weaker domestic and foreign price pressures in Australia. On the QE front, the RBA also has much more room to expand its balance sheet relative to developed market peers, and will feel pressured to do so if the Australian dollar continues to rally. Finally, the RBA expects a much slower recovery in Australian unemployment than the Fed does for the US. This should further push down fair value if the central bank forecasts play out as expected. Chart 12The Australia-US 10-Year Spread Is Undervalued

The Australia-US 10-Year Spread Is Undervalued

The Australia-US 10-Year Spread Is Undervalued

Technical considerations also seem to be in favor of our trade (Chart 14). While the deviation of the Australia-US 10-year spread from its 200-day moving average, and its 26-week change, are both slightly negative, the 2008 period is instructive. Chart 13Relative Fundamentals Point Towards A Lower Australia-US Spread

Relative Fundamentals Point Towards A Lower Australia-US Spread

Relative Fundamentals Point Towards A Lower Australia-US Spread

Chart 14Technicals Favor Further Reduction In The Australia-US Spread

Technicals Favor Further Reduction In The Australia-US Spread

Technicals Favor Further Reduction In The Australia-US Spread

For both measures, after blowing up to around the +75-150bps zone, they likewise fell by a commensurate amount, attributable to a strong “base effect”. A similar dynamic should play out now after the dramatic 2020 spike in spread momentum. Meanwhile, duration positioning in the US, while it is short on net, is still far from levels where it has troughed. Lastly and most importantly, forward curves are pricing in an Australia-US spread close to zero, which provides us a golden opportunity to “beat the forwards” as the spread tightens without incurring negative carry. As a reference, we are initiating this trade with the cash 10-year Australia-US bond spread at 4bps, with a target range of -30bps to -80bps over the usual 0-6 month horizon that we maintain for our Tactical Overlay positions. Bottom Line: We seek to capitalize on our view that Australian yields will be slower to rise relative to US yields by introducing a new spread trade: buy Australian government bond 10-year futures and sell US 10-year Treasury futures. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Shakti Sharma Research Associate ShaktiS@bcaresearch.com Footnotes 1https://www.bloombergquint.com/markets/record-number-of-fund-managers-overweight-on-emerging-markets-says-bofa-survey 2 Please see BCA Research Global Fixed Income Strategy Special Report, "Australia: Regime Change For Bond Yields & The Currency?", dated January 20, 2021, available at gfis.bcaresearch.com. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

A Pause, Not A Peak, In Global Bond Yields

A Pause, Not A Peak, In Global Bond Yields

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

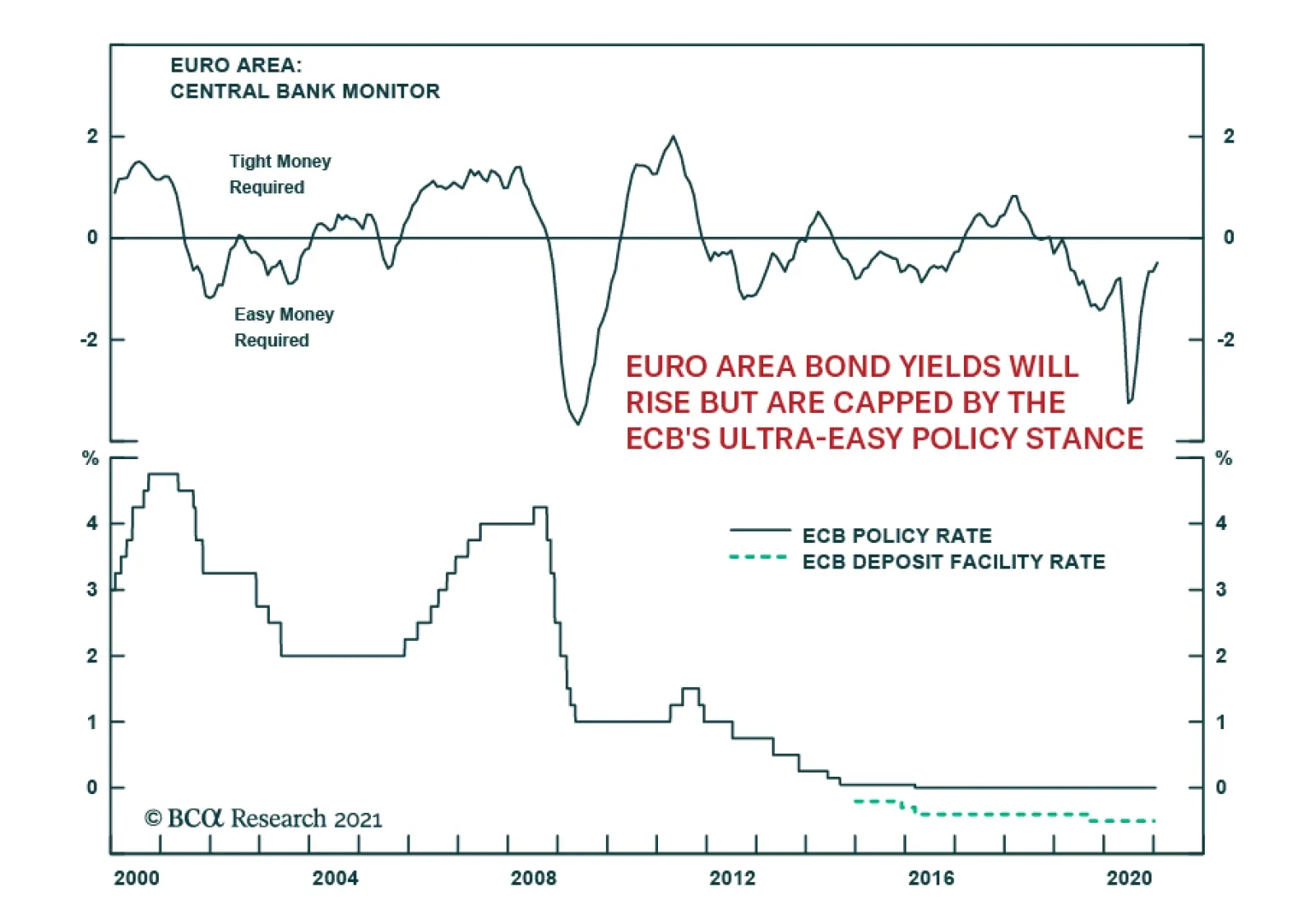

As expected, the European Central Bank did not make any changes to its policy at its first monetary policy meeting of the year yesterday. The benchmark deposit rate was maintained at -0.5% and the quota for bond purchases under the Pandemic Emergency Purchase…

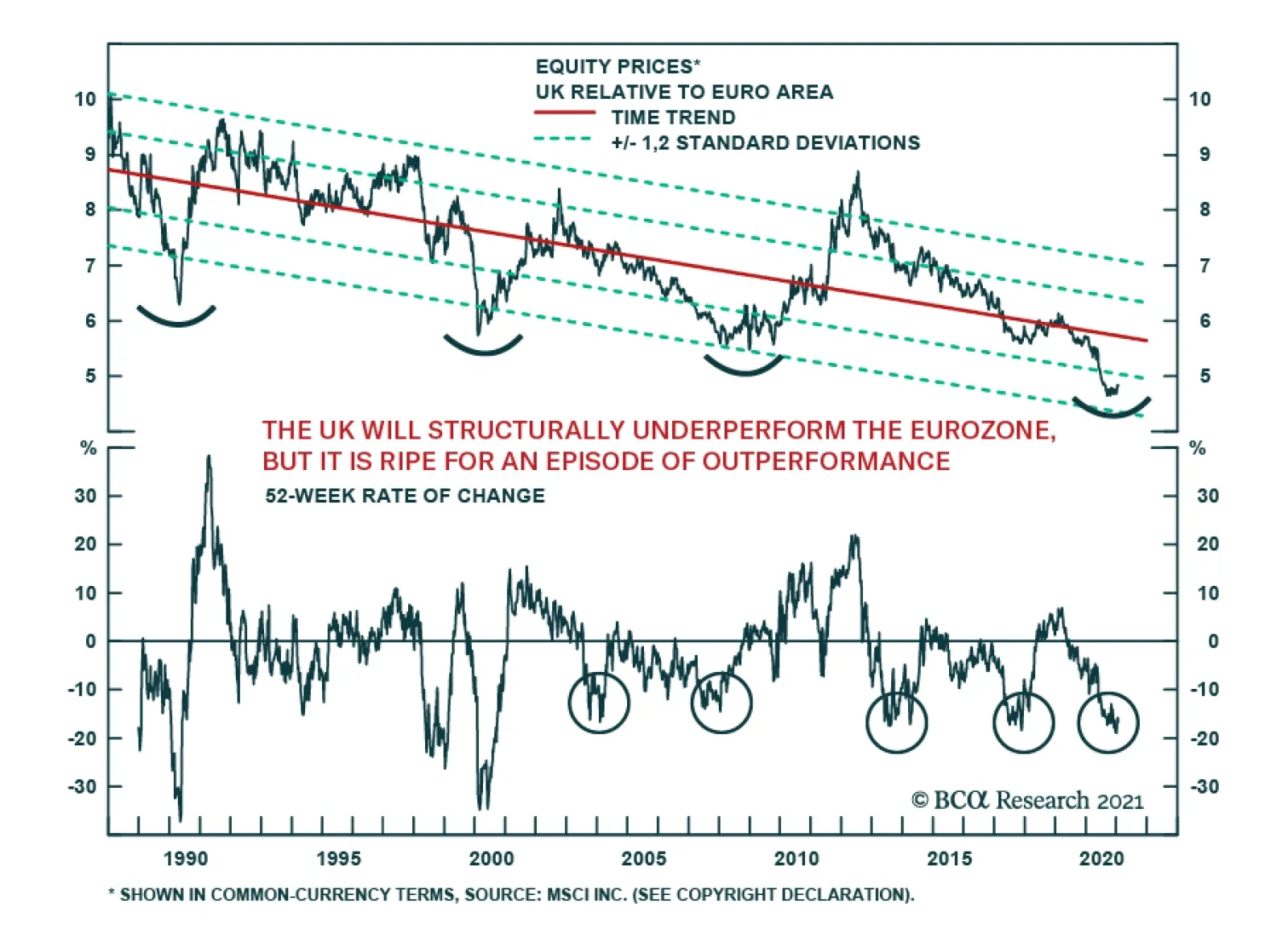

While it is well known that UK equities have been in a secular downtrend against the US, it is often less appreciated that they have greatly underperformed euro area stocks for the past 32 years. There is little reason to believe that the secular…

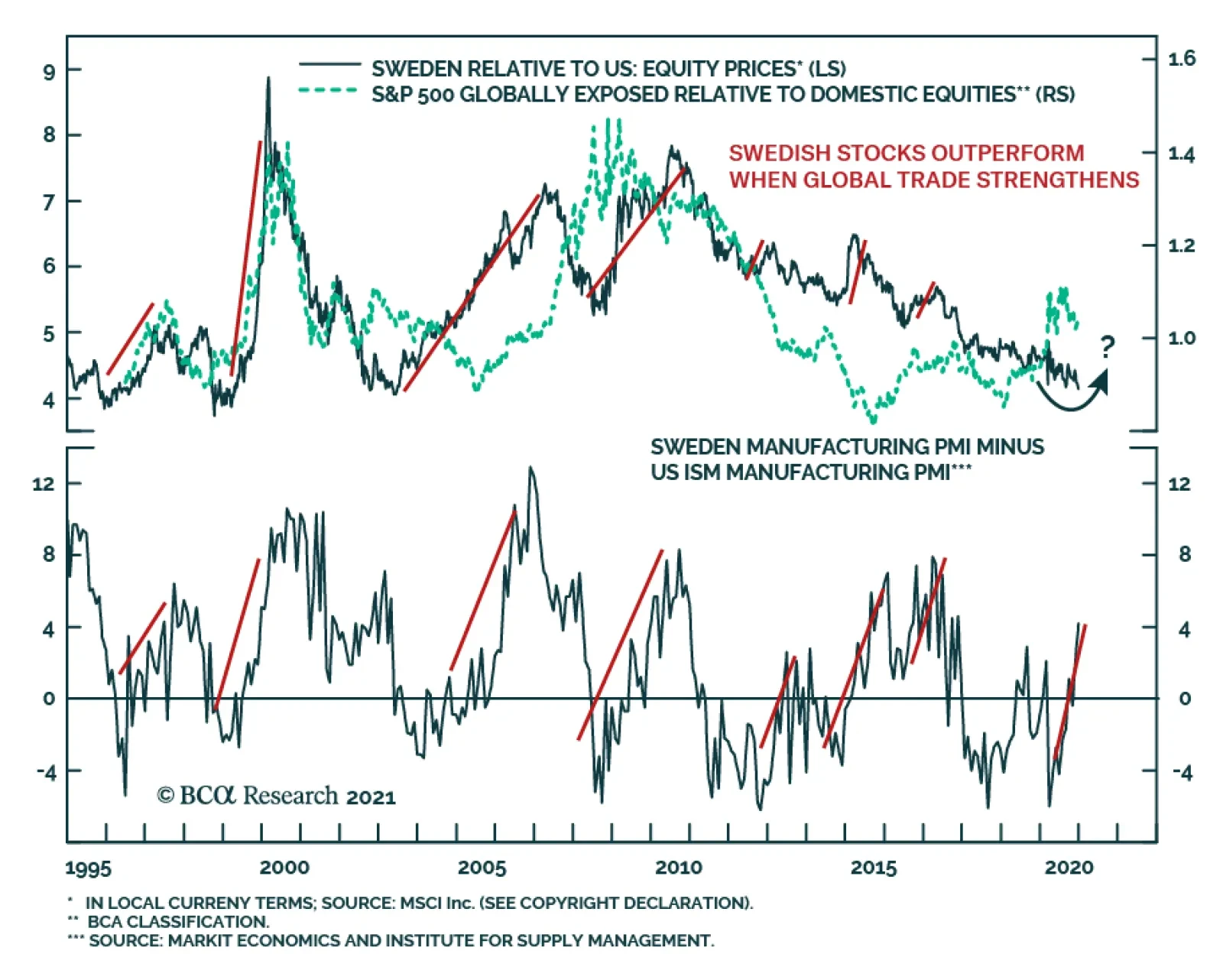

Over the coming 12 to 18 months, investors should overweight Swedish equities relative to US ones. Swedish equities overweight value stocks and cyclical sectors. This characteristic means that an acceleration in global economic activity, particularly…

Highlights In the wake of COVID-19, the low-probability, high-impact “Black Swan” event is as relevant as ever. Investors should already expect US terrorist incidents, a fourth Taiwan Strait crisis, and crises involving Turkey – these are no longer black swans. What if Russia had a color revolution, Japan confronted China, or Saudi Arabia collapsed? What if the US and China brokered a North Korean deal? Or a major terrorist attack caused government change in Germany? Ultimately this exercise illustrates what the market is not prepared for – a new rally in the US dollar – though some scenarios would fuel the rise of the euro and renminbi. Feature The COVID-19 pandemic reminded us all of the power of the “Black Swan” – the random, unpredictable event with massive ramifications. As historian Niall Ferguson pointed out at the BCA Conference last fall, COVID-19 was not really a black swan, as epidemiologists had predicted that a pandemic would occur and the world was not ready. Astrophysicist Martin Rees made a bet with psychologist and linguist Steven Pinker that “bioterror or bioerror will lead to one million casualties in a single event within a six month period starting no later than 31 December 2020.”1 Tellingly, countries neighboring China were the best prepared for the outbreak, having dealt with SARS and bird flu. COVID accelerated major trends building up throughout the past decade – notably the shift toward pro-active fiscal policy, which had been gaining traction in policy circles ever since the austerity debates of the early 2010s. In that sense forecasting is still necessary. If solid trends can be identified, then random shocks may simply reinforce them (Chart 1). Chart 1US Fiscal Stimulus About To Get Even Bigger

Five Black Swans For 2021

Five Black Swans For 2021

In this year’s “Five Black Swans” report, we focus on geopolitical risks that are highly unlikely, not at all being discussed, and yet would have a major impact on financial markets. Domestic terrorist events in the United States in 2021 would not qualify as a black swan by this definition. A crisis in the Taiwan Strait, which we have warned about for several years, is now widely (and rightly) expected. Black Swan #1: A Color Revolution In Russia Russia is one of the losers of the US election. Not because Trump was a Russian agent – the Trump administration ended up authorizing a fairly hawkish posture toward Russia in eastern Europe – but rather because the Democratic Party threatens Russia with a strengthening of the trans-Atlantic alliance and a recovery of liberal democratic ideology. Geopolitical risk surrounding Russia is therefore elevated, as we argued last year. Both President Vladimir Putin and his government have seen their approval rating drop, a development that has often led Russia to lash out abroad (Chart 2). But our expectation of rising political risk within Russia’s sphere has been reinforced by Russia’s alleged poisoning of opposition politician Alexei Navalny and the eruption of pro-democracy protests in Belarus. Vladimir Putin is increasingly focusing on home affairs due to domestic instability worsened by the pandemic and recession. Fiscal and monetary austerity have weighed on the public. The largest protests since 2011 occurred in mid-2019 in opposition to the fixing of the Moscow municipal elections. This could be a harbinger of larger unrest around the Russian legislative elections on September 19, 2021. Nominal wage growth has collapsed and is scraping its 2015-16 lows (Chart 3). Chart 2Black Swan #1: A Color Revolution In Russia

Black Swan #1: A Color Revolution In Russia

Black Swan #1: A Color Revolution In Russia

Chart 3Russia's Fiscal Austerity

Russia's Fiscal Austerity

Russia's Fiscal Austerity

Meanwhile US policy toward Russia will become more confrontational. New US presidents always start with outreach to Russia, but the Democratic Party blames Russia for betraying the good faith of the Obama administration’s “diplomatic reset” from 2009-11. Russia invaded Ukraine and took Crimea in exchange for cooperating on the 2015 Iran nuclear deal. Adding in the Snowden affair, the 2016 election interference, and now the monumental SolarWinds cyberattack, the Democratic Party will want to strike back and reestablish deterrence against Russia’s asymmetrical warfare. While Biden will seek to negotiate an extension of the New START missile treaty from February 5, 2021 until 2026, he will gear up for confrontation in other areas. The US could seek to go on offense with Russia’s wonted tools: psychological warfare and cyberattacks. The Americans are not willing or able to attempt regime change in Moscow. That would be taken as an act of war among nuclear powers. But if Russia is less stable internally than it appears, then US meddling could hit a weak spot and set off a chain reaction. Even if the US is incapable of anything of the sort, Russia is still ripe for social unrest. Should the authorities mishandle it, it could metastasize. Russia has a long tradition of peasant uprisings – a descent into anarchy is not out of the question. The regime would not be devoting so much attention to suppressing domestic dissent if the conditions for it were not ripe.2 Putin’s constitutional reforms in mid-2020, which could extend his term until 2036, also speak to concerns about regime stability. A successful Russian uprising would threaten to raise serious instability in Europe and the world. When great but decadent empires are destabilized, political struggle can intensify rapidly and spill out to affect the neighbors. Bottom Line: Russian domestic political instability could produce a black swan. The ruble would tank and the US dollar would catch a bid against European currencies. Black Swan #2: A Major Terror Attack In Germany 2020 was a banner year for European solidarity. Brexit went forward but none of the European states have followed – nor would any want to follow given the political turmoil it aroused. Brussels initiated a recovery fund to combat the global pandemic that consisted of a mutual debt scheme – in what has been hailed somewhat excessively as a “Hamiltonian moment,” a move toward federalism. Germany stood at the center of this process. After opening the doors to a flood of migrants from Syria in 2015, Chancellor Angela Merkel suffered a blow to her popularity and was eventually forced to make plans for her exit. But she stuck to her core liberal policies and her fortunes have recovered (Chart 4). She is stepping down in 2021 as the longest-serving chancellor since Helmut Kohl and an influential European stateswoman. The EU member states are more integrated than ever while Germany has taken another step toward improving its international image. The public has rewarded the ruling coalition for its relatively competent handling of the global pandemic (Chart 5). Chart 4Black Swan #2: A Major Terror Attack In Germany

Black Swan #2: A Major Terror Attack In Germany

Black Swan #2: A Major Terror Attack In Germany

Chart 5German People Happy With Their Government

Five Black Swans For 2021

Five Black Swans For 2021

Merkel’s approval coincides with a recovery of the liberal democratic consensus in Europe after a series of challenges from anti-establishment and populist parties. Only in Italy did populists take power, and they were forced to back down from their extravagant fiscal policy demands while modifying their policy platform with regard to membership in the monetary union. Even today, as Italy’s ruling coalition comes apart at the seams, the risk of a populist backlash is lower than it was in most of the past decade. One of the main ways the European establishment neutralized the populist challenge was by tightening control over immigration and cracking down on terrorism (Charts 6 and 7). These two forces have played a large role in generating support for right wing parties, and these parties have declined in popularity as these two forces have abated. Chart 6Terrorist Attacks Have Fallen In Europe

Terrorist Attacks Have Fallen In Europe

Terrorist Attacks Have Fallen In Europe

Chart 7Europeans Softening Toward Immigrants?

Europeans Softening Toward Immigrants?

Europeans Softening Toward Immigrants?

Still, the risk posed by terrorist groups has not disappeared – and it is always possible that disaffected individuals could evade detection. French President Emmanuel Macron faced seven terrorist attacks over the past year, which partly stemmed over the commemoration of the Charlie Hebdo massacre but also points to the persistence of underground extremist networks (Chart 8).3 Chart 8French Fear Of Terrorism Has Increased

Five Black Swans For 2021

Five Black Swans For 2021

Chart 9European Breakup Risk At Testing Point

European Breakup Risk At Testing Point

European Breakup Risk At Testing Point

What would happen if a major attack occurred in Germany in 2021? Would it upset the country’s liberal consensus and fuel another surge in popular support for far-right parties like the Alternative for Germany? Only a major attack would have a lasting impact. A systemically important attack in the pivotal year of Merkel’s retirement could create more uncertainty in domestic German politics than has been seen since the 1990s and early 2000s. It is possible that an attack could strengthen the ruling coalition and the public’s desire to continue with the leadership of the Christian Democrats after Merkel. More likely, however, it would divide the conservative and right-wing parties among themselves. Merkel’s chosen successor, Defense Minister Annagret Kramp-Karrenbauer, was forced to abandon her bid for the chancellorship last year after members of her Christian Democratic Union in the state of Thuringia voted along with the anti-establishment Alternative for Germany to remove the state’s left-wing leader. The cooperation was minimal but it set off a firestorm by suggesting that Kramp-Karrenbauer was willing to work together with the far right.4 She bowed out and now the party is about to pick a new leader. The point is that if any event strengthens the far right, it would suck away votes from the Christian Democrats. The latter could also see divisions emerge with their Bavarian sister party, the Christian Social Union, which has differed on immigration in the past. Or the conservatives could alienate the median German voter by tacking too far to the right to preempt the anti-establishment vote (e.g. overreacting to the attack). Either way, German politics would be rocked. Ironically, if the coalition was seen as mishandling the response, a left-wing coalition of the Greens and the Social Democrats could be the beneficiaries. The risk of a government change – in the wake of Merkel and the pandemic – is greatly underrated, entirely aside from black swans. Nevertheless a major shock that strengthens the far right would be a black swan by forcing the question of whether the center-right is willing to cooperate with its fringe. If that occurred, then Europe would be stunned. If it did not, then the conservatives could lose the election and plunge into intra-party turmoil. The takeaway of a rightward shift on the back of any shock would be a renewed risk of fiscal hawkishness – a partial relapse from the past two years’ fiscal expansion to the more traditionally austere German posture. The takeaway of a leftward shift would be the opposite – a doubling down on that fiscal expansion. German hawkishness would increase the European breakup risk premium, while a confirmation of the new German dovishness would further suppress it (Chart 9). Bottom Line: The fiscal dovish turn is the more likely response to such a black swan in today’s climate, but a major terrorist attack could have unpredictable consequences. Black Swan #3: A US-China Deal On North Korea Critics misunderstood President Trump’s policy on North Korea. Trump’s policy – even his belligerent rhetoric – echoed that of Bill Clinton in the 1990s. The intention of the US show of force was to create an overwhelming threat that would force Pyongyang into serious negotiations toward a nuclear deal. That in turn would pave the way to economic cooperation. Trump’s efforts failed – Kim Jong Un stonewalled him in the final year and a half. Kim’s bet paid off since he avoided making major concessions and now Biden must start from scratch. Pyongyang has ramped up its threats and Kim has elevated his sister, Kim Yo Jong, to a higher standing in the party – apparently to lob attacks at South Korea full-time. Biden will put the technocrats and Korea experts in charge. Pyongyang may test nuclear weapons or launch intercontinental ballistic missiles to attract Biden’s attention. But Kim could also go straight to negotiations. Optimistically, a few years of talks could result in a phased reduction of sanctions in exchange for nuclear inspections. Kim has the incentive and the dictatorial powers to open up the economy and engage in market reforms while managing any backlash among the army. He has already prepared the ground by elevating economic policy to the level of military policy in the national program. For years he has allowed some market activity to little effect. The North must have suffered from the pandemic, as Kim publicly confessed to the failure of economic management at the latest party meeting. His country needs a vaccine for COVID. And if he intends to go the way of Vietnam, then he needs to open up the doors while a new global business cycle is beginning (Chart 10). The black swan would emerge if the Biden administration’s attempt to reboot relations with China produced a unified effort to force a resolution onto Kim. It is undeniable that Trump broke diplomatic ice by meeting with Kim directly, giving Biden the option of doing so quickly and with minimal controversy if he should so desire. Most importantly, China has enforced sanctions, if official statistics can be trusted (Chart 11). Beijing made no secret that it saw North Korea as an area of compromise to appease US anger. After all, success on the peninsula would remove the reason for the US to keep troops there. Chart 10Black Swan #3: A US-China Deal On North Korea

Five Black Swans For 2021

Five Black Swans For 2021

Chart 11An Area Of US-China Cooperation Under Biden?

An Area Of US-China Cooperation Under Biden?

An Area Of US-China Cooperation Under Biden?

The last point is the material point. If the North sought to open up, it would likely have to do so through talks with the US, China, South Korea, and Japan. Success would mean that US-China engagement is still effective. Bottom Line: A breakthrough on the Korean peninsula would mean that investors could begin imagining a future in which the US and China are not “destined for war” but rather capable of reviving their old cooperative approach. This has far-reaching positive implications, but most concretely the Korean won and Chinese renminbi would rally against the US dollar and Japanese yen on the historic reduction of war risk. Black Swan #4: Saudi Arabia (And Oil Prices) Collapse Saudi Arabia is an even greater loser from the US election than Russia. The Saudis came face to face with their geopolitical nightmare of US abandonment under the Obama administration, as the US gained energy independence while reaching out to Iran. The 2015 nuclear deal gave Iran a strategic boost and enabled it to resume pumping oil (Chart 12). The Saudis, like the Israelis, lobbied hard to stop the deal but failed. They threw their full support behind President Trump, who reciprocated, and now face the restoration of the Obama policy under Joe Biden. Chart 12Black Swan #4: Saudi Arabia (And Oil Prices) Collapse

Black Swan #4: Saudi Arabia (And Oil Prices) Collapse

Black Swan #4: Saudi Arabia (And Oil Prices) Collapse

Chart 13Fiscal Pressure On Saudis

Fiscal Pressure On Saudis

Fiscal Pressure On Saudis

Global investors should expect Biden to return to the nuclear deal with Iran as quickly as possible, notwithstanding Iran’s latest nuclear provocations, since the latter are designed to increase negotiating leverage. The Joint Comprehensive Plan of Action was an executive agreement that Biden could restore with the flick of his wrist, as long as Iranian President Hassan Rouhani returned to compliance. Rouhani can do so before a new president is inaugurated in August – he could secure his legacy at the cost of taking the blame for “dealing with the devil.” This would save the regime from further economic and social instability as it prepares for the all-important succession of the supreme leader in the coming years. A black swan would occur if this diplomatic situation led to a breakdown in support for Crown Prince Mohammed bin Salman (MBS). MBS, whose nickname is “reckless,” in part because his foreign policies have backfired, could attempt to derail or sabotage the US-Iran détente. If he tried and failed, the US could effectively abandon Saudi Arabia – energy self-sufficiency, public war-weariness, and Iranian détente would pave the way for the US to downgrade its commitment. This would create an existential risk for the kingdom, which depends on the US for national security. It could also be the final straw for MBS, who already faces opposition from elites who have been shoved aside and do not wish to see him ascend the throne in a few years’ time. A different trigger for the same black swan would be a collapse of the OPEC 2.0 oil cartel. The Saudis and Russians have fought two market-share wars over the past seven years. They could relapse into conflict in the face of shifting global dynamics, such as the green energy revolution, that disfavor oil. Arthur Budaghyan and Andrija Vesic, of BCA’s Emerging Markets Strategy, have argued that financial markets will start pricing in a higher probability of Saudi currency depreciation versus the US dollar in coming years. Lower-for-longer oil prices (say $40 per barrel average over next few years) would pose a dilemma to the authorities: either (1) cut fiscal spending further and tighten liquidity or (2) resort to local banks financing (money creation “out of thin air”) to sustain economic activity. The first scenario would impose severe fiscal austerity on the population (Chart 13), which is politically difficult to endure in the long run. The second scenario will lead to depleting the country’s FX reserves, robust money growth and some inflation culminating in downward pressure on the currency. The main reason for believing the devaluation will not happen is that it would topple the regime. Currency devaluation would result in unbearable inflation in a country that lacks domestic production and domestically sourced staples. But that is precisely why it is a black swan risk. After all, prolonged fiscal austerity may not be feasible either. Bottom Line: MBS controls the security forces and has consolidated power for years but that may not save him if his foreign policies led to American abandonment or a breakdown of the peg. Black Swan #5: A Sino-Japanese Crisis For the first time since 2016, we are not including US-China tensions over Taiwan in our list of black swans. A crisis in the strait is only a matter of time and the global news media is increasingly aware of it (Chart 14). It would not necessarily have to be a war or even a show of military force, though either are possible. A mere Chinese boycott or embargo of Taiwan would violate the US’s Taiwan Relations Act and trigger a US-China crisis from the get-go of the Biden administration. What is less widely recognized is that peaceful resolution of the China-Taiwan predicament is not just a concern for the United States. It is a concern for Japan and South Korea as well – whose vital supplies must travel around the island one way or another. These two nations would face constriction if mainland China reunified Taiwan by force – and therefore Beijing’s signals of increasing willingness to contemplate armed action are already reverberating among the neighbors. Japan sounded an uncharacteristically stark warning just last month. The hawkish statement from State Minister of Defense Yasuhide Nakayama is worth quoting at length: We are concerned China will expand its aggressive stance into areas other than Hong Kong. I think one of the next targets, or what everyone is worried about, is Taiwan … There’s a red line in Asia – China and Taiwan. How will Joe Biden in the White House react in any case if China crosses this red line? The United States is the leader of the democratic countries. I have a strong feeling to say: America, be strong!5 China and Japan have improved trade relations through the RCEP agreement, as Beijing looks to diversify from the United States. But China’s rise is of enormous strategic concern for Japanese policymakers. COVID-19 and the rollback of Hong Kong’s freedoms have made matters worse. The belt of sea and land around China – the “first island chain” – is the critical area from which Beijing seeks to expel American and foreign military presence. With China already having shown a willingness to clash with India and Australia simultaneously in 2020 – as it carves a sphere of influence in the absence of American pushback – it should be no surprise to see conflicts erupt in the East or South China Sea (Chart 15). Chart 14Differences In The Taiwan Strait

Differences In The Taiwan Strait

Differences In The Taiwan Strait

Chart 15Black Swan #5: A Sino-Japanese Crisis

Black Swan #5: A Sino-Japanese Crisis

Black Swan #5: A Sino-Japanese Crisis

In the aftermath of the last global crisis, in 2010, China and Japan clashed mightily over maritime-territorial disputes in the East China Sea. China imposed a brief embargo on exports of rare earth elements to Japan. The two clashed again the following year and tensions escalated dramatically when China rolled out an Air Defense Identification Zone (ADIZ) in 2013. Tense periods come and go and are often attended by mass anti-Japanese protests, as in 2005 and 2012. Usually these events are of passing importance, though they have the potential to escalate. What would truly be a black swan would be if Japan took the initiative to challenge China and test the Biden administration’s commitment to Japanese security. With the US internally divided and distracted, and China ascendant, Japan could grow increasingly insecure and seek to take precautions. China could see these as offensive. A new Sino-Japanese crisis could ensue that would catch investors by surprise. It is highly unlikely that Tokyo would provoke China – hence the black swan designation – but the effective absence of the Americans is a strategic liability that Tokyo may wish to resolve sooner rather than later. In this case the market reaction would be predictable – the yen would appreciate while the renminbi and Taiwanese dollar would fall. The risk-off period could be extended if the US failed to reinforce the Japanese alliance for fear of China, with the whole world watching. Bottom Line: Global investors would be blindsided if a sudden explosion of Sino-Japanese tensions prevented any US-China thaw and confirmed their worst fears about China’s economic decoupling from the West. Investment Takeaways This exercise in identifying black swans may be useful in at least one way: it exposes the vulnerability of financial markets to a sudden reversal of the US dollar’s weakening trend (Chart 16). The dollar would surge on broad Russian instability, Sino-Japanese conflict, or another exogenous geopolitical shock. This kind of dollar surprise would be much greater than a temporary counter-trend bounce, which our Foreign Exchange Strategist Chester Ntonifor fully expects. It would upset the financial community’s dollar-bearish consensus, with far-reaching ramifications for the global economy and financial markets. A rising dollar against the backdrop of a recovering global economy represents a de facto tightening of global financial conditions. Equity markets, for example, have only started to rotate away from the US and this trend would be reversed (Chart 17). Whereas further appreciation of the euro and the renminbi is not only expected but would support global reflation. Chart 16The USD Over Trump's Four Years

The USD Over Trump's Four Years

The USD Over Trump's Four Years

Chart 17Global Market Cap Over Trump's Four Years

Global Market Cap Over Trump's Four Years

Global Market Cap Over Trump's Four Years

There is a much plainer and straighter way to an upset of the dollar-bearish consensus. Rather than a black swan it is a “gray rhino,” the term that Michele Wucker uses for risks that are common, expected, and staring you right in the face.6 This would be the peak of China’s stimulus, which holds out the risk of a major reversal to the pro-cyclical global financial market rally in late 2021 (Chart 18). Chart 18China Impulse Will Linger In 2021, But EM Stocks Tactically Stretched

China Impulse Will Linger In 2021, But EM Stocks Tactically Stretched

China Impulse Will Linger In 2021, But EM Stocks Tactically Stretched

It would be a colossal error if Beijing over-tightened monetary and fiscal policy in 2021 in the context of high debt, deflation, and unemployment (Chart 19). Chart 19Three Reasons China Will Avoid Over-Tightening (If It Can)

Three Reasons China Will Avoid Over-Tightening (If It Can)

Three Reasons China Will Avoid Over-Tightening (If It Can)

Nevertheless the government’s renewed efforts to contain asset bubbles and credit excesses clearly increase the risk. Financial policy tightening is always a risky endeavor, as global policymakers routinely discover. Chart 20Book Profits But Stay Cyclically Positive On Reflation Trades

Book Profits But Stay Cyclically Positive On Reflation Trades

Book Profits But Stay Cyclically Positive On Reflation Trades

We maintain that China’s major stimulus will have a lingering positive effects for the economy for most of this year and that the authorities will relax policy and regulation as needed to secure the recovery. The Central Economic Work Conference in December suggested that the Politburo still views downside economic risks as the most important. But this is a clear and present risk that will have to be monitored closely. Clearly the global reflation trend has extended to dangerous technical extremes over the past month on the realization that US fiscal stimulus will surprise to the upside. Therefore we are doing some housekeeping. We will book 31.1% profit on long cyber security, 16.7% on long US infrastructure, and 24.3% on long US materials. We will also book 9.5% gains on our long EM-ex-China equity trade, which has gone vertical (Chart 20). Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1 Such epidemiologists include Michael Osterholm and Lawrence Brilliant. For Pinker and Rees, see George Eaton, "Steven Pinker interview: How does a liberal optimist handle a pandemic?" The New Statesman, July 22, 2020, newstatesman.com. 2 Thomas Grove, "New Russian Security Force Will Answer To Vladimir Putin," Wall Street Journal, April 24, 2016, wsj.com. 3 Elaine Ganley, "Grisly beheading of teacher in terror attack rattles France," Associated Press, October 16, 2020, apnews.com. 4 Philip Oltermann, "German politician elected with help from far right to step down," The Guardian, February 6, 2020, theguardian.com. 5 Ju-min Park, "Japan official, calling Taiwan ‘red line,’ urges Biden to ‘be strong,’" Reuters, December 25, 2020, reuters.com. 6 See www.wucker.com.

Yesterday, Matteo Renzi pulled out of the center-left coalition currently governing Italy. The former PM believes he can improve his party’s standing in parliament. The Conte government will try to create a new coalition, but this will be challenging…

Highlights Markets largely ignored the uproar at the US Capitol on January 6 because the transfer of power was not in question. Democratic control over the Senate, after two upsets in the Georgia runoff, is the bigger signal. US fiscal policy will become more expansive yet the Federal Reserve will not start hiking rates anytime soon. This is a powerful tailwind for risk assets over the short and medium run. Politics and geopolitics affect markets through the policy setting, rather than through discrete events, which tend to have fleeting market impacts. The current setting, in the US and abroad, is negative for the US dollar. The implication is positive for emerging market stocks and value plays. Go long global stocks ex-US, long emerging markets over developed markets, and long value over growth. Cut losses on short CNY-USD. Feature Chart 1Market's Muted Response To US Turmoil

Market's Muted Response To US Turmoil

Market's Muted Response To US Turmoil

Scenes of mayhem unfolded in the US Capitol on January 6 as protesters and rioters flooded the building and temporarily interrupted the joint session of Congress convened to count the Electoral College votes. Congress reconvened later and finished the tally. President-elect Joe Biden will take office at noon on January 20. Financial markets were unperturbed, with stocks up and volatility down, though safe havens did perk up a bit (Chart 1). The incident supports our thesis that the US election cycle of 2020 was a sort of “Civil War Lite” and that the country is witnessing “Peak Polarization,” with polarization likely to fall over the coming five years. The incident was the culmination of the past year of pandemic-fueled unrest and President Trump’s refusal to concede to the Electoral College verdict. Trump made a show of force by rallying his supporters, and apparently refrained from cracking down on those that overran Congress, but then he backed down and promised an orderly transfer of power. The immediate political result was to isolate him. Fewer Republicans than expected contested the electoral votes in the ensuing joint session; one Republican is openly calling for Trump to be forced into resignation via the 25th amendment procedure for those unfit to serve. The electoral votes were promptly certified. Vice President Mike Pence and other actors performed their constitutional duties. Pence reportedly gave the order to bring out the National Guard to restore order – hence it is possible that Pence and Trump’s cabinet could activate the 25th amendment, but that is unlikely unless Trump foments rebellion going forward. Vandals and criminals will be prosecuted and there could also be legal ramifications for Trump and some government officials. Do Politics And Geopolitics Affect Markets? The market’s lack of concern raises the question of whether investors need trouble themselves with politics at all. Philosopher and market guru Nassim Nicholas Taleb tweeted the following: If someone, a year ago, described January 6, 2021 (and events attending it) & asked you to guess the stock market behavior, admit you would have gotten it wrong. Just so you understand that news do not help you understand markets.1 This is a valid point. Investors should not (and do not) invest based on the daily news. Of course, many observers foresaw social unrest surrounding the 2020 election, including Professor Peter Turchin.2 Social instability was rising in the data, as we have long shown. When you combined this likelihood with the Fed’s pause on rate hikes, and a measurable rise in geopolitical tensions between the US and other countries, the implication was that gold would appreciate. So if someone had told you a year ago that the US would have a pandemic, that governments would unleash a 10.2% of global GDP fiscal stimulus, that the Fed would start average inflation targeting, that a vaccine would be produced, and that the US would have a contested election on top of it all, would you have expected gold to rise? Absolutely – and it has done so, both in keeping with the fall in real interest rates plus some safe-haven bonus, which is observable (Chart 2). Chart 2Gold Price In Excess Of Fall In Real Rates Implies Geopolitical Risk

Gold Price In Excess Of Fall In Real Rates Implies Geopolitical Risk

Gold Price In Excess Of Fall In Real Rates Implies Geopolitical Risk

The takeaway is that policy matters for markets while politics may only matter briefly at best. Which brings us back to the implications of the Trump rebellion. What Will Be The Impact Of The Trump Rebellion? We have highlighted that this election was a controversial rather than contested election – meaning that the outcome was not in question after late November when the court cases, vote counts, and recounts were certified. This was doubly true after the Electoral College voted on December 14. The protests and riots yesterday never seriously called this result into question. Whatever Trump’s intentions, there was no military coup or imposition of martial law, as some observers feared. In fact the scandal arose from the President’s hesitation to call out the National Guard rather than his use of security forces to prevent the transfer of power, as occurs during a coup. This partially explains why the market traded on the contested election in December 2000 but not in 2020 – the result was largely settled. The Biden administration now has more political capital than otherwise, which is market-positive because it implies more proactive fiscal policy to support the economic recovery. Trump’s refusal to concede gave Democrats both seats in the Georgia Senate runoffs, yielding control of Congress. Household and business sentiment will revive with the vaccine distribution and economic recovery, while the passage of larger fiscal stimulus is highly probable. US fiscal policy will almost certainly avoid the mistake of tightening fiscal policy too soon. Taken with the Fed’s aversion to raising rates, greater fiscal stimulus will create a powerful tailwind for risk assets over the next 12 months. The primary consequence of combined fiscal and monetary dovishness is a falling dollar. The greenback is a counter-cyclical and momentum-driven currency that broadly responds inversely to global growth trends. But policy decisions are clearly legible in the global growth path and the dollar’s path over the past two decades. Japanese and European QE, Chinese devaluation, the global oil crash, Trump’s tax cuts, the US-China trade war, and COVID-19 lockdowns all drove the dollar to fresh highs – all policy decisions (Chart 3). Policy decisions also ensured the euro’s survival, marking the dollar’s bottom against the euro in 2011, and ensuring that the euro could take over from the dollar once the dollar became overbought. Today, the US’s stimulus response to COVID-19 – combined with the Fed’s strategic review and the Democratic sweep of government – marked the peak and continued drop-off in the dollar. Chart 3Euro Survival, US Peak Polarization, Set Stage For Rotation From USD To EUR

Euro Survival, US Peak Polarization, Set Stage For Rotation From USD To EUR

Euro Survival, US Peak Polarization, Set Stage For Rotation From USD To EUR

Chart 4China's Yuan Says Geopolitics Matters

China's Yuan Says Geopolitics Matters

China's Yuan Says Geopolitics Matters

The Chinese renminbi is heavily manipulated by the People’s Bank and is not freely exchangeable. The massive stimulus cycle that began in 2015, in reaction to financial turmoil, combined with the central bank’s decision to defend the currency marked a bottom in the yuan’s path. China’s draconian response to the pandemic this year, and massive stimulus, made China the only major country to contribute positively to global growth in 2020 and ensured a surge in the currency. The combination of US and Chinese policy decisions has clearly favored the renminbi more than would be the case from the general economic backdrop (Chart 4). Getting the policy setting right is necessary for investors. This is true even though discrete political events – including major political and geopolitical crises – have fleeting impacts on markets. What About Biden’s Trade Policy? Trump was never going to control monetary or fiscal policy – that was up to the Fed and Congress. His impact lay mostly in trade and foreign policy. Specifically his defeat reduces the risk of sweeping unilateral tariffs. It makes sense that global economic policy uncertainty has plummeted, especially relative to the United States (Chart 5). If US policy facilitates a global economic and trade recovery, then it also makes sense that global equities would rise faster than American equities, which benefited from the previous period of a strong dollar and erratic or aggressive US fiscal and trade policy. Trump’s last 14 days could see a few executive orders that rattle stocks. There is a very near-term downside risk to European and especially Chinese stocks from punitive measures, or to Emirati stocks in the event of another military exchange with Iran (Chart 6). But Trump will be disobeyed if he orders any highly disruptive actions, especially if they contravene national interests. Beyond Trump’s term we are constructive on all these bourses, though we expect politics and geopolitics to remain a headwind for Chinese equities. Chart 5Big Drop In Global Policy Uncertainty

Big Drop In Global Policy Uncertainty

Big Drop In Global Policy Uncertainty

US tensions with China will escalate again soon – and in a way that negatively impacts US and Chinese companies exposed to each other. Chart 6Geopolitical Implications Of Biden's Election

Geopolitical Implications Of Biden's Election

Geopolitical Implications Of Biden's Election

The cold war between these two is an unavoidable geopolitical trend as China threatens to surpass the US in economic size and improves its technological prowess. Presidents Xi and Trump were merely catalysts. But there are two policy trends that will override this rivalry for at least the first half of the year. First, global trade is recovering– as shown here by the Shanghai freight index and South Korean exports and equity prices (Chart 7). The global recovery will boost Korean stocks but geopolitical tensions will continue to brood over more expensive Taiwanese stocks due to the US-China conflict. This has motivated our longstanding long Korea / short Taiwan recommendation. Chart 7Global Economy Speaks Louder Than North Korea

Global Economy Speaks Louder Than North Korea

Global Economy Speaks Louder Than North Korea

Chart 8China Wary Of Over-Tightening Policy

China Wary Of Over-Tightening Policy

China Wary Of Over-Tightening Policy

Chart 9Global Stock-Bond Ratio Registers Good News

Global Stock-Bond Ratio Registers Good News

Global Stock-Bond Ratio Registers Good News

Second, China’s 2020 stimulus will have lingering effects and it is wary of over-tightening monetary and fiscal policy, lest it undo its domestic economic recovery. The tenor of China’s Central Economic Work Conference in December has reinforced this view. Chart 8 illustrates the expectations of our China Investment Strategy regarding China’s credit growth and local government bond issuance. They suggest that there will not be a sharp withdrawal of fiscal or quasi-fiscal support in 2021. Stability is especially important in the lead up to the critical leadership rotation in 2022.3 This policy backdrop will be positive for global/EM equities despite the political crackdown on General Secretary Xi Jinping’s opponents will occur despite this supportive policy backdrop. The global stock-to-bond ratio has surged in clear recognition of these positive policy trends (Chart 9). Government bonds were deeply overbought and it will take several years before central banks begin tightening policy. What About Biden’s Foreign Policy? Chart 10OPEC 2.0 Cartel Continues (For Now)

Accommodative US Monetary Policy, Tighter Commodity Markets Will Stoke Inflation OPEC 2.0 Cartel Continues (For Now)

Accommodative US Monetary Policy, Tighter Commodity Markets Will Stoke Inflation OPEC 2.0 Cartel Continues (For Now)

Iran poses a genuine geopolitical risk this year – first in the form of an oil supply risk, should conflict emerge in the Persian Gulf, Iraq, or elsewhere in the region. This would inject a risk premium into the oil price. Later the risk is the opposite as a deal with the Biden administration would create the prospect for Iran to attract foreign investment and begin pumping oil, while putting pressure on the OPEC 2.0 coalition to abandon its current, tentative, production discipline in pursuit of market share (Chart 10). Biden has the executive authority to restore the 2015 nuclear deal (Joint Comprehensive Plan of Action). He is in favor of doing so in order to (1) prevent the Middle East from generating a crisis that consumes his foreign policy; (2) execute an American grand strategy of reviving its Asia Pacific influence; (3) cement the Obama administration’s legacy. The Iranian President Hassan Rouhani also has a clear interest in returning to the deal before the country’s presidential election in June. This would salvage his legacy and support his “reformist” faction. The Supreme Leader also has a chance to pin the negative aspects of the deal on a lame duck president while benefiting from it economically as he prepares for his all-important succession. The problem is that extreme levels of distrust will require some brinkmanship early in Biden’s term. Iran is building up leverage ahead of negotiations, which will mean higher levels of uranium enrichment and demonstrating the range of its regional capabilities, including the Strait of Hormuz, and its ability to impose economic pain via oil prices. Biden will need to establish a credible threat if Iran misbehaves. Hence the geopolitical setting is positive for oil prices at the moment. Beyond Iran, there is a clear basis for policy uncertainty to decline for Europe and the UK while it remains elevated for China and Russia (Chart 11). Chart 11Relative Policy Uncertainty Favors Europe and UK Over Russia And China

Relative Policy Uncertainty Favors Europe and UK Over Russia And China

Relative Policy Uncertainty Favors Europe and UK Over Russia And China

The US international image has suffered from the Trump era and the Biden administration’s main priorities will lie in solidifying alliances and partnerships and stabilizing the US role in the world, rather than pursuing showdown and confrontation. However, it will not be long before scrutiny returns to the authoritarian states, which have been able to focus on domestic recovery and expanding their spheres of influence amid the US’s tumultuous election year. Chart 12GeoRisk Indicators Say Risks Underrated For These Bourses

GeoRisk Indicators Say Risks Underrated For These Bourses

GeoRisk Indicators Say Risks Underrated For These Bourses

The US will not seek a “diplomatic reset” with Russia, aside from renegotiating the New START treaty. The Democrats will seek to retaliate for Russia’s extensive cyberattack in 2021 as well as for election interference and psychological warfare in the United States. And while there probably will be a reset with China, it will be short-lived, as outlined above. This situation contrasts with that of the Atlantic sphere. The Biden administration is a crystal clear positive, relative to a second Trump term, for the European Union. The EU and the UK have just agreed to a trade deal, as expected, to conclude the Brexit process, which means that the US-UK “special relationship” will not be marred by disagreements over Ireland. European solidarity has also strengthened as a result of the pandemic, which highlighted the need for collective policy responses, including fiscal. Thus the geopolitical risks of the new administration are most relevant for China/Taiwan and Russia. Comparing our GeoRisk Indicators, which are market-based, with the relative equity performance of these bourses, Taiwanese stocks are the most vulnerable because markets are increasingly pricing the geopolitical risk yet the relative stock performance is toppy (Chart 12). The limited recovery in Russian equities is also at risk for the same reason. Only in China’s case has the market priced lower geopolitical risk, not least because of the positive change in US administration. We expect Biden and Xi Jinping to be friendly at first but for strategic distrust to reemerge by the second half of the year. This will be a rude awakening for Chinese stocks – or China-exposed US stocks, especially in the tech sector. Investment Takeaways Chart 13Global Policy Shifts Drive Big Investment Reversals

Global Policy Shifts Drive Big Investment Reversals

Global Policy Shifts Drive Big Investment Reversals

The US is politically divided. Civil unrest and aftershocks of the controversial election will persist but markets will ignore it unless it has a systemic impact. The policy consequence is a more proactive fiscal policy, resulting in virtual fiscal-monetary coordination that is positive both for global demand and risk assets, while negative for the US dollar. The Biden administration will succeed in partially repealing the Trump tax cuts, but the impact on corporate profit margins will be discounted fairly mechanically and quickly by market participants, while the impact on economic growth will be more than offset by huge new spending. Sentiment will improve after the pandemic – and Biden has not yet shown an inclination to take an anti-business tone. The past decade has been marked by a dollar bull market and the outperformance of developed markets over emerging markets and growth stocks like technology over value stocks like financials. Cyclical sectors have traded in a range. Going forward, a secular rise in geopolitical Great Power competition is likely to persist but the macro backdrop has shifted with the decline of the dollar. Cyclical sectors are now poised to outperform while a bottom is forming in value stocks and emerging markets (Chart 13). We recommend investors go strategically long emerging markets relative to developed. We are also going long global value over growth stocks. We are not yet ready to close our gold trade given that the two supports, populist fiscal turn and great power struggle, will continue to be priced by markets in the near term. We are throwing in the towel on our short CNY-USD trade after the latest upleg in the renminbi, though our view continues to be that geopolitical fundamentals will catch yuan investors by surprise when they reassert themselves. We also recommend preferring global equities to US equities, given the above-mentioned global trends plus looming tax hikes. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1 January 6, 2020, twitter.com. 2 See Turchin and Andrey Korotayev, "The 2010 Structural-Demographic Forecast for the 2010-2020 Decade: A Retrospective Assessment," PLoS ONE 15:8 (2020), journals.plos.org. 3 Not to mention that 2021 is the Communist Party’s 100th anniversary – not a time to make an unforced policy error with an already wobbly economy.

After bottoming in Q4, the German DAX is rallying and outperforming the Euro Stoxx 50 in the process. While the near-term is muddled by the pandemic’s resurgence, the global manufacturing recovery this year will ultimately benefit the German economy and…

The Swedish PMIs have been extraordinarily strong in December, jumping near 65, or levels normally associated with maximum output growth for the manufacturing sector. Historically, the momentum in the Swedish krona relative to the Swiss franc closely tracks…