Europe

Highlights Since 2004, Sweden’s private sector leverage trend can be explained using a simple Taylor rule approach. The approach clearly highlights three distinct monetary policy phases, and underscores the singular role of inflation (not systemic risk from rising indebtedness) as a driving factor for Riksbank policy. Since 2015, the Riksbank has maintained interest rates well below what a Taylor rule approach would suggest, owing to the desire to raise inflation expectations and Sweden’s high trade exposure to the euro area. This highlights strong similarities between the experience of Sweden and Canada: both countries are in the orbit of a major neighboring central bank, which has created serious distortions in both economies. Given the extent of the spread of the SARS-CoV-2 virus, especially in Europe, our assessment of the Riksbank’s reaction function suggests the odds appear to be high that the repo rate will move back into negative territory at some point this year (despite their reluctance to do so). Over the near-term, Swedish policy easing suggests that investors should avoid the krona versus both the US dollar and euro. Over a medium-term time horizon, one implication of a return to negative interest rates is that Swedish house price appreciation is likely to trend higher once the economic impact of the COVID-19 pandemic ends, potentially to the benefit of Swedish consumer durable and apparel stocks. Finally, over the long-term, Sweden is very likely to face a period of domestic economic stagnation stemming from the extraordinary rise in private sector debt that has built up over the past two decades. The co-ordinated global response to the pandemic suggests that this is not the end of Sweden’s debt supercycle, but timing the transition from reflation to stagnation will be of crucial importance for investors exposed to the domestic Swedish economy over the coming few years. Feature One of the worrying legacies of the global financial crisis has been a substantial buildup in private sector debt in many economies around the world. This has most famously occurred in China, but private indebtedness is also very high in many developed economies. Among advanced countries, Sweden stands out as being particularly exposed to elevated private sector debt. Chart I-1 highlights that Sweden’s private sector debt-to-GDP ratio has ballooned to a massive 250% of GDP over the past 15 years, from a starting point of roughly average indebtedness. Chart I-1Sweden's Extremely Indebted Private Sector

Sweden's Extremely Indebted Private Sector

Sweden's Extremely Indebted Private Sector

In this report we explore why Sweden has seen an explosion in private sector debt-to-GDP, and highlight that Sweden’s experience can be compared closely with that of Canada – both countries are in the orbit of a major neighboring central bank, which has created distortions in each economy. We also summarize what this implies for Riksbank policy, and what investment recommendations can be drawn from our analysis. We conclude that while the Riksbank is clearly reluctant to cut the repo rate after having just existed its negative interest rate position last year, it appears likely that they will forced to do so unless the negative economic impact from the COVID-19 pandemic abates very soon. Over the short-term, this suggests that investors should avoid the Swedish krona, versus either the US dollar or the euro. Why has Sweden seen such an explosion in private-sector debt? Over the medium-term, easy Riksbank policy and the probable absence of any additional macroprudential measures is likely to spur a renewed increase in Swedish house prices and household debt, which will likely benefit consumer durables and apparel stocks relative to the broad Swedish equity market. But this will reinforce Sweden’s existing credit bubble, and similar to Canada will set the stage for domestic economic stagnation over the very long-term. Riksbank Policy and Sweden’s Private Sector Debt: A Tale Of Three Phases Much of the investor attention on Sweden's extremely high private sector debt load has occurred following the global financial crisis. But Chart I-1 clearly highlights that the process of private sector leveraging began in 2004, arguing that the Riksbank’s easy monetary policy stance following the global financial crisis is not the only cause of Sweden’s extremely elevated private debt-to-GDP ratio. In a previous Special Report for our Global Investment Strategy service,1 we investigated a similar experience in Canada and used a simple Taylor rule approach to show that the Bank of Canada’s decision to maintain interest rates below equilibrium levels for nearly two decades has contributed to a substantial buildup in private sector leverage. A similar approach for Sweden highlights similar conclusions, albeit with some complications: Chart I-2 shows our Taylor rule estimate for Sweden alongside the policy rate, and shows the deviation from the rule in the second panel. Chart I-2Since 2000, Sweden Has Had Three Distinct Monetary Policy Phases

Since 2000, Sweden Has Had Three Distinct Monetary Policy Phases

Since 2000, Sweden Has Had Three Distinct Monetary Policy Phases

Compared with Canada’s experience, which has maintained too-low interest rates consistently for the past 20 years, Chart I-2 shows that the stance of Sweden’s monetary policy since 2000 falls into three distinct phases: Persistently easy policy from 2000 to 2008 A period of less easy and then relatively tight policy from 2009 to early-2014 A period of extremely easy policy from 2015 until today. The first phase noted above closely resembles the experience of Canada: policymakers in both countries simply kept interest rates too low during the last global economic expansion. In the second phase, the stance of monetary policy in Sweden became progressively less easy: the Taylor rule collapsed in 2009/2010, and trended lower again during the euro area sovereign debt crisis as well as its aftermath. In fact, Chart I-2 suggests that Sweden’s monetary policy stance was outrightly tight from 2012-2014, and in early-2014 the Taylor rule recommended negative policy rates while the actual policy rate was above 1%. In the third phase, the Riksbank appears to have overcompensated for the second phase of relatively less easy and eventually tight monetary policy. The Riksbank pushed policy rates into negative territory in late-2014, as had been recommended by the Taylor rule a year before, at a time when the rule was rising sharply. Roughly 2/3rds of the rise in the rule from early-2014 to late-2018 occurred due to the significant rise in Swedish inflation, with the rest due to a rise in Sweden’s output gap – which turned positive in late-2016 according to the OECD (Chart I-3). It is this third phase, featuring a massive and glaring gap between Swedish policy rates and a monetary policy rule that correctly recommended easy policy from 2010 – 2014, that has attracted global investor attention over the past few years. But Chart I-4 presents Sweden’s Taylor rule gap alongside its private sector debt-to-GDP ratio, and highlights that over 80% of the rise in the latter since 2000 actually occurred in the first phase described above – a period of persistently easy monetary policy as defined by our Taylor rule approach. The behavior of Sweden’s private sector debt-to-GDP ratio in the second and third phases also seems to validate our approach, as gearing essentially stopped during the second phase and restarted in the third phase. Chart I-3Since 2014, Sweden’s Rising Taylor Rule Has Been Driven Mostly By Inflation

Since 2014, Sweden's Rising Taylor Rule Has Been Driven Mostly By Inflation

Since 2014, Sweden's Rising Taylor Rule Has Been Driven Mostly By Inflation

Chart I-4Sweden’s Monetary Policy Phases Explain Its Private Sector Leveraging

Sweden's Monetary Policy Phases Explain Its Private Sector Leveraging

Sweden's Monetary Policy Phases Explain Its Private Sector Leveraging

The Riksbank: “Talk To Us About Inflation, Not Debt” Chart I-5During Phase 2, Households Clearly Took Advantage Of Low Mortgage Rates

During Phase 2, Households Clearly Took Advantage Of Low Mortgage Rates

During Phase 2, Households Clearly Took Advantage Of Low Mortgage Rates

It is crucial to understand the motivations of Sweden’s central bank during each of these phases in order to be able to forecast the likelihood of a return to negative interest rates this year, as well as the Riksbank’s likely policy response once the COVID-19 pandemic subsides. In the first monetary policy phase that we have described, Sweden was not the only country to maintain persistently easy monetary policy. Given the relative scarcity of private sector deleveraging events in the post-war era, most policy makers, academic economists, and market participants were regrettably unconcerned about rising private sector indebtedness during this period, and only came to understand the consequences during the crisis and its aftermath. Most advanced economies leveraged during the first of Sweden’s monetary policy phases, and Sweden really only stands out as a major outlier from 2007 – 2009 when nearly 60% of the country’s total 2000-2019 private sector leveraging occurred (most of which, in turn, occurred before the collapse of Lehman Brothers in September 2008). In essence, by the time that Swedish policymakers were given a vivid and painful demonstration of the dangers of elevated private sector debt, it was too late to prevent most of the increase in debt-to-GDP that is facing the country today. In the second phase of Sweden's modern monetary policy, our Taylor rule framework highlights that the Riksbank largely acted as appropriate. One complication, however, is the difference in the leverage trend between Sweden's nonfinancial corporate and household sectors. Chart I-5 clearly highlights that Sweden's household sector took advantage of low interest rates during the country’s second monetary policy phase. Household sector leveraging began to rise again starting in late-2011, whereas it was completely absent for the corporate sector during the period. A crucial reason why the Riksbank ignored this renewed household sector leveraging is also part of the reason that it has maintained extremely low policy rates in the third phase noted above. The Riksbank’s monetary policy strategy, which is published in every monetary policy report, includes the following: “According to the Sveriges Riksbank Act, the Riksbank’s tasks also include promoting a safe and efficient payment system. Risks linked to developments in the financial markets are taken into account in the monetary decisions. With regard to preventing an unbalanced development of asset prices and indebtedness however, well-functioning regulation and effective supervision play a central role. Monetary policy only acts as a compliment to these.” In other words, the Riksbank has been very clear that preventing excessive leveraging is not its responsibility, and that the job ultimately falls to the Swedish government. But if the Taylor rule was recommending meaningfully higher interest rates during phase 3, then why did the Riksbank continue to lower interest rates into negative territory until last year? In our view, their behavior can be explained by the confluence of three factors: 1. Sweden’s deflation scare in 2014: Sweden’s underlying inflation rate had been trending lower for four years by the time that it dipped briefly into negative territory in March 2014. By this point, the Riksbank appears to have become increasingly concerned about inflation expectations rather than the trend in actual inflation. Chart I-6 presents Sweden’s underlying inflation rate and an adaptive-expectations based estimate of inflation expectations alongside the repo rate, and shows that inflection points in the repo rate match inflection points in expectations. Specifically, the repo rate continued to fall until inflation expectations stabilized in early-2016, and the Riksbank did not raise the repo rate until expectations crossed above 1.5%, a level that was reasonably close to the central bank’s 2% target. Chart I-6During Phase 3, The Riksbank Focused On Low Inflation Expectations

During Phase 3, The Riksbank Focused On Low Inflation Expectations

During Phase 3, The Riksbank Focused On Low Inflation Expectations

2. Sweden’s high trade sensitivity: Chart I-7 highlights that Sweden’s economy, like Canada and other Scandinavian countries, is highly exposed to exports to top trading partners. The euro area accounts for a large portion of Sweden’s exports, and Chart I-8 highlights that nominal euro area imports from Sweden remained very weak from 2012-2016. In addition, Sweden’s import sensitivity is also very high, with total imports of goods and services accounting for over 40% of Sweden’s GDP. By our calculations, roughly 2/3rds of Swedish imports are for domestic consumption,2 and Chart I-9 highlights how closely (inversely) correlated imported consumer and capital goods prices are to Sweden’s trade-weighted currency index. By pushing the repo rate into negative territory, the Riksbank reinforced rising inflation expectations by supporting exports and importing inflation from its trading partners via a weaker krona. Chart I-7Sweden, Like Other Small DM Countries, Are Highly Exposed To Trade

Sweden, Like Other Small DM Countries, Are Highly Exposed To Trade

Sweden, Like Other Small DM Countries, Are Highly Exposed To Trade

Chart I-8Euro Area Demand For Swedish Goods Remained Weak For Several Years

Euro Area Demand For Swedish Goods Remained Weak For Several Years

Euro Area Demand For Swedish Goods Remained Weak For Several Years

Chart I-9To 'Import' Inflation, The Riksbank Had To Weaken The Krona

To 'Import' Inflation, The Riksbank Had To Weaken The Krona

To 'Import' Inflation, The Riksbank Had To Weaken The Krona

3. The euro area’s persistently weak inflation and extremely easy monetary policy: While this is related to Sweden's overall trade sensitivity, the fact that the euro area had to combat persistently weak inflation with negative interest rates and asset purchases from late-2014 to late-2018 has had a particularly strong impact on Riksbank policy given the latter’s goal of boosting Swedish inflation via higher import prices. Chart I-10 highlights the strong link between the SEK-EUR exchange rate and the real interest rate differential between the two countries, and in particular shows that the Riksbank had to lower the differential into negative territory in order to bring the krona below “normal” levels (defined here as the average of the past global economic expansion). When faced with a real euro area policy rate of roughly -1.5% during the period (Chart I-11), the only way to achieve a negative real rate differential was to maintain the repo rate at an extremely low level as Swedish inflation rose. Chart I-10To Weaken The ##br##Krona...

To Weaken The Krona...

To Weaken The Krona...

Chart I-11…Deeply Negative Real Policy Rates Were Required

...Deeply Negative Real Policy Rates Were Required

...Deeply Negative Real Policy Rates Were Required

Where Next For The Repo Rate? In February 2019 the Riksbank was forecasting that the repo rate would return into positive territory by the end of this year, and would rise as high as 80 basis points by mid-2022. They downgraded this assessment in April, and again in October, highlighting that they expected a 0% repo rate for essentially the entire three-year forecast period. In other words, the Riksbank had been moving in a dovish direction even before the COVID-19 pandemic began. Prior to the outbreak, we would have been inclined to argue that the Riksbank’s forecast of a 0% repo rate beyond 2020 was suspect, given the budding recovery in global growth. Chart I-12 highlights that the global PMI had been improving for several months prior to the outbreak, and the Swedish PMI and consumer confidence index had recently rebounded sharply. A negative repo rate was essential to “import” inflation. But, given the extent of the spread of the SARS-CoV-2 virus, especially in Europe, and our description of the Riksbank mandate and reaction function, the odds appear to be high that the repo rate will move back into negative territory at some point this year. Besides the very negative direct impact to global trade from the pandemic, Chart I-13 highlights that Swedish inflation is now falling, and that our measure of inflation expectations has now peaked. Chart I-12Swedish Economic Momentum Was Building Prior To The Pandemic...

Swedish Economic Momentum Was Building Prior To The Pandemic...

Swedish Economic Momentum Was Building Prior To The Pandemic...

Char I-13...But Inflation Is Falling And The Unemployment Rate Is Rising

...But Inflation Is Falling And The Unemployment Rate Is Rising

...But Inflation Is Falling And The Unemployment Rate Is Rising

In addition, the Swedish unemployment rate has been trending higher since early-2018 (Chart I-13, second panel), in response to several factors: a shock to household wealth in late-2015/early-2016 due to sharply falling equity prices, a meaningful decline in house prices driven by newly introduced macroprudential policies, and a sharp albeit seemingly one-off decline in the contribution to Swedish economic growth from government expenditure (Chart I-14). These trends would have likely reversed at some point this year given the building economic momentum that was evident in January and early-February, but it is now clear that the pandemic will more than offset the budding improvement in economic activity. Chart I-14Swedish Policymakers Will Have To Reverse The Factors That Caused The Pre-Pandemic Slowdow

Swedish Policymakers Will Have To Reverse The Factors That Caused The Pre-Pandemic Slowdow

Swedish Policymakers Will Have To Reverse The Factors That Caused The Pre-Pandemic Slowdow

Over the past week the Riksbank has announced two policies: it will provide cheap loans to the country’s banks (500 billion SEK) to bolster credit supply to Swedish small & medium-sized enterprises, and it will increase its asset purchase program by 300 billion SEK. The Riksbank is clearly reluctant to cut the repo rate after having just existed its negative interest rate position last year, and has argued that strong liquidity support and stepped up asset purchases are more likely to be effective measures in the current environment. However, Charts I-10 & I-11 underscored the link between real interest rate differentials and the currency, and the Riksbank will risk having the krona appreciate versus the euro and other currencies if inflation continues to fall and the policy rate is kept unchanged. Chart I-15 shows that market participants have already begun to price in cuts to the repo rate, and our sense is that the Riksbank will be forced to act in a way that is consistent with the market’s view. Chart I-15The Market Expects The Riksbank To Return To Negative Interest Rates. We Agree.

The Market Expects The Riksbank To Return To Negative Interest Rates. We Agree.

The Market Expects The Riksbank To Return To Negative Interest Rates. We Agree.

Investment Conclusions Over a cyclical (i.e. 6-12 month) time horizon, the Swedish krona is the asset with the clearest link to our discussion of Riksbank policy, and investors should recognize that the krona call is now a binary one based on the evolution of the COVID-19 pandemic. It is one of the cheapest currencies in the G10 space, but foreign exchange markets have recently ignored fundamentals such as interest rate differentials and valuation. This is particularly true in the face of a spike in US dollar cross-currency basis swaps, which have started to send the dollar higher even against the safe haven currencies. In such an a environment, selling pressure could continue to push SEK lower, especially if the Riksbank is pushed to reduce the repo rate sooner rather than later. The SEK is one of the most procyclical currencies in the FX space, suggesting that investors should stand aside until markets stabilize (Chart I-16). Right now, the Swedish krona is the clearest play on Riksbank policy. As for the EUR/SEK cross, any renewed ECB stimulus suggests that Sweden will act accordingly to prevent the SEK from appreciating too far, too fast. EUR/SEK will top out after global growth is in an eventual upswing, and the Riskbank has eased policy further. Over the medium-term time horizon, one implication of a return to negative interest rates is that Swedish house price appreciation is likely to trend higher once the economic impact of the COVID-19 pandemic ends. House prices will likely decelerate in the near term given the shock to household wealth from falling equity prices, but we showed in Chart I-5 that Sweden’s household sector ultimately took advantage of low interest rates during Sweden’s second monetary policy phase. We expect a similar dynamic to unfold beyond the coming 6-9 months, and Chart I-17 highlights that overweighting Swedish consumer durable and apparel stocks within the overall Swedish equity market is likely the best way to eventually play a resumption of household leveraging and rising house prices. Chart I-16Avoid Krona Exposure ##br##For Now

Avoid Krona Exposure For Now

Avoid Krona Exposure For Now

Chart I-17Swedish Consumer Durables & Apparel Stocks Linked To Domestic, Not Global, Demand

Swedish Consumer Durables & Apparel Stocks Linked To Domestic, Not Global, Demand

Swedish Consumer Durables & Apparel Stocks Linked To Domestic, Not Global, Demand

With the exception of a selloff in 2013, the relative performance of the industry group has closely correlated with house price appreciation, and is now deeply oversold. The companies included the industry group earn a significant portion of their revenue from global sales, but the close correlation of relative performance with Swedish house prices and limited correlation with the global PMI suggests that domestic economic performance matter in driving returns for these stocks (Chart I-17, bottom panel). We are not yet prepared to recommend a long relative position favoring this industry group, but we are likely to view signs of policy traction and a relative performance breakout as a good entry point. Finally, the key long-term implication of our research is that Sweden will at some point likely face a period of stagnation stemming from the extraordinary rise in private sector debt that has built up over the past two decades. While regulators had begun to combat excessive debt with macroprudential measures, further measures to restrict household sector debt are extremely unlikely to occur until after another substantial reacceleration in Swedish house prices and another nontrivial rise in household sector leverage. This will be cyclically positive for Sweden coming out of the pandemic, but will ultimately make Sweden’s underlying debt problem meaningfully worse. Macroprudential control of rising nonfinancial corporate debt has not and is not likely to occur, and no regulatory control measure will be able to significantly ease the existing debt burden facing the private sector. Chart I-18 highlights that while Sweden’s private sector debt service ratio (DSR) is not the highest in the world, is it extremely elevated compared to other important DM countries such as the US, UK, Japan, and core euro area. Several other countries with higher private sector DSRs, such as Canada and Hong Kong, are also at serious risk of long-term stagnation. Chart I-18Swedish Domestic Economic Stagnation Is A 'When', Not An 'If'

Swedish Domestic Economic Stagnation Is A 'When', Not An 'If'

Swedish Domestic Economic Stagnation Is A 'When', Not An 'If'

We have not yet identified a specific list of assets that will be negatively impacted by Swedish domestic economic stagnation over the longer term. Our European Investment Strategy service recently argued that Swedish stocks are attractive over the very long term versus Swedish bonds, based on valuations and the fact that the Swedish equity market as a whole is heavily driven by the global business cycle. We plan on revisiting the question of which equity sectors are most vulnerable to domestic stagnation in a future report, as the onset of stagnation draws nearer. As we noted in our report on Canada,3 it is difficult to identify precisely when Sweden’s high debt load will meaningfully and sustainably impact Swedish economic activity and related equity sectors. The acute shock to global activity from the COVID-19 pandemic is an obvious potential trigger, but the fact that policymakers around the world are responding forcefully to the pandemic suggests that this is not the end of Sweden’s debt supercycle. In this regard, the prospect of globally co-ordinated fiscal spending is especially significant. Our best guess is that Sweden’s true reckoning will come once US and global activity contracts for conventional reasons, instigated by tight monetary policy to control rising and above-target inflation. This may mean that Sweden will avoid a balance sheet recession for some time, but investors exposed to domestically-linked Swedish financial assets should take heed that the eventual consequences of such an event are likely to grow in magnitude the longer it takes to arrive. In short, beyond the acute nearer-term impact of the pandemic, Sweden is likely to experience short-term gain for long-term pain. The short- to medium-term focus of investors should be on the former, but with full recognition that the latter will eventually occur. Timing the transition between these two states will be of crucial importance for investors exposed to the domestic Swedish economy over the coming few years. Stay tuned! Jonathan LaBerge, CFA, Vice President Special Reports jonathanl@bcaresearch.com Footnotes 1 Please see Global Investment Strategy Special Report "Canada: A (Probably) Happy Moment In An Otherwise Sad Story," dated July 14, 2017, available at uses.bcaresearch.com 2 We assume that all services imports are consumed domestically. Among goods exports, we assume domestic consumption of all imports of food & live animals, beverages & tobacco, mineral fuels, lubricants, and related materials, miscellaneous manufactured articles, road vehicles, and other goods. 3 Please see Global Investment Strategy Special Report "Canada: A (Probably) Happy Moment In An Otherwise Sad Story," dated July 14, 2017, available at uses.bcaresearch.com

Yesterday, BCA Research's Global Fixed Income Strategy service urged investors to stay tactically defensive on corporate credit. The COVID-19 global market rout has generated levels of market volatility not seen since the 2008 Global Financial Crisis.…

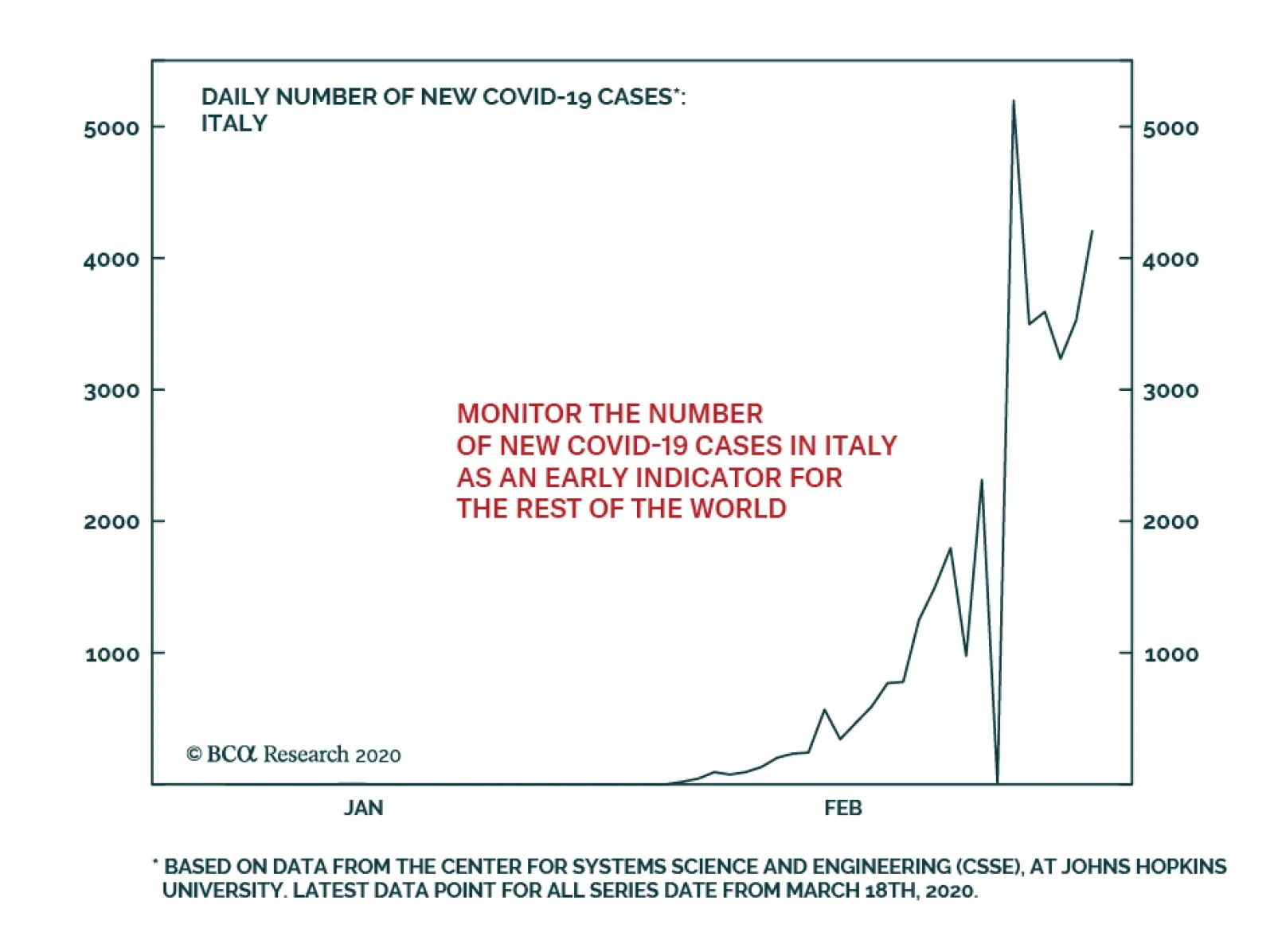

We recommend investors closely follow the number of new COVID-19 cases in Italy. At 4,207, as of March 18th, this number remains lower than it was on March 13th. However, new cases have nonetheless trended up over that past three days. Italy is…

Highlights Policy Responses: The COVID-19 pandemic has become a full-blown global crisis and recession. Governments and central bankers worldwide are now responding with aggressive monetary easing and fiscal stimulus. Markets will not respond positively to such stimulus, however, until there is some visibility on the true depth, and duration, of the economic downturn. Fixed Income Strategy: With a global recession now a certainty, bond yields will remain under downward pressure and credit spreads should widen further. Given how far yields have already fallen, we recommend emphasizing country and credit allocation in global bond portfolios, while keeping overall duration exposure around benchmark levels. Model Portfolio Changes: Following up on our tactical changes last week, we continue to recommend overweighting government debt versus spread product. Specifically, overweighting US & Canadian government bonds versus Japan and core Europe, and underweighting US high-yield and all euro area and EM credit. Feature In stunning fashion, the sudden stop in the global economy due to the COVID-19 pandemic has triggered a rapid return to crisis-era monetary and fiscal policies. The battle has now shifted to trying to fill the massive hole in global private sector demand left by efforts to contain the spread of the virus. It is unlikely that lower interest rates and more quantitative easing can mitigate the negative growth effects from travel bans, closing of bars and restaurants, and full scale lockdowns of cities. Fiscal policy, combined with efforts to boost market liquidity and ease the coming collapse of cash flows for the majority of global businesses, are the only plausible options remaining. It is unlikely that lower interest rates and more quantitative easing can mitigate the negative growth effects from travel bans, closing of bars and restaurants, and full scale lockdowns of cities. While the speed of these dramatic policy moves is unprecedented, the reason for them is obvious. Plunging equities and surging corporate bond credit spreads are signaling a global recession, but one of uncertain depth and duration given the uncertainties surrounding the spread of COVID-19 (Chart of the Week). Chart of the WeekCan Crisis-Era Monetary Policies Be Effective During A Pandemic?

Can Crisis-Era Monetary Policies Be Effective During A Pandemic?

Can Crisis-Era Monetary Policies Be Effective During A Pandemic?

Chart 2Risk Assets Will Not Bottom Until New COVID-19 Cases Ex-China Peak

Risk Assets Will Not Bottom Until New COVID-19 Cases Ex-China Peak

Risk Assets Will Not Bottom Until New COVID-19 Cases Ex-China Peak

The ability for policymakers to calibrate stimulus measures is pure guesswork at this point. The same thing goes for investors who see zero visibility on global growth, with the full extent of the virus yet to be felt in large economies like the United States and Germany – even as new cases in China, where the epidemic began, approach zero. The response from central bankers has been swift and bold – rapid rate cuts, increased liquidity programs for bank funding and increased asset purchases. The fact that global financial markets have remained volatile, even after what is a clear coordinated effort from policymakers, highlights how the unique threats to growth from the COVID-19 pandemic may be beyond fighting with traditional demand-side stimulus measures. We continue to recommend a cautious near-term investment stance, particular with regards to corporate bond exposure, until there is clear evidence that the growth rate of new COVID-19 cases outside China has peaked (Chart 2). Policymakers Throw The Kitchen Sink At The Problem The market moves and policy announcements have come fast and furious this past week, from virtually all major economies. We summarize some of the moves below: United States The Fed cut rates by -100bps in a Sunday night emergency move, taking the funds rate back to the effective lower bound of 0% - 0.25%. Importantly, Fed Chair Powell made it clear at his press conference that negative rates are not on the table, suggesting that we may have seen the last of the rate cuts for this cycle. A new round of quantitative easing (QE) was also announced, with purchases of $500 billion of Treasury securities and $200 billion of agency MBS that will occur in the “coming months”; Powell hinted that those amounts could be increased, if necessary (Chart 3). The MBS purchases are a clear effort to help bring down mortgage rates, which have not declined anywhere near as rapidly as US Treasury yields during the market rout (bottom panel). The Fed also cut the discount window rate – the rate at which banks can borrow from the Fed for periods of up to 90 days – by -150bps, bringing it down to 0.25%. The Fed said it is “encouraging banks to use their capital and liquidity buffers” – essentially telling banks to hold less cash for regulatory purposes. The Fed also reduced the rate on its US dollar swap lines with other central banks. The new rate is OIS +25bps. Coming on top of the massive increase in existing repo lines last week, the Fed is attempting to ensure that banks, both in the US and globally, that need USD funding have more liquidity available to support lending. Already, there are signs of worsening liquidity in the bank funding markets, like widening FRA-OIS spreads, but also evidence of illiquidity in financial markets like wide bid-ask spreads on longer-maturity US Treasuries and the growing basis between high-yield bonds and equivalent credit default swaps (Chart 4). Chart 3A Return To Fed QE

A Return To Fed QE

A Return To Fed QE

Chart 4Market Liquidity Issues Forced The Fed's Hand

Market Liquidity Issues Forced The Fed's Hand

Market Liquidity Issues Forced The Fed's Hand

Turning to fiscal policy, the full response of the Trump administration is still being formed, but a major $850bn spending package has been proposed that would provide tax relief for American households and businesses while also including a $50bn bailout of the US airline industry. This comes on top of previously announced plans to offer free testing for the virus, paid sick leave, business tax credits and a temporary suspension of student loan interest payments. Chart 5The ECB Has Limited Policy Options

The ECB Has Limited Policy Options

The ECB Has Limited Policy Options

Euro Area The European Central Bank (ECB) unexpectedly made no changes to policy interest rates last week. It opted instead to increase asset purchases by €120bn until the end of 2020 (both for government bonds and investment grade corporates), while introducing more long-term refinancing operations (LTROs) to “provide a bridge” to the targeted LTRO (TLTRO-3) that is set to begin in June. The terms of TLTRO-3 were improved, as well; banks that accessed the liquidity to maintain existing lending could do so at a rate up to -25bps below the current ECB deposit rate of -0.5%, for up to 50% of the existing stock of bank loans. The ECB obviously had to do something, given the coordinated nature of the global monetary policy response to COVID-19. Yet the decisions taken show that the ECB is much more limited in its ability to ease policy further, with interest rates already negative, asset purchases approaching self-imposed country limits and, most worryingly, inflation expectations falling to fresh lows (Chart 5). The bigger responses to date have come on the fiscal front, with stimulus packages proposed by France (€45bn), Italy (€25bn), Spain (€3bn) and the European Commission (€37bn). The biggest news, however, came from Germany which has offered affected businesses tax breaks and cheap loans through the state development bank, KfW – the latter with an planned upper limit of €550bn (and with the German government assuming a greater share of risk on those new KfW loans). The German government has also vaguely promised to temporarily suspend its so-called “debt brake” to allow deficit financing of virus-related stimulus programs, if necessary. Other Countries The Bank of England cut interest rates by -50bps last week, while also lowering capital requirements for UK banks by allowing use of counter-cyclical buffers for lending. On the fiscal side, a £30bn package was introduced last week that included a tax cut for retailers, cash grants to small business, sick pay for those with COVID-19 and extended unemployment benefits. The Bank of Japan held an emergency meeting this past Sunday night, announcing no changes in policy rates but doubling the size of its ETF purchase program to $56 billion a year to $112 billion, while also increasing purchases of corporate bonds and commercial paper. The central bank also announced a new program of 0% interest loans to increase lending to businesses hurt by the virus. The Bank of Canada delivered an emergency -50bps cut in its policy rate last Friday, coming soon after the -50bp reduction from the previous week. The central bank also introduced operations to boost the liquidity of Canadian financial markets. The Canadian government also announced a fiscal package of up to C$20bn, including increased money for the state business funding agencies. The Reserve Bank of Australia did not cut its Cash Rate last week, which was already at a record-low 0.5%. It did, however, signal that it would begin a quantitative easing program for the first time, and introduce Fed-like repo operations, to provide more liquidity to the economy and local financial markets. The Australian government has also announced A$17bn of fiscal stimulus. Fiscal packages have also been introduced in New Zealand (where the Reserve Bank of New Zealand just cut its policy rate by -75bps), Sweden, Switzerland, Norway, and South Korea. To date, China has leaned more on monetary and liquidity measures – lowering interest rates and cutting reserve requirements – rather than a big fiscal stimulus package. Will all these policy measures be enough to offset the hit to global growth from COVID-19 and help stabilize financial markets? It is certainly a good start, particularly in countries with low government and deficit levels that have the fiscal space for even more stimulus, like Germany, Australia and Canada (Chart 6). Given these competing forces of global recession and monetary policy exhaustion on one side, but with increasingly more expansive fiscal policy on the other, we recommend a neutral (at benchmark) stance on overall global duration exposure on both a tactical and strategic basis. The ability to calibrate the necessary policy response is impossible to assess without knowing the full impact of COVID-19 pandemic on the global economy – including the size of related job losses and corporate defaults/bankruptcies. Policymakers are likely to listen to the combined message of financial markets – equity prices, credit spreads and government bond yields. The low level of yields and flat yield curves, despite near-0% policy rates across the developed world (Chart 7), suggests that investors see monetary policy as “tapped out”, leaving fiscal stimulus as the only way to fight the economic war against COVID-19. Chart 6At Global ZIRP, The Policy Focus Shifts To Fiscal

At Global ZIRP, The Policy Focus Shifts To Fiscal

At Global ZIRP, The Policy Focus Shifts To Fiscal

Chart 7Are Bond Yields Discounting A Global Liquidity Trap?

Are Bond Yields Discounting A Global Liquidity Trap?

Are Bond Yields Discounting A Global Liquidity Trap?

Given these competing forces of global recession and monetary policy exhaustion on one side, but with increasingly more expansive fiscal policy on the other, we recommend a neutral (at benchmark) stance on overall global duration exposure on both a tactical and strategic basis. Bottom Line: The COVID-19 pandemic has become a full-blown global crisis and recession. Governments and central bankers worldwide are now responding with aggressive monetary easing and fiscal stimulus. Markets will not respond positively to such stimulus, however, until there is some visibility on the true depth, and duration, of the economic downturn. Corporate Bonds In The US & Europe – Stay Tactically Defensive Chart 8This Crisis Is Different Than 2008

This Crisis Is Different Than 2008

This Crisis Is Different Than 2008

The COVID-19 global market rout has generated levels of market volatility not seen since the 2008 Global Financial Crisis. The US VIX index of option-implied equity volatility spiked to a high of 84, while the equivalent German VDAX measure reached a shocking high of 93. Equity valuations in both the US and Europe remain much higher on a forward price/earnings ratio basis compared to the troughs seen in 2008, even after the COVID-19 bear market. Yet even though volatility has returned to crisis-era extremes, and corporate credit has sold off hard in both the US and Europe, credit spreads remain well below the 2008 highs (Chart 8). Nonetheless, the credit selloff seen over the past few weeks has still been intense. Both investment grade and high-yield spreads have blown out, and across all credit tiers in both the US (Chart 9) and euro area (Chart 10). Even the highest-rated segments of the corporate bond universe have seen spreads explode, with AAA-rated investment grade spreads having doubled in both the US and Europe. Chart 9Broad-Based Spread Widening For Both Investment Grade...

Broad-Based Spread Widening For Both Investment Grade...

Broad-Based Spread Widening For Both Investment Grade...

Chart 10...And High-Yield

...And High-Yield

...And High-Yield

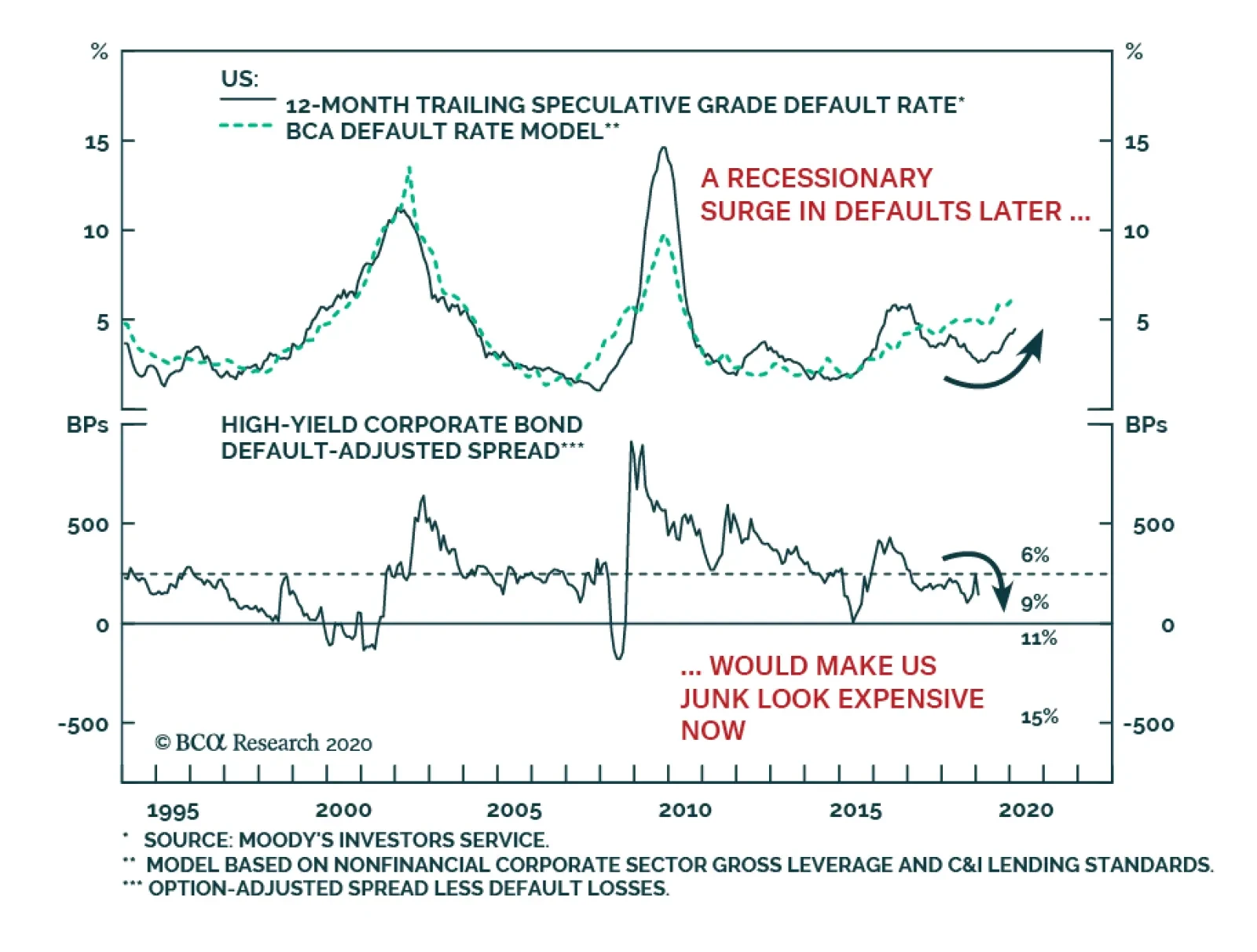

With the COVID-19 pandemic tipping the global economy into recession, it is not clear that the spread widening seen to date has been enough to compensate for the typical surge in downgrades and defaults seen during recessions – even though spreads do look wide on a duration-adjusted basis. With the COVID-19 pandemic tipping the global economy into recession, it is not clear that the spread widening seen to date has been enough to compensate for the typical surge in downgrades and defaults seen during recessions – even though spreads do look wide on a duration-adjusted basis. One of our favorite metrics to value corporate bonds is to look at option-adjusted spreads, adjusted for interest rate duration risk. We call this the 12-month breakeven spread, as it measures the amount of spread widening over one year that would leave corporate bond returns equal to those of duration-matched US Treasuries. We then look at the percentile rankings of those breakeven spreads versus their history as one indicator of corporate bond value. Chart 11US Corporates Look Cheaper On A Duration-Adjusted Basis

US Corporates Look Cheaper On A Duration-Adjusted Basis

US Corporates Look Cheaper On A Duration-Adjusted Basis

For the US, the 12-month breakeven spreads for the overall Bloomberg Barclays investment grade and high-yield indices are in the 82nd and 97th percentiles, respectively (Chart 11). This suggests that the latest credit selloff has made corporate debt quite cheap, although only looking through the prism of spread risk rather than potential default losses. Another of our preferred valuation metrics for high-yield debt is the duration-adjusted spread, or the high-yield index option-adjusted spread minus default losses. We then look at that default-adjusted spread versus its long-run average (+250bps) as a measure of high-yield value. To assess the current level of spreads, we use a one-year ahead forecast of the expected default rate using our own macro model. Over the past 12 months, the high-yield default rate was 4.5% and our macro model is currently calling for a rise to 6.2%. That estimate, however, does not yet include the certain hit to corporate profits from the COVID-19 recession. By way of comparison, the default rate peaked at 11.2% during the 2001/02 default cycle and at 14.6% during the 2008 financial crisis. In Chart 12, we show the historical default rate, our macro model for the default rate, and the history of the default-adjusted spread. We also show what the default-adjusted spread would look like in four different scenarios for the default rate over the next 12 months: 6%, 9%, 11% and 15%. The placement of these numbers in the bottom panel of Chart 12 indicates where the Default-Adjusted Spread will be if each scenario is realized. Chart 12US High-Yield Is Not Cheap On A Default-Adjusted Basis

US High-Yield Is Not Cheap On A Default-Adjusted Basis

US High-Yield Is Not Cheap On A Default-Adjusted Basis

Right now, our expectation is that there will be a virus driven US recession, but it will be shorter in magnitude than past recessions; this suggests a peak default rate closer to 9%. Such a scenario would still be consistent with a positive default-adjusted spread and likely positive excess returns for US high-yield relative to US Treasuries on a 12-month horizon. However, if a default rate similar to that seen during past recessions (11% or 15%) is realized, that would lead to a negative default-adjusted spread. Adding up both pieces of our valuation framework suggests that, while US high-yield spreads offer value on a duration-adjusted basis, spreads do not compensate enough for potential default losses if the US recession lasts longer than we expect. Thus, we recommend a tactical underweight position in US high-yield until we see better visibility on the severity, and duration, of the US recession. Adding up both pieces of our valuation framework suggests that, while US high-yield spreads offer value on a duration-adjusted basis, spreads do not compensate enough for potential default losses if the US recession lasts longer than we expect. As for euro area corporates, spreads for both investment grade and high-yield do look relatively wide on a breakeven spread basis, although less so than US credit (Chart 13). However, with the World Health Organization declaring Europe as the new epicenter of the COVID-19 pandemic, the harsh containment measures seen in Italy, Germany, France and elsewhere – coming from a starting point of weak overall economic growth – suggest that euro area spreads need to be wider to fully reflect downgrade and default risks. Chart 13Euro Area Corporates Look A Bit Cheaper On A Duration-Adjusted Basis

Euro Area Corporates Look A Bit Cheaper On A Duration-Adjusted Basis

Euro Area Corporates Look A Bit Cheaper On A Duration-Adjusted Basis

We recommend a tactical underweight allocation to both euro area corporate debt and Italian sovereign debt, as spreads have room to reprice wider to reflect a deeper recession (Chart 14). Chart 14Stay Underweight Euro Area Spread Product

Stay Underweight Euro Area Spread Product

Stay Underweight Euro Area Spread Product

Bottom Line: Corporate bond spreads on both sides of the Atlantic discount a sharp economic slowdown, but the odds of a deeper recession – and more spread widening - are greater in Europe relative to the US. A Quick Note On Recent Changes To Our Model Bond Portfolio In last week’s report, we made several adjustments to our model bond portfolio recommended allocations on a tactical (0-6 months) basis.1 Specifically, we downgraded our overall recommended exposure to global spread product to underweight, while increasing the overall allocation to government debt to overweight. The specific changes made to the model bond portfolio are presented in tables on pages 14 & 15. Within the country allocation of the government bond side of the portfolio, we upgraded US and Canada (markets more sensitive to changes in global bond yields, and with central banks that still had room to ease policy) to overweight, while downgrading core Europe to underweight and Japan to maximum underweight (both markets less sensitive to global yields and with no room to cut rates). On the credit side of the portfolio, we downgraded US high-yield to underweight (with a 0% allocation to Caa-rated debt), while also downgrading euro area investment grade and high-yield debt to underweight. We also lowered allocations to emerging market USD denominated debt, both sovereign and corporate, to underweight. We left the allocation to US investment grade debt at neutral, as the other reductions left our overall spread product allocation at the desired level (35% versus the 43% spread product weighting in our custom benchmark portfolio index). In terms of the specific weightings, the portfolio is now +11% overweight US fixed income versus the benchmark, coming most through US Treasury exposure. The portfolio is now -7% underweight euro area versus the benchmark, equally thorough government bond and corporate debt exposure. The portfolio is now also has a -7% weight in Japan versus the benchmark, entirely from government bonds. Note that these weightings represent a tactical allocation only, as we are recommending a defensive stance on spread product exposure given the near-term uncertainties over COVID-19 and global growth. On a strategic (6-12 months) horizon, however, we are neutral overall spread product exposure versus government bonds. Corporate bond spreads already discount a sharp economic slowdown and some increase in defaults. However, the rapid shift to aggressive monetary and fiscal easing by global policymakers to combat the virus will likely limit the duration and, potentially, the severity of the global slowdown currently discounted in wide credit spreads. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 Please see BCA Global Fixed Income Strategy Weekly Report, "The Train Is Empty", dated March 10, 2020, available at gfis.bcarsearch.com. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Panicked Policymakers Move To A Wartime Footing

Panicked Policymakers Move To A Wartime Footing

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

Highlights The path of least resistance for the DXY remains up. The internal dynamics of financial markets remain constructive for the DXY. We explore more key indicators to complement the analysis in our February 28 report. Our limit buy on NOK/SEK was triggered at parity. We were also stopped out of our long petrocurrency basket trade, which we will re-establish in the coming weeks. Feature Riot points in capital markets usually elicit a swathe of differing views. But more often than not, the internal dynamics of financial markets usually hold the key to a sober view. Given market action over the past few weeks, we are reviewing a few of the key indicators we look at for guidance on buying opportunities as well as false positives. In short, it is a story of standing aside on the DXY for now, while taking advantage of a few opportunities at the crosses. Currency Market Indicators Chart I-1The Dollar Has Scope To Rise Further

The Dollar Has Scope To Rise Further

The Dollar Has Scope To Rise Further

Many currency market signals continue to point to a higher DXY index for the time being. One of our favorite risk-on/risk-off pairs is the AUD/JPY cross. Not surprisingly, it tends to correlate very strongly with the dollar, which is a counter-cyclical currency. The AUD/JPY cross has consistently bottomed at the key support zone of 70-72 since the financial crisis. This defensive line held notably during the European debt crisis, China’s industrial recession, and more recently, the global trade war. The latest market moves have nudged it decisively lower (Chart I-1). This pins the next level of support in the 55-57 zone, at par with the recessions of 2001 and 2008. The yen appears headed towards 100. A rising yen is usually accompanied by a dollar rally against other procyclical currencies. Outside of the Fukushima crisis, this was a key indicator that the investment environment was becoming precarious (Chart I-2). We laid out our conviction last week as to why we thought 100 is the resting spot for the yen.1 That said, in our trades, our 104 profit target for short USD/JPY was hit this week. We are reinstating this trade with a target of 100, but tightening the stop to 105.4. Chart I-2The Yen Rally Usually Stalls At 100

THe Yen Rally Usuallyy Stalls At 100

THe Yen Rally Usuallyy Stalls At 100

The recent drop in the dollar is perplexing to most, but it fits the profile of most recessions we have had in recent history. As the world’s reserve bank, the Federal Reserve tends to be the most proactive during a crisis. This means US interest rates drop faster than in the rest of the world, which tends to pressure the dollar lower. Eventually, as imbalances in the economic system come home to roost, the dollar rallies (Chart I-3). 62% of global reserves are still in dollars, suggesting it remains the currency of choice in a crisis. Currencies such as the Norwegian krone and Swedish krona that were already quite cheap are still selling off indiscriminately. Granted, the Norwegian krone has been hit especially hard due to the fallout of the OPEC cartel. But the Swedish krona and Australian dollar that were equally cheap are selling off as well. This suggests the currency market is making a binary switch from fundamentals to sentiment, as we highlighted last week. Chart I-3The Dollar And ##br##Recessions

The Dollar And Recessions

The Dollar And Recessions

Chart I-4Carry Trades: Long-Term Bullish, Short-Term Cautious

Carry Trades: Long-Term Bullish, Short-Term Cautious

Carry Trades: Long-Term Bullish, Short-Term Cautious

Correspondingly, high-beta currencies such as the RUB/USD, ZAR/USD and BRL/USD are plunging into uncharted territory. These currencies are usually good at sniffing out a change in the investment landscape, specifically one becoming precarious for carry trades. The message so far is that the drop in US bond yields may not have been sufficient to make these currencies attractive again (Chart I-4). On a similar note, it is interesting that the USD/CNY is still holding near the 7-defense line. We suggested in a previous report that this represented a handshake agreement between President Xi and President Trump during the trade negotiations. Should USD/CNY break decisively above 7.15 (for example, if Trump’s reelection chances dwindle), it will send Asian currencies into the abyss. The velocity of asset price moves is both surprising and destabilizing. At this rate, previously solvent countries can rapidly step into illiquid territory, especially those with already huge levels of external debt. Granted, this is more a problem for emerging markets than for G10 currencies. So far, it is encouraging that cross-currency basis swaps for the dollar (a measure of currency hedging costs) remain muted (Chart I-5). Chart I-5Hedging Costs Remain Contained

Hedging Costs Remain Contained

Hedging Costs Remain Contained

In a nutshell, the message from currency markets warns against shorting the DXY for now. Bottom Line: Our profit target on short USD/JPY was hit at 104 this week. We are reinstating this trade with a new target of 100 and a stop-loss at 105.4. Currency market dynamics suggest the DXY is headed higher in the near term. The Message From Equity And Commodity Markets Equity and commodity market indicators continue to suggest the path of least resistance for the DXY remains up over the next few weeks. Since the 2009 lows, the S&P 500 has respected a well-defined upward-sloped trend line, characterized by a series of higher highs and lows. Given this defense line has been tested (and broken), it could pin the S&P 500 around 2200-2400 (Chart I-6). A further drop of this magnitude is likely to unravel financial markets as stop losses are triggered and reinforced selling is supercharged. Non-US equity markets have a much higher concentration of cyclical stocks in their bourses. Thus, whenever cyclical sectors are underperforming defensives at the same time as non-US markets are underperforming US ones, it is a clear sign that the marginal dollar is rotating towards the US (in this case fixed income). During the latest downdraft, what has been clear is that cyclical (and non-US) markets have been underperforming from already oversold levels (Chart I-7A and Chart I-7B). As contrarian investors, we tend to view this development positively, but catching a falling knife before eventual capitulation can also be quite painful. Chart I-6A Break Below The Defense Line Is Bearish

A Break Below The Defense Line Is Bearish

A Break Below The Defense Line Is Bearish

Chart I-7ANot A Bullish Configuration For Cyclical Currencies

Not A Bullish Configuration For Cyclical Currencies

Not A Bullish Configuration For Cyclical Currencies

Chart I-7BNot A Bullish Configuration For Cyclical Currencies

Not A Bullish Configuration For Cyclical Currencies

Not A Bullish Configuration For Cyclical Currencies

The 2015-2016 roadmap was instructive on when such a capitulation might occur. Even as the market was selling off, certain cyclical sectors such as industrials started to outperform defensives ones (Chart I-8). So far, it appears that selling pressure in cyclical markets have not yet been exhausted. Chart I-8Equity Market Internals Are Worrisome

Equity Market Internals Are Worrisome

Equity Market Internals Are Worrisome

In commodity markets, the copper-to-gold and oil-to-gold ratios continue to head lower from oversold levels. Together with the fall in government bond yields, it signifies that the liquidity-to-growth transmission mechanism is impaired (Chart I-9). The speed and magnitude of the latest drop could signify capitulation, but since the European debt crisis there has been ample time to catch the upswings, since they tend to be powerful and durable. Earnings revisions continue to head lower across all markets. Bottom-up analysts are usually spot on about the direction or earnings. Not surprisingly, the downgrades have been driven by emerging markets, meaning that return on capital will be lower in cyclical bourses. Chart I-9Commodity Market Internals Are Worrisome

Commodity Market Internals Are Worrisome

Commodity Market Internals Are Worrisome

A selloff in equity markets has tended to occur in cycles. The speed and intensity of the first selloff usually wipes out stale longs, especially those that bought close to the recent market peak. It is fair to assume with yesterday’s selloff that the process is near complete. The next wave comes from medium-term investors, making a judgment call on whether they are at the cusp of a recession. Unfortunately, this phase usually involves a cascading selloff with capitulation only evident a few weeks or months later. The fact that cheap and deeply oversold currencies like the Norwegian krone and Australian dollar are still falling suggests we are stepping into the second wave of selloffs. What remains peculiar about the dollar is that it continues to be whipsawed between relative fundamentals and sentiment. Bottom LIne: Equity market internals continue to suggest we have not yet hit a capitulation phase for pro-cyclical currencies. Stand aside on the DXY for now. On Interest Rates, The Euro, And Petrocurrencies Chart I-10The Bear Case For The US Dollar

The Bear Case For The US Dollar

The Bear Case For The US Dollar

What remains peculiar about the dollar is that it continues to be whipsawed between relative fundamentals and sentiment. For example, interest rate differentials across much of the developed world have risen versus the dollar, in stark contrast with the drop in their exchange rates (Chart I-10). The risk is that as a momentum currency, a surge in the dollar triggers a negative feedback loop that tightens global financial conditions, reinforcing the same negative feedback loop. A few questions we have fielded this week have been in surprise to the rise in the euro. What has been remarkable is that the drop in Treasury yields has wiped out the carry from being long the dollar for a number of countries. For example, the German bund-US Treasury spread continues to collapse. The message is that at least initially, room for policy maneuvering remains higher at the Fed, which corroborates the market view of a disappointing European Central Bank meeting this week. A drop in oil prices is also a huge dividend on the European economy, which partly explains recent strength in the euro. Within this sphere of multiple moving parts, one key question is what to do with oil plays. Usually recessions are triggered by rising oil prices that impose a tax on the domestic economy. But rather, oil prices have fallen dramatically in recent weeks as the pseudo-alliance between Russia and OPEC appears to have broken down. Our commodity and geopolitical strategists believe that while some sort of resolution will ultimately be reached, the path of least resistance for oil prices in the interim is down, as market share wars are re-engaged.2 Risks to oil demand are now also firmly tilted to the downside. Oil demand tends to follow the ebb and flows of the business cycle. Transport constitutes the largest share of global petroleum demand, and the rising bans on travel will go a long way in curbing consumption (Chart I-11). Balance-of-payment dynamics also tend to deteriorate during oil bear markets. Altogether, these forces combine to become powerful headwinds for petrocurrencies. A fall in oil prices tends to be bullish for the US dollar. This is because falling oil prices reduce government spending in oil-producing countries, which depresses aggregate demand and leads to easier monetary policy. Meanwhile, a fall in oil prices also implies falling terms of trade, which further reduces the fair value of the exchange rate. Balance-of-payment dynamics also tend to deteriorate during oil bear markets. Altogether, these forces combine to become powerful headwinds for petrocurrencies. Chart I-11Oil Demand Will Collapse Further

Oil Demand Will Collapse Further

Oil Demand Will Collapse Further

Chart I-12Resell CAD/NOK NOK Will Outperform CAD

Resell CAD/NOK NOK Will Outperform CAD

Resell CAD/NOK NOK Will Outperform CAD

We were stopped out of our long petrocurrency basket trade for a small loss of 0.9% (on the back of a positive carry). We are standing aside on this trade for now. We were also stopped out of our short CAD/NOK trade which we are reinstating this week. Further improvement in Canadian energy product sales will require not only rising oil prices, but an improvement in pipeline capacity and a smaller gap between Western Canadian Select (WCS) and Brent crude oil prices. With the US shale revolution grabbing production market share from both OPEC and non-OPEC producing countries, the divergence between the WCS (and WTI) price of oil versus Brent is likely to remain wide (Chart I-12). Rebuy NOK/SEK Our limit buy on long NOK/SEK was triggered at parity this week. Relative fundamentals, especially from an interest rate perspective, still favor the cross. The cross has approached an important technical level, with our intermediate-term indicator signaling oversold conditions. Should the NOK/SEK pattern of higher lows and higher highs in place since the 2015 bottom persist, we should be on the cusp of a reversal (Chart I-13). Interest rate differentials continue to favor the NOK over the SEK (Chart I-14). Meanwhile, Norway mainland GDP growth continues to outpace that of Sweden. Chart I-13Rebuy NOK/SEK Rebuy NOK/SEK

Rebuy NOK/SEK Rebuy NOK/SEK

Rebuy NOK/SEK Rebuy NOK/SEK

Chart I-14A Yield Cushion

A Yield Cushion

A Yield Cushion

The risk to this trade is that we have not yet seen a capitulation in oil prices. This will largely be driven by geopolitics. But given that the cross is already trading near the 2016 lows in oil prices, this has already largely been priced in. We are placing a tight stop at 0.94 to account for volatility in the coming weeks. Housekeeping Our short CHF/NZD trade briefly hit our stop loss of 1.75. We are reinstating this trade today, with a new entry level of 1.74 and a stop-loss of 1.76. We were also stopped out of our short USD/NOK trade, and we will look to rebuy the krone in the near future. Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Footnotes 1 Please see Foreign Exchange Strategy Weekly Report, titled “Are Competitive Devaluations Next?”, dated March 6, 2020, available at fes.bcaresearch.com. 2 Please see Commodity & Energy Strategy Special Report, titled “Russia Regrets Market-Share War?”, dated March 12, 2020, available at ces.bcaresearch.com. Currencies U.S. Dollar Chart II-1USD Technicals 1

USD Technicals 1

USD Technicals 1

Chart II-2USD Technicals 2

USD Technicals 2

USD Technicals 2

Recent data in the US have been positive: Nonfarm payrolls increased by 275 thousand and average hourly earnings grew by 3% year-on-year in February. The NFIB business optimism index ticked up to 104.5 in February. Core CPI grew by 2.4% year-on-year from 2.3% in February. The DXY index appreciated by 0.8% this week. Core inflation has consistently printed at or above 2% for the last two years, but with inflation expectations plunging to new lows, the February print is likely to mark an intermediate-term high in CPI. As a counter-cyclical currency, the DXY is likely to continue getting a bid in the near term, even if we get more aggressive stimulus from the Fed. Report Links: Are Competitive Devaluations Next? - March 6, 2020 The Near-Term Bull Case For The Dollar - February 28, 2020 On The DXY Breakout, Euro, And Swiss Franc - February 21, 2020 The Euro Chart II-3EUR Technicals 1

EUR Technicals 1

EUR Technicals 1

Chart II-4EUR Technicals 2

EUR Technicals 2

EUR Technicals 2

Recent data in the euro area have been mixed: GDP grew by 1% year-on-year in Q4 2019, from 0.9% in Q3. The Sentix investor confidence index plummeted to -17.1 from 5.2 in March. Industrial production grew by 2.3% month-on-month in January from a contraction of 1.8% in December. The euro appreciated by 0.5% against the US dollar this week. The European Central Bank (ECB) kept rates unchanged at its Thursday meeting but implemented measures that support bank lending to small and medium-sized enterprises and injected liquidity through longer-term refinancing operations. The ECB also introduced additional net asset purchases of EUR 120 billion until the end of the year. This will help ease financial conditions in the euro area, but until global demand picks up, the exodus of capital from cyclical European stocks could continue. Report Links: On The DXY Breakout, Euro, And Swiss Franc - February 21, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 On Money Velocity, EUR/USD And Silver - October 11, 2019 Japanese Yen Chart II-5JPY Technicals 1

JPY Technicals 1

JPY Technicals 1

Chart II-6JPY Technicals 2

JPY Technicals 2

JPY Technicals 2

Recent data in Japan have been negative: The current account surplus increased to JPY 612.3 billion from JPY 524 billion while the trade balance went into a deficit of JPY 985.1 billion from a surplus of JPY 120.7 billion in January. Machine tool orders contracted by 30.1% year-on-year in February. The outlook component of the Eco Watchers survey plummeted to 24.6 from 41.8. The Japanese yen appreciated by 2.2% against the US dollar this week. An increase in foreign investments boosted the current account surplus, helping offset the deficit in goods trade. The government announced a package totaling JPY 430.8 billion to support financing for small businesses squeezed by the virus. The sharp rally in the yen could begin to garner discussions from both the MoF and BoJ on further actions. Report Links: The Near-Term Bull Case For The Dollar - February 28, 2020 Building A Protector Currency Portfolio - February 7, 2020 Currency Market Signals From Gold, Equities And Flows - January 31, 2020 British Pound Chart II-7GBP Technicals 1

GBP Technicals 1

GBP Technicals 1

Chart II-8GBP Technicals 2

GBP Technicals 2

GBP Technicals 2

Recent data in the UK have been negative: GDP growth was flat month-on-month in January. Industrial production contracted by 2.9% year-on-year in January, from a contraction of 1.8% the previous month. The total trade balance shrank to GBP 4.2 billion from GBP 6.3 billion in January. The British pound depreciated by 2.2% against the US dollar this week. The Bank of England (BoE) responded to the Covid-19 shock with an emergency rate cut of 50 basis points. This dovetailed with the government’s announcement of a GBP 30 billion stimulus package financed largely by additional borrowing. With the policy rate at 0.25%, the BoE has ruled out negative rates so further easing will likely come in the form of QE if rates go to zero. Report Links: Updating Our Balance Of Payments Monitor - November 29, 2019 A Few Trade Ideas - Sept. 27, 2019 United Kingdom: Cyclical Slowdown Or Structural Malaise? - Sept. 20, 2019 Australian Dollar Chart II-9AUD Technicals 1

AUD Technicals 1

AUD Technicals 1

Chart II-10AUD Technicals 2

AUD Technicals 2

AUD Technicals 2

Recent data in Australia have been negative: The Westpac consumer confidence index fell to 91.9 from 95.9 in February, a five-year low. National Australia Bank business confidence decreased to -4 from -1 while business conditions fell to 0 from 2 in February. Home loans grew by 3.1% month-on-month in January, from 3.6% the previous month. The Australian dollar depreciated by 3.9% against the US dollar this week. The Australian government joined other economies in announcing a stimulus package worth more than $15 billion that includes an extension of asset write-offs and measures to protect apprenticeships across the country. Reserve Bank of Australia Deputy Governor Debelle confirmed that the bank would consider quantitative easing if necessary. Report Links: On AUD And CNY - January 17, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 A Contrarian View On The Australian Dollar - May 24, 2019 New Zealand Dollar Chart II-11NZD Technicals 1

NZD Technicals 1

NZD Technicals 1

Chart II-12NZD Technicals 2

NZD Technicals 2

NZD Technicals 2

Recent data in New Zealand have been negative: Manufacturing sales grew by 2.7% quarter-on-quarter in Q4 2019. The preliminary ANZ business confidence numbers plummeted to -53.3 from -19.4 in March. Export intentions, at -21.5, hit an all-time low in March. Electronic card retail sales grew by 8.6% year-on-year in February, picking up from 4.2% in January. The New Zealand dollar depreciated by 1.9% against the US dollar this week. The government is planning a business continuity package that will be ready in coming weeks. Reserve Bank of New Zealand Governor Orr stated that the bank would consider unconventional policy such as negative rates, interest rate swaps, and large scale asset purchases only if policy rates hit the effective zero bound. Report Links: Updating Our Balance Of Payments Monitor - November 29, 2019 Place A Limit Sell On DXY At 100 - November 15, 2019 USD/CNY And Market Turbulence - August 9, 2019 Canadian Dollar Chart II-13CAD Technicals 1

CAD Technicals 1

CAD Technicals 1

Chart II-14CAD Technicals 2

CAD Technicals 2

CAD Technicals 2

Recent data in Canada have been mixed: Average hourly earnings grew by 4.3% year-on-year and 30.3 thousand new jobs were added to the Canadian economy in February. Imports fell to CAD 49.6 billion, exports fell to CAD 48.1 billion, and the deficit in international merchandise trade swelled to CAD 1.47 billion in February. The Ivey PMI decreased to 54.1 from 57.3 on a seasonally-adjusted basis in February. The Canadian dollar depreciated by 3% against the US dollar this week. The petrocurrency sold off as oil plunged in its biggest decline since the Gulf War in 1991. Exports of motor vehicles and energy products were down, contributing to the widening deficit. Supply and demand factors are bearish for oil, which will put a floor under our long EUR/CAD trade. Report Links: The Loonie: Upside Versus The Dollar, But Downside At The Crosses Updating Our Balance Of Payments Monitor - November 29, 2019 Making Money With Petrocurrencies - November 8, 2019 Swiss Franc Chart II-15CHF Technicals 1

CHF Technicals 1

CHF Technicals 1

Chart II-16CHF Technicals 2

CHF Technicals 2

CHF Technicals 2

There were scant data out of Switzerland this week: The unemployment rate remained flat at 2.3% in February. Foreign currency reserves increased to CHF 769 billion from CHF 764 billion in February while total sight deposits ticked up to CHF 598.5 billion from CHF 503.6 billion in the week ended March 6. The Swiss franc appreciated by 0.7% against the US dollar this week. The franc was driven by safe-haven flows at the beginning of the week but sold off as the market posted a tentative rally. Sight deposit and reserve data suggest the Swiss National Bank (SNB) intervened to keep EUR/CHF above the key 1.06 level. The ECB’s decision to hold rates will take some pressure off the SNB. Report Links: On The DXY Breakout, Euro, And Swiss Franc - February 21, 2020 Currency Market Signals From Gold, Equities And Flows - January 31, 2020 Portfolio Tweaks Before The Chinese New Year - January 24, 2020 Norwegian Krone Chart II-17NOK Technicals 1

NOK Technicals 1

NOK Technicals 1

Chart II-18NOK Technicals 2

NOK Technicals 2

NOK Technicals 2

Recent data in Norway have been negative: Headline CPI grew by 0.9% from 1.8% while the core figure grew by 2.1%, slowing from 2.9%, in February. Manufacturing output contracted by 1.4% month-on-month in January. The PPI contracted by 7.4% year-on-year in February, deepening the contraction of 3.9% the previous month. The Norwegian krone depreciated by 8.2% against the US dollar this week. As expected, the currency was hit hard by tumbling oil prices. The government is set to present emergency measures which will target bankruptcies and layoffs in sectors hit hard by Covid-19, such as airlines, hotels, and parts of the manufacturing industry. There may also be scope for the government to directly stimulate demand in the oil industry. Report Links: Building A Protector Currency Portfolio - February 7, 2020 On Oil, Growth And The Dollar - January 10, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 Swedish Krona Chart II-19SEK Technicals 1

SEK Technicals 1

SEK Technicals 1

Chart II-20SEK Technicals 2

SEK Technicals 2

SEK Technicals 2

There were scant data out of Switzerland this week: The current account surplus shrank to SEK 39 billion from SEK 65 billion in Q4 2019. The Swedish krona depreciated by 3% against the US dollar this week. The Swedish government announced a SEK 3 billion supplementary budget bill to combat the shock from Covid-19, in addition to preexisting tax credits and an extra SEK 5 billion promised to local authorities in the upcoming spring mini-budget. Riksbank Governor Ingves emphasized the need to maintain liquidity via more generous terms for loans to banks or direct purchases of securities. A rate cut, however, does not seem to be on the table. Report Links: Updating Our Balance Of Payments Monitor - November 29, 2019 Where To Next For The US Dollar? - June 7, 2019 Balance Of Payments Across The G10 - February 15, 2019 Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Limit Orders Closed Trades

Highlights China is moving from virus containment to normalization and economic stimulus. The full weight of the virus panic is only now hitting the US public and has not yet peaked. The US – and western democracies in general – have the raw capabilities to manage the virus outbreak. The profile of global political risk is shifting as a result of the economic shock stemming from the virus. This implies that while equity markets are close to their bottom, they face more volatility. Feature Chart 1No Peak In New Cases Outside China

Can Democracies Manage The Virus?

Can Democracies Manage The Virus?

China’s President Xi Jinping visited Wuhan, the epicenter of the coronavirus breakout that has triggered a global bear market, on March 10. While he did not declare outright victory over the virus, his symbolic visit reinforced the fact that China has drastically reduced the number of new daily cases both within and without Hubei province. Meanwhile the virus is spreading rapidly across the rest of the world (Chart 1). It is not clear if the outbreak and emergency response in the United States will follow the Italian or South Korean trajectory. The initial US response is not encouraging, but the US has latent institutional strengths. Either way the US is facing a tsunami of new cases in the very near term. Hence the panic among the American population can still escalate from here (Chart 2). Panic among households translates to a drop in economic activity that will ensure financial markets remain volatile, even if US equities are close to their bottom. Chart 2US Public Panic Has Not Peaked Yet

Can Democracies Manage The Virus?

Can Democracies Manage The Virus?

Can Democracies Manage The Crisis? Chart 3Developed Economies Have Better Health

Can Democracies Manage The Virus?

Can Democracies Manage The Virus?

The question has become salient because of the poorly managed cordon sanitaire in Italy and the slow and halting initial reaction of the United States. Moreover, to distract from China’s domestic crisis, the Communist Party has turned up the volume of its propaganda organs, advertising the success of China’s draconian containment measures and warning that the virus cannot be contained if the rest of the world does not follow suit. However, it is not the case that the pandemic can only be managed through absolutist policies. To date, developed economies and democracies – including westernized countries like Japan – have the best record in the world of improving public health and reducing mortality from infectious diseases. This is apparent simply by looking at life expectancy for those aged 60. Europe and Japan have the longest lives beyond 60, including extension of life when dealing with late-life health problems, while other regions lag, including Asia. The United States is on the low end of the developed countries but still considerably better than emerging market economies at prolonging life, even for unhealthy elderly folks (Chart 3). Chart 4US Has Reduced Flu/Pneumonia Deaths Dramatically

Can Democracies Manage The Virus?

Can Democracies Manage The Virus?