Europe

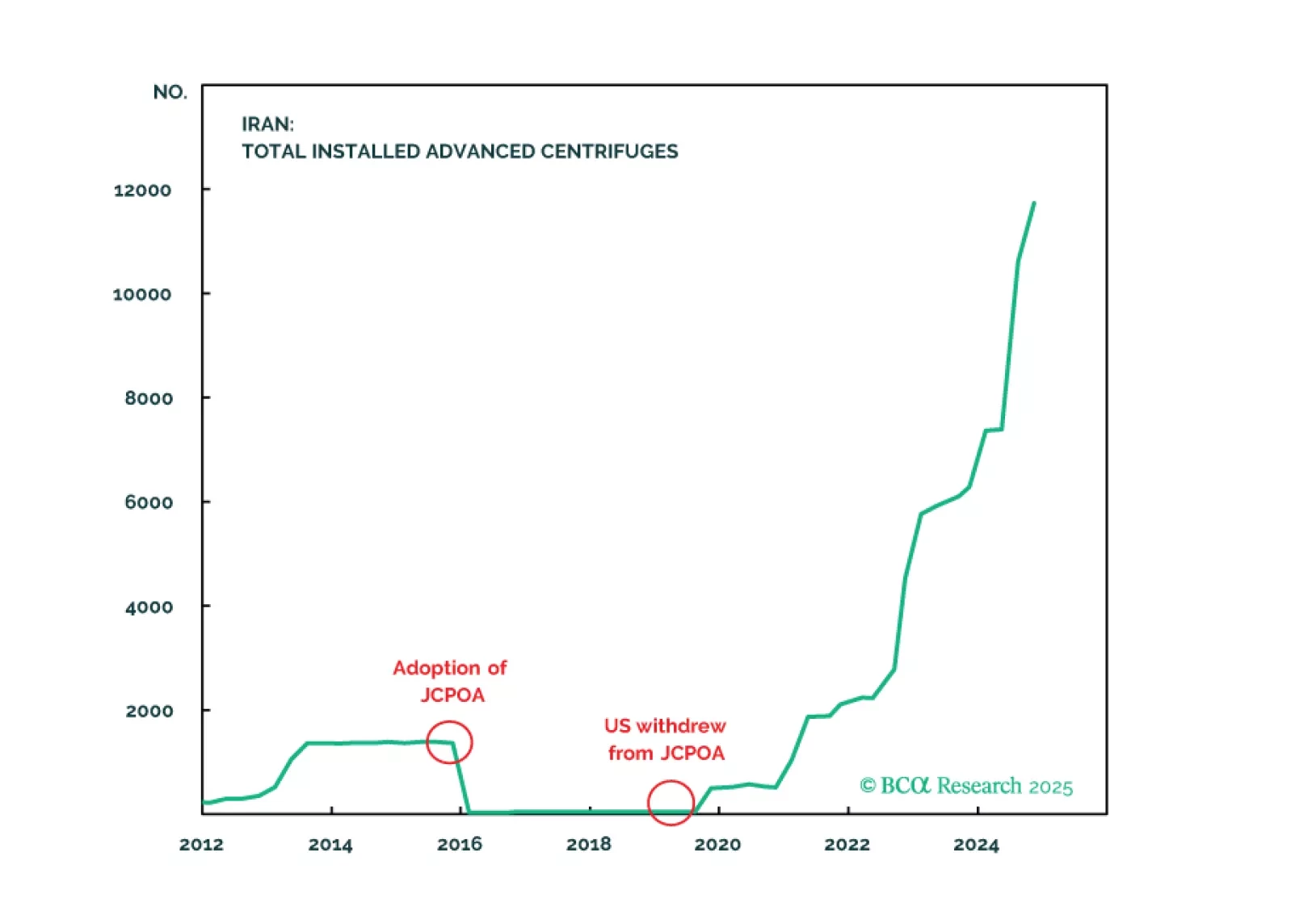

Every year we highlight five low-odds scenarios that would have a major impact on global financial markets if they happened. This year we contemplate a total reversal of Chinese policy, a US-Iran nuclear deal, a breakdown of NATO, US military action across the Americas, and an internationally coordinated FX intervention.

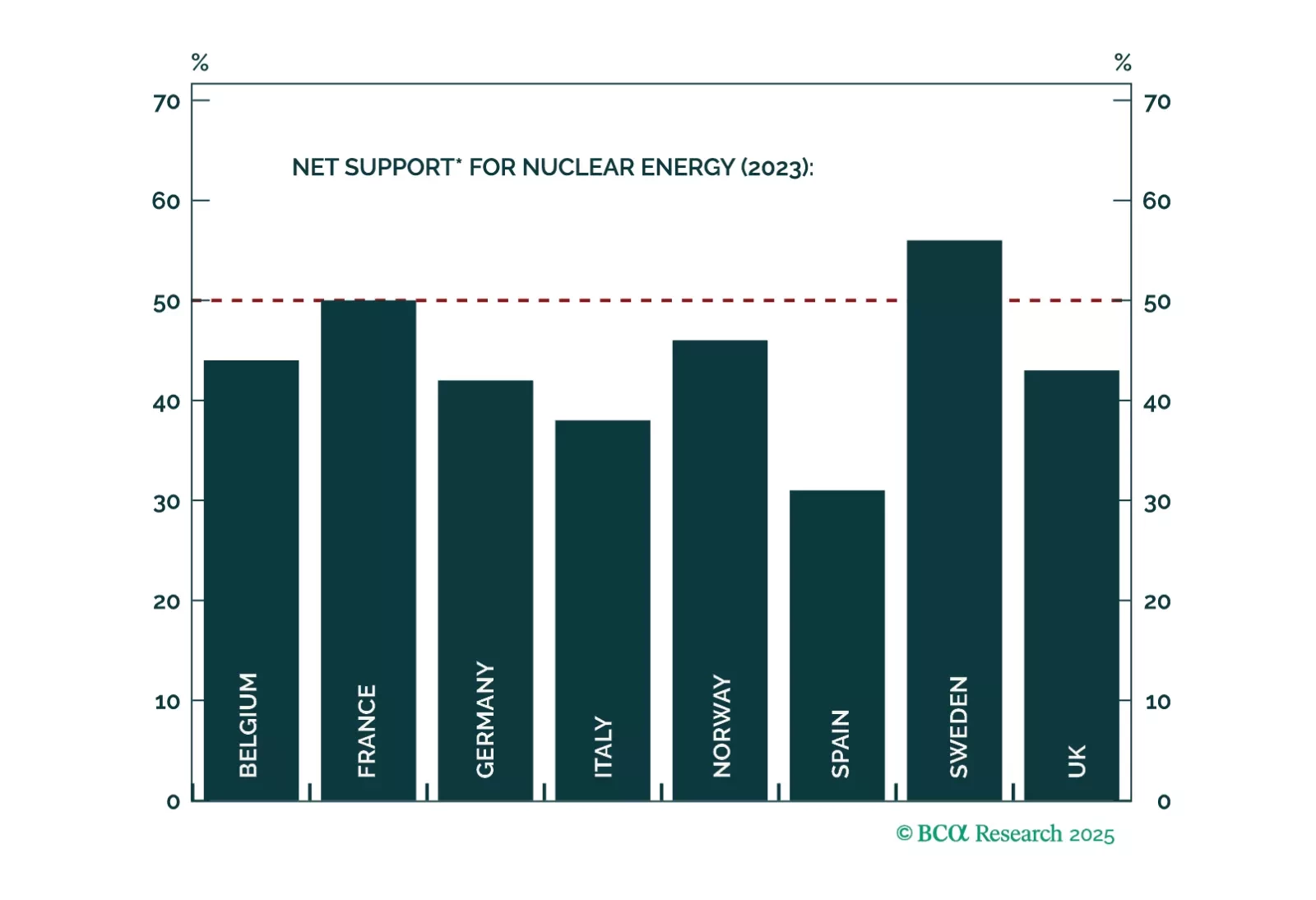

This report takes you on a tour of Europe’s nuclear energy industry, assessing its current situation and possible future.

Paradoxically, raging optimism on the US economy is making a reacceleration in growth less likely in 2025. The reaction of the bond market has made the Fed rethink its cutting campaign. Markets are also constraining Trump’s agenda. US manufacturing will not recover with a surging dollar. Fears of inflation and debt sustainability have made moderate House Republicans push back against the President Elect’s wishes. Given the sky-high optimism embedded in asset prices, we believe a defensive portfolio stance is warranted on a 12-month horizon. Overweight gold to hedge the risk of a fiscal crisis.