Europe

Highlights Buy the pound as soon as the U.K. parliament coalesces a majority around an action plan to counter a no-deal Brexit. For equity investors the best play is a FTSE Small Company Index ETF and/or U.K. REITS. Beaten-down banks, industrials and materials can continue their recent countertrend outperformances. This necessarily means that the cyclical-heavy Eurostoxx50 can continue its recent countertrend outperformance versus the S&P500. Go overweight industrials versus utilities as a tactical trade. Feature Chart of the WeekWere It Not For Brexit, U.K. Interest Rates Would be 1 Percent Higher

Were It Not For Brexit, U.K. Interest Rates Would be 1 Percent Higher

Were It Not For Brexit, U.K. Interest Rates Would be 1 Percent Higher

Please join me for a webcast today at 10.00 AM EST (3.00 PM GMT, 4.00 PM CET, 11.00 PM HKT) when I will be elaborating on some of the ideas in this report as well as other major investment themes. For those of you who cannot participate live, the webcast will also be available as a playback. Were it not for the psychodrama called Brexit, the pound would be trading at $1.50 rather than at $1.28. We can say this with utmost confidence because ‘cable’ is very closely tracking the difference in 2-year interest rates in the U.K. versus the U.S. Absent the Brexit shenanigans, U.K. interest rates would be around 1 percent closer to those in the U.S., implying that pound/dollar would be around 15 percent higher ( Chart I-2 and Chart I-3 ). Chart I-2Absent The Brexit Discount On U.K. Interest Rates...

Absent The Brexit Discount On U.K. Interest Rates...

Absent The Brexit Discount On U.K. Interest Rates...

Chart I-3...The Pound Would Be At $1.50

The Pound Would Be At $1.50

The Pound Would Be At $1.50

Explaining Brexit’s Impact On U.K. Interest Rates And The Pound The difference in U.K. versus U.S. interest rates usually tracks the difference in their inflation rates, in effect equalizing real interest rates in the two economies. But the Brexit referendum in 2016 forced the Bank of England into an ‘emergency monetary policy’ mode, whereby interest rates were left depressed relative to the inflation fundamentals, and U.K. real interest rates collapsed. Applying the BoE’s pre-Brexit reaction function to the current inflation dynamics, U.K. interest rates – and therefore the pound – would be in a completely different ballpark. After all, U.K. and U.S. core inflation rates and unemployment rates are virtually identical ( Chart of the Week ). It follows that the pound’s trajectory will be higher in any negotiated Brexit – or indeed ‘no Brexit’ – which avoids a complete and overnight no-deal divorce. The simple reason is that a transition period lasting several years that continues to give the U.K. access to the EU single market will allow the BoE to revert to its pre-Brexit monetary policy reaction function. But any workable alternative to a no-deal Brexit must satisfy two conditions: the way forward must be acceptable to the EU27; and it must command a majority in the U.K. parliament. From the perspective of investors, what this way forward turns out to be – Common Market 2.0, permanent customs union, second referendum, or general election – does not really matter. What matters is that a parliamentary majority exists for a course of action that avoids no-deal. The investment strategy is to buy the pound as soon as the U.K. parliament coalesces a majority around an action plan to counter a no-deal Brexit . In this event, do not buy the FTSE100. Whenever the pound strengthens, the weaker translation of the FTSE100 companies’ dollar-denominated earnings tends to weigh down this large-cap index. A better play is the FTSE250 mid-cap index ( Chart I-4 ), but for equity investors t he best play is a FTSE Small Company Index ETF and/or U.K. REITS ( Chart I-5 ). Chart I-4A Negotiated Brexit Would Favour The FTSE250...

A Negotiated Brexit Would Favour The FTSE250...

A Negotiated Brexit Would Favour The FTSE250...

Chart I-5...And U.K. Small Companies

...And U.K. Small Companies

...And U.K. Small Companies

Europeans Are Celebrating Lower Oil Europeans will be celebrating the near halving of the crude oil price from its $86 high just three months ago. The simple reason is that Europeans are net importers of energy, and the amount of energy they consume tends to be price inelastic. After all, Europeans have to do the school run and stay warm in winter, irrespective of the oil price. Hence, when energy prices soar as they did for most of 2018, it squeezes European real spending. Conversely, when energy prices plunge as they have more recently, it boosts real spending ( Chart I-6 ). A second transmission mechanism is via credit creation: higher inflation, through its implication for tighter monetary policy, lifts bond yields and depresses credit impulses; lower inflation does the opposite, it depresses bond yields and lifts credit impulses. The upshot is that higher oil weighed on European growth in 2018 while lower oil should boost growth in early 2019. Chart I-6Inflation Is Likely To Plunge, Boosting Real Incomes

Inflation Is Likely To Plunge, Boosting Real Incomes

Inflation Is Likely To Plunge, Boosting Real Incomes

Compelling proof comes from the oscillations in the euro area economy. For several years, these growth oscillations have perfectly and inversely tracked oscillations in the oil price ( Chart I-7 ). The economic implication is that the recent collapse in energy prices should engineer some sort of growth rebound in the euro area. The investment implication is that such a growth rebound will support the classically cyclical equity sectors – banks, industrials and materials – because of their very high operational leverage to economic growth. Chart I-7Euro Area Growth Oscillations Inversely Track Oil Price Oscillations

Euro Area Growth Oscillations Inversely Track Oil Price Oscillations

Euro Area Growth Oscillations Inversely Track Oil Price Oscillations

Profit is a small number created from the difference between two large numbers: sales minus the cost of generating those sales. But the dominant cost – the wage bill – tends to be quite sticky. Hence, if a company’s sales are highly sensitive to the economy, the power of operational leverage means that a small change in GDP can have a dramatically large proportional impact on profit. This is a simple principle, but it turns out to be an excellent explanation for the Eurostoxx50 earnings per share (eps) cycle. Because the index is dominated by the classically economic-sensitive sectors, Eurostoxx50 eps growth has a very high operational leverage to changes in euro area GDP growth, potentially as high as 50 times over short periods such as six months ( Chart I-8 ). In contrast the less cyclical S&P500 has an operational leverage to economic growth of less than 10 ( Chart I-9 ). Chart I-8Eurostoxx50 Profits Growth Is Highly Geared To Economic Growth

Eurostoxx50 Profits Growth Is Highly Geared To Economic Growth

Eurostoxx50 Profits Growth Is Highly Geared To Economic Growth

Chart I-9S&P500 Profits Growth Is Less Geared To Economic Growth

S&P500 Profits Growth Is Less Geared To Economic Growth

S&P500 Profits Growth Is Less Geared To Economic Growth

On the expectation that euro area growth will rebound modestly in early 2019, the beaten-down banks, industrials and materials can continue their recent countertrend outperformances. And this necessarily means that the cyclical-heavy Eurostoxx50 can continue its recent countertrend outperformance versus the S&P500. Explaining The ‘Unexplainable’ Moves In Markets During the recent Christmas holiday period, financial markets experienced sharp moves with no explainable catalyst. Such reversals leave many strategists and analysts scratching their heads in bewilderment, wondering: what was the catalyst for that reversal? The answer is there was no fundamental catalyst; the market reversed because liquidity dried up . But to explain why liquidity dried up and markets ‘unexplainably’ reversed, we first need to understand what creates market liquidity in the first place. Market liquidity is the ability to convert cash into an investment quickly and in volume without affecting its price. But for an investor to convert a large amount of cash into an investment without affecting its price, another investor must be willing to do the exact opposite – convert a large amount of the investment into cash at the given price. Therefore, market liquidity comes from a disagreement about the attractiveness of an investment at that given price. Investors disagree about the attractiveness of an investment at a given price because investors with different time horizons interpret the same facts and information very differently. Hence, a market remains stable when it possesses investors with many different time horizons. The reason is that when a day-trader experiences a ‘six-sigma’ price move, an investor with a longer investment horizon, for example 65 days, will step in and stabilize the market. The longer-term investor will do so because, within his investment horizon, the day-trader’s six-sigma price move is not unusual. As long as another investor has a longer trading horizon than the investor experiencing an extreme event, the market will stabilize itself. Therefore, the market’s liquidity and stability are maximized when its participants possess a variation of investment horizons, say, both the 1 day horizon and the 65 day horizon. The corollary is that the market’s liquidity and stability disappear when its participants no longer possesses this healthy variation in horizons. In technical terms, this occurs when the market’s 65-day fractal dimension collapses to its lower bound. Without a shadow of a doubt, this is what happened to the S&P500 on Christmas Eve and triggered a 5 percent market rebound on Boxing Day ( Chart I-10 ). And this is now what is happening to the relative performance of industrials versus utilities, which is also in the process of a similar liquidity-triggered rebound ( Chart I-11 ). Chart I-10A Liquidity Shortage Triggered A Sharp Rebound In The S&P500

A Liquidity Shortage Triggered A Sharp Rebound In The S&P500

A Liquidity Shortage Triggered A Sharp Rebound In The S&P500

Chart I-11Expect A Liquidity-Triggered Rebound In Industrials Versus Utilities

Expect A Liquidity-Triggered Rebound In Industrials Versus Utilities

Expect A Liquidity-Triggered Rebound In Industrials Versus Utilities

Fractal Trading System* This week we note that the strong rally in the Indian rupee versus the Pakistan rupee has reached a point where an imminent liquidity shortage could trigger a countertrend move. Go short the Indian rupee versus the Pakistan rupee with a profit target of 3 percent, and a symmetrical stop-loss. For any investment, excessive trend following and groupthink can reach a natural point of instability, at which point the established trend is highly likely to break down with or without an external catalyst. An early warning sign is the investment’s fractal dimension approaching its natural lower bound. Encouragingly, this trigger has consistently identified countertrend moves of various magnitudes across all asset classes. Chart I-12

Short Indian rupee versus Pakistan rupee

Short Indian rupee versus Pakistan rupee

The post-June 9, 2016 fractal trading model rules are: When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. Use the position size multiple to control risk. The position size will be smaller for more risky positions. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com Dhaval Joshi , Senior Vice President Chief European Investment Strategist dhaval@bcaresearch.com Fractal Trading System Recommendations Asset Allocation Equity Regional and Country Allocation Equity Sector Allocation Bond and Interest Rate Allocation Currency and Other Allocation Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights Global Corporates: The Fed is now clearly signaling a near-term capitulation to tightening financial conditions alongside slowing global growth and inflation. A pause in the U.S. rate hiking cycle, after credit spread valuations have cheapened up, opens up a window of opportunity for global corporate bond market outperformance versus government debt over the next 3-6 months. Country Allocation: Move to overweight (4 of 5) on both U.S. investment grade and high-yield corporates, while downgrading U.S. Treasuries to underweight (2 of 5). Upgrade euro area investment grade and high-yield corporates to neutral (3 of 5), while downgrading euro area governments to underweight (2 of 5). Upgrade emerging market U.S. dollar denominated debt (both sovereign and corporate) from maximum underweight to underweight (2 of 5). Feature We downgraded our overall recommended investment stance on global corporate debt to neutral on June 26 of last year.1 That decision reflected our concern at the time that less accommodative central banks, a rising U.S. dollar, weakening global growth momentum and intensifying U.S.-China trade tensions had all significantly worsened the near-term risk/reward tradeoff for owning corporate bonds. This accompanied a firm-wide call at BCA to pare back our recommended exposure to global equities for the same reasons. We now see an opportunity, driven by better value and diminished market volatility after the Fed has clearly signaled a pause on U.S. rate hikes (Chart of the Week), to go back to an overweight stance on corporate credit on a tactical basis (3-6 months). Chart of the WeekTime For A Pause In Corporate Spread Widening

Time For A Pause In Corporate Spread Widening

Time For A Pause In Corporate Spread Widening

To be clear, we still see medium-term risks for corporate credit once global growth stabilizes and a resilient U.S. economy forces the Fed to restart the rate hikes in the latter half of 2019. A move to a restrictive stance by the Fed toward year-end, signaled by an inversion of the U.S. Treasury yield curve, will raise recession risks and be the eventual death knell for this credit cycle. In the meantime, corporate debt is likely to outperform government bonds, justifying a tactical overweight position. This mirrors the recent change in the BCA House View, returning to a tactical overweight stance on global equities. On a regional basis, we prefer taking more of our upgraded credit risk in U.S. corporates over European and emerging market (EM) equivalents. The outlook for growth remains more favorable on a relative basis to Europe or China, the latter being most critical for the outperformance of EM assets. Why The Spread Widening Will Pause: A Patient Fed Is Taking A Break Global corporate bond spreads have widened since we did our downgrade in June, across all countries and credit tiers (Chart 2). Typically, some underperformance of corporate credit should occur when global growth momentum slows, as was the case throughout 2018. Yet the most violent period of spread widening only began once the Fed began signaling that it would continue with its interest hikes and balance sheet runoff, despite softening global growth.

Chart 2

This set off yet another clash between policy and the markets – one of BCA’s key investment themes for 2018 that still applies in 2019 – resulting in a sharp selloff in global risk assets, including corporate debt. The result was a tightening of U.S. financial conditions, first through a stronger U.S. dollar (supported by rate hike expectations) and later through lower equity prices and wider corporate spreads. This echoed the 2014/15 period when the Fed was trying to lift rates off the zero bound after ending its quantitative easing program. The Fed was only able to deliver a single rate hike in December 2015 before pausing because of severely slumping global growth (most notably in China) and a sharp tightening in financial conditions, both of which knocked the wind out of the U.S. economy. Turning to 2019, the downturn in cyclical growth indicators like manufacturing purchasing managers indices (PMI) and the global leading economic indicator (LEI) has reached levels last seen after that 2014/15 episode (Chart 3). Importantly, our global LEI diffusion index, which measures the number of countries with rising LEIs compared to falling LEIs and is itself a reliable leading indicator of the global LEI, is bottoming out at the same level that preceded the 2016 LEI revival (middle panel). This suggests that a stabilization of the global LEI could unfold in the next few months, which would also signal a potential rebound in corporate credit returns (bottom panel). Chart 3Credit Returns Already Reflect Slowing Growth

Credit Returns Already Reflect Slowing Growth

Credit Returns Already Reflect Slowing Growth

Given the many similarities between today and the 2014/15 backdrop, it is sensible to look for other indicators that accurately heralded the end of that period of spread widening to help time a potential increase in recommended exposure to corporates. Over the past several weeks, our colleagues at our sister BCA service, U.S. Bond Strategy, have been following a checklist of market-based signals to determine the timing of a potential peak in U.S. credit spreads.2 These are grouped into two categories: signals of rebounding global growth and signals of Fed capitulation on rate hikes. For global growth, the indicators monitored are shown in Chart 4: Chart 4Checklist For Peak U.S. Spreads: Global Growth

Checklist For Peak U.S. Spreads: Global Growth

Checklist For Peak U.S. Spreads: Global Growth

the CRB raw industrials index of commodity prices (a broader measure that excludes highly volatile oil prices) the BCA Market-Based China Growth Indicator (created by our China Investment Strategy team as a proxy of investor expectations of Chinese growth3) the Global Industrial Mining equity price index For Fed capitulation, the indicators monitored are shown in Chart 5: Chart 5Checklist For Peak U.S. Spreads: Fed Capitulation

Checklist For Peak U.S. Spreads: Fed Capitulation

Checklist For Peak U.S. Spreads: Fed Capitulation

our 12-month fed funds discounter, which measures the amount of expected Fed rate hikes over the next year discounted in the U.S. Overnight Index Swap (OIS) curve the price of gold in dollars (a higher price correlating with perceptions of easier U.S. monetary policy and vice versa) the nominal trade-weighted U.S. dollar index Among the growth-focused elements of the checklist, only the China Growth Indicator is in a clear uptrend. Non-oil commodity prices had been stabilizing at the end of 2018 but appear to be rolling over, while it is not yet clear if the downturn in Mining stocks has ended. With momentum in global PMIs and LEIs still having not yet bottomed out, it may be too early to expect a cyclical rebound in non-oil commodities and related equities. At a minimum, that will require even greater signs that China’s economy is regaining some vigor. However, as we discussed last week, Chinese policymakers’ options to stimulate growth are far more limited now than they were in 2015 and 2016 when a rebounding China boosted commodity demand and EM asset performance.4 Within the Fed-focused components of the “Peak Spreads Checklist”, the near-term bullish signal for credit is much stronger. Our fed funds discounter has rapidly priced out all rate hikes for 2019. Since November, gold is up nearly 8% and the nominal trade-weighted U.S. dollar is down 2%. The shift in recent Fed messaging from signaling a “gradual pace” of tightening to exhibiting “patience” on any future policy moves was a highly dovish signal for investors. This alone has been enough to stabilize equity and credit markets, which had been discounting that Fed tightening in 2019 would drive the U.S. into a possible recession. In the constant battle between financial conditions and the Fed, the former has won this latest round. How long will this Fed pause last? Continuing with the comparison to the 2014/15 episode, a critical difference is that underlying trends in U.S. economic growth and inflation are firmer today. This is evident in the BCA Fed Monitor, which is comprised of economic and financial data that indicate pressure on the Fed to tighten or ease monetary policy. Chart 6 shows a “cycle-on-cycle” comparison of the Fed Monitor (and its subcomponents) today versus 2014/15. The Fed Monitor is still signaling a need for the Fed to continue tightening because the Economic Growth and Inflation Components remain elevated. Yet the Monitor has declined from its recent peak thanks entirely to the plunge in the Financial Conditions Component, which has fallen even faster than it did in 2014/15. Chart 6BCA Fed Monitor: Today Vs 2014/15

BCA Fed Monitor: Today Vs 2014/15

BCA Fed Monitor: Today Vs 2014/15

The implication from our Fed Monitor is that there needs to be more evidence of slowing U.S. economic growth and reduced inflation pressures for the Fed to stay on hold for longer. If the data stay firm, but financial conditions ease because investors expect a prolonged pause from the Fed, then the Fed could quickly return to a hawkish bias later this year. This is now our base case scenario for how 2019 will play out. This is also why we are only upgrading corporate debt on a tactical basis. We do not expect U.S. growth or inflation to slow enough to prevent more Fed tightening later this year – an outcome that will weigh on credit returns as the Fed moves to a restrictive policy stance. Yet even if we are wrong and the U.S. economy decelerates more sharply, that is also a bad outcome for credit because it means weaker corporate profits and rising downgrades and defaults. For bond investors with longer-time horizons than 3-6 months, the credit rally that we are anticipating can actually provide an opportunity to reduce credit exposure for the final leg of the Fed’s monetary policy cycle and the multi-year corporate credit cycle. In other words, selling into the rally rather than chasing it. For now, we are choosing to play for the shorter-term move by upgrading our recommended global credit allocations. Yet we do not envision this turning into a long-term position. The medium-term outlook for corporates is far more challenging given the advanced age of the monetary, business and credit cycles. Bottom Line: The Fed is now clearly signaling a near-term capitulation to tightening global financial conditions alongside slowing global growth and inflation. A pause in the U.S. rate hiking cycle, after credit spread valuations have cheapened up, opens up a window of opportunity for global corporate bond market outperformance versus government debt over the next 3-6 months. The Specific Changes To Our Recommended Asset Allocation As part of our tactical upgrade of global corporate debt, we are making the following changes to our recommended portfolio allocation tables (see Page 13): Upgrade overall global credit exposure to overweight (4 out of 5) Upgrade both U.S. investment grade and high-yield corporate exposure to overweight (4 out of 5), while downgrading U.S. Treasury exposure to underweight (2 out of 5) Upgrade euro area investment grade and high-yield corporate exposure to neutral (3 out of 5) and downgrade euro area government bond exposure to underweight (2 out of 5) Upgrade EM U.S. dollar denominated debt from maximum underweight to underweight (2 out of 5), both for sovereign and corporate debt. The changes all represent a one-notch upgrade from our previous allocations, based on our more positive tactical view on overall global credit risk, while still maintaining our relative preference for U.S. corporates over non-U.S. equivalents. We prefer U.S. credit not only because we expect better relative economic growth momentum in the U.S., but also because our preferred valuation metrics indicate that U.S. corporate bond spreads now look relatively attractive. Our estimate of the default-adjusted spread on U.S. high-yield corporates, which is simply the current spread minus losses from defaults, has risen to 302bps, well above the long-run average of 268bps (Chart 7). That is a function of the high-yield spread now discounting a 2019 default rate of nearly 6%, well above our forecasted default rate of 2.5%.5 Chart 7Too Much Default Risk Priced Into U.S. Junk

Too Much Default Risk Priced Into U.S. Junk

Too Much Default Risk Priced Into U.S. Junk

Corporate credit spreads in the U.S. also look attractive on a volatility-adjusted basis. Our estimates of Breakeven Spreads – the amount of spread widening required for corporate returns to break-even with duration-matched U.S. Treasuries on a one-year horizon – shows that credit spreads have cheapened to levels that are in the upper end of the historical range for both investment grade and high-yield debt (Charts 8 & 9). Chart 8Vol-Adjusted IG Spreads Have Cheapened

Vol-Adjusted IG Spreads Have Cheapened

Vol-Adjusted IG Spreads Have Cheapened

Chart 9Vol-Adjusted HY Spreads Are Cheap

Vol-Adjusted HY Spreads Are Cheap

Vol-Adjusted HY Spreads Are Cheap

Credit spreads have also cheapened up in Europe and EM, and a “risk-on” rally from a Fed pause will likely benefit spread product in those regions. However, the performance of U.S. credit versus non-U.S. credit remains largely determined by relative growth trends (Charts 10 & 11). Given our more positive view on U.S. growth on a relative basis, we are maintaining a higher recommended allocation to U.S. corporates versus euro area and EM equivalents, even as we upgrade overall global corporate exposure. This is also a way to provide a partial hedge to the specific risks in the latter regions coming from: Chart 10Global Corporates: Continue Favoring U.S. Over Europe

Global Corporates: Continue Favoring U.S. Over Europe

Global Corporates: Continue Favoring U.S. Over Europe

Chart 11Global Corporates: Continue Favoring U.S. Over EM

Global Corporates: Continue Favoring U.S. Over EM

Global Corporates: Continue Favoring U.S. Over EM

a) an end of the ECB’s corporate bond buying as part of its Asset Purchase Program, which takes a major buyer out of the euro area corporate market b) a more persistent slowing of Chinese growth momentum and softer non-oil commodity prices, both of which would be negatives for EM assets On a final note, we are also changing the specific weighting in our Model Bond Portfolio on Page 12 to reflect all of the above changes. The allocations to all U.S., euro area and EM corporates are increased – with bigger allocation changes in the U.S. – funded out of reduced weightings in U.S., German and French government bonds. Note that we are not making any changes to our relative U.K. exposures this week, given the unique risk for U.K. financial markets from the Brexit uncertainty. Thus, we are maintaining an overweight stance on U.K. Gilts in the government bond portion of the model portfolio, while remaining underweight U.K. corporates on the credit side. Robert Robis, CFA, Senior Vice President Global Fixed Income Strategy rrobis@bcaresearch.com Footnotes 1 Please see BCA Global Fixed Income Strategy Weekly Report, “Time To Take Some Chips Off The Table: Downgrade Global Corporate Bond Exposure To Neutral”, dated June 26th 2018, available at gfis.bcaresearch.com. 2 Please see BCA U.S. Bond Strategy Weekly Report, “A Checklist For Peak Credit Spreads”, dated November 27th 2018, available at usbs.bcaresearch.com. 3 Please see BCA China Investment Strategy Weekly Report, “Trade Is Not China’s Only Problem”, dated November 21st 2018, available at cis.bcaresearch.com. 4 Please see BCA Global Fixed Income Strategy Weekly Report, “Three Big Questions To Start Off 2019”, dated January 8th 2019, available at gfis.bcaresearch.com. 5 That forecasted default rate is taken from Moody’s, who have a similarly positive outlook on 2019 U.S. growth as BCA. Therefore, we see no reason to use a different default rate assumption in our high-yield valuation estimate. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Enough With The Gloom: Upgrade Global Corporates On A Tactical Basis

Enough With The Gloom: Upgrade Global Corporates On A Tactical Basis

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

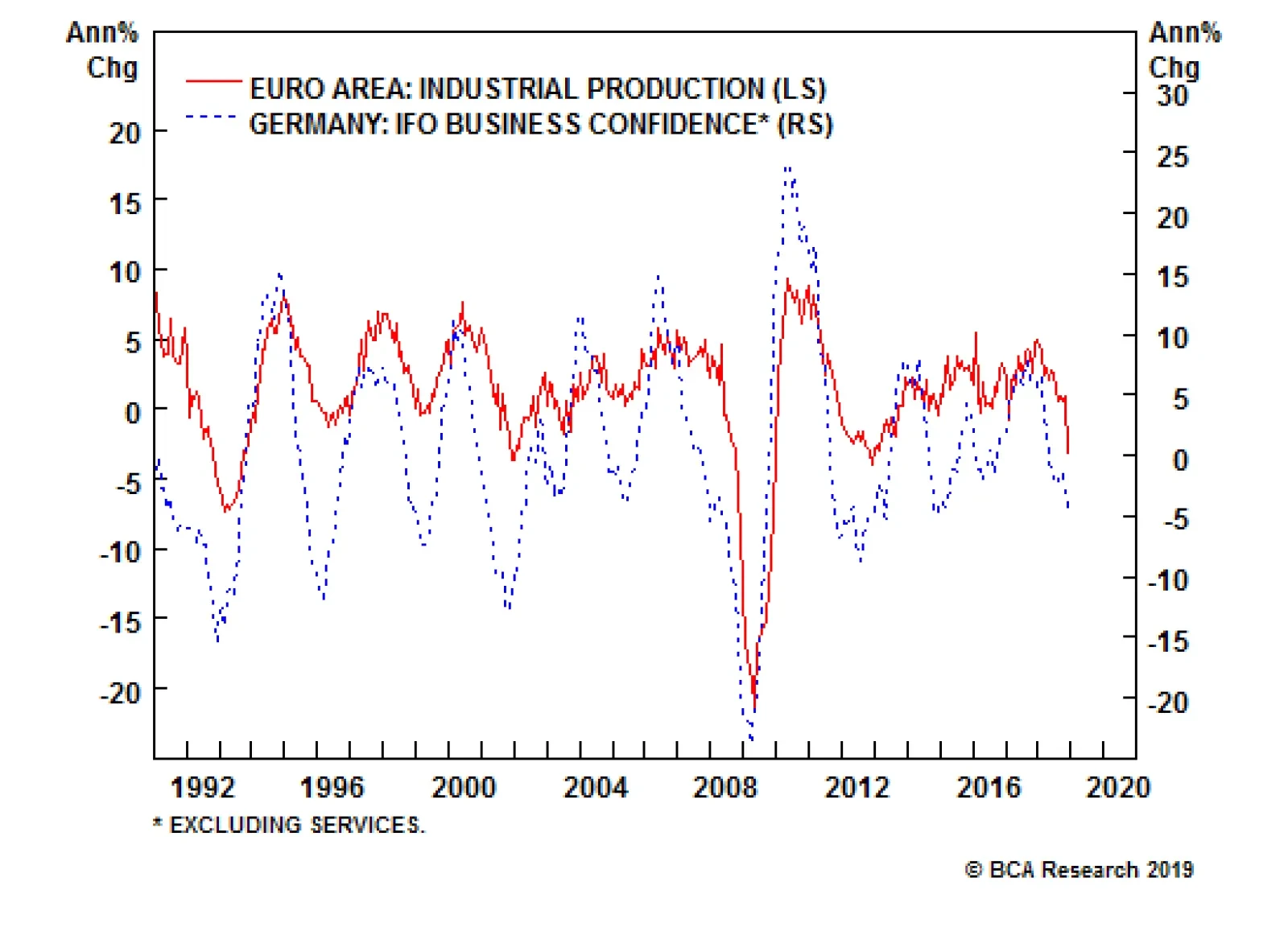

Today’s Industrial production in the euro area dropped to -3.3% on a year-on-year basis, much worse than expectations. The month-over-month number is -1.7%. This grim result raises concerns on the growth conditions in Europe. First, political tensions in…

Highlights All of our recent investment recommendations have performed very strongly but have further to go: 1. Own a combination of European banks plus U.S. T-bonds. 2. Overweight EM versus DM. 3. Overweight European versus U.S. equities. 4. Overweight Italian assets versus European assets. 5. Overweight the JPY. Feature Chart of the WeekBank Outperformance Corroborates A Growth Rebound

Bank Outperformance Corroborates A Growth Rebound

Bank Outperformance Corroborates A Growth Rebound

2019 will be the investment mirror-image of 2018. Last year started with growth fading and inflation on the cusp of picking up, both in Europe and around the world. This year has started with the European and global economies in the mirror-image configuration: growth likely to rebound, albeit modestly, and inflation set to fade (Chart I-2). Chart I-2Why 2019 Is The Mirror-Image Of 2018

Why 2019 Is The Mirror-Image Of 2018

Why 2019 Is The Mirror-Image Of 2018

However, as 2019 unfolds, the configuration will reverse, requiring a flip from a pro-cyclical to a pro-defensive investment tilt later in the year. This contrasts with 2018 which started pro-defensive and ended pro-cyclical. In this regard, the economic and investment shape of 2019 will be the mirror-image of 2018. Growth To Rebound, Inflation To Fade A tell-tale sign of a growth rebound is the recent outperformance of banks. Around the world, yield curves have flattened – or even inverted – meaning that banks’ net interest margins have compressed. This compression of bank profit margins is normally bad news for bank equities. Yet banks have been outperforming, not just in Europe but globally (Chart I-3). If margins are compressing, the plausible explanation for outperformance would be an improved outlook for asset growth, reflecting both a reduction in bad debt provisioning and a pick-up in bank credit growth. Chart I-3Banks Have Been Outperforming Since October

Banks Have Been Outperforming Since October

Banks Have Been Outperforming Since October

Independently and reassuringly, our proprietary credit impulse analysis supports this thesis (Chart of the Week). Six-month credit impulses have been rebounding not only in Europe, but also in the United States and very impressively in China (Chart I-4). Chart I-46-Month Credit Impulses Have Rebounded Everywhere

6-Month Credit Impulses Have Rebounded Everywhere

6-Month Credit Impulses Have Rebounded Everywhere

At the same time, inflation is set to disappoint as the recent near-halving of the crude oil price feeds into both headline and core consumer price indexes. With central banks now promising even greater “dependence on the incoming data”, this unfolding dynamic will force them to temper any hawkish intentions and rhetoric, limiting the extent of upside in bond yields. In this configuration, the combination of European banks plus U.S. T-bonds which we first recommended in November is still appropriate (Chart I-5). The position is up 3 percent in little more than a month and has further to go.1 Chart I-5Own A Combination Of Banks And Bonds

Own A Combination Of Banks And Bonds

Own A Combination Of Banks And Bonds

Europe’s largest economy, Germany, should benefit from another support to growth. Last year, the auto sector – a major engine of the German economy – spluttered as it absorbed the new WLTP emissions testing standard. Through the middle of 2018 German motor vehicle exports suffered a €20 billion hit which shaved 0.6 percent from Germany’s €3.4 trillion economy (Chart I-6). Now, if auto exports stabilize, this drag will disappear. And if auto exports recover to the pre-WLTP level after this one-off and temporary shock, Germany will receive a 0.6% mirror-image boost to growth.2 Chart I-6German Auto Exports Suffered A WLTP Hit

German Auto Exports Suffered A WLTP Hit

German Auto Exports Suffered A WLTP Hit

Regional Allocation Is Always And Everywhere About Sectors The European equity earnings cycle is tightly connected with global growth oscillations (Chart I-7). The simple reason is that the European equity market is over-exposed to classically growth-sensitive sectors such as banks and industrials. Chart I-7The European EPS Cycle Is Tightly Connected With Global Growth Oscillations

The European EPS Cycle Is Tightly Connected With Global Growth Oscillations

The European EPS Cycle Is Tightly Connected With Global Growth Oscillations

The emerging market earnings cycle is also connected with global growth oscillations (Chart I-8) because emerging markets have a very high exposure to banks. But the much less understood reason is that emerging markets have a near-zero exposure to healthcare (Table I-1). In sharp contrast, the U.S. equity earnings cycle has almost no connection with global growth oscillations (Chart I-9) because the U.S. equity market is over-exposed to technology and healthcare, neither of which are classically cyclical sectors. Chart I-8The EM EPS Cycle Is Also Connected With Global Growth Oscillations...

The EM EPS Cycle Is Also Connected With Global Growth Oscillations...

The EM EPS Cycle Is Also Connected With Global Growth Oscillations...

Chart I-9...But The U.S. EPS Cycle Is Not Connected With Global Growth Oscillations

...But The U.S. EPS Cycle Is Not Connected With Global Growth Oscillations

...But The U.S. EPS Cycle Is Not Connected With Global Growth Oscillations

Chart I-

Hence the allocation to emerging market (EM) versus developed market (DM) equities, and to Europe versus the U.S. reduce to simple equity sector calls. A quick glance at Chart I-10 and Chart I-11 will reveal two fundamental and inescapable truths: Chart I-10EM Outperforms DM When Global Banks Outperform Healthcare

EM Outperforms DM When Global Banks Outperform Healthcare

EM Outperforms DM When Global Banks Outperform Healthcare

Chart I-11European Equities Outperform U.S. Equities When Global Banks Outperform Technology

11. European Equities Outperform U.S. Equities When Global Banks Outperform Technology

11. European Equities Outperform U.S. Equities When Global Banks Outperform Technology

EM outperforms DM when global banks outperform global healthcare. European equities outperform U.S. equities when global banks outperform global technology. But is this just about so-called ‘beta’? No, banks can outperform in a rising market by going up more or, as recently, in a falling market by going down less. So this is always and everywhere about head-to-head sector relative performances. My colleague Arthur Budaghyan, our chief emerging market strategist, remains steadfastly pessimistic on the structural outlook for EM versus DM. We agree with Arthur, albeit we arrive at the structural conclusion from a completely different perspective. To reiterate, for EM to outperform DM global banks must outperform global healthcare. However, over an extended period this will prove to be an extremely tall order. As detailed in European Banks: The Case For And Against, blockchain is a long-term extinction threat to banks’ business models and profitability. Whereas healthcare is still a major growth sector as people focus more spending on improving the quality and quantity of their lifespans.3 Nevertheless, from a purely tactical perspective, the growth up-oscillation phase that started in October can continue for a little while longer allowing the recent countertrend moves to persist – especially as the recent decline in bond yields could further spur credit growth in the near term. So for the moment stay overweight: EM versus DM. European equities versus U.S. equities. Italian assets versus European assets. Bargain Basement Currencies Another of my colleagues Doug Peta, our chief U.S. strategist, has coined a lovely metaphor: “you cannot get hurt falling out of a basement window”. The metaphor beautifully captures the asymmetry when you are near the floor or ‘zero-bound’. Doug uses it to explain that small contributors to an economy have a limited capacity to damage economic growth because they cannot fall very far. We think the metaphor applies equally to interest rates when they are at or near their lower bound, which is to say, in the basement. This begs the obvious question: if interest rates are in the basement, then what is it that cannot get hurt much? The answer is: the exchange rate. The payoff profile for exchange rates just tracks expected long-term interest rate differentials. This means that when the expected interest rate is in or near the basement, the currency possesses a highly attractive payoff profile called positive skew. In essence, for any central bank already at the realistic limit of ultra-loose policy – such as the BoJ and ECB – policy rate expectations are effectively in the basement. They cannot go significantly lower. In contrast, policy rate expectations for the Federal Reserve are somewhere between the seventh and twelfth storey of the building (Chart I-12). From which you can get seriously hurt if you fall out of the window! Chart I-12You Cannot Get Hurt Falling Out Of A Basement Window

You Cannot Get Hurt Falling Out Of A Basement Window

You Cannot Get Hurt Falling Out Of A Basement Window

The upshot is that currency investors should always own at least one currency whose interest rate is in the basement against one whose interest rate is high up in the building, susceptible to fall out at some point, and get seriously hurt. The near term complication is the risk, albeit low, of a no-deal Brexit which would hurt European economies and currencies to a greater or lesser extent. Until the Brexit fog shows some signs of clearing, we would prefer the currency whose interest rate is in the basement to be a non-European currency. So for the moment, our favourite major currency remains the JPY. Dhaval Joshi, Senior Vice President Chief European Investment Strategist dhaval@bcaresearch.com Fractal Trading System* We are pleased to report that the 50:50 combination of Litecoin and Ethereum has surged by 42 percent in just two weeks! Also, long EUR/NZD achieved its 2.5 percent profit target and is now closed. This week’s trade is in line with the recommendation in the main body of this report to become pro-cyclical. Go long global industrials versus global utilities with a profit target of 3 percent and a symmetrical stop-loss. For any investment, excessive trend following and groupthink can reach a natural point of instability, at which point the established trend is highly likely to break down with or without an external catalyst. An early warning sign is the investment’s fractal dimension approaching its natural lower bound. Encouragingly, this trigger has consistently identified countertrend moves of various magnitudes across all asset classes. Chart I-13

Long Global Industrials Vs. Global Utilities

Long Global Industrials Vs. Global Utilities

The post-June 9, 2016 fractal trading model rules are: When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. Use the position size multiple to control risk. The position size will be smaller for more risky positions. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com Footnotes 1 The European banks position is relative to the broader equity market, and the recommended combination is 25 cents in the banks and 75 cents in the bonds. 2 German auto net exports and GDP are quoted at annualized rates. The Worldwide Harmonized Light Vehicle test Procedure (WLTP) is a new standard for auto emissions that took effect on September 1, 2018. 3 Please see the European Investment Strategy Special Report “European Banks: The Case For And Against”, November 8, 2018 available at eis.bcaresearch.com. Fractal Trading System Recommendations Asset Allocation Equity Regional and Country Allocation Equity Sector Allocation Bond and Interest Rate Allocation Currency and Other Allocation Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Question Three: Have central banks become less concerned about financial market selloffs? The idea that central banks have fallen “out of tune” with financial markets has spooked investors who fear that policymakers will not provide sufficient easing when…

Dear Client, In lieu of next week’s report, I will be hosting a webcast on Wednesday, January 9th at 10 AM EST, when I will be discussing the economic and financial market outlook for 2019 and answering your questions. Best regards, Peter Berezin, Chief Global Strategist Highlights The lack of major financial and economic imbalances in the U.S., as well as the Fed’s ability to moderate the pace of rate hikes, reduce the risk of a vicious cycle where tighter financial conditions lead to slower economic growth and even tighter financial conditions. The scope for central banks to cut rates is more limited outside the United States. Imbalances are also greater abroad. Nevertheless, the news is not all bleak, with the recent rebound in China’s credit impulse being a case in point. We turned more bullish on risk assets following December’s post-FOMC equity sell-off. A moderately overweight position in global equities over a 12-month horizon is currently justified. While we continue to favor the U.S. over other bourses in dollar terms, our conviction level in this regional bias has decreased. Treasury yields are likely to rise in an environment where U.S. growth is strong enough to enable the Fed to continue raising rates. Outside Japan, global government bond yields will also increase in 2019. We are removing our long June-2019 Fed funds futures contract hedge, and we are now solely outright short the December-2020 contract. We are also taking profits on our March-2019 EEM ETF put for a gain of 104%. Feature Merry Crisis And A Happy New Fear Santa arrived early this year. The plunge in stocks allowed investors to buy some of the world’s premier companies at a mouthwatering 20%-to-30% discount to what they would have paid just a few months earlier. What a gift! Needless to say, most investors would not regard last month’s stock market performance in such a favorable light. But why not? One answer is that investors must mark their portfolios to market. Thus, even if the decline in equity prices raised future returns, it still implied a decline in present net worth. Yet, this cannot be the whole explanation, because if all investors expected stocks to bounce back quickly, they would not have sold in the first place. Clearly, many investors must have come to the conclusion that the stock market would not only go down but stay down. However, this presents a puzzle. The economic environment did not change that much in the weeks leading up to the October sell-off. Growth has slowed more recently (Chart 1), with this morning’s disappointing ISM manufacturing report being the latest example, but this appears to have been mainly a response to the souring market climate rather than the cause of it. Chart 1Tighter Financial Conditions Have Led To Slower Growth

Tighter Financial Conditions Have Led To Slower Growth

Tighter Financial Conditions Have Led To Slower Growth

Reverse Causality? This raises an intriguing possibility: What if the drop in stock prices and jump in credit spreads that began in late September hurt expectations of economic growth by enough to justify a further discount in risk asset valuations? Such a “Financial Conditions Index (FCI) doom loop” is not just a theoretical construct. The last two U.S. recessions were both the products of burst asset bubbles — first the dotcom bubble and then the housing bubble. Could such a self-fulfilling vicious cycle be erupting again? If so, any rally in stocks or credit should be sold into, just as was the case in both 2001 and 2007. U.S. Fairly Resilient To A Doom Loop Fortunately, there are two reasons to think that such an outcome will not reoccur, at least not in the United States. First, as Box 1 explains, an FCI doom loop is more likely to unfold when economic growth becomes very sensitive to changes in financial conditions. This normally happens when economic and financial imbalances are elevated. That does not appear to be the case today. Unlike in the lead-up to the last two recessions, the U.S. private sector is a net saver whose income outstrips spending by 2.1% of GDP (Chart 2). Cyclical spending – the sum of residential investment, business capex, and expenditures on consumer durable goods – is also far below prior business-cycle peaks as a share of GDP (Chart 3). Chart 2The U.S. Private Sector Is A Net Saver

The U.S. Private Sector Is A Net Saver

The U.S. Private Sector Is A Net Saver

Chart 3U.S. Economy: Cyclical Spending Is Still Restrained

U.S. Economy: Cyclical Spending Is Still Restrained

U.S. Economy: Cyclical Spending Is Still Restrained

Despite recent releveraging in some categories, U.S. household debt has continued to decline in relation to the size of the economy. The ratio of personal debt-to-disposable income is now 34 percentage points below pre-crisis levels (Chart 4). Chart 4Household Leverage Is Below Its Peak

Household Leverage Is Below Its Peak

Household Leverage Is Below Its Peak

U.S. corporate debt has moved in the opposite direction. Nevertheless, while the ratio of U.S. corporate debt-to-GDP has climbed to a record high, it is still quite low by global standards (Chart 5). Perhaps more importantly, corporate debt is generally held by non-leveraged institutions. If corporate defaults were to rise unexpectedly, the losses to lenders would not pose the same systemic risk to the financial sector as mortgage defaults did during the Global Financial Crisis. Chart 5U.S. Corporate Debt Is High, But It Is Higher Elsewhere

U.S. Corporate Debt Is High, But It Is Higher Elsewhere

U.S. Corporate Debt Is High, But It Is Higher Elsewhere

The Fed’s Reaction Function It is not surprising that the stock market sell-off accelerated in early October following Fed Chairman, and failed golfer, Jay Powell’s comment that interest rates were “far from neutral.” We think that worries that the Fed will tighten too quickly are misplaced. Yes, monetary policy operates with “long and variable lags.” However, financial conditions, which lead growth, can be observed in real time (Chart 6). Chart 6Global Financial Conditions Have Tightened

Global Financial Conditions Have Tightened

Global Financial Conditions Have Tightened

Most of the tightening in financial conditions since late September has been due to falling equity prices. Our baseline scenario envisions a gain of roughly 10% in the S&P 500 in 2019. A rebound in stocks of this magnitude will reverse most of the recent FCI tightening, thereby allowing the Fed to raise rates three times this year. But if equities continue to sag, the Fed will scale back further monetary tightening or even cut rates. The mere possibility of such a policy response reduces the odds of an FCI doom loop. A Mixed Bag Outside The U.S. The economic outlook is murkier outside the United States. Economic and financial imbalances are greater in the EM space and parts of Europe. Non-U.S. central banks also have less scope to respond to adverse shocks, either because of fears that looser monetary policy will spark capital outflows (as is the case in many emerging markets) or because of the presence of the zero-bound constraint on interest rates (as is the case in the euro area and Japan). Nevertheless, the situation is not that bad. EM assets have been fairly resilient over the past few months, at least in comparison to their developed economy counterparts (Chart 7). China’s credit impulse has actually perked up, an indication that while credit growth is falling, it is doing so at a slower pace. Chart 8 shows that the Chinese credit impulse is highly correlated with global industrial commodity prices. We still expect global growth to slow in the first half of 2019, but at this point, much of the slowdown has been discounted in asset markets. With that in mind, we are raising the stop on our short AUD/JPY trade to 10% and instituting a profit target of 15%. Chart 7EM Assets Have Been Outperforming Recently

EM Assets Have Been Outperforming Recently

EM Assets Have Been Outperforming Recently

Chart 8The Increase In China's Credit Impulse Bodes Well For Industrial Commodity Prices

The Increase In China's Credit Impulse Bodes Well For Industrial Commodity Prices

The Increase In China's Credit Impulse Bodes Well For Industrial Commodity Prices

The Perils Of Discrete Decision-Making One of the annoyances of being an investment strategist is that you often feel compelled to take discrete views on where the markets are heading. Are you bullish, bearish, or neutral? Actually, it is usually just bullish or bearish because most people regard neutral views as lacking in conviction and insight. This incentive structure is counterproductive. Not only does it cause analysts to turn a blind eye to incoming data that may challenge their thesis, it disregards how professional investors actually operate. Successful investors scale into positions as the market gets cheaper and scale out as it becomes more expensive. Trying to time the bottom (or the top) with exact precision is futile. With that in mind, we are going to tweak the way we make recommendations going forward in order to improve transparency, accountability, and accuracy. Rather than simply stating whether we are bullish, bearish, or neutral, we will assign the main asset classes a subjective score between zero and one hundred, with 0-to-40 being bearish, 40-to-60 being neutral, and 60-to-100 being bullish. We will adjust the score in every publication. To add analytic rigor to this framework, we will also compare our subjective model score with that of our MacroQuant model. Where Things Now Stand We downgraded global equities last June, but moved back to overweight following December’s post-FOMC meeting sell-off, as valuations reached that rather blurry line at which a modest equity overweight was warranted. Our subjective score for global equities currently stands at 65%, above the model’s estimate of 50%. Our moderately bullish view reflects our expectation that global growth will stabilize by mid-year and monetary policy will remain accommodative, even if the Fed raises rates by more than what the markets are currently discounting. Tempering our enthusiasm is the recognition that the business cycle is getting long in the tooth – especially in the U.S. – and that global equity valuations, while far cheaper than they were a few months ago, are still significantly less favorable than they were near past market bottoms (Chart 9). Chart 9Global Equity Valuations Have Improved

Global Equity Valuations Have Improved

Global Equity Valuations Have Improved

Regionally, we continue to favor U.S. stocks over other developed markets, and DM over EM more broadly. However, our conviction level on this view is not high, and we are prepared to revise it if it looks like global growth is accelerating, an outcome that would limit any further dollar strength (our subjective dollar score currently stands at 70%, below the model’s estimate of 92%). Reflecting our expectation of decent global equity returns in 2019 and our waning conviction to be underweight EM, we are taking profits on in our March-2019 EEM ETF put for a gain of 104%. Please note that our view on EM is more optimistic than that of Arthur Budaghyan, BCA’s chief emerging markets strategist, who continues to see considerable downside risks to EM assets. For now, Treasury yields are likely to rise in an environment where U.S. growth is strong enough to enable the Fed to continue raising rates. We assign the 10-year yield a score of 30%, which is close to our model estimate of 32%. Accordingly, we are removing our long June-2019 Fed funds futures contract hedge, and we are now solely outright short the December-2020 contract. Core European bond yields will increase, reflecting diminished excess capacity in the euro area and the end of ECB net asset purchases. U.K. yields should also grind higher, as the odds of a soft Brexit (or no Brexit) improve. Only in Japan will yields remain contained, thanks to the BoJ’s ongoing yield curve control regime. We do not expect spread product to have a banner year, but the current yield pick-up should be sufficient to ensure that risky credit outperforms cash. Peter Berezin, Chief Global Strategist Global Investment Strategy peterb@bcaresearch.com Box 1 The Analytics Of Doom Loops When will a tightening in financial conditions stemming from lower equity prices and higher borrowing costs lead to a vicious circle of slower economic growth and even tighter financial conditions? The answer depends on how sensitive economic growth is to financial conditions in relation to how sensitive financial conditions are to growth. Figure 1 shows two equilibrium schedules, one for the economy (EE) and one for asset markets (AA). Both schedules slope downward. The EE schedule is downward-sloping because easier financial conditions boost growth. If growth is too strong given the prevailing level of financial conditions, economic activity will slow (Panel A). The AA schedule is downward-sloping because equity prices tend to fall and credit spreads rise when growth slows. If equity prices are too high and credit spreads are too narrow for a certain level of growth, then financial conditions will tighten (Panel B). Suppose economic growth is not very sensitive to changes in financial conditions, perhaps because imbalances in the economy are limited (Panel C). Then changes in financial conditions will be fleeting: A decline in equity prices or a widening in credit spreads will not hurt growth very much, allowing the stock market and credit market to quickly normalize. In contrast, suppose that economic growth is very sensitive to financial conditions, so much so that the EE schedule is flatter than the AA schedule. In this case, the economy will be vulnerable to self-reinforcing booms and busts (Panel D). In particular, a small random jump from U to UI will send the economy careening towards a doom loop of ever-weaker growth and tighter financial conditions.

Chart 10

Strategy & Market Trends MacroQuant Model And Current Subjective Scores

Chart 11

Tactical Trades Strategic Recommendations Closed Trades

GAA DM Equity Country Allocation Model Update The GAA DM Equity Country Allocation model is updated as of December 31, 2018. The quant model reduced Spain’s large overweight to a slight overweight, and further downgraded the U.S. allocation. As a result, the model now has assigned overweight allocations to Germany, Switzerland, the Netherlands, Canada and Italy, with underweight allocations to the U.S., Japan, France and U.K. Australia and Sweden are now in the neutral zone, as shown in Table 1. Table 1Model Allocation Vs. Benchmark Weights

GAA Quant Model Updates

GAA Quant Model Updates

As shown in Table 2 and Chart 1, Chart 2 and Chart 3, the overall model outperformed the MSCI world benchmark by 38 bps in December, with a 48 bps of outperformance from Level 1 model offset by a 21 bps of underperformance from Level 2. Since going live, the overall model has outperformed by 96 bps, with Level 2 outperforming by 120 bps and level 1 outperforming by 57 bps. Table 2Performance (Total Returns In USD %)

GAA Quant Model Updates

GAA Quant Model Updates

Chart 1GAA DM Model Vs. MSCI World

GAA DM Model Vs. MSCI World

GAA DM Model Vs. MSCI World

Chart 2GAA U.S. Vs. Non U.S. Model (Level 1)

GAA U.S. Vs. Non U.S. Model (Level 1)

GAA U.S. Vs. Non U.S. Model (Level 1)

Chart 3GAA Non U.S. Model (Level 2)

GAA Non U.S. Model (Level 2)

GAA Non U.S. Model (Level 2)

Please see also the website http://gaa.bcaresearch.com/trades/allocation_performance. For more details on the models, please see Special Report, “Global Equity Allocation: Introducing The Developed Markets Country Allocation Model,” dated January 29, 2016, available at https://gaa.bcaresearch.com. Please note that the overall country and sector recommendations published in our Monthly Portfolio Update and Quarterly Portfolio Outlook use the results of these quantitative models as one input, but do not stick slavishly to them. We believe that models are a useful check, but structural changes and unquantifiable factors need to be considered too in making overall recommendations. GAA Equity Sector Selection Model Dear Client, As advised in our October 2018 Special Alert, we have suspended the GAA Equity Sector Selection Model due to the significant changes in the GICS sector classifications, implemented at the end of September. We will rebuild the model using the newly constituted sectors once full back data is available from MSCI, which we understood would be in December but which we have not received yet. We thank you for your understanding. Xiaoli Tang, Associate Vice President xiaoliT@bcaresearch.com Amr Hanafy, Research Associate amrh@bcaresearch.com

Highlights Investors ran for cover in December as they succumbed to a litany of worries regarding the outlook. The key question is whether the pessimism is overdone or an extended equity bear market is underway. Our outlook for the U.S. and global economies has not changed since we published our 2019 Outlook. There are some tentative signs that the two U.S. weak spots, housing and capital spending, are bottoming out. However, our global leading economic indicators continue to herald a soft first half of 2019 outside of the U.S. The dollar thus has more upside in the near term. The political risks facing investors have not diminished either. In particular, we expect turbulence related to the U.S./China trade war to extend well beyond the 3-month “truce” period. The returns to stocks, corporate bonds and commodities historically have not been particularly attractive on average when the U.S. yield curve is this flat. Nonetheless, the risk/reward balance has improved enough as prices fell over the past month to justify upgrading equities in the advanced economies back to overweight. Move to a neutral level of cash, and keep bonds underweight on a 6-12 month investment horizon. The upgrade to stocks in the developed markets does not carry over to emerging markets. The backdrop will remain hostile to EM assets until China pulls out the big policy stimulus guns and the dollar peaks. Stay clear of EM assets and neutral on base metals for now, but be prepared to upgrade sometime in 2019. Global government bonds could rally a little more in the near term if the risk-off phase continues. Nonetheless, with little chance of any more rate hikes discounted in the U.S. yield curve, the risks for U.S. and global yields are tilted to the upside. Bond investors with a 6-12 month horizon should ride out the near-term volatility with a short-duration position. Oil prices have overshot to the downside. Supply is adjusting and, given robust energy demand in 2019, we still expect prices to rise to $82. Feature Investors ran for cover in December as they succumbed to concerns regarding the U.S./China trade war, corporate leverage, global growth, rising U.S. interest rates and the shift toward quantitative tightening. Some equity indexes, such as the Russell 2000, reached bear market territory, having lost more than 20%. Losses have been even worse outside the U.S. Earnings revisions have plunged into the “net downgrade” zone. Implied volatility has spiked and corporate bond spreads are surging (Chart I-1). The key question is whether the pessimism is overdone or an extended equity bear market is underway. Chart I-1A Flight To Quality

A Flight To Quality

A Flight To Quality

We laid out our economic view in detail in the BCA Outlook 2019 report, published in late November. Not enough has changed on the global economic front in the three weeks since then that would justify such a violent shift in investor sentiment. That said, our favorite global leading economic indicators continue to erode (Chart I-2). The only ray of hope is that the diffusion index constructed from our Global Leading Economic Indicator appears to have bottomed. Nonetheless, the actual LEI will keep falling until the diffusion index shifts into positive territory. Chart I-2Global Leading Indicators Still Weak

Global Leading Indicators Still Weak Global Leading Indicators Flashing Red

Global Leading Indicators Still Weak Global Leading Indicators Flashing Red

For China, a key source of investor angst, the latest retail sales and industrial production reports reinforced that economic momentum continues to recede. We will not be convinced that growth is bottoming until we see an upturn in our credit impulse indicator (Chart I-3). Its continued decline in November suggests that the outlook for emerging market assets and commodity prices is poor for at least the next quarter. Global industrial output appears headed for a mild contraction. The manufacturing troubles are centered in the emerging Asian economies, but Europe and Japan are also feeling the negative effects. Chart I-3China: No Bottom Yet

China: No Bottom Yet

China: No Bottom Yet

In the U.S., November’s bounce in housing starts and permits is a hopeful sign that the soft patch in this sector is ending. However, it is not clear how the devastating wildfires on the west coast have affected the housing data (Chart I-4). The downdraft in capital goods orders may also be drawing to a close, based on the latest reading from the Fed’s survey of capital spending intentions. The U.S. leading economic indicator dipped slightly in November, but remains consistent with above-trend real GDP growth in the months ahead. Chart I-4U.S.: Some Hopeful Signs

U.S.: Some Hopeful Signs

U.S.: Some Hopeful Signs

The bottom line is that our outlook for growth has not been significantly altered. We see little risk of a U.S. recession in 2019. The global economy continues to weaken, but we expect enough policy stimulus out of China to stabilize growth in that economy in the second half of the year. We highlighted in the BCA Outlook 2019 that, while the risks appeared elevated, we would consider shifting back to overweight in stocks if they cheapened sufficiently. Valuation has indeed improved in recent weeks and sentiment has turned more cautious. Global growth will likely continue to decelerate in the first half of 2019, but markets have largely discounted this outcome. In other words, the shift toward pessimism in financial markets appears overdone. The fact that the Fed has signaled a move away from regular quarter-point rate hikes adds to our confidence in playing what will likely be the last upleg in risk assets in this cycle. Fed: Rate Hikes No Longer On Autopilot The Fed lifted rates by a quarter point in December and signaled that any additional tightening will be data-dependent. The FOMC also trimmed the expected peak in the funds rate and its estimate of the long-run, or neutral, level. Policymakers were likely swayed by some disappointing U.S. economic data, the pullback in core PCE inflation, and the sharp tightening in financial conditions (Chart I-5). Chart I-5Financial Conditions Have Tightened

Financial Conditions Have Tightened

Financial Conditions Have Tightened

Monetary conditions are not tight by historical yardsticks, such as the level of real interest rates. The problem is that investors fear that the neutral level of the fed funds rate, the so-called R-star, remains very depressed. If true, it could mean that the Fed is already outright restrictive, which would signal that the monetary backdrop has turned hostile for risk assets. The OIS curve signals that the consensus believes that the Fed is pretty much done the tightening cycle (Chart I-6) Chart I-6Investors Believe The Fed Is Done!

Investors Believe The Fed Is Done!

Investors Believe The Fed Is Done!

We believe that R-star is higher than the current policy setting and is rising, as the growth headwinds related to the Great Financial Crisis fade with the passage of time. The problem is that nobody knows the level of the neutral rate. Thus, we need to watch for signs that the fed funds rate has surpassed that level, such as an inverted yield curve. The 10-year/3-month T-bill spread is still in positive territory, but barely so. Meanwhile, our R-star indicator is also flashing yellow as it sits on the zero line (Chart I-7). It is a composite of monetary indicators that in the past have been useful in signaling that monetary policy had become outright restrictive, leading to slower growth and trouble for risk assets. The lead time of this indicator relative to economic activity and risk asset prices has been quite variable historically, but a breakdown below zero would send a powerful bearish signal for risk assets if confirmed by an inverted yield curve. Chart I-7Worrying Signs Of Tight Money

Worrying Signs Of Tight Money

Worrying Signs Of Tight Money

The Implications Of Four Fed Scenarios It is not surprising that investors are struggling with a number of different possible scenarios on how the R-star/Fed policy nexus will play out. We can perhaps boil down discussion of the Fed and the implications for financial markets to a matrix of four main outcomes, based on combinations related to the level of R-Star (high or low) and the pace of Fed rate hikes in 2019 (pause or continue increasing rates by 25 basis points per quarter). Policy Mistake #1: R-star is still very low, but policymakers do not realize this and the FOMC continues to tighten into restrictive territory in 2019. By definition, the economy begins to suffer in this scenario, inflation and inflation expectations decline and long-bond yields are flat-to-lower. The yield curve inverts. However, current real rates are still so low that the fed funds rate cannot be very far above R-Star, which means it would represent only a small policy mistake. As long as the Fed recognizes the economic slowdown early enough and truncates the rate hike cycle, then there is a good chance that a recession would be avoided. Investors would initially fear a recession, however, which means that risk assets would be hit hard in absolute terms and relative to bonds and cash until recession fears fade. The direction of the dollar is perhaps trickiest part because there are so many potential cross currents. To keep things simple we will assume that global growth follows our base-case view and remains lackluster in the first half of 2019, followed by a modest re-acceleration. We believe the dollar would likely rally a little as the Fed continues tightening, but then would fall back as the FOMC is forced to turn dovish in the face of a U.S. growth scare. Policy Mistake #2: R-Star is high and rising but the Fed fails to hike rates fast enough to keep up. The economy accelerates in this scenario because monetary policy remains stimulative through 2019, at a time when the 2018 fiscal stimulus will still be providing a demand tailwind. Core PCE inflation moves above 2% and long-term inflation expectations shift up, signaling to investors that the Fed has fallen behind the inflation curve. Risk assets rip for a while and the yield curve bear-steepens as the 10-year Treasury yield moves gradually higher at first. Belatedly, the FOMC realizes it has underestimated the neutral rate and signals a hawkish policy shift. A 50-basis point rate hike at one FOMC meeting causes risk assets to buckle on the back of surging Treasury yields. The yield curve begins to bear-flatten. Eventually the curve inverts and the economy enters recession. The dollar weakens at first because higher inflation lowers U.S. real interest rates relative to the rest of the world. Global growth prospects would initially get a boost from the acceleration in U.S. growth, which is also dollar-bearish. However, in the end the dollar would likely rise as global financial markets turn risk-off. Fed Gets It Right (1): R-star is high and rising. The Fed continues to tighten in line with the increase in the neutral rate. Treasurys sell off hard and the yield curve shifts higher, but remains fairly flat (parallel shift). The curve could mildly invert temporarily, but market worries about a recession eventually recede as economic momentum remains robust, allowing the curve to subsequently trade in the 0-50 basis point range. As discussed below, risk assets tend to outperform Treasurys and cash when the yield curve is in this range, but not by much. The Treasury market would suffer significant losses. This is the most dollar-bullish of the four scenarios, given our global growth view (tepid) and the fact that the market is not even priced for a full quarter-point rate hike in 2019. Fed Gets It Right (2): R-Star is actually still quite low, but the Fed correctly sees recent economic data disappointments and the tightening in financial conditions as signs that policy is close to neutral. The Fed pauses the rate hike cycle, followed by a slower and more data-dependent pace of tightening. The yield curve stays fairly flat and flirts with inversion as investors try to figure out if the Fed has overdone it. Risk assets are volatile and deliver little return over cash. Treasurys rally a bit as the chance of any further rate hikes is priced out of the market, but the rally is limited unless the economy falls into recession (which is not part of this scenario because we are assuming the Fed “gets it right”). The dollar fluctuates, but delivers no real trend since U.S. yield differentials versus the rest of the world do not change much. As we go to press, financial markets are moving in a way that is consistent the Policy Mistake #1; the consensus appears to believe that the Fed has already lifted the fed funds rate too far, causing financial conditions to tighten. But if U.S. real GDP growth remains above-trend as we expect, then the market view could eventually transition to a belief in Mistake #2; the Fed falls behind the inflation curve. The curve would re-steepen and risk assets could have one last hurrah before the Fed gets hawkish again and the 2020 recession arrives. The transition from Mistake #1 to Mistake #2 is essentially our base-case outlook. Nonetheless, obviously the risks around this central scenario are high, especially given how late it is in the U.S. economic and policy cycle. Asset Returns And The Yield Curve Our 2018 late-cycle investing theme focussed on historical asset return and policy dynamics after the U.S. unemployment rate fell below the full-employment level in past cycles. We found that risk assets tend to run into trouble once the U.S. S&P 500 operating margin peaks. As we highlighted in the BCA Outlook 2019, our margin proxies are still not heralding that a peak is at hand. Given the recent investor obsession with the U.S. yield curve, this month we look at historical asset returns at different levels of the 10-year/3-month T-bill yield curve slope: Phase I, when the slope is above 50 basis points; Phase II, when the curve is between 0 and 50 basis points; and Phase III, when the curve is inverted (Table I-1). The data are presented as (not annualized) monthly average returns. It may be surprising that risk asset returns are for the most part positive even in when the curve is inverted. However, keep in mind that we are focussing on the curve, not on recession periods. The curve can be inverted for a long time before the subsequent recession occurs. Risk asset returns often remain positive during this period. The broad conclusions are as follows: Unsurprisingly, risk assets perform their best, in absolute terms and relative to government bonds and cash, in Phase I when the yield curve is steep. Returns tend to deteriorate as the curve flattens. This includes equities, corporate bonds and commodities. Small caps underperform large caps when the curve is between 0 and 50 basis points, but the reverse is true when the curve is flatter or steeper than that range. The ratio of cyclical stocks to defensives has not revealed a consistent pattern with respect to the yield curve, although this may reflect the short historical period available. Value stocks shine versus growth when the curve is inverted. Hedge fund and private equity returns have not varied greatly across the three yield curve environments. Structured product, such as CMBS and ABS, have enjoyed their best performance when the curve is inverted. Timberland and Farmland have also rewarded investors during Phase III. We suspected that asset returns when the curve is in the 0-50 basis point range would vary importantly with the direction of the curve. In Table I-I we split Phase II into two parts: when the curve is steepening after being inverted, and when the curve is flattening after being steep. In other words, when the consensus is either transitioning from quite bullish to very bearish, or vice-versa.

Chart I-