Europe

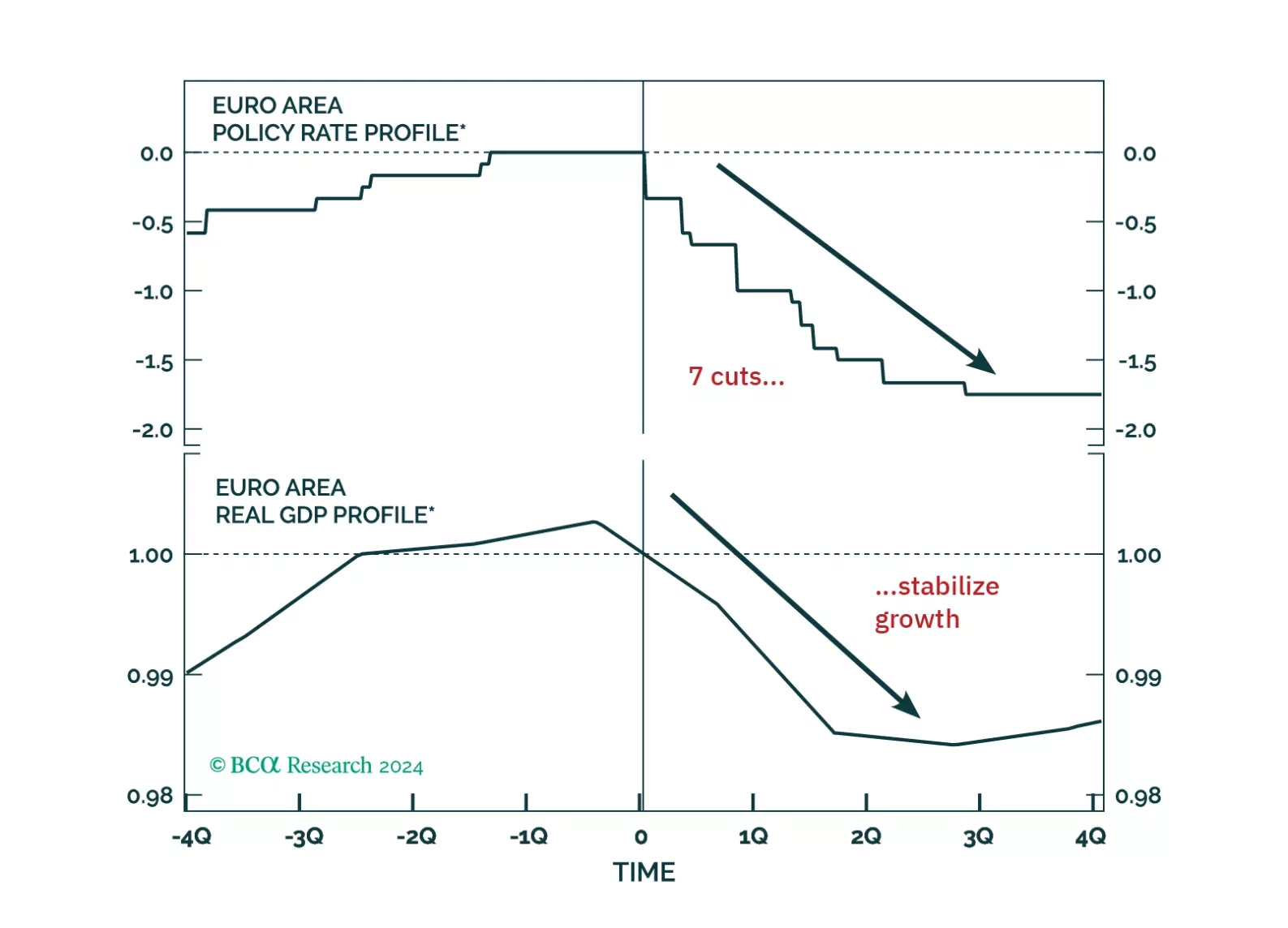

Our European Investment Strategy team published their annual outlook, outlining five key themes that will shape Europe’s economy and markets in 2025. Europe will enter a mild recession in H1 2025, but growth is expected to rebound quickly in the…

December flash PMIs for the core advanced economies showed service sector growth picking up. Manufacturing keeps contracting, and the US continues to outperform its DM peers. The US composite index beat expectations and increased to 56.6 from 54.9.…

Our Chart Of The Week comes from Mathieu Savary, Chief Strategist of our European Investment Strategy service. Mathieu sees a dimming outlook for European industrial stocks in the near term.The sector has been one of the strongest performers in Europe this…

For our last publication of the year, we explore five key themes that will dominate the European macro landscape and markets next year. While the start of 2025 will be challenging for European assets, the latter part will offer some much-needed relief.

The December Sentix Economic Index for the Euro Area missed expectations, declining to -17.5 vs. -12.8 in November. Both the current situation and expectations components declined. As the first sentiment indicator for December, the Sentix confirms…

In the final installment of their “PIGS Have Wings” special series, our European investment strategists took a deep dive into the Spanish economy and financial assets. Spain outperformed most developed markets since 2022, with strong gains in both…

Spain has outperformed most developed markets since 2022 – real economic output and risk assets alike. Can it last?

German factory orders decreased less than expected in October, falling 1.5% m/m after rising 7.2% in September. Excluding major orders, which often distort the overall picture, core new orders rose 0.1%, after rising 2.7% a month prior. Despite the…

Our European Investment Strategy and GeoMacro Strategy teams published a joint report, digging into the structural challenges behind Europe’s economic underperformance, while pointing out to potential turnaround opportunities. Europe’s prolonged…

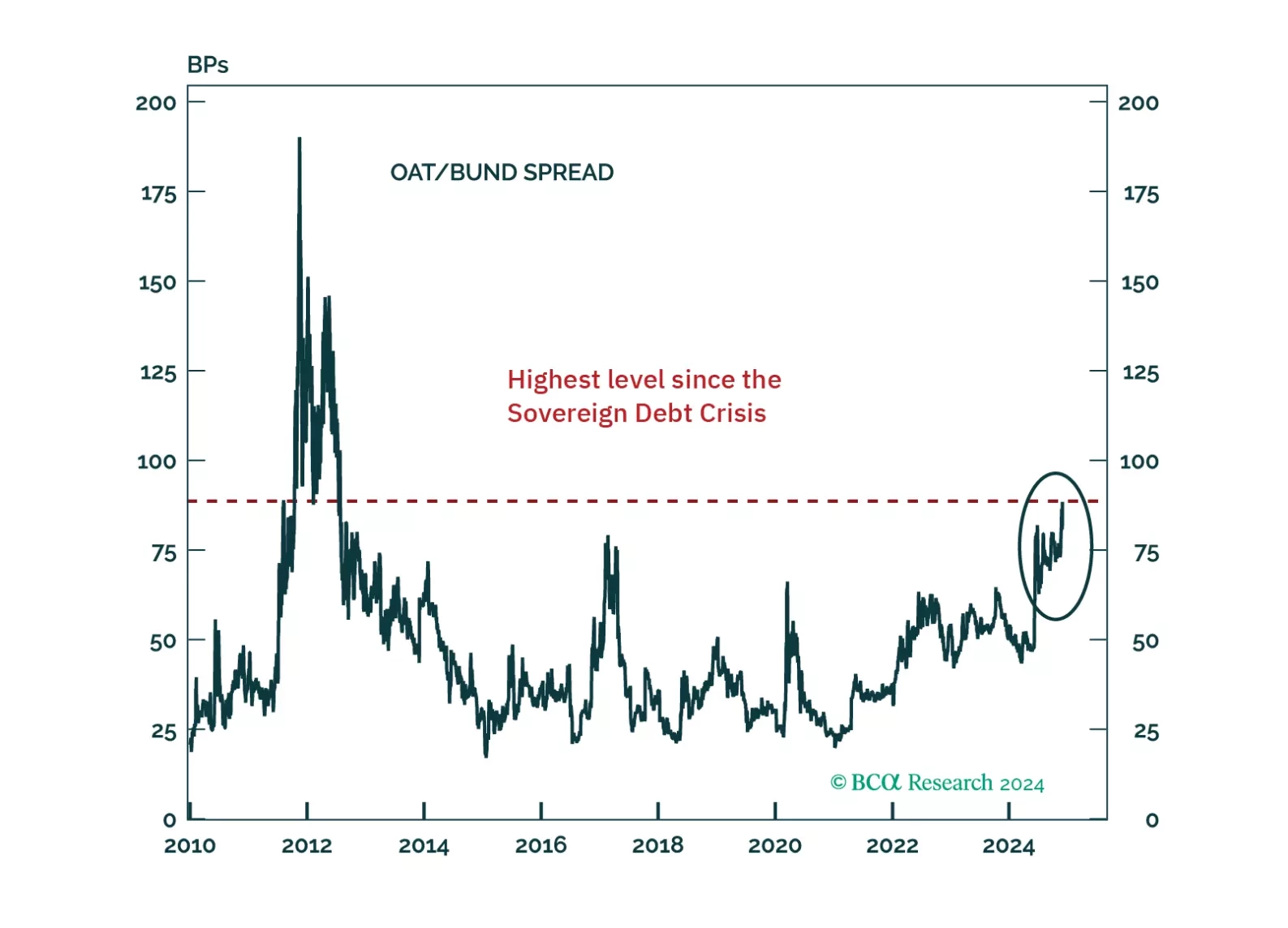

France finds itself in a unique, thorny situation. Can it heave itself out of it? And what does it mean for investors?