Europe

Highlights The USD remains supported by fundamentals, especially now that its late-2016 excesses have been purged. Solid U.S. growth contrasts with weaker growth in the rest of the world, which will incentivize further inflows into the U.S. dollar. Despite this positive cyclical view, the tactical outlook remains risky for dollar bulls. In the immediate term, the euro will benefit from easing Italian tensions and as well as from the dollar's correction, but its six-month outlook remains poor. The AUD could also rebound right now, but any such rally should be used to build further short positions. Feature After a furious rally from February to August, the dollar has been weakening since the middle of last month. Since July, we have been worried that the dollar could stage a bit of a correction,1 but we remained committed to the view that ultimately the greenback would rise further in 2018. It is now time to review whether this thesis still holds. BCA believes that the USD's correction could run through the fall, but that the final quarter of 2018 should still prove a rewarding period for dollar bulls. Ultimately, policy divergences will remain a crucial support for the dollar, especially as EM weakness continues to affect the distribution of growth across the globe. USD: Not Yet Extended The dollar ultimately follows the path implied by its fundamental drivers - whether they are interest rate spreads, growth and inflation differentials, relative equity prices, or even relative money-supply growth. However, the path taken by the USD around its drivers is rather wide, and the dollar regularly overshoots and undershoots the equilibrium implied by the aggregation of all these fundamentals (Chart I-1). Academics call this the "band of agnosticism." Chart I-1The Dollar To Follow Fundamentals Higher

The Dollar To Follow Fundamentals Higher

The Dollar To Follow Fundamentals Higher

This cycle was no exception. BCA's Fundamentals Index for the dollar hooked up in 2011, a move associated with a turning point in the greenback itself. However, the dollar remained in undershoot territory for many years. Then suddenly, in 2014, the coiled spring was released and the dollar surged higher, moving above its "band of agnosticism" in 2015 - a moved exacerbated by the sudden rally that followed the election of Donald Trump in November 2016. Once the dollar had become over-loved, over-owned and expensive, it also became vulnerable. The pick-up in global growth that was so evident in 2017 caused a serious correction in this vulnerable currency. However, the selloff had a positive impact: U.S. growth, interest rates, equities and so on continued to move favorably, and the dollar is now positioned to rebound anew, having purged its most egregious excesses. The global economic backdrop is also positive for the dollar. For one, the theme of monetary divergences is still at play. Boosted by a healthy banking sector, healthy household balance sheets and an untimely fiscal stimulus of 1.7% of GDP, U.S. growth has hit 2.8%, well above potential. Moreover, growth has been above potential for eight years, and now U.S. capacity utilization is at its tightest level since the late 1980s. Historically, so large an absence of slack has been linked to higher U.S. interest rates (Chart I-2). Yet interest rate markets are pricing in roughly four increases over the next 24 months, even as Lael Brainard warned that the Federal Reserve could move beyond the hikes implied by its own forecast, the "dot plots." Chart I-2Tight Capacity Utilization Implies Higher U.S. Rates...

Tight Capacity Utilization Implies Higher U.S. Rates...

Tight Capacity Utilization Implies Higher U.S. Rates...

The U.S. economy continues to fare well, as U.S. real interest rates remain 60 basis points below neutral rates and the yield curve has yet to invert. However, U.S. rates matter for the rest of the world as well. There, the picture is less pretty. EM dollar debt stands near record levels (Chart I-3). Hence, EM financial conditions have been hit by the combined assault of higher U.S. rates and an appreciating dollar. Nowhere is this clearer than when looking at the interplay between U.S. bond yields and the South African rand or AUD/JPY, a cross highly correlated to EM currencies. This cycle, rising U.S. bond yields have most often been associated with a rising ZAR or a rising AUD/JPY (Chart I-4). However, this time around, as was the case during the May 2013 Taper Tantrum, rising bond yields are linked to these pro-cyclical currency pairs falling. This suggests that rising yields are not reflecting global growth anymore, and are in fact restrictive for the rest of the world, even if they are not a problem for the U.S. Chart I-3... Which Will Hurt EM Economies

... Which Will Hurt EM Economies

... Which Will Hurt EM Economies

Chart I-4Higher U.S. Rates Now Hurt Global Growth

Higher U.S. Rates Now Hurt Global Growth

Higher U.S. Rates Now Hurt Global Growth

This inference is underpinned by the decline in BCA's U.S. Financial Liquidity Index, which heralds additional weakness in global growth and commodity prices (Chart I-5). Already we are seeing symptoms of the malaise. Japanese foreign machine tool orders are contracting, and BCA's Asian Leading Economic Indicator is in deep contraction (Chart I-6). Chart I-5Dollar Liquidity Is A Problem For Growth

Dollar Liquidity Is A Problem For Growth

Dollar Liquidity Is A Problem For Growth

Chart I-6Signs That Global Growth Is Already Suffering

Signs That Global Growth Is Already Suffering

Signs That Global Growth Is Already Suffering

A rising fed funds rate and falling ex-U.S. growth is likely to continue to support the dollar. The dollar loves nothing more than falling global growth. The U.S. economy has low exposure to global trade and to the global industrial sector, and therefore when global growth slows, the U.S. economy is relatively insulated from foreign shocks. This means that U.S. rates of return do not suffer as much as foreign ones. This is even truer in the rare instances when global growth slows while U.S. economic activity continues to power ahead, especially when artificially inflated by untimely fiscal stimulus. This is a characterization of the current environment. Hence, money will continue to flow into the U.S. economy on a two- to three-quarter horizon. In fact, portfolio flows into the U.S. remain well below the levels that prevailed during the previous decade (Chart I-7). The current account deficit is also smaller, hence, if net foreign portfolio flows can increase due to the attraction of higher U.S. rates of return, the U.S. balance of payments will move into a greater surplus, creating a strong underpinning for the dollar. This positive cyclical backdrop for the greenback is not without impediments. Most crucially are the short-term dynamics. Since July, we have been warning clients that a tactical correction in the dollar was likely. While EUR/USD has indeed rebounded, most other currencies have displayed rather tepid performances. This does not mean that the tactical risks to the dollar have abated. Quite the opposite, they are rising. As Chart I-8 illustrates, a large buildup in dollar longs has materialized, yet the G10 economic surprise index is making a trough. Moreover, the diffusion index of the BCA Global Leading Economic indicator is also stabilizing. Additionally, USD /CNY has failed to make new highs and the Turkish central bank just raised rates to 24% - which if Argentina is any guide is likely to provide only temporary relief for the TRY. This means that a period of risk-on sentiment in EM could emerge. Stretched dollar positioning, a temporary stabilization in global growth and EM inflows could precipitate a serious correction in the dollar. Chart I-7Dollar Favorable Flows

Dollar Favorable Flows

Dollar Favorable Flows

Chart I-8Tactical Risks To The Dollar

Tactical Risks To The Dollar

Tactical Risks To The Dollar

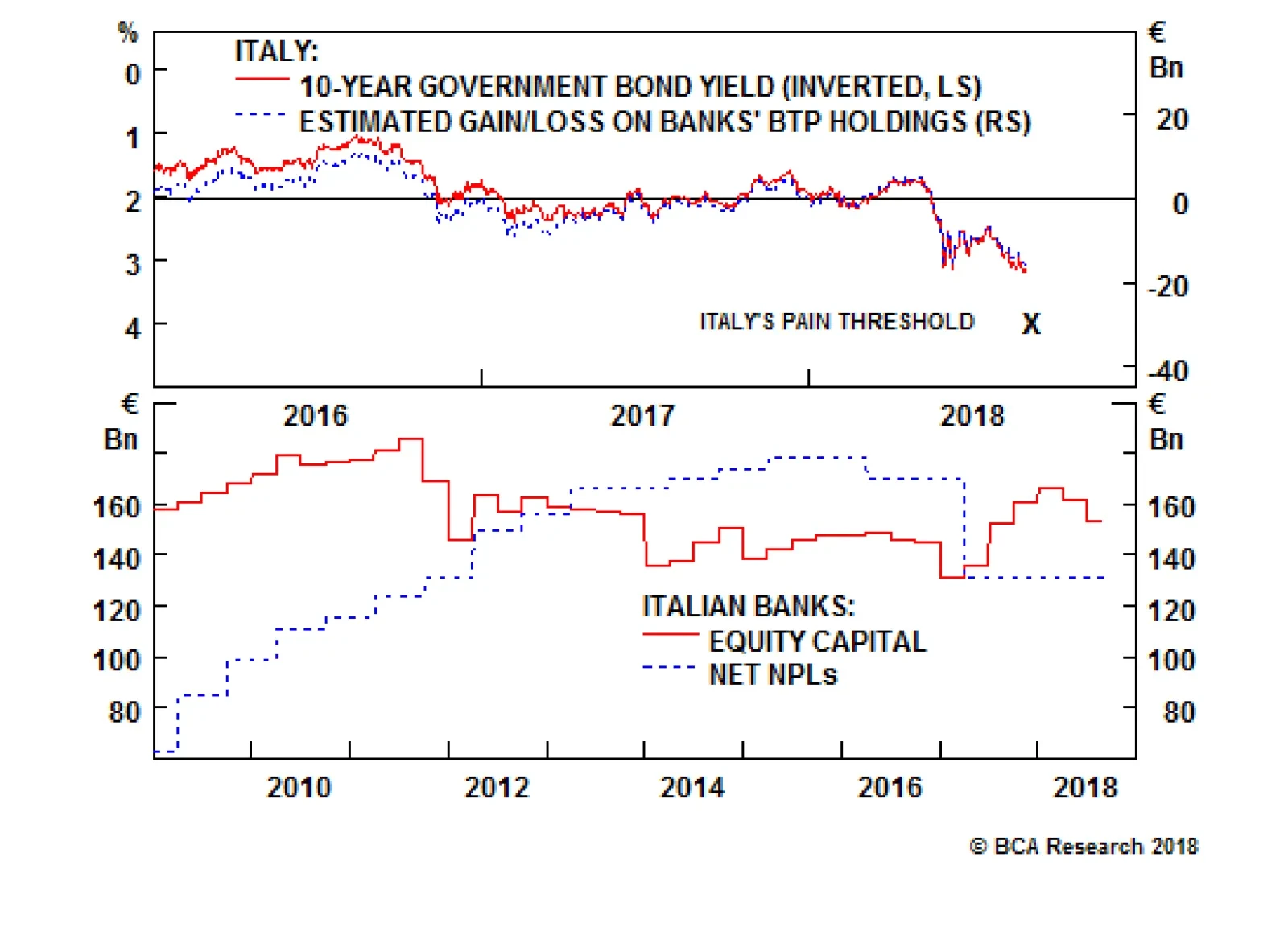

Bottom Line: The dollar is still supported by potent cyclical tailwinds. The U.S. economy is roaring and at full employment, yet global growth is suffering because global liquidity conditions are deteriorating. Higher rates of return in the U.S. will therefore attract additional capital, supporting the greenback in the process. Despite this positive cyclical backdrop, the short-term outlook is murkier. Speculators have aggressively bought the dollar, leaving them vulnerable to any positive surprises in global growth, even temporary ones. Fade The Euro Rebound The euro has benefited from the cool-off in Italian politics. The populist Five Star Movement / Lega Nord coalition is backing away from a budget confrontation with Brussels, as Giovanni Tria, Italy's minister of finance, wants a 2% budget deficit, while Deputy Prime Minister Matteo Salvini is arguing for a 2.9% budget hole - well south of the 6% levels touted during the campaign. As a result, the spread between Italian BTPs and German bunds has fallen from 193 basis points at the beginning of the month to 150 basis points this week (Chart I-9). Since gyrations in Italian spreads reflect the evolution of the perceived probability that the euro area will fall apart, the fall in the spreads has implied a fall in the euro area-breakup risk premium. This has created a boon for the euro. Another support for the euro emerged yesterday. At his press conference, European Central Bank President Mario Draghi divulged that the ECB has curtailed its growth forecast for 2018 and 2019, but not its inflation forecast. In fact, Draghi went as far as mentioning that his confidence that euro area inflation would move back to target in the medium term has increased. There is no denying that the inflationary backdrop has improved as European wages and labor costs have indeed starting to recover (Chart I-10). However, the picture is not that straightforward. The lagged impact of the previous fall in euro area inflation relative to the U.S. is likely to continue to be felt in EUR/USD moving forward, as has been the case over the past 10 years (Chart I-11). Chart I-9The Euro Area Break Up Risk Premium Is Declining

The Euro Area Break Up Risk Premium Is Declining

The Euro Area Break Up Risk Premium Is Declining

Chart I-10Rising Euro Area Labor Costs

Rising Euro Area Labor Costs

Rising Euro Area Labor Costs

Chart I-11Relative Inflation Backdrop Is Still Euro Bearish

Relative Inflation Backdrop Is Still Euro Bearish

Relative Inflation Backdrop Is Still Euro Bearish

This risk is compounded by developments in China. As we have often argued, the growth differential between the euro area and China can largely be explained by growth dynamics in China. As Chart I-12 illustrates, when Chinese monetary conditions tighten, or when China's marginal propensity to consume - as approximated by the gap between M1 and M2 - declines, this often leads to underperformance of European economic activity relative to the U.S. Chart I-12AChinese Economy Still Hurting Euro Area Vs U.S. (I)

Chinese Economy Still Hurting Euro Area Vs U.S. (I)

Chinese Economy Still Hurting Euro Area Vs U.S. (I)

Chart I-12BChinese Economy Still Hurting Euro Area Vs U.S. (II)

Chinese Economy Still Hurting Euro Area Vs U.S. (II)

Chinese Economy Still Hurting Euro Area Vs U.S. (II)

Today, Chinese monetary conditions have improved somewhat as the Chinese authorities try to combat the shock to the Chinese economy created by the growing trade war between the U.S. and China. However, Matt Gertken, BCA's Geopolitical Strategy service's expert on Chinese policy, believes that Chinese policymakers do not intent to actually cause economic growth to pick up. Indeed, they are committed to reform and deleveraging, and only want to limit downside to the Chinese economy.2 Thus, the large growth gap between the U.S. and the euro area is here to stay. As markets absorb news of Chinese stimulus, EUR/USD could rebound toward 1.19, but we are inclined to fade such a rebound. For one, the growth and inflation gap between the U.S. and the euro area remains euro bearish. Additionaly BCA's Central Bank Monitor for the Fed clearly points toward the need to tighten U.S. monetary policy, while our indicator for the ECB points to the need to maintain an extremely loose policy setting in Europe (Chart I-13). With the euro still trading above its intermediate-term fair value estimate (Chart I-14), beyond any short-term rally the euro still possesses ample downside in the fourth quarter. As such, we would use the current rebound in the euro as an opportunity to buy the dollar once again. Chart I-13The U.S. Needs More Tightening, Europe Does Not

The U.S. Needs More Tightening, Europe Does Not

The U.S. Needs More Tightening, Europe Does Not

Chart I-14The Euro Possesses Downside

The Euro Possesses Downside

The Euro Possesses Downside

Bottom Line: Falling risk premia in Italy, a pick-up in European wages and signs of stimulus in China are creating some support under the euro. However, European growth and inflation are set to continue to lag well behind the U.S. as China's stimulus is not designed to reverse its deleveraging campaign and boost growth, but instead to limit downside to growth created by the U.S.-China trade war. Hence, we will use the current rebound in the euro and correction in the USD to buy the greenback again in the coming weeks. What's Going On Down Under? In recent months, the Australian economy has managed to generate some impressive numbers on the employment front. However, until recently this was not enough to prompt investors to push the AUD higher. In fact, as recently as Monday, AUD/USD was trading at 0.71. Investors are skeptical about the Australian economy's underlying strength. The NAB Business Confidence for the Next Period has weakened sharply, while mortgage approvals and house prices have also sagged. This suggests that new orders, employment and consumption could follow lower (Chart I-15). This represents a big problem for the Aussie, as our central bank monitor for the Reserve Bank of Australia is already in "easing required" territory (Chart I-16). The RBA will therefore not be able to hike rates any time soon, despite the fact that U.S. interest rates are currently in an uptrend. As such, interest rate differentials between Australia and the U.S. will continue to deteriorate. Chart I-15Australia Is Set To Slowdown

Australia Is Set To Slowdown

Australia Is Set To Slowdown

Chart I-16China And Australia Are Joined At The Hip

China And Australia Are Joined At The Hip

China And Australia Are Joined At The Hip

Moreover, Australia has been hit directly by the decline in Chinese industrial activity. As Chart I-17 illustrates, Australian exports are a direct function of China's Li-Keqiang index. This has two implications. First, the current rebound in the Li-Keqiang index suggests that investors could bid up the AUD with great alacrity if the USD were to correct further, a thesis we espouse. However, since we do not anticipate the rebound in the Li-Keqiang indicator to have much longevity, nor do we anticipate the greenback's correction to morph into a bear market, this also means that we would use any rebound in the AUD to sell more of it. Beyond China, EM at large still constitutes a risk for AUD/USD. Arthur Budaghyan, our Chief EM strategist, argues that the period of weakness in EM assets has further to run. Our views on the U.S. dollar, on declining global liquidity and on Chinese policy corroborate this assessment. If EM economies slow further, the still-elevated expected long-term growth rate in EM earnings could decline further as well. Since growth expectations on EM EPS are indicative of expected interest rates and terms-of-trade for Australia, this also suggests that the AUD could suffer significant downside in the coming quarters (Chart I-18). Finally, the AUD remains a pricey currency. AUD/USD continues to trade significantly above its purchasing-power-parity fair value, and the real trade-weighted AUD remains above its long-term average (Chart I-19). As such, the AUD does not possess the required valuation cushion to make it a buy in this challenging context. Chart I-17RBA ##br##Cannot Hike

RBA Cannot Hike

RBA Cannot Hike

Chart I-18EM Has Yet To Be Fully Re-Rated, ##br##And So Does The AUD

EM Has Yet To Be Fully Re-Rated, And So Does The AUD

EM Has Yet To Be Fully Re-Rated, And So Does The AUD

Chart I-19No Valuation Cushion##br## In The AUD

No Valuation Cushion In The AUD

No Valuation Cushion In The AUD

Bottom Line: The Australian economy has posted some solid employment numbers, but the trends in business confidence and the housing market augur poorly. Australian monetary policy will have to remain very loose. Moreover, since China's stimulus is likely to be limited, any rebound in the AUD on the back of a dollar correction should be faded, especially as the Aussie does not offer any valuation cushion. Mathieu Savary, Vice President Foreign Exchange Strategy mathieu@bcaresearch.com 1 Please see Foreign Exchange Strategy Weekly Report, titled "Time To Pause And Breathe", dated July 6, 2018, available at fes.bcaresearch.com 2 Please see Foreign Exchange Strategy Special Report, titled "China: How Stimulating is The Stimulus?", dated August 24, 2018, available at fes.bcaresearch.com Currencies U.S. Dollar Recent data in the U.S. has been mixed: Average hourly earnings growth outperformed expectations significantly, coming in at 2.9%. Moreover, nonfarm payrolls also surprised to the upside, coming in at 201 thousand, but this was mitigated by large downward revisions to the previous two months. Additionally initial jobless claims surprised positively, coming in at 203 thousand. However, core inflation underperformed expectations, coming in at 2.2%. Finally, DXY has been flat for the past couple of weeks. We continue to be bullish on the dollar on a cyclical basis, as inflationary pressures will continue to accumulate in the U.S., causing the fed to hike more than expected, particularly in 2019. Moreover, high U.S. borrowing cost will likely weigh on global growth, giving an additional boost to the dollar, as the U.S. has a lower beta than other DM economies to the global economic cycle. Report Links: The Dollar And Risk Assets Are Beholden To China’s Stimulus - August 3, 2018 Rhetoric Is Not Always Policy - July 27, 2018 Time To Pause And Breathe - July 6, 2018 Chart II-1USD Technicals 1

USD Technicals 1

USD Technicals 1

Chart II-2USD Technicals 2

USD Technicals 2

USD Technicals 2

The Euro Recent data in the euro area has been negative: Both headline and core inflation surprised to the downside, coming in at 2% and 1% respectively. Moreover, industrial production yearly growth also surprised to the downside, coming in at -0.1%. Finally, retail sales yearly growth also underperformed expectations, coming in at 1.1%. EUR/USD has been flat the past two weeks. Yesterday, however the market rallied as the ECB confirmed that it expects to wind down its bond-buying program. Nevertheless, it also lowered growth forecast for this year and next. We continue to believe that the euro will have downside until the end of the year, as a policy and regulatory tightening in China will weigh on the global industrial cycle, to which Europe is highly levered. Report Links: Time To Pause And Breathe - July 6, 2018 What Is Good For China Doesn’t Always Help The World - June 29, 2018 Updating Our Long-Term FX Fair Value Models - June 22, 2018 Chart II-3EUR Technicals 1

EUR Technicals 1

EUR Technicals 1

Chart II-4EUR Technicals 2

EUR Technicals 2

EUR Technicals 2

The Yen Recent data in Japan has been mixed: Tokyo ex fresh food inflation outperformed expectations, coming in at 0.9%. Moreover, overall household spending yearly growth also surprised positively, coming in at 0.1%. However, labor cash earnings yearly growth underperformed expectations substantially, coming in at 1.5%. Finally, Markit Services PMI surprised to the downside, coming in at 51.5. USD/JPY has been flat the past couple of weeks. Overall, we are bullish on the yen against the euro and the commodity currencies, as the tightening in monetary policy in the U.S. as well as in China should create a risk off environment where safe heavens like the yen benefits and cyclical currencies suffer. Report Links: Rhetoric Is Not Always Policy - July 27, 2018 Updating Our Long-Term FX Fair Value Models - June 22, 2018 Rome Is Burning: Is It The End? - June 1, 2018 Chart II-5JPY Technicals 1

JPY Technicals 1

JPY Technicals 1

Chart II-6JPY Technicals 2

JPY Technicals 2

JPY Technicals 2

British Pound Recent data in the U.K. has been mixed: Average hourly earnings yearly growth excluding and including bonuses both came in above expectations, at 2.9% and 2.6% respectively. Moreover, Markit Services PMI also outperformed expectations, coming in at 54.3. However, industrial production surprised to the downside, coming in at 0.9%. Finally, nationwide housing prices yearly growth also surprised negatively, coming in at 2%. GBP/USD has rallied by roughly 0.5% the past couple of weeks. We believe that the pound could have some short term upside, as positioning continues to be significantly bearish. That being said, we are bearish on the pound on a cyclical basis, particularly against the yen. At this moment, the pound does not appear to have much of a geopolitical risk premium embedded in its price. Thus, any turbulence in the Brexit negotiations could result in significant downside for the GBP. Report Links: Updating Our Long-Term FX Fair Value Models - June 22, 2018 Inflation Is In The Price - June 15, 2018 Updating Our Intermediate Timing Models - May 18, 2018 Chart II-7GBP Technicals 1

GBP Technicals 1

GBP Technicals 1

Chart II-8GBP Technicals 2

GBP Technicals 2

GBP Technicals 2

Australian Dollar Recent data in Australia has been mixed: Gross domestic product yearly growth came in above expectations, at 3.4%. However, building permits month-on-month growth surprised to the downside, coming in at -5.2%. Finally, the RBA Commodity Index SDR yearly growth surprised positive, coming in at 6.7%. After a bout of pronounced weakness, AUD/USD has been flat for the past couple of weeks. We believe that the Australian dollar has further downside particularly against the yen and the dollar. Australia's economy is very sensitive to the Chinese industrial cycle, as iron ore is Australia's main commodity export. However, the overleveraged industrial complex is precisely the economic sector where Chinese policymakers want to rein in credit excesses. This will curb industrial activity in China, and hurt the economies of commodity supplies like Australia. Report Links: What Is Good For China Doesn’t Always Help The World - June 29, 2018 Updating Our Long-Term FX Fair Value Models - June 22, 2018 Updating Our Intermediate Timing Models - May 18, 2018 Chart II-9AUD Technicals 1

AUD Technicals 1

AUD Technicals 1

Chart II-10AUD Technicals 2

AUD Technicals 2

AUD Technicals 2

New Zealand Dollar Recent data in New Zealand has been mixed: Retail sales and retail sales ex autos yearly growth both outperformed expectations, coming in at 1.1% and 1.4% respectively. Moreover, the trade balance also surprised to the upside, coming in at -4.4 billion dollars/ However, the terms of trade Index underperformed expectations, coming in at 0.6%. NZD/USD has fallen by roughly 0.8% against the dollar for the past couple of weeks. We continue to be bearish on kiwi on a cyclical basis. The combination of high U.S. rates and deleveraging in China will weigh on carry currencies like the NZD. Furthermore, we also hold a bearish view on a structural basis, given that the new government has vowed to curb immigration and add an unemployment mandate to the RBNZ, both developments which are negative for the currency. Report Links: Updating Our Long-Term FX Fair Value Models - June 22, 2018 Updating Our Intermediate Timing Models - May 18, 2018 Value Strategies In FX Markets: Putting PPP To The Test - May 11, 2018 Chart II-11NZD Technicals 1

NZD Technicals 1

NZD Technicals 1

Chart II-12NZD Technicals 2

NZD Technicals 2

NZD Technicals 2

Canadian Dollar Recent data in Canada has been mixed: Both core and headline inflation outperformed expectations, coming in at 1.6% and 3% respectively. Moreover, manufacturing shipments month-on-month growth also outperformed expectations, coming in at 1.1%. However, retail sales month-on-month growth surprised to the downside, coming in at -0.2%. USD/CAD has been flat for the past couple of weeks. We are short this cross as a hedge to our dollar bullish view, as inflationary pressures in Canada remain strong. Moreover, the CAD will continue to outperform the AUD, as the divergence between Canada's and Australia's main export markets- China and the U.S. - will persist. Report Links: Updating Our Long-Term FX Fair Value Models - June 22, 2018 Inflation Is In The Price - June 15, 2018 Rome Is Burning: Is It The End? - June 1, 2018 Chart II-13CAD Technicals 1

CAD Technicals 1

CAD Technicals 1

Chart II-14CAD Technicals 2

CAD Technicals 2

CAD Technicals 2

Swiss Franc Recent data in Switzerland has been mixed: Gross domestic product yearly growth outperformed expectations, coming in at 3.4%. The SVME PMI also surprised to the upside, coming in at 64.8. However, the KOF leading indicator surprised negatively, coming in at 100.3. Finally, real retail sales growth also underperformed expectations, coming in at -0.3%. EUR/CHF has risen by roughly 0.5% this past two weeks. We continue to be bearish on the franc on a long-term basis, as inflationary pressures in Switzerland are still too weak for the SNB to remove its accommodative monetary policy, or stop its currency intervention. That being said, the CHF could experience some short term upside if the sell-off in emerging markets continues. Report Links: Updating Our Long-Term FX Fair Value Models - June 22, 2018 Updating Our Intermediate Timing Models - May 18, 2018 Value Strategies In FX Markets: Putting PPP To The Test - May 11, 2018 Chart II-15CHF Technicals 1

CHF Technicals 1

CHF Technicals 1

Chart II-16CHF Technicals 2

CHF Technicals 2

CHF Technicals 2

Norwegian Krone Recent data in Norway has been mixed: Both headline and core inflation outperform expectations, coming in at 3.4% and 1.9%. Moreover, the Labour Force survey also surprised to the upside, coming in at 3.9%. However, retail sales growth underperformed expectations, coming in at 0.7%. USD/NOK has fallen by nearly 2% over the last two weeks. We are bullish on the NOK against other commodity currencies like the AUD and the NZD. This is because oil will likely outperform within the commodity space. After all, Our commodity strategist have explained at length why political risk in Iraq and Venezuela could cause a shortage of supply in the oil markets, while Chinese deleveraging in the industrial sector will weigh on base metal demand. Report Links: Updating Our Long-Term FX Fair Value Models - June 22, 2018 Updating Our Intermediate Timing Models - May 18, 2018 Value Strategies In FX Markets: Putting PPP To The Test - May 11, 2018 Chart II-17NOK Technicals 1

NOK Technicals 1

NOK Technicals 1

Chart II-18NOK Technicals 2

NOK Technicals 2

NOK Technicals 2

Swedish Krona Recent data in Sweden has been mixed: Retail sales yearly growth surprised to the downside, coming in at -1.2%. However, consumer confidence outperformed expectations, coming in at 102.6. The krona has been the best performing currency during the past two weeks, with USD/SEK falling by roughly 2% over this period. At the moment we continue to be bullish USD/SEK, as the krona is the most sensitive currency to the dollar's strength. However, on a longer term basis, we believe that inflationary pressures in Sweden will ultimately force the Riskbank to hike more than the market expects, providing support for the SEK. Report Links: Updating Our Long-Term FX Fair Value Models - June 22, 2018 Updating Our Intermediate Timing Models - May 18, 2018 Value Strategies In FX Markets: Putting PPP To The Test - May 11, 2018 Chart II-19SEK Technicals 1

SEK Technicals 1

SEK Technicals 1

Chart II-20SEK Technicals 2

SEK Technicals 2

SEK Technicals 2

Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Closed Trades

Highlights In an environment where both interest rates and inflation are low but rising at a time of stretched equity valuations, what can investors do to enhance risk-adjusted portfolio returns? In this report, we investigate the roles of three types of popular instruments in a portfolio context: 1) Floating-Rate Notes, 2) Leveraged Loans and 3) Danish Mortgage Bonds. Floating-rate notes benefit from rising interest rates, but they are not a free lunch. Leveraged loans also benefit from rising interest rates; their very high correlation with high-yield bonds make them a good substitute for a portion of high-yield exposure in a rising-rate environment. Danish mortgage bonds have attracted foreign investors in recent years, but foreign ownership already accounts for about a quarter of the less than half a trillion USD market. Their positive correlation with aggregate bonds and negative correlation with equities in both Japan and the euro area make them a possible substitute for a portion of the bond basket in a balanced portfolio. Feature BCA has upgraded cash to overweight in the current environment, where inflation and interest rates are both low but rising, and equity valuations are stretched.1 For U.S. investors, holding cash is quite attractive as the cash yield is now higher than the equity dividend yield. For investors in the euro area, Switzerland, Sweden, Denmark and Japan, however, holding cash actually is a sure way to eat into portfolio returns, given the negative yields in these countries (Table 1). Table 1Current Yields* (%)

Searching For Yield In A Low-Return Environment

Searching For Yield In A Low-Return Environment

Some clients, particularly those in Europe, have asked where to put cash to get higher returns. Unfortunately, it's hard to increase return without assuming additional risk. As shown in Table 1, investors could pick up some yield by putting money in 3-month deposits instead of 3-month Treasury bills, but even 3-month deposit rates are still negative in some European countries. In this report, we investigate the roles of three types of popular instruments in a low but rising rate environment: 1) Floating-Rate Notes (FRNs), 2) Leveraged Loans (LLs) and 3) Danish Mortgage Bonds (DMBs). 1. Floating-Rate Notes An FRN offers coupon payments that float or adjust periodically based on a predetermined benchmark rate. Typical benchmarks in the U.S. are Treasury bills, LIBOR, the prime rate or some other short-term interest rate. Once the benchmark is chosen, the issuer will establish an additional spread that it is willing to pay over the chosen benchmark rate. The spread mainly reflects an issuer's credit quality and the time to maturity of the note. Even though coupon reset frequency can vary between daily, weekly, monthly, quarterly and yearly, the average coupon rate has responded quickly to the fed funds rate, as shown in Chart 1. Issuers can be both government-sponsored enterprises and investment-grade corporations. Before the 2008 Great Financial Crisis, FRNs were mostly issued by corporations. Some of the notes, however, performed badly during the financial crisis, causing a drop in both total issuance and the share of corporate issuance (Chart 2). FRNs can be either callable or non-callable with or without caps and floors, so FRNs carry credit risk - and callable ones also carry call risk. In terms of interest rate risk, it applies mostly to the income received. Chart 1Rising Rate Environment Benefits FRNs

Rising Rate Environment Benefits FRNs

Rising Rate Environment Benefits FRNs

Chart 2Corporate Dominance In FRN Market

Corporate Dominance In FRN Market

Corporate Dominance In FRN Market

Because of the nature of floating rates, FRNs can benefit from rising interest rates and have limited price sensitivity to interest rates. As shown in Chart 3, the Bloomberg/Barclays U.S. Floating-Rate Note index has lower duration than the cash index, as represented by the Bloomberg/Barclays Treasury (<1 year) index, while it offers a nice yield pickup. Since the inception of the index in December 2003 it has, in general, outperformed the cash index. This reward, however, has come at a cost: it does not provide cash-like protection when such protection is needed in times like the Great Financial Crisis and the euro debt crisis in 2011 (Chart 3, panels 3 and 4). This is because the majority of FRNs are offered by corporations that carry credit risk. Consequently, FRNs have higher correlations to high-yield bonds and equities than to the aggregate bond index, as shown in Chart 4. Chart 3FRNs: Not A Free Lunch

FRNs: Not A Free Lunch

FRNs: Not A Free Lunch

Chart 4FRNs: A Lower Risk Alternative To Junk Bonds

FRNs: A Lower Risk Alternative To Junk Bonds

FRNs: A Lower Risk Alternative To Junk Bonds

The ideal time to invest in FRNs is when rates are low and are expected to rise. This is essentially our view on rates now. Instead of thinking of it as a cash alternative with higher risk, however, we recommend clients take the funding from the high-yield bucket, in line with our downgrade of high yield to neutral from overweight, and also our call of reducing portfolio duration. So how to invest in FRNs? According to Bloomberg Barclays, the U.S. FRN market has a market value of US$505.8 billion, which is small compared to the US$1,267.5 billion high-yield bond market. As such, FRNs are relatively less liquid to trade than corporate bonds. Therefore, they are mostly suitable for purchasing and holding to maturity. One can purchase individual floating-rate securities through a broker, or can invest in mutual funds that invest only in FRNs. Also, there are ETFs that only hold FRNs. Table 2 shows some basic information on three dedicated FRN ETFs. Table 2FRN ETFs*

Searching For Yield In A Low-Return Environment

Searching For Yield In A Low-Return Environment

2. Leveraged Loans Leveraged loans, also known as bank loans or senior secured loans, are a type of corporate debt that also have floating coupon rates, which, like the FRNs, adjust to changes in prevailing interest rates and hence benefit from rising rates. These loans tend to be senior to an issuer's traditional corporate bonds, and are collateralized by a pledge of the issuer's assets. However, secured does not mean safe. These loans are private investments which are generally held by funds or large institutional investors. Most of them carry sub-investment-grade ratings and can default. They also tend to be very illiquid to trade, because physical delivery to the buyer is often needed from a seller (by faxing the paperwork, for example). As such, during periods of market volatility, these loans can be subject to significant price declines. Even though bank loans share the same feature of having "floating coupon rates" as FRNs, they are higher risk securities. In the U.S., bank loans have been mostly inferior to FRNs on a risk-adjusted return basis, as their higher return is offset by much higher volatility (Chart 5A). In the euro area, however, these loans have become more favorable than FRNs since the start of 2018 (Chart 5B). Chart 5ALeveraged Loans Vs. FRNs: U.S.

Leveraged Loans Vs. FRNs: U.S.

Leveraged Loans Vs. FRNs: U.S.

Chart 5BLeveraged Loans Vs. FRNs: Euro Area

Leveraged Loans Vs. FRNs: Euro Area

Leveraged Loans Vs. FRNs: Euro Area

Historically, when interest rates have risen, bank loans have outperformed traditional fixed-income securities, and vice versa, because of their floating-rate feature, as shown in Charts 6A and 6B. This positive correlation with rates has been more consistent when the relative performance of bank loans is compared to government bonds and investment-grade corporate bonds. When compared to high-yield bonds, however, the correlation appears weak, as shown in the bottom panels of Charts 6A and 6B. This is not surprising given that these loans share similar "sub-investment grade" credit quality with junk bonds. In fact, as shown in Chart 7, bank loans have a highly positive correlation with junk bonds, yet a mostly negative correlation with the aggregate bond index both in the U.S. and the euro area. Chart 6ALLs Outperform When Rates Rise: U.S.

LLs Outperform Whe Rates Rise: U.S.

LLs Outperform Whe Rates Rise: U.S.

Chart 6BLLs Outperform When Rates Rise: Euro Area

LLs Outperform When Rates Rise: Euro Area

LLs Outperform When Rates Rise: Euro Area

Chart 7Bank Loan Correlations With Traditional Bonds

Bank Loan Correlations With Traditional Bonds

Bank Loan Correlations With Traditional Bonds

This correlation feature has two very interesting implications: a) Adding bank loans to a standard aggregate bond portfolio could add diversification, and b) replacing some high-yield holdings with bank loans could generate a sub-investment grade basket with a better risk/reward profile compared to high-yield alone. Chart 8 and Table 3 show that historically there has existed an "optimal" combination of bank loans and high-yield bonds that somewhat improves the risk-adjusted return of the sub-investment grade basket. It's worth noting, however, that this historically "optimal" combination is subject to data frequency and time period, as is the case for the U.S. where the optimal weight for bank loans has been about 40% from 2002 to the present, but about 80% in the period from 1997 to the present. As such, in addition to thorough credit analysis to evaluate the suitability of bank loans, investors should also consider the variable nature of correlation when considering replacing part of their high-yield bond exposure with bank loans. Chart 8Junk Bonds - Leverage Loans Basket Profiles

Searching For Yield In A Low-Return Environment

Searching For Yield In A Low-Return Environment

Table 3Risk Return Profiles Of Sub-Investment Grade Baskets

Searching For Yield In A Low-Return Environment

Searching For Yield In A Low-Return Environment

3. Danish Mortgage Bonds A Danish mortgage bond (DMB) is essentially a loan to a borrower who has taken out a mortgage on his or her home. Mortgage bonds are issued by mortgage credit institutions which often have high credit ratings. Some DMBs have fixed rates, while others have floating rates with a minimum of zero percent. Some of these bonds can also be callable, often at par (100). With a solid history of over 200 years, the DMB market has survived numerous occasions of economic and political turmoil, including the bankruptcy of the Kingdom of Denmark in 1813, the Great Depression of the 1930s and the Great Financial Crisis and ensuing recession in 2008. Over its entire history, every single issued bond has been repaid in full to investors, in large part due to the strong legislative framework that protects the bond investors (see Appendix 1). As of the end of July 2018, the DMB market consisted of kr. 2.672 trillion of AAA-rated covered bonds. Once largely dominated by local pensions and insurance companies, the DMB market has seen increasing interest from foreign investors in recent years. According to data from the Danish central bank, foreign ownership of fixed rate mortgage bonds stood at kr. 295 billion (29%) in July 2018 compared to kr. 154 billion (18%) in January 2016 (Chart 9). In terms of total holdings of all mortgage bonds (fixed rate, variable rate and bonds backing interest adjustment loans), foreigners held kr. 614 billion (23%), an increase of kr. 27 billion compared to the beginning of 2016. Japanese investors, who have suffered many years of extremely low yields domestically, have been quite active in the DMB market. According to data from the Bank of Japan, Japanese investors purchased some kr. 50 billion of long-term Danish non-government bonds in the period from 2016 to June 2018.3 In June 2018, Nykredit, the largest Danish mortgage bank with a market share of about 40%, even created a DMB index hedged to yen using one-month forward rates due to popular demand and corresponding requests from Japanese investors. As shown in Chart 10, since 2009, the DMB index hedged to yen has outperformed both JGBs and Japanese corporate bonds. Chart 9Foreign Ownership of Danish Fixed Rate Mortgage Bonds*

Searching For Yield In A Low-Return Environment

Searching For Yield In A Low-Return Environment

Chart 10DMBs For Japanese Investors

DMBs For Japanese Investors

DMBs For Japanese Investors

Even though interest rates in the U.S. are much higher than those in the euro area, investing in the U.S. after hedging the currency is not really attractive for euro investors. For example, U.S. bank loans have outperformed European bank loans in local currency terms; after being hedged into euro, however, the yield advantage disappears. In terms of government bonds, euro investors really have no incentive to invest in U.S. Treasurys, hedged or unhedged (Chart 11). Given the Danish krone's peg to the euro, it is natural for euro investors to look at the DMB market. Chart 12 shows that DMBs have indeed outperformed both government and corporate bonds in the euro area when 3-month deposit rate turns negative. During the 2008 financial crisis, DMBs also outperformed euro area corporate bonds. However, they did underperform both euro area corporate and government bonds when the European Central Bank started buying bonds after the euro debt crisis. So, how would the exposure of DMBs impact a portfolio's risk/return profile? We have two interesting observations from Chart 13: Chart 11Rate Advantage Vs. Currency Risk

Rate Advantage Vs. Currency Risk

Rate Advantage Vs. Currency Risk

Chart 12DMBs For Euro Investors

DMBs For Euro Investors

DMBs For Euro Investors

Chart 13DMBs As A Domestic Bond Substitute?

DMBs As A Domestic Bond Substitute?

DMBs As A Domestic Bond Substitute?

In Japan, hedged DMBs have a very low correlation with equities, corporate bonds and JGBs, even though the correlation with equities has generally been negative, and with bonds generally positive. In the euro area, DMBs have a negative correlation with equities, but a highly positive correlation with both government and corporate bonds. And the correlation to government bonds is quite similar to that of corporate bonds. Therefore, in theory, replacing part of a standard bond portfolio with DMBs could improve a balanced portfolio's risk/return profile for both Japanese and euro area investors. Table 4 shows the risk/return profiles of hypothetical 60/40 standard domestic equity/bond portfolios for Japan and euro area that have a certain percentage of domestic bonds replaced with Danish mortgage bonds: for Japan, the DMBs are hedged to yen, and for the euro area they are unhedged but converted into euros. Table 460/40 Equity/Bond Portfolio Profile with DMB Exposures

Searching For Yield In A Low-Return Environment

Searching For Yield In A Low-Return Environment

As expected, for Japan, substituting domestic aggregate bonds with hedged DMBs increases portfolio return more than volatility, thereby improving risk/adjusted returns. For the euro area, however, the story is not straightforward. Over a longer time frame, DMBs have not been a good substitute for euro area aggregate bonds. Since the 3-month euro rate turned negative in June 2015, however, DMBs have largely improved a balanced portfolio's risk/return profile. It is also worth noting that, unlike Japanese investors who benefit from a positive hedging gain since the Danish three-month rate has been lower than Japan's since 2015, euro area investors do not have such a benefit. Also, even though the DMB market is the largest covered bond market in the world, its market size is less than half a trillion USD. Given the fact that foreign investors already account for about a quarter of the market, it is not clear how euro area investors can significantly deploy more capital to enhance portfolio returns. Xiaoli Tang, Associate Vice President xiaoliT@bcaresearch.com Appendix 1: The Danish Mortgage Act4 Danish mortgage bonds are issued under the Danish Mortgage Act. Two key features of the Act protect investors in DMBs. First, the central element in the Danish Mortgage Act is the "balancing principle." This principle requires that there is a match between the inflows and outflows of a mortgage-issuing bank, and limits the amount of risk (interest rate, FX, volatility and liquidity) that a Danish mortgage bank can undertake. In addition, Danish mortgage banks must meet minimum capital requirements of 8% of risk-weighted assets. Second, the "Danish title number and land registration systems and efficient compulsory sale procedure" ensures well-defined property rights through a general register of all properties in Denmark. Ownership and encumbrances on individual properties are easily identified, and that information is available to the public. If a borrower defaults on a payment, the mortgage bank can take over the property and the compulsory sale procedure ensures that a mortgage bank can sell the property in the real estate market or through a forced sale. The period from default to a forced sale to be completed can be as short as six months. 1 Please see Global Investment Strategy Special Report entitled, "Three Policy Puts Go Kaput: Downgrade Global Equities To Neutral," dated June 20, 2018. 2 Please see "Fixed Rate Mortgage Bonds Are Attractive For Foreigners," Portfolio Investment, Danmarks Nationalbank, dated August 28, 2018. 3 Please see "Fixed Rate Mortgage Bonds Are Attractive For Foreigners," Portfolio Investment, Danmarks Nationalbank, dated August 28, 2018. 4 Please see "Danish Covered Bond Handbook," Danske Bank, dated September 15, 2017.

Dear Client, I am travelling in Europe this week visiting clients. Instead of our Weekly Report, we are sending you a Special Report written by my colleague Xiaoli Tang of BCA's Global Asset Allocation. The report examines three types of instruments investors can look to in order to enhance risk-adjusted portfolio returns at a time when interest rates and inflation are low but rising: floating-rate notes, leveraged loans and Danish mortgage bonds. I trust you will find it informative. Best regards, Peter Berezin, Chief Global Strategist Highlights In an environment where both interest rates and inflation are low but rising at a time of stretched equity valuations, what can investors do to enhance risk-adjusted portfolio returns? In this report, we investigate the roles of three types of popular instruments in a portfolio context: 1) Floating-Rate Notes, 2) Leveraged Loans and 3) Danish Mortgage Bonds. Floating-rate notes benefit from rising interest rates, but they are not a free lunch. Leveraged loans also benefit from rising interest rates; their very high correlation with high-yield bonds make them a good substitute for a portion of high-yield exposure in a rising-rate environment. Danish mortgage bonds have attracted foreign investors in recent years, but foreign ownership already accounts for about a quarter of the less than half a trillion USD market. Their positive correlation with aggregate bonds and negative correlation with equities in both Japan and the euro area make them a possible substitute for a portion of the bond basket in a balanced portfolio. Feature BCA has upgraded cash to overweight in the current environment, where inflation and interest rates are both low but rising, and equity valuations are stretched.1 For U.S. investors, holding cash is quite attractive as the cash yield is now higher than the equity dividend yield. For investors in the euro area, Switzerland, Sweden, Denmark and Japan, however, holding cash actually is a sure way to eat into portfolio returns, given the negative yields in these countries (Table 1). Table 1Current Yields* (%)

Searching For Yield In A Low-Return Environment

Searching For Yield In A Low-Return Environment

Some clients, particularly those in Europe, have asked where to put cash to get higher returns. Unfortunately, it's hard to increase return without assuming additional risk. As shown in Table 1, investors could pick up some yield by putting money in 3-month deposits instead of 3-month Treasury bills, but even 3-month deposit rates are still negative in some European countries. In this report, we investigate the roles of three types of popular instruments in a low but rising rate environment: 1) Floating-Rate Notes (FRNs), 2) Leveraged Loans (LLs) and 3) Danish Mortgage Bonds (DMBs). 1. Floating-Rate Notes An FRN offers coupon payments that float or adjust periodically based on a predetermined benchmark rate. Typical benchmarks in the U.S. are Treasury bills, LIBOR, the prime rate or some other short-term interest rate. Once the benchmark is chosen, the issuer will establish an additional spread that it is willing to pay over the chosen benchmark rate. The spread mainly reflects an issuer's credit quality and the time to maturity of the note. Even though coupon reset frequency can vary between daily, weekly, monthly, quarterly and yearly, the average coupon rate has responded quickly to the fed funds rate, as shown in Chart 1. Issuers can be both government-sponsored enterprises and investment-grade corporations. Before the 2008 Great Financial Crisis, FRNs were mostly issued by corporations. Some of the notes, however, performed badly during the financial crisis, causing a drop in both total issuance and the share of corporate issuance (Chart 2). FRNs can be either callable or non-callable with or without caps and floors, so FRNs carry credit risk - and callable ones also carry call risk. In terms of interest rate risk, it applies mostly to the income received. Chart 1Rising Rate Environment Benefits FRNs

Rising Rate Environment Benefits FRNs

Rising Rate Environment Benefits FRNs

Chart 2Corporate Dominance In FRN Market

Corporate Dominance In FRN Market

Corporate Dominance In FRN Market

Because of the nature of floating rates, FRNs can benefit from rising interest rates and have limited price sensitivity to interest rates. As shown in Chart 3, the Bloomberg/Barclays U.S. Floating-Rate Note index has lower duration than the cash index, as represented by the Bloomberg/Barclays Treasury (<1 year) index, while it offers a nice yield pickup. Since the inception of the index in December 2003 it has, in general, outperformed the cash index. This reward, however, has come at a cost: it does not provide cash-like protection when such protection is needed in times like the Great Financial Crisis and the euro debt crisis in 2011 (Chart 3, panels 3 and 4). This is because the majority of FRNs are offered by corporations that carry credit risk. Consequently, FRNs have higher correlations to high-yield bonds and equities than to the aggregate bond index, as shown in Chart 4. Chart 3FRNs: Not A Free Lunch

FRNs: Not A Free Lunch

FRNs: Not A Free Lunch

Chart 4FRNs: A Lower Risk Alternative To Junk Bonds

FRNs: A Lower Risk Alternative To Junk Bonds

FRNs: A Lower Risk Alternative To Junk Bonds

The ideal time to invest in FRNs is when rates are low and are expected to rise. This is essentially our view on rates now. Instead of thinking of it as a cash alternative with higher risk, however, we recommend clients take the funding from the high-yield bucket, in line with our downgrade of high yield to neutral from overweight, and also our call of reducing portfolio duration. So how to invest in FRNs? According to Bloomberg Barclays, the U.S. FRN market has a market value of US$505.8 billion, which is small compared to the US$1,267.5 billion high-yield bond market. As such, FRNs are relatively less liquid to trade than corporate bonds. Therefore, they are mostly suitable for purchasing and holding to maturity. One can purchase individual floating-rate securities through a broker, or can invest in mutual funds that invest only in FRNs. Also, there are ETFs that only hold FRNs. Table 2 shows some basic information on three dedicated FRN ETFs. Table 2FRN ETFs*

Searching For Yield In A Low-Return Environment

Searching For Yield In A Low-Return Environment

2. Leveraged Loans Leveraged loans, also known as bank loans or senior secured loans, are a type of corporate debt that also have floating coupon rates, which, like the FRNs, adjust to changes in prevailing interest rates and hence benefit from rising rates. These loans tend to be senior to an issuer's traditional corporate bonds, and are collateralized by a pledge of the issuer's assets. However, secured does not mean safe. These loans are private investments which are generally held by funds or large institutional investors. Most of them carry sub-investment-grade ratings and can default. They also tend to be very illiquid to trade, because physical delivery to the buyer is often needed from a seller (by faxing the paperwork, for example). As such, during periods of market volatility, these loans can be subject to significant price declines. Even though bank loans share the same feature of having "floating coupon rates" as FRNs, they are higher risk securities. In the U.S., bank loans have been mostly inferior to FRNs on a risk-adjusted return basis, as their higher return is offset by much higher volatility (Chart 5A). In the euro area, however, these loans have become more favorable than FRNs since the start of 2018 (Chart 5B). Chart 5ALeveraged Loans Vs. FRNs: U.S.

Leveraged Loans Vs. FRNs: U.S.

Leveraged Loans Vs. FRNs: U.S.

Chart 5BLeveraged Loans Vs. FRNs: Euro Area

Leveraged Loans Vs. FRNs: Euro Area

Leveraged Loans Vs. FRNs: Euro Area

Historically, when interest rates have risen, bank loans have outperformed traditional fixed-income securities, and vice versa, because of their floating-rate feature, as shown in Charts 6A and 6B. This positive correlation with rates has been more consistent when the relative performance of bank loans is compared to government bonds and investment-grade corporate bonds. When compared to high-yield bonds, however, the correlation appears weak, as shown in the bottom panels of Charts 6A and 6B. This is not surprising given that these loans share similar "sub-investment grade" credit quality with junk bonds. In fact, as shown in Chart 7, bank loans have a highly positive correlation with junk bonds, yet a mostly negative correlation with the aggregate bond index both in the U.S. and the euro area. Chart 6ALLs Outperform When Rates Rise: U.S.

LLs Outperform Whe Rates Rise: U.S.

LLs Outperform Whe Rates Rise: U.S.

Chart 6BLLs Outperform When Rates Rise: Euro Area

LLs Outperform When Rates Rise: Euro Area

LLs Outperform When Rates Rise: Euro Area

Chart 7Bank Loan Correlations With Traditional Bonds

Bank Loan Correlations With Traditional Bonds

Bank Loan Correlations With Traditional Bonds

This correlation feature has two very interesting implications: a) Adding bank loans to a standard aggregate bond portfolio could add diversification, and b) replacing some high-yield holdings with bank loans could generate a sub-investment grade basket with a better risk/reward profile compared to high-yield alone. Chart 8 and Table 3 show that historically there has existed an "optimal" combination of bank loans and high-yield bonds that somewhat improves the risk-adjusted return of the sub-investment grade basket. It's worth noting, however, that this historically "optimal" combination is subject to data frequency and time period, as is the case for the U.S. where the optimal weight for bank loans has been about 40% from 2002 to the present, but about 80% in the period from 1997 to the present. As such, in addition to thorough credit analysis to evaluate the suitability of bank loans, investors should also consider the variable nature of correlation when considering replacing part of their high-yield bond exposure with bank loans. Chart 8Junk Bonds - Leverage Loans Basket Profiles

Searching For Yield In A Low-Return Environment

Searching For Yield In A Low-Return Environment

Table 3Risk Return Profiles Of Sub-Investment Grade Baskets

Searching For Yield In A Low-Return Environment

Searching For Yield In A Low-Return Environment

3. Danish Mortgage Bonds A Danish mortgage bond (DMB) is essentially a loan to a borrower who has taken out a mortgage on his or her home. Mortgage bonds are issued by mortgage credit institutions which often have high credit ratings. Some DMBs have fixed rates, while others have floating rates with a minimum of zero percent. Some of these bonds can also be callable, often at par (100). With a solid history of over 200 years, the DMB market has survived numerous occasions of economic and political turmoil, including the bankruptcy of the Kingdom of Denmark in 1813, the Great Depression of the 1930s and the Great Financial Crisis and ensuing recession in 2008. Over its entire history, every single issued bond has been repaid in full to investors, in large part due to the strong legislative framework that protects the bond investors (see Appendix 1). As of the end of July 2018, the DMB market consisted of kr. 2.672 trillion of AAA-rated covered bonds. Once largely dominated by local pensions and insurance companies, the DMB market has seen increasing interest from foreign investors in recent years. According to data from the Danish central bank, foreign ownership of fixed rate mortgage bonds stood at kr. 295 billion (29%) in July 2018 compared to kr. 154 billion (18%) in January 2016 (Chart 9). In terms of total holdings of all mortgage bonds (fixed rate, variable rate and bonds backing interest adjustment loans), foreigners held kr. 614 billion (23%), an increase of kr. 27 billion compared to the beginning of 2016. Japanese investors, who have suffered many years of extremely low yields domestically, have been quite active in the DMB market. According to data from the Bank of Japan, Japanese investors purchased some kr. 50 billion of long-term Danish non-government bonds in the period from 2016 to June 2018.3 In June 2018, Nykredit, the largest Danish mortgage bank with a market share of about 40%, even created a DMB index hedged to yen using one-month forward rates due to popular demand and corresponding requests from Japanese investors. As shown in Chart 10, since 2009, the DMB index hedged to yen has outperformed both JGBs and Japanese corporate bonds. Chart 9Foreign Ownership of Danish Fixed Rate Mortgage Bonds*

Searching For Yield In A Low-Return Environment

Searching For Yield In A Low-Return Environment

Chart 10DMBs For Japanese Investors

DMBs For Japanese Investors

DMBs For Japanese Investors

Even though interest rates in the U.S. are much higher than those in the euro area, investing in the U.S. after hedging the currency is not really attractive for euro investors. For example, U.S. bank loans have outperformed European bank loans in local currency terms; after being hedged into euro, however, the yield advantage disappears. In terms of government bonds, euro investors really have no incentive to invest in U.S. Treasurys, hedged or unhedged (Chart 11). Given the Danish krone's peg to the euro, it is natural for euro investors to look at the DMB market. Chart 12 shows that DMBs have indeed outperformed both government and corporate bonds in the euro area when 3-month deposit rate turns negative. During the 2008 financial crisis, DMBs also outperformed euro area corporate bonds. However, they did underperform both euro area corporate and government bonds when the European Central Bank started buying bonds after the euro debt crisis. So, how would the exposure of DMBs impact a portfolio's risk/return profile? We have two interesting observations from Chart 13: Chart 11Rate Advantage Vs. Currency Risk

Rate Advantage Vs. Currency Risk

Rate Advantage Vs. Currency Risk

Chart 12DMBs For Euro Investors

DMBs For Euro Investors

DMBs For Euro Investors

Chart 13DMBs As A Domestic Bond Substitute?

DMBs As A Domestic Bond Substitute?

DMBs As A Domestic Bond Substitute?

In Japan, hedged DMBs have a very low correlation with equities, corporate bonds and JGBs, even though the correlation with equities has generally been negative, and with bonds generally positive. In the euro area, DMBs have a negative correlation with equities, but a highly positive correlation with both government and corporate bonds. And the correlation to government bonds is quite similar to that of corporate bonds. Therefore, in theory, replacing part of a standard bond portfolio with DMBs could improve a balanced portfolio's risk/return profile for both Japanese and euro area investors. Table 4 shows the risk/return profiles of hypothetical 60/40 standard domestic equity/bond portfolios for Japan and euro area that have a certain percentage of domestic bonds replaced with Danish mortgage bonds: for Japan, the DMBs are hedged to yen, and for the euro area they are unhedged but converted into euros. Table 460/40 Equity/Bond Portfolio Profile with DMB Exposures

Searching For Yield In A Low-Return Environment

Searching For Yield In A Low-Return Environment

As expected, for Japan, substituting domestic aggregate bonds with hedged DMBs increases portfolio return more than volatility, thereby improving risk/adjusted returns. For the euro area, however, the story is not straightforward. Over a longer time frame, DMBs have not been a good substitute for euro area aggregate bonds. Since the 3-month euro rate turned negative in June 2015, however, DMBs have largely improved a balanced portfolio's risk/return profile. It is also worth noting that, unlike Japanese investors who benefit from a positive hedging gain since the Danish three-month rate has been lower than Japan's since 2015, euro area investors do not have such a benefit. Also, even though the DMB market is the largest covered bond market in the world, its market size is less than half a trillion USD. Given the fact that foreign investors already account for about a quarter of the market, it is not clear how euro area investors can significantly deploy more capital to enhance portfolio returns. Xiaoli Tang, Associate Vice President xiaoliT@bcaresearch.com Appendix 1: The Danish Mortgage Act4 Danish mortgage bonds are issued under the Danish Mortgage Act. Two key features of the Act protect investors in DMBs. First, the central element in the Danish Mortgage Act is the "balancing principle." This principle requires that there is a match between the inflows and outflows of a mortgage-issuing bank, and limits the amount of risk (interest rate, FX, volatility and liquidity) that a Danish mortgage bank can undertake. In addition, Danish mortgage banks must meet minimum capital requirements of 8% of risk-weighted assets. Second, the "Danish title number and land registration systems and efficient compulsory sale procedure" ensures well-defined property rights through a general register of all properties in Denmark. Ownership and encumbrances on individual properties are easily identified, and that information is available to the public. If a borrower defaults on a payment, the mortgage bank can take over the property and the compulsory sale procedure ensures that a mortgage bank can sell the property in the real estate market or through a forced sale. The period from default to a forced sale to be completed can be as short as six months. 1 Please see Global Investment Strategy Special Report entitled, "Three Policy Puts Go Kaput: Downgrade Global Equities To Neutral," dated June 20, 2018. 2 Please see "Fixed Rate Mortgage Bonds Are Attractive For Foreigners," Portfolio Investment, Danmarks Nationalbank, dated August 28, 2018. 3 Please see "Fixed Rate Mortgage Bonds Are Attractive For Foreigners," Portfolio Investment, Danmarks Nationalbank, dated August 28, 2018. 4 Please see "Danish Covered Bond Handbook," Danske Bank, dated September 15, 2017. Strategy & Market Trends Tactical Trades Strategic Recommendations Closed Trades

Highlights An inflation scare would initially take bond yields higher. But the higher bond yields would undermine the valuation support of global risk-assets worth several times the size of the global economy. Thereby, an inflation scare could unleash a potentially much larger disinflationary scare. And the subsequent decline in yields would exceed the original rise. Using the 10-year T-bond yield for our roadmap (because it is least impacted by the lower bound to yields) a short trip to the uplands of 3.5% would precede a longer journey down to 2%. Feature The global long bond yield has been trapped within a tight sideways channel for almost two years (Chart of the Week); the global equity market has also lacked any clear direction in recent quarters (Chart I-2). The result is that this year's defining feature for asset-class returns is that there is no defining feature! Global equities, bonds and cash have delivered near-identical returns.1 Chart Of The WeekThe Global Long Bond Yield ##br##Has Been Trapped

The Global Long Bond Yield Has Been Trapped

The Global Long Bond Yield Has Been Trapped

Chart I-2World Equities Have Drifted ##br##Sideways This Year

At Higher Bond Yields, The Correlation With Equity Prices Has Flipped From Positive To Negative

At Higher Bond Yields, The Correlation With Equity Prices Has Flipped From Positive To Negative

This is not to say that 2018 has been a dull year for investors. Far from it. But all the action has been underneath the main asset allocation decision, across sectors, regions and countries. For example, European healthcare has outperformed European banks by 35 percent; and developed market equities have outperformed emerging market equities by 15 percent (Chart I-3 and Chart I-4). Chart I-3The Main Action Has Been Across Sectors...

The Main Action Has Been Across Sectors...

The Main Action Has Been Across Sectors...

Chart I-4...And Across Regions

...And Across Regions

...And Across Regions

Unshackling Bond Yields Might Be Difficult In the major developed economies, unemployment rates keep hitting new generational lows, implying that the main labour markets are tight. Yet policy interest rates range from a crisis-level negative 0.4 percent in the euro area to just 0.75 percent in the U.K. to a modest 2 percent in the U.S. This raises the potential for an inflation scare. At any moment, the bond market might panic that central banks are well behind the (Phillips) curve.2 The spike in bond yields would of course unleash a countervailing disinflationary feedback, by cooling credit growth and credit-sensitive sectors in the economy. But this feedback would take weeks or months to take effect and to show up in the economic data. Until then, it would liberate bond yields to reach higher ground. However, there would be a more powerful and immediate feedback which would keep the shackles on bond yields. That feedback would come not from the economy, but from the financial markets themselves. In Finance 101, all investment students learn that the valuations of risk-assets depend (inversely) on bond yields. But what is less well understood is that at very low bond yields this relationship becomes exponential. Approaching the lower bound of bond yields, bonds become doubly ugly. Not only do they offer feeble returns, but the bond returns take on an unattractive asymmetry. Specifically, you can no longer make a sudden large gain, but you can still suffer a sudden deep loss. In effect, bonds become much riskier investments.3 Confronted with this increased riskiness of bonds, 'risk-assets' becomes a misnomer because risk-assets are no longer riskier than bonds! This requires risk-asset returns to collapse to the feeble return offered by bonds with no additional 'risk-premium', giving their valuations an exponential uplift (Chart I-5). The big problem is that if bond yields normalise, the process goes into sharp reverse - the lofty valuations of risk-assets must decline as exponentially as they rose. Chart I-5At Low Bond Yields ##br##The Valuation Of Equities Changes Exponentially

Trapped: Have Equities Trapped Bonds?

Trapped: Have Equities Trapped Bonds?

The global bond yield appears close to this crossover point at which risk-asset valuations become vulnerable to an exponential derating. In the past year, whenever the global bond yield has reached the upper limits of its recent range - defined by the sum of 10-year yields on the U.S. T-bond, German bund, and JGB reaching 3.5 percent - the correlation between bond yields and equities has turned sharply negative (Chart I-6). And the subsequent sell-off in equities has eventually pegged back the rise in bond yields, effectively trapping them. Chart I-6At Higher Bond Yields The Correlation With Equity Prices Has Flipped From Positive To Negative

At Higher Bond Yields The Correlation With Equity Prices Has Flipped From Positive To Negative

At Higher Bond Yields The Correlation With Equity Prices Has Flipped From Positive To Negative

But what would happen if there were an inflation scare? The answer depends on the relative sizes of the inflationary impulse compared with the disinflationary impulse that resulted from sharply lower risk-asset prices. If central banks were more concerned about the inflationary impulse, they would have to keep tightening - in which case, bond yields would be liberated to reach elevated territory. Conversely, if the bigger worry was the disinflationary impulse, central banks would quickly reverse course, and bond yields would return to the lowlands. We now explain why the disinflationary impulse from lower risk-asset prices would end up as the bigger worry. An Inflation Scare Would Be Disinflationary The current episode of elevated risk-asset valuations is not unprecedented, but there is a crucial difference. Previous episodes of elevated risk-asset valuations tended to be localised, either by geography or sector: 1990 was focussed in Japan; 2000 was focussed in the dot com related sectors; 2008 was focussed in the U.S. mortgage and credit markets and preceded the emerging market credit boom (Chart I-7). Chart I-7The Emerging Market Boom Happened After 2008

The Emerging Market Boom Happened After 2008

The Emerging Market Boom Happened After 2008

By comparison, the post-2008 global experiment with quantitative easing, and zero and negative interest rate policy has boosted the valuations of all risk-assets across all geographies and all asset-classes - global equities (Chart I-8), global credit (Chart I-9), and global real estate. This makes it considerably more dangerous, because we estimate that the total value of global risk-assets is $400 trillion, equal to about five times the size of the global economy. Chart I-8Elevated Valuations On Global Equities

Elevated Valuations On Global Equities

Elevated Valuations On Global Equities

Chart I-9Elevated Valuations On Global Credit

Elevated Valuations On Global Credit

Elevated Valuations On Global Credit

Let's say you had an investment that was priced to generate 5 percent a year over the next decade. Now imagine that the valuation boost from ultra-accommodative monetary policy capitalises all of those future returns to today. For those future returns to drop to zero, today's price must surge by 63 percent.4 If you were prudent, you might amortise today's windfall to generate the original 5 percent a year over the next decade. But if you were imprudent, you might spend a large amount of the windfall today. Now let's imagine a valuation derating moves the investment's returns back to the future. For those that had prudently amortised the original windfall, nothing has really changed and future spending patterns would not be impacted. But not everybody is prudent. For those that had imprudently spent the original windfall, future spending would inevitably suffer a nasty recession. The key takeaway is that any inflationary impulse would - through higher bond yields - undermine the valuation support of global risk-assets worth several times the size of the global economy. Thereby, it could unleash a potentially much larger disinflationary impulse. A Roadmap For An Inflation Scare The high sensitivity of risk-asset valuations to bond yields is the genesis of our 'rule of 4' strategy for equity allocation, which is based on the sum of the 10-year yields on the U.S. T-bond, German bund and JGB: Above 3.5 is the level to go to a neutral exposure to equities; above 4 is the level to go underweight. Today, our metric stands at exactly 3.5 (Chart I-10). Chart I-10The 'Rule Of 4' Is At 3.5

10. The 'Rule Of 4' Is At 3.5

10. The 'Rule Of 4' Is At 3.5

For bonds, this means that 4 on this metric is also a good level to buy a mixed portfolio of high-quality 10-year government bonds. The equivalent level for high-quality 30-year government bonds is 5.5 (using the sum of the three 30-year yields). To sum up, an inflation scare would initially take bond yields higher. But this would threaten to unleash a much larger disinflation scare, causing the subsequent decline in yields to exceed the original rise. Using the 10-year T-bond yield as an illustration - as it is least impacted by the lower bound to yields - this would suggest the following roadmap: a short trip to the uplands of 3.5% would precede a longer journey down to 2%. Dhaval Joshi, Senior Vice President Chief European Investment Strategist dhaval@bcaresearch.com 1 The global long bond yield is captured by the simple average of the 30-year yields on the U.S. T-bond, German bund and Japanese government bond (JGB). The global equity market is captured by the MSCI All Country World Index in local currency terms. 2 The -0.4 percent refers to the ECB deposit rate. 3 Please see the European Investment Strategy Weekly Report "The Rule Of 4 For Equities And Bonds," August 2, 2018, available at eis.bcaresearch.com. 4 5 percent compounded over ten years. Fractal Trading Model* This week’s recommended trade is an intra-commodity pair trade: short palladium/long copper. The profit target is 6% with a symmetrical stop-loss. In other trades, short euro area energy versus financials was closed at the end of its 65 trading day holding period, albeit in loss. This leaves five open trades. For any investment, excessive trend following and groupthink can reach a natural point of instability, at which point the established trend is highly likely to break down with or without an external catalyst. An early warning sign is the investment’s fractal dimension approaching its natural lower bound. Encouragingly, this trigger has consistently identified countertrend moves of various magnitudes across all asset classes. Chart I-11

Long Global Basic Resources, Short Global Chemicals

Long Global Basic Resources, Short Global Chemicals

Fractal Trading Model Recommendations Equities Bond & Interest Rates Currency & Other Positions Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights The U.S. midterm elections are far less investment-relevant than consensus holds; Trump will increase the pressure on China and Iran regardless of the likely negative election results for the GOP; The Iranian sanctions, civil conflict in Iraq, and other oil supply issues are the real geopolitical risk; Despite the tentative good news on Brexit, political uncertainty in the U.K. makes now a bad time to buy the pound; Go long Brent crude / short S&P 500; long U.S. energy / tech equities; long JPY / short GBP. Feature The U.S. political cycle begins in earnest after Labor Day. Understandably, we have noticed an uptick in client interest, with a steady stream of questions and conference call requests about U.S. politics. Generally, our forecast remains unchanged since our April net assessment of the upcoming midterm election.1 Democrats have a slightly better than 60% probability of winning the House of Representatives, with a solid 45% probability of taking the Senate, and rising. The latter is astounding, given that the "math" of the Senate rotation is against the Democrats. Our bias toward a Democratic victory is based on current polling (Chart 1) and President Trump's woeful approval rating (Chart 2). There are a lot of other moving parts, however, and we will update them next week in detail. Chart 1GOP Trails In Polls, But It Is Still Close

GOP Trails In Polls, But It Is Still Close

GOP Trails In Polls, But It Is Still Close

Chart 2Trump's Approval Rating Lines The GOP Up For Steep Losses

Fade The Midterms, Not Iraq Or Brexit

Fade The Midterms, Not Iraq Or Brexit