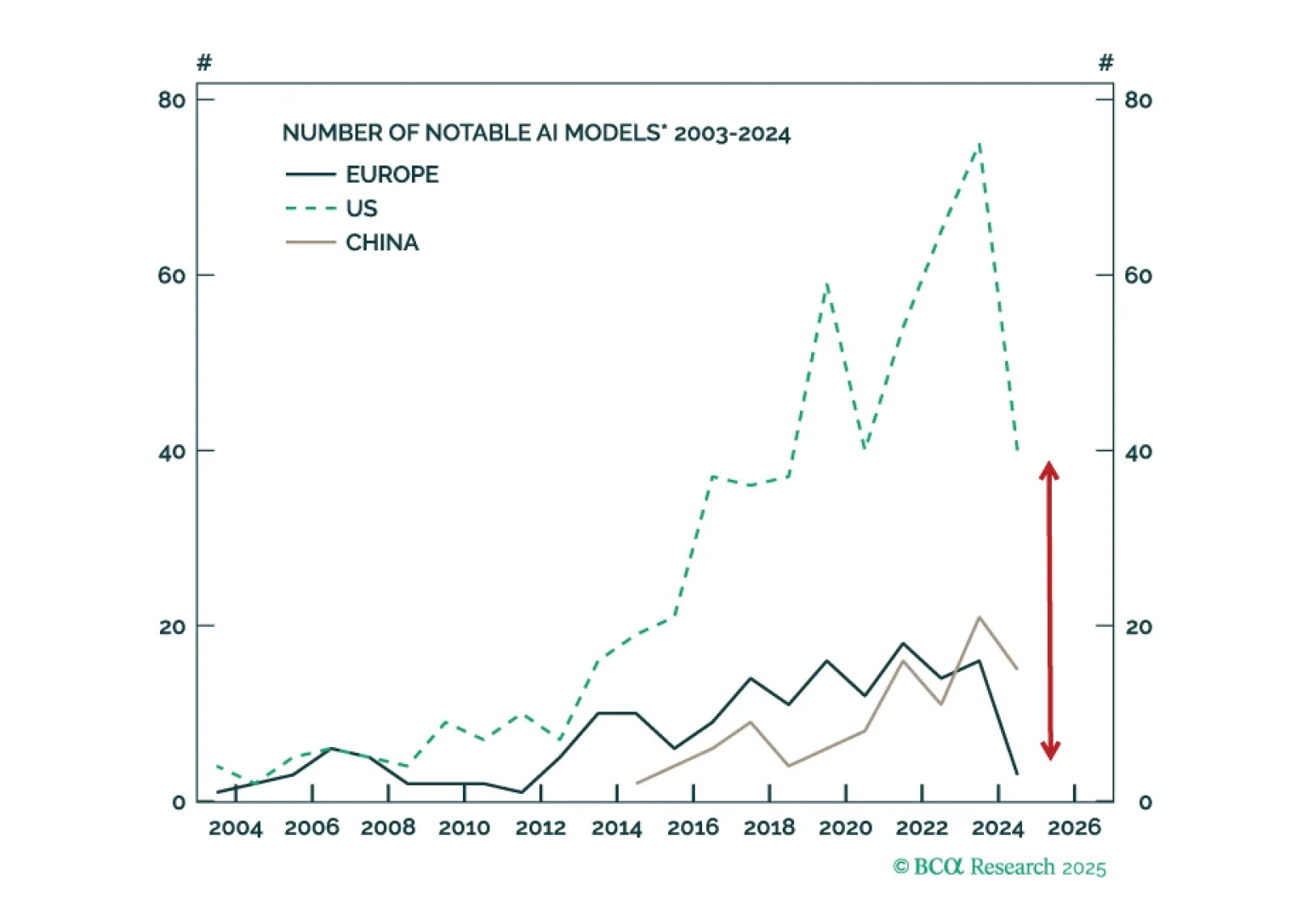

Europe

Europe is not left out of the AI race. Despite lagging US and China in LLMs and AI capex, Europe is quietly making progress where it matters, including industrial adoption. European capitals and the EU seem committed to not let that technology slip away, and are investing to support a “second-wave” role in AI. Scaling remains uneven, especially for SMEs, but will not prevent productivity gains in the region.

Markets are increasingly pricing an end to the global easing cycle, with many central banks expected to remain on hold. But uncertainty remains high, and policy surprises are likely going into 2026. This Strategy Report breaks down the current drivers behind G10 central bank policies, and how to position for the next moves across FX and fixed income.

Markets are increasingly pricing an end to the global easing cycle, with many central banks expected to remain on hold. But uncertainty remains high, and policy surprises are likely going into 2026. This Strategy Report breaks down the current drivers behind G10 central bank policies, and how to position for the next moves across FX and fixed income.

This week, our screeners explore opportunities arising from Europe’s electrification, identify high-quality Rare Earth plays, and propose a portfolio to hedge against a major global conflict.

In this week’s note, we share the main implications for European investors from what was discussed at the BCA Conference in New York and provide a short list of the questions most frequently asked by investors we met recently in Lisbon, Madrid, and Barcelona.

In this Q4 Strategy Outlook, we discuss where we stand on our recession call, the outlook for stocks and bonds in various scenarios, why investors are misunderstanding the impact of AI on corporate profits, whether the US dollar has entered a structural downtrend, our perspective on the yen, gold and other commodities, and much more.