Europe

After briefly breaking a 27-month streak of negative sentiment back in June, the Eurozone Sentix Economic index disappointed in August. The overall index worsened from July’s negative reading to -13.9, below expectations of a milder deterioration. The…

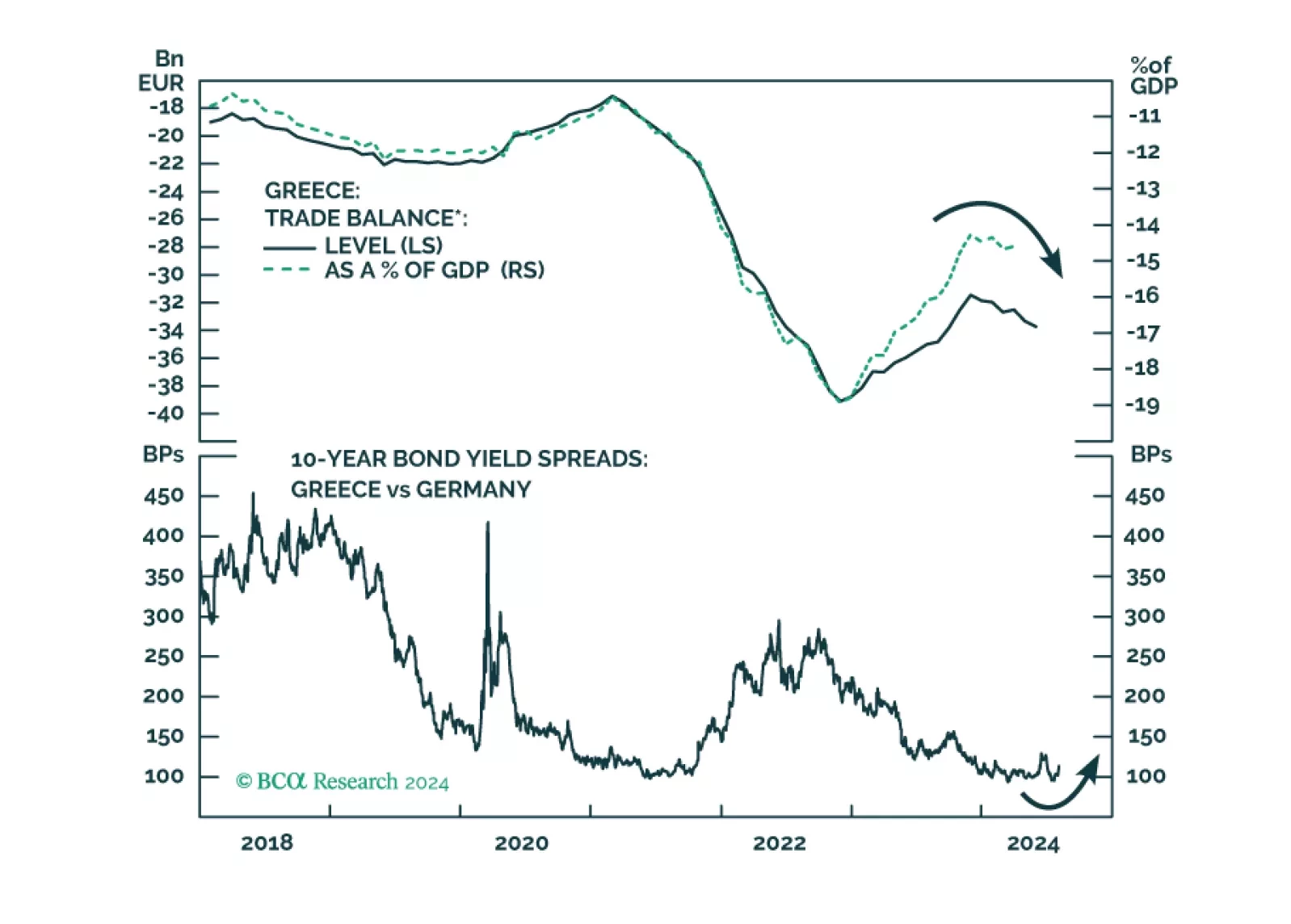

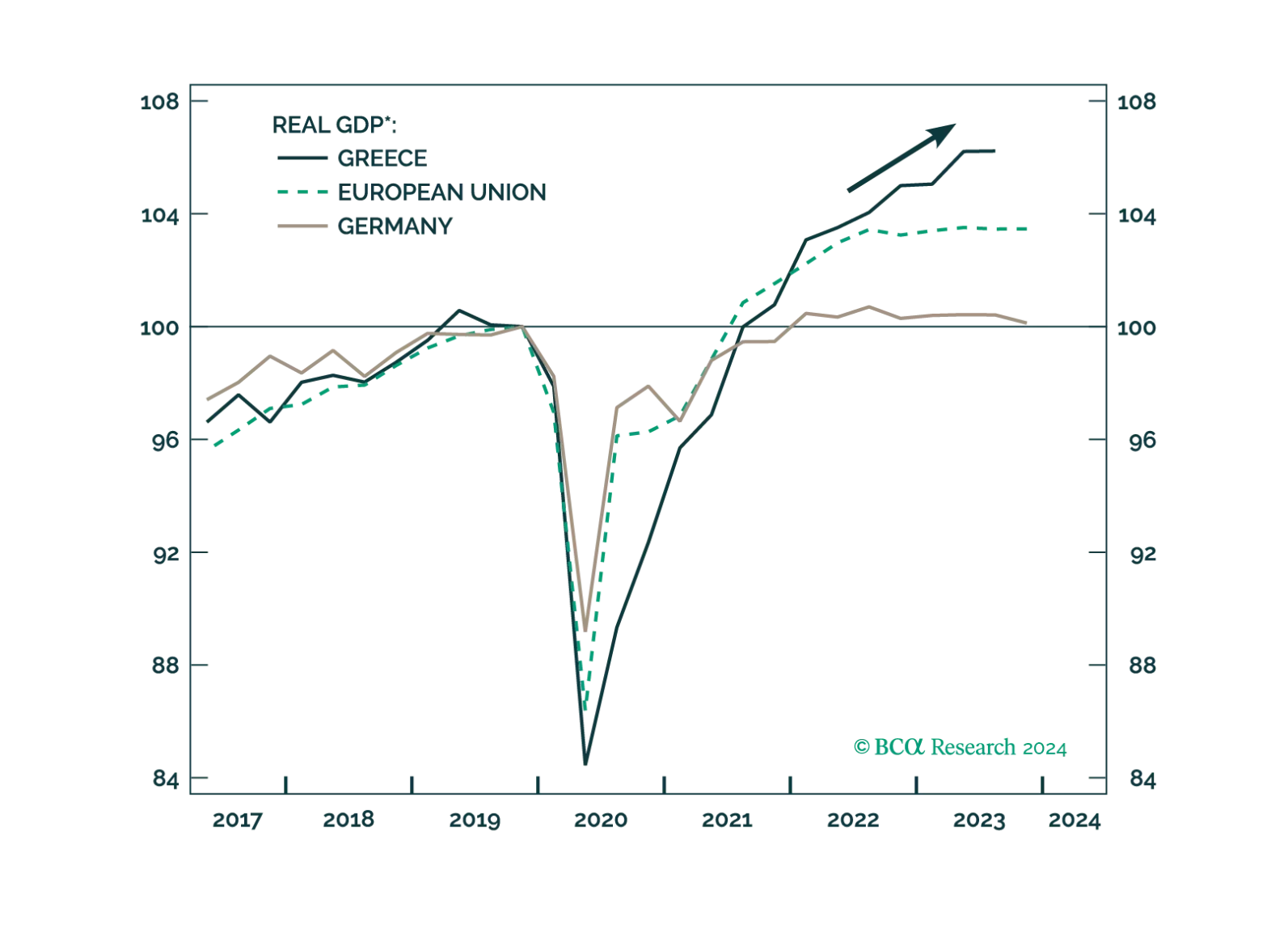

Absolute return investors should be tactically cautious on Greek assets. Dedicated EM equity portfolios, however, should overweight Greek stocks.

Greece has staged a surprising economic recovery in recent years. Greek risk assets are the best performers in Europe. Can it last?

The Bank of England (BoE) lowered its policy rate by 25 basis points to 5% at its meeting on Thursday. While the move was expected, the governing board was split, voting 5 – 4 in favor of reducing the key interest rate. The BoE cut its policy rate despite…

Sweden’s manufacturing PMI started contracting in July, plummeting from 53 to 49.2, falling far short of expectations that growth would broaden. Weakness was broad-based. Notably, new orders and new export orders plunged a whopping 15.1 and 8.7 points in…

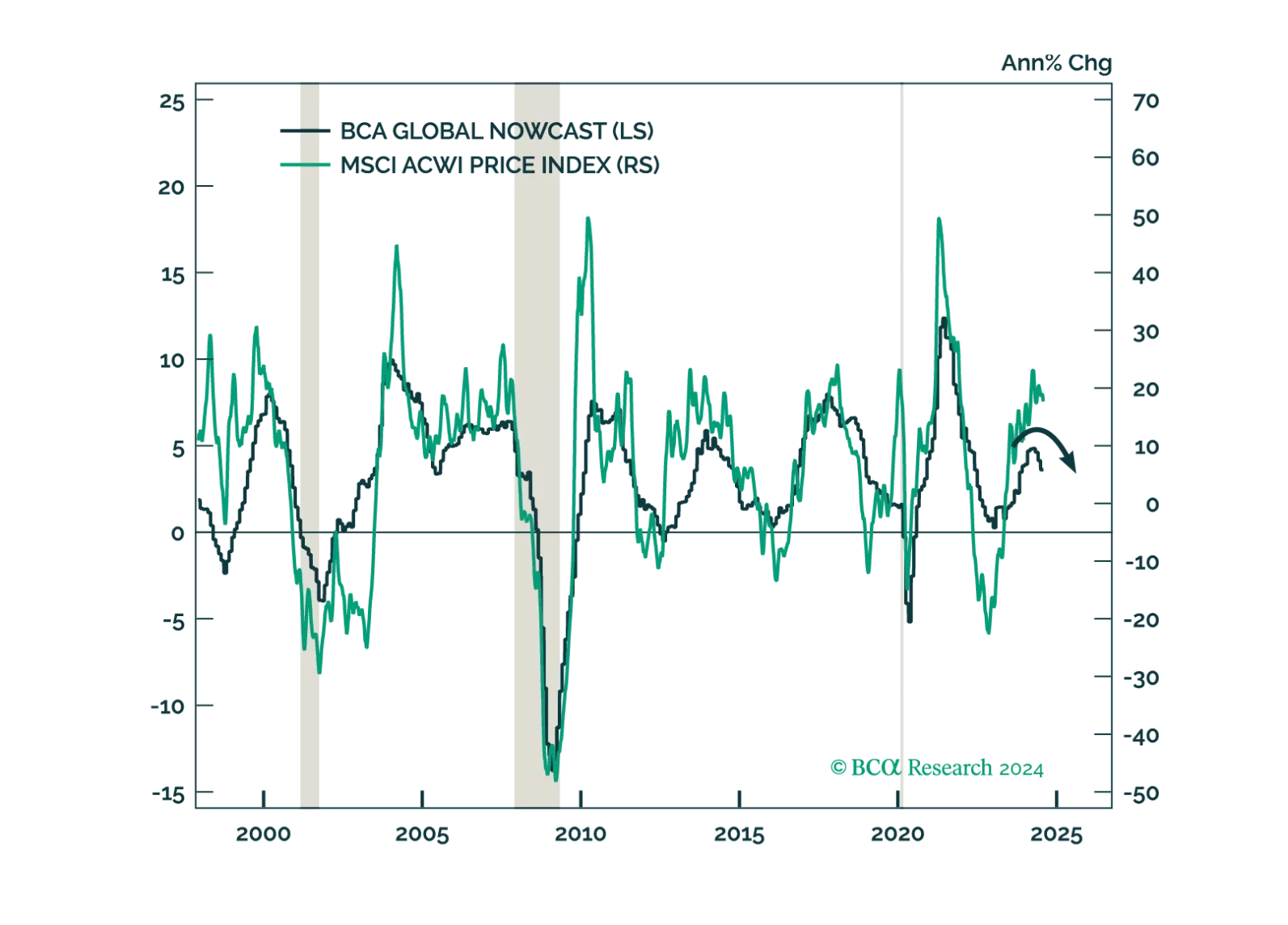

The market is pricing in a soft landing, but we see growing signs that the global economy is faltering. Investors should be defensively positioned.

Eurozone headline CPI inflation unexpectedly accelerated in July, from 2.5% y/y to 2.6%. Core CPI remained stable at 2.9% despite expectations it would ease. EU Harmonized CPI accelerated in the regions’ three largest economies, surprising by a large margin…

Preliminary estimates suggests that the Swedish economy unexpectedly contracted in Q2. The seasonally adjusted GDP Indicator declined by 0.8% q/q, following a 0.7% Q1 rise in actual GDP growth. Flash estimates lack details and are prone to revisions.…

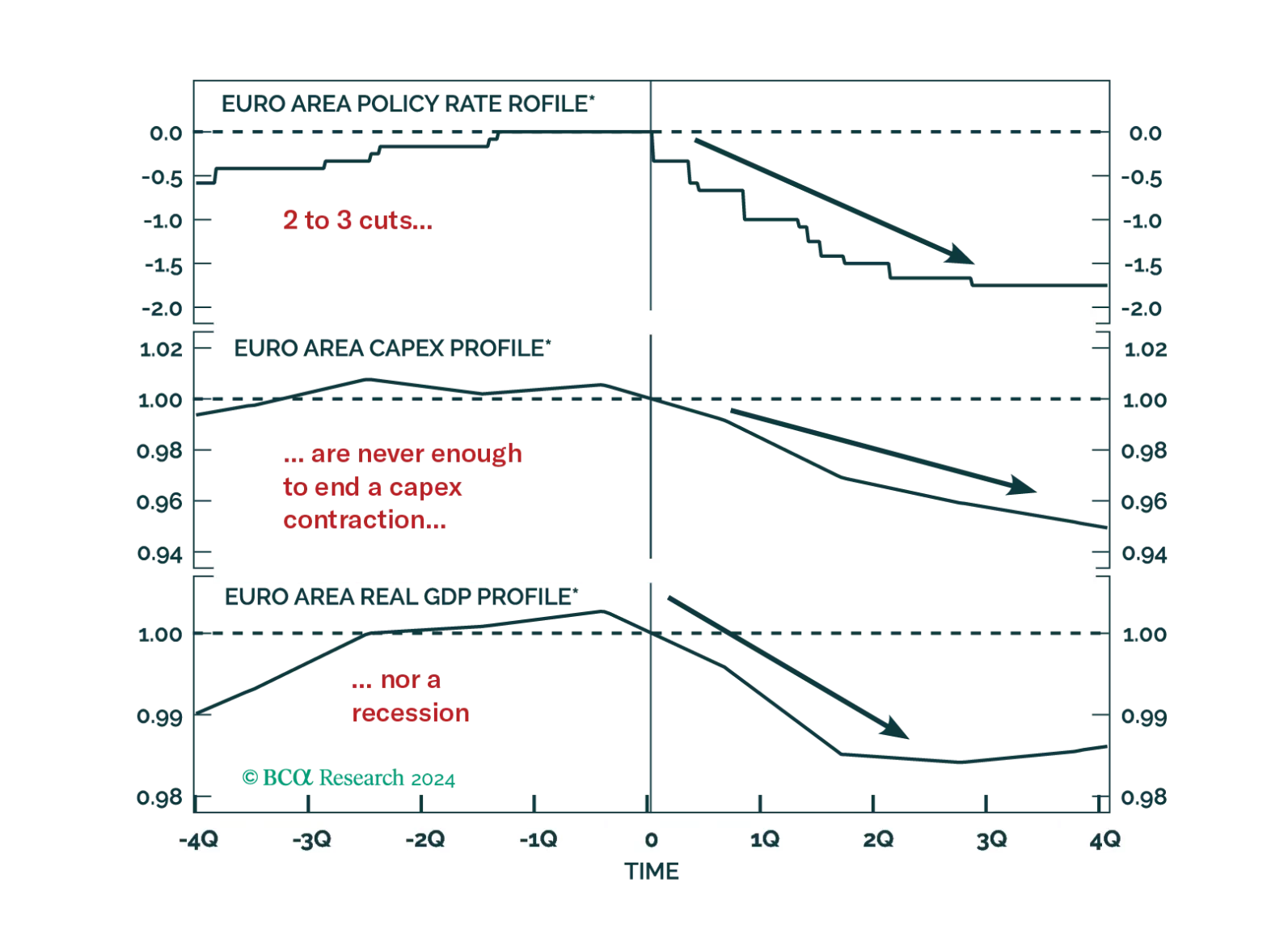

According to BCA Research’s European Investment Strategy service, a foreign shock is likely to tip the Eurozone economy into a recession because important vulnerabilities have emerged domestically. Policy is restrictive. Real interest rates stand 370bps…

Investors hope that the ECB rate cuts priced into the curve will be sufficient to achieve a soft landing in Europe. History argues against this view, but will this time be different?