Europe

The ECB delivered its first rate cut in June, moderating the degree of restriction rather than pivoting outright to easy monetary policy settings. Indeed, the rate cut was accompanied by an upward revision of inflation and growth forecasts. Since then,…

According to BCA Research’s China Investment Strategy service, Beijing will engage in ongoing negotiations with the EU regarding its import tax decision rather than impose meaningful retaliatory measures. The EU and China appear to be negotiating ahead of…

Eurozone equities sold off 7% from their June 6 highs, according to MSCI indices. The surprise French legislative elections and renewed fears of populism and European Union exits are spooking investors. Yet, our European Investment strategists argued that…

European assets are selling off as investors panic about the upcoming French election. Is this panic justified, and if so, for how long?

The BoE had to deal with a stagflationary headache in the second half of 2023. Inflation was stickier and growth was weaker in the UK than in many of its DM peers. This trend turned around earlier this year with a late-cycle growth reacceleration. The UK…

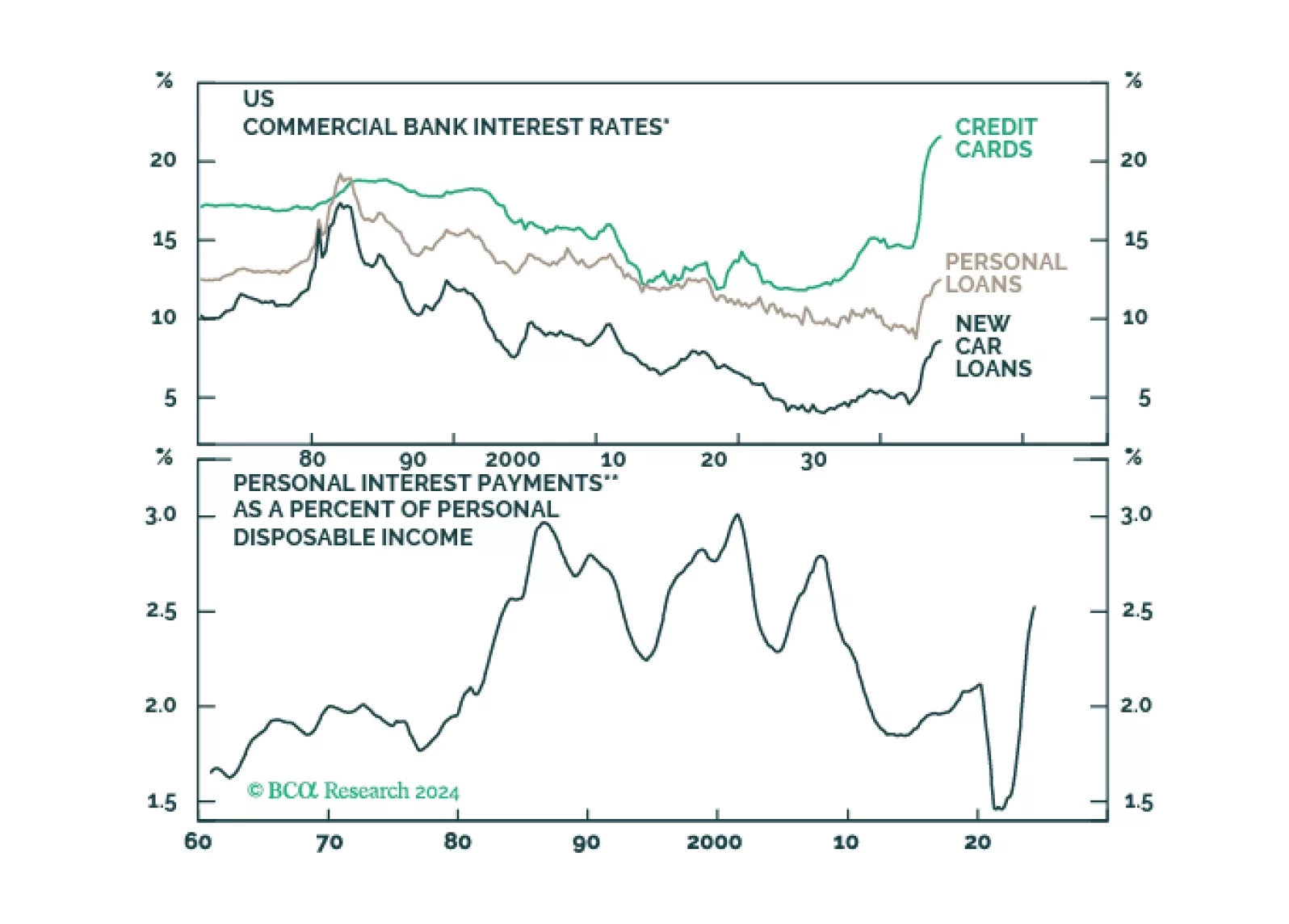

According to BCA Research’s Global Investment Strategy service, aggressive fiscal stimulus and labor market flexibility contributed to the relative strength of the US consumer. However, adverse region-specific effects also played a role. Most notably, the…

Global consumer spending is likely to slow over the coming quarters, culminating in a major economic downturn in late 2024 or early 2025. Investors should maintain benchmark exposure to equities for now but look to turn more defensive by the end of this summer.

On Wednesday, the European Commission announced it would impose tariffs ranging between 17% and 38% on imports of Chinese EVs starting next month. These duties will be applied on top of existing 10% across-the-board tariffs on all Chinese EV imports, and…

The UK unemployment rate surprised to the upside in the 3-month period ending in April, ticking up to 4.4% against expectations it would remain stable at March’s originally reported 4.3%. Concurrently, wage growth remains elevated. The 3-month measure of…

The Eurozone Sentix Economic index improved from -3.6 to 0.3 in June, easily surpassing expectations of a more muted improvement to -1.7. Notably, the Expectation and Current Situation subindices rose to 28-month and 13-month highs of 10 and -9, respectively.…