Europe

Preliminary GDP estimates suggest that the UK economy started growing again in Q1, thus exiting a technical recession in the past two quarters. Q1 growth came in at 0.6%, improving from a 0.3% contraction last quarter, surpassing expectations of 0.4%. On a…

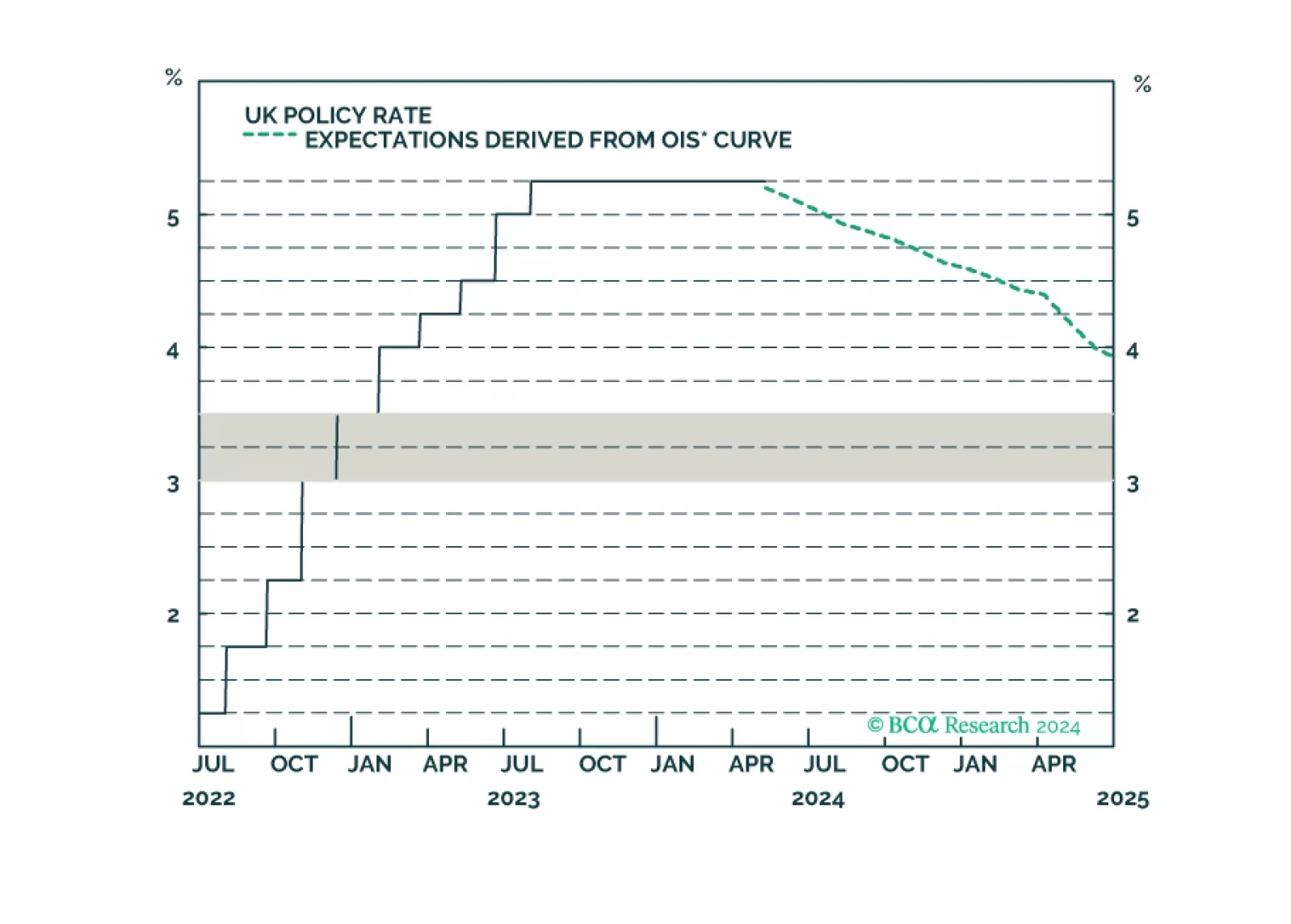

In a widely expected move, the Bank of England (BoE) maintained its policy rate at 5.25% in May. Nevertheless, two Committee Members voted in favor of cutting rates, one more than was anticipated. The tone of the report was overall dovish. The BoE…

An update to our views on UK rates and currency following today’s Bank of England meeting.

In a widely expected move, the Riksbank cut its policy rate by 25 basis points on Wednesday from 4% to 3.75%. The policy statement highlighted that inflation is approaching its 2% target, that leading indicators are pointing to further downside in prices and…

European retail sales were stronger-than-expected in March. They grew by 0.7% y/y from an upwardly revised 0.5% contraction in February, upending expectations that they would continue to decline. Improved sales in food products were the main drivers,…

The final estimates of Spain's and France’s services PMIs were revised upwards of expectations in April, increasing from 56.1 to 56.2 and from 50.5 to 51.3 respectively. The services European harmonized PMI also increased from 52.9 to a higher-than-expected…

The cyclical outlook is gloomy for EUR/USD. We subscribe to neither the soft-landing nor the no-landing view and expect a recession to occur in late 2024/early 2025. The pro-cyclical euro would suffer in a global downturn while a recession would support the…

According to BCA Research’s European Investment Strategy service, US and Euro Area growth will likely converge in the next 12 months. Fiscal policy differences were the most visible headwind to Eurozone growth last year. The IMF estimates that the…

Central banks are in a dilemma whether to prioritize supporting growth or bringing inflation back to target. This is unlikely to end well. Investors should be defensively positioned.

Euro area inflation and GDP numbers were released on Tuesday. The preliminary harmonized core consumer price index came in at 0.7% on a month-on-month basis, a decrease from 1.1% in March. The preliminary year-on-year core CPI also decreased, clocking in at…