Europe

In this Q4 Strategy Outlook, we discuss where we stand on our recession call, the outlook for stocks and bonds in various scenarios, why investors are misunderstanding the impact of AI on corporate profits, whether the US dollar has entered a structural downtrend, our perspective on the yen, gold and other commodities, and much more.

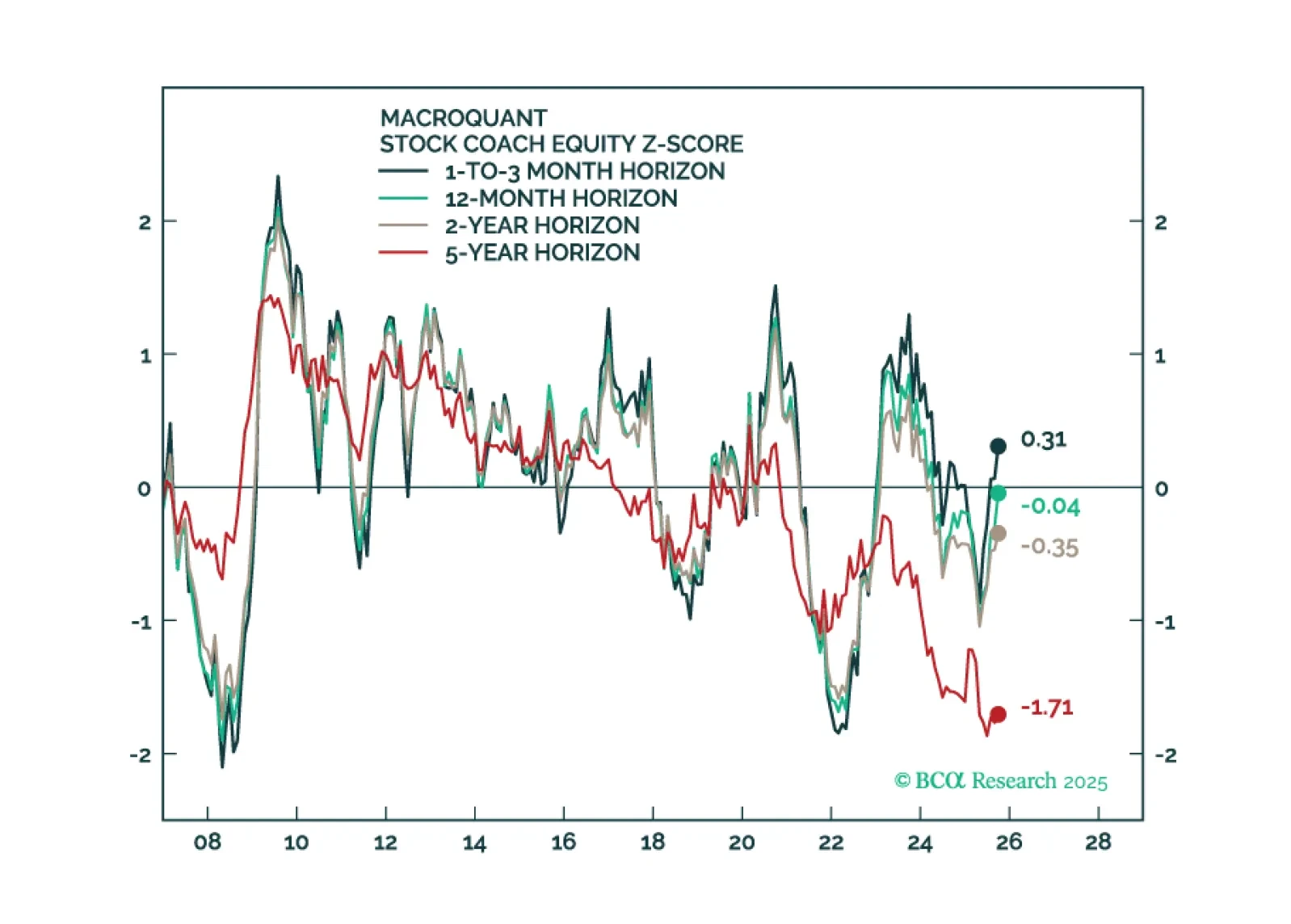

In this update, we apply our Macro Surprises framework to equities for the first time. Overall, the message is broadly consistent with our current equity views: Investors should favor Eurozone equities and continue to overweight cyclical sectors relative to defensive ones.

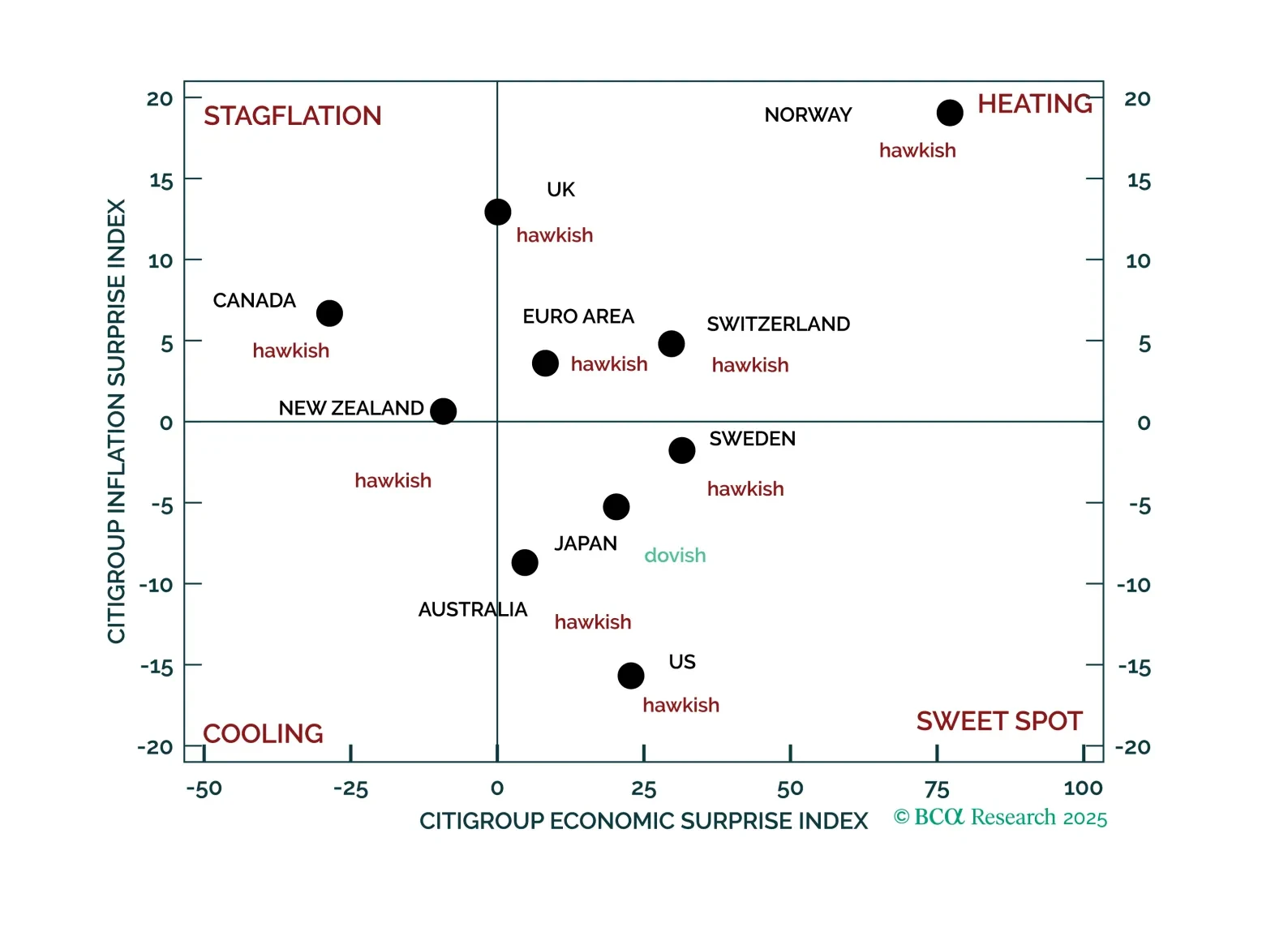

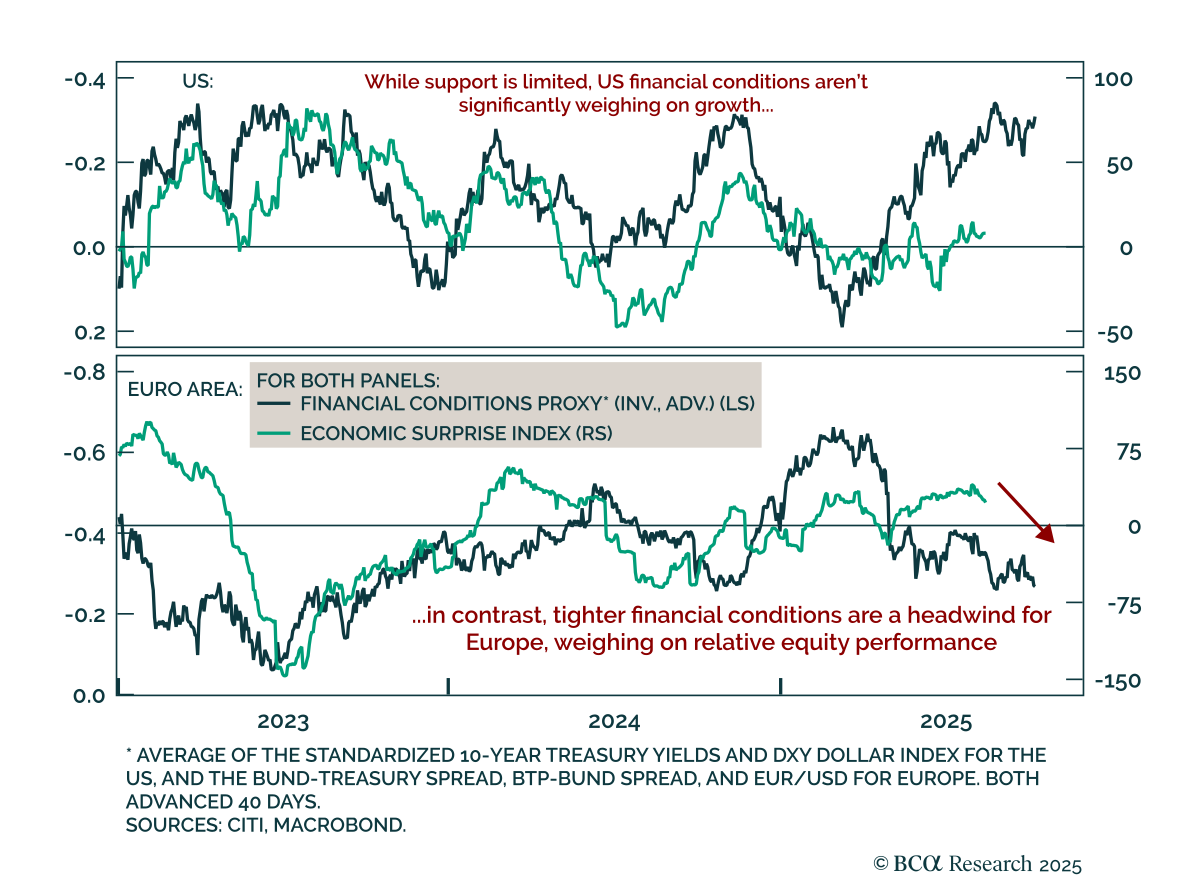

The ECB stood pat today, yet the policy path remains fraught with uncertainty as domestic resilience collides with global headwinds. This dichotomy continues to hold important implications for European assets over the coming months.

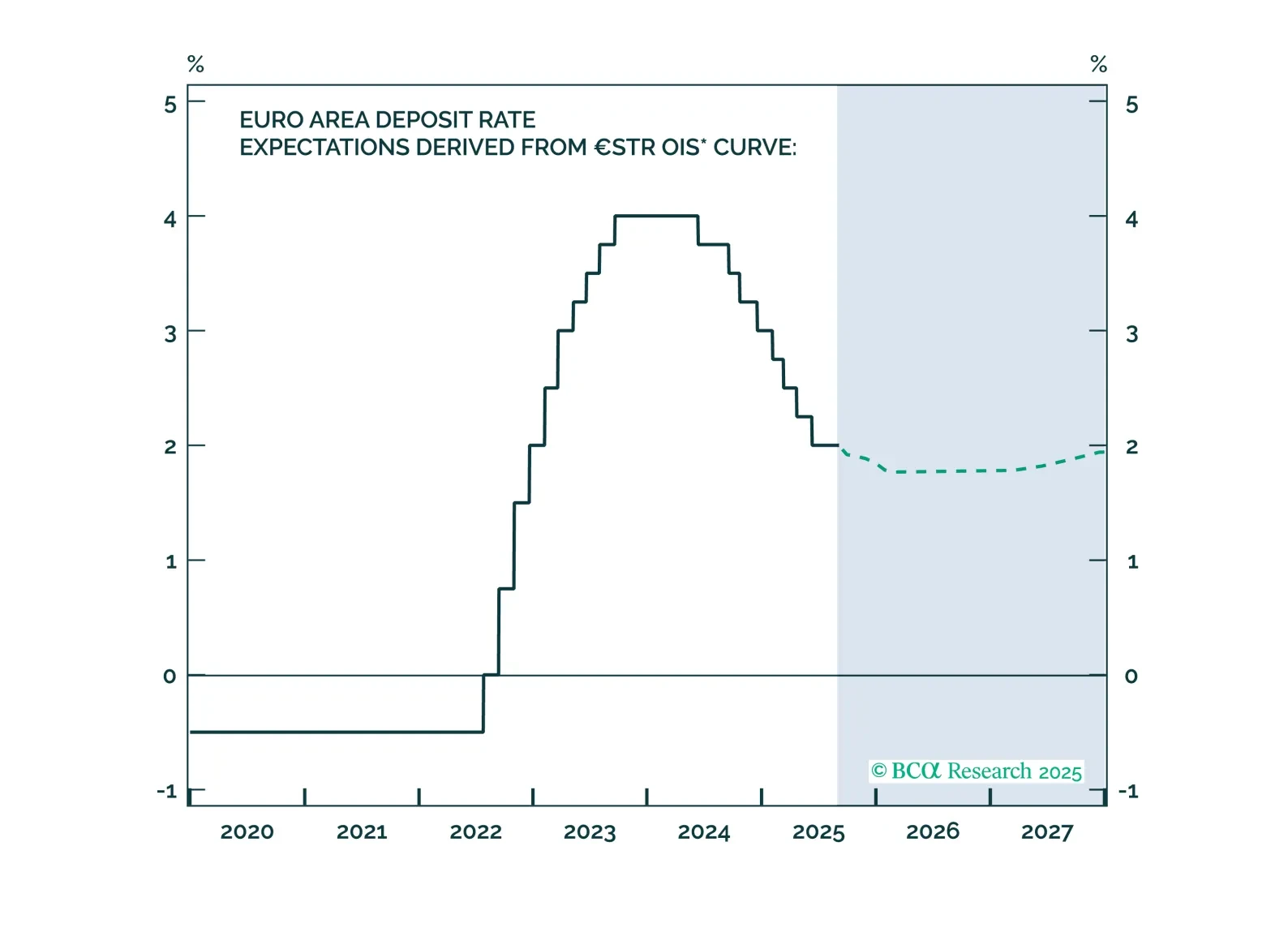

The European Central Bank has achieved a soft landing. Inflation is back to target, with well-anchored inflation expectations. The unemployment rate is historically low, and real economic growth is stable, albeit weak. Given that little to no additional easing will come from the ECB, investors should underweight government bonds relative to equities.

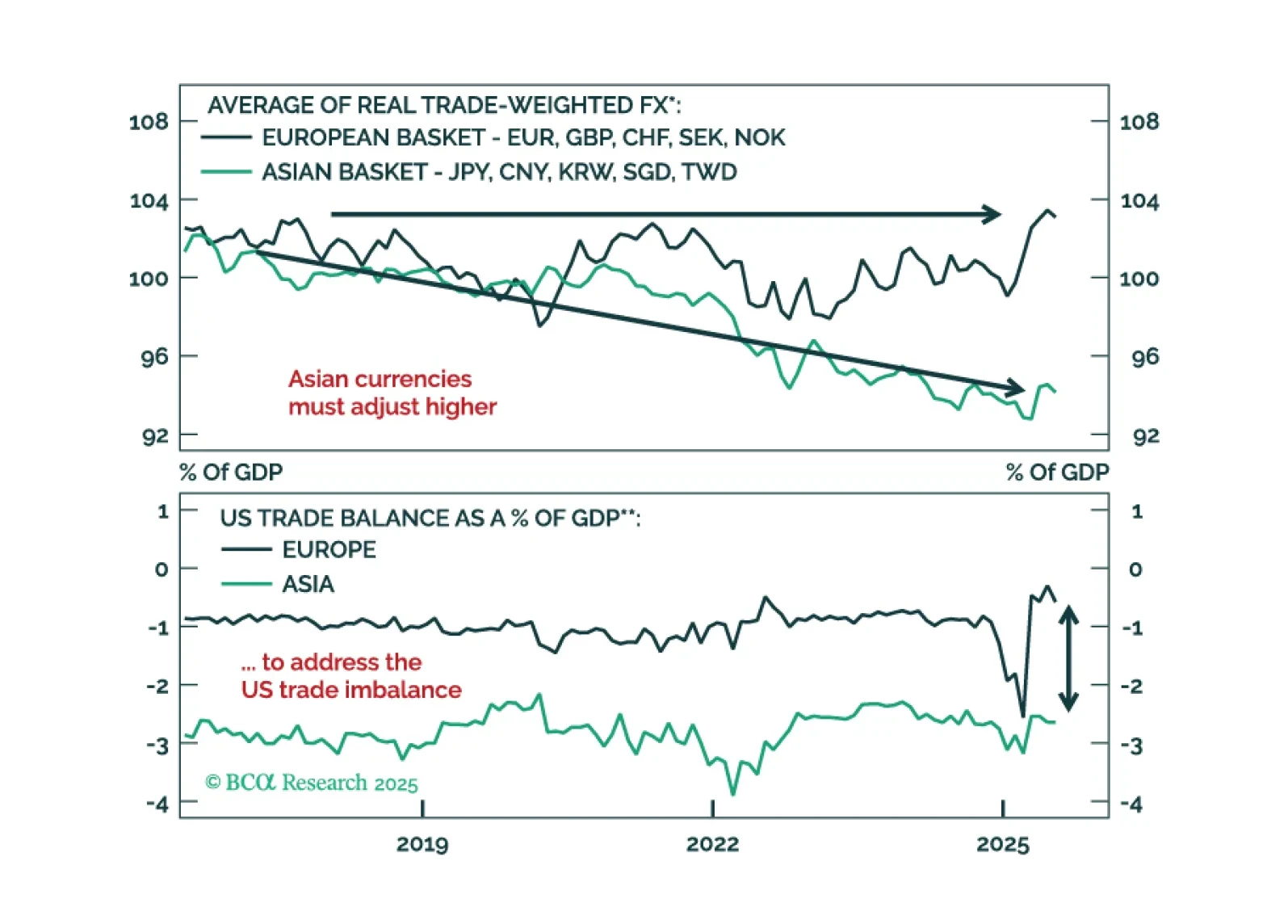

A fleeting greenback rally post Fed rate cut will offer a final chance to reset short dollar exposures. See why undervalued Asian FX are poised to lead the next leg lower in USD and how to position now.

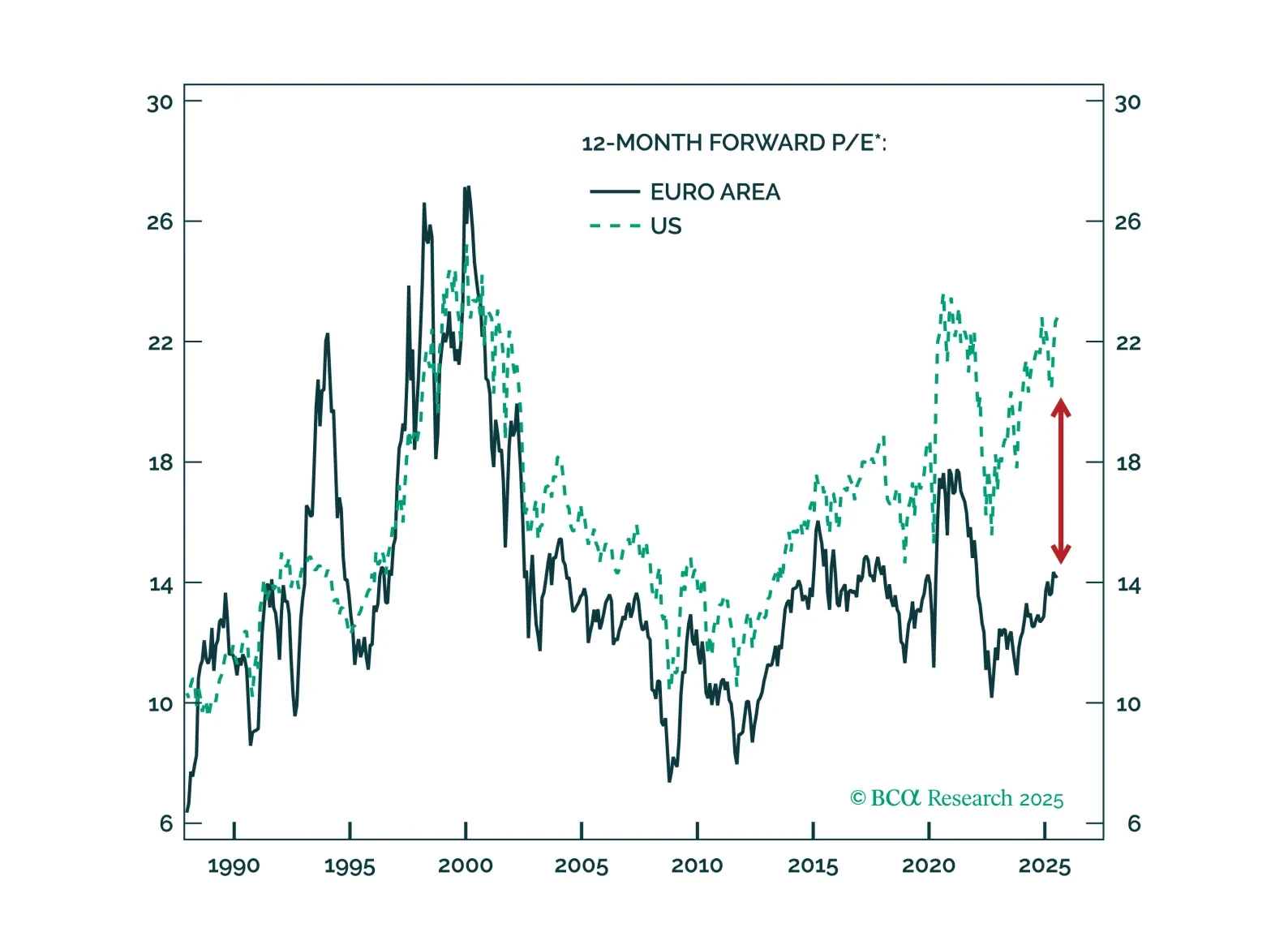

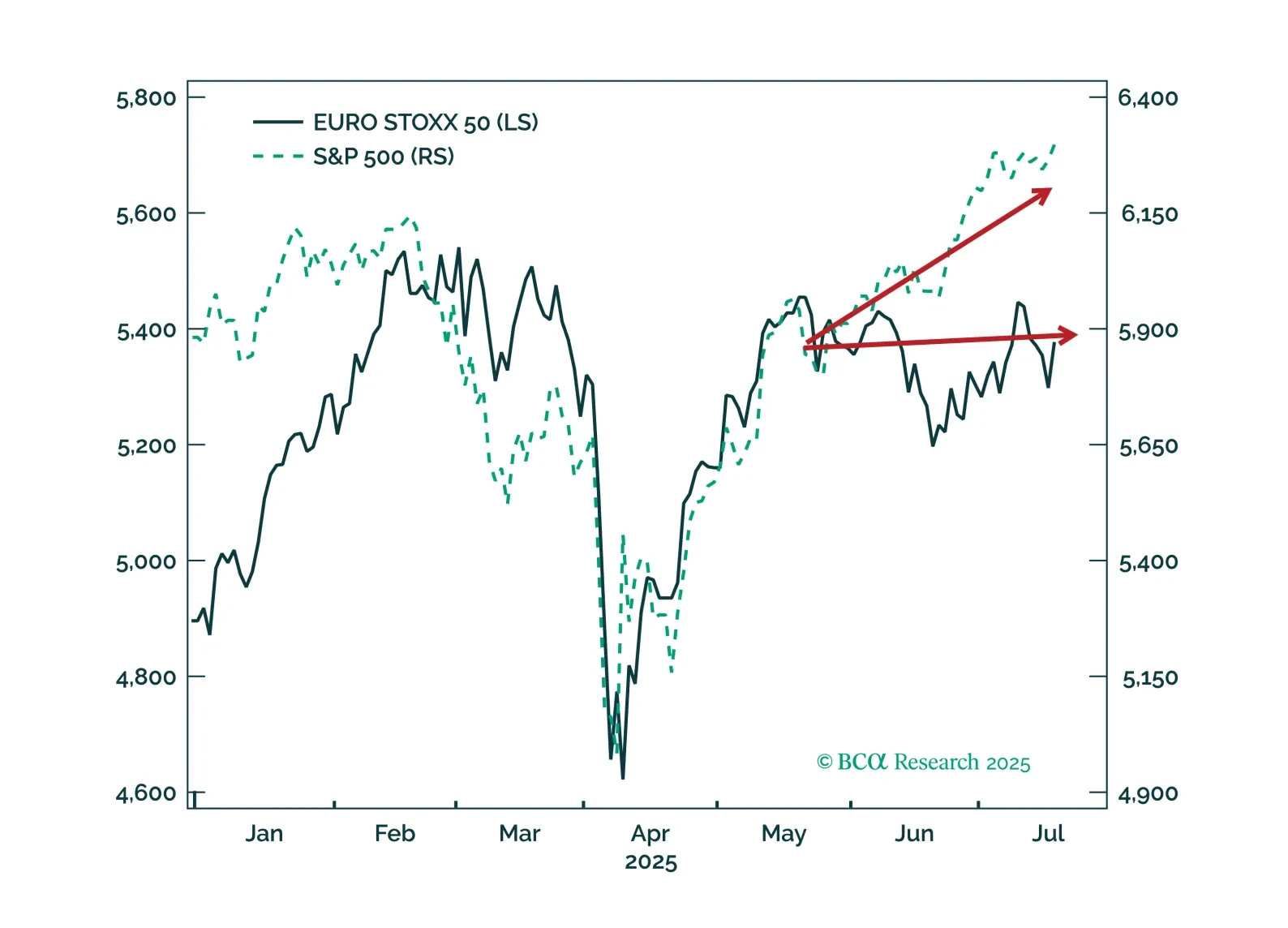

The outlook for European equities is becoming more appealing relative to US equities. Many structural headwinds are fading in Europe, and valuations remain historically cheap. Investors should position accordingly to benefit from the region’s cyclical rerating.

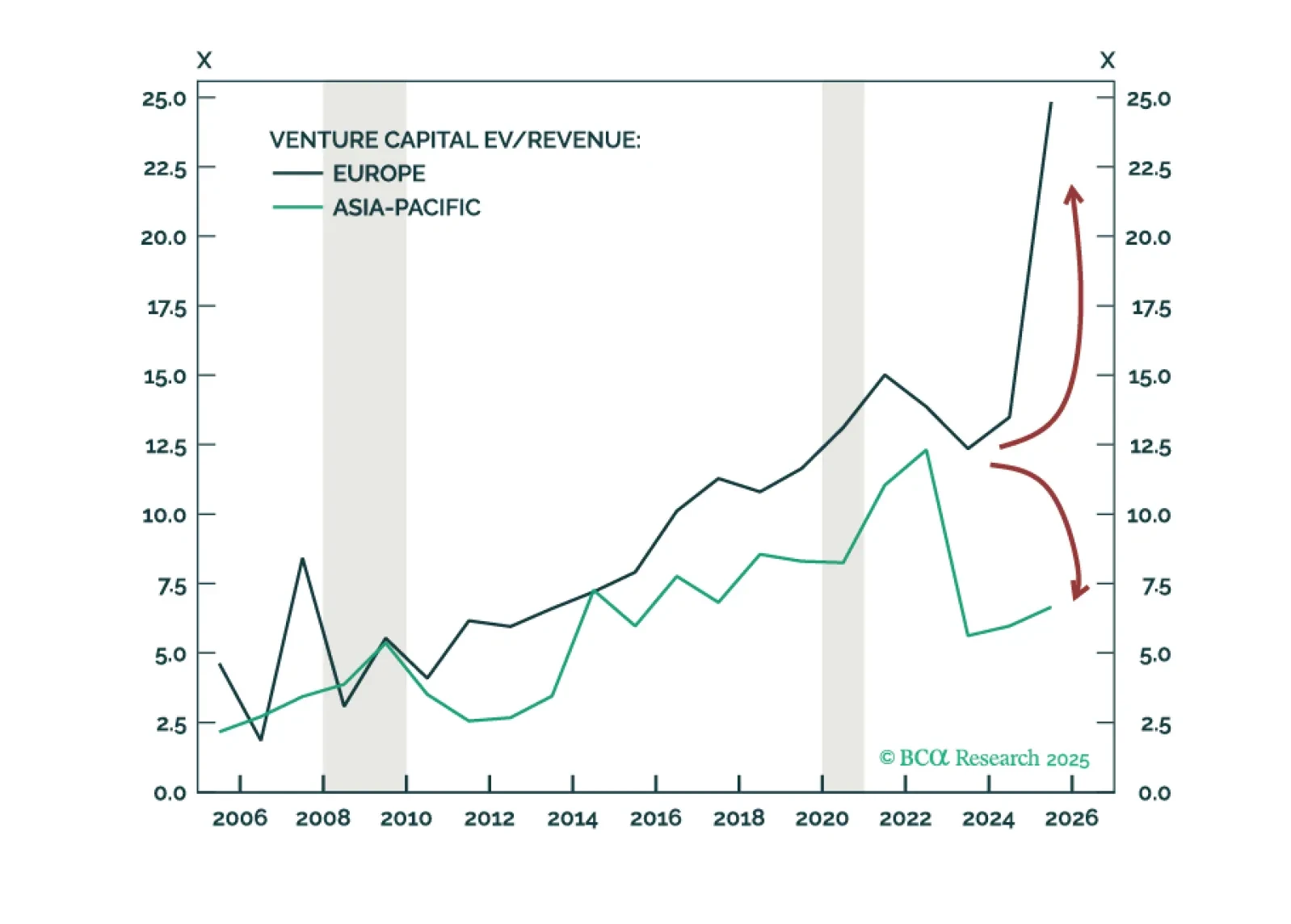

European euphoria is overdone. The most exceptional asset class in Europe is Infrastructure, but granular opportunities span other asset classes by sector and country. Venture Capital is a North America and Asia-Pacific play. We downgrade Private Credit, and upgrade Global Buyouts. Time to take profits on Long-Short Equity Hedge Funds.

This insight gives life to four high-conviction views on European small caps, aero¬space & defense, banks, and telecoms by harnessing the power of BCA’s Equity Analyzer (EA).