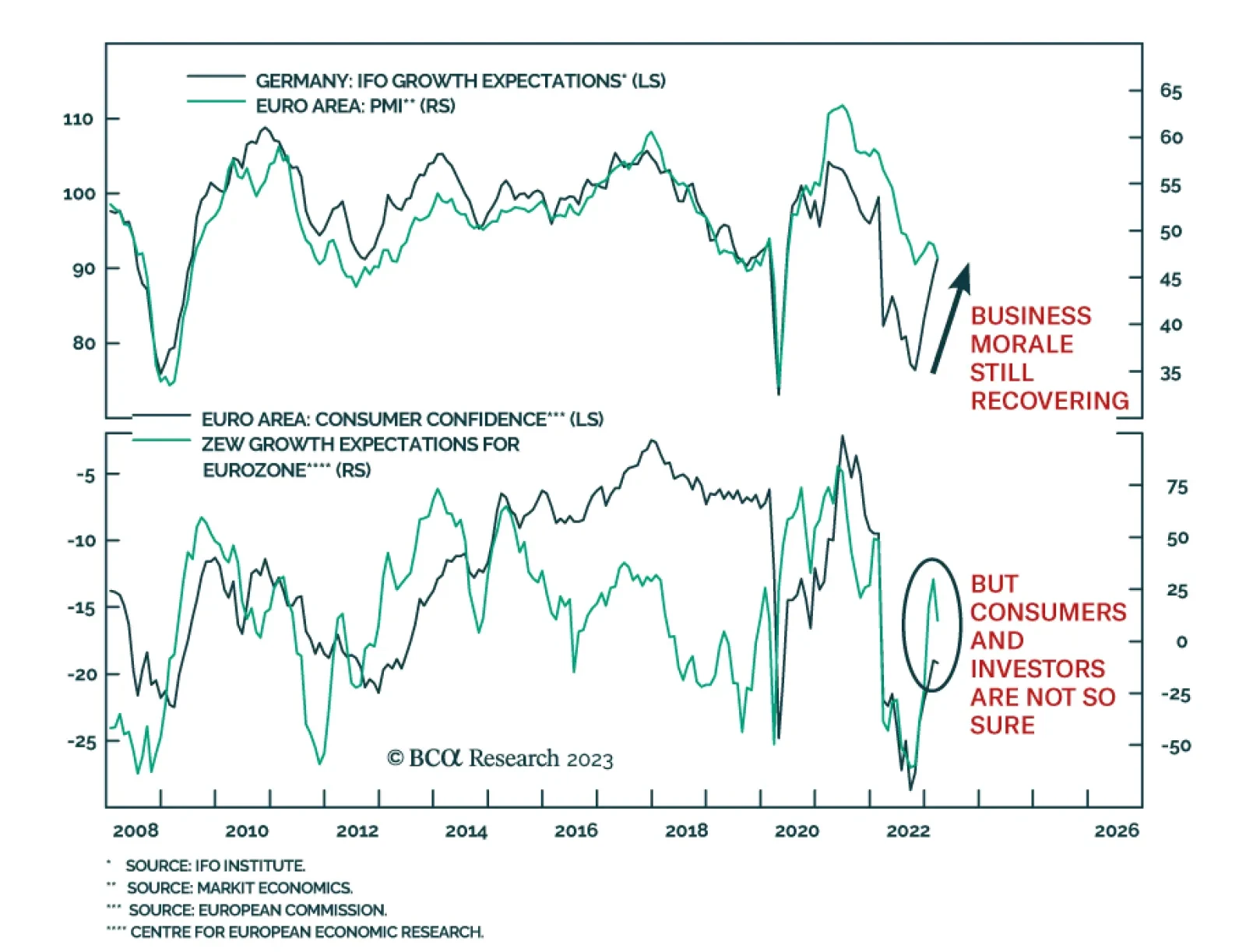

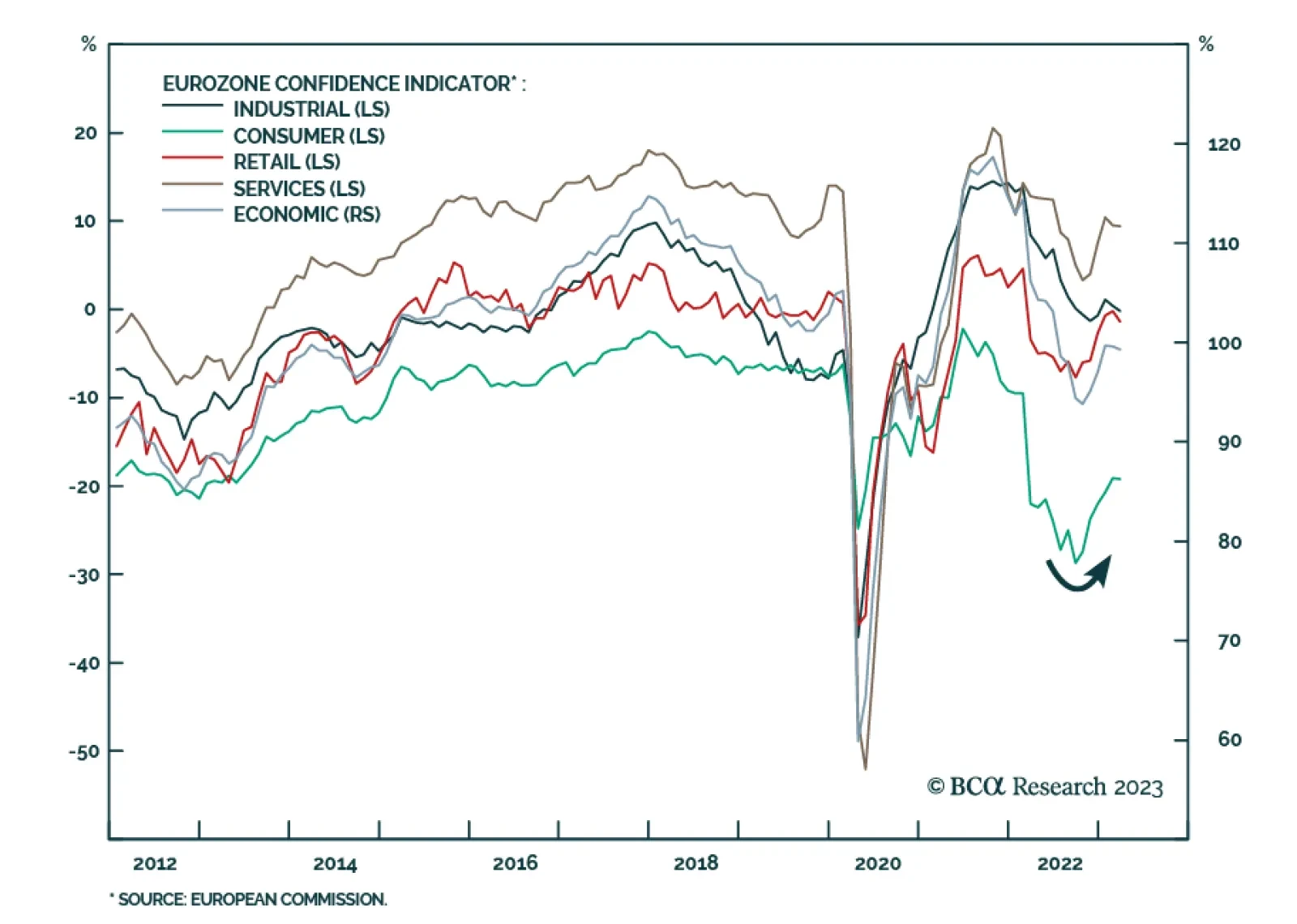

Europe

High rates have hurt real estate and, now, banks. The next shoes to drop: Loan growth, profits, and employment. Stay defensive. Recession is probable, but risk assets have not priced it in.

In this Strategy Outlook, we present the major investment themes and views we see playing out for the rest of 2023 and beyond.

It is a big mistake to think that rate cuts or lower bond yields will ease credit conditions. Quite the contrary. After an aggressive tightening of monetary policy, the first rate cuts always coincide with much tighter credit conditions. We discuss the implications for credit, government bonds and equities. Plus, we find a startling anomaly in equity sector performance.

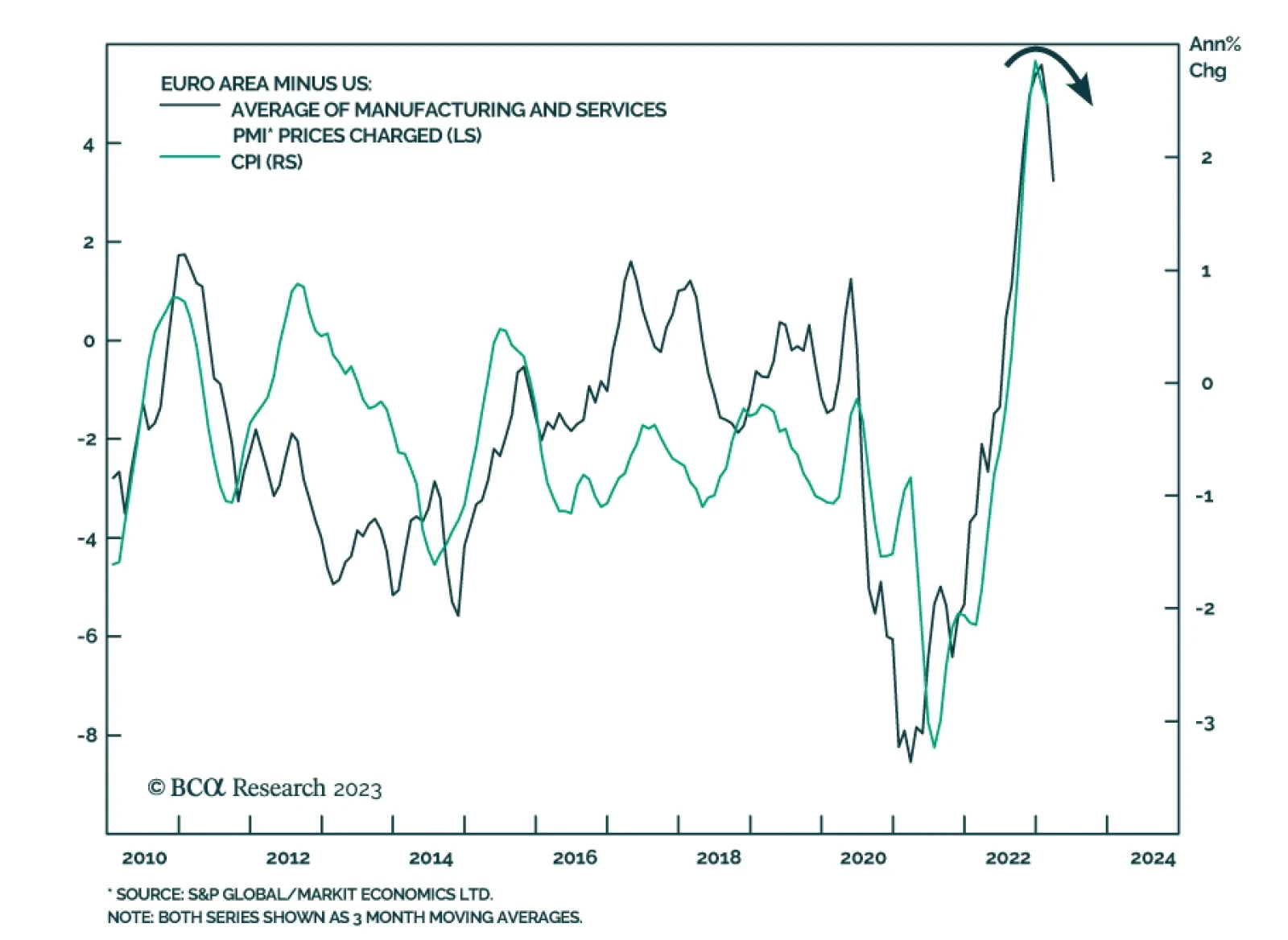

The recent uncertainty regarding the health of the banking systems in the US and Europe is not having any material impact on overall financial conditions or economic sentiment. The aggressive rate cut expectations, especially in the US, are unlikely to be realized. Although the macro growth and policy backdrop remains unfriendly for corporate debt on both sides of the Atlantic.

China is launching a diplomatic charm offensive to improve relations with the world excluding the United States. But China’s proposals in Ukraine and the Middle East are overrated in their ability to restore global stability and reduce geopolitical risk.