Europe

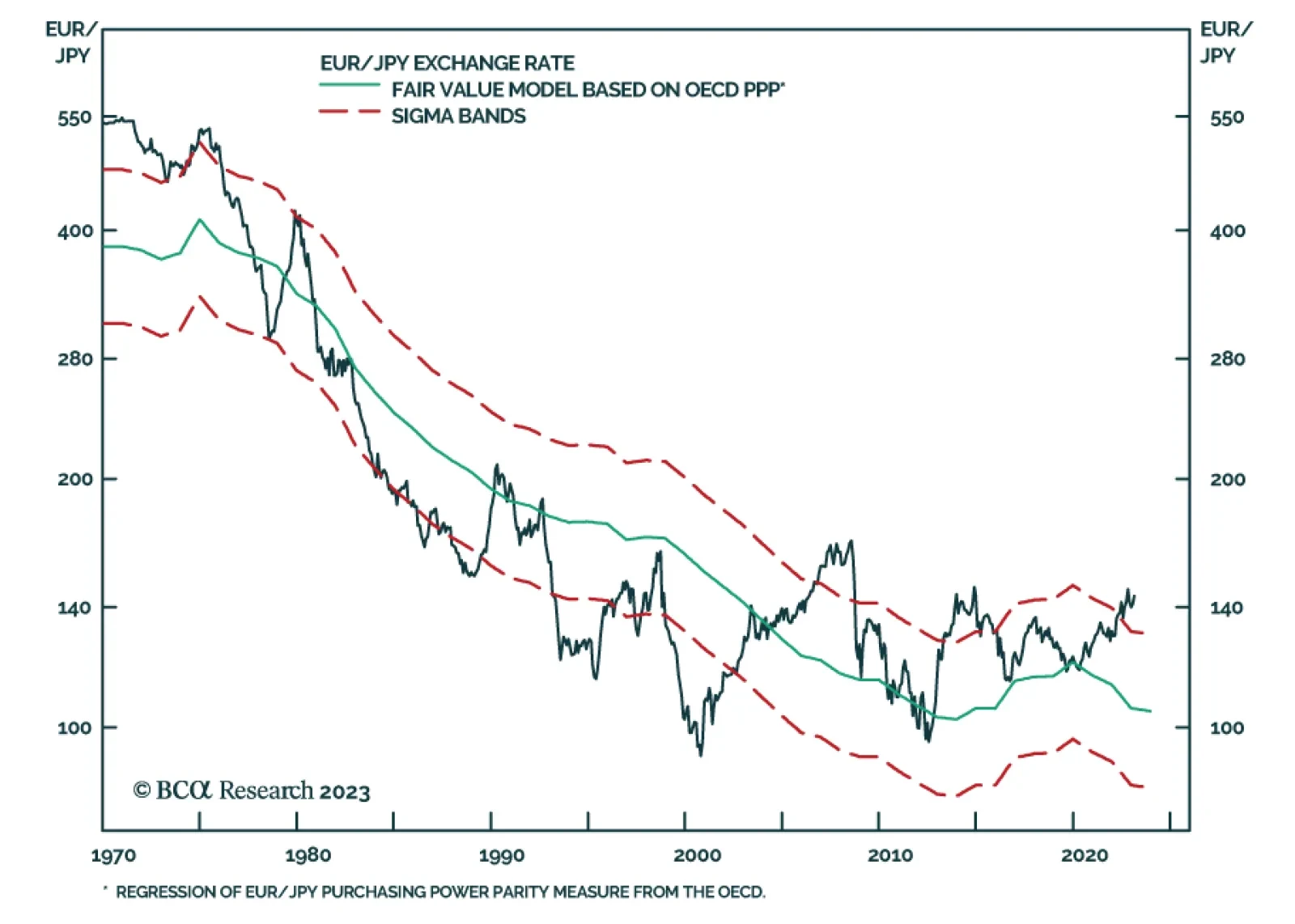

In this week’s report, we speculate on the evolution of euro trading in light of the near-term hiccups, but tremendous value that can be unlocked for longer-term investors.

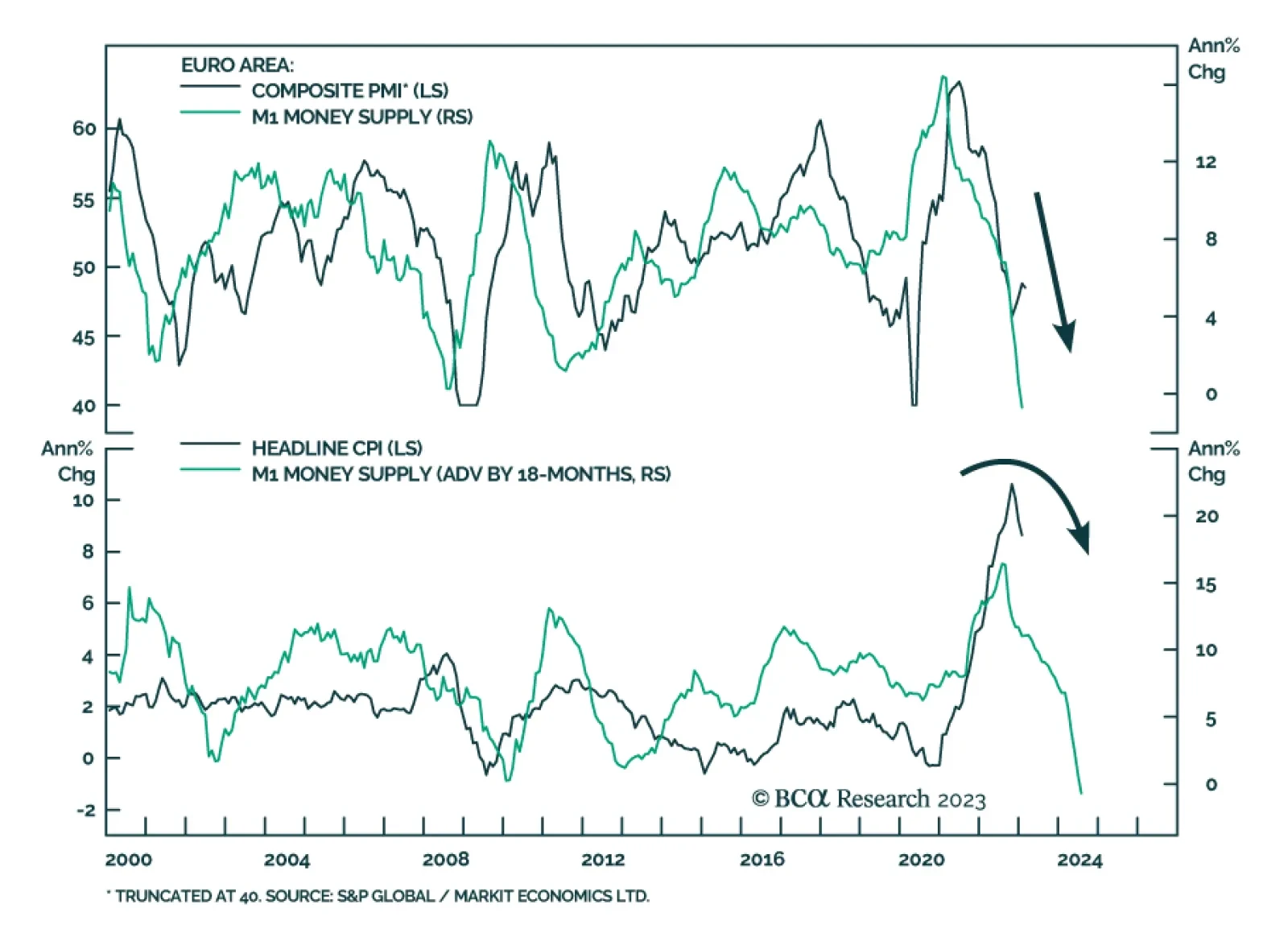

Rather than teetering into recession, global growth has firmed since the start of the year. While we still expect inflation to decline, the risk that central banks will need to lift rates more than discounted has increased. Long-term focused investors should start raising cash allocations by trimming their equity holdings.

The rebound in growth is pushing up inflation. More aggressive monetary policy is likely to trigger recession over the next 12 months or so. Investors should stay defensive.

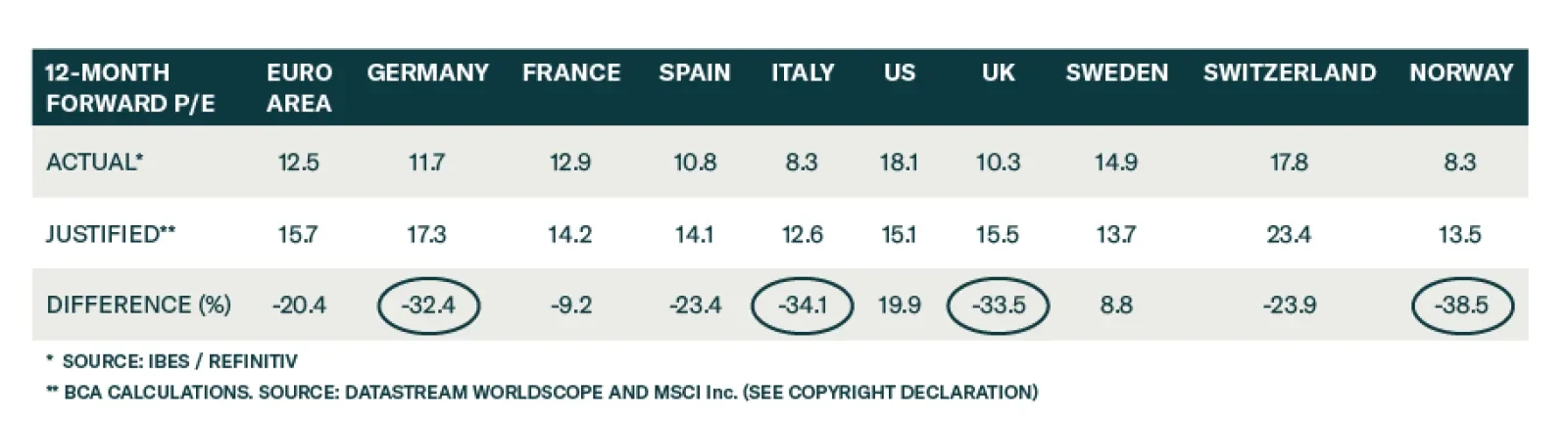

It is easy to conclude that European equities are attractively valued by looking at multiples; however, a method rooted in fundamentals is essential to find out which bourses are genuinely cheap.

Great Power Rivalry is taking another leg up as Russia and China further align their geopolitical interests. Investors should stay long USD-CNY, favor defensives over cyclicals, and markets like North America and DM Europe that have less exposure to geopolitical risk.