Europe

Ironically, increased confidence that the economy can withstand higher bond yields may be necessary to lift yields to a level that is actually detrimental to growth. Thus, until more investors are convinced that a recession will be averted, a recession will be averted. Remain tactically bullish on stocks for now. A more defensive posture will likely be necessary later this year.

The Fed is betting that the usual non-linearity of unemployment is different this time, but so far, there is nothing to suggest that it is different. We discuss the key signposts to watch out for, plus the implications for interest rates and asset allocation.

This week, we articulate what the actions of the three major central banks that met (Fed, ECB and BoE) mean for currency markets. This is within the context of our analysis of the latest data releases in the G10, that allows us to calibrate currency strategy.

Financial markets were taken on a wild ride between Wednesday and Friday of this week, with hugely important monetary policy meetings in the US, euro area and UK along with a rash of economic data. Despite all the news, noise and market volatility, the underlying message for monetary policy and bond yields in the US, euro area and UK is unchanged.

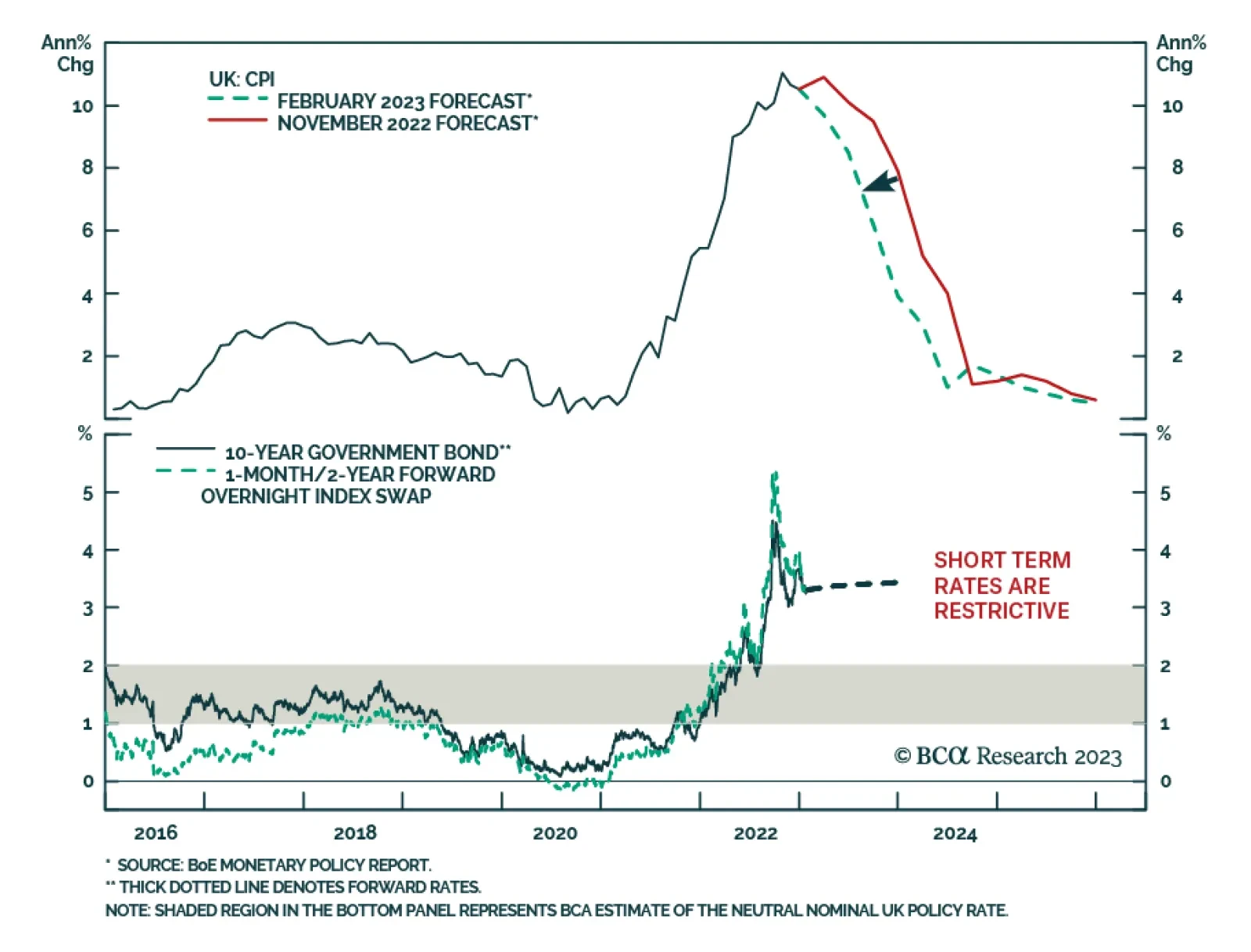

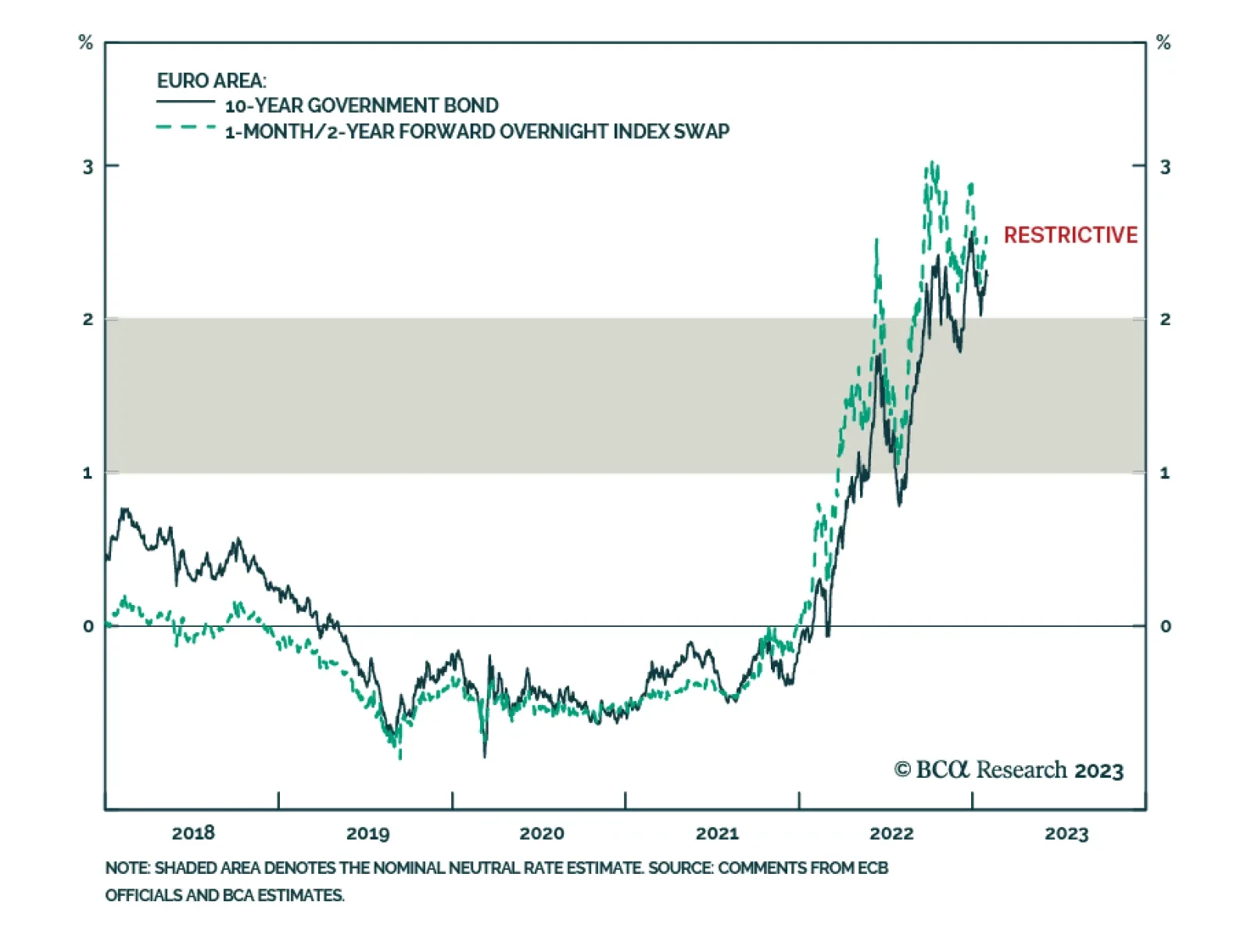

The ECB and the BoE provided a comforting signal to markets that the end of the respective tightening campaigns is coming before the summer. In the process, they are closing their hawkishness gap relative to the Fed.

The US economy will experience a period of benign disinflation over the next few quarters. Beyond this goldilocks period, either the economy will slip into a mild recession in 2024, or more ominously, a second wave of inflation will prompt the Fed to slam on the brakes, leading to a deep recession.