Europe

The Web 2.0 bubble is bursting, with far-reaching consequences for US stock market behaviour, sector allocation, and global asset allocation.

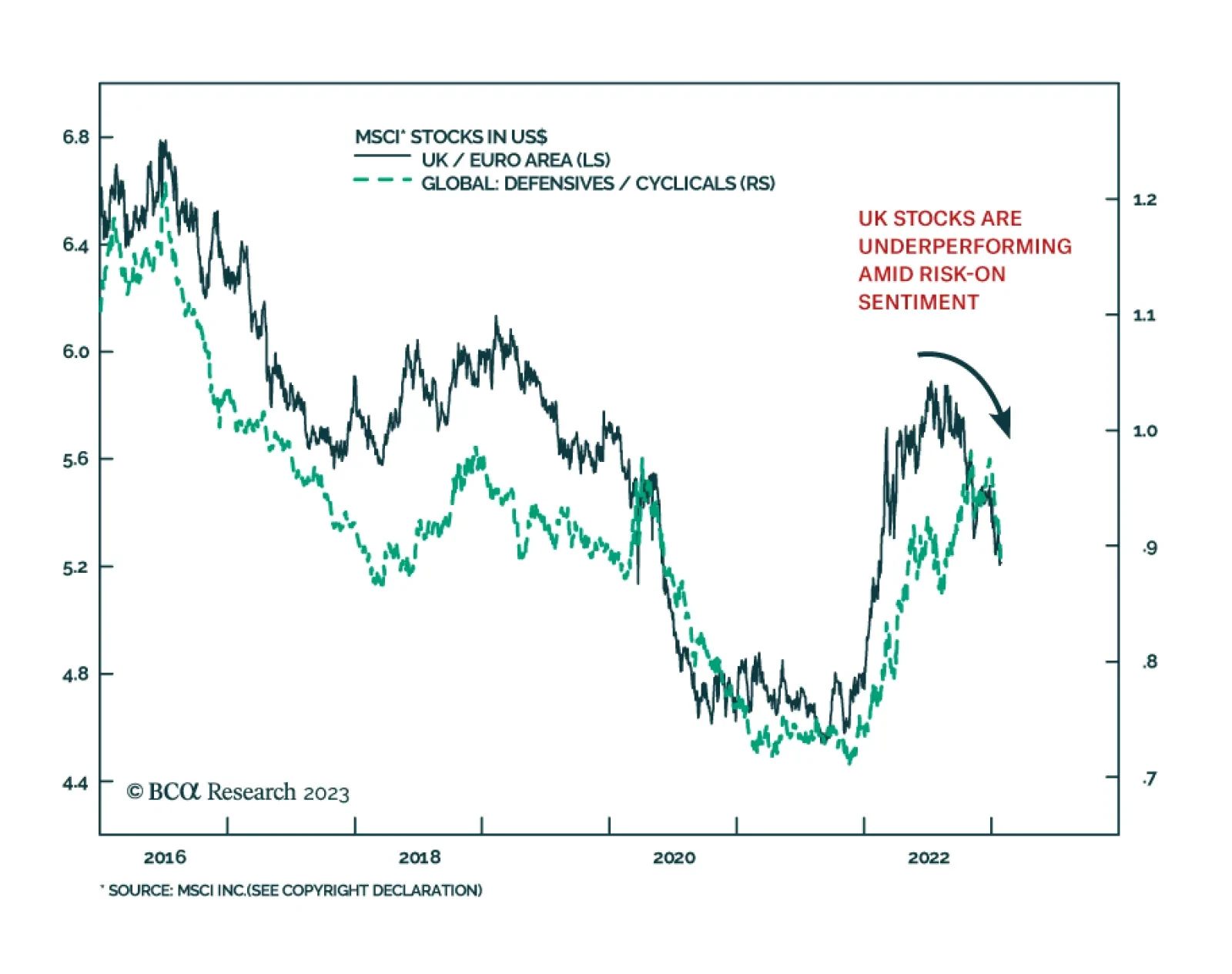

This week’s Special Report goes over the structural problems facing the UK economy and our outlook for UK gilts and the sterling following turbulent moves in 2022.

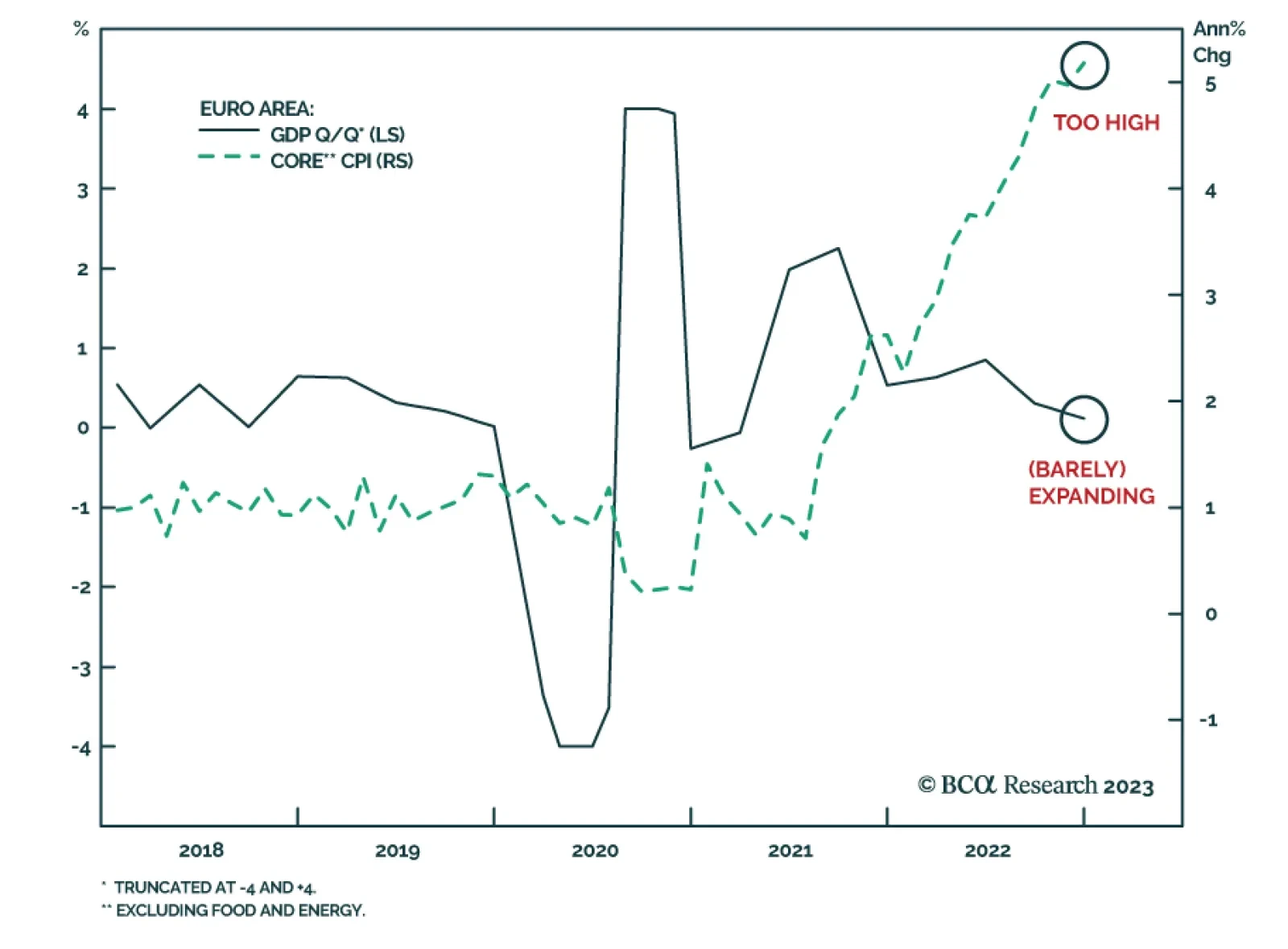

Europe’s domestic economy continues to surprise to the upside, can small-cap stocks do the same?

Remain cautious and defensive overall. Stay long DM Europe over EM Europe. Look for EM opportunities in Southeast Asia and Latin America over Greater China.

In Section I, we explain why we do not see the deceleration in US inflation, the likely near-term pickup in European growth, and the end of China’s dynamic zero-COVID policy as signs of a sustainable rebound in global economic activity over the coming 6-12 months. The key question is not whether inflation will fall back to central bank targets, but rather how quickly this will occur. For now, our indicators point to slower but still elevated inflation this year. In Section II, we explore what it will take for the Fed to cut interest rates, and note that nonrecessionary rate cuts are possible but not especially likely.