Europe

While the housing downturn will be fairly mild in the US, it will be more severe abroad. Continue to favor bonds of countries whose housing fundamentals will limit rate hikes.

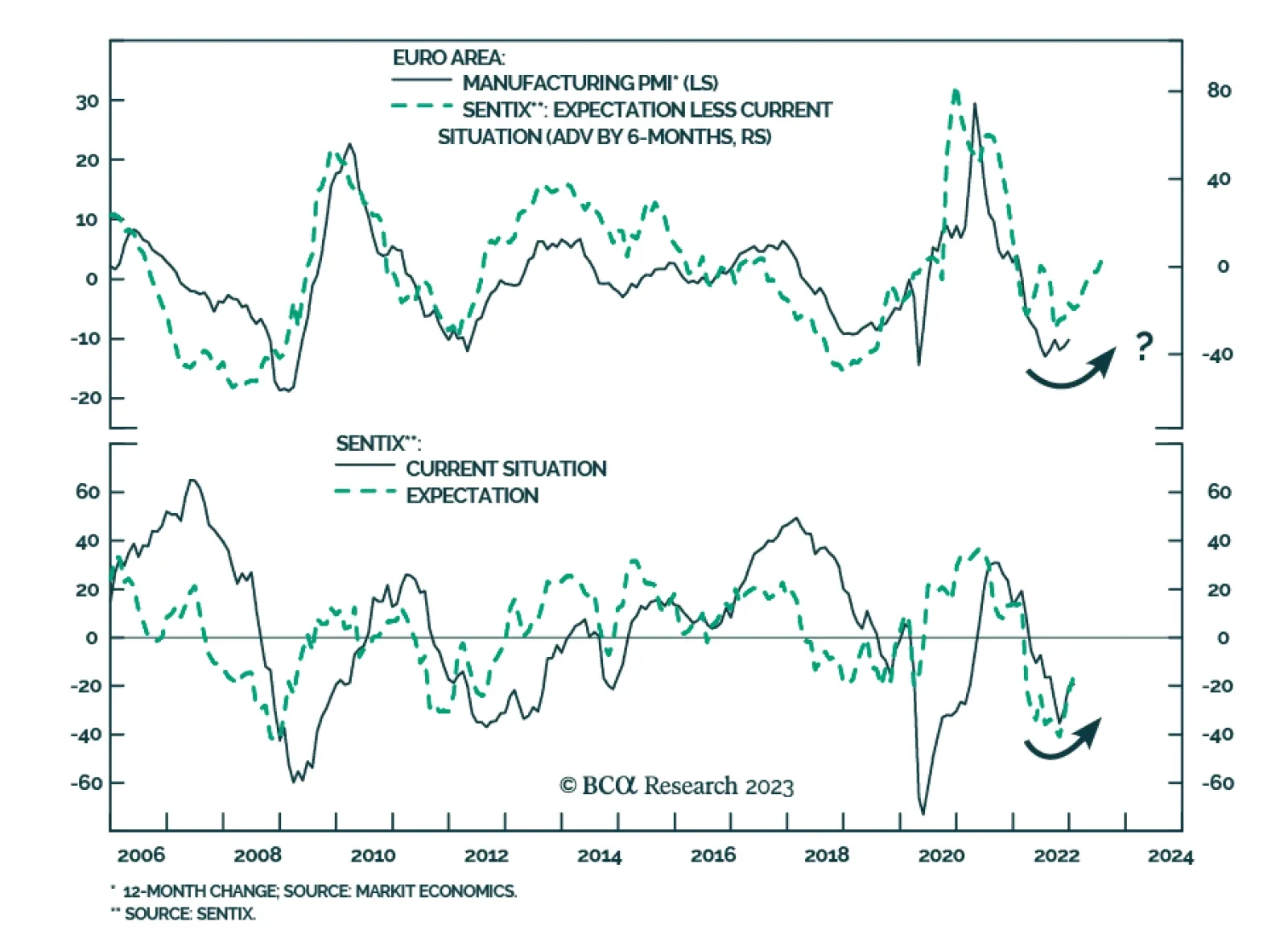

The crucial question for 2023 is: will the US and UK Beveridge Curves shift back inwards to their pre-pandemic versions, ushering in a soft landing? Or, will we slide down the new post-pandemic Beveridge Curves into recession? Plus: we reveal the most important chart for Europe and the most important chart for China in early 2023.

The European Commission risks retarding the development of long-term contracting for renewable energy just as momentum is building. Policy uncertainty will continue to dog firms and households in the EU, if the Commission's attempts to lower energy costs for consumers at the expense of renewable-energy producers by extending “windfall profits taxes” and mandated lower costs succeed. Such measures will lower producers’ revenues, which will translate into lower renewables investment.

Slowing growth would be bad for equities, but so would stronger growth since it would mean more rate hikes.

In Section I, we note that the global growth outlook has modestly deteriorated over the past month, despite an improving 12-month outlook for Chinese domestic demand in response to the imminent end of the nation’s “dynamic zero-COVID” policy. Investors should remain conservatively positioned over the coming year, as we recommended in our Annual Outlook report. In Section II, we examine whether the structural risks facing global stocks are higher or lower today than they were prior to the global financial crisis, and what that implies for stock and bond risk premia.

This week, we look at the latest data releases in the G10, along with implications for all the major currencies.