Europe

The pandemic gave older Americans and Brits a massive carrot and stick to retire early. The carrot being a surge in wealth, the stick being a risk to health. In other major economies, the carrots and sticks were smaller or non-existent. Hence, the shortage of older workers, and the resulting wage inflation, is a specific US and UK problem. We go through the important economic and investment implications for 2023.

European inflation will decline through 2023, which will greatly help households and consumption. But can European inflation remain low after that?

MacroQuant is overweight bonds, underweight equities, and neutral on cash. Within the equity universe, the model is underweight the US and overweight Japan, the UK, and Australia.

Recession is not yet fully priced in, so markets have further to fall next year. But watch for a buying opportunity in the second half.

The Chinese government will repress social unrest, then relax Covid-19 social restrictions to try to stabilize the economy. Russia will be aggressive in the short term but will pursue a ceasefire before March 2024. European and Italian risk will stay high on energy constraints.

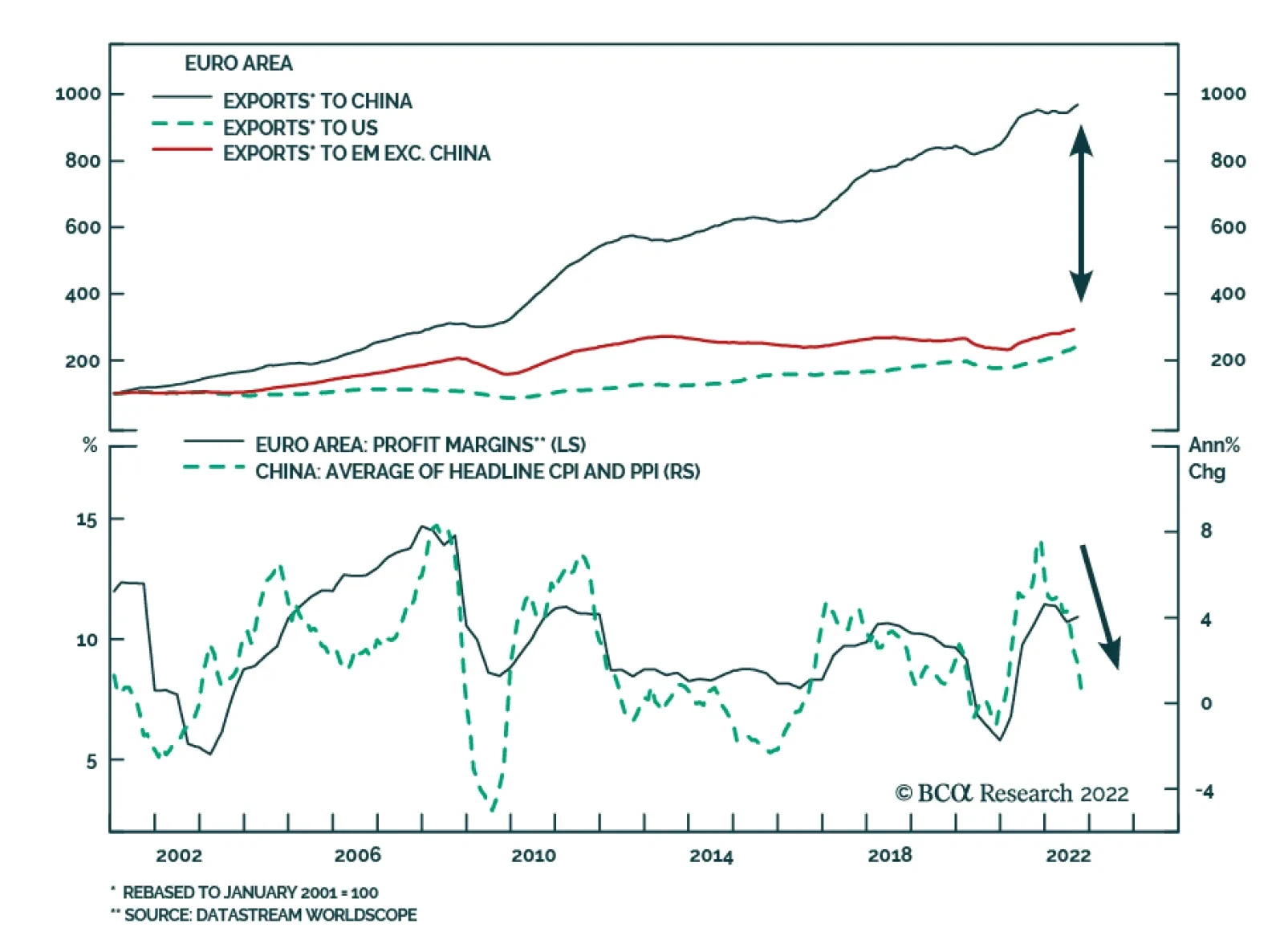

European asset prices have rebounded sharply since September. Can this trend survive in the face of a weak Chinese economy where deflation prevails?