Europe

Our 4Q22 and 2023 Brent forecasts remain at $100/bbl and $116/bbl. Upside price risk continues to dominate oil markets. We remain long the XOP and COMT ETFs to retain exposure to oil and gas producers’ equities, and higher commodity prices and further backwardation, particularly in copper.

The messages from the deteriorating fundamental backdrop (tight monetary policy, slowing global growth) and improved credit valuation (elevated 12-month breakeven spreads) are giving conflicting signals on corporate bond strategy. We are putting more weight on the fundamentals and are staying with an overall underweight stance on global investment grade corporates, with a slight bias towards Europe given more attractive spread valuations. At the same time, we see selective opportunities in sectors where risk-adjusted spreads are wide as signaled by our individual country sector valuation models, like US Energy and euro area Financials.

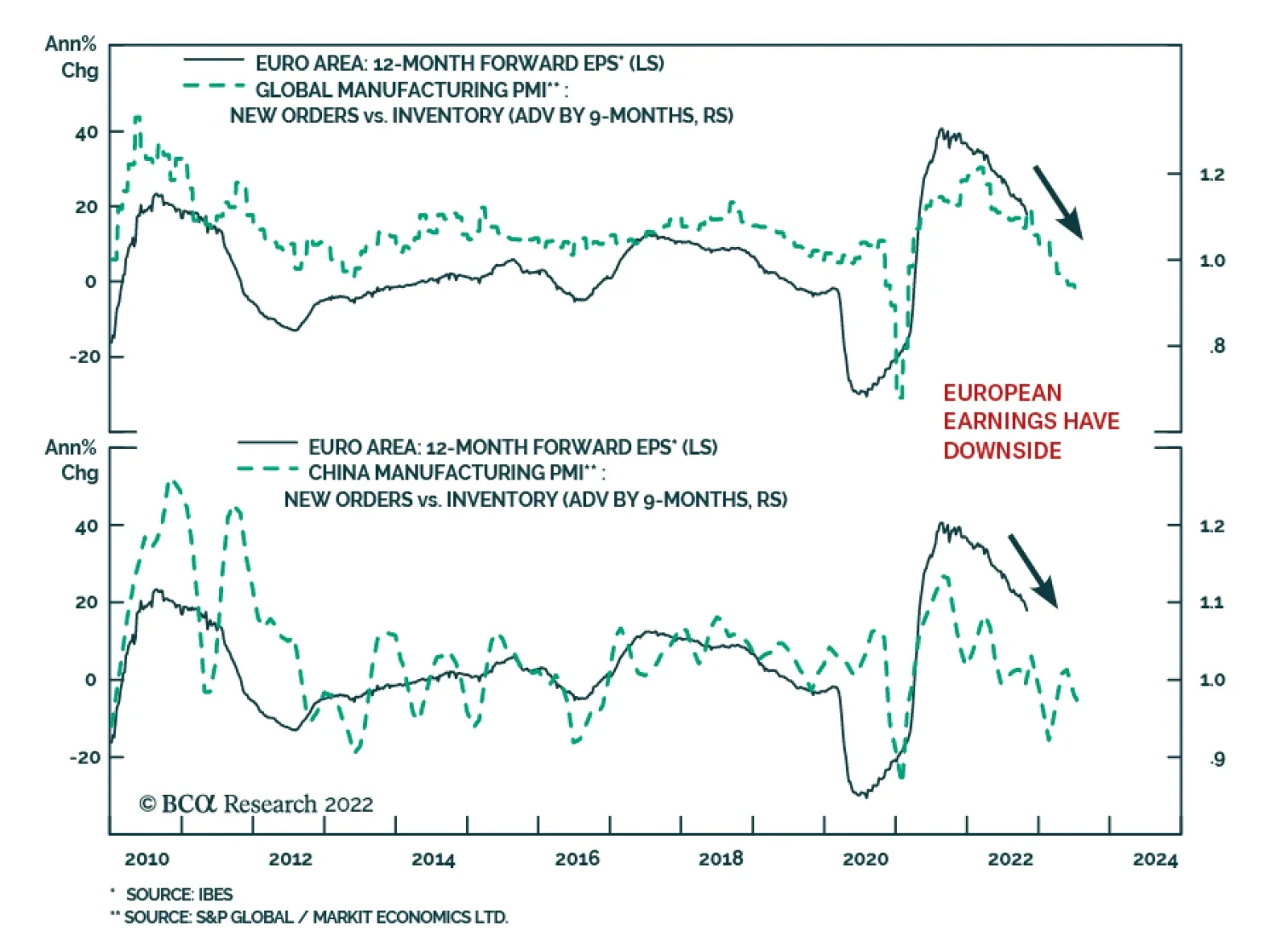

The decline in the US CPI is a tailwind for European stocks, but does it compensate for weaker global growth?

In this report, we identify the Norwegian krone as a currency that could outperform especially at the crosses, irrespective of the broad dollar trend.

A client concerned about the slump in asset prices, the stubbornness of inflation, and rising bond yields asks what went wrong, and what happens next? This report is the full transcript of our conversation.

Central banker messaging after the latest rate hike announcements in the US, UK and Australia indicates a shift in focus from the pace of hikes to how high rates must rise to slow growth and bring down inflation. This represents the next stage of the global tightening cycle, where rates will go higher in countries where neutral rates are higher, like the US, compared to countries with lower neutral rates like the UK and Australia.