Europe

Older workers have deserted the labour force in the US and the UK, but not so in the Euro area and Japan. The result is that wage inflation is red hot in the US and the UK, but not so in the Euro area and Japan. Hence, the Bank of Japan is right to remain a lone dove, the ECB must pivot from its uber-hawkish stance quite soon, but the Fed and the BoE must not pivot from their uber-hawkish stance too soon. We go through the major investment implications.

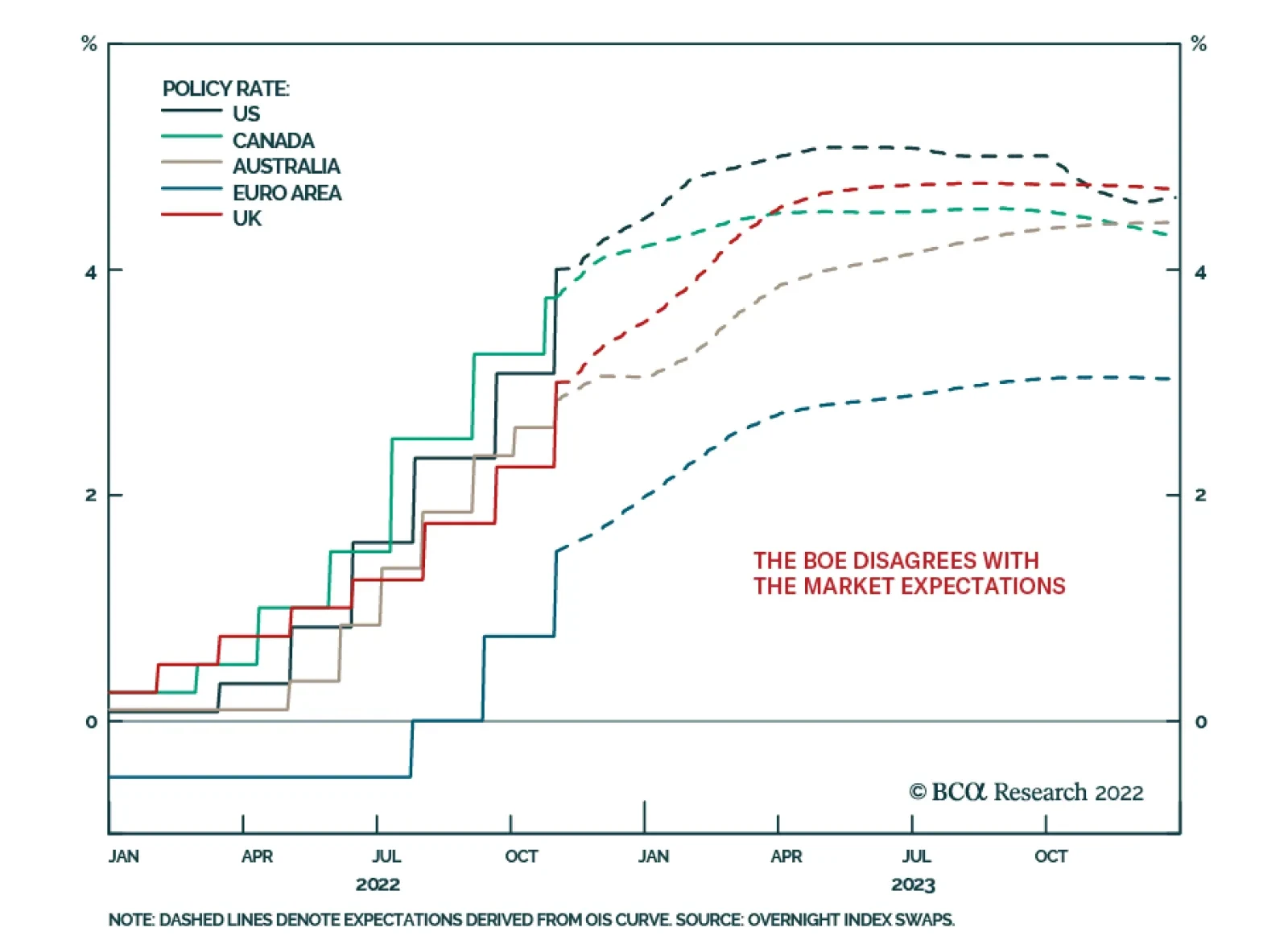

This week’s report examines the state of the global monetary tightening cycle and addresses some frequently asked questions about the Fed’s QT program. New yield curve trades are recommended for the US and German yield curves.

Stay short Greater China assets. Stay long Japanese yen. Hold back on Brazil for now but look forward to opportunities in future.

The ECB increased interest rates and announced the start of its balance sheet wind down; yet, markets took the news as a dovish outcome. Are we really getting close to the end of the ECB’s tightening campaign? How asset prices will react?