Europe

Executive Summary EU Metal Industry Under Threat

EU Energy Crisis, Strong USD Imperil Bloc’s Metals Industry

EU Energy Crisis, Strong USD Imperil Bloc’s Metals Industry

Russia’s threat to cut off all remaining exports of natural gas to the EU via Ukraine will further imperil the bloc’s struggling metals industry, particularly aluminum smelting – where half of its capacity already has been shut – and zinc refining. The EU will have to prioritize energy security over its renewable-energy goals, given the challenges its manufacturing industries will confront for the next 3-5 years. Surging imports of raw copper concentrates and unwrought metal will consolidate the global dominance of China’s copper refiners, which sharply increased their treatment and refining charges this week. The US likely will see more investment in metals mining and refining on the back of the EU distress, which realistically cannot be addressed until gas and power prices fall to levels that allow them to sustain their operations. Bottom Line: Ongoing supply shocks to the EU’s base-metals industry will force the bloc to prioritize energy security over its renewable-energy goals. This will drive the bloc’s demand for liquified natural gas (LNG) and oil higher, even after short-term measures to increase LNG intake and distribution capacity are completed over the next 2-3 years. We expect the equities of oil and gas producers to outperform metals miners over this period. After being stopped out, we will be re-instating our long XOP ETF position at tonight’s close. Feature Earlier this month, Eurometaux, the EU metals lobbying group, published a memo to the European Commission drawing attention to “Europe’s worsening energy crisis and its existential threat to our future.”1 This is not hyperbole. At the heart of the industry’s woes is a chronic shortage of energy – in any form – for industrial use. Utilities are signing long-term LNG supply contracts to address this shortage, but they can expect to wait 3-4 years or more before gas arrives on Europe’s shores.2 Spot and one-off cargoes will become available over that time, but most of the existing LNG production is under long-term contract. Oil, coal, and nuclear energy are available for power generation, industrial applications and space-heating, and they increasingly are being used in the bloc, but these too are constrained.3 Measures to address the chronic energy shortage hammering the EU base-metals industry will take years to effect, and could come too late to meaningfully preserve existing refining capacity, which has been contracting for years (Chart 1).4 Most of the EU’s metals production is accounted for by aluminum, copper and zinc, which are extremely energy intensive, copper only less so (Chart 2). The surge in LNG prices following Russia's invasion of Ukraine propelled electricity prices higher, given gas is the marginal fuel for EU power generation (Chart 3). This crushed zinc and aluminum refining. Half of the EU’s aluminum smelter capacity – ~ 1mm MT – will be curtailed or shuttered this year, according to European Aluminum.5 Chart 1EU Metal Industry Under Threat

EU Energy Crisis, Strong USD Imperil Bloc’s Metals Industry

EU Energy Crisis, Strong USD Imperil Bloc’s Metals Industry

Chart 2EU Metals Are Extremely Energy Intensive

EU Energy Crisis, Strong USD Imperil Bloc’s Metals Industry

EU Energy Crisis, Strong USD Imperil Bloc’s Metals Industry

Chart 3EU Power Price Surge Crushes Metals Refining

EU Energy Crisis, Strong USD Imperil Bloc’s Metals Industry

EU Energy Crisis, Strong USD Imperil Bloc’s Metals Industry

The surge in European electricity prices and the resulting curtailment or shuttering of zinc refining paced the 2.6% y/y decline in global output in 1H22, which took global production down to 6.77mm MT, according to the International Lead and Zinc Study group. Europe accounts for ~ 15% of global zinc refining.6 Refined zinc consumption fell 3% y/y in 1H22 to 6.74mm MT. China Bingeing On Copper Global refined copper output in the January – July 2022 period slightly outpaced usage – with 3% growth in the former and 2.6% growth in the latter, according to the International Copper Study Group (ICSG). On the back of this report, we lowered our expected supply growth estimate to 3% this year, (Chart 4). This brings our estimate for total supply down by ~400k MT vs. our previous iteration to 25.3mm MT. We are keeping our estimate of 2023 supply growth rate at ~ 4.5%. Our copper demand estimate is a function of real GDP estimated by the World Bank, and remains at just under 26mm MT and 27.2 mm MT for 2022 and 2023 respectively. As a result of the lower 2022 production growth rate, our forecasted copper deficit has widened to ~ 605k tons in 2022 and 480k tons in 2023. The mismatch in supply and demand levels will keep inventories in China and the West under pressure (Charts 5A and 5B). Chart 4Copper Supply Estimate Lowered

Copper Supply Estimate Lowered

Copper Supply Estimate Lowered

Chart 5AChinese Copper Inventories Continue To Draw

Chinese Copper Inventories Continue to Draw

Chinese Copper Inventories Continue to Draw

Chart 5BAs Do Stocks In The West

As Do Stocks In The West

As Do Stocks In The West

China’s imports of copper condensates – the raw material used to make refined copper – surged to 16.65mm tons over January – August 2022, up 9% y/y. Imports of unwrought and semi-fabricated copper were up 8% over the same period at 3.9mm MT, according to Mysteel.com. As is to be expected, treatment and refining charges at Chinese smelters also moved higher: for 3Q22, refiners were charging $93/MT, up $13 from 2Q22 levels and $23/MT from 4Q21, according to Reuters. These charges increase when raw-material supplies increase, and vice versa. This is meant to be a floor charged for refining concentrates to produce refined copper. Real USD Matches US PPI After Re-Opening In an unusual turn of events, the USD Real Effective Exchange Rate (REER) has been moving higher along with the US Producer Price Index for all commodities. This trend started as the global economy accelerated its re-opening in 2021 (Chart 6). The USD has a profound affect on commodity prices: Most globally traded commodities are denominated in USD, funded in USD and invoiced in USD. This is the channel through which the Fed’s monetary policy impacts commodity buyers ex-US. A stronger dollar means commodities in local-currency terms are more expensive, and vice versa. It also means production costs in states that do not peg their currencies to the USD go down, and vice versa. Chart 6Real USD Gains With US PPI During Reopening

Real USD Gains With US PPI During Reopening

Real USD Gains With US PPI During Reopening

Given the USD’s elevated level, copper prices in local-currency terms will continue to face a massive headwind on the demand side, and a massive tailwind on the production side. For households and firms buying commodities, or durable goods with a lot of metals in them (copper, stainless steel, etc.), Fed policy has a direct effect on how their budgets get allocated.7 In the short and long run macroeconomic variables such as the USD influence copper prices by increasing the cost of copper ex-US when the dollar rallies, and vice versa. Fundamental variables like tight inventories, which arise when demand is consistently above supply, impart an upward price bias to the copper forward curve (backwardation increases as inventories decrease). Domestic economic factors matter, too. Copper prices have been pummeled by the meltdown of China’s property sector, which has been the growth engine for the country’s economy, accounting for ~ 30% of its copper demand. The USD has remained well bid following Russia’s invasion of Ukraine, presenting a powerful headwind to commodity prices in general. This is particularly true for refined copper, given China accounts for more than 50% of total global consumption. China’s RMB dropped 11.4% vs. the USD from the start of the year to now. This has not stood in the way of a sharp increase in imports of the copper ore and refined metal this year, despite the country’s weak economic performance. Given China’s property-market slowdown and its zero-tolerance COVID-19 policy and its attendant lockdowns, it is difficult to pinpoint a cause for its increased copper demand. It may be opportunistic purchasing – buying the metal when prices are far lower than their peak earlier this year – or it could signal a post-Communist Party Congress increase in economic activity (e.g., more fiscal stimulus hitting the system) officials are preparing for. Investment Implications The EU’s metals-refining sector faces existential challenges as a result of the bloc’s energy crisis. Significant employers – not just the metal refiners – will be confronting limited energy supply and higher costs for years, given the tightness in conventional energy markets – oil, gas and coal. The renewable-energy sector also faces daunting challenges, as a result of difficulties faced by metals refiners and the energy crisis they presently confront. It is worthwhile noting that none of the renewables technology is possible without metals. Given the abundant lessons re reliance on a single supply source Russia’s invasion of Ukraine has provided, we expect investment in US metals mining and refining to increase, as consumers of copper, aluminum and zinc seek to diversify away from Chinese dominance of this sector. This will take time to build out, just as the increase in LNG supplies will take time. This likely will keep a bid under the USD, as manufacturing, mining and refining capex investment shifts to the US. We expect the EU’s drive to secure conventional energy will drive the bloc’s demand for liquified natural gas (LNG) and oil higher, even after currently planned short-term measures to increase LNG intake and distribution capacity are completed over the next 2-3 years. After being stopped out this past week, we will be re-instating our long XOP ETF position on tonight’s close, consistent with our view. Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Ashwin Shyam Research Analyst Commodity & Energy Strategy ashwin.shyam@bcaresearch.com Commodities Round-Up Energy: Bullish. European Commission President Ursula von der Leyen proposed additional economic sanctions against Russia yesterday including extending price caps on oil to third countries, following the call-up of reserves in Russia last week, and a veiled threat to use nuclear weapons against Ukraine. In a related matter, Gazprom, the state-owned gas producer and trading company, threatened to cut off the remaining gas sales to Europe via Ukraine – close to half the ~ 80mm cm /d still being sold via pipeline to the continent (Chart 7). It is apparent the EU has been anticipating a full shut-off of Russian pipeline gas shipments, which likely motivates von der Leyen’s proposal. Any proposal to increase sanctions on Russia would have to be unanimously approved. Base Metals: Bullish. In a boost to prospective Chile copper production, a BHP executive indicated he expects regulatory uncertainties in the largest copper producing state to ease. BHP mentioned earlier this year that legal certainty in Chile would be key to investing over USD 10 billion in the state. Earlier this month, Chilean voters rejected a constitution, which, among other things, could have curtailed mining operation by including new taxes and environmental regulations. Precious Metals: Neutral. In their Q2 platinum balances report, the World Platinum Investment Council (WPIC) expects FY 2022 surplus to rise more than 50% vs. its Q1 estimates to 974k oz. Weak platinum ETF demand resulting from a strong USD and rising interest rates is expected to outweigh operational constraints in South African and North American mining operations. Bolstering supply is the fact that Russian platinum – which constitutes ~11% of global supply – has been reaching buyers. However, this security of supply may not last. Once buyers’ long-term contracts for Russian platinum end, as in the case with aluminum, companies may self-sanction, turning to the spot market and other producing states instead. For palladium, SFA Oxford sees the metal's surplus dropping to ~92% y/y, as demand is expected to increase and production is forecast to fall (Chart 8). Chart 7

EU Energy Crisis, Strong USD Imperil Bloc’s Metals Industry

EU Energy Crisis, Strong USD Imperil Bloc’s Metals Industry

Chart 8

Palladium Balances Expected To Drop

Palladium Balances Expected To Drop

Footnotes 1 Please see Europe’s non-ferrous metals producers call for emergency EU action to prevent permanent deindustrialisation from spiralling electricity and gas prices, posted by Eurometaux 6 September 2022. 2 See, e.g., Exclusive: German utilities close to long-term LNG deals with Qatar, sources say published by reuters.com 20 September 2022. 3 For additional discussion, please see Energy Security Rolls Over EU's ESG Agenda, which we published 28 July 2022. It is available at ces.bcaresearch.com. 4 Please see Agenda for a resilient European metals supply for the green and digital transitions, posted by Eurometaux in mid-2020. 5 Please see Reconciling growth and decarbonisation amidst the energy crisis, posted by European Aluminium May 2022. 6 Please see Column: European smelter hits mean another year of zinc shortfall published by reuters.com 17 May 2022. 7 Please see "Global Dimensions of U.S. Monetary Policy" by Maurice Obstfeld, which appeared in the February 2020 issue of International Journal of Central Banking for an in-depth discussion and analysis. Investment Views and Themes Strategic Recommendations Trades Closed in 2022

Dear Client, This month’s Special Report has been written by my colleagues Mathieu Savary and Jeremie Peloso, of BCA’s European Investment Strategy service. The report was published in that service on September 26, and addressed the outlook for European assets. The EUR/USD stop buy mentioned in the report has since been triggered, meaning that our European Investment Strategy service is now long the euro with a stop loss position at 0.94. Although this is a tactical position for that service, it is consistent with the view expressed in Section 1 of our report that the dollar has significantly overshot versus the euro what currency fundamentals would imply. I trust you will find their report both interesting and insightful. Jonathan LaBerge, CFA The Bank Credit Analyst Highlights The outlook for European assets is uniquely muddled. European energy prices will remain elevated, but the worst of the adjustment is already behind us. The global economy is teetering on the edge of a recession and weak global growth is historically very negative for European assets. However, European valuations and earnings forecasts already discount an extremely severe outcome for global growth. A hawkish Fed should support the dollar, but investors increasingly realize foreign central banks are fighting inflation equally aggressively. The dollar already anticipates a global recession. Meantime, European credit offers a large spread pickup over sovereigns and even appears as a decent alternative to equities. Within a credit portfolio, we adopt a more cautious approach towards European investment grade bonds (IG) relative to their US counterpart. Instead, we recommend favoring UK IG over Euro Area IG as well as Swedish IG relative to US IG. Feature Following the hawkishness that transpired from the Fed press conference and revised forecasts last week, EUR/USD plunged below 0.99 and hit a 20-year low. Moreover, President Vladimir Putin’s announcement of a broader mobilization of the Russian army is stoking fears that the Ukrainian conflict will only be prolonged. The prospects of a lengthier war and greater energy market shock are raising further worries for Europe’s growth outlook, which weighs on European asset prices, notably the euro and the pound. The odds of a global financial accident are on the rise. Global central banks have joined the Fed and are relentlessly tightening global monetary and financial conditions. Moreover, the surging dollar is adding to global risks by raising the cost of capital around the world. This is a very fragile situation and the odds of a global recession have jumped significantly. Against this backdrop, investors should continue to overweight defensive equities at the expense of cyclical stocks. The euro also has more downside, but we are issuing a tentative stop-buy at EUR/USD 0.9650 with a stop at 0.9400. Credit remains a safer alternative to European stocks. The Evolving European Energy Backdrop Chart II-1All About The Gas

All About The Gas

All About The Gas

The surge of natural gas and electricity prices since the fall of 2021 has been one of the main drivers of the underperformance of European assets and the fall in the euro (Chart II-1). While the medium-term outlook for European energy prices remains fraught with risk, the near-term prospects have improved. Following a surge from €77.4/MWh in June to €340/MWh on August 26, one-month forward natural gas prices at the Dutch Title Transfer Facility (TTF) have declined 45% to €187/MWh. These wild gyrations reflect the evolution of both the natural gas flows from Russia, which have fallen from 3,060Mcm to 599 Mcm today, and the rapid buildup of natural gas inventories across the European Union. The good news is that the costly efforts to rebuild European gas inventories have been successful. EU-wide inventories are at 85.6% capacity, achieving its 80% storage objective well before November. Germany has gone even further, with storage use now standing at 90% of capacity. This large stockpile, along with the re-opening of coal power plants and consumption curtailment efforts, should allow Europe to survive the winter without Russian energy imports, as long as the temperatures are not abnormally cold. The absence of a summer dip in Norwegian gas exports and the surge in LNG flows to Europe have partially replaced the missing Russian inflows, thus helping Europe rapidly rebuild its natural gas inventories (Chart II-2). This success was a consequence of elevated European natural gas prices, which have allowed Europe to absorb LNG flows from the rest of the world (Chart II-3). Chart II-2No Restocking Without LNG

No Restocking Without LNG

No Restocking Without LNG

Chart II-3LNG Flowed Toward High Prices

LNG Flowed Toward High Prices

LNG Flowed Toward High Prices

So far, the European industrial sector has managed to adjust better than expected to the jump in the price of natural gas, a crucial energy input. Take Germany as an example. For the month of August, Germany’s consumption of natural gas by the industrial sector fell 22% below the 2018-2021 average (Chart II-4, top panel), while PPI moved up vertically. Yet, industrial output is only down 5% year-on-year and industrial capacity utilization stands at 85%, which is still a level that beats two thirds of the readings recorded between 1990 and this the most recent quarter (Chart II-4, bottom panel). The adjustment will be uneven across various industries, with those most voracious of natural gas likely to experience a declining share of Europe’s gross value added. Using the German example once again, we can see that the chemicals, basic metal manufacturing, and paper products sectors are the most at risk from higher natural gas prices and most likely therefore to suffer the most from gas rationing this winter (Chart II-5). Chart II-4A Surprisingly Successful Transition

A Surprisingly Successful Transition

A Surprisingly Successful Transition

Chart II-5The Three Sectors Most At Risk

October 2022

October 2022

Going forward, important changes are likely to take place that will allow the European economy to continue to survive on diminished Russian gas flows: European natural gas prices will remain elevated compared to the rest of the world to attract LNG flows to the region. Importantly, Europe’s capacity to absorb these flows keeps increasing, as more re-gasification ships are docked around the continent. Moreover, North America is building more facilities to export LNG to Europe. Chart II-6Nuclear Energy's Contribution Will Rebound

Nuclear Energy's Contribution Will Rebound

Nuclear Energy's Contribution Will Rebound

Nuclear electricity production will rebound. Currently, the EU’s nuclear production is around 43.2TWh, well below the normal 60TWh to 70TWh winter levels, driven mostly by the collapse in French production from 35TWh to 18TWh (Chart II-6). This decline in nuclear electricity generation has accentuated the upward pressure on European natural gas and electricity prices. One of the key objectives of the nationalization of EDF by the French government is to accelerate the maintenance of France’s ageing nuclear power plants and allow a return to more normal production levels by the winter. The role of natural gas in European household’s energy mix will decline. Currently, EU households are the largest natural gas consumers and account for 41% of the bloc’s gas consumption (Chart II-7). It will be easier to replace their natural gas consumption over time with other sources of energy than it will be to cut the industrial sector’s consumption extensively. As a result, even if European natural gas imports are permanently below 2021 levels, the industrial sector will not bear the brunt of the adjustment. Chart II-7Households To Be Displaced

October 2022

October 2022

These developments imply that natural gas prices have limited downside. However, we believe that the worst of the spike in prices is behind us, at least over the near term. The reason is that the inelastic buying created by the inventory re-stocking exercise since May 2022 is ending. In fact, the German Federal Minister for Economic Affairs and Climate Action, Robert Habeck, declared last week that his country would no longer purchase gas at any price. Chart II-8The Most Painful Part Of The Adjustment Is Over

The Most Painful Part Of The Adjustment Is Over

The Most Painful Part Of The Adjustment Is Over

If prices stabilize around €200/MWh, European industrial activity will continue to face a headwind, but the worst of the adjustment process will be in the rearview mirror as natural gas inflation recedes (Chart II-8). Ultimately, capitalist systems are dynamic, and it is this rapid change in price that causes the most pain. In other words, the impoverishment of the European private sector has already happened. Steady states are easier to manage. Moreover, if natural gas prices eventually follow the future’s curve (this is a big “if”), the picture for Europe will improve considerably. One additional mitigating factor should ease the pain being experienced by the European private sector. Fiscal policy is responding very aggressively to the current energy crisis. So far, EU countries and the UK have allocated more than €500 billion to protect their private sectors against higher energy costs (Chart II-9) and the UK just announced tax cuts of £45 billion. This is in addition to the disbursement of €150 billion from the NGEU funds in 2023. Moreover, the European commission is planning to modify the EU fiscal rules to abandon annual structural deficit targets and for debt sustainability to be evaluated over a ten-year period. Bottom Line: The worst of Europe’s adjustment to higher energy prices is now behind us. However, European energy prices will remain elevated, which will continue to put Europe at a handicap compared to the rest of the world. Chart II-9Massive Fiscal Support

October 2022

October 2022

Bad News From The Rest Of The World Chart II-10A Global Recession This Way Comes

A Global Recession This Way Comes

A Global Recession This Way Comes

The worst of Europe’s energy crisis is behind us, but the world is teetering toward a recession, which will hurt the trade- and manufacturing-sensitive European economy. The tightening in global financial conditions created by the surge in the dollar and by the jump in global yields is pushing the US Manufacturing ISM and the Euro Area PMIs toward the low-40s, which is consistent with a recession (Chart II-10). The problem does not stop there. Global central banks have become solely focused on fighting inflation. For 2023, the FOMC’s dot plot forecasts both an interest rate rise to 4.6% and a 0.7% increase in the unemployment rate. This is tantamount to the Fed telling the market that it will increase interest rates as a recession emerges to repress inflation. Not to be undone, European central banks are also rapidly increasing their policy rates, even as they also forecast an imminent deterioration in domestic growth conditions. Quickly tightening policy in a slowing growth environment, especially as the dollar hits a 20-year high, is a recipe for a financial accident and a global recession. Chart II-11No Help From China

No Help From China

No Help From China

Moreover, China’s economy is still unable to create a positive offset to the deterioration in global monetary and financial conditions. The marginal propensity of China’s private sector to consume remains in a downtrend, hampered by the country’s zero-COVID policy and the continuing meltdown in real estate activity (Chart II-11). Furthermore, the most rapid decline in the yuan exchange rate in 5 years is imparting an additional downside risk to the global economy. European stocks are uniquely exposed to these threats. Europe overweights deep cyclicals, which are currently squeezed by the deteriorating global growth outlook. The message from the collapse in FedEx’s stocks on very poor guidance is particularly ominous: this company has a much closer correlation with the Dow Jones Euro STOXX 50 than with the S&P 500 (Chart II-12). European share prices are already factoring in much of the bad news. Valuations are significantly less expensive than they once were. The Shiller P/E ratio of European equities and their equity risk premium stand at the same levels as those in the 1980s. This is in sharp contrast to the US (Chart II-13). Chart II-12FedEx's Gloomy Delivery

FedEx's Gloomy Delivery

FedEx's Gloomy Delivery

Chart II-13Low CAPE In Europe

Low CAPE In Europe

Low CAPE In Europe

European forward earnings have also already done considerable work adjusting downward. Excluding energy, 2022 and 2023 forward EPS are down 11.7% and 13.3% since their peak, respectively (Table II-1). But inflation flatters earnings growth and European large-cap indices are dominated by multinational firms, which implies that looking at earnings in USD terms makes more sense. In both real and USD terms, 2022 and 2023 forward EPS, excluding energy, are already down 28.7% and 30.1%, respectively. These adjustments are in line with previous recessions. Table II-1A Deep Downgrade To European Earnings

October 2022

October 2022

The counterargument is that analysts still expect positive earnings growth in 2023 relative to 2022. However, at 4%, this increase in expected earnings is still well below inflation and 6% below the average expected growth in forward earnings recorded over the past 35 years (Chart II-14). Additionally, a global recession could put further downward pressure on energy prices in Europe, which would create an additional cushion under European earnings in 2023. The implication here is that it still makes sense to be modestly long European equities in absolute terms, especially for investors with an investment horizon of twelve months or more. However, we cannot be complacent, as the risk of an additional selloff is still too large for comfort. As a result, for now investors should only garner a small exposure to European equities and do so while favoring defensive names over cyclical ones (Chart II-15). Chart II-14Weak Forward Earnings Growth

Weak Forward Earnings Growth

Weak Forward Earnings Growth

Chart II-15Continue To Favor Defensive Names

Continue To Favor Defensive Names

Continue To Favor Defensive Names

Bottom Line: European stocks must still contend with the growing threat of a global recession catalyzed by tighter financial conditions and aggressive global central banks. The good news is that they already discount considerable pessimism, as illustrated by their low valuations and downgraded forward earnings. Consequently, investors can continue to nibble at European equities, but do so to a limited degree and by favoring defensive stocks over cyclical ones, at least for now. The Euro Dilemma On the back of the very hawkish Fed meeting and the announcement of Russia’s broadened military mobilization, the EUR/USD broke below the 0.99 support level and fell under 0.98, a level we judged in the past as very attractive on a six-to-nine months basis. Obviously, Fed Chair Jerome Powell’s reaffirmation of the FOMC’s war on inflation is a major boost to the dollar. The momentum property of the greenback implies that it has room to rally further in the near term. This narrative, however, overlooks the fact that the Fed is not the only central bank intent on fighting inflation, no matter the cost. The Norges Bank, the Riksbank, the ECB, and even the SNB have all showed their willingness to move aggressively against inflation. While the BoE only increased rates by 50bps last week, its communication suggested that an at least 75bps increase would be due at the November meeting, when the MPC publishes its Monetary Policy report that will incorporate the impact of the budget measures announced by new British Prime Minister, Liz Truss. As a result, market interest rate expectations are climbing in the US, but they are rising even faster in Europe, albeit from a lower base. However, the decline in the expected rate of interest in the US relative to Europe and in the number of expected hikes in the US relative to Europe are consistent with a sharp decline in the DXY in the coming months (Chart II-16). Due to its 80% weight in European currencies, a weaker DXY implies a rebound in the EUR, GBP, CHF, NOK, and SEK against the USD. Moreover, there could be room for expected interest rate differentials to narrow further against the dollar. The analysis we published two weeks ago shows that, even when the different nonfinancial private debt loads are accounted for, the gap in the US and Eurozone r-star stands at 1%. However, the spread between the Fed funds rate’s upper bound and the ECB Deposit Rate is 2%. The gap between the July 2023 US and Eurozone OIS is 1.7%. Since European inflation may prove more stubborn than that of the US in the near term, there is scope for the expected interest rate gap to narrow further, especially as the Euro Area final domestic demand is surprisingly more robust than that of the US (Chart II-17). Chart II-16The Rest Of The World Is Catching Up To The Fed

The Rest Of The World Is Catching Up To The Fed

The Rest Of The World Is Catching Up To The Fed

Chart II-17Surprising European Resilience

Surprising European Resilience

Surprising European Resilience

What about global growth? The view that the global economy is about to experience a recession is consistent with a stronger dollar, since the greenback is an extremely countercyclical currency. However, the DXY’s 25% rally since January 2021 already prices in such an outcome (Chart II-18). Similarly, the euro is trading again at 2002 levels, which is also in line with a global recession with deep negative repercussions for the Eurozone. Additionally, the Euro has fallen 21% since May 2021, which compares to the 21.4% fall in 2008, the 20% decline in 2010, the 18% plunge in 2011/12 and the 24% collapse in 2014/15; yet EUR/USD is much cheaper now than in any of those instances. Moreover, the wide difference between the competitiveness of Germany and that of the rest of the Euro Area has now faded, which means that a major handicap against the euro has disappeared (Chart II-19). Chart II-18The Dollar Already Foresees A Recession

The Dollar Already Foresees A Recession

The Dollar Already Foresees A Recession

Chart II-19Normalizing Eurozone Internal Competitiveness

Normalizing Eurozone Internal Competitiveness

Normalizing Eurozone Internal Competitiveness

This does not mean that the euro is not without risk. First, since the major euro collapse began in June 2021, EUR/USD breakdowns have been followed by average declines of 3.6%, ranging from 2.7% to 4.2%. Since the dollar is a momentum currency, it is unlikely that this time will be different. Second, if the tightening in global policy does cause a financial accident, the dollar will catch one last major bid that could push EUR/USD toward 0.9. As a result, to mitigate the danger, we recommend setting a stop-buy in the euro at EUR/USD 0.965 or 2.6% below the breakdown level of 0.9904. This position comes with a stop-loss at 0.94. For now, we would view this bet as a tactical position if it were triggered. Bottom Line: While a hawkish FOMC is very positive for the dollar, markets now expect foreign central banks to catch up to some extent with the Fed. This process is dollar bearish. Additionally, while a global recession would be supportive of the greenback, the USD already discounts this scenario. Instead, Europe is proving surprisingly resilient, which could soon create a tailwind for EUR/USD. Set a stop-buy at EUR/USD 0.965, with a stop-loss at 0.94. Market Update: European Credit After Central Bank Week For investors concerned with the left-tail risk in European equities, European credit offers a credible alternative in the near term. This asset class is also attractive relative to European government bonds. Chart II-20Central Bank Week

October 2022

October 2022

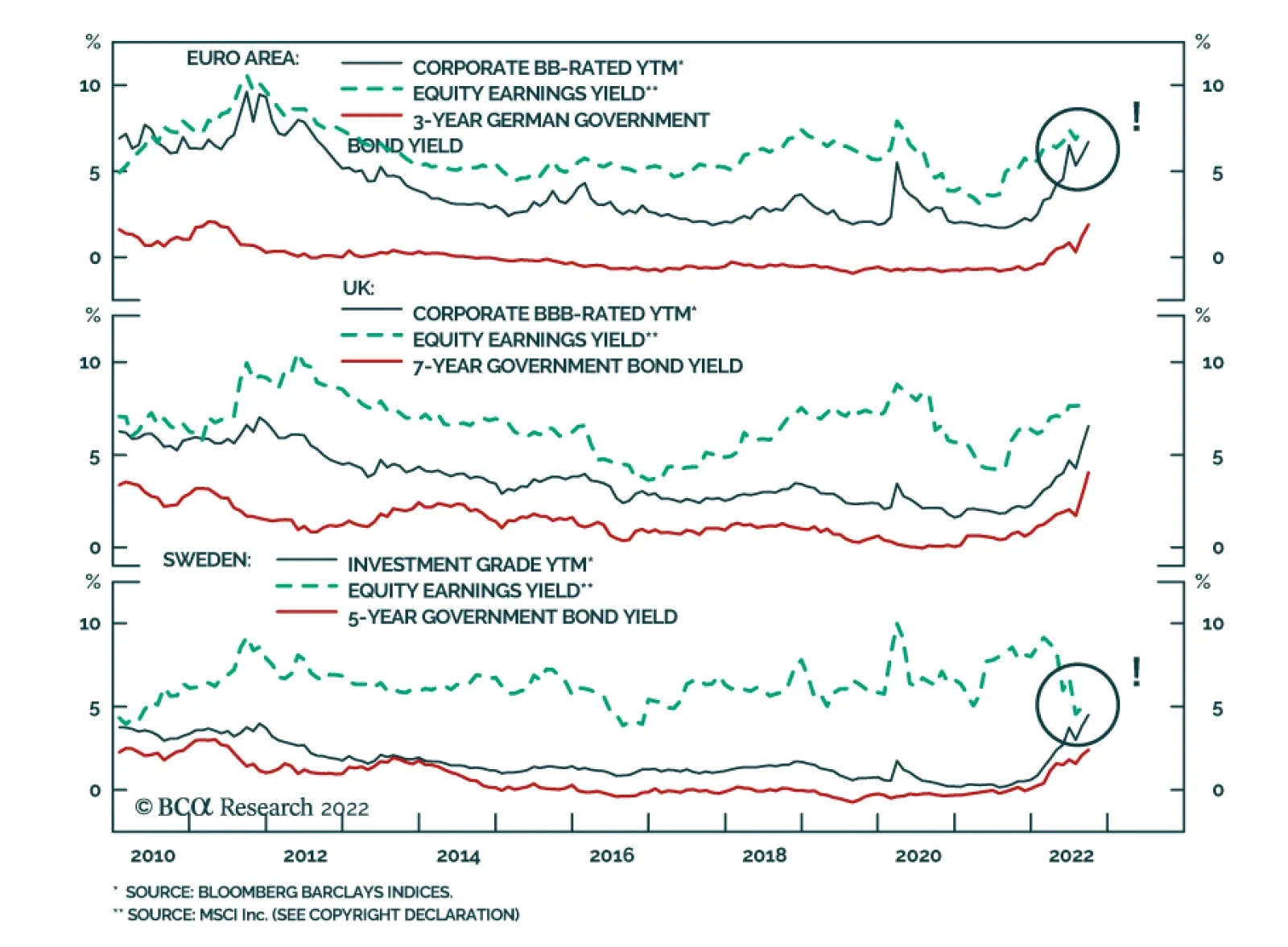

Taken together, the Fed, the ECB, the BoE, the Riksbank, the Norges Bank, the SNB, and the BoC have tightened policy by 475bps over the past month (Chart II-20). Moreover, the SNB’s hike closed the chapter of negative rates in Europe. But make no mistake – there will be a second chapter. Until then, European corporate bond yields have risen enough to offer attractive spreads over duration-matched government bonds and to challenge the earnings yield provided by equities (Chart II-21). Besides, the volatility observed in equity markets over the past few months makes the European corporate bond more appealing. In the Euro Area, BB-rated bonds, which are the highest credit quality and largest tranche within the high-yield space, are particularly attractive. They sport a 6.6% YTM, at a spread of 480bps over 3-year German government bond yields. This compares to an equity earnings yield of 7.4% (Chart II-21, top panel). In other European corporate bond markets, there is no need to go down in credit quality. Yields-to-maturity for investment grade corporate bonds in the UK, Sweden, and Switzerland provide appealing alternatives to equities, with shorter duration still. This is especially true in Sweden, where the equity earnings yield has collapsed and is now only 60bps above Swedish IG yield, with substantially greater risk. Meanwhile, the spread pickup offered by Swiss IG over Swiss government bonds of similar duration is at its widest in more than ten years (Chart II-21, bottom panel). This week, we turn neutral on European credit versus US credit. Back in March, we made the case that European credit would outperform its US counterpart in response to a more hawkish Fed than the ECB. Since then, European IG outperformed US IG by 1% on a total return basis. However, with the Fed funds rate at 3.25%, traders now expect more monetary policy tightening from the ECB, which often corresponds to an underperformance of Euro Area credit relative to that of the US (Chart II-22, top panel). On the other hand, Swedish IG is expected to outperform US IG over the next six months (Chart II-22, bottom panel). Chart II-21Push Back Against TINA Argument

Push Back Against TINA Argument

Push Back Against TINA Argument

Chart II-22Heed The Message From OIS Curve Differentials

Heed The Message From OIS Curve Differentials

Heed The Message From OIS Curve Differentials

Mathieu Savary, Chief European Strategist Mathieu@bcaresearch.com Jeremie Peloso, Editor/Strategist JeremieP@bcaresearch.com Footnotes

Executive Summary For the first time in a decade, it is much less attractive to buy than to rent a home. In both the UK and US, the mortgage rate is now almost double the average rental yield. To reset the equilibrium between buying and renting a home, either mortgage rates must come down by around 150 bps, or house prices must suffer a large double-digit correction. Or some combination, such as mortgage rates down 100 bps and house prices down 10 percent. In the US, a 10-year upcycle in housing investment has resulted in overinvestment relative to the number of households. Falling house prices coming hot on the heels of a combined stock and bond market crash will unleash a deflationary impulse in 2023, which will return economies to 2 percent inflation. This reiterates our ‘2022-23 = 1981-82’ template for the markets. A coordinated global recession will cause bond prices to enter a sustained rally in 2023, in which the 30-year T-bond yield will fall to sub-2.5 percent. Meanwhile, the S&P 500 will test 3500, or even 3200, before a strong rally will lift it through 5000 later in 2023. It Now Costs Twice As Much To Buy Than To Rent A UK Home!

It Now Costs Twice As Much To Buy Than To Rent A UK Home!

It Now Costs Twice As Much To Buy Than To Rent A UK Home!

Bottom Line: Falling house prices coming hot on the heels of a combined stock and bond market crash will unleash a deflationary impulse in 2023, which will return economies to 2 percent inflation. Feature Mortgage rates around the world have skyrocketed. The UK 5-year fixed mortgage rate which started the year at under 2 percent has more than doubled to over 5 percent. And the US 30-year mortgage rate, which began the year at 3 percent, now stands at an eyewatering 7 percent, its highest level since the US housing bubble burst in 2008. This raises a worrying spectre. Is the recent surge in mortgage rates about to trigger another housing crash? (Chart I-1 and Chart I-2). Chart I-1UK Mortgage Rate Has Doubled

UK Mortgage Rate Has Doubled

UK Mortgage Rate Has Doubled

Chart I-2US Mortgage Rate Has Doubled

US Mortgage Rate Has Doubled

US Mortgage Rate Has Doubled

A good way to answer the question is to compare the cashflow costs of buying versus renting a home. This is because home prices are set by the volume of homebuyers versus home-sellers. If would-be homebuyers decide to rent rather than to buy – because renting gets them ‘more house’ – then it will drag down home prices. Here’s the concern. For the first time in a decade, it is much less attractive to buy than to rent a home. In both the UK and US, the mortgage rate is now almost double the average rental yield. Put another way, whatever your monthly housing budget, you can now rent a home worth twice as much as you can buy (Chart I-3 and Chart I-4). Chart I-3It Now Costs Twice As Much To Buy Than To Rent A UK Home!

It Now Costs Twice As Much To Buy Than To Rent A UK Home!

It Now Costs Twice As Much To Buy Than To Rent A UK Home!

Chart I-4It Now Costs Twice As Much To Buy Than To Rent A US Home!

It Now Costs Twice As Much To Buy Than To Rent A US Home!

It Now Costs Twice As Much To Buy Than To Rent A US Home!

The Universal Theory Of House Prices Buying and renting a home are not the same thing, so the head-to-head comparison between the mortgage rate and rental yield is a simplification. Buying and renting are similar in that they both provide you with somewhere to live, a roof over your head or, in economic jargon, the consumption service called ‘shelter’. But there are two big differences. First, unlike renting, buying a home also provides you with an investment whose value you expect to increase in the long run. Second, unlike renting, buying a home incurs you the costs of maintaining it and keeping it up-to-date. Studies show that the annual cost averages around 2 percent of the value of the home.1 So, versus renting, buying a home provides you with an expected capital appreciation, but incurs you a ‘depreciation’ cost of around 2 percent a year. Which results in the following equilibrium between buying and renting: Mortgage rate = Rental yield + Expected house price appreciation - 2 But we can simplify this. In the long run, the price of any asset must trend in line with its income stream. Therefore, expected house price appreciation equates to expected rental growth. Also, rents move in lockstep with wages (Chart I-5). Understandably so, because rents must be paid from wages. And wage growth itself just equals consumer price inflation plus productivity growth, which averages around 1 percent (Chart I-6). Pulling all of this together, the equilibrium simplifies to: Chart I-5Rents Track Wages

Rents Track Wages

Rents Track Wages

Chart I-6Rent Inflation = Wage Inflation = Consumer Price Inflation + 1

Rent Inflation = Wage Inflation = Consumer Price Inflation + 1

Rent Inflation = Wage Inflation = Consumer Price Inflation + 1

Mortgage rate = Rental yield + Expected consumer price inflation - 1 So, here’s our first conclusion. Assuming central banks achieve their long-term inflation target of 2 percent, the equilibrium becomes: Mortgage rate = Rental yield + 1 Under this assumption, to justify the current UK rental yield of 3 percent, the UK mortgage rate must plunge to 4 percent. But given that the government has just triggered an incipient balance of payments and currency crisis, the mortgage rate is likely to head even higher. In which case the rental yield must rise to at least 4 percent. Meaning either house prices falling 25 percent, or rents rising 33 percent. Meanwhile, to justify the current US rental yield of 3.7 percent, the US mortgage rate must plunge to 4.7 percent. Alternatively, to justify the current mortgage rate of 7 percent, the rental yield must surge to 6 percent. Meaning either house prices crashing 40 percent, or rents surging 60 percent. More likely though, all variables will correct. The equilibrium between buying and renting will be re-established by some combination of lower mortgage rates, lower house prices, and higher rents. The Housing Investment Cycle Is Turning Down The relationship between buying and renting a home raises an obvious counterargument. What if central banks cannot achieve their goal of price stability? In this case, expected inflation in the equilibrium would be considerably higher than 2 percent. This would justify a much higher mortgage rate for a given rental yield. Put differently, it would justify rental yields to stay structurally low (house prices to stay structurally high), even if mortgage rates marched higher. In an inflationary environment, houses would become the perfect foils against inflation. In an inflationary environment, houses would become the perfect foils against inflation because expected rental growth would track inflation – allowing rental yields to stay depressed versus much higher mortgage rates. This is precisely what happened in the 1970s. When the US mortgage rate peaked at 18 percent in 1981, the US rental yield barely got above 6 percent (Chart I-7). Chart I-7In The Inflationary 70s, The Rental Yield Remained Well Below The Mortgage Rate...

In The Inflationary 70s, The Rental Yield Remained Well Below The Mortgage Rate...

In The Inflationary 70s, The Rental Yield Remained Well Below The Mortgage Rate...

If the market fears another such inflationary episode, would it make the housing market a good investment? In the near term, the answer is still no, for two reasons. First, even if rental yields do not track mortgage rates higher point for point, the yields do tend to move in the same direction – especially when mortgage rates surge as they did in the 1970s (Chart I-8). Some of this increase in rental yields might come from higher rents, but some of it might also come from lower house prices. Chart I-8...But Even In The 70s, The Rental Yield And Mortgage Rate Moved Directionally Together

...But Even In The 70s, The Rental Yield And Mortgage Rate Moved Directionally Together

...But Even In The 70s, The Rental Yield And Mortgage Rate Moved Directionally Together

Second, based on the US, it is a bad time in the housing investment cycle. Theoretically and empirically, residential fixed investment tracks the number of households in the economy. But there are perpetual cycles of underinvestment and overinvestment – the most spectacular being the overinvestment boom that preceded the 2007-08 housing crisis. US housing investment has just experienced a 10-year upcycle in which it has overshot its relationship with the number of households. Therefore, contrary to the popular perception, there is not an undersupply of homes, but a marked oversupply relative to the number of households. (Chart I-9). This is important because, as the cycle turns down now – as it did in 1973, 1979, 1990, and 2007 – the preceding overinvestment always weighs down housing valuations (Chart I-10). Chart I-9The US Housing Investment Cycle Has Moved Into Overinvestment

The US Housing Investment Cycle Has Moved Into Overinvestment

The US Housing Investment Cycle Has Moved Into Overinvestment

Chart I-10A Housing Investment Downcycle Always Weighs On Housing Valuations

A Housing Investment Downcycle Always Weighs On Housing Valuations

A Housing Investment Downcycle Always Weighs On Housing Valuations

The Investment Conclusions Let’s sum up. If the market believes that economies will return to price stability, then to reset the equilibrium between buying and renting a home, either mortgage rates must come down by around 150 bps, or house prices must suffer a large double-digit correction. Or some combination, such as mortgage rates down 100 bps and house prices down 10 percent. If the market believes that economies will not return to price stability, then house prices are still near-term vulnerable to rising mortgage rates – especially in the US, as a 10-year upcycle in housing investment has resulted in overinvestment relative to the number of households. US housing investment has just experienced a 10-year upcycle in which it has overshot its relationship with the number of households. Falling house prices coming hot on the heels of a combined stock and bond market crash will unleash a deflationary impulse in 2023, which will return economies to 2 percent inflation – even if the markets do not believe it now. This reiterates our ‘2022-23 = 1981-82’ template for the markets, as recently explained in Markets Still Echoing 1981-82, So Here’s What Happens Next. In summary, a coordinated global recession will cause bond prices to enter a sustained rally in 2023, in which the 30-year T-bond yield will fall to sub-2.5 percent. Meanwhile, the S&P 500 will test 3500, or even 3200, before a strong rally will lift it through 5000 later in 2023. Analysing The Pound’s Crash Through A Fractal Lens Finally, the incipient balance of payments and sterling crisis triggered by the UK government’s unfunded tax cuts has collapsed the 65-day fractal structure of the pound (Chart I-11). This would be justified if the Bank of England does not lean against the fiscal laxness with a compensating tighter monetary policy. But if, as we expect, monetary policy adjusts as a short-term counterbalance, then sterling will experience a temporary, but playable, countertrend bounce. Chart I-11The Pound Usually Turns When Its Fractal Structure Has Collapsed

The Pound Usually Turns When Its Fractal Structure Has Collapsed

The Pound Usually Turns When Its Fractal Structure Has Collapsed

On this assumption, a recommended tactical trade, with a maximum holding period of 65 days, is to go long GBP/CHF, setting a profit target and symmetrical stop-loss at 4 percent. Chart 1Hungarian Bonds Are Oversold

Hungarian Bonds Are Oversold

Hungarian Bonds Are Oversold

Chart 2Copper's Tactical Rebound Maybe Over

Copper's Tactical Rebound Maybe Over

Copper's Tactical Rebound Maybe Over

Chart 3US REITS Are Oversold Versus Utilities

US REITS Are Oversold Versus Utilities

US REITS Are Oversold Versus Utilities

Chart 4FTSE100 Outperformance Vs. Euro Stoxx 50 Is Vulnerable

FTSE100 Outperformance Vs. Euro Stoxx 50 Is Vulnerable

FTSE100 Outperformance Vs. Euro Stoxx 50 Is Vulnerable

Chart 5Netherlands' Underperformance Vs. Switzerland Has Ended

Netherlands' Underperformance Vs. Switzerland Has Ended

Netherlands' Underperformance Vs. Switzerland Has Ended

Chart 6The Sell-Off In The 30-Year T-Bond At Fractal Fragility

The Sell-Off In The 30-Year T-Bond At Fractal Fragility

The Sell-Off In The 30-Year T-Bond At Fractal Fragility

Chart 7Food And Beverage Outperformance Is Exhausted

Food And Beverage Outperformance Is Exhausted

Food And Beverage Outperformance Is Exhausted

Chart 8German Telecom Outperformance Has Started Is Fragile

German Telecom Outperformance Has Started Is Fragile

German Telecom Outperformance Has Started Is Fragile

Chart 9Japanese Telecom Outperformance Vulnerable To Reversal

Japanese Telecom Outperformance Vulnerable To Reversal

Japanese Telecom Outperformance Vulnerable To Reversal

Chart 10The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

Chart 11The Strong Downtrend In The 3 Year T-Bond Is Fragile

The Strong Downtrend In The 3 Year T-Bond Is Fragile

The Strong Downtrend In The 3 Year T-Bond Is Fragile

Chart 12The Outperformance Of Tobacco Vs. Cannabis Is Fragile

The Outperformance Of Tobacco Vs. Cannabis Is Fragile

The Outperformance Of Tobacco Vs. Cannabis Is Fragile

Chart 13Biotech Is A Major Buy

Biotech Is A Major Buy

Biotech Is A Major Buy

Chart 14Norway's Outperformance Has Ended

Norway's Outperformance Has Ended

Norway's Outperformance Has Ended

Chart 15Cotton Versus Platinum Has Reversed

Cotton Versus Platinum Has Reversed

Cotton Versus Platinum Has Reversed

Chart 16Switzerland's Outperformance Vs. Germany Is Exhausted

Switzerland's Outperformance Vs. Germany Is Exhausted

Switzerland's Outperformance Vs. Germany Is Exhausted

Chart 17USD/EUR Is Vulnerable To Reversal

USD/EUR Is Vulnerable To Reversal

USD/EUR Is Vulnerable To Reversal

Chart 18The Outperformance Of MSCI Hong Kong Versus China Has Ended

The Outperformance Of MSCI Hong Kong Versus China Has Ended

The Outperformance Of MSCI Hong Kong Versus China Has Ended

Chart 19US Utilities Outperformance Vulnerable To Reversal

US Utilities Outperformance Vulnerable To Reversal

US Utilities Outperformance Vulnerable To Reversal

Chart 20The Outperformance Of Oil Versus Banks Is Exhausted

The Outperformance Of Oil Versus Banks Is Exhausted

The Outperformance Of Oil Versus Banks Is Exhausted

Dhaval Joshi Chief Strategist dhaval@bcaresearch.com Footnotes 1 The Rate of Return on Everything, 1870–2015 (frbsf.org) Fractal Trading System Fractal Trades

Will Surging Mortgage Rates Crash House Prices?

Will Surging Mortgage Rates Crash House Prices?

Will Surging Mortgage Rates Crash House Prices?

Will Surging Mortgage Rates Crash House Prices?

6-12 Month Recommendations 6-12 MONTH RECOMMENDATIONS EXPIRE AFTER 15 MONTHS, IF NOT CLOSED EARLIER. Structural Recommendations Closed Fractal Trades Indicators To Watch - Bond Yields Chart II-1Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Chart II-2Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Chart II-3Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Chart II-4Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Interest Rate Expectations Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

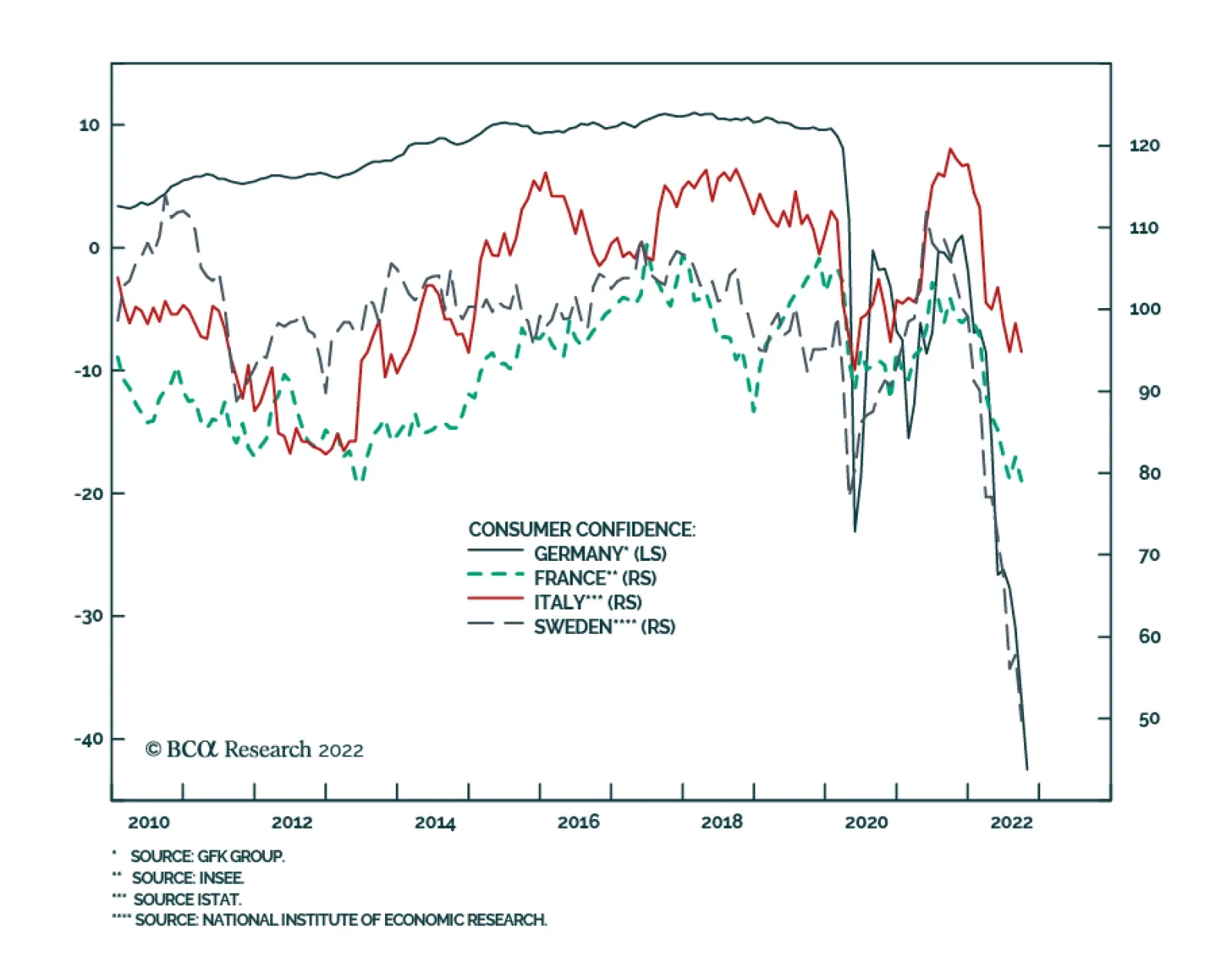

Consumer confidence continues to deteriorate across Europe. In Germany, GFK consumer confidence fell for the fourth straight month, collapsed to a new record low of -42.5 from -36.8. Similarly, French consumer confidence declined from 82 to 79, matching the…

Executive Summary Upward Repricing Of Bond Yields Continues

Upward Repricing Of Bond Yields Continues

Upward Repricing Of Bond Yields Continues

In this report, we discuss our move last week to shift to a below-benchmark overall global duration stance in more detail. Our strongest conviction view on developed market government bonds is underweighting US Treasuries. The outcome of last week’s FOMC meeting, where the Fed committed to a rapid shift to restrictive US monetary policy, supports that position. Our strongest conviction overweight is on Japan, with the Bank of Japan both willing and able to maintain its cap on longer-term JGB yields. We are also overweight countries where it will be difficult for central banks to lift rates as much as markets expect – core Europe, Australia and Canada. The explosion in UK bond yields, and collapse of the British pound, seen after last week’s UK “mini-budget” shows that investors have not lost the power to punish fiscal and monetary policies that are non-credible - like a massive debt-financed tax cut at a time of high inflation. As a result, the Bank of England will now be forced to raise rates much more than we had been expecting, and Gilts will remain extremely volatile in the near-term. Bottom Line: Maintain a below-benchmark overall duration stance in global bond portfolios. Stay underweight US Treasuries. Upgrade exposure to government bonds in Japan and Canada to overweight, but tactically downgrade UK Gilts to underweight until a more market-friendly policy mix leads to greater stability of the British pound. Feature We shifted our recommended stance on overall global portfolio duration to below-benchmark in a Special Alert published last week. In this report, we go into the rationale for that move in more detail, and present specific details of that shift in terms of allocations by country across the various yield curves. Related Report Global Fixed Income StrategyReduce Global Portfolio Duration To Below-Benchmark The global inflation and monetary policy backdrops remain toxic for bond markets. Last week saw interest rate increases from multiple developed economy central banks, including the Fed and Bank of England (BoE). The magnitudes of the rate hikes unnerved bond investors, with even the likes of perennial low yielders like the Swiss National Bank and Riksbank lifting rates by 75bps and 100bps, respectively. The Fed followed up its own 75bp hike by digging in its heels on the need for additional policy tightening after the 300bps of hikes already delivered this year (Chart 1). Fed Chair Jerome Powell strongly hinted that a policy-induced US recession is likely the only way to return overshooting US inflation back to the Fed’s 2% target. This triggered a breakout of the benchmark US 10-year Treasury yield above 3.5%. But the real fireworks in global bond markets occurred after the UK government announced its “mini-budget” last Friday that included massive tax cuts to be funded by debt issuance, triggering a sharp decline in the British Pound and spike in UK Gilt yields – a move that spilled over into other bond markets, pushing government bond yields to cyclical highs in the US and euro area. Chart 1Central Banks Keep Trying To “Out-Hawk” Each Other

The Global Bond Bear Market Continues

The Global Bond Bear Market Continues

Chart 2Yields Are Now Driven By Rate Hike Expectations, Not Inflation

Yields Are Now Driven By Rate Hike Expectations, Not Inflation

Yields Are Now Driven By Rate Hike Expectations, Not Inflation

We had been anticipating another move upward in global bond yields for this cycle, and we shifted to a below-benchmark overall global duration stance in advance of the Fed and BoE meetings last week. We see this next move higher in yields as being driven not by rising inflation expectations but by an upward repricing of interest rate expectations, leading to additional increases in real bond yields (Chart 2). Trying to pick a top in bond yields has now become a game of forecasting the level to which policy rates must rise in the current global monetary tightening cycle. On that front, there is still scope for rate expectations, and bond yields, to move higher in most developed market countries, justifying our downgrade of our recommended overall duration exposure to below-benchmark. Shifting rate expectations also lead to the changes in country bond allocations we announced last week. Rate Expectations And Country Bond Allocations Our proxy for medium-term nominal terminal rate expectations in developed market countries, the 5-year/5-year forward overnight index swap (OIS) rate, has been tracking 10-year bond yields very closely in the US and UK and, to a lesser extent, Europe (Chart 3). In those regions, the OIS curves are pricing in an increasing medium-term level of policy rates, leading to markets repricing government bond yields higher. In the US, the OIS curve is pricing in a 2023 peak for the fed funds rate of 4.67%, but with only a modest path of rate cuts in 2024 and 2025, leading to a 5-year/5-year OIS projection of 3.36% as of Monday’s market close. After the Gilt market rout, the UK OIS curve is now pricing in a 2023 peak Bank Rate over 6%, with our medium-term nominal rate proxy settling at 3.69%. In the euro area, the OIS curve is discounting a 2023 peak in the ECB policy rate of 3.22%, with a 5-year/5-year forward OIS rate of 2.7%. For all three of those regions, the market is now pricing in the highest peak in rates for the current tightening cycle. That is not the case in Canada or Australia, where rate expectations and longer-term bond yields are still below cyclical peaks (Chart 4). Japan remains the outlier, with the Bank of Japan’s yield curve control keeping 10-year JGB yields capped at 0.25%, even with the Japan OIS curve pricing in a medium-term terminal rate of 0.75%. Chart 3Rising Yields Reflect Higher Terminal Rate Expectations

Rising Yields Reflect Higher Terminal Rate Expectations

Rising Yields Reflect Higher Terminal Rate Expectations

Chart 4Our High-Conviction Government Bond Overweights

Our High-Conviction Government Bond Overweights

Our High-Conviction Government Bond Overweights

After looking at all the repricing of interest rate expectations and bond yields, we can determine our preferred government bond allocations within our strategic model bond portfolio framework. The US Remains Our Favorite Government Bond Underweight The new set of interest rate forecasts (“the dots”) presented at last week’s Fed meeting showed that the median FOMC member was forecasting the fed funds rate to rise to 4.4% by the end of 2022 and 4.6% by the end of 2023, before falling to 3.9% and 2.9% and the end of 2024 and 2025, respectively. Those are all significant increases from the June dots, where the expectations called for the funds rate to hit 3.4% by end-2022 and 3.8% by end-2023. The median Fed forecasts are now broadly in line with the pricing in the US OIS curve for 2022-2024, although the market expects higher rates than the FOMC in 2025 (Chart 5). Chart 5USTs Still Vulnerable To Additional Fed Hawkish Surprises

The Global Bond Bear Market Continues

The Global Bond Bear Market Continues

There has been a lot of back and forth between the Fed and the markets this year, but the market has generally lagged the Fed interest rate projections for 2023 and 2024 before last week. Market pricing is now in line with the Fed dots, as investors have adjusted to the increasingly hawkish message from Fed officials that are focused solely on slowing growth, and tightening financial conditions, in an effort to bring US inflation down. We see the US Treasury curve as still vulnerable to additional hawkish messaging from the Fed, and a potentially higher-than-anticipated peak in the funds rate versus the FOMC dots. The US consumer is facing a lot of headwinds from higher interest rates and rising food and gasoline prices. However, the latter has fallen 26% from the June 13/2022 peak and is acting as a “tax cut” that also helps reduce US inflation expectations (Chart 6). Consumer confidence measures like the University of Michigan expectations survey have already shown improvement alongside the fall in gas prices, which has boosted real income expectations according to the New York Fed’s Consumer Survey (bottom panel). Even a subtle improvement in consumer confidence due to some easing of inflation expectations can help support a somewhat faster pace of consumer spending at a time of robust labor demand and accelerating wage growth. The Atlanta Fed Wage Tracker is now growing at a year-over-year pace of 5.7%, while the ratio of US job openings to unemployed workers remains near a record high (Chart 7). Fed Chair Powell has noted that the Fed must see significant weakening of the US jobs market for the Fed to consider pausing on its current rate hike path. So far, there is little evidence pointing to a loosening of US labor market conditions that would ease domestically-generated inflation pressures. Chart 6Lower Gas Prices Can Provide A Lift To US Consumer Spending

Lower Gas Prices Can Provide A Lift To US Consumer Spending

Lower Gas Prices Can Provide A Lift To US Consumer Spending

Chart 7A Tight US Labor Market Will Keep The Fed Hawkish

A Tight US Labor Market Will Keep The Fed Hawkish

A Tight US Labor Market Will Keep The Fed Hawkish

Chart 8Stay Underweight US Treasuries

Stay Underweight US Treasuries

Stay Underweight US Treasuries

We expect overall US inflation to decelerate next year on the back of additional slowing of goods inflation, but will likely settle in the 3-4% range in 2023 given stubbornly sticky services inflation and wage growth. The Fed should follow through on its current interest rate projections, with a good chance that rates will need to be pushed up even higher in response to resilient labor market conditions in the first half of 2023. The risk/reward still favors higher US Treasury yields over at least the next 3-6 months, particularly with an improving flow of US data surprises and with bond investor duration positioning now much closer to neutral according to the JPMorgan client survey (Chart 8). Bottom Line: The US remains our highest conviction strategic government bond underweight in the developed markets. Recommended Allocations In Other Countries The path for monetary policy rates outside the US shows a similar profile as in the US, with a “front loading” of rate hikes to mid-2023 followed by modest rate cuts over the subsequent two years (Chart 9). The OIS-implied path for the level of rates is nearly identical in the US, Australia and Canada. On the other hand, markets are discounting much lower of levels of policy rates in Europe and Japan compared to the US, and a considerably higher path for rates in the UK (more on that in the next section). Chart 9Markets Priced For Global 'Front-Loaded' Rate Hikes

Markets Priced For Global 'Front-Loaded' Rate Hikes

Markets Priced For Global 'Front-Loaded' Rate Hikes

We would lean against the US-like pricing of interest rates in Australia and Canada. Based on work we published in a recent Special Report along with our colleagues at BCA Research European Investment Strategy, the neutral real interest rate (“r-star”) is estimated to be deeply negative in Australia and Canada after adjusting for the high level of non-financial debt in those countries (Table 1). That financial fragility makes it much less likely that the Bank of Canada and Reserve Bank of Australia can raise rates as much as the Fed. Table 1Some Big Swings In Our R* Estimates When Including Debt

The Global Bond Bear Market Continues

The Global Bond Bear Market Continues

US-like interest rates would almost certainly trigger a major downturn in house prices and household wealth given the inflated housing values in those two countries – the growth of which is already slowing rapidly in response to rate hikes delivered in 2022. We are maintaining our overweight recommendation on Australian government bonds, while we upgraded Canada to overweight from neutral after last week’s duration downgrade. Chart 10Move To Overweight Japan

Move To Overweight Japan

Move To Overweight Japan

We are also staying overweight on German and French government bonds, as the ECB is unlikely to deliver the full extent of rate increases discounted in the European OIS curve. Our estimated debt-adjusted r-star is also quite negative in the euro area, suggesting that financial fragility issues (due to high government debt in Italy and high corporate debt in France) will likely limit the ECB’s ability to continue with recent chunky rate increases for much longer. In Japan, we continue to view JGBs as an “anti-duration” instrument, given the Bank of Japan’s persistence in maintaining negative interest rates and yield curve control. That makes JGBs a good overweight when global bond yields are rising and a good underweight when global bond yields are falling (Chart 10). Given our decision to reduce our recommended duration exposure to below-benchmark, the logical follow through decision is to upgrade JGBs to overweight. The only remaining country to consider is our view on UK Gilts, which has now become more complicated. Anarchy In The UK The selloff in the UK Gilt market has been stunning in its ferocity. Dating back to last Thursday’s 50bp rate hike by the BoE, the 10-year UK Gilt yield has jumped 120bps and now sits at 4.52%. The increase in yields was identical at the front-end of the Gilt curve, with the 2-year yield jumping 120bps to 4.68%. The surge in longer-term Gilt yields stands out to the rise in bond yields seen outside the UK, as it also incorporates an increase in our estimate of the UK term premium – a move that was not matched in other countries (Chart 11). The rise in Gilt yields was also much more concentrated in real yields compared to inflation expectations (Chart 12), as markets aggressively repriced the path for UK policy rates after the UK government’s announced debt-financed fiscal package, including £45bn of tax cuts. Chart 11Upward Repricing Of Bond Yields Continues

Upward Repricing Of Bond Yields Continues

Upward Repricing Of Bond Yields Continues

Chart 12The Gilt Market Becomes Unhinged

The Gilt Market Becomes Unhinged

The Gilt Market Becomes Unhinged

The UK’s National Institute for Economic And Social Research (NIESR) estimates that the combined impact of the tax cuts and additional spending measures would increase the UK government deficit by a whopping £150bn, or 5% of GDP. The NIESR also estimated that the fiscal measures, including the previously-announced plan for the UK government to cap energy price increases, would result in positive UK GDP growth in the 4th quarter and also lift annual real GDP growth to 2% over 2023-24. The UK government now faces a major credibility issue with markets on its announced fiscal plans. The sheer size of the package, coming at a time when the US economy was already operating at full employment with high inflation, invites a greater than expected monetary policy tightening response from the BoE. The UK OIS curve now forecasts a peak in rates of 6.3% in October 2023, up from the current 2.25%. That would be a massive move in rates in just one year from a central bank that has been relatively gun shy in lifting rates since the 2008 financial crisis, even during the current inflation overshoot. New UK Prime Minister Liz Truss, and her new Chancellor of the Exchequer Kwasi Kwarteng, have both noted they would prefer a mix of looser fiscal policy (aimed at boosting the supply side of the economy to lift potential growth) with tighter monetary policy that would prevent asset bubbles and inflation overshoots. While there is certainly merit in any plan designed to boost medium-term growth by lifting anemic UK productivity through supply-side reforms, the timing of the announcement could not have been worse. Just one day earlier, the BoE announced a plan to go forward with the sale of Gilts from its balance sheet accumulated during quantitative easing. The Truss government needs to find buyers for all the Gilts that must be issued to pay for the tax cuts and stimulus, but the BoE will not be one of them. In the end, however, the BoE’s expected path for interest rates matters more than the increase in Gilt supply in determining the level of Gilt yields and the slope of the Gilt curve. The NIESR estimates that the UK public debt/GDP ratio will rise to 92% by 2024-25, versus its pre-budget forecast of 88%. While that is a meaningful increase, the correlation between the debt/GDP ratio and the slope of the Gilt curve has been negative for the past few years (Chart 13, top panel). The stronger relationship is between the slope of the curve and the level of the BoE base rate (bottom panel), which is pointing to an inversion of the 2-year/30-year curve if the BoE follows market pricing and lifts rates to 6%. Our view dating back to the early summer was that a low neutral interest rate would prevent the BoE from lifting rates as much as markets were discounting without causing a deep recession, lower inflation and, eventually, a quick reversal of rate hikes. The huge UK fiscal stimulus package changes that calculus, as the nominal neutral rate that will be needed to bring UK inflation back to target is likely now much higher. We have always believed that when a thesis underlying an investment recommendation is challenged by new information, it is best to adjust the recommendation to reflect the new facts. Thus, this week, we are tactically downgrading UK Gilts to underweight in our model bond portfolio framework. We still see a significant medium-term opportunity to go overweight Gilts, as UK policy rates pushing into the 4-6% range are not sustainable. However, the BoE will likely have no choice to begin lifting rates at a much more aggressive pace to restore UK policy credibility, especially with the British pound under immense selling pressure (Chart 14). Despite rumors of an inter-meeting rate hike by the BoE this week to try and support the pound, that is likely too risky a step for the BoE to take as it would invite a battle with investors and currency speculators. Such a battle would be difficult to win without a more credible and market-friendly medium-term fiscal policy from the Truss government. Chart 13The BoE Matters More Than Debt Levels For Gilts

The BoE Matters More Than Debt Levels For Gilts

The BoE Matters More Than Debt Levels For Gilts

Chart 14Tactically Move To Underweight UK Gilts

Tactically Move To Underweight UK Gilts

Tactically Move To Underweight UK Gilts

Bottom Line: We will review our UK Gilt stance once there are more clear signals of stability in the pound, but for now, we will step aside and limit our recommended exposure to Gilts – even after the huge selloff seen to date, which likely has more to go. Summarizing All The Changes In Our Model Bond Portfolio All the changes to our recommended duration exposure and country allocations after the past week, including the new weightings in our model bond portfolio, are shown in the tables on pages 14-16. To summarize: We moved the overall recommended global duration exposure to below-benchmark, and shifted the model bond portfolio duration to 0.9 years below that of the custom benchmark index. We increased the size of the US Treasury underweight, and moved Canada and Japan to overweight. We moved the UK to underweight, on top of the reduction in UK duration exposure that was part of last week’s move to reduce overall portfolio duration. We are also cutting exposure to UK investment grade corporates to underweight, as part of an overall move to reduce UK risk in the portfolio. We slightly increased the overweight in Germany. In next week’s report, we will present the quarterly performance review of our model bond portfolio and, more importantly, we will present out scenario-based return expectations after all the changes made this week. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com GFIS Model Bond Portfolio Recommended Positioning Active Duration Contribution: GFIS Recommended Portfolio Vs. Custom Performance Benchmark

The Global Bond Bear Market Continues

The Global Bond Bear Market Continues

The GFIS Recommended Portfolio Vs. The Custom Benchmark Index Global Fixed Income - Strategic Recommendations* Cyclical Recommendations (6-18 Months)

The Global Bond Bear Market Continues

The Global Bond Bear Market Continues

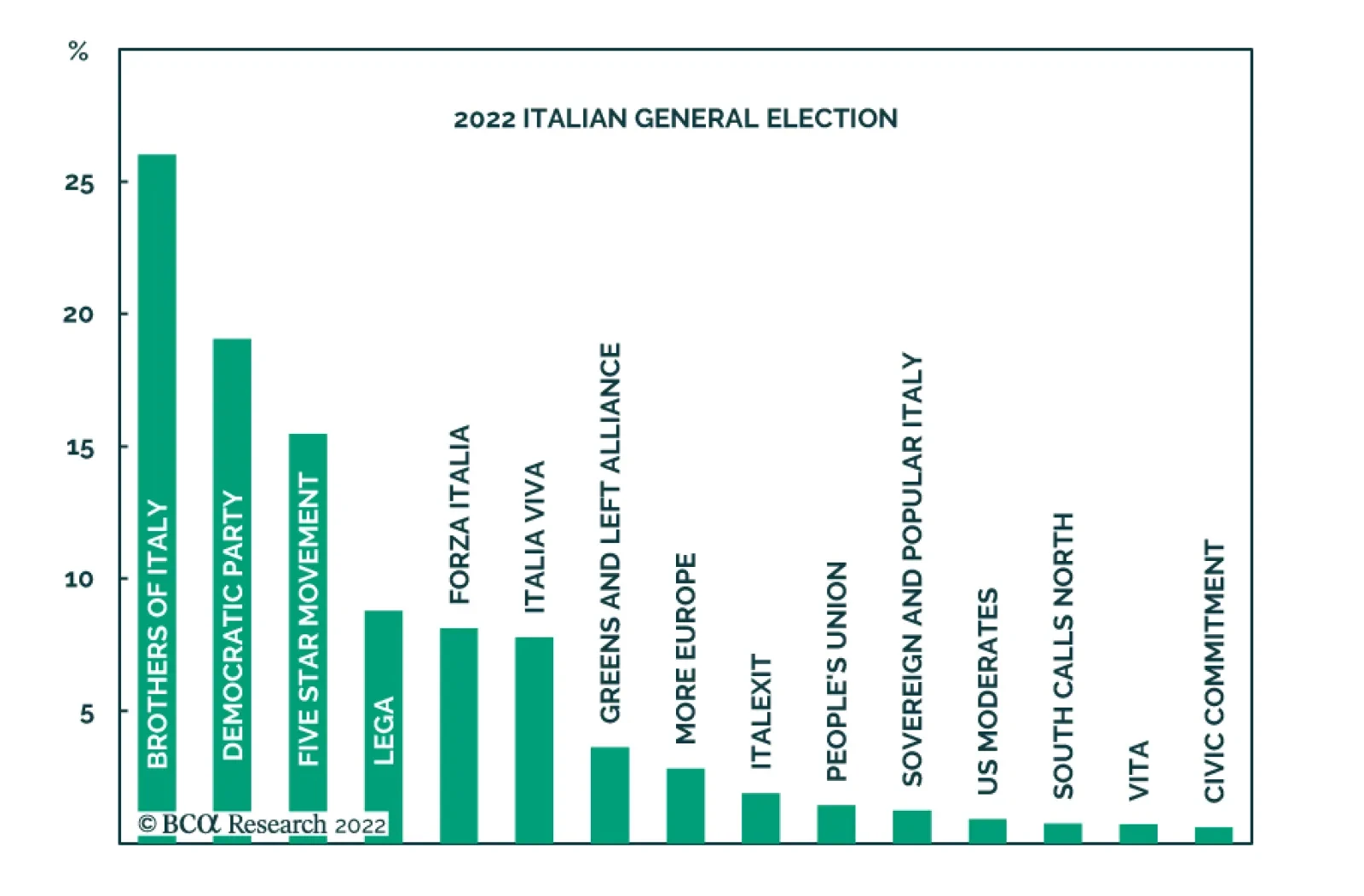

Italy’s right-wing coalition led by Giorgia Meloni of the far-right Brothers of Italy party –which also includes the League and Forza Italia – secured 44% of the vote in Sunday’s general election. Italian government bond yields rose 21bps on Monday following…

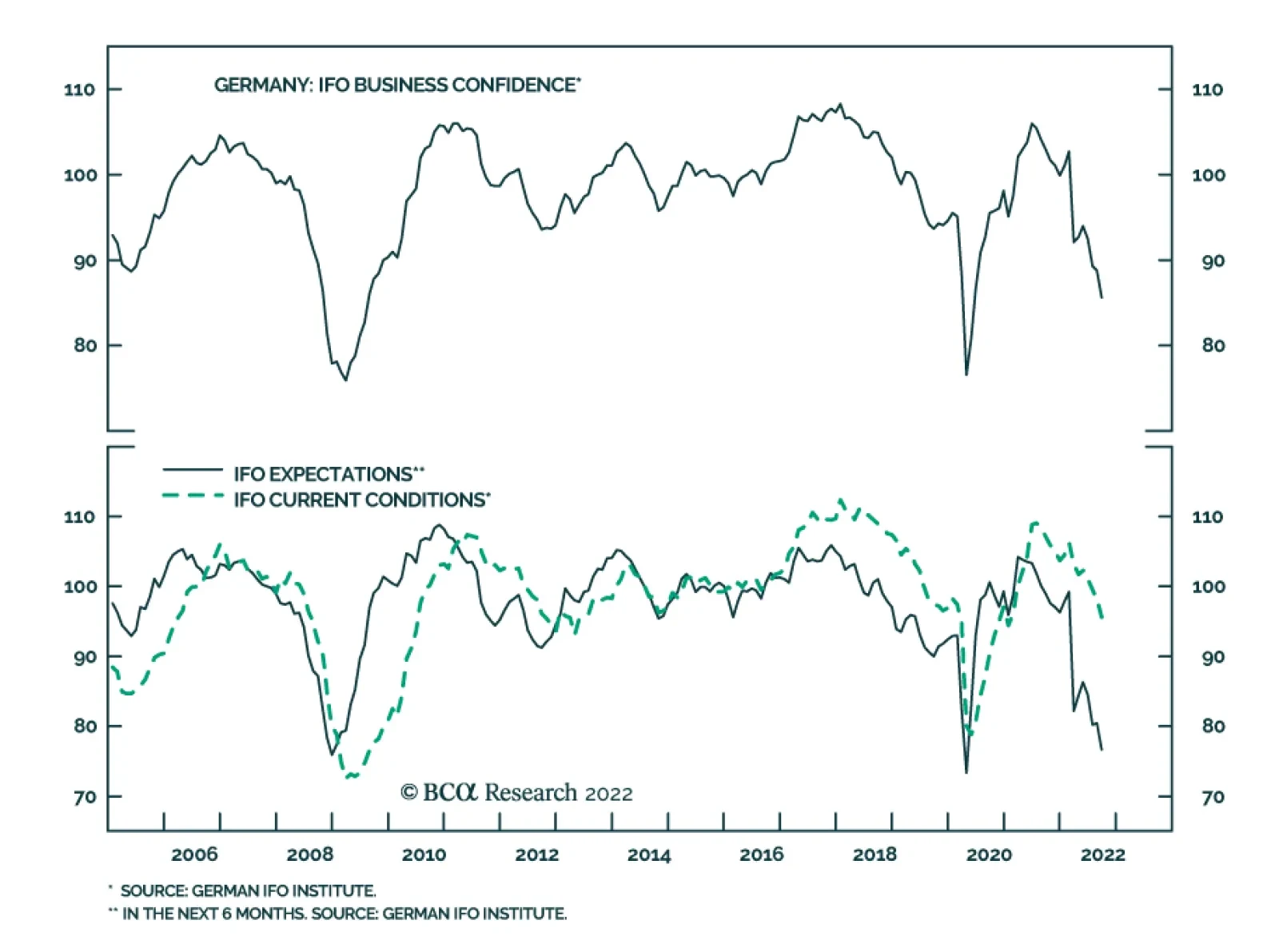

The German Ifo Business Climate Index weakened further in September, sliding from 88.6 to 84.3, below expectations of a milder deterioration to 87.0. The current situation and expectations sub-components ticked down 3.0 points and 5.3 points, respectively,…

Sterling collapsed to an all-time low in intra-day trading on Monday. The weakness follows UK Chancellor Kwasi Kwarteng’s Friday mini-budget announcement and weekend comments that more tax cuts are coming. The Bank of England’s Monday pledge that “the MPC…

According to BCA Research’s European Investment Strategy service for investors concerned with the left-tail risk in European equities, European credit offers a credible alternative in the near term. This asset class is also attractive relative to European…

Executive Summary What To Do With The Euro?

What To Do With The Euro?

What To Do With The Euro?

The outlook for European assets is uniquely muddled. European energy prices will remain elevated, but the worst of the adjustment is already behind us. The global economy is teetering on the edge of a recession and weak global growth is historically very negative for European assets. However, European valuations and earnings forecasts already discount an extremely severe outcome for global growth. A hawkish Fed should support the dollar, but investors increasingly realize foreign central banks are fighting inflation equally aggressively. The dollar already anticipates a global recession. Meantime, European credit offers a large spread pickup over sovereigns and even appears as a decent alternative to equities. Within a credit portfolio, we adopt a more cautious approach towards European investment grade bonds (IG) relative to their US counterpart. Instead, we recommend favoring UK IG over Euro Area IG as well as Swedish IG relative to US IG. Recommendations INCEPTION DATE RETURN SINCE INCEPTION (%) COMMENT Set a stop buy at EUR/USD 0.9650 with a stop-loss at 0.9400 9/26/2022 Bottom Line: Investors should maintain a modest long position in equities in European portfolios, with a preference for defensive stocks over cyclicals. The conditions are falling in place to buy the euro tentatively. Following the hawkishness that transpired from the Fed press conference and revised forecasts last week, EUR/USD plunged below 0.99 and hit a 20-year low. Moreover, President Vladimir Putin’s announcement of a broader mobilization of the Russian army is stoking fears that the Ukrainian conflict will only be prolonged. The prospects of a lengthier war and greater energy market shock are raising further worries for Europe’s growth outlook, which weighs on European asset prices, notably the euro and the pound. The odds of a global financial accident are on the rise. Global central banks have joined the Fed and are relentlessly tightening global monetary and financial conditions. Moreover, the surging dollar is adding to global risks by raising the cost of capital around the world. This is a very fragile situation and the odds of a global recession have jumped significantly. Against this backdrop, investors should continue to overweight defensive equities at the expense of cyclical stocks. The euro also has more downside, but we are issuing a tentative stop-buy at EUR/USD 0.9650 with a stop at 0.9400. Credit remains a safer alternative to European stocks. The Evolving European Energy Backdrop Chart 1All About The Gas

All About The Gas

All About The Gas