Financial Markets

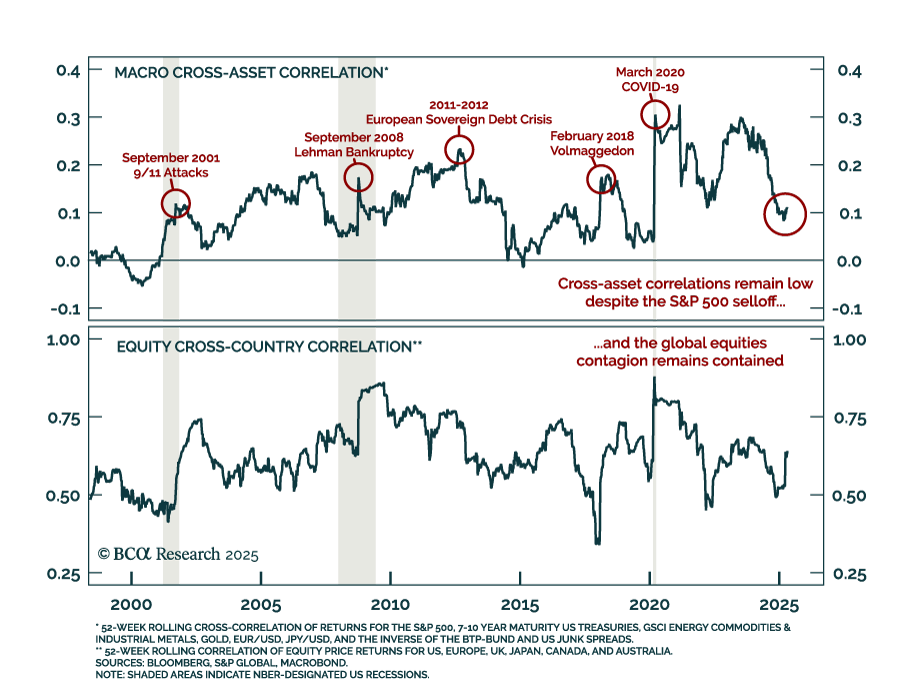

Cross-asset signals remain distorted by policy developments, but we expect the US dollar to rebound tactically. More than observable fundamentals, policy headlines have been driving cross-asset movements. Traditional leading indicators have had limited market…

Markets no longer trade on soft-data fears; they now wait for hard-data proof, keeping us defensive on risk assets. Friday’s payroll beat highlighted the soft-hard split: Surveys flag weakness, but actual jobs hold up. In past cycles, markets priced…

Our Global Asset Allocation strategists recommend staying defensively positioned. They remain underweight equities and the US specifically, while maintaining an overweight in fixed income yet downgrading duration to neutral. Uncertainty around US governance…

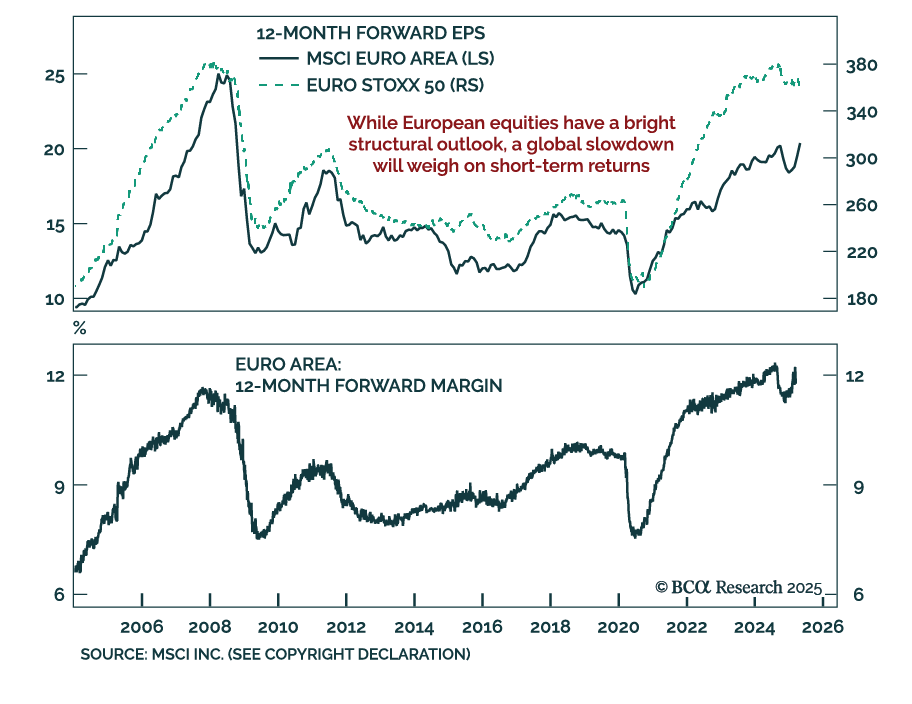

Germany's political transition supports long-term equity upside, but near-term growth risks justify caution. Friedrich Merz was narrowly elected Chancellor on Tuesday, but his fragile coalition and his decision to suspend the debt brake could lead to internal…

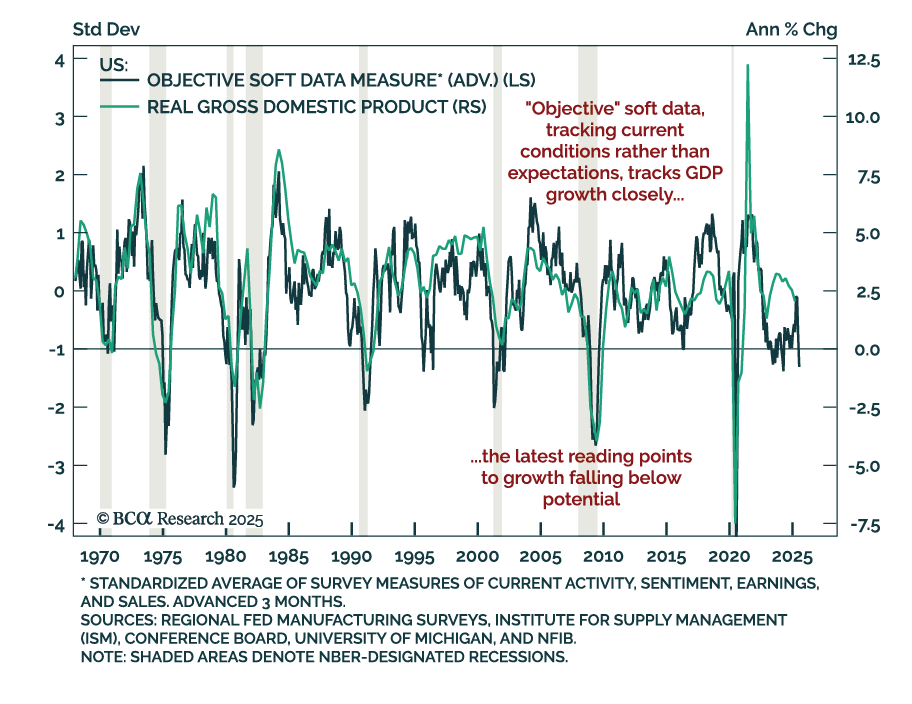

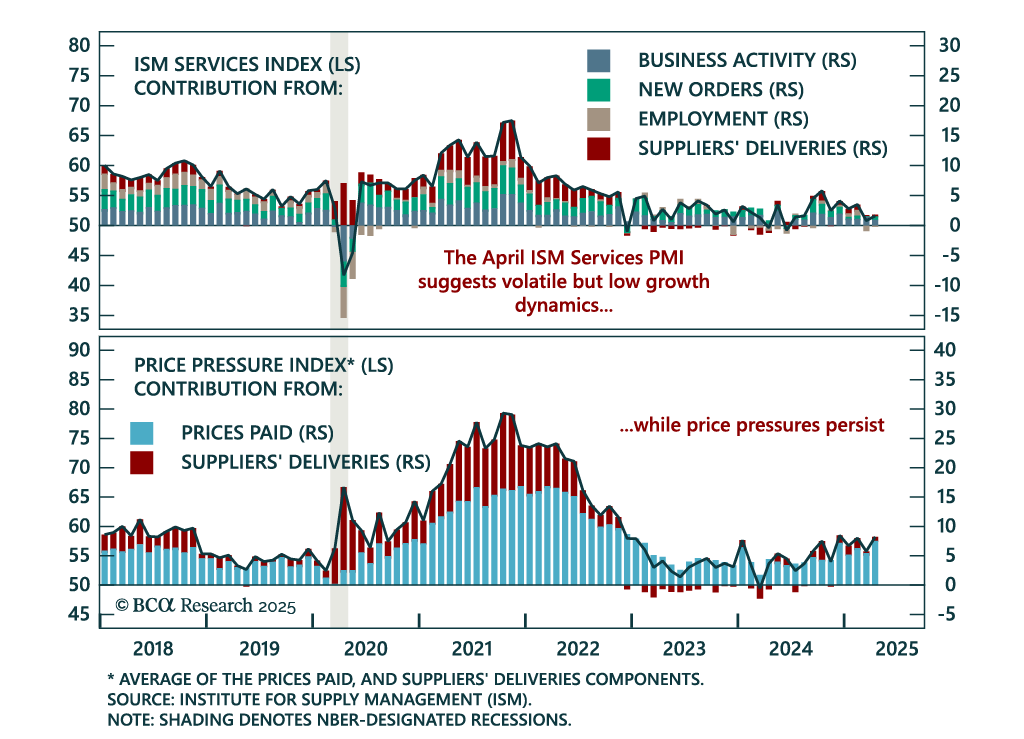

April’s ISM Services upside surprise does not shift our defensive stance, as its components show mixed momentum and rising price pressures. The headline index beat estimates, rising to 51.6 from 50.8. Business activity and new orders picked up, yet the…

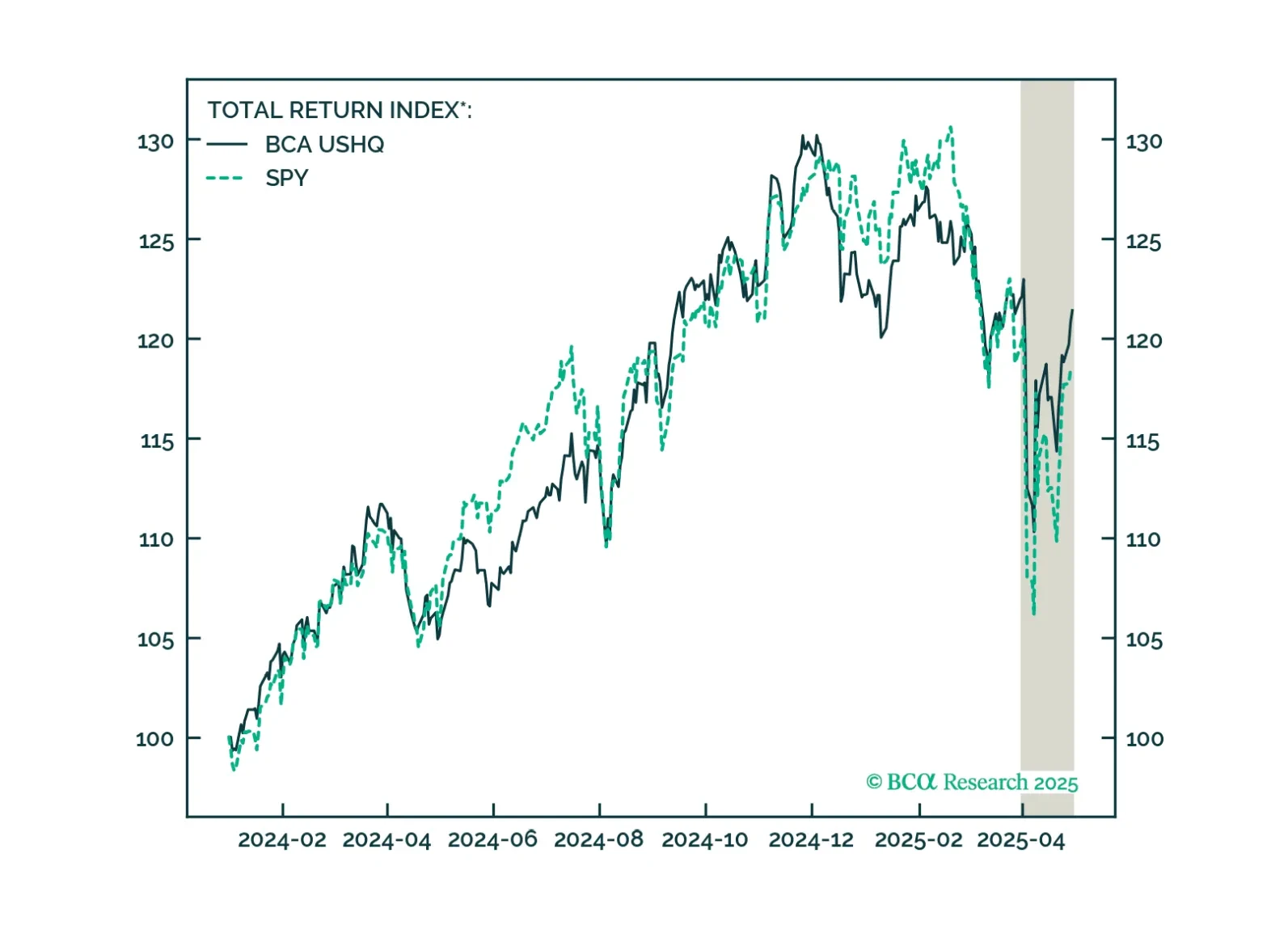

The US High Quality (USHQ) portfolio outperformed on the margin through April, returning -0.6%, whilst its SPY benchmark returned -1.2%. On a trailing three-month basis, performance remains robust vs. benchmark, with USHQ generating +230bps of excess return. Volatility and drawdown are lower too.

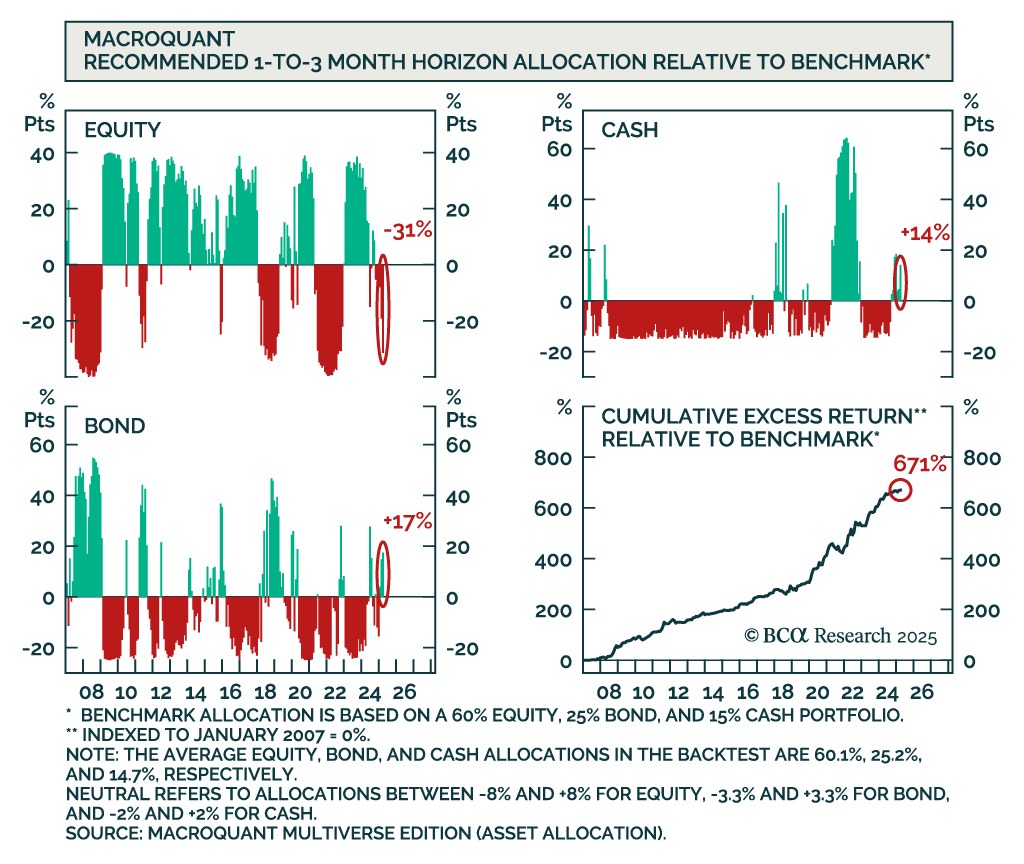

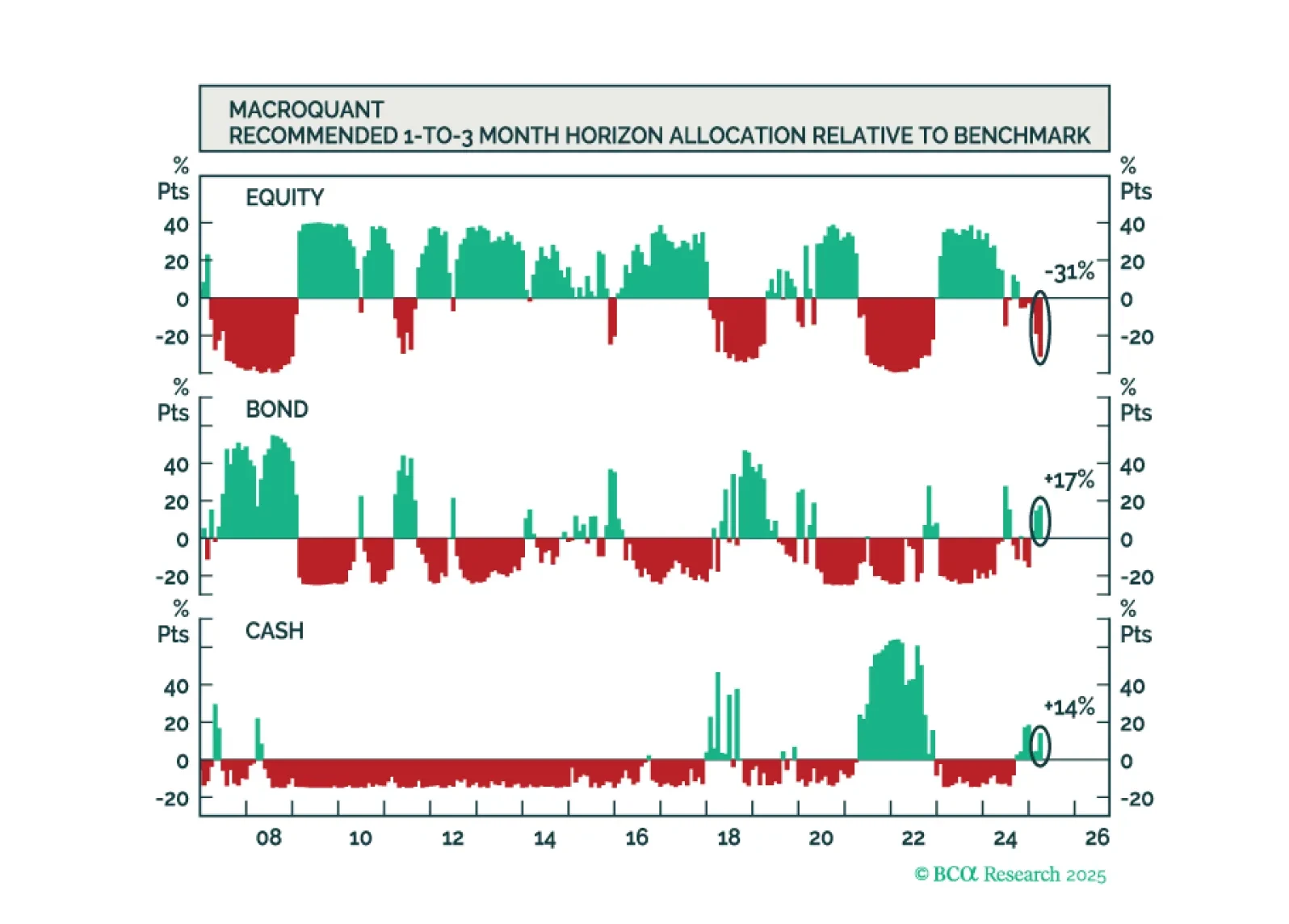

BCA’s MacroQuant model sees downside risks to US growth and upside risks to inflation. Our Chart Of The Week comes from Chanhyuck Lee in our Global Investment Strategy team. The model tracks hundreds of leading indicators and applies the economic and…

MacroQuant sees the risks to US growth as being to the downside and the risks to inflation as being to the upside. Such a stagflationary brew justifies an underweight on stocks.

MacroQuant sees the risks to US growth as being to the downside and the risks to inflation as being to the upside. Such a stagflationary brew justifies an underweight on stocks.

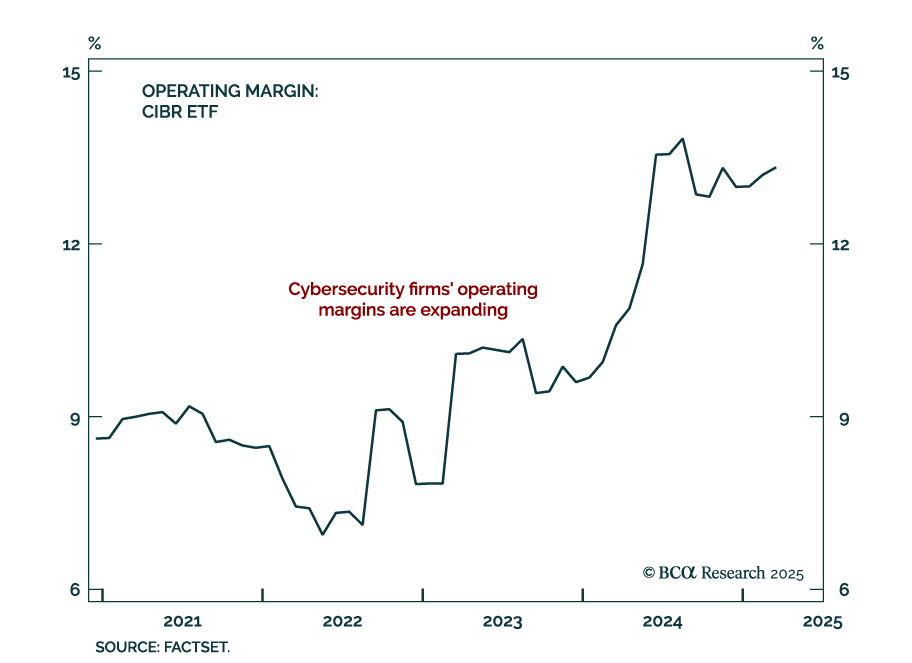

BCA’s US Equity strategists recommend building or adding to cybersecurity positions. The industry remains a strategic long-term theme with improving fundamentals and reduced valuation risk. The sector’s defensive characteristics, domestic focus, and…