Financial Markets

BCA Research is proud to announce a new feature to help clients get the most out of our research: an Executive Summary cover page on each of the BCA Research Reports. We created these summaries to help you quickly capture the main points of each report through an at-a-glance read of key insights, chart of the day, investment recommendations and a bottom line. For a deeper analysis, you may refer to the full BCA Research Report. Executive Summary The Software and Services Industry is undergoing a fundamental transformation in its business model catalyzed by a momentous migration of software applications to the cloud and broad-based digitization of the economy. This shift is accompanied by displacement of the traditional on-prem license and support model with a more lucrative cloud-based subscription model. While on-prem software sales are contracting, cloud revenue is growing in double digits. As a result, the industry enjoys spectacular margins and earnings growth. Its earnings have also proven to be resilient across the business cycle because software and IT services increase companies’ productivity in good times and bad. Rising rates are a headwind, but a temporary one. Margins Will Continue To Expand

Margins Are To Continue Expanding

Margins Are To Continue Expanding

Bottom Line: The Software and Services industry group is an all-weather industry with resilient earnings and strong growth throughout the business cycle. It is also in the epicenter of technological innovation: Migration to the cloud and digital transformation enhance the industry’s growth and profitability. We continue recommending both a tactical and a structural overweight. Feature Performance Technology stocks found themselves in the eye of this month’s market rout. After falling 19% from its peak, the NASDAQ is now firmly in correction territory. The Technology sector is down 11%, while the Software and Services industry group is down 10% (Chart 1). In the “Are We There Yet?” report published last week, we posited that it is not yet the right time to bottom fish: While the Technology sector appears oversold, macroeconomic headwinds from the imminent monetary tightening and a slowdown in demand for technology goods and services may prolong the pain. The interplay of valuations and fundamentals for the sector is not yet favorable. While we are underweight the Technology sector, thanks to our underweight positions in Semiconductors and Hardware and Equipment, we remain overweight Software and Services (S&S). In this report, we will conduct a “deep dive” into S&S and reevaluate our positioning (Table 1). Although S&S is down more than 10% from the peak, it has outperformed the S&P 500 by 88% since 2011 (Chart 2). The million-dollar question we will try to answer is whether this outperformance continues over the tactical and structural time horizons. Chart 1Software And Services Outperformed Other Tech Industries

Software And Services: On The Seventh Cloud

Software And Services: On The Seventh Cloud

Chart 2S&S Outperformed The S&P 500 By 88% Over The Past 10 Years

S&S Outperformed The S&P 500 By 88% Over The Past 10 Years

S&S Outperformed The S&P 500 By 88% Over The Past 10 Years

Table 1Performance

Software And Services: On The Seventh Cloud

Software And Services: On The Seventh Cloud

Sneak Preview: We maintain our overweight of the Software and Services sector thanks to positive market trends, the all-weather nature of the industry, and resilient earnings. Industry Group Composition The Software And Services Industry Group Is Top Heavy The S&P 500 Software and Services industry group is the largest in the Technology sector and is 48% of the sector market cap. The industry group is split between Software, which is about two-thirds of its market cap, and IT Services, which is one-third (Chart 3). Just like other technology industries, it is dominated by one of the FAANGs+M, Microsoft in this case, which makes up 42% of the industry group index weight. The top 10 constituents out of 36 comprise 80% of the industry’s weight (Table 2). During the current pullback, the S&S industry group has fallen by more than 10%, cushioned by the performance of its larger players. But this masks the pain of the smaller and less profitable constituents, which have fallen by more than 30% (Chart 4). Chart 3Software Dwarfs IT Services

Software And Services: On The Seventh Cloud

Software And Services: On The Seventh Cloud

Chart 4Some Smaller Constituents Have Fallen More Than 15% YTD

Software And Services: On The Seventh Cloud

Software And Services: On The Seventh Cloud

Table 2S&S Industry Is Dominated By A Handful Of Successful Companies

Software And Services: On The Seventh Cloud

Software And Services: On The Seventh Cloud

However, market dominance runs much deeper than just market capitalization: Microsoft, Adobe, Salesforce, and Oracle account for 87% of the Software Industry revenue, while Visa, Mastercard, Accenture, and PayPal generate 42% of the IT Services industry revenue. Larger industry players are also more profitable thanks to the high operating leverage the industry enjoys. Clearly, just a few companies drive sales and earnings growth, valuations, and performance. On the bright side, these are some of the most successful US technology companies, and their size is their competitive moat. We believe that the industry group is in “good hands.” Key Trends Cloud Migration Following the success of offshoring the US manufacturing base to China that allowed corporations to reduce labor costs, companies are now experimenting with outsourcing other key infrastructure elements. This time, however, the migration is happening to digital cloud platforms. Instead of investing in pricey servers and other hardware assets, corporations have the choice of going with Software-as-a-Service (SaaS), Platform-as-a-Service (PaaS), or Infrastructure-as-a-Service (IaaS) solutions offered by the tech titans. Not only are cloud solutions more cost-effective, but they also offer the convenience and flexibility to scale corporate hardware infrastructure by simply purchasing more or less computational power. COVID-19 lockdowns and the migration of the white-collar workforce towards remote work have motivated companies to transition their technology and operations to the cloud, and have acted as a catalyst for “digital offshoring.” Digital Transformation Digital transformation is in many ways similar to cloud migration. Essentially, it represents broader software penetration into the US economy. Whether it is a manufacturing production or customer relationship management process, wider adoption of software allows for a more efficient business solution via automation and process optimization. Airbnb and Uber are the poster children of digital transformation. While some industries have already undergone digital transformation, there are notable areas which lag behind. For instance, banks’ failure to modernize their digital infrastructure to speed up transactions and to increase overall user convenience has arguably led to the development of the crypto space as an alternative to the slow-evolving traditional financial institutions. The broader implication is that there are still major sectors in the economy that are yet to ramp up automation and increase efficiencies via digital transformation, meaning that there is a healthy demand pipeline for the tech companies. Types Of Software And Services Companies Software: Migration To The Cloud Is A Key Driver Of Growth In the past, classifying software companies was a relatively straightforward exercise: They were divided into system software vs. application software. System software included such categories as operating systems for PCs, and other hardware and database software. Application software covered Enterprise Resource Planning (ERP), Customer Relationship Management (CRM), Communications and Collaborations, etc. However, over time, the industry landscape has changed, first by the mergers that blurred the distinction across these lines, and lately, thanks to ubiquitous migration to the cloud model and digitization of the economy. Therefore, it is most practical to classify software companies by their type of business model, i.e., legacy license and support model, or cloud-based, or hybrid. Pure cloud-first: These companies derive 100% of their sales from the cloud model – Salesforce.com (CRM), ServiceNow (Now), and Twilio (TWLO) are among the biggest winners. Cloud/license hybrid: These are companies that derive 50%+ of their sales from the cloud, such as Microsoft (MSFT), Atlassian (TEAM), Autodesk (ADSK), and Adobe (ADBE). Legacy license and support model (aka On-Premises): Constellation Software (CSU), Citrix Systems (CTSX) – these companies are likely to struggle to grow organically. Types Of Cloud Application Services The cloud-based business model in turn can be classified under three different types of service: Software-as-a-Service (SaaS), Infrastructure-as-a-Service (IaaS), or Platform-as-a-Service (PaaS). Software-as-a-Service: Customers configure and access a web-based application operated by a SaaS provider over the internet. Salesforce.com, Workday (DAY), ServiceNow, and Oracle are some of the most established players. Infrastructure-as-a-Service: This service gives customers access to virtual storage and servers over the internet, enabling them to develop and run any application just as if it were running in their own data center. Amazon’s AWS, Microsoft’s Azure, and IBM are the key competitors in this space. Platform-as-a-Service: This service occupies a middle ground between SaaS and IaaS, i.e. between a full-fledged app that can be used “out-of-the-box” and a “raw server and storage” instance, making the customer responsible for installing and configuring its own “full stack.” PaaS offerings tend to be less standardized. Salesforce.com, Microsoft, and Oracle are the leaders. IDC projects the continued strength of this segment and expects it to grow at an annualized rate of 29.7% over the next five years. The following table from Microsoft presents a perfect explanation of the different software service models (Table 3). Table 3Differences In Cloud Computing Service Models

Software And Services: On The Seventh Cloud

Software And Services: On The Seventh Cloud

License And Support Vs. Cloud Subscription Model Growth Rates Broad-based migration to the cloud is shifting the industry’s revenue composition, with accelerating bifurcation between cloud and on-prem models: Cloud subscription revenue is replacing the traditional license and support model. As a result, legacy on-prem revenue has recently been contracting, and once the last of the legacy enterprise applications are retired, it will be fully replaced by cloud revenue. According to estimates by CFRA,1 the software industry grew by 4% in 2021, with a 22% year-on-year increase in cloud subscription revenue, which now constitutes 37% of total industry revenue, and a 3% decline in traditional software revenue. The surge in cloud growth is likely to continue, thanks to the accelerating pace of digital transformation. This trend is also promulgated by some of the largest players, such as Microsoft, whose cloud subscription revenue now constitutes more than half of the overall revenue and is an engine of growth in the software space. Strong cloud revenue growth is not just a function of recruiting new users but is also supported by the proliferation of new cloud apps and upgrades to the existing ones. Importantly, the cloud subscription model is also more profitable than the license model, whose EBITDA margins rarely exceed 40%. Cloud-based services take longer to become profitable but have much higher operating leverage: Once profitable, cloud and hybrid companies often have operating margins around 50-60%. Software is one of the most resilient technology industries, performing equally well in a growing economy and during downturns: Subscription pricing is sticky, and switching costs are high. As a result, companies, which derive a large share of their revenue from the cloud, have stable and predictable sales. Once clients are onboarded, cloud providers may also be able to exercise their pricing power. IT Services IT services is a smaller segment of the Software and Services industry group and is a hodge-podge of different companies that provide a wide range of services from IT consulting to FinTech. The following is a brief description of the key categories: IT Consulting: The S&P 500 IT Consulting companies are Accenture, Gartner, and Cognizant. Companies offer Professional advice in IT, management, HR, logistics, and many others. Since the pandemic, these companies’ key focus is on assisting their clients with digital transformation and improving companies’ operations. This industry is one of the key beneficiaries of accelerated migration to the cloud and has enjoyed exponential growth over the past decade. Its revenue stream is highly resilient, as even during economic downturns, clients are seeking advice on the best ways to navigate an uncertain market environment. Outsourcing: Companies such as ADP and Paychex provide HR and business services solutions for mid-sized and small companies. Their services cover payroll, benefits, retirement, and insurance services. This industry has been growing its sales and profits at a healthy clip over the past few years. Now it is focused on modernizing itself by moving its own operations to the cloud and deploying Artificial Intelligence to improve operations. These companies are also undergoing digital transformation and are moving towards the SaaS model. Financial Transaction Services: This is a FinTech industry that includes card and payment processors, such as Visa, Mastercard, and PayPal, and each of these players operates their own proprietary payment networks. Digital payments and the wide acceptance of e-commerce drive this space. Lately, these companies have been at the forefront of the adoption of digital currencies as viable payment options. Payment companies are among the earliest adopters of the cloud, and their business model is best described as Transaction-processing-as-a-service. These are highly profitable companies that consistently generate an operating margin above 60%. Key Industry Drivers Software Enhances Productivity And Improves Profitability Broadly speaking, the Software and Services industry group is considered a defensive holding owing to the resiliency of its earnings (Chart 5). Software enhances productivity: During economic downturns, it helps reduce costs, and during expansions, it helps overcome capacity constraints and labor shortages. While pandemic labor shortages and lockdowns produced a spike in productivity, more recently it has been falling, which has warranted a year-over-year increase in software investment (Chart 6). Chart 5S&S Earnings Are Resilient Across The Business Cycle

S&S Earnings Are Resilient Across The Business Cycle

S&S Earnings Are Resilient Across The Business Cycle

Chart 6Investing In Software Improves Productivity

Investing In Software Improves Productivity

Investing In Software Improves Productivity

Further, both labor shortages and rising wages are prompting companies to redesign their operations to contain costs and preserve margins. To do so, many are accelerating investments in Capex and automation, much of which is achieved through investment in software and IT services, replacing both labor and capital. According to CFRA, “software is no longer used to manage a means of production, but rather IS means of production .” Software-related Capex is not only garnering a larger slice of tech spending budgets but also of the overall Capex pie (Chart 7). Chart 7Share Of Software In Overall Capex Has Been Rising Steadily

Share Of Software In Overall Capex Has Been Rising Steadily

Share Of Software In Overall Capex Has Been Rising Steadily

Macroeconomic Backdrop Imminent Rate Hikes Tighter monetary policy and runaway inflation are at the fore of investors’ minds and, arguably, a cause of the current market rout. Software stocks have outperformed the other long-duration technology stocks. To gauge the reaction of S&S to the upcoming rate hike, we have repeated an exercise we conducted for the Technology sector last week – historical performance of the industry six months before and after the first rate hike (Chart 8). Clearly, industry returns fall two to three months before the first rate hike, but eventually recover once a new monetary regime is priced in. The year-to-date correction of the software stocks is textbook behavior. Chart 8S&S Underperforms Before The First Rate Hike

Software And Services: On The Seventh Cloud

Software And Services: On The Seventh Cloud

Software And Services Is A Global Industry – Beware Of A Strong Dollar The Technology sector is one of the most global sectors in the S&P 500 and derives 40% of sales from abroad; similarly, Software and Services has a broad international footprint. As US rates trend higher, and the interest rate differential favors the US vs. other countries, the USD is likely to appreciate further. With a stronger dollar, products of US software firms are more expensive to foreigners, which may have a dampening effect on demand. The US firms’ profitability has also been hit by an unfavorable translation from foreign currency back to the USD. Historically, the path of the dollar and the returns of S&S were inversely correlated (Chart 9). Chart 9Historically, Stronger Dollar Has Been A Headwind For The Industry

Historically, Stronger Dollar Has Been A Headwind For The Industry

Historically, Stronger Dollar Has Been A Headwind For The Industry

The redeeming grace is that, as we mentioned before, software subscription revenue is sticky, and switching costs for customers are high. As such, we expect the adverse effect on demand to be minor. Fundamentals Sales Growth According to Grandview Research , the business software and services market is expected to grow at a compound annualized rate of 11.3% from 2021 to 2028. This strong growth is underpinned by the robust pace of enterprise application cloud migration and digital transformation, which see no end in sight. The street expects the Software and Services industry to grow on par with the Technology sector at just under 20% over the next 12 months, and growth is slowing off high levels. The pandemic has shifted forward some of the spending on software, as companies rushed to adjust to remote work. However, the industry continues to grow at a healthy clip (Chart 10). Chart 10Sales Growth Is Slowing

Sales Growth Is Slowing

Sales Growth Is Slowing

Labor Costs Are Contained For Now The S&S companies first and foremost rely on the talent and ingenuity of their workforce to deliver cutting-edge technological solutions. Wages are one of the largest expenses in the industry. Recent increases in salaries accompanied by labor shortages and “the great resignation” are bound to cut into the margins of these companies. So far, software and services companies have been able to counter the trend (Chart 11) by deploying creative solutions, offering their employees a wide range of perks, and throwing their net wide in search of talent by offering remote work. Chart 11Industry Labor Costs Have Been Contained

Industry Labor Costs Have Been Contained

Industry Labor Costs Have Been Contained

Resilient Earnings Growth For the reasons discussed above, S&S earnings growth is remarkably resilient and stable throughout the business cycle (Chart 12). Currently, earnings expectations of S&S over the next 12 months exceed growth expectations for both the Technology sector and the S&P 500. Over the next 12 months, S&S earnings are expected to grow at 14% compared to 8.6% for the S&P 500 (Table 4). Chart 12S&S EPS Growth Bests The Tech Sector And The S&P 500

S&S EPS Growth Bests The Tech Sector And The S&P 500

S&S EPS Growth Bests The Tech Sector And The S&P 500

Table 4Earnings Growth Vs. Valuations

Software And Services: On The Seventh Cloud

Software And Services: On The Seventh Cloud

Despite the slowdown in sales growth and the pick-up in labor costs, EBITDA margins have exceeded the previous peak, and are projected to trend higher towards 40% over the course of the year (Chart 13). Expecting a growth slowdown, analysts have been revising earnings expectations down for S&S companies, but by now the downgrading process has run its course, and the bar is set low (Chart 14). Chart 13Margins Will Continue To Expand

Margins Will Continue To Expand

Margins Will Continue To Expand

Chart 14Downgrades Are Bottoming

Downgrades Are Bottoming

Downgrades Are Bottoming

Valuations Since the S&S industry group’s earnings are expected to grow faster than the earnings of the Tech sector and the S&P 500, it is not surprising that it trades with a 44% premium to the S&P 500 on a forward earnings basis – a steep mark-up. The current correction has taken some froth off the industry’s valuations , with multiples contracting by 3.9 points. Even after the correction, the sector appears overvalued (Chart 15). Adjusting for expected 12-month EPS growth, S&S appears more attractively valued and trades with a discount both to tech and the broad market (Table 4). It is also important to note that the industry group is home to a plethora of quite a few smaller companies, which tend to be more expensive and more volatile: Chart 16 plots companies’ forward earnings multiples against their weight in the industry group. Chart 15Valuations Are Still Dear...

Valuations Are Still Dear...

Valuations Are Still Dear...

Chart 16Significant Valuation Dispersion Among The Constituents

Software And Services: On The Seventh Cloud

Software And Services: On The Seventh Cloud

Technicals Recently, the BCA Technical Indicator has moved into the oversold territory, indicating investor capitulation. This means that this bar is cleared, and from a technical standpoint alone, Software and Services is a buy (Chart 17). Chart 17... But Technicals Indicate That S&S Is Oversold

... But Technicals Indicate That S&S Is Oversold

... But Technicals Indicate That S&S Is Oversold

Investment Implications We are both tactically and structurally bullish on the Software and Services industry group. Tactically Bullish The Software and Services industry group is an all-weather industry with an unprecedented combination of both earnings resiliency and strong growth throughout the business cycle. It is also undergoing a fundamental transformation in its business model catalyzed by a ubiquitous shift in software applications to the cloud, accompanied by displacement of the traditional on-prem license and support model with a more lucrative subscription model. The industry is expected to grow earnings in double digits and expand margins, unhindered by rising labor costs. Rising rates are certainly a headwind, but hopefully a temporary one. Froth has come off valuations, and a new monetary regime is gradually getting priced in. According to the technical indicator, the sector is oversold. On balance, we have a positive outlook on the industry group (Table 5) and maintain our overweight position. Table 5Software And Services Scorecard

Software And Services: On The Seventh Cloud

Software And Services: On The Seventh Cloud

Structurally Bullish Our long-held belief is that the broader push to the cloud, augmented reality, AI, cybersecurity, and autonomous driving, which are all software dependent, are not fads but are here to stay. Software and Services are at the epicenter of technological innovation and are home to some of the best American companies. Irene Tunkel Chief Strategist, US Equity Strategy irene.tunkel@bcaresearch.com Footnotes 1 CFRA, Industry Surveys, Software, July 2021 Recommended Allocation

Highlights The selloff in equities since the start of the year marks a long overdue correction rather than the start of a bear market. Stocks often suffer a period of indigestion when bond yields rise suddenly, but usually bounce back as long as yields do not move into economically restrictive territory. BCA’s bond strategists expect the 10-year yield to rise to 2%-to-2.25% by the end of the year, which is well below the level that could trigger a recession. While valuations in the US remain stretched, they are much more favorable abroad. Investors should overweight non-US markets, value stocks, and small caps in 2022. Go long homebuilders versus the S&P 500. US homebuilders are trading at only 6.5-times forward earnings and will benefit from tight housing supply conditions and a moderation in input costs. FAQ On Recent Market Action The selloff in stocks since the start of the year has garnered a lot of attention. In this week’s report, we address some of the key questions clients are asking. Q: What do you see as the main reasons for the equity selloff? A: At the start of the year, the S&P 500 had gone 61 straight weeks without experiencing a 6% drawdown, the third longest stretch over the past two decades. Stocks were ripe for a pullback. The backup in bond yields provided a catalyst for the sellers to come out. Not surprisingly, growth stocks fell hardest, as they are most vulnerable to changes in the long-term discount rate. At last count, the S&P 500 Growth index was down 13.7% YTD, compared to 4.1% for the Value index. Our research has found that stocks often suffer a period of indigestion when bond yields rise suddenly, but usually bounce back as long as yields do not move into economically restrictive territory (Table 1). BCA’s bond strategists expect the 10-year yield to rise to 2%-to-2.25% by the end of the year, which is well below the level that could trigger a recession. Table 1As Long As Bond Yields Don’t Rise Into Restrictive Territory, Stocks Should Recover

A Correction Not A Bear Market

A Correction Not A Bear Market

Historically, equity bear markets have coincided with recessions (Chart 1). Corrections can occur outside of recessionary periods, but for stocks to go down and stay down, corporate earnings need to fall. That almost never happens unless there is a major economic downturn (Chart 2). In fact, the only time in the last 50 years the US stock market fell by more than 20% outside of a recessionary environment was in October 1987. Chart 1Recessions And Bear Markets Tend To Go Hand In Hand

Recessions And Bear Markets Tend To Go Hand In Hand

Recessions And Bear Markets Tend To Go Hand In Hand

Chart 2Business Cycles Drive Earnings

Business Cycles Drive Earnings

Business Cycles Drive Earnings

Chart 3The Bull-Bear Ratio Is Below Its Pandemic Lows

The Bull-Bear Ratio Is Below Its Pandemic Lows

The Bull-Bear Ratio Is Below Its Pandemic Lows

It is impossible to know when this correction will end. However, considering that the bull-bear spread in this week’s AAII survey fell below the trough reached both in March 2020 and December 2018, our guess is that it will be sooner rather than later (Chart 3). With global growth likely to remain solid, equity prices should rise. Q: What gives you confidence that growth will hold up? A: Households are sitting on a lot of excess savings – $2.3 trillion in the US and a similar amount abroad. That is a lot of dry powder. Banks are also actively looking to expand credit, as the recent easing in lending standards demonstrates (Chart 4). Leading indicators of capital spending are at buoyant levels (Chart 5). Chart 4US Banks Are Easing Lending Standards

US Banks Are Easing Lending Standards

US Banks Are Easing Lending Standards

Chart 5The Outlook For US Capex Is Bright

The Outlook For US Capex Is Bright

The Outlook For US Capex Is Bright

It is striking how well the global economy has handled the Omicron wave. While service PMIs have come down, manufacturing PMIs have remained firm. In fact, the euro area manufacturing PMI reached 59 in January versus expectations of 57.5. It was the strongest manufacturing print for the region since August. The manufacturing PMI also ticked up slightly in Japan. The China Caixin/Markit PMI and the official PMI published by the National Bureau of Statistics also ticked higher. After dipping below zero last August, the Citi global economic surprise index has swung back into positive territory (Chart 6). Chart 6The Omicron Wave Did Not Drag Down The Global Economy

The Omicron Wave Did Not Drag Down The Global Economy

The Omicron Wave Did Not Drag Down The Global Economy

Markets are also not pricing in much of a growth slowdown (Chart 7). Growth-sensitive industrial stocks have outperformed the overall index by 1.1% in the US so far this year. EM equities have outperformed the global benchmark by 5.9%. The Bloomberg Commodity Spot index has risen 7.2%. Credit spreads have barely increased. Chart 7Markets Are Not Discounting Much Of A Growth Slowdown

Markets Are Not Discounting Much Of A Growth Slowdown

Markets Are Not Discounting Much Of A Growth Slowdown

Q: What is your early read on the earnings season? A: Nothing spectacular, but certainly not bad enough to justify the steep drop in equity prices. According to Refinitiv, of the 145 S&P 500 companies that have reported Q4 earnings, 79% have beat analyst expectations while 19% reported earnings below expectations. Usually, 66% of companies report earnings above analyst estimates, while 20% miss expectations. In aggregate, the reported earnings are coming in 3.2% above estimates, slightly lower than the historic average of 4.1%. Guidance has been lackluster. However, outside of a few tech names like Netflix, earnings disappointments have generally been driven by higher-than-expected expenses, rather than weaker sales. Overall EPS estimates for 2022 have climbed 0.4% in the US and by 1.1% in foreign markets since the start of the year (Chart 8). Q: To the extent that the Fed is trying to engineer tighter financial conditions, doesn’t this imply that stocks must continue falling? A: That would be true if the Fed really did want to tighten financial conditions, either via lower stock prices, a stronger dollar, higher bond yields, or wider credit spreads. However, we do not think that this is what the Fed wants. Despite all the chatter about inflation, the 5-year/5-year forward TIPS breakeven inflation rate has fallen to 2.05%, which is 25 basis points below the bottom end of the Fed’s comfort zone (Chart 9).1 Chart 8Earnings Expectations Have Not Been Revised Lower

Earnings Expectations Have Not Been Revised Lower

Earnings Expectations Have Not Been Revised Lower

Chart 9Market-Based Long-Term Inflation Expectations Are Below The Fed's Comfort Zone

Market-Based Long-Term Inflation Expectations Are Below The Fed's Comfort Zone

Market-Based Long-Term Inflation Expectations Are Below The Fed's Comfort Zone

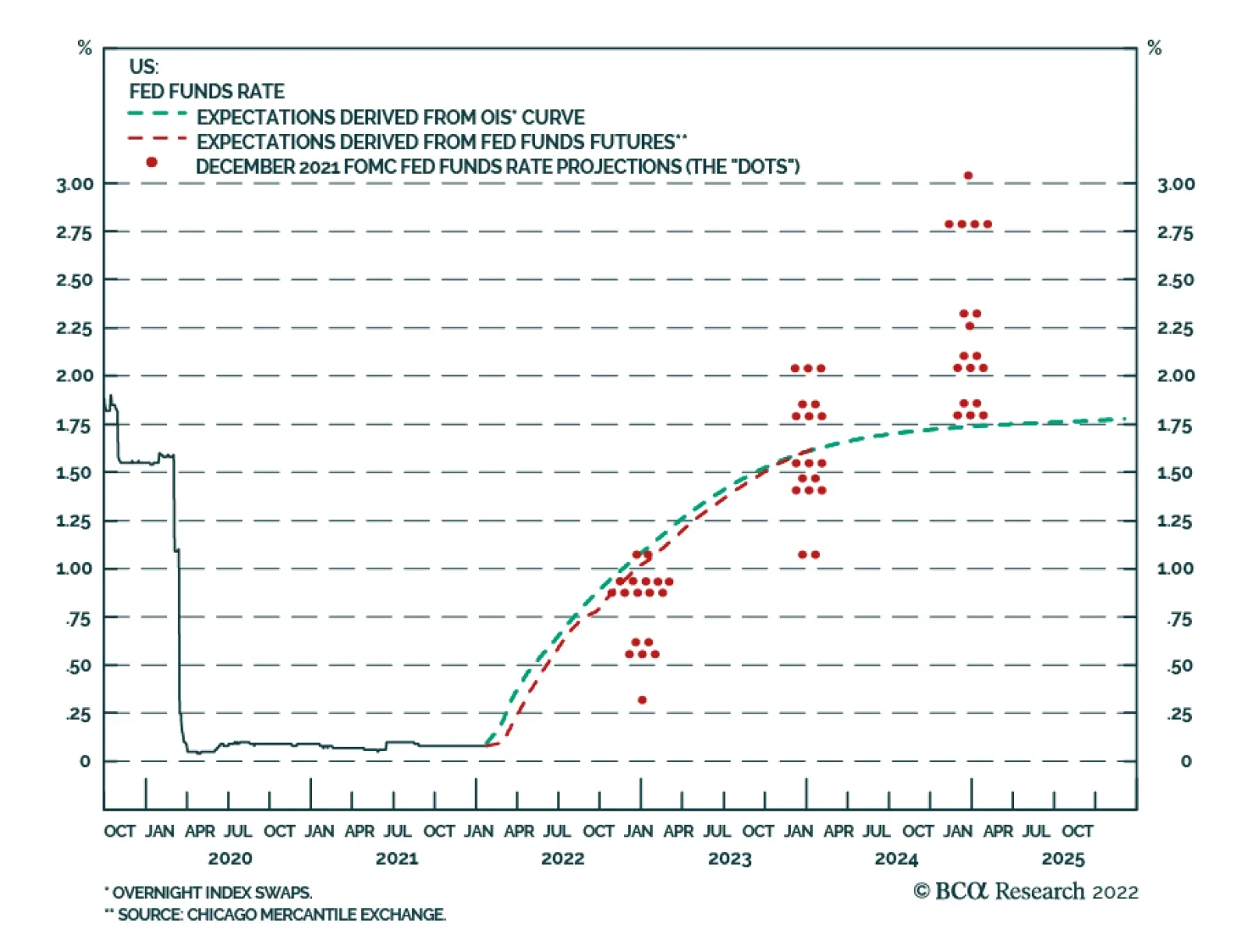

Chart 10The Terminal Fed Funds Rate Seen At 2%-2.5%

The Terminal Fed Funds Rate Seen At 2%-2.5%

The Terminal Fed Funds Rate Seen At 2%-2.5%

Chart 11The Market Thinks The Fed Will Not Be Able To Lift Rates Above 2%

The Market Thinks The Fed Will Not Be Able To Lift Rates Above 2%

The Market Thinks The Fed Will Not Be Able To Lift Rates Above 2%

Remember that the Fed’s estimate of the neutral rate, R*, is very low. The Fed thinks it will only be able to raise rates to 2.5% during this tightening cycle, which would barely bring real rates into positive territory (Chart 10). The market does not think the Fed will be able to raise rates to even 2% (Chart 11). The last thing the Fed wants to do is inadvertently invert the yield curve. In the past, an inverted yield curve has reliably predicted a recession (Chart 12). Chart 12A Yield Curve Inversion Usually Signals The End Of A Business Cycle (And Can Even Predict A Pandemic)

A Yield Curve Inversion Usually Signals The End Of A Business Cycle (And Can Even Predict A Pandemic)

A Yield Curve Inversion Usually Signals The End Of A Business Cycle (And Can Even Predict A Pandemic)

The Fed is about to start raising rates and shrinking its balance sheet not because it wants to slow growth, but because it wants to maintain its credibility. While the Fed will never admit it, it is very much attuned to the direction in which the political winds are blowing. The rise in inflation, and the Fed’s failure to predict it, has been embarrassing for the FOMC. Doing nothing is no longer an option. However, doing “something” does not necessarily imply having to raise rates more than the market is already discounting. Contrary to the consensus view that the Fed has turned hawkish, we think that the main takeaway from this week’s FOMC meeting is that Jay Powell, aka Nimble Jay, wants more flexibility in how the Fed conducts monetary policy. This makes perfect sense, as layer upon layer of forward guidance merely served to confuse market participants while unnecessarily tying the Fed’s hands. Q: How confident are you that inflation will fall without a meaningful tightening in financial conditions? A: If we are talking about a horizon of 2-to-3 years, not very confident. As we discussed two weeks ago in a report entitled The New Neutral, the interest rate consistent with stable inflation and full employment is substantially higher than either the Fed believes or the market is pricing in. This means that the Fed is likely to keep rates too low for too long. However, if we are talking about a 12-month horizon, there is a high probability that inflation will fall dramatically, even if monetary policy stays very accommodative. Today’s inflation is largely driven by rising durable goods prices. Durables are the one category of the CPI basket where prices usually fall over time, so this is not a sustainable source of inflation (Chart 13). As demand shifts back from goods to services and supply bottlenecks abate, durable goods inflation will wane. Chart 14 shows that the price indices for a number of prominent categories of goods – including new and used vehicles, furniture and furnishings, building supplies, and IT equipment – are well above their trendlines. Not only is inflation in these categories likely to fall, but it is apt to turn negative, as the absolute level of prices reverts back to trend. This will put significant downward pressure on inflation. Chart 13Durable Goods Prices Are The Main Driver Of Inflation

Durable Goods Prices Are The Main Driver Of Inflation

Durable Goods Prices Are The Main Driver Of Inflation

Chart 14Some Of These Prices Will Fall Outright

Some Of These Prices Will Fall Outright

Some Of These Prices Will Fall Outright

Chart 15Wage Growth Has Picked Up, Especially At The Bottom Of The Income Distribution

Wage Growth Has Picked Up, Especially At The Bottom Of The Income Distribution

Wage Growth Has Picked Up, Especially At The Bottom Of The Income Distribution

Granted, service inflation will accelerate this year as the labor market continues to tighten. However, rising service inflation is unlikely to offset falling goods inflation. While wage growth has accelerated, wage pressures have been concentrated at the bottom end of the wage distribution (Chart 15). According to the Census Household Pulse Survey, a record 8.75 million workers – many of them in relatively low-paid service jobs – were not working in the second week of January due to pandemic-related reasons (Chart 16). As the Omicron wave fades, most of these workers will re-enter the labor force. This should help boost labor participation among low-wage workers, which has recovered much less than for higher paid workers (Chart 17). Chart 16The Pandemic Is Still Affecting Labor Supply

The Pandemic Is Still Affecting Labor Supply

The Pandemic Is Still Affecting Labor Supply

Chart 17Employment In Low-Wage Industries Has Not Fully Recovered

Employment In Low-Wage Industries Has Not Fully Recovered

Employment In Low-Wage Industries Has Not Fully Recovered

Q: Tensions between Ukraine and Russia have risen to a fever pitch. Could this destabilize global markets? Chart 18Valuations Matter For Long-Term Returns

Valuations Matter For Long-Term Returns

Valuations Matter For Long-Term Returns

A: In a note published earlier today, Matt Gertken, BCA’s Chief Geopolitical Strategist, increased his odds that Russia will invade Ukraine from 50% to 75%. However, of that 75% war risk, he gives only 10% odds to Russia invading and conquering all of Ukraine. A much more likely scenario is one where Russia invades Donbas and perhaps a few other regions in Eastern or Southern Ukraine where there are large Russian-speaking populations and/or valuable coastal territory. While such a limited incursion would still invite sanctions from the West, Matt does not think that Russia will retaliate by cutting off oil and natural gas exports to Europe. Not only would such a retaliation deprive Russia of its main source of export earnings, but it could lead to a hostile response from countries such as Germany which so far have pushed for a more measured approach than the US has championed. Q: Valuations are still very stretched. Even if the conflict in Ukraine does not spiral out of control and the goldilocks macroeconomic scenario of above-trend global growth and falling inflation comes to pass, hasn’t much of the good news already been discounted? A: US stocks are quite pricey. Both the Shiller PE ratio and households’ allocations to equities point to near-zero total returns for stocks over a 10-year horizon (Chart 18). That said, valuations are not a useful timing tool. The business cycle, rather than valuations, tends to dictate the path of stocks over medium-term horizons of 6-to-12 months (Chart 19). Chart 19AThe Business Cycle Drives The Stock Market Over Medium-Term Horizons (I)

The Business Cycle Drives The Stock Market Over Medium-Term Horizons (I)

The Business Cycle Drives The Stock Market Over Medium-Term Horizons (I)

Chart 19BThe Business Cycle Drives The Stock Market Over Medium-Term Horizons (II)

The Business Cycle Drives The Stock Market Over Medium-Term Horizons (II)

The Business Cycle Drives The Stock Market Over Medium-Term Horizons (II)

Moreover, stocks are not expensive everywhere. While US equities trade at 20.8-times forward earnings, non-US stocks trade at a more respectable 14.1-times. The valuation gap is even more extreme based on other measures such as normalized earnings, price-to-book, and price-to-sales (Chart 20). Chart 20AUS Stocks Are Trading At A Significant Premium To Their Non-US Peers (I)

US Stocks Are Trading At A Significant Premium To Their Non-US Peers (I)

US Stocks Are Trading At A Significant Premium To Their Non-US Peers (I)

Chart 20BUS Stocks Are Trading At A Significant Premium To Their Non-US Peers (II)

US Stocks Are Trading At A Significant Premium To Their Non-US Peers (II)

US Stocks Are Trading At A Significant Premium To Their Non-US Peers (II)

In terms of equity styles, both small caps and value stocks trade at a substantial discount to large caps and growth stocks (Chart 21). We recommend that investors overweight these cheaper areas of the market in 2022. Trade Recommendation: Go Long US Homebuilders Versus The S&P 500 US homebuilder stocks have fallen by 19.4% since December 10th. Beyond the general market malaise, worries about rising mortgage rates and soaring input costs have weighed on the sector. Yet, current valuations more than adequately discount these risks. The sector trades at 6.5-times forward earnings, a steep discount to the S&P 500. Whereas demand for new homes is near record high levels according to the National Association of Home Builders (NAHB) survey, the homeowner vacancy rate is at a multi-decade low. The supply of recently completed new homes is half of what it was on the eve of the pandemic (Chart 22). With demand continuing to outstrip supply, home prices will maintain their upward trend. As building material prices stabilize and worries about an overly aggressive Fed recede, homebuilder stocks will rally. Chart 21Value Stocks And Small Caps Are Cheap

Value Stocks And Small Caps Are Cheap

Value Stocks And Small Caps Are Cheap

Chart 22US Homebuilders Looking Attractive

US Homebuilders Looking Attractive

US Homebuilders Looking Attractive

Peter Berezin Chief Global Strategist peterb@bcaresearch.com Footnotes 1 The Federal Reserve targets an average inflation rate of 2% for the personal consumption expenditures (PCE) index. The TIPS breakeven is based on the CPI index. Due to compositional differences between the two indices, CPI inflation has historically averaged 30-to-50 basis points higher than PCE inflation. This is why the Fed effectively targets a CPI inflation rate of about 2.3%-to-2.5%. Global Investment Strategy View Matrix

A Correction Not A Bear Market

A Correction Not A Bear Market

Special Trade Recommendations Current MacroQuant Model Scores

A Correction Not A Bear Market

A Correction Not A Bear Market

Feature Is the worst over for US and EM equities? Clearly, the risk-reward of stocks has somewhat improved, given they are no longer overbought and some bad news has already been priced in. However, conditions for a durable bottom and a sustainable and lasting rally do not yet exist. In the case of the S&P 500, our capitulation indicator has not yet reached the lows that marked the major bottoms of the past 12 years (Chart 1). Chart 1US Stocks Have Not Reached Their Selling Climax Yet

US Stocks Have Not Reached Their Selling Climax Yet

US Stocks Have Not Reached Their Selling Climax Yet

Chart 2Components Of US Equity Capitulation Indicator

Components Of US Equity Capitulation Indicator

Components Of US Equity Capitulation Indicator

None of its four components – the advance/decline line, momentum, breadth and investor sentiment – are back to their lows of 2010, 2011, 2015-16 and 2018 (Chart 2). In the past three cases, the S&P 500 corrected by 17-20%. A correction of this magnitude is our base case for the S&P 500 at the moment. The S&P drawdown has so far been half of this. US inflation and the Fed’s policy remain the key headwinds to US share prices. Core consumer price inflation is substantially above the Fed’s preferred range (2-2.25%) and wage growth is accelerating. As a result, the Fed will lose credibility if it does not sound ready to hike interest rates materially. The US equity market is vulnerable to such a not-dovish stance from the Fed because it is still very expensive. Inflation has also become a political problem. One reason Biden’s popularity has been sliding in the polls is the rapid pace of consumer price increases. Heading into the mid-term elections in the fall, the White House and the Democrats will not oppose the Fed raising interest rates to fight inflation. Overall, BCA’s Emerging Markets Strategy team believes markets/investors are underestimating inflation risks in the US. Core inflation will not drop below 3% unless the economy slows down and employment/wages slump. High and rising trimmed-mean and median CPI measures suggest inflation is broad-based. Normalization in supply-side factors will not be enough to lower core inflation below 3%. Importantly, the median and trimmed-mean core inflation measures strip out goods and services that post abnormal fluctuations. Their elevated readings corroborate that inflation is genuine and broad-based. Hence, pressure on the Fed to tighten will remain substantial. This is bad news for a still overvalued US stock market. Chart 3EM EPS Is Set To Dissapoint

EM EPS Is Set To Dissapoint

EM EPS Is Set To Dissapoint

Concerning EM equities and currencies, economic growth in EM will disappoint. Chart 3 suggests that EM corporate profits are set to deteriorate materially in the coming six months or so. Besides, investor sentiment on EM equities is not downbeat – it is neutral (Chart 28 below). From a contrarian perspective, there is not yet a case to buy EM stocks in absolute terms. China’s business cycle recovery is still several months away. In other EM countries, monetary policy has tightened substantially, real interest rates remain high, or the banking system is too unhealthy to support growth. Finally, fiscal policy will be slightly tight this year in the majority of EM. As domestic demand in China and in mainstream EMs disappoint and the Fed does not do a dovish pivot soon, EM currencies will resume their depreciation versus the US dollar. Chart 4 shows that China’s credit and fiscal impulse leads EM currency cycles and is presently pointing to more EM currency depreciation. Charts 32 and 33 (below) are pointing to further greenback strength. Finally, EM growth disappointments and a strong greenback will pressure EM fixed income markets. EM high-yield (HY) credit – both sovereign and corporate – has been selling off, but investment-grade (IG) credit has been holding up (Chart 5). This is a sign that investors have been reluctant to offload EM IG credit and points to lingering positive sentiment on EM and lack of capitulation. Sluggish EM growth and an appreciating US dollar are headwinds for EM credit markets. Chart 4EM Currencies Remain At Risk

EM Currencies Remain At Risk

EM Currencies Remain At Risk

Chart 5EM Credit Markets: The Selloff Will Broaden

EM Credit Markets: The Selloff Will Broaden

EM Credit Markets: The Selloff Will Broaden

Bottom Line: We continue to recommend a defensive strategy for absolute return investors. For global equity portfolios, we recommend underweighting EM and the US, and overweighting Europe and Japan. The path of least resistance for the US dollar is up for now. The charts on the following pages are the most important ones for investors today. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com US Stocks Have Not Reached Their Selling Climax Yet Even though only 17% of the NASDAQ’s stocks are above their 200-day moving average, the same measure for the NYSE index is 38%, well above its previous lows. Besides, the NYSE’s advance/decline line has broken down, signifying a broadening equity rout. Finally, the US median stock has broken below its 200-day moving average after going sideways for 9-12 months. When such a profile occurs, the sell-off lasts more than a couple of weeks. Chart 6

US Stocks Have Not Reached Their Selling Climax Yet

US Stocks Have Not Reached Their Selling Climax Yet

Chart 7

US Stocks Have Not Reached Their Selling Climax Yet

US Stocks Have Not Reached Their Selling Climax Yet

Chart 8

US Stocks Have Not Reached Their Selling Climax Yet

US Stocks Have Not Reached Their Selling Climax Yet

Chart 9

US Stocks Have Not Reached Their Selling Climax Yet

US Stocks Have Not Reached Their Selling Climax Yet

Non-US Stocks Are Not Oversold Yet Neither global ex-US nor EM stocks are very oversold. Global ex-US and European share prices in SDR terms have been moving sideways for about 9-12 months prior to breaking down recently. Such a breakdown means a weakness in share prices that will likely last for a while. Chart 10

Non-US Stocks Are Not Oversold Yet

Non-US Stocks Are Not Oversold Yet

Chart 11

Non-US Stocks Are Not Oversold Yet

Non-US Stocks Are Not Oversold Yet

Chart 12

Non-US Stocks Are Not Oversold Yet

Non-US Stocks Are Not Oversold Yet

Chart 13

Non-US Stocks Are Not Oversold Yet

Non-US Stocks Are Not Oversold Yet

Growth Stocks Have Broken Down Various indexes of growth/TMT stocks have broken below their moving averages that have served as a support since spring 2020. This along with the fact that US interest rates will likely rise suggests that the bull market in growth stocks is either over or in for a prolonged hibernation. Chart 14

Growth Stocks Have Broken Down

Growth Stocks Have Broken Down

Chart 15

Growth Stocks Have Broken Down

Growth Stocks Have Broken Down

Chart 16

Growth Stocks Have Broken Down

Growth Stocks Have Broken Down

Chart 17

Growth Stocks Have Broken Down

Growth Stocks Have Broken Down

Is FAANGM A Bubble? In the past 12 years, US FAANGM stocks rose as much as the previous bubbles. When those bubbles peaked, their prices did not move sideways but rather collapsed. We do not assert that US FAANGM stocks will drop by more than 35% (we simply do not know). The point we would like to emphasize is that the bull market is over for now. At best, US growth stocks will likely be in a trading range in the coming 12-24 months. Chart 18

Is FAANGM A Bubble?

Is FAANGM A Bubble?

Chart 19

Is FAANGM A Bubble?

Is FAANGM A Bubble?

US Share Prices And Corporate Margins: Defying Gravity? From a very long-term perspective, the US equity market is rather overextended. Share prices in real terms are almost two standard deviations above their time trend. Similarly, corporate profits in real terms are also very elevated, not least in their reflection of record-high profit margins. The key questions for US equity investors are: (1) how persistent/sticky core inflation will be; and (2) how low corporate profit margins will drop. Wages are the key to both inflation and corporate margins. We believe wage growth will accelerate materially. That will be bad for the outlook of inflation and corporate profit margins, although it will be good news for corporate top lines. Chart 20

US Share Prices And Corporate Margins: Defying Gravity?

US Share Prices And Corporate Margins: Defying Gravity?

Chart 21

US Share Prices And Corporate Margins: Defying Gravity?

US Share Prices And Corporate Margins: Defying Gravity?

The Levels of EM Share Prices And Corporate Profits Have Been Flat For 12 years Contrary to the US, EM share prices are not overextended – they have been flat in absolute terms for the past 12 years. The reason for such dismal performance has been stagnant corporate profits. The latter have been flat-to-down in real terms for the past 12-14 years. A breakout in EM share prices in absolute terms will require their EPS entering a secular uptrend. While this is not impossible this decade, it is not imminent. Chart 22

The Levels Of EM Share Prices And Corporate Profits Have Been Flat For 12 Years

The Levels Of EM Share Prices And Corporate Profits Have Been Flat For 12 Years

Chart 23

The Levels Of EM Share Prices And Corporate Profits Have Been Flat For 12 Years

The Levels Of EM Share Prices And Corporate Profits Have Been Flat For 12 Years

Long-Term Equity Valuations (Cyclically-Adjusted P/E Ratio) Based on a cyclically-adjusted P/E (CAPE) ratio, EM stocks are close to their fair value. In contrast, based on the same measure, US equities are very overvalued. As a result, the relative CAPE ratio of EM versus the US is at a record low. Hence, on a multi-year horizon, odds are that EM share prices will outperform their US peers. In a nutshell, EM ex-China, Korea, Taiwan currencies are also close to their fair value. We will be looking to upgrade EM in the coming months. Chart 24

Long-Term Equity Valuations (Cyclically-Adjusted P/E Ratio)

Long-Term Equity Valuations (Cyclically-Adjusted P/E Ratio)

Chart 25

Long-Term Equity Valuations (Cyclically-Adjusted P/E Ratio)

Long-Term Equity Valuations (Cyclically-Adjusted P/E Ratio)

Chart 26

Long-Term Equity Valuations (Cyclically-Adjusted P/E Ratio)

Long-Term Equity Valuations (Cyclically-Adjusted P/E Ratio)

Chart 27

Long-Term Equity Valuations (Cyclically-Adjusted P/E Ratio)

Long-Term Equity Valuations (Cyclically-Adjusted P/E Ratio)

Investors Are Not Bearish On EM And Europe One missing factor to upgrade EM (non-US markets in general) is investor sentiment. Sentiment is neutral on EM stocks and is fairly upbeat on Europe. In brief, a capitulation has also not yet occurred in non-US markets. On the whole, the current EM sell-off will likely linger until sentiment becomes downbeat. Chart 28

Investors Are Not Bearish On EM And Europe

Investors Are Not Bearish On EM And Europe

Chart 29

Investors Are Not Bearish On EM And Europe

Investors Are Not Bearish On EM And Europe

Directional Indicators For EM Stocks Points To More Downside The cross rate between SEK (a pro-cyclical currency) and CHF (a defensive one) moves in tandem with EM share prices. The same holds for the NZD versus the USD. The rationale is as follows: all of these currencies correlate with the global business cycle and global risk-on/off trends. Presently, the SEK/CHF cross and the NZD point to lower EM share prices. Chart 30

Directional Indicators For EM Stocks Points To More Downside

Directional Indicators For EM Stocks Points To More Downside

Chart 31

Directional Indicators For EM Stocks Points To More Downside

Directional Indicators For EM Stocks Points To More Downside

The US Dollar Is To Rally Further The Fed’s willingness (for now) to hike rates is positive for the greenback. The trend in relative TIPS yields between the US and Germany heralds further USD strength against the euro. Also, the cross rate between SEK (a pro-cyclical currency) and CHF (a defensive one) entails more upside in the broad trade-weighted US dollar. Chart 32

The US Dollar Is To Rally Further

The US Dollar Is To Rally Further

Chart 33

The US Dollar Is To Rally Further

The US Dollar Is To Rally Further

Worrisome Market Profiles Several markets such as EM non-TMT share prices, Korean tech stocks, the Chinese onshore CSI300 stock index and silver prices have all failed to break above their 200-day moving averages and are now relapsing. Such a profile is often consistent with new cyclical lows in these markets. Chart 34

Worrisome Market Profiles

Worrisome Market Profiles

Chart 35

Worrisome Market Profiles

Worrisome Market Profiles

Chart 36

Worrisome Market Profiles

Worrisome Market Profiles

Chart 37

Worrisome Market Profiles

Worrisome Market Profiles

China’s Liquidity And Credit Cycles Even though China has heightened the pace of monetary easing, it will take several months before its credit impulse rebounds. On average, it takes about six months for reductions in the required reserve ratio (liquidity injections) to produce a meaningful recovery in the credit impulse. So far, the excess reserve ratio has stabilized but not improved. This means the credit impulse will continue stabilizing in the coming months, but a major rise is unlikely in the near term. In turn, the credit cycle leads share prices by several months. All in all, a risk window for China-related plays remains open in the coming months. Chart 38

China's Liquidity And Credit Cycles

China's Liquidity And Credit Cycles

Chart 39

China's Liquidity And Credit Cycles

China's Liquidity And Credit Cycles

Footnotes

As expected, the Fed maintained the target range for the fed funds rate unchanged at 0 to 0.25% following its meeting on Wednesday. However, the FOMC statement noted that “it will soon be appropriate to raise the target range for the federal funds rate.” At…

Highlights The Biden administration faces significant risks from outside the US economy – our third “key view” for 2022. The Ukraine conflict brings one external risk to the forefront. These external risks would exacerbate the global supply squeeze, potentially pushing up commodity prices until they start to kill demand. Investors should prepare for oil price overshoots. Exogenous risks – such as foreign policy crises – rarely help the president’s party in the midterm election. Any crisis that adds to short-term inflation will hurt the ruling party. Tactically we continue to prefer defensive equities. Close our tactical long industrials / short consumer discretionary trade for a gain of 11.6%. Close long energy stocks for a 15.6% gain and convert to long energy small caps versus large caps. Buy the dip in cyber security stocks. Feature Stock market volatility is back, thanks in no small part to external risks such as Europe’s energy shortage and Russia’s conflict with the West over Ukraine. In our forecast for 2022, we highlighted the Biden administration’s external risks as our third key view. The rapidly deteriorating geopolitical situation was one of several reasons behind this view and it has now clearly moved to the forefront. In this report we highlight the consequences for domestic-oriented US investors. Biden’s immediate external risks, if they materialize, will increase the likelihood that Democrats will lose control of Congress, causing US fiscal policy to freeze and driving policy uncertainty and the dollar upward. For detailed coverage of the Ukraine conflict and its global geopolitical, macro, and market implications please refer to our Geopolitical Strategy reports. Why Is Biden Vulnerable To External Risks The Biden administration and the Democratic Party face serious external risks in 2022. The Omicron variant and global supply constraints are a major factor. Also the US’s domestic political divisions invite challenges from abroad. President Biden is politically weak ahead of midterm elections on November 8. His net approval rating is under water at -10 percentage points. Republicans are now leading the generic congressional ballot with 45.5% support against Democrats’ 41.8%. On a deeper level, Democrats are beset by a socialist fringe on their left wing, making it difficult to pass legislation, and an enthusiastic nationalist opposition movement with a viable challenger for the presidency in 2024 (former President Trump). At best they will pass one more major bill this year before Congress gets gridlocked. Foreign rivals have an advantage in this context. America’s chief rivals face limited political constraints at home (no midterm elections) but they can make low-cost, high-impact threats against the Biden administration through their leverage over the global supply chain and hence voters’ pocketbooks. External Risks Are Inflationary (At Least At First) External risks begin with inflation. The US’s large imbalance of investment over savings is evident in a current account deficit of 3.3% and deteriorating terms of trade. American demand is exceedingly strong due to accumulated household savings, a new capex cycle, and lingering effects of monetary and fiscal stimulus. Yet global supply is impeded. Import prices are rising at a 5.7% rate, the fastest since the BLS started the series in 2010, while imports from China are rising at a 4.7% clip. China’s “zero Covid” policy implies that supply disruptions will keep up the inflationary pressure this year (Chart 1, first panel). The US is also importing inflation from rising commodity prices. West Texas Intermediate crude oil prices have risen to $83 per barrel and average gasoline prices stand at $3.3. With global supply-demand balances tight, WTI prices should average $77 per barrel this year and $78 next year, according to our Commodity & Energy Strategy. In this context, unplanned supply disruptions are likely and will put more pressure on the supply side. Any conflicts with oil producers such as Russia and Iran will backfire in the form of higher prices at the pump (Chart 1, second panel). Yet geopolitical competitors (Russia, Iran, China) have unfinished business with the US stemming from the Trump administration. It is also possible that Biden could negotiate diplomatic solutions, reducing the risk of an oil price spike, but that is not the current trajectory. Chart 1Biden's External Risks Are Inflationary For Now

Biden's External Risks Are Inflationary For Now

Biden's External Risks Are Inflationary For Now

Interest rate hikes from the Federal Reserve will not easily control inflation derived from external sources and supply constraints. They will take time to dampen domestic demand. Yet voters usually solidify their opinions by mid-summer. Inflation may not have come down much by that time. Biden and the Democratic Party are at the mercy of the global supply chain. In this context Russia deliberately forced its way to the top of the US and global agenda by demanding that the West renounce any attempt to threaten its national security via Ukraine or the former Soviet Union. Energy Shock From Russia? The Ukraine crisis threatens an increase in global energy prices. Russia provides 8% of Europe’s commodity imports, 18% of its energy imports, and 16% of its natural gas imports (Chart 2). Russia is already withholding energy supplies from Europe, helping push natural gas prices up by 122% since last August. If war ignites, Russia could reduce energy flows to Ukraine and hence to the rest of Europe. Europe would not be willing to impose as harsh of sanctions as the US because its energy supply depends on it. The US can increase exports to Europe but it cannot replace Russia without depriving its other allies and partners, including India, Japan, and South Korea (Chart 3). The squeeze will cause prices to rise at first but if it is not addressed by higher output from the US and OPEC 2.0, then demand will be destroyed. Note that in 1979, 2008, and 2014, Russian military invasions coincided with a peak in global oil prices. Chart 2Geopolitical Risks Cause Resource Squeeze

Biden’s External Risks

Biden’s External Risks

Chart 3Can US Replace Russia For Europe? Not Really.

Biden’s External Risks

Biden’s External Risks

If other supply problems emerged simultaneously, the slowdown could be especially disruptive. If US-Iran negotiations fail, then another energy supply risk will emerge immediately this spring. The implication is not only a rise in oil prices but also a resilient dollar, which is also the implication of the Fed’s looming rate hikes. Defensive plays would tend to beat cyclical plays, at least in the short run until the crisis abates. But it is important to look at previous examples of Russian aggression to test this hypothesis. US Market Response To Russian Belligerence When Russia invaded Georgia in August 2008, the attack had limited impact on global financial markets, which were focused on the subprime mortgage crisis unfolding on Wall Street. Naturally stocks underperformed bonds, cyclicals underperformed defensives, and value went sideways against growth. Small caps rallied at first versus large caps but then hit a turning point from outperformance to underperformance (Chart 4). Note that the invasion began while President Putin watched the summer Olympics live in Beijing. So one cannot rule out a limited military action against Ukraine in the near term just because Putin is also headed to Beijing for this winter’s Olympics. When Russia invaded Ukraine in February 2014, seizing the Crimean peninsula in the Black Sea, the attack had a greater impact on global financial markets than with Georgia, although Ukraine’s relevance to the global economy was (and is) still limited. Chart 4Market Reaction To Russia Invasion Of Georgia, 2008

Market Reaction To Russia Invasion Of Georgia, 2008

Market Reaction To Russia Invasion Of Georgia, 2008

Chart 5Market Reaction To Russia Invasion Of Ukraine, 2014

Market Reaction To Russia Invasion Of Ukraine, 2014

Market Reaction To Russia Invasion Of Ukraine, 2014

Bonds outperformed stocks, cyclicals were flat-to-up against defensives (energy clearly outperformed defensives), and small caps stumbled but then beat out large caps (Chart 5). Energy stocks theoretically stood to benefit but crashed later that year due to supply glut and China policy tightening. In 2022 the situation is different from these previous Russian invasions in that the world is already in the thrall of an energy supply squeeze brought on by various factors. China’s economy is growing slowly but authorities are easing policy. A comparison of the winter of 2021-22 with that of 2013-14, when Russia invaded Crimea, suggests that energy stocks have already far outpaced growth and defensives (Chart 6). Energy small caps, however, could rally substantially against large cap peers. Tactically US investors should maintain a risk-averse positioning until the Russians make a military decision and the West announces its retaliatory measures. This analysis suggests that cyclicals and small caps face volatility but can ultimately grind higher after the onset of any new war in Ukraine. The magnitude of the war will obviously matter, which is why we maintain a defensive tactical positioning. The next question centers on the medium-term policy impact of Biden’s external risks. Chart 6Market Context: 2022 Versus 2014

Market Context: 2022 Versus 2014

Market Context: 2022 Versus 2014

Implications For US Midterms And Policy It is possible that Biden’s external risks will play a role in the 2022 midterms. It depends on which risks materialize. Most likely a Russian re-invasion of Ukraine would have a negative effect on the Democrats, especially if it adds to voters’ inflation woes. Major foreign policy successes or failures have a substantial impact on a president’s re-election chances but midterms are less obvious. Midterms almost always go against the president’s party because the previous election’s losers turn out in droves while winners sit home in complacency or disillusionment. The midterm electorate tends to be older, whiter, and more educated than the presidential electorate. Chart 7 shows only midterm elections in which external risks – such as foreign policy – played a major role. In the House, the only time the president’s party gained seats was in 2002, though it only lost four seats in 1962. In the Senate, the president’s party gained seats in 1962, 2002, and 2018 and only lost 2 seats in 1954. From these points we can draw the following conclusions: Chart 7US Midterm Elections: Ruling Party Performance Amid Foreign Policy Crises

Biden’s External Risks

Biden’s External Risks

Foreign policy crises do not generally help the president’s party. While major crises like 9/11 helped the Republicans, and the 1962 Cuban Missile Crisis minimized Democrats’ losses, nevertheless the 1942 midterm occurred after Pearl Harbor and the Democrats lost seats. Minor crises like the 1958 “Lebanon Crisis” also do not help. Russia’s invasion of Ukraine in 2014 falls under this category and did not help President Obama’s Democrats. A major threat to the homeland can help the president’s party on the margin. This is the significance of 1962 and 2002. The ruling party either minimized losses or made absolute gains in the House, while gaining seats in the Senate. (The 2018 midterm is the other case in which the president’s party gained Senate seats, amid President Trump’s trade war with China, but Republicans suffered heavily in the House.) Wartime escalation and entanglement hurt the president’s party. President Johnson’s Democrats suffered deep losses in 1966, as did President George W. Bush’s Republicans in 2006. Obama’s troop surge in Afghanistan was not the main issue but did not help his party in 2010. Ceasefires and peace treaties do not help the president’s party, even when the end of the war is seen as a victory. World War I was drawing to a close in 1918 but Democrats suffered for having gotten the US involved. Democrats also lost in 1946, despite US triumph in WWII. The Korean war ended on a far more ambivalent note and Republicans suffered at the ballot box. Vietnam was drawing to an ignominious close in 1974, which also occurred in the aftermath of the Arab oil embargo, recession, and Watergate scandal, so no surprise Republicans lost seats. If there is a foreign policy crisis this year, the “best case” for Biden’s Democrats – in crass political terms – would be one that engenders a patriotic rally, like happened with the Cuban Missile Crisis or 9/11. If Democrats only lose four seats in 2022, like Kennedy in 1962, they will have a one-seat majority in the House. However, this best-case scenario is unlikely. As noted, 1962 and 2002 consisted of direct threats to the US homeland. All other crises either hurt or did not help the president’s party. In 2014, while voters had other things on their minds that year, Russia’s invasion of Crimea reinforced criticisms of Obama’s foreign policy already centered on Libya, Syria, and Iran. Obama responded with sanctions and aid to Ukraine, as Biden threatens to do today. Democrats lost 13 seats in the House and 9 seats in the Senate. A similar negative impact should be expected if Russia re-invades in 2022. Biden is already vulnerable: his approval rating collapsed after his messy withdrawal from Afghanistan (reinforcing the fourth bullet about ending wars above). A new foreign policy crisis could cement the narrative of foreign policy incompetence. It matters a great deal whether an exogenous crisis automatically hurts the voter’s pocketbook. If it does, then any initial rally around the flag will fade over time, leaving the negative material impact behind and angering voters. In 1974, President Ford’s approval rating shot up above 50% as he took over from Nixon, yet his party still suffered from the inflationary economic backdrop and dour foreign policy backdrop. In 1978, President Carter’s approval rating also recovered to nearly 50% in time for the vote but it was not enough to overcome inflationary malaise – and Iranian oil strikes began in September (Chart 8). If we subtract the Misery Index (unemployment plus inflation) from the president’s approval rating, we see that Kennedy had a 70% approval during the Cuban Missile Crisis, and Bush had a 62% approval in 2002. But Johnson and Carter were sinking toward 35% during their first midterms, which is where Biden stands today (Chart 9). Chart 8Different Reactions For Different Crises

Biden’s External Risks

Biden’s External Risks

Chart 9Best And Worst Case Scenarios Of Foreign Policy Crisis For Democrats

Biden’s External Risks

Biden’s External Risks

Thus Biden’s external risks, depending on which ones materialize, suggest that the Democratic Party will face another headwind in November. Democrats are very likely to lose the House and somewhat likely to lose the Senate. Gridlock is already setting in – as will be apparent with the potential government shutdown over the February 18 deadline to pass spending bills. But the midterm will formalize it. Policy uncertainty will continue to creep up and weigh on investor risk appetite this year. In other words, even if cyclicals rally through a Ukraine conflict, they may not outperform defensives later this year. Investment Takeaways Cyclically we are booking an 15.6% gain on our long energy trade and will convert it to a long US energy small caps relative to large caps trade. The external risks highlighted in this report would push up oil prices at least initially (Chart 10). However, volatility will pick up from here. OPEC 2.0 will want to keep Brent crude prices from settling above the $90 per barrel that starts to crimp demand, as our Commodity & Energy Strategy argues. Higher prices will also encourage new production, including from the US shale patch (Chart 11). Note that energy stocks, like other cyclicals, tend to underperform during midterm election years as policy uncertainty affects markets. Chart 10Book Gains On Tactical Long Energy Equities Trade

Book Gains On Tactical Long Energy Equities Trade

Book Gains On Tactical Long Energy Equities Trade

Chart 11US Oil Producers Will Step Up

US Oil Producers Will Step Up

US Oil Producers Will Step Up

Tactically we recommend closing our long industrials / short consumer discretionary for a gain of 11.6%. Normally, consumer discretionary stocks are the best performing sector during midterm election years while industrials are the worst. But because of China’s policy easing, we took a tactical bet that the opposite would occur at the start of the year. However, external risks should now cause this situation to reverse by pushing up the dollar, penalizing industrials, without hurting the American consumer too much (Chart 12). Industrial equities are pricing in strong capex intentions but geopolitical conflicts would weigh on those intentions, while new orders and core durable goods orders could suffer a bit (Chart 13). The midterms will come into focus later this year and weigh on industrials as well. Chart 12Close Long Industrials Trade For Now

Close Long Industrials Trade For Now

Close Long Industrials Trade For Now

Chart 13Industrials Still Attractive On Cyclical Basis

Industrials Still Attractive On Cyclical Basis

Industrials Still Attractive On Cyclical Basis

Cyclically stick with cyber security stocks. They have sold off along with the tech sector as interest rates rise. But long cyber security is a secular investment thesis based on digitization of the economy, rising cyber crime, and geopolitical risk. Tensions with Russia, proxied by the fall in the ruble and rise in aerospace/defense stocks, point to the fact that investors recognize international tensions will remain high (Chart 14). Cyber space will remain an area of conflict even if physical conflict does not materialize. Growth stocks should also revive later as midterm policy uncertainty picks up. Chart 14Cyber Security Is A Secular Trade ... Buy The Dip

Cyber Security Is A Secular Trade ... Buy The Dip

Cyber Security Is A Secular Trade ... Buy The Dip

Chart 15Overweight Health Care Amid Political Risk

Overweight Health Care Amid Political Risk

Overweight Health Care Amid Political Risk

Tactically stick with overweight health care on rising uncertainty and expectations that the dollar will pick up (Chart 15). Defensives, especially health, should also outperform as the year goes on and midterms approach. Pricing power is returning to the sector but the Biden administration only has a little legislative ammunition left and its regulatory focus lies elsewhere for now. Matt Gertken Vice President US Political Strategist mattg@bcaresearch.com Strategic View Open Tactical Positions (0-6 Months) Open Cyclical Recommendations (6-18 Months) Table A2Political Risk Matrix

Biden’s External Risks

Biden’s External Risks

Table A3US Political Capital Index

Biden’s External Risks

Biden’s External Risks

Image

Image

Table A4APolitical Capital: White House And Congress

Biden’s External Risks

Biden’s External Risks

Table A4BPolitical Capital: Household And Business Sentiment

Biden’s External Risks

Biden’s External Risks

Table A4CPolitical Capital: The Economy And Markets

Biden’s External Risks

Biden’s External Risks

Highlights Banks, households, and businesses are still swimming in cash: Asset purchases and zero rates are ending, but banks, households and businesses have more cash than they know what to do with. It will not be easy for the Fed to mop up enough accommodation to slow the economy in a material way this year. The flood of liquidity may be a headwind for interest rates in 2022, … : The biggest banks have positioned themselves to benefit from rising rates and may limit the backup in yields as they deploy their unused capital hoard into it. … and protect equities from suffering meaningful de-rating: All the money has to go somewhere, and equities may be the default winner if bonds and cash are poised to deliver negative real returns. The rosy near-term outlook implied by the biggest banks’ observations suggests that the bull market in risk assets isn’t over yet: Households have ramped up spending but have barely begun to tap into their excess savings and businesses are confident and well-heeled. Above-trend economic growth should bolster corporate earnings, credit performance and financial asset prices, keeping the bull market going through the end of the year. What The Banks See The SIFI banks (BAC, C, JPM and WFC) and USB kicked off fourth quarter earnings across three days bracketing the Martin Luther King long weekend. Their performance wasn’t bad – the SIFIs squarely beat analysts’ consensus estimates and USB came up about 3% short – but investors apparently wanted more from a group that had burst out of the gate to start 2022. Banks were market darlings in the year’s first nine sessions as investors sought out stocks that could outperform in a rising rate environment, and the SIFIs and USB beat the S&P 500 by 12 percentage points (Chart 1). Over the three sessions that they reported earnings, they gave back more than a third of their relative outperformance, though they still have a 7-point year-to-date advantage. Chart 1Rate Play

Rate Play

Rate Play