Financial Markets

As 2021 draws to a close, we thank you for your ongoing readership and support. We wish you and your loved ones a happy holiday season and all the best for a healthy and prosperous 2022. Highlights Over the coming three months, the odds are high that the Omicron variant of COVID-19 will disrupt economic activity in advanced economies, but the magnitude of the disruption will be heavily determined by the variant’s capacity to produce severe illness. For now, we remain of the view that the pandemic will recede in importance over the course of the next year. Relative to the assessment that we published in our 2022 Outlook report, the Omicron variant of COVID-19 has modestly raised the odds of a stagflationary outcome next year. Our base case view of above-trend growth and above-target inflation remains the most likely scenario for 2022. We do not think that the actual risk of a recession has risen significantly since we published our annual outlook, but we can envision a scenario in which Fed tightening causes investors to become fearful of a recession. The true risk of a monetary policy-induced recession over the coming 12-18 months will only rise if long-dated inflation expectations break above the range that prevailed prior to the Global Financial Crisis. Beyond 2022, the main risk to financial markets is that investors raise their longer-term interest rate expectations closer to the trend rate of economic growth. This would not be bad news for real economic activity, but it would imply meaningfully lower prices for financial assets that have benefited from low interest rates. We continue to advise that investors position themselves in line with the investment recommendations that we presented in our Outlook report. Over the coming year, investors should watch for the following when deciding whether to reduce exposure to risky assets: a breakout in long-dated inflation expectations, a significant flattening in the yield curve, or a rise in 5-year, 5-year forward US Treasury yields above 2.5%. Feature Our recently published 2022 Outlook report laid out the main macroeconomic themes that we see driving markets next year, as well as our cyclical investment recommendations.1 In this month’s report, we discuss the most relevant risks to our base case view in more depth, and update our fixed-income view in the wake of the December FOMC meeting. The Near-Term Risks Chart I-1DM Policymakers Are Afraid That Omicron Will Overwhelm The Medical System

DM Policymakers Are Afraid That Omicron Will Overwhelm The Medical System

DM Policymakers Are Afraid That Omicron Will Overwhelm The Medical System

Over the coming 0-3 months, the greatest risks to economic growth stem from the likely impact of the Omicron variant of COVID-19 on the medical system and the evolution of Europe’s energy crisis. News about the Omicron variant emerged just a few days prior to the publication of our annual outlook, and considerable uncertainty remains about its impact. Some early evidence suggests that the variant causes less severe disease, with a recent press release from South Africa’s largest private health insurance administrator suggesting that the risk of hospital admission was 29 percent lower for adults with the Omicron variant after adjusting for age, sex, underlying health conditions, and vaccine status. More recent studies from South Africa have suggested a much larger reduction in the severity of disease,2 but it is not yet clear whether these findings are applicable to advanced economies,given South Africa’s more recent vaccination campaign and higher proportion of a previously infected population. If Omicron turns out to result in 30 percent less hospitalizations, that only reduces the net impact on the medical system if the Omicron variant is no more than 1.5x as transmissible as the Delta variant. The sheer speed at which Omicron is spreading suggests it is far more contagious than this, the result in part to its ability to evade two-dose immunity. The potential for Omicron to quickly overwhelm available health system resources has alarmed authorities in several advanced economies, especially given that cases and hospitalizations have already trended higher in several countries even while Delta remained the dominant variant (Chart I-1). Additional restrictions on economic activity in the DM world appear to be likely over the coming weeks, and may be in effect until booster doses have been fully administered and/or Pfizer’s drug Paxlovid becomes widely available. For Europe, a worsening of the COVID situation has the potential to exacerbate the economic impact of the region’s ongoing energy crisis. Chart I-2 highlights that European natural gas prices have again exploded, reaching a new high that is fourteen times its pre-pandemic level. We noted in our Outlook report that European natural gas in storage is well below that of previous years, and Chart I-3 highlights that the gap in stored gas relative to previous years persists. This is occurring despite roughly average temperatures in central Europe over the past month (Chart I-4), underscoring that, barring atypically warmer temperatures, European natural gas prices are likely to remain elevated throughout the winter. Chart I-2Another Explosion In European Natural Gas Prices

Another Explosion In European Natural Gas Prices

Another Explosion In European Natural Gas Prices

Chart I-3

Chart I-5For Europe, COVID Is More Of A Problem Than Natural Gas Prices

For Europe, COVID Is More Of A Problem Than Natural Gas Prices

For Europe, COVID Is More Of A Problem Than Natural Gas Prices

Chart I-4

For now, it appears that the rise in COVID cases is having a more pronounced effect on the European economy than the energy price situation. Chart I-5 highlights that the flash December euro area manufacturing PMI fell only modestly, and that Germany’s manufacturing PMI actually rose in December. By contrast, the euro area services PMI fell over two points, reflecting the toll that recent pandemic control measures have taken on non-goods producing activity. Over the coming three months, the odds are high that the Omicron variant will disrupt economic activity in advanced economies to some degree, but the magnitude of the disruption will be heavily determined by the variant’s capacity to produce severe illness. Investors will have more information on hand in a few weeks by which to judge the extent of this risk. We will provide an update to our own assessment in our February report. Risks Over The Next Year In our Outlook report, we assigned a 60% chance to an above-trend growth and above-target inflation scenario next year, a 30% chance to a “stagflation-lite” scenario of growth at or below potential and inflation well above target, and a 10% chance of a recession. We present below our assessment of the risk that one of the latter two scenarios occurs in 2022. The Risk Of “Stagflation-Lite” Chart I-6Aside From Europe's Energy Crisis, Supply-Side Constraints Are Slowly Easing

Aside From Europe's Energy Crisis, Supply-Side Constraints Are Slowly Easing

Aside From Europe's Energy Crisis, Supply-Side Constraints Are Slowly Easing

The Omicron variant of COVID-19 has modestly raised the odds of a stagflationary outcome next year. Over the past few months, supply-side pressures have been modestly improving outside of Europe. Chart I-6 presents our new BCA Supply-Side Pressure Indicator, which measures the impact of supply-side restrictions across four categories: energy prices, shipping costs, the semiconductor shortage impact on automobile production, and labor availability. When we include all eleven components, the index has been trending higher of late, but trending flat-to-down after excluding European natural gas prices. While Omicron has the potential to reduce energy price pressure outside of Europe, it has the strong potential to cause a further increase in global shipping costs and postpone US labor market normalization. On the shipping cost front, we noted in our Outlook report that supply-side effects have been a significant driver of higher costs this year. The large rise in China/US shipping costs since late-June has been seemingly caused by the one-month closure of the Port of Yantian that began in late-May. While China has made enormous progress in vaccinating its population over the course of the year, and has prioritized the vaccination of workers in key industries, recent reports suggest that the Sinovac vaccine provides essentially no protection against contracting the Omicron variant of COVID-19. It is possible that Sinovac will offer protection against severe illness, but in terms of preventing transmission of the disease, Omicron has essentially returned China’s vaccination campaign back to square one. Chart I-7Further Price Increases May Seriously Slow Goods Spending

Further Price Increases May Seriously Slow Goods Spending

Further Price Increases May Seriously Slow Goods Spending

That fact alone makes it almost certain that China will maintain its zero-tolerance COVID policy for most of 2022, which significantly raises the risk of additional factory and port shutdowns – and thus even higher shipping costs and imported goods prices. One optimistic point is that these shutdowns are more likely to occur in mainland China than in Taiwan Province or Malaysia, two key semiconductor exporters. This is because these two regions have distributed doses of Pfizer’s vaccine, and thus presumably have the ability to provide three-dose mRNA protection to workers in crucial exporting industries (should policymakers choose to do so). Still, US consumer goods prices would clearly be impacted by even higher shipping costs, which would likely have the combined effect of slowing growth and raising prices. Chart I-7 highlights that the recent sharp deterioration in US households’ willingness to buy durable goods has been closely linked to higher goods prices, arguing that goods spending may slow meaningfully if prices rise further alongside renewed weakness in services spending. Omicron’s contagiousness may also exacerbate the ongoing US labor shortage. The shortage has occurred because of a surge in the number of retirees, difficult working conditions in several industries, and increased childcare requirements during the pandemic. The increase in the number of retirees has not happened for structural reasons; it has been driven by a sharp slowdown in the number of older Americans shifting from “retired” to “in the labor force”, which has occurred because of health concerns. None of these factors are likely to improve meaningfully while Omicron is raging, suggesting that services prices are likely to remain elevated or accelerate further even if services spending falls anew.

Chart I-8

To conclude on this point, we estimate that the odds of a stagflation-lite scenario have risen to 35% (from 30%), and the odds of our base-case scenario of above-trend growth and above-target inflation have fallen to 55% (Chart I-8). Still, our base-case view remains the most probable outcome, given that we do not believe the odds of a recession next year have risen. The Risk Of Recession We do not think that the actual risk of a recession has risen significantly since we published our annual outlook, but we can envision a scenario in which Fed tightening causes investors to become fearful of a recession. Such a scenario would have a material impact on cyclical investment strategy, and thus warrants a discussion. Following the December FOMC meeting, BCA’s baseline expectation is that a first Fed hike will occur in June 2022 and that rate increases will proceed at a pace of 25 basis points per quarter through the end of the year. BCA’s house view on this question is now in line with the view of The Bank Credit Analyst service, which published in a September Special Report that the Fed could hit its maximum employment objective as early as next summer.3 The Fed’s shift implies that the 2-year yield should rise to 1.85%, and the 10-year yield to 2.35%, by the end of next year (Chart I-9). Chart I-9A More Hawkish Fed Means A 2.35% 10-Year Yield Next Year

A More Hawkish Fed Means A 2.35% 10-Year Yield Next Year

A More Hawkish Fed Means A 2.35% 10-Year Yield Next Year

We doubt that US monetary policy will become economically restrictive next year. If the Omicron variant of COVID-19 causes a serious slowdown in economic activity, the Fed will ramp down its expectations for rate hikes. And if the Fed meets our baseline expectations for hikes next year in the context of above-trend economic growth, we do not believe that a 2.35% 10-year Treasury yield will be, in any way, limiting for economic activity. However, investors do not agree with our view about the boundary between easy and tight monetary policy, and may begin to fear a recession in response to Fed tightening next year. We noted in our Outlook report that we believe the neutral rate of interest (“R-star”) is likely higher that investors believe, but the fact remains that the Fed and market participants have judged, with deep conviction, that the neutral rate remains very low relative to the potential growth rate of the economy. Chart I-10 presents the fair value path of the 2-year Treasury yield based on our expectations for the Fed funds rate, alongside the actual 10-year Treasury yield. The chart highlights that the 2/10 yield curve could flatten significantly or even invert in the second half of 2022 if long-maturity yields rise only modestly in response to Fed tightening, which could occur if investors focus on the view that the neutral rate of interest is low and that Fed rate hikes will not prove to be sustainable. Based on two different measures of the yield curve, fixed-income investors believe that the current economic expansion is already 50-60% complete (Chart I-11), implying a recession at some point in the first half of 2023. Chart I-10The US Yield Curve Could Invert Next Year If Long-Maturity Yields Rise Only Marginally

The US Yield Curve Could Invert Next Year If Long-Maturity Yields Rise Only Marginally

The US Yield Curve Could Invert Next Year If Long-Maturity Yields Rise Only Marginally

Chart I-11More Than Half Of The Economic Expansion Has Already Occurred, According To The Yield Curve

More Than Half Of The Economic Expansion Has Already Occurred, According To The Yield Curve

More Than Half Of The Economic Expansion Has Already Occurred, According To The Yield Curve

Chart I-12A Serious Flattening In The Yield Curve Could Unnerve Stocks

A Serious Flattening In The Yield Curve Could Unnerve Stocks

A Serious Flattening In The Yield Curve Could Unnerve Stocks

If the yield curve were to flirt with inversion and investors began to price in the potential for a recession, it would cause significant financial market turmoil regardless of whether the risk of recession is real or not. Chart I-12 highlights that the S&P 500 fell 20% in late 2018 as the 2/10 yield curve flattened towards 20 basis points, in response to the economic impact of the China-US Trade War and the global impact of US tariffs on the auto industry. So it is possible that a “recessionary narrative” negatively impacts risky asset prices in the second half of 2022, even if an actual recession is ultimately avoided. Based on this, we would be much more inclined to reduce our recommended exposure to equities if the US 2/10 yield curve were to flatten below 30 basis points next year. In our view, the risk of a monetary policy-induced recession over the coming 12-18 months will only legitimately rise if long-dated inflation expectations break above the range that prevailed prior to the Global Financial Crisis. We noted in our Outlook report that this has not yet occurred for either household or market-based expectations, although it is a risk that cannot be ruled out. The odds of a breakout in long-dated inflation expectations will rise the longer that actual inflation remains elevated, and our inflation probability model suggests that core PCE inflation will remain well above 3% next year and potentially above 4% – although Chart I-13 highlights that the odds of the latter are falling. Chart I-13US Core Inflation Will Remain Well Above Target Next Year

US Core Inflation Will Remain Well Above Target Next Year

US Core Inflation Will Remain Well Above Target Next Year

A dangerous breakout in inflation expectations would raise the risk of a recession because of the Fed’s awareness of the “sacrifice ratio”, a very important economic concept that has been mostly irrelevant for the past 25 years. The sacrifice ratio is an estimate of the amount of output or employment that must be given up in order to reduce inflation by one percentage point. Table I-1 highlights some academic estimates of the sacrifice ratio, which have typically varied between 2-4% in output terms. For comparison purposes, real GDP has typically fallen no more than 2% on a year-over-year basis during most post-war US recessions. Real GDP growth fell 4% year-over-year in 2009, highlighting that the cost of reducing the rate of inflation by 1 percentage point is effectively a severe recession.

Chart I-

In his Senate testimony in late-November, Fed Chair Jay Powell noted that persistently high inflation threatens the economic recovery. He also implied that to reach its maximum employment goal, the Fed may need to act pre-emptively to tame inflation. This was implicit recognition of the sacrifice ratio, and should be seen as an expression of the Fed’s desire to avoid a scenario in which persistently high inflation causes inflation expectations to become unanchored (to the upside), as it would force the Fed to sacrifice economic activity in order to ensure price stability. By acting earlier to normalize monetary policy, the Fed hopes to keep inflation expectations well contained. Chart I-14Long-Dated Market-Based Inflation Expectations Are Not Out Of Control

Long-Dated Market-Based Inflation Expectations Are Not Out Of Control

Long-Dated Market-Based Inflation Expectations Are Not Out Of Control

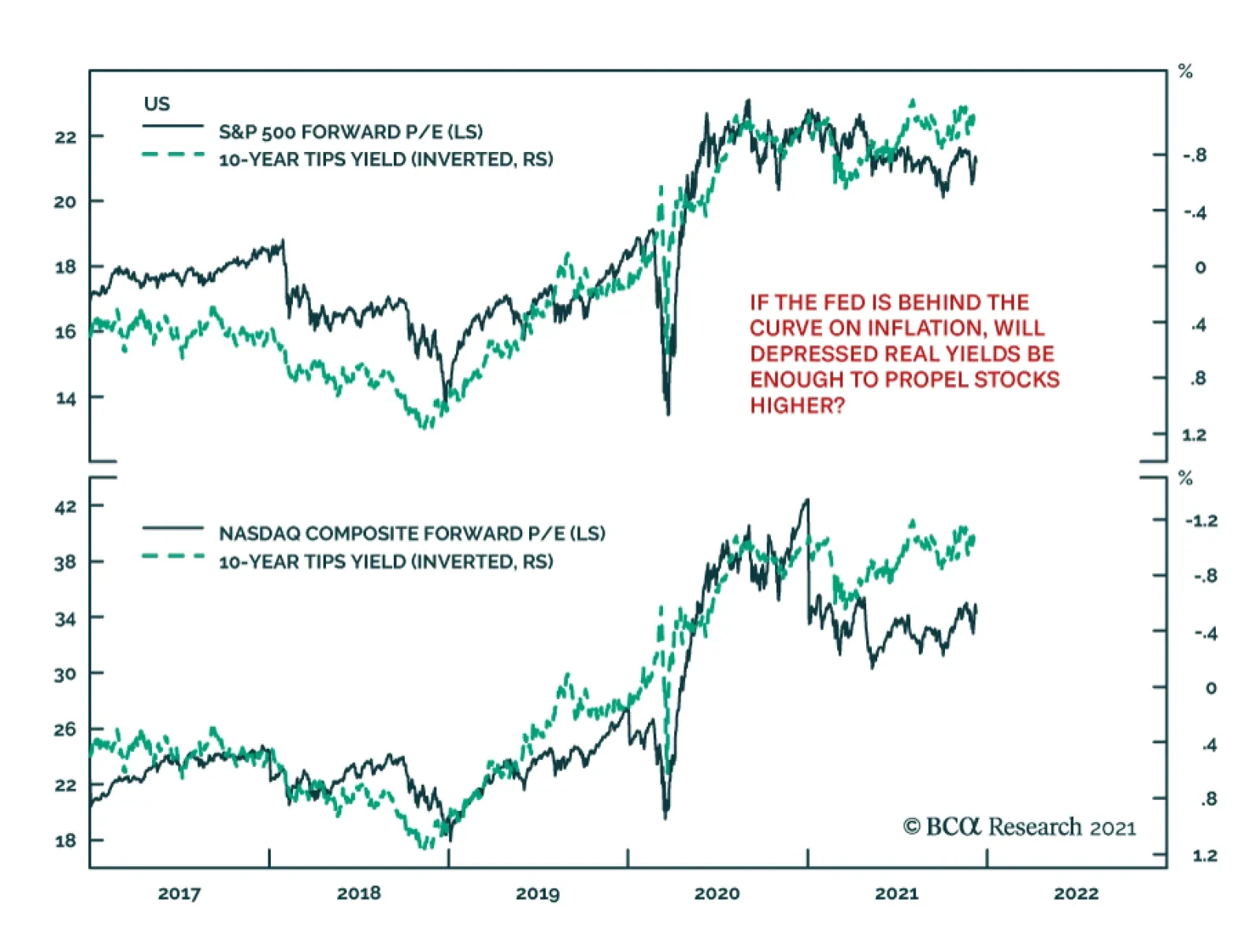

For now, we see no signs that the Fed will fail to keep inflation expectations from rising dangerously. Chart I-14 highlights that long-dated market expectations for inflation have been falling over the past two months, and are essentially at the same level that they were on average in 2018. Given this, we maintain the 10% odds of recession that we presented in our Outlook report, although investors will need to monitor inflation expectations closely over the coming year to judge whether the risks of a monetary policy-induced recession are indeed rising. Risks Beyond The Next Year Beyond 2022, the main risk to risky asset prices is probably not overly tight monetary policy. Instead, the risk is that investors will come to the conclusion that the Fed funds rate will ultimately end up rising above what the Fed is currently projecting, and that the economy will be capable of tolerating interest rates that are closer to the prevailing rate of economic growth. This would not be bad news for real economic activity, but it would imply meaningfully lower prices for financial assets that have benefited from low interest rates. Chart I-15US Stocks Would Suffer Significant Losses If Interest Rates Rise Towards Potential Growth

US Stocks Would Suffer Significant Losses If Interest Rates Rise Towards Potential Growth

US Stocks Would Suffer Significant Losses If Interest Rates Rise Towards Potential Growth

Chart I-15 drives the point home by comparing the current S&P 500 forward P/E ratio to a “justified” P/E. Here, we calculate the justified P/E using the average ex-ante equity risk premium (ERP) since 1980, and real potential GDP growth as a stand-in for the real risk-free rate of interest. The chart highlights that US stocks would experience a 30% contraction in equity multiples should real long-maturity bond yields approach 2%. A decline in the ERP could potentially reduce losses for equity holders in a higher interest rate scenario, but it is very likely that the net effect would still be negative for stocks. We detailed in our Outlook report why we believe that the neutral rate of interest is higher than most acknowledge. We agree that R-star fell in the US for a time following the Global Financial Crisis (GFC), but we strongly question that it is as low as the Fed and investors believe. The neutral rate of interest fell during the first half of the last economic cycle because of a persistent period of household deleveraging and balance-sheet repair, which was a multi-year consequence of the financial crisis and the insufficient fiscal response to the 2008-09 recession. We highlighted in our Outlook report that US household balance sheets have been repaired, and that the household debt service ratio has fallen to mid-1960s levels. However, Chart I-16 highlights that even the corporate sector, which has leveraged itself significantly over the past decade, has seen its debt service ratio plummet. In a scenario in which long-maturity Treasury yields were to rise to 4%, we estimate that the debt service burden of the nonfinancial corporate sector would rise to its 70th-80th percentile historically. Chart I-16The US Corporate Sector Debt Service Burden Has Room To Rise

The US Corporate Sector Debt Service Burden Has Room To Rise

The US Corporate Sector Debt Service Burden Has Room To Rise

That would be a meaningful increase from current levels, but it would not be unprecedented, and thus would not render a 4% 10-year Treasury yield to be economically unsustainable. In addition, we strongly suspect that corporations would reduce their interest burden in such a scenario by issuing equity to retire debt. That would lower firms’ debt burden and reduce the economic impact of higher interest rates, although it would be additionally negative for equity investors given that this would dilute earnings per share. We argued in our Outlook report that a shift in investor expectations about the neutral rate of interest is unlikely to occur before the Fed begins to normalize monetary policy. Ryan Swift, BCA’s US Bond Strategist, presented further evidence of this perspective in a Special Report earlier this week.4 Ryan highlighted results from a recent academic paper, which showed that the entire decline in the 10-year Treasury yield since 1990 has occurred during three-day windows centered around FOMC meetings (Chart I-17). Ryan argued that this suggests investors change their neutral rate expectations in response to Fed interest rate decisions, rather than in response to independent macroeconomic factors that are distinct from monetary policy action. This argues that a shift in neutral rate expectations is unlikely before the Fed begins to lift interest rates in the middle of the year, and probably not until the Fed has raised rates a few times. We are thus unlikely to recommend that investors reduce their equity exposure in response to this risk until 5-year, 5-year forward Treasury yields break above 2.5% (the Fed’s long-run Fed funds rate projection), which is 80 basis points above current levels (Chart I-18). Chart I-17Fed Rate Decisions Drive Long-Maturity Bond Yields

Fed Rate Decisions Drive Long-Maturity Bond Yields

Fed Rate Decisions Drive Long-Maturity Bond Yields

Chart I-18We Will Consider Selling Stocks If Market-Based Neutral Rate Estimates Exceed 2.5%

We Will Consider Selling Stocks If Market-Based Neutral Rate Estimates Exceed 2.5%

We Will Consider Selling Stocks If Market-Based Neutral Rate Estimates Exceed 2.5%

Investment Conclusions We continue to advise that investors position themselves in line with the investment recommendations that we presented in our Outlook report. Over the following 12-months, we expect the following: Global stocks to outperform bonds Short-duration fixed-income positions to outperform long High-yield corporate bonds to outperform within fixed-income portfolios Value stocks to outperform growth Non-resource cyclicals to outperform defensives Small caps to outperform large A modest rise in commodity prices led by oil A decline in the US dollar However, our discussion of the risks to our views has highlighted three things for investors to monitor next year when deciding whether to reduce exposure to stocks (and risky assets more generally): A breakout in long-dated inflation expectations, as that would likely cause the Fed to raise interest rates more aggressively than it currently projects. A significant flattening in the yield curve, as that would indicate that investors ultimately expect existing Fed rate hike projections to prove recessionary. A rise in 5-year, 5-year forward US Treasury yields above 2.5%, as that would indicate that investors may be upwardly shifting their expectations for the neutral rate of interest. Over the shorter-term, our discussion also underscored that the Omicron variant will likely disrupt economic activity to some degree over the coming three months, and that the risks of a stagflation-lite scenario next year have modestly increased because of the likely maintenance of China’s zero-tolerance COVID policy. We continue to expect that the widespread rollout of booster doses, as well as the progressive availability of effective and safe antiviral drugs, will limit Omicron’s impact on economic activity to the first half of 2022, and that the pandemic will recede in importance next year on average in comparison to 2021. As noted above, this assessment will be monitored continually in response to the release of new information, and we will provide an update in our February report. Jonathan LaBerge, CFA Vice President The Bank Credit Analyst December 23, 2021 Next Report: January 27, 2022 II. Stock Buybacks – Much Ado About Nothing Dear Client, This month’s Special Report is a guest piece by Doug Peta, BCA Research’s Chief US Investment Strategist. Doug’s report examines the impact of US stock buybacks using a median bottom-up approach, and presents a different perspective of the value vs. growth distribution of buybacks than we did in our October Section 2. I trust you will find his report interesting and insightful. Jonathan LaBerge, CFA The Bank Credit Analyst Elected officials’ antipathy for buybacks is unfounded, … : For the companies that are the primary drivers of buyback activity, returning cash to shareholders is more likely to have a positive impact on employment and investment than retaining it. and the idea that they boost stock returns may be, as well, … : Over the last ten years, a cap-weighted bucket of large-cap stocks that most reduced their share counts underperformed the bucket that most increased their share counts by 2% annually. especially within the Tech sector, which has most enthusiastically executed them: Despite the success of Apple, which has seen its market cap soar since embarking on a deliberate strategy to shrink its shares outstanding, a strategy buying Tech’s biggest net reducers and selling its biggest net issuers would have generated sizable negative alpha over the last ten years. The problem is the relative profile of net buyers and net issuers: In general, companies that consistently buy back their own stock are mature companies that cannot earn an accretive return by redeploying the capital their incumbent business generates. Net issuers, on the other hand, are often young companies seeking fresh capital to realize their abundant growth opportunities. The next year is likely to see a pickup of share buybacks nonetheless, … : Our US Equity Strategy service’s Cash Yield Prediction Model points to increased buyback activity in 2022. … as management teams are wedded to them and buying back stock is the best use of capital for the mature companies executing them: Better to return cash to shareholders than to enter new business lines beyond the company’s area of expertise or embark on dubious acquisitions, even in the face of a potential 1% surtax. In Capitol Hill’s current polarized state, stock buybacks are in select company with the tech giants and China as issues that unite solons on both sides of the aisle. They are also a hot-button issue for some investors, who see them as telltale signs of a market kept aloft by sleight of hand. Although we do not think they’re worth getting worked up over – they do not promote the misallocation of capital and they may not actually boost stock prices – they come up repeatedly in client discussions and are likely to remain a feature of the landscape even if they are eventually subjected to a modest federal surtax. We have therefore joined with the BCA Equity Analyzer team to pore over its bottom-up database for insights into the buyback phenomenon. After ranking nearly 600 stocks in our large-cap universe in order of their rolling 12-month percentage change in shares outstanding across the last ten years, we were surprised to discover that the companies that most reduced their share count underperformed the companies that most grew it. We were also surprised to find that Tech was by far the worst performer among the six sectors with negative net issuance. Ultimately, the performance story seemed to boil down to Growth stocks’ extended recent edge over Value stocks. We present the data, our interpretation of it, and some future investment implications in this Special Report. Buybacks’ Bad Rap From Capitol Hill to the White House, prominent Washington voices bemoan buybacks. In a February 2019 New York Times opinion piece,5 Senators Sanders (I-VT) and Schumer (D-NY) argued that equity buybacks divert resources from productive investment in the narrow interest of boosting share prices for the benefit of shareholders and corporate executives. To counter the increasing popularity of buybacks, they proposed legislation that would permit buybacks only after several preconditions for investing in workers and communities had been met. Echoing their concerns, the White House's framework for the Build Back Better bill included a 1% surcharge on stock buybacks, “which corporate executives too often use to enrich themselves rather than investing in workers and growing the economy.” Chart II-1The Smallest Companies Sell Stock; The Largest Buy It Back

The Smallest Companies Sell Stock; The Largest Buy It Back

The Smallest Companies Sell Stock; The Largest Buy It Back

Buybacks’ opponents may mean well, but they seem to be missing an essential point: by and large, the companies that buy back their own stock lack enough attractive investment opportunities to absorb the cash their operations generate. Companies with more opportunities than cash don’t buy back stock; they issue it (and/or borrow) to get the capital to pursue them. The simple generalization that large, mature companies buy back shares while small, growing companies issue new ones is borne out by rolling 12-month percentage changes in shares outstanding by large-cap and small-cap companies (Chart II-1). On an equal-weighted basis, large-cap companies’ rolling share count was flat to modestly down for ten years before the pandemic drove net issuance. Adjusting for market cap, rolling net issuance has been uninterruptedly negative, shrinking by more than 2% per year, on average. The equally weighted small-cap population has been a net issuer to the tune of about 4% annually, with the biggest small-caps issuing even more, pushing the cap-weighted annual average to north of 6%. The bottom line is that large-cap companies in the aggregate have been modestly trimming their share counts, with the biggest companies retiring more than 2% of their shares each year, while small-cap companies are serial issuers, led by their largest (and presumably most bankable) constituents. We are investors serving investors, not policymakers, academics or editorial columnists charged with developing and evaluating public policy. Our mandate is bullish or bearish, not good or bad. We point out the flaws in the prevailing criticism of buybacks simply to make the point that buybacks are not an impediment to productive investment and that no one should therefore expect that productivity and income will rise if legislators or regulators restrict them. On the contrary, since we believe that buybacks represent an efficient allocation of capital, we would expect that successful attempts to limit them will hold back growth at the margin. The Buyback Calculus A company that buys back more of its shares than it issues reduces its share count. All else equal, a company with fewer shares outstanding will report greater earnings per share and a higher return on equity. Increased earnings per share (EPS) does not necessarily ensure a higher share price; if a company’s P/E multiple declines by more than EPS rises, its price will fall. Distributing retained earnings to shareholders reduces a company’s capital buffer against shocks and limits its ability to fund investment internally, but companies that embark on the most ambitious buyback campaigns likely face limited investment opportunities and have much more of a buffer than they could conceivably require. Revealed preferences suggest that management teams like buybacks. They have every interest in getting share prices higher to maximize the value of their own compensation, which typically contains an equity component that accounts for an increasing share of total compensation the more they rise in the company’s hierarchy. It is unclear, however, just how much their attachment to buybacks is founded on an expectation that buying back stock will boost its price. The opportunity to extend their tenure by pursuing a shareholder-friendly policy may well offer a stronger incentive. Do Buybacks Boost Share Prices? Returning cash to shareholders is widely perceived as good corporate governance. It increases the effective near-term yield on an equity investment and denies management the cash to pursue dubious expansion schemes or squander capital on lavish perquisites. It facilitates the reallocation of capital away from cash cows to more productive uses. Buybacks are squarely beneficial in theory, but are they good for investors in practice? (Please see the Box II-1 for a description of the methodology we followed to answer the empirical question.) Box II-1 Performance Calculation Methodology After separating stocks into large- and small-cap categories based on Standard & Poor’s market cap parameters for inclusion in the S&P 500 and the SmallCap 600 indexes, we ranked the constituents in each category in reverse order of their rolling 12-month percentage change in shares outstanding at the end of each month from 2011 through 2021. We then placed the top three deciles (the biggest reducers of their share counts) into the High Buybacks bucket and the bottom three deciles (the biggest net issuers) into the Low Buybacks bucket. We used the buckets to backtest a zero-net-exposure strategy of buying the stocks in the High bucket with the proceeds from shorting the stocks in the Low bucket, calling it the High-Minus-Low (“HML”) strategy. We computed two sets of HML results for the large-cap and small-cap universes. The first populated the buckets without regard for sector representation (“sector-agnostic”) and the second populated the buckets in line with the sector composition of the S&P 500 and SmallCap 600 Indexes (“sector-neutral”). We also track equal-weighted and cap-weighted versions of each HML bucket to gain a sense of performance differences between constituents by size. The experience of the last ten years fails to support the widely held view that stock buybacks boost share prices. Following a zero-net-exposure strategy of owning the top three deciles of large-cap companies ranked by the rolling 12-month percentage reduction of shares outstanding and shorting the bottom three deciles generated a modest positive annual return above 1% (Chart II-2). Small caps merely broke even, largely because their biggest share reducers sharply underperformed in Year 1 of the pandemic. On a cap-weighted basis, however, the large-cap strategy generated a negative annual return a little over 1% during the period, indicating that the largest companies pursuing buyback programs lagged their net issuer counterparts. For small caps, the cap-weighted strategy also lagged the equal-weighted strategy, albeit by a smaller margin. On a sector-neutral basis, the large-cap HML strategy roundly disappointed. The equal-weighted version was never able to do much more than break even, slipping into the red when COVID arrived, while the cap-weighted version continuously lagged it, shedding about 1.5% annually (Chart II-3). Though it was hit hard by the pandemic, the equal-weighted small-cap HML strategy managed to generate about 1% annually, and boasted a 3.5% annualized return for the eight years through 2019. Chart II-2Buybacks May Help A Company's Stock Price At The Margin ...

Buybacks May Help A Company's Stock Price At The Margin ...

Buybacks May Help A Company's Stock Price At The Margin ...

Chart II-3... But They Are Not An Exploitable Factor

... But They Are Not An Exploitable Factor

... But They Are Not An Exploitable Factor

Drilling down to the sector level offers some additional insights. While changes in shares outstanding vary across large-cap sectors, with six sectors reducing their shares outstanding and five expanding them, every small-cap sector has been a net issuer in every single year, ex-Discretionaries and Industrials in 2019 (Chart II-4). Relative sector capital needs are largely consistent regardless of market cap, however, with REITs, which distribute all their income to preserve their tax-free status, unable to expand without raising cash in the capital markets, and Utilities, Energy and traditional Telecom Services being capital-intensive industries (Table II-1). Many Tech niches are capital-light, and established Industrials and Consumer businesses often throw off cash.

Chart II-4

Chart II-

There is less large- and small-cap commonality in HML relative sector performance than in relative sector issuance. Away from Real Estate, Tech and Discretionaries, small-cap HML sector strategies generated aggregate positive returns, led by Communication Services and Energy (Chart II-5). For the large caps, most HML sector strategies produced negative alpha, though the four winners and the one modest loser (Financials) are among the six sectors that have net retired shares outstanding since 2012. Tech is the conspicuous exception, with its HML strategy yielding annualized losses exceeding 3%, contrasting with the sector’s enthusiastic buyback embrace.

Chart II-5

The Corporate Life Cycle Surprising as they may be on their face, negative cap-weighted ten-year HML returns do not mean that buybacks are counterproductive. We simply think they illustrate that net issuance activity follows from a company’s position in the corporate life cycle (Figure II-1). Investors have prized growth in the aftermath of the global financial crisis, and the companies with the best growth prospects are often younger companies just beginning to tap their addressable markets. They have a long pathway of market share capture ahead of them and need to raise capital to begin traveling it. Many of these strong growers populate the Low basket, especially in the Tech sector.

Chart II-

Chart II-

Companies that return cash to their owners via share repurchases are often more mature. Their operations are comfortably profitable and generate more than enough cash to sustain them. They have already captured all the market share they’re likely to gain in their primary business and may not have an outlet for its proceeds in a space in which they have a plausible competitive advantage. Lacking a clear path to bettering the returns from their main operations, they have been steadily accumulating cash for a long time. Through the lens of the Boston Consulting Group’s (BCG) growth share matrix,6 a successful business in the Maturity stage of the business life cycle is known as a Cash Cow. Cash Cows have gained considerable market share in their industry, affording them a competitive advantage based on scale, brand and experience, but little scope for growth because they have saturated a market that is itself mature (Figure II-2). BCG advises management teams with a portfolio of business lines to milk Cash Cows for capital to reinvest in high-share, high-growth-potential Stars or low-share, high-growth-potential Question Marks that could be developed into Stars. In the public markets, a mature large-cap company that retains its excess capital impedes its owners’ ability to redeploy that capital to faster growing investments, subverting the overall economy’s ability to redirect capital to its best uses. Walmart, Twentieth-Century Growth Darling Chart II-6From Young Turk To Respected Elder

From Young Turk To Respected Elder

From Young Turk To Respected Elder

Walmart fits the business life cycle framework to a T and has evolved into a textbook Cash Cow. It is a dominant player that executed its initial strategy so well that it has maxed out its share in the declining/stagnating brick-and-mortar retail industry. Its international attempts to replicate its domestic success have uniformly failed to gain traction, and it currently operates in fewer major countries than it's exited. Given Walmart’s star-crossed international experience and the dismal history of large corporate combinations, returning cash may be the optimal use of shareholder capital. Walmart began life as a public company in fiscal 1971 squarely in the Growth phase. It was profitable from the start and grew annual revenues by at least 25% for every one of its first 23 years of public ownership (Chart II-6, top panel). It was a modest issuer of shares during its Growth phase, conducting just one secondary common stock offering 12 years after its IPO and otherwise limiting growth in shares outstanding to acquisitions, management incentive awards and debt and preferred stock conversions. Once its revenue growth slipped into the low double-digits in the late nineties, it began retiring its shares at a deliberate pace (Table II-2). That retirement inaugurated a ramping up of Walmart’s annual payout ratio (Chart II-6, bottom panel) and cash yield (dividend yield plus buyback yield), underlining its transition from Growth to Maturity. Walmart’s 2010 admission into the S&P 500 Pure Value Index marked its ripening into full maturity, and it has been a Pure Value fixture since 2013. Today’s stolid icon is a far cry from the ambitious disruptor on display in its 1980 Annual Report:

Chart II-

Subsequent to year end, your Company’s directors authorized [a one-third] increase in the annual dividend[.] This continues your Company’s approach of distributing a portion of profits to our shareholders and utilizing the balance to fund our aggressive expansion program. [T]he decade of the ’70’s … has been a tremendous growth period for your Company. In January 1970, we … had 32 stores …, comprising less than a million square feet of retail space. In the next ten years, we added 258 … stores, … constructed and opened three new distribution facilities, and increased our retail space to 12.6 million square feet. During that same period of time, we increased our sales and earnings at an annual compounded rate well in excess of 40 percent. Reflecting upon the progress we have made in the ‘70’s makes it apparent that there is even more opportunity in the ‘80’s for your Company, and we are better positioned to maximize our opportunities … than ever before. The Exception That Proves The Rule Apple has shined so far in the twenty-first century much like Walmart did in the latter stages of the twentieth, growing its revenues and net income at compound annual rates exceeding 20% and 25%, respectively. Unlike Walmart, however, Apple hasn’t required a steady stream of capital to grow. While Walmart had to plow its earnings right back into the business to fund the acquisition and buildout of property to create stores, warehouses and distribution centers, Apple has simply had to make incremental improvements to its music players, phones and tablets while shoring up the moats around its virtual app and music marketplaces. As a result, cash and retained earnings began silting up on Apple’s balance sheet, lying fallow in short-term marketable securities and crimping a range of return metrics.

Chart II-

Beginning in its 2013 fiscal year, Apple embarked on a lengthy strategy of returning that cash to shareholders, buying back stock at a rate that has allowed it to reduce its shares outstanding by 37.5% in the space of nine years (Table II-3). It has reduced its retained earnings by more than $90 billion over that span and is on course to wipe them out completely in the fiscal year ending next September. Equity issuance in the form of incentive compensation augments Apple’s capital by about $5 billion per year, but if it continues to distribute more than 100% of its annual earnings in the form of dividends and repurchases, it could wipe out the rest of its recorded equity capital as well. Does this mean Apple is in danger of sliding into insolvency? Not in the least. The value of its assets dramatically exceeds the value of its liabilities, as evidenced by its nearly $3 trillion market cap and the top AAA credit rating Moody’s awarded it this week. Its reported book value is artificially suppressed by generally accepted accounting principles’ inability to value organically developed intellectual property (IP). Apple’s book value and that of other companies that generate similar IP, or benefit from internally generated moats, are dramatically undervalued. Takeaways For now, Apple is an anomaly when it comes to aggressively returning cash to shareholders while it is still in the Growth stage of its life cycle. Returning cash is typically the province of mature companies with steady operations that are unlikely to grow. It is generally good for the economy when those companies return excess cash to shareholders, freeing it up for more productive uses. If lawmakers or regulators manage to restrict the flow of capital from cash-cow companies to potential stars, we should expect activity to slow at the margin, not quicken. The experience of the last ten years suggests that companies that shrink their share counts do not outperform their counterparts that expand them. The trading strategy of shorting the biggest net share issuers to purchase the biggest net share reducers has produced negative returns. It is unclear if shareholders of companies who cannot redeploy their internally generated capital to augment the returns from their primary operations would be better served if their manager-agents retained the capital, though we suspect they would not. It seems inevitable that manager-agents with access to too much capital will eventually get into mischief. If buying back stock represents good corporate stewardship at mature companies, their shareholders should someday be rewarded for it. Given that the companies most suited to buying back stock tend to fit in the Value style box, the zero-net-exposure HML strategy may continue to accrue losses. Apple remains an outlier among Growth companies as an avid buyer of its stock; much more common are the S&P 500 Life and Multi-Line Insurer sub-industry groups, without which the S&P 500 Pure Value Index would have a hard time reaching a quorum (Table II-4). Their constituents have assiduously bought back their stock over the last ten years, albeit to no relative avail (Chart II-7). However, they should be better positioned once Value returns to favor and rising interest rates make investing their cash flow a more attractive proposition.

Chart II-

Chart II-7... But No One Else Seems To Want To

... But No One Else Seems To Want To

... But No One Else Seems To Want To

Doug Peta, CFA Chief US Investment Strategist III. Indicators And Reference Charts BCA’s equity indicators highlight that the “easy” money from expectations of an eventual end to the pandemic have already been made. Our technical, valuation, and sentiment indicators remain very extended, highlighting that investors should expect positive but modest returns from stocks over the coming 6-12 months. Our monetary indicator has retreated below the boom/bust line, although this mostly reflects the use of producer prices to deflate money growth. In nominal terms, the supply of money continues to grow. Still, the retreat in the indicator over the past year highlights that the monetary policy stance is likely to move in a tighter direction over the coming year, which is in line with the Fed’s recent hawkish shift. Forward equity earnings are pricing in a substantial further rise in earnings per share. Net earnings revisions and net positive earnings surprises are rolling over, but there is no meaningful sign of waning forward earnings momentum. Bottom-up analyst earning expectations remain too high, but stocks are likely to be supported by robust revenue growth over the coming year. Within a global equity portfolio, we continue to recommend that investors position for the underperformance of financial assets that are negatively correlated with long-maturity government bond yields. The US 10-Year Treasury Yield remains well below the fair value implied by a mid-2022 rate hike scenario, underscoring that a move higher over the coming year is quite likely. Commodity prices remain elevated, and our composite technical indicator highlights that they remain overbought. An eventual slowdown in US goods spending, coupled with eventual supply-chain normalization and the absence of a significant reflationary impulse from Chinese policy, could weigh on commodity prices at some point over the coming 6 months. We expect stronger metals prices in the back half of 2022. US and global LEIs remain very elevated but have started to roll over. Our global LEI diffusion index has declined very significantly, but this likely reflects the outsized impact of a few emerging market countries (whose vaccination progress is still lagging). Still-strong leading and coincident indicators underscore that the global demand for goods is robust, and that output is below pre-pandemic levels in most economies because of very weak services spending. The latter will recover significantly at some point over the coming year, as the severity of the pandemic wanes. EQUITIES: Chart III-1US Equity Indicators

US Equity Indicators

US Equity Indicators

Chart III-2Willingness To Pay For Risk

Willingness To Pay For Risk

Willingness To Pay For Risk

Chart III-3US Equity Sentiment Indicators

US Equity Sentiment Indicators

US Equity Sentiment Indicators

Chart III-4US Stock Market Breadth

US Stock Market Breadth

US Stock Market Breadth

Chart III-5US Stock Market Valuation

US Stock Market Valuation

US Stock Market Valuation

Chart III-6US Earnings

US Earnings

US Earnings

Chart III-7Global Stock Market And Earnings: Relative Performance

Global Stock Market And Earnings: Relative Performance

Global Stock Market And Earnings: Relative Performance

Chart III-8Global Stock Market And Earnings: Relative Performance

Global Stock Market And Earnings: Relative Performance

Global Stock Market And Earnings: Relative Performance

FIXED INCOME: Chart III-9US Treasurys And Valuations

US Treasurys And Valuations

US Treasurys And Valuations

Chart III-10Yield Curve Slopes

Yield Curve Slopes

Yield Curve Slopes

Chart III-11Selected US Bond Yields

Selected US Bond Yields

Selected US Bond Yields

Chart III-1210-Year Treasury Yield Components

10-Year Treasury Yield Components

10-Year Treasury Yield Components

Chart III-13US Corporate Bonds And Health Monitor

US Corporate Bonds And Health Monitor

US Corporate Bonds And Health Monitor

Chart III-14Global Bonds: Developed Markets

Global Bonds: Developed Markets

Global Bonds: Developed Markets

Chart III-15Global Bonds: Emerging Markets

Global Bonds: Emerging Markets

Global Bonds: Emerging Markets

CURRENCIES: Chart III-16US Dollar And PPP

US Dollar And PPP

US Dollar And PPP

Chart III-17US Dollar And Indicator

US Dollar And Indicator

US Dollar And Indicator

Chart III-18US Dollar Fundamentals

US Dollar Fundamentals

US Dollar Fundamentals

Chart III-19Japanese Yen Technicals

Japanese Yen Technicals

Japanese Yen Technicals

Chart III-20Euro Technicals

Euro Technicals

Euro Technicals

Chart III-21Euro/Yen Technicals

Euro/Yen Technicals

Euro/Yen Technicals

Chart III-22Euro/Pound Technicals

Euro/Pound Technicals

Euro/Pound Technicals

COMMODITIES: Chart III-23Broad Commodity Indicators

Broad Commodity Indicators

Broad Commodity Indicators

Chart III-24Commodity Prices

Commodity Prices

Commodity Prices

Chart III-25Commodity Prices

Commodity Prices

Commodity Prices

Chart III-26Commodity Sentiment

Commodity Sentiment

Commodity Sentiment

Chart III-27Speculative Positioning

Speculative Positioning

Speculative Positioning

ECONOMY: Chart III-28US And Global Macro Backdrop

US And Global Macro Backdrop

US And Global Macro Backdrop

Chart III-29US Macro Snapshot

US Macro Snapshot

US Macro Snapshot

Chart III-30US Growth Outlook

US Growth Outlook

US Growth Outlook

Chart III-31US Cyclical Spending

US Cyclical Spending

US Cyclical Spending

Chart III-32US Labor Market

US Labor Market

US Labor Market

Chart III-33US Consumption

US Consumption

US Consumption

Chart III-34US Housing

US Housing

US Housing

Chart III-35US Debt And Deleveraging

US Debt And Deleveraging

US Debt And Deleveraging

Chart III-36US Financial Conditions

US Financial Conditions

US Financial Conditions

Chart III-37Global Economic Snapshot: Europe

Global Economic Snapshot: Europe

Global Economic Snapshot: Europe

Chart III-38Global Economic Snapshot: China

Global Economic Snapshot: China

Global Economic Snapshot: China

Jonathan LaBerge, CFA Vice President The Bank Credit Analyst Footnotes 1 Please see The Bank Credit Analyst "OUTLOOK 2022: Peak Inflation – Or Just Getting Started?", dated December 1, 2021, available at bca.bcaresearch.com 2 Early assessment of the clinical severity of the SARS-CoV-2 Omicron variant in South Africa by Wolter et al., medRxiv preprint, December 21, 2021. 3 Please see The Bank Credit Analyst “The Return To Maximum Employment: It May Be Faster Than You Think”, dated August 26, 2021, available at bca.bcaresearch.com 4 Please see US Bond Strategy “The Fed In 2022”, dated December 21, 2021, available at bca.bcaresearch.com 5 Opinion | Schumer and Sanders: Limit Corporate Stock Buybacks - The New York Times (nytimes.com) Accessed December 17, 2021. 6 https://www.bcg.com/about/overview/our-history/growth-share-matrix Accessed December 19, 2021. EQUITIES:FIXED INCOME:CURRENCIES:COMMODITIES:ECONOMY:

Highlights Below-Benchmark Portfolio Duration: Bond investors should keep portfolio duration low in 2022. While the market’s pricing of the expected Fed liftoff date and initial pace of rate hikes is reasonable, terminal fed funds rate expectations are far too low. Own Treasury Curve Steepeners: The 2/10 Treasury slope will flatten by less than what is currently discounted in the forward curve in 2022. Investors should position for this by going long the 2-year note versus a duration-matched barbell consisting of cash and the 10-year note. Sell Short-Maturity TIPS: Investors should maintain a neutral allocation to long-maturity TIPS versus nominal Treasuries and an underweight allocation to short-maturity TIPS versus nominal Treasuries. We also recommend an outright short position in 2-year TIPS, as short-maturity real yields have a lot of upside in 2022. Overweight Corporate Bonds Versus Treasuries … For Now: We are overweight corporate bonds versus duration-matched Treasuries, for now, but expect to turn more defensive in the first half of 2022 once the yield curve sustainably moves into a flatter regime. Relative valuations suggest that investors should favor high-yield corporates over investment grade. Overweight Emerging Market Bonds Versus US Corporates: EM bonds offer an attractive spread advantage versus US corporates, and a weakening US dollar will help boost returns in 2022. A Maximum Overweight Allocation To Municipal Bonds: Municipal bonds offer exceptional value, especially at the long-end of the curve, and state & local government balance sheets are in excellent shape. Underweight Agency MBS: Agency Mortgage-Backed Securities don’t adequately compensate investors for the likely pace of refi activity in 2021. An up-in-coupon stance is also advisable to take advantage of rising bond yields. Feature BCA published its 2022 Outlook on December 1st. That report lays out the main macroeconomic themes that our strategists see driving markets next year. This Special Report explains how investors can profit from those themes in US fixed income markets. Specifically, we offer seven key US fixed income views for 2022. This report is limited to the seven key investment views, and only discusses Fed policy in the context of how it influences those views. Next week we will publish a more comprehensive “Fed In 2022” report that will delve into our outlook for the Fed next year. Outlook Summary First, a summary of the main economic views presented in BCA’s 2022 Outlook.1 On Economic Growth: The COVID-19 pandemic will recede in importance in 2022 allowing US economic growth to remain above trend. Sizeable household savings and wealth will support consumer spending, the composition of which will shift away from goods and towards services. Corporate capital expenditures also look set to surge. On Inflation: A transition in consumer spending from goods to services and an increase in labor supply will cause US inflation to fall in 2022, though it will remain above the Fed’s target. On Fed Policy: The first Fed rate hike will occur between June and December 2022, depending on the paths of inflation and inflation expectations during the next few months. Fed tightening will continue into 2023. On China and Emerging Markets: Further policy easing in H1 2022 will lead to a reacceleration in Chinese economic activity in the back half of the year. The BCA house view is negative on EM equities for now but will turn more bullish when clearer signs of Chinese policy easing emerge. Risks To The Outlook: The greatest risk to the outlook is that the spread of the Omicron variant leads to the re-imposition of public health measures that will weigh on economic activity. The effect of the Omicron variant remains uncertain, but increasingly widespread vaccination and the advent of anti-viral treatments should help mitigate any negative economic impacts. Key View #1: Below-Benchmark Portfolio Duration Bond investors should keep portfolio duration low in 2022, favoring the 2-year maturity over the 10-year. While the market’s pricing of the expected Fed liftoff date and initial pace of rate hikes is reasonable, terminal fed funds rate expectations are far too low. Our recommendation to keep portfolio duration low in 2022 stems directly from our assessment of Federal Reserve policy. Without going into too much detail – we will do that in next week’s “Fed In 2022” report – the Fed appears to have adopted a more hawkish reaction function during the past month. The Fed’s official forward guidance says that it will not lift rates until the labor market reaches “maximum employment”. However, Fed Chair Jay Powell weakened that commitment in recent Senate testimony. Powell said that persistently high inflation threatens the economic recovery and implied that to reach its maximum employment goal the Fed may need to act pre-emptively to tame inflation. To us, this means that the Fed’s “maximum employment” condition for lifting rates is no longer binding. The Fed will accelerate the pace of tapering when it meets this week and will start lifting rates between June and December of next year, depending on the interim trends in inflation and inflation expectations. After liftoff, Fed rate hikes will proceed at a predictable pace of 75-100 bps per year until economic growth slows significantly. We expect the fed funds rate to reach at least 2% before that occurs, consistent with survey estimates of the long-run neutral fed funds rate. Let’s compare our estimate of the future fed funds rate path with what is currently priced in the bond market (Chart 1). Chart 1The Market's Rate Expectations

The Market's Rate Expectations

The Market's Rate Expectations

Liftoff The overnight index swap (OIS) curve is priced for Fed liftoff in May 2022. This is a tad early compared to our projections, but not by much. Pace After liftoff, the OIS curve is priced for the fed funds rate to rise 79 bps during the subsequent 12 months. Again, this is roughly consistent with our own expectations that the Fed will deliver three or four 25 basis point rate hikes per year. Terminal Rate It is the market’s pricing of the endpoint of the next tightening cycle – the terminal fed funds rate – that disagrees significantly with our forecast. The OIS curve is priced for the funds rate to reach 1.5% in 2024 and then stabilize. This is too low. It is too low compared to the last tightening cycle when the fed funds rate reached 2.45% in 2019. It is also too low compared to survey estimates from market participants and primary dealers. The median respondent to the New York Fed’s Survey of Market Participants estimates that the long-run neutral fed funds rate is 2%. The median response to the same question from the Survey of Primary Dealers is 2.25% and the median FOMC participant pegs the long-run neutral rate at 2.5%. Meanwhile, the 5-year/5-year forward Treasury yield – a rough proxy for the long-run neutral interest rate that’s priced in the Treasury market – sits at only 1.73%. Historically, the 5-year/5-year forward yield converges with survey estimates of the long-run neutral rate as the Fed moves toward tightening (Chart 2). This means the 5-year/5-year forward Treasury yield has at least 27-52 bps of upside in 2022. Chart 25y5y Has Room To Rise

5y5y Has Room To Rise

5y5y Has Room To Rise

Treasury Yield Forecasts Chart 3Treasury Yield Forecasts

Treasury Yield Forecasts

Treasury Yield Forecasts

Chart 3 shows the 2-year, 5-year and 10-year Treasury yields along with the expected paths that are discounted in the forward curve for the next 12 months. The shaded regions in each panel represent our fair value estimates of where those yields will trade if the market moves to price-in our expected future path for the fed funds rate. The upper bound of the fair value range represents the most hawkish fed funds rate scenario that we think is feasible. It assumes that Fed liftoff occurs in June, that rate hikes proceed at a pace of 100 bps per year and that the fed funds rate levels-off at a terminal rate of 2.08% (8 bps above the lower-end of a 2%-2.25% target range). The lower bound of the fair value range represents the most dovish fed funds rate scenario that we think is feasible. It assumes that Fed liftoff occurs in December 2022, that rate hikes proceed at a pace of 75 bps per year and that the fed funds rate levels-of at a terminal rate of 2.08%. Chart 3 shows that the 10-year Treasury yield is well below even the lower-end of our fair value range. The 5-year Treasury yield is a bit too low compared to our target range and the 2-year yield is consistent with our fair value range, though at the very upper-end. The investment conclusions are obvious. Bond investors should keep portfolio duration low in 2022. They should avoid the 10-year maturity and allocate most funds to shorter maturities like the 2-year. It should be noted that we used a conservative 2.08% terminal rate estimate in the scenarios presented in Chart 3. This is at the low-end of most survey estimates. What’s more, the BCA Outlook makes a strong case that those survey estimates will be revised higher once it becomes apparent that interest rates will have to rise to well above 2% to contain inflation. We agree that survey estimates of the long-run fed funds rate are probably too low, but we don’t expect them to be revised higher in 2022. Upward terminal rate revisions are probably a story for 2023 or 2024, sometime after the Fed has delivered a few rate hikes and it becomes apparent that more will be needed to slow an overheating economy. Appendix A at the end of this report translates different fed funds rate scenarios into 12-month expected returns for every Treasury maturity. We show scenarios where the liftoff date varies between June 2022 and December 2022, where the pace of rate hikes varies between 75 bps and 100 bps per year and where the terminal fed funds rate varies between 2.08% and 2.58%. The 10-year Treasury note is projected to deliver negative returns in every scenario we tested. Meanwhile, the 2-year Treasury note is projected to deliver a small positive return in every single scenario. These results support our conclusion from Chart 3. Investors should maintain below-benchmark portfolio duration and favor short maturities over long maturities. Risks To The View The first risk to our bearish view on US Treasuries is a resurgence of the pandemic. The 10-year Treasury yield continues to track the “pandemic trade” in the stock market. That is, the 10-year yield rises when a basket of equities that benefit from economic re-opening outperforms a basket of equities that benefit from lockdowns, and vice-versa (Chart 4). So far, the news about the virulence of the Omicron COVID variant has been encouraging, and our base case scenario assumes a further easing of pandemic concerns over the course of 2022. The second risk to our view is that the Fed moves too aggressively toward rate hikes causing an abrupt tightening of financial conditions that weighs on economic growth and sends long-dated bond yields lower. The shaded region in Chart 5 shows that this exact dynamic played out in 2018. Fed rate hikes started to pressure the dollar higher and weigh on equities. This led to tighter financial conditions and slower economic growth. The impact of tighter financial conditions was not immediately evident in the bond market, but slower growth eventually caused the Fed to back away from rate hikes leading to a late-2018 peak in the 10-year yield. Chart 410yr Tracks The "Pandemic Trade"

10yr Tracks The "Pandemic Trade"

10yr Tracks The "Pandemic Trade"

Chart 5Watch Financial Conditions In 2022

Watch Financial Conditions In 2022

Watch Financial Conditions In 2022

Compared to the 2018 scenario, we see less risk of Fed over-tightening in 2022 mainly because the fed funds rate is starting out at a much lower level. However, it will be important to track financial conditions as the Fed moves toward liftoff. Undue tightening would cause us to reverse our positioning. Key View #2: Own Treasury Curve Steepeners The 2/10 Treasury slope will flatten by less than what is currently discounted in the forward curve in 2022. Investors should position for this by going long the 2-year note versus a duration-matched barbell consisting of cash and the 10-year note. We also recommend buying the 20-year bond versus a duration-matched barbell consisting of the 10-year note and 30-year bond as an attractive duration-neutral carry trade. The scenarios presented in the prior section show that the 2-year Treasury yield is priced within the bounds of our estimated fair value range while the 10-year Treasury yield looks too low. Logically, it makes sense to position for a steepening of the 2/10 Treasury curve to profit from this divergence. Chart 6 illustrates the implications of the prior section’s fair value estimates for different Treasury slopes. Our fair value range projects that the 2/10 Treasury slope will be between 38 bps and 89 bps in 12 months, above the 37 bps that is currently priced into the forward curve. The forward curve is also priced for too much flattening in the 2/5 Treasury slope, while the 5/10 slope is consistent with the lower end of our fair value range. The conclusion is that investors should implement 2/10 Treasury curve steepeners in 2022 on the expectation that the 2/10 slope will flatten by less than what is currently discounted in the forward curve. A comparison of the 5-year/5-year forward Treasury yield with a target range based on survey estimates of the long-run neutral fed funds rate also supports the case for 2/10 steepeners. Historically, an increase in the 5-year/5-year forward yield towards its target range corresponds with a steepening of the 2/10 slope (Chart 7). Bear-flattening moves in the 2/10 slope only occur when the 5-year/5-year forward is within its target band, as was the case in 2017/18. Given that the 5-year/5-year forward yield is currently well below its survey-derived target range, there is room for some 2/10 steepening as yields rise. Chart 6Treasury Slope Forecasts

Treasury Slope Forecasts

Treasury Slope Forecasts

Chart 7A Rising 5y5y Will Steepen The Curve

A Rising 5y5y Will Steepen The Curve

A Rising 5y5y Will Steepen The Curve

One way to position for a steeper 2/10 curve is to go long the 5-year Treasury note versus a duration-matched barbell consisting of the 2-year and 10-year notes. Presently, this trade looks very attractive. The 2/5/10 butterfly spread shows a significant yield advantage in the 5-year bullet over the 2/10 barbell, both in absolute terms and relative to our fair value model (Chart 8). While we view this as a good trade, we don’t think it’s the best way to position for 2/10 steepening. We prefer a position long the 2-year note versus a duration-matched barbell consisting of cash and the 10-year note. This trade gives you long exposure at the 2-year maturity instead of the 5-year maturity which will boost returns if the 2/5 slope steepens, as we anticipate it will (Chart 6, panel 2). Chart 8Curve Steepeners Are Cheap

Curve Steepeners Are Cheap

Curve Steepeners Are Cheap

In addition to our recommended 2/10 steepener, we advise clients to favor the 20-year bond versus a duration-matched barbell consisting of the 10-year note and 30-year bond. While we’d expect some flattening of the 10/30 slope in 2022, this trade should still perform well because of its huge carry advantage. The tables in Appendix A show that the 20-year bond earns a massive 12-month carry (income plus rolldown return) of 3.05% compared to 1.85% for the 10-year note and 1.80% for the 30-year bond. Key View #3: Sell Short-Maturity TIPS Chart 9TIPS Breakevens

TIPS Breakevens

TIPS Breakevens

Investors should maintain a neutral allocation to long-maturity TIPS versus nominal Treasuries and an underweight allocation to short-maturity TIPS versus nominal Treasuries. Other attractive positions include: an outright short position in 2-year TIPS, an inflation curve steepener (short 2yr TIPS/long 2yr nominal/long 10yr TIPS/short 10yr nominal), and a TIPS curve flattener (short 2yr TIPS/long 10yr TIPS). As noted at the beginning of this report, we see inflation trending down in 2022. Inflation will remain high enough for the Fed to feel comfortable lifting rates, but it won’t match the elevated readings that are currently discounted in TIPS. Interestingly, long-maturity TIPS breakeven inflation rates are roughly consistent with the Fed’s 2.3%-2.5% target range (Chart 9). The 5-year/5-year forward TIPS breakeven inflation rate is a bit too low, at 2.13%, and the 10-year TIPS breakeven inflation rate is currently 2.47%. With long-dated TIPS breakevens so close to the Fed’s target, we recommend a neutral allocation to long-maturity TIPS versus long-maturity nominal Treasuries heading into 2022. In our view, the mispricing in TIPS lies at the front-end of the curve. The 2-year TIPS breakeven inflation rate has risen to 3.23%, well above the Fed’s 2.3%-2.5% target range. This year’s surge in short-maturity TIPS breakevens has also resulted in a deeply inverted inflation slope (Chart 9, bottom panel). Table 1Regression of Monthly Changes In CPI Swap Rate Versus Monthly Changes In 12-Month Headline CPI Inflation (2010 - Present)

2022 Key Views: US Fixed Income

2022 Key Views: US Fixed Income

Short-maturity inflation expectations are highly sensitive to changes in CPI inflation, much more so than long-maturity expectations. In fact, monthly changes in the 2-year CPI swap rate are more than twice as sensitive to headline inflation than are monthly changes in the 10-year CPI swap rate (Table 1). This means that the cost of short-maturity inflation compensation will decline as inflation moderates in 2022. We recommend an underweight allocation to short-maturity TIPS versus short-maturity nominal Treasuries. We also think an outright short position in 2-year TIPS will be highly profitable in 2022. If we assume that the 2-year TIPS breakeven inflation rate falls to the middle of the Fed’s target range during the next 12 months, and additionally that the 2-year nominal Treasury yield converges with our fair value estimate using the scenario of a September Fed liftoff, 100 bps per year hike pace and 2.08% terminal rate, then we calculate that the 2-year TIPS yield will rise from its current -2.56% to -0.98% during the next 12 months (Chart 10). Chart 10A Lot Of Upside In Short-Maturity Real Yields Short 2-Year TIPS

A Lot Of Upside In Short-Maturity Real Yields Short 2-Year TIPS

A Lot Of Upside In Short-Maturity Real Yields Short 2-Year TIPS

Chart 10 also shows that the anticipated rise in the 2-year TIPS yield greatly outpaces the modest expected increase in the 10-year TIPS yield. This means that a position in 2/10 TIPS curve flatteners will turn a profit in 2022 (Chart 10, bottom panel). Key View #4: Overweight Corporate Bonds Versus Treasuries … For Now We are overweight corporate bonds versus duration-matched Treasuries, for now, but expect to turn more defensive in the first half of 2022 once the yield curve sustainably moves into a flatter regime. Relative valuations suggest that investors should favor high-yield corporates over investment grade. A key pillar of our corporate bond investment process is to split the economic cycle into three phases based on the slope of the yield curve (Chart 11). Phase 1 of the cycle is defined as the period from the end of the last recession until the 3-year/10-year Treasury slope breaks below 50 bps. Phase 2 of the cycle spans the period when the slope is between 0 bps and 50 bps. Phase 3 lasts from when the yield curve inverts until the start of the next recession. Chart 11The Three Phases Of The Economic Cycle

The Three Phases Of The Economic Cycle

The Three Phases Of The Economic Cycle

Our historical analysis shows that excess corporate bond returns versus duration-matched Treasuries tend to be strongest in Phase 1. They are usually positive, but much lower, in Phase 2 and are often negative in Phase 3 (Table 2). Table 2Corporate Bond Returns Across The Three Phases Of The Cycle

2022 Key Views: US Fixed Income

2022 Key Views: US Fixed Income

We have been firmly in Phase 1 since April 2020 and, as we would expect, excess corporate bond returns have been strong. However, we will not remain in Phase 1 much longer. The 3-year/10-year Treasury slope is currently 50 bps, right on the precipice between Phase 1 and Phase 2. We recommend an overweight allocation to corporate bonds versus Treasuries for now, but we will adopt a more defensive posture toward corporates once we transition into Phase 2. We expect this will happen sometime in the first half of 2022. Why Are We Not In Phase 2 Already? Chart 12Curve Flattening Is Overdone

Curve Flattening Is Overdone

Curve Flattening Is Overdone

The 3-year/10-year Treasury slope is hovering right around 50 bps. However, as is noted earlier in this report, we think that recent yield curve flattening is overdone and expect it to reverse somewhat in the coming months. Chart 12 shows the 3-year/10-year slope along with an expected fair value range. This range is based on a 100 bps Fed rate hike pace, a 2.08% terminal rate and varying the liftoff date between June 2022 and December 2022. This fair value range only breaks below 50 bps between March and September of next year. Given our yield curve view, we are positioned for one last period of strong corporate bond outperformance during the next few months. But we will turn more defensive once we judge that we have sustainably transitioned into a Phase 2 environment. Why Turn More Defensive In Phase 2? Chart 13IG Corporate Valuations

IG Corporate Valuations

IG Corporate Valuations

It’s correct to point out that excess corporate bond returns are still generally positive in Phase 2 environments, so ideally, we would remain overweight corporate bonds versus Treasuries throughout Phase 2. This makes sense theoretically, but strategically we think it will be wise to adopt a different approach this cycle. The main reason to err on the side of caution is that corporate bond valuations are extremely stretched. The 12-month breakeven spread for the investment grade corporate bond index is at its 6th percentile since 1995. This means that the investment grade corporate bond index has only been more expensive than today 6% of the time since 1995 (Chart 13). Tight spreads mean that expected returns will be modest, even in a favorable cyclical environment. In other words, we are not sacrificing much expected return by reducing exposure early in the cycle. Given that we can’t predict the start of the next Phase 3 period with exact precision, we think it makes sense to be more defensive this cycle. We will sacrifice some modest expected returns to ensure that we are well positioned for the next period of significant spread widening. Our corporate bond strategy is supported by an empirical study of historical returns. Table 3A shows average 12-month excess returns for the investment grade corporate bond index after certain combinations of the 3/10 Treasury slope and average index option-adjusted spread (OAS) are observed. Table 3B shows 90% confidence intervals for the averages presented in Table 3A.

Chart

Chart

The tables show that a strategy of remaining overweight corporate bonds versus Treasuries after the yield curve transitions into Phase 2 only works when the corporate index OAS is above 100 bps. A transition into Phase 2 portends negative excess corporate bond returns when the OAS is below 100 bps, as it is today. Favor High-Yield Over Investment Grade Chart 14HY Corporate Valuations