Financial Markets

Highlights Equity valuations are extremely stretched versus bonds, so there is little wiggle room for bonds to sell off before pulling down large tracts of the stock market. We estimate that bond yields can rise by no more than 30 bps, before the Fed is forced to talk them back down again. Starting from an earnings yield that is extreme versus its history, we should prudently assume that the prospective long-term real return from equities will be far below the current earnings yield of 4.6 percent, and closer to zero, even if not actually negative. In capitalist economies, gluts may or may not lead to shortages; but shortages always lead to gluts. In other words, the current inflation is sowing the seeds of its own destruction. Hence, we reiterate our structural recommendation to overweight US T-bonds versus US TIPS. Fractal analysis: Cotton, and Polish equities. Feature Chart of the WeekTech Stocks Have Been Tracking The 30-Year T-Bond Price One-For-One

Tech Stocks Have Been Tracking The 30-Year T-Bond Price One-For-One

Tech Stocks Have Been Tracking The 30-Year T-Bond Price One-For-One

Equity valuations are extremely stretched versus bonds. The upshot is that there is little wiggle room for bonds to sell off before pulling down large tracts of the stock market. This is not just an abstract hypothesis – it is an empirical fact, as recent market action is making painfully clear. Since February, the global tech sector has tracked the 30-year T-bond price almost one-for-one. The near perfect fit proves that the tech (and broader growth stock) rally has been entirely premised on the bond market rally. Hence, on the three occasions that bonds have sold off sharply – including in the last couple of weeks – tech stocks have sold off sharply too (Chart of the Week). Put simply, the performance of the tech sector is being driven by the change in its valuation, and the change in its valuation is being driven by the change in the bond yield (Chart I-2). Chart I-2Tech Stock Valuations Are Being Driven By The Bond Yield

Tech Stock Valuations Are Being Driven By The Bond Yield

Tech Stock Valuations Are Being Driven By The Bond Yield

Of course, stock prices are also premised on earnings. So, given enough time, rising earnings can make valuations less stretched, adding more wiggle room for bonds to sell off. The trouble is that a change in earnings happens much more gradually than can a change in valuation – a 10 percent rise in earnings can take a year, whereas a 10 percent fall in valuation can happen in a week. Bond Yields Remain The Dominant Driver Of The Stock Market For the next few months at least, the movement in bond yields will remain the dominant driver of the most stretched parts of the stock market and, by extension, the overall market itself. This is especially true for the growth-heavy S&P 500 which, since March, has been tracking the 30-year T-bond price one-for-one (Chart I-3). Chart I-3The S&P 500 Has Also Been Tracking The 30-Year T-Bond Price One-For-One

The S&P 500 Has Also Been Tracking The 30-Year T-Bond Price One-For-One

The S&P 500 Has Also Been Tracking The 30-Year T-Bond Price One-For-One

The key question for investors is, what is the upper limit to bond yields before stock market damage causes the Federal Reserve to talk them down again? To answer this question, our working assumption is that a 15 percent drawdown in growth stocks would damage the growth-heavy S&P 500 enough – and thereby worsen ‘financial conditions’ enough – for the Fed to change its tone. Based on this year’s very tight relationship between tech stocks and the 30-year T-bond yield, a 15 percent drawdown would occur if the 30-year T-bond yield increased to 2.4 percent from 2.1 percent today (Chart I-4). Chart I-4The Fed's 'Pain Point' Is Only 30 Basis Points Away

The Fed's 'Pain Point' Is Only 30 Basis Points Away

The Fed's 'Pain Point' Is Only 30 Basis Points Away

This confirms our view that the resistance level to long-duration bond yields is around 30 bps above current levels, equivalent to around 1.8 percent on the 10-year T-bond yield. More About The ‘Negative Equity Risk Premium’ Our recent report The Equity Risk Premium Turns Negative For The First Time Since 2002 caused quite a stir. So, let’s elaborate and clarify the arguments we made about the equity risk premium (ERP) – the estimated excess return that stocks will deliver over bonds over a long investment horizon, such as 10 years. Many investors estimate the ERP by taking the stock market’s earnings yield – currently 4.6 percent in the US1 – and subtracting the real 10-year bond yield – currently -0.9 percent on US Treasury Inflation Protected Securities (TIPS). At first glance, this presents a very generous ERP of 5.5 percent. So, equities are attractively valued versus bonds, right? Wrong. The glaring error is that the earnings yield estimates the stock market’s prospective return only if the earnings yield starts and ends at the same level. If it does not, then the prospective return could be very different to the earnings yield. For example, imagine that the stock market was trading at a bubble price-to-earnings multiple of 100, meaning an earnings yield of 1 percent. Clearly, from such a bubble valuation, nobody would expect the market to return 1 percent. Instead, as the bubble burst, and valuations normalised, the prospective return would be deeply negative. It follows that when, as now, the earnings yield is extreme versus its history, we must build in some prudent normalisation to estimate the prospective return. The question is, how? One approach is to use history to inform us of the likely normalisation. Chart I-5 does this using the ‘best-fit’ relationship between the earnings yield at each point through 1990-2011 and subsequent 10-year real return from each starting point. Using the best-fit for this specific episode, the current earnings yield of 4.6 percent implies a prospective 10-year real return not of 4.6 percent, but of -1.1 percent. Chart I-5Based On History, The Current Earnings Yield Implies A Prospective 10-Year Real Return Much Less Than 4.6 Percent

Based On History, The Current Earnings Yield Implies A Prospective 10-year Real Return Much Less Than 4.6 Percent

Based On History, The Current Earnings Yield Implies A Prospective 10-year Real Return Much Less Than 4.6 Percent

Yet this best-fit approach meets a common reproach – that the best-fit for this specific episode is massively distorted by the dot com bubble peak and the global financial crisis (GFC) trough occurring (by coincidence) almost 10 years apart. We can counter this reproach in two ways. First, the best-fit relationship is much better than the raw earnings yield even for undistorted 10-year periods such as 1995-2005 or 2011-2021. Better still, we can change the prospective return from 10 years to 7 years and thereby remove the dot com bubble peak to GFC trough distortion. Chart I-6 shows that this 7-year best-fit relationship also works much better than the raw earnings yield. Chart I-6Based On History, The Current Earnings Yield Implies A Prospective 7-Year Real Return Much Less Than 4.6 Percent

Based On History, The Current Earnings Yield Implies A Prospective 7-year Real Return Much Less Than 4.6 Percent

Based On History, The Current Earnings Yield Implies A Prospective 7-year Real Return Much Less Than 4.6 Percent

Admittedly, the best-fit comes from just one episode in history, and there is no certainty that the 10-year and 7-year relationships that applied during that one episode should apply through 2021-31 and 2021-28 respectively. Nevertheless, starting from an earnings yield that is extreme versus its history, as is the case now, we should prudently assume that the prospective long-term real return from equities will be far below 4.6 percent, and closer to zero, even if not actually negative. Will The ‘Real’ Real Yield Please Stand Up Measuring the ERP also requires an estimate of the prospective real return on bonds. This part should be easy because the yield on the US 10-year TIPS – currently -0.9 percent – is the guaranteed 10-year real return of buying and holding that investment. It is derived by taking the yield on the 10-year T-bond – currently 1.5 percent – and subtracting the market’s expected rate of inflation over the next 10 years – currently 2.4 percent. But the equivalent real return on the much larger conventional bond market could be quite different. In this case, it will be the 10-year T-bond yield minus the actual rate of inflation over the next 10 years. To the extent that the actual rate of inflation turns out less than the expected rate of 2.4 percent, the real return on the T-bond will turn out higher than that on the TIPS. In fact, this has consistently turned out to be the case. The market has consistently overestimated the inflation rate over the subsequent 10 years, meaning that the real return on T-bonds has been around 1 percent higher than that on TIPS (Chart I-7). Chart I-7Will The 'Real' Real Yield Please Stand Up

Will The 'Real' Real Yield Please Stand Up

Will The 'Real' Real Yield Please Stand Up

Yet given the current surge in inflation, and no end in sight for supply chain disruptions and bottlenecks, is it plausible that the next ten years’ rate of inflation will be lower than 2.4 percent? The answer is yes. Because, as my colleague Peter Berezin points out: in capitalist economies, gluts may or may not lead to shortages; but shortages always lead to gluts. And gluts always cause prices to collapse. In other words, the current inflation is sowing the seeds of its own destruction. Hence, we reiterate our structural recommendation to overweight US T-bonds versus US TIPS. The Cotton Is Stretched, And So Are Polish Equities Talking of shortages, cotton now adds to the list of commodities in which supply bottlenecks have raised prices to extremes. Cotton prices have reached a 10-year high due to weather conditions in the US (the world’s biggest cotton producer) combined with shipping disruptions. However, with cotton now exhibiting extreme fragility on its combined 130/260-day fractal structure, there is a high likelihood of a price reversal in the coming months when the shortage turns into a glut (Chart I-8). Chart I-8The Cotton Is Stretched

The Cotton Is Stretched

The Cotton Is Stretched

Meanwhile, the bank-heavy Polish equity market has surged on the back of the spectacular outperformance of its banks sector. This strong uptrend has now reached the point of fragility on its 130-day fractal structure that has indicated several previous reversals (Chart I-9). Chart I-9Poland's Outperformance Is Stretched

Poland's Outperformance Is Stretched

Poland's Outperformance Is Stretched

Accordingly, this week’s recommended trade is to underweight the Warsaw General Index versus the Eurostoxx 600, setting a profit target and symmetrical stop-loss at 6 percent. Dhaval Joshi Chief Strategist dhaval@bcaresearch.com Footnotes 1 Based on the 12-month forward earnings yield. Fractal Trading System Fractal Trades 6-Month Recommendations Structural And Thematic Recommendations Closed Fractal Trades Indicators To Watch - Bond Yields Chart II-1Indicators To Watch - Bond Yields ##br##- Euro Area

Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Chart II-2Indicators To Watch - Bond Yields ##br##- Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Chart II-3Indicators To Watch - Bond Yields ##br##- Asia

Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Chart II-4Indicators To Watch - Bond Yields ##br##- Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Interest Rate Expectations Chart II-5Indicators To Watch ##br##- Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch ##br##- Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch ##br##- Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch ##br##- Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights European small-cap equities have structurally outperformed large-cap stocks. This outperformance echoes the desirable sectoral biases of small-cap stocks. It also reflects the inability of European large-cap stocks to expand their markups, unlike US large caps. The pro-cyclicality of European small-cap stocks and the limited correlation of their relative performance to the Chinese credit cycle make them an attractive play in European portfolios. The current risk-off phase in global markets suggests it is still too early to buy European small-cap stocks, but an opportunity to overweight them will emerge in the coming weeks. Feature Markets last week were volatile and corrected sharply. This fit with the view expressed in our previous strategy report, which argued that the near-term outlook for European equities was still clouded by the confluence of the coming Fed tightening and a Chinese economic slowdown. Chart 1Ebbing COVID Allows For Central Bank Repricing

Ebbing COVID Allows For Central Bank Repricing

Ebbing COVID Allows For Central Bank Repricing

The market seems especially concerned by the deterioration in liquidity conditions. The Delta wave is ebbing around the world (Chart 1) and inflation is proving to be stickier than policymakers had originally anticipated. As a result, investors appear to be pricing in the potential implications of central banks moving from being behind the curve to ahead of the curve. Moreover, surging natural gas prices in Europe, empty gas stations in the UK, labor shortages around the world, and steep automobile production cuts by major players like Toyota and GM raise the specter of stagflation. In this context, bond yields are rising and stocks are agitated. The dollar’s rally further tightens global financial conditions and adds to the systemic stress, which intensifies the very unsettling environment for investors. Consequently, seasonal October weakness remains on the table. Chart 2Tactical Vulnerabilities Remain

Tactical Vulnerabilities Remain

Tactical Vulnerabilities Remain

We continue to see this selling phase as temporary. Sentiment will be consistent with a trough in risk assets soon (Chart 2). Additionally, Chinese authorities will reflate the economy much more aggressively than they have so far, even if it probably takes more market pain first. In this context, we focus on what to buy to take advantage of the eventual rebound in cyclical plays. This week, we look at European small-cap stocks that have handsomely outperformed their larger counterparts over the past ten years. In Europe, Small Is Beautiful Chart 3Small Caps Lead In Europe

Small Caps Lead In Europe

Small Caps Lead In Europe

The underperformance of European stocks relative to the US over the past 13 years is well known by investors. Less known is that, since 2012, European small-cap stocks have performed roughly in line with their US counterparts. In other words, European small-cap stocks have massively outperformed Euro Area equity benchmarks (Chart 3). Two forces explain the ability of European small caps to beat their larger competitors by 85% since the Great Financial Crisis. The sectoral composition of European small-cap indexes helped them outperform their larger competitors. Using MSCI benchmarks, the small-cap index largest overweight are industrials and real estate, compared to financials, healthcare, and consumer staples for large caps (Table 1). Industrials have been one of the best performing sectors in the cyclicals and value categories, while financials have greatly suffered. Meanwhile, real estate equities enjoy falling yields, while financials hate them. This dichotomy explains why European small caps outperformed as European yields collapse (Chart 4). It is also why, unlike in the US, the relative performance of European small-cap equities exhibits little correlation with the slope of the yield curve. Table 1Small Caps Overweighs The Right Sectors

Small Caps Win Big?

Small Caps Win Big?

Chart 4European Small Caps Like Lower Bund Yields

European Small Caps Like Lower Bund Yields

European Small Caps Like Lower Bund Yields

The poor performance of the European large-cap stocks is the second element explaining the outperformance of European small caps. The European large-cap stocks lie at the heart of Europe’s underperformance relative to the US, not the smaller firms. According to researchers De Loecker, Eeckhout, and Unger, US firms have grown their markups massively since the 1980s (Chart 5).1 These expanding markups reflect a growing market power, which is the result of rising market concentration among the dominant players in nearly all the industries.2 In fact, Grullon, Larkin & Michaely show that industries with a greater level of concentration also display higher levels of RoA (Chart 6).3 The problem for European large firms is that they have not experienced the same increase in industry concentration as US businesses. Research by the OECD demonstrates that industry concentration rose significantly more in the US than in Europe over the past 20 years (Chart 7). This is particularly true in the service sector (Chart 7, middle panel) and the less digital-intensive industries (Chart 7, bottom panel).4 Chart 5Higher US Markups

Small Caps Win Big?

Small Caps Win Big?

Chart 6As Concentration Increases, So Do RoAs

Small Caps Win Big?

Small Caps Win Big?

Chart 7Europe Did Not Witness The Same Increase In Concentration

Small Caps Win Big?

Small Caps Win Big?

Without this increase in market power, European large caps could not experience a meaningful pick up in their RoEs relative to those of small-cap stocks. They have therefore been fully victim to their sector composition and massively underperform smaller firms as well as US large businesses. Bottom Line: The structural outperformance of European small caps relative to large-cap stocks reflects the former’s large overweight in industrials and real estate stocks compared to the latter’s overrepresentation of financials, healthcare, and consumer staples names. Additionally, the inability of large-cap European names to increase industrial concentration has prevented them from mimicking the extraordinary growth in markups and RoE witnessed in the US. As a result, European small-cap names could massively beat their larger counterparts. Can The Outperformance Continue? The structural outperformance of small caps will become challenged if Europe experiences a structural increase in yields, which will hurt real estate stocks while helping financials. This sectoral effect will result in a structural outperformance of European stocks. On a cyclical horizon, however, the outlook continues to favor small-cap over large-cap equities in Europe and the Eurozone. Chart 8The Relative Performance Of European Small Caps is Procyclical

Small Caps Win Big?

Small Caps Win Big?

As in the US, the relative performance of European small-cap stocks is pro-cyclical. As Chart 8 shows, small-cap stocks generate the largest excess returns at the beginning of business cycle upswings. They continue to outperform, as long as the business cycle points up. Only once a slowdown begins do small- cap names underperform. Similarly, the relative performance of small-cap equities correlates closely with the Euro Area Manufacturing PMI (Chart 9). It also displays a negative correlation with high-yield spreads (Chart 9, middle panel). Additionally, small-cap stocks track the evolution of inflation swaps (Chart 9, bottom panel). This behavior of small caps means that they remain an attractive bet over the next 18 to 24 months. The European economy is likely to continue to grow robustly over the coming two years and thus stay in the quadrant where small caps outperform. Moreover, the ECB’s policy will generate very accommodative monetary conditions for an extended period. Hence, European high-yield bonds will continue to outperform safe havens and the labor market will tighten further, which will help CPI swap climb up. Despite this procyclicality, the relative performance of small-cap stocks displays only a loose correlation with the European cyclical/defensive split (Chart 10). Moreover, small caps do not correlate closely with commodity prices (Chart 10 middle panel). These two observations reflect the limited relationship between the relative performance of small-cap equities and the Chinese credit impulse (Chart 10, bottom panel). The small caps’ lack of sensitivity to the Chinese economy is the consequence of their lower international bent compared to that of large-cap firms. Chart 9More Signs Of Procyclicality

More Signs Of Procyclicality

More Signs Of Procyclicality

Chart 10Low Correlation To China Plays

Low Correlation To China Plays

Low Correlation To China Plays

This low correlation with Chinese economic variables is likely to prove another asset for small-cap equities. As we have witnessed with the Evergrande saga or the rotating crackdowns from one industry to the next, China will remain a source of uncertainty for the global economy and global capital markets for the foreseeable future. Thus, a low-correlation relative performance is an attractive attribute. Chart 11Not Particularly Cheap

Not Particularly Cheap

Not Particularly Cheap

European small-cap stocks are not without blemish. Unlike in the US, they trade at a premium to large-cap stocks on many valuation metrics. For example, their price-to-forward earnings, price-to-trailing earnings, price-to-cash flow ratios and dividend yields stands at 21 vs 16, 35 vs 35, 18 vs 10 and 1.2% vs 2%, respectively. True, small-cap indexes carry a large proportion of companies with negative earnings. Adjusting for this characteristic, the forward P/E ratio falls to 15.12, which is just under the similarly adjusted forward P/E ratio of the Eurozone benchmark. Our Composite Small Cap Relative Valuation Indicator, which amalgamates this information, is directly in the neutral zone (Chart 11). The neutral relative valuation of small-cap stocks is a handicap because they sport operating metrics that are worse than their larger cousins. Their RoE are a meagre 6.3% vs 7.7%. Moreover, forward earnings have rebounded sharply already and long-term growth expectations are lofty (Chart 12). This leaves the euro as the ultimate arbiter of the path of European small caps. As Chart 13 illustrates, the trade-weighted euro closely tracks the relative performance of the Euro Area small-cap benchmark. This reflects the more domestic nature of small caps, but also, their procyclicality, which mimics that of the euro. Chart 12Some Good News In The Price

Some Good News In The Price

Some Good News In The Price

Chart 13A Play On The Euro

A Play On The Euro

A Play On The Euro

Chart 14A Weaker Yuan Could Lift The Dollar

A Weaker Yuan Could Lift The Dollar

A Weaker Yuan Could Lift The Dollar

The euro continues to face near-term hurdles, which creates a problem for small-cap stocks. The dollar is catching a bid as the Fed moves closer to its tapering and eventual rate hike. Moreover, interest rate differentials between China and the US are narrowing, which will weigh on the yuan (Chart 14). A weaker CNY often causes EM currencies to depreciate and puts downward pressure on the euro. Furthermore, if the global equity correction perdures a few more weeks, the dollar will benefit from additional risk-off flows, which will also hurt the euro. Beyond these near-term risks, BCA’s foreign exchange strategists continue to hold a positive cyclical outlook on the dollar. The greenback’s defining characteristic is its counter-cyclicality. Thus, BCA’s expectation that the period of risks to global growth is temporary also means that the dollar’s rally has a finite life. As we argued last week, Chinese policymakers are unlikely to let the economic deterioration fester for too long, as it would risk uncontrolled deleveraging pressures. Moreover, global capex and inventory trends also point toward a growth re-acceleration in the first half of 2022. In this environment, the euro—which still behaves as the anti-dollar—will be able to regain its footing. Therefore, we will not chase EUR/USD below the 1.15 - 1.12 zone. Chart 15History Rhymes

History Rhymes

History Rhymes

The near-term risks to the euro and small-cap stocks create a buying opportunity for investors with a 12- to 18-month investment horizon. A short period of small-cap underperformance will allow small-cap equities to digest completely the period of outperformance that took place between March 2020 and June 2021 (Chart 15). It will also follow the pattern of the past ten years, wherein periods of outperformance last 18 to 24 months and are followed by a short decline before resuming anew. Bottom line: Small-cap stocks are an attractive vehicle to bet on pro-cyclical assets in Europe. They have benefited from a structural outperformance as a result of their attractive sectoral profile. Moreover, their relative performance strengthens when the global business cycle is in expansion, yet it is a rare cyclical asset with a limited correlation to Chinese credit trends. European small-cap stocks are tightly correlated with the trade-weighted euro. In the near term, this could cause a period of underperformance to develop; however, this is a buying opportunity for investors with a 12- to 18-month investment horizon. Mathieu Savary, Chief European Strategist Mathieu@bcaresearch.com Footnotes 1J. De Loecker, J. Eeckhout, G. Unger, “The Rise Of Market Power And The Macroeconomic Implications,” Mimeo 2018. 2Please see The Bank Credit Analyst Section II "The Productivity Puzzle: Competition Is The Missing Ingredient," dated June 27, 2019, available at bcaresearch.com 3G. Grullon, Y. Larkin and R. Michaely, “Are Us Industries Becoming More Concentrated?,” April 2017. 4Bajgar, M., et al. (2019), “Industry Concentration in Europe and North America,” OECD Productivity Working Papers, No. 18, OECD Publishing, Paris, https://doi.org/10.1787/2ff98246-en. Tactical Recommendations

Small Caps Win Big?

Small Caps Win Big?

Cyclical Recommendations

Small Caps Win Big?

Small Caps Win Big?

Structural Recommendations

Small Caps Win Big?

Small Caps Win Big?

Closed Trades

Small Caps Win Big?

Small Caps Win Big?

Currency Performance Fixed Income Performance Equity Performance

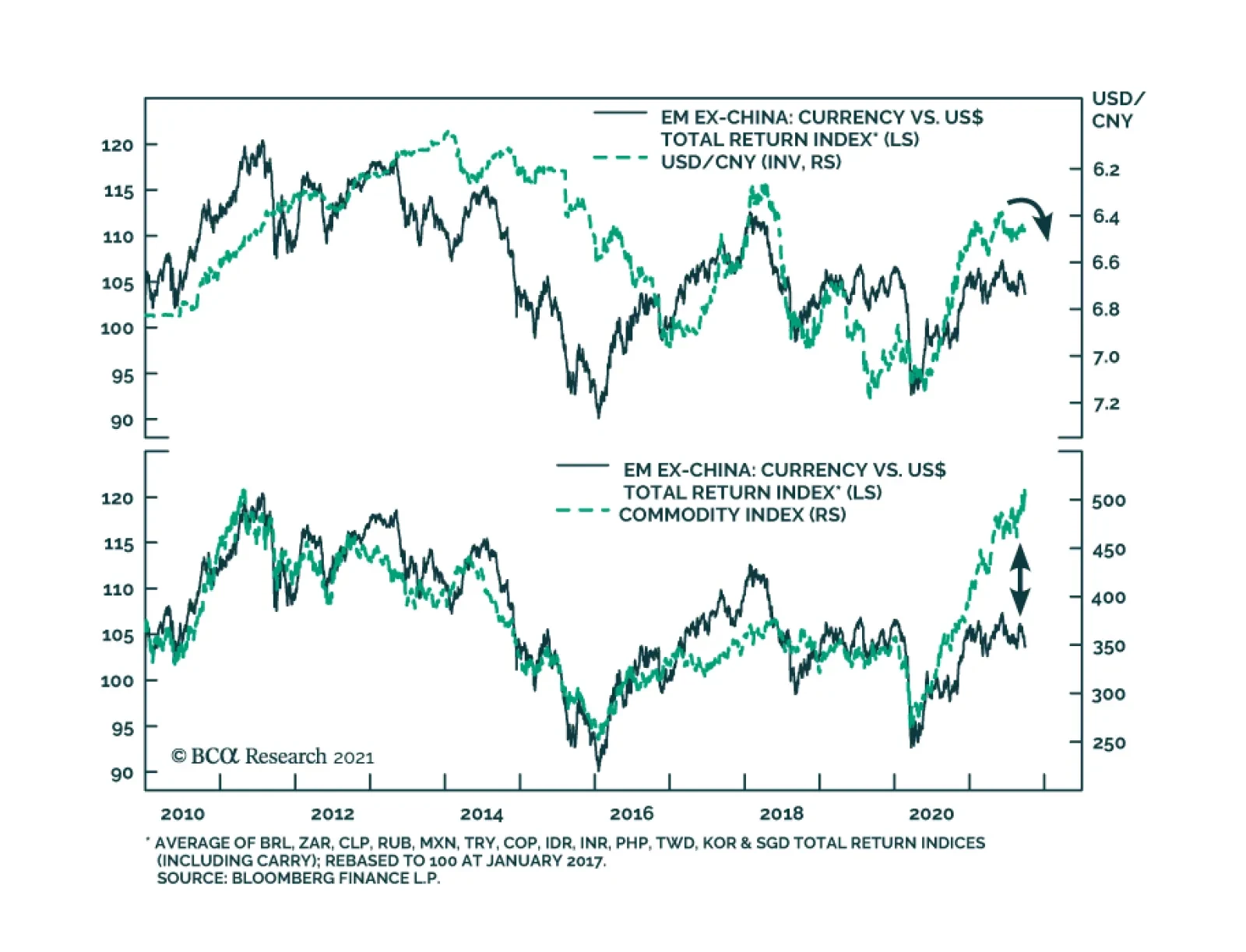

Emerging market currencies have recently rolled over in early-June and are depreciating sharply vis-à-vis the US dollar. Odds are that this downtrend will continue. On the domestic front, it is true that many Emerging Market central banks are already…

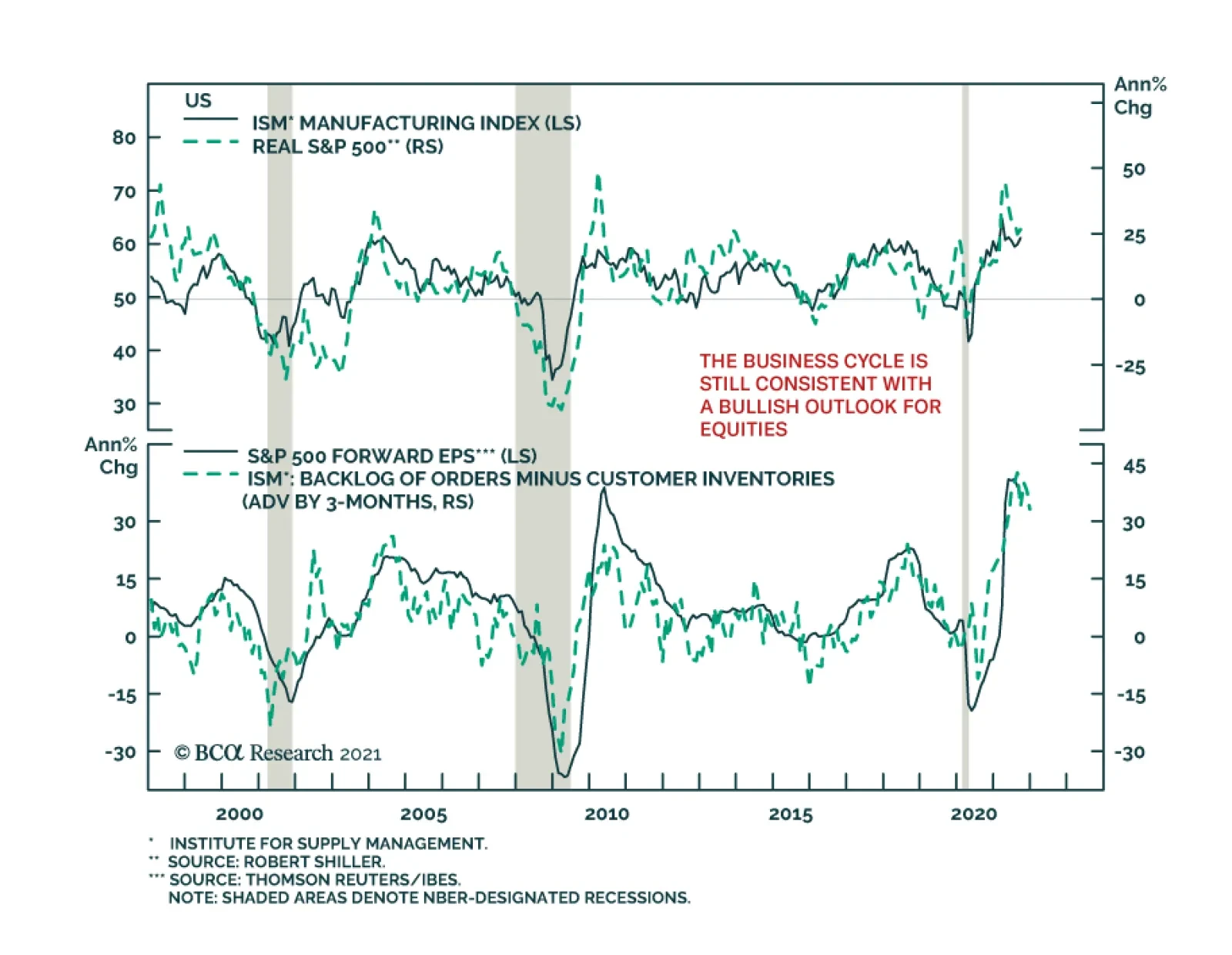

Both the ISM and Markit PMIs suggest that US manufacturing activity accelerated in September. The ISM index increased 1.2 points to a four-month high of 61.1, surprising expectations of a decline. Similarly, the Markit measure inched up 0.2 points to 60.7. …

Highlights Recommended Allocation

Quarterly Portfolio Outlook: Stay Bullish But Verify

Quarterly Portfolio Outlook: Stay Bullish But Verify

The global economy will continue to grow at an above-trend rate over the next 12 months and central banks will remove accommodation only slowly.But the second year of a bull market is often tricky: Growth slows after its initial rebound, and monetary policy starts to be tightened, amid rising inflation.Equities are likely to outperform bonds over the next 12 months, driven by improving earnings, but at a slower pace than over the past year and with higher volatility.We continue to recommend only a cautiously optimistic stance on equities, with an overweight in US equities, and underweight in Europe. Our sector overweights are a mix of cyclicals (Industrials), plays on higher rates (Financials), and selective defensives (Health Care).China is likely to announce a stimulus to cushion the impact from Evergrande, which might push up oversold Chinese stocks. We close our underweight on Chinese equities, but raise them only to neutral as the real estate sector looks vulnerable. That could be bad news for commodities and the rest of Emerging Markets, which we cut to underweight.The Fed is likely to announce tapering this quarter, and raise rates in December 2022. This is likely to push up 10-year Treasury yields to 2-2.25% by then, and so we remain underweight duration.Investment-grade credit is expensive, but B-rated high-yield bonds still look attractive as defaults continue to decline. EM corporate debt is riskier post-Evergrande, but higher-rated sovereign dollar debt offers a good spread pickup.OverviewThe second year of a bull market is often tricky. Growth starts to slow after its initial rebound, and central banks move towards tightening policy. This does not signal the end of the bull market, but equity returns in Year 2 are typically lacklustre (Table 1).That is exactly the situation markets face now. Growth has been surprising on the downside, and inflation on the upside over the past few months (Chart 1). Table 1Year 2 Of Bull Markets Often Has Only Weak Returns

Quarterly Portfolio Outlook: Stay Bullish But Verify

Quarterly Portfolio Outlook: Stay Bullish But Verify

Chart 1Growth Surprising On The Downside, Inflation On The Upside

Growth Surprising On The Downside, Inflation On The Upside

Growth Surprising On The Downside, Inflation On The Upside

Our basic investment stance remains that the global economy will continue to grow at an above-trend rate over the next 12 months (as the consensus forecasts – Chart 2), and that central banks will remove accommodation only slowly. We can see no signs of a recession on the 18-to-24-month horizon and, as Chart 3 shows, equities almost always outperform bonds except during and in the run-up to recessions. Chart 2But Growth Will Continue To Be Above Trend

But Growth Will Continue To Be Above Trend

But Growth Will Continue To Be Above Trend

Chart 3Equities Outpeform Bonds Except Around Recessions

Equities Outpeform Bonds Except Around Recessions

Equities Outpeform Bonds Except Around Recessions

This justifies a moderately pro-risk stance, with overweights in equities and (selectively) credit, and a big underweight in government bonds. But the risks to this sanguine view are rising, and the next few months could be choppy. Stay bullish, but keep a close eye on what could go wrong.The slowdown in growth is largely because manufacturing boomed last year and now simply the pace of growth is decelerating. Manufacturing PMIs are (mostly) still above 50, but have fallen from their peaks (Chart 4). Supply-chain bottlenecks have also dented production. And consumers will spend less on durables and more on services, as lockdowns are eased.We have emphasized that the $2.5 trillion of excess savings in the US will boost spending over coming quarters. But enhanced unemployment benefits have now ended and most of the savings left are with richer households who have a lower propensity to spend (see page 9 for more on this). Covid also remains a risk: Cases are stickily high in some countries and consumers are still not 100% confident about going out to dine and for entertainment (Chart 5). Chart 4PMIs Falling But Mostly Still Above 50

PMIs Falling But Mostly Still Above 50

PMIs Falling But Mostly Still Above 50

Chart 5Consumers Still A Bit Wary About Going Out

Consumers Still A Bit Wary About Going Out

Consumers Still A Bit Wary About Going Out

China is an increasing risk to growth. Its economy has been slowing all year as a result of monetary tightening (Chart 6) and this may be exacerbated by the fallout from Evergrande. The Chinese authorities are likely to announce a stimulus package to offset the slowdown (which is why we are neutralizing our underweight on Chinese equities). But the stimulus will probably be only moderate and targeted, and they will not allow a renewed boom in real estate (as we explain on page 11), which has been a significant driver of Chinese growth in recent years (Chart 7). This could hurt the economies of Emerging Markets and other commodity producers, which depend on Chinese demand. Chart 6China Has Been Slowing All Year

China Has Been Slowing All Year

China Has Been Slowing All Year

Chart 7Real Estate Has Been A Big Driver Of Chinese Growth

Real Estate Has Been A Big Driver Of Chinese Growth

Real Estate Has Been A Big Driver Of Chinese Growth

At the same time that growth is slowing, inflation is proving a little stickier and broader-based than was expected. Measures of underlying inflation pressure, such as trimmed-mean CPIs, suggest that it is no longer only pandemic-related prices that are rising in the US and some other countries (Chart 8). Rising shipping charges (container rates are up 228% this year) are pushing up the cost of imported goods. And the first signs are emerging that labor shortages, especially in restaurants and shops, are causing wage rises (Chart 9). Chart 8Inflation Is Broadening Out In Some Countries

Inflation Is Broadening Out In Some Countries

Inflation Is Broadening Out In Some Countries

Chart 9The First Signs Of Wage Rises?

The First Signs Of Wage Rises?

The First Signs Of Wage Rises?

Unsurprisingly, then, central banks are starting to wind down their asset purchases and even raise rates. Norges Bank was the first developed central bank to hike this cycle in September. New Zealand may follow in Q4. And the Fed has pretty clearly signaled that it, too, will announce tapering before year-end. And this is not to mention Emerging Market central banks, many of which have had to raise rates sharply in the face of soaring inflation (Chart 10).A shrinking of excess liquidity is another common phenomenon of the second stage of expansions, as monetary policy starts to be tightened and liquidity is directed more towards the real economy and less towards speculation. This, too, often caps the upside for risk assets, though it doesn’t usually cause them to collapse (Chart 11). Chart 10EM Central Banks Raising Rates Sharply

EM Central Banks Raising Rates Sharply

EM Central Banks Raising Rates Sharply

Chart 11Excess Liquidity Is Drying Up

Excess Liquidity Is Drying Up

Excess Liquidity Is Drying Up

Table 2Who Will Raise Rates When?

Quarterly Portfolio Outlook: Stay Bullish But Verify

Quarterly Portfolio Outlook: Stay Bullish But Verify

While there are many factors that might cause market jitters over the coming months, the underlying picture is that robust growth is likely to continue and central banks will remain cautious about tightening too quickly. Excess savings will propel consumption, companies will need to increase capex to fulfill that demand, and the impact of fiscal stimulus is still coming through (Chart 12). The big central banks won’t raise rates for some time: The Fed perhaps in late-2022, but the ECB and the Bank of Japan not over the forecast horizon (Table 2). Decent growth and easy policy remains a positive backdrop for risk assets over the 12-month horizon. Chart 12Fiscal Stimulus Is Still Coming Through

Quarterly Portfolio Outlook: Stay Bullish But Verify

Quarterly Portfolio Outlook: Stay Bullish But Verify

Garry Evans, Senior Vice PresidentChief Global Asset Allocation Strategistgarry@bcaresearch.comWhat Our Clients Are AskingHow Worried Should We Be About Inflation?Since the beginning of the year, we have argued that the current period of high inflation will be transitory. The market has adopted this view, with 5-year/5-year forward inflation expectations remaining at 2.2%. Chart 13Growing Signs That Inflation Might Not Be Transitory

Growing Signs That Inflation Might Not Be Transitory

Growing Signs That Inflation Might Not Be Transitory

However, we have grown worried about the possibility that inflation might be stickier at a higher level than we initially expected. Specifically, while it is true that prices of supply-constrained items – such as used cars – have started to ease, there are signs that higher inflation has began to broaden. Core CPI excluding pandemic-related items and cars has started to pick up, with its 6-month rate of change reaching its highest level in more than a decade (Chart 13, panel 1). Meanwhile 42% of the PCE basket grew at an annual rate of more than 5% in July, compared to just 24% in March.Currently, we are watching the behavior of prices in the housing and labor markets to check if our worries are justified. We pay particular attention to these sectors because price pressures in housing and labor can be self-sustaining, giving rise to inflationary spirals if left unchecked.What is happening to inflation in these areas? So far, the signals are mixed. Even though wage growth remains within the historical norm for now, any further advance in wages will take us to a decade high (Chart 13, panel 2). Likewise, annual growth of shelter cost remains low, though its 6-month change suggests that it will soon begin to rise to its pre-pandemic levels (Chart 13, panel 3).Our base case continues to be that high inflation is transitory. That being said, we have positioned our portfolio to hedge for the risk that this view is wrong. We have given an overweight to real estate in our alternatives portfolio and within equities. Will Consumers Really Spend All Those Savings? Chart 14Low-Income Households Did Not Save Much

Quarterly Portfolio Outlook: Stay Bullish But Verify

Quarterly Portfolio Outlook: Stay Bullish But Verify

Generous unemployment benefits and the year-long lockdown have pushed up US excess savings over the past 18 months to an estimated $2.5 trillion, and the household savings ratio to 9.6% (Chart 14, panel 1). The consensus is that these savings will bolster consumer spending and support broad economic growth over the coming quarters. However, this expectation is based on the assumption that all consumers have accumulated savings, whereas the reality is a bit different.Survey results from the US Census Bureau show that households earning under $75,000, which have the highest propensity to consume, have almost entirely spent their first stimulus checks and three-quarters of their second and third checks on expenses and paying off debt. Even for those earning over $75,000, only 50% of those stimulus receipts have gone into savings (Chart 14, panel 2).With the labor market still not back to full employment (albeit mostly because of labor supply issues), enhanced unemployment benefits coming to an end, fears of further Covid variants and lockdowns, and higher inflation, could precautionary savings rise? The years following the Global Financial Crisis suggest that they might: The savings rate rose from 3% at the onset of the GFC to 8% five years after it (Chart 14, panel 3). A similar attitude among consumers this time could put a dent in US growth, given that consumption makes up about 70% of GDP.This raises the risk that consumption might slow over the coming quarters. In our latest Monthly Portfolio Outlook, we highlighted that consumption is shifting away from goods towards services. While value added from manufacturing is only 11% of GDP, the effect on markets might be bigger, since goods producers make up about 40% of US market cap. What Is The Risk Of A Big Upside Surprise In US Employment?The recovery of the labor market remains at the center of investors’ and Fed officials’ attention. The reluctance to return to the workforce mostly reflects overly generous unemployment benefits and fears of getting infected. With the fourth wave of the pandemic showing signs of cresting and benefits expiring, the consensus is that the unemployment gap will soon shrink. We would, however, question whether the labor market can surprise significantly to the upside and recover faster than the market currently implies. A swift recovery would push up bond yields and bring forward the Fed’s liftoff date, which could hurt the outlook for risk assets. Chart 15The Labor Market Could Surprise To The Upside

The Labor Market Could Surprise To The Upside

The Labor Market Could Surprise To The Upside

The number of men not in the labor force but who want a job has fallen back to the pre-pandemic level (Chart 15, panel 1). The sharp decline in this indicator in August coincided with the expiration of unemployment benefits in some Republican states. The overall Federal pandemic benefits program expired in early September. This should push even more people to return to the workforce (Chart 15, panel 2).However, there are still close to 3.5 million women (almost half a million above the pre-pandemic level) who are not in the labor force but would like a job: Some of these are keen to return to the workplace once they deem it safe for their children to get vaccinated and return to school. With governments eager to speed up vaccination rollouts and Pfizer’s recent announcement showing positive results of its Covid vaccine in trials on children under the age of 12, more women should return to the workforce.It is also worth noting that some of the most hard-hit sectors – such as leisure & hospitality – have already recovered over 80% of the jobs lost since February 2020. For sectors yet to reach such a high recovery rate, for example education & health services, returning workers have room to choose from jobs. For every job lost since the onset of the pandemic, there are now 2.1 job openings (Chart 15, panel 3). What Is The Risk Of Contagion From Evergrande?In September, Chinese property developer Evergrande failed to make an interest payment on an overseas bond issue. What would be the consequences for the Chinese and global economy if it went bankrupt? Chart 16Chinese Companies Are Highly Indebted

Chinese Companies Are Highly Indebted

Chinese Companies Are Highly Indebted

Evergrande is big. Its debts are $306 billion, 2% of Chinese GDP. It has yet to build 1 million units that have already been paid for. It employs 200,000 people. And the issue is bigger. For years, investors have worried about China’s corporate debt, which is 160% of GDP (Chart 16). Chinese companies have issued almost $1 trillion of bonds in foreign currencies. The property market plays an outsized role in the economy: It comprises 66% of household wealth (versus 24% in the US); real estate and related industries amount to some 30% of GDP.The government will likely rescue Evergrande. But it faces a dilemma: For years it has been trying to reduce bad debt and stabilize house prices. It cannot bail out Evergrande’s creditors without undermining those efforts.It will probably aid apartment buyers, who have paid upfront for Evergrande properties, and make arrangements for domestic banks to swap their debt for equity or land holdings. But it won’t bail out equity owners or foreign bond holders. It will also not ease real-estate market restrictions, such as the “three red line” rules on property companies’ leverage. Such a package could damage Chinese individuals’ confidence in property, and foreigners willingness to provide capital to the industry.China may also announce a stimulus package to bolster the economy. But local governments are dependent on land sales for around a third of their income (Chart 17). If the property market is weak, the transmission mechanism of stimulus may be damaged. Finally, Chinese housing sales are highly correlated to global commodities prices, which may fall as a result (Chart 18). Chart 17Local Governments Depend On Land Sales

Local Governments Depend On Land Sales

Local Governments Depend On Land Sales

Chart 18A Slowdown In Housing Would Hurt Commodities

A Slowdown In Housing Would Hurt Commodities

A Slowdown In Housing Would Hurt Commodities

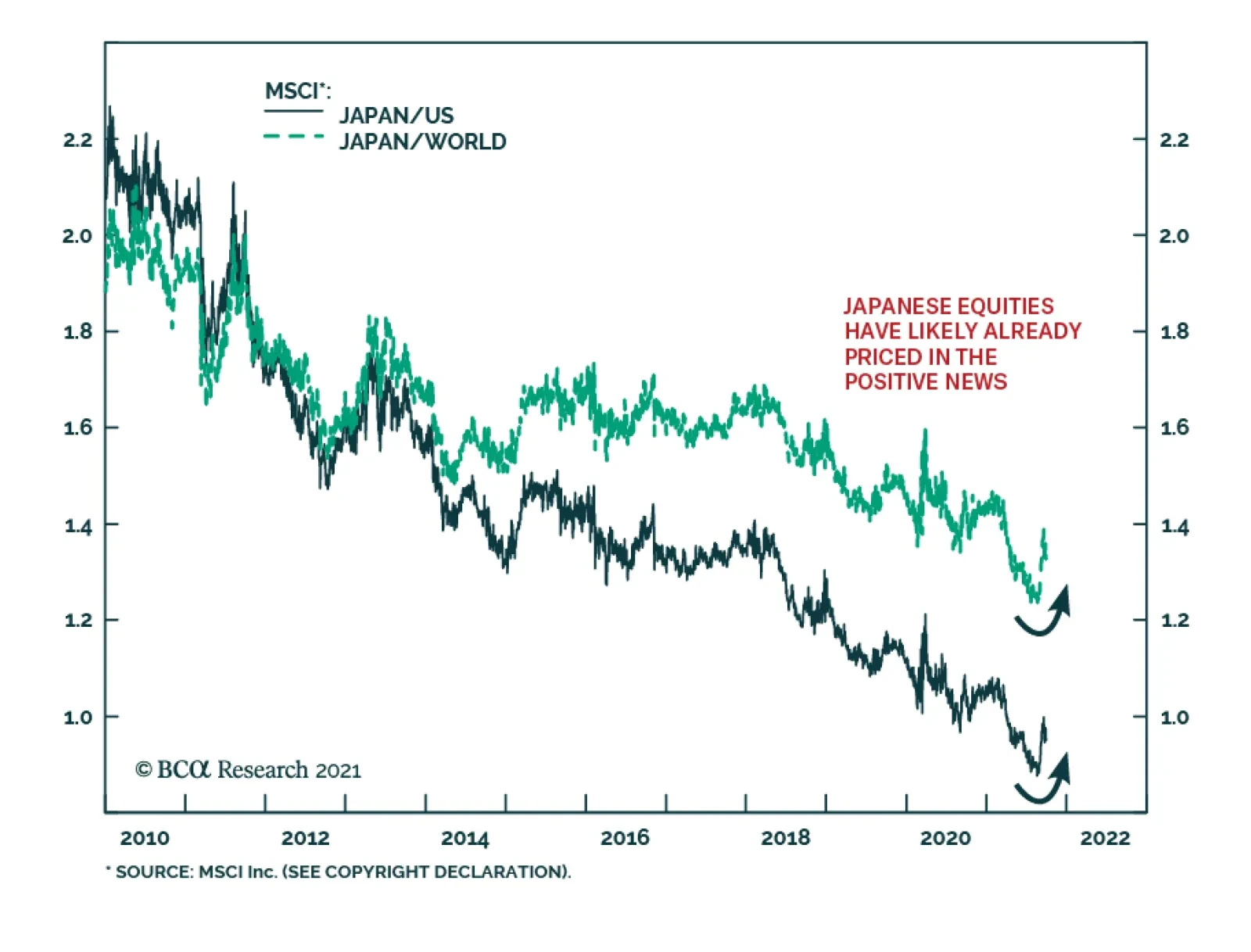

BCA Research’s EM and China strategists do not see Evergrande as likely to trigger a systemic crisis or crash, but it will reinforce the chronic credit tightening that has been underway in China.1Is It Time To Overweight Japanese Equities?Japanese equities staged a strong rally in the third quarter, outperforming the MSCI global equity index by about 5% in US dollar total return terms. On an absolute basis, the MSCI Japan price index in USD is near its 1989 historical high, even though the local-currency index is still more than 30% below its 1989 all-time high.We have been underweight Japanese equities in our global equity portfolio since July 2019, mainly due to unfavorable structural forces such as the aging population and chronic deflationary pressures. Japanese equities have tended to stage counter-trend bounces, some of which were quite significant in magnitude (Chart 19, panel 1). We therefore recommend clients move to the sidelines to avoid the potentially short-lived but sharp upside risk, supported by the following two considerations:First, foreign investors play a significant role in the Japanese equity market. The fact that MSCI Japan in USD terms is near its all-time high could trigger more foreign buying, given the positive correlation between the price index and price momentum (Chart 19, panels 3 and 5).Second, Japanese equities are among the cheapest globally, trading at a large discount to the global index. Currently, the discount is larger than its 3-year moving average, making it risky to underweight Japan.So why not overweight Japanese equities?The Japanese equity index is dominated by Industrials. It should benefit from our favorable view on this sector. However, Japan’s machinery and machine tool industries have heavy reliance on Asia, especially China. Orders from China have already rolled over with the Chinese PMI now in contractionary territory. In the meantime, the rolling-over of the US and European PMIs also does not bode well for orders from the other two large regions (Chart 20). Chart 19Upgrade Japanese Equities To Neutral

Upgrade Japanese Equities To Neutral

Upgrade Japanese Equities To Neutral

Chart 20Japan's Heavy External Reliance

Japan's Heavy External Reliance

Japan's Heavy External Reliance

We expect that China will eventually inject stimulus into its economy in a measured fashion such that the negative spillover to Japan and Europe may be limited. That’s why we are also taking profit in our underweight position on China after the recent sharp selloff in the offshore Chinese equity index (see page 18).Global EconomyOverview: The developed world continues to see strong growth, albeit at a slower pace than nine months ago. This is causing a more persistent – and more broad-based – rise in inflation, especially in the US, than was previously expected. However, the Fed is unlikely to raise rates for at least another 12 months, and the ECB and BOJ not on the forecast horizon. The biggest risk to global economic growth is the slowdown in China and now the troubles at Evergrande. We assume that the Chinese government will launch a stimulus to cushion the slowdown, but it may be less effective than the market expects. Chart 21US Growth Has Slowed But Remains Above Trend

US Growth Has Slowed But Remains Above Trend

US Growth Has Slowed But Remains Above Trend

US: Growth has been slowing relative to expectations all year (Chart 21, panel 1). Nonetheless, it is still well above trend. The September Markit PMIs remained high at 60.5 for manufacturing and 54.4 for services. Although consumer confidence has fallen back a little because of the third Covid wave in some southern states, retail sales in August were still up 15% year-on-year and 1.8% (ex autos) month-on-month. Growth seems set to remain above trend, as consumers spend their $2.5 trillion of excess savings, companies increase capex to ease supply-chain bottlenecks, and the government rolls out more fiscal spending. The IMF forecasts 4.9% real GDP growth in 2022, after 7.0% this year. Euro Area growth also remains robust, with the manufacturing and services PMIs at 58.7 and 56.3 respectively in September. Vaccination levels have risen (more quickly than in the US) and, as a consequence, lockdowns and international travel restrictions have been largely eased. Inflation pressures remain more restrained than in the US, with core CPI at only 1.6% (mainly pushed up by pandemic-related shortages) and the trimmed-mean CPI barely above zero. The ECB persuaded the market that its tapering, announced in September, is very dovish, and it is certainly true that – with its new 2% symmetrical inflation target – the ECB is not set to raise rates any time soon. The IMF’s forecasts are for 4.6% real GDP growth this year, and 4.3% next.Japan has generally lagged the recovery in the rest of the world, due to its structural headwinds, but it is now seeing some more robust data. Industrial production is up 12% year-on-year and exports 26%, although the PMIs still remain somewhat depressed at 51.2 for manufacturing and 47.4 for services in September. Japan’s initial slow vaccine rollout has recently accelerated and the percent of double-vaccinated adults now exceeds the US. This suggests that sluggish consumption (with retail sales up only 2% year-on-year) might start to recover. Markets got excited about the prospects for fiscal stimulus ahead of the general election, which has to be held by the end of November. We do not see new LDP leader Fumio Kishida, who is likely to win that election, making any significant change in policy. Chart 22China Is The One Market Where Growth Is Slowing Sharply

China Is The One Market Where Growth Is Slowing Sharply

China Is The One Market Where Growth Is Slowing Sharply

Emerging Markets: China’s slowdown – and the government’s possible reaction to it with a large stimulus – dominate the outlook for Emerging Markets. Both China’s manufacturing and services PMIs are now below 50 (Chart 22, panel 3), and retail sales, industrial production and fixed-asset investment all surprised sharply on the downside last month. We expect an easing of policy, but only a moderate one. Elsewhere in Emerging Markets, central banks continue to struggle with the puzzle of whether they need to raise rates (as Russia, Brazil and Mexico have done) in the face of rising inflation and falling currencies, despite continuing underlying weakness in their economies. Interest Rates: US inflation looks stickier than believed three months ago, with a broadening of inflation away from just pandemic-affected items (see “How Worried Should We Be About Inflation?" on page 8). But inflation expectations are still well under control (Chart 22, panel 4) and so the Fed is likely to begin tapering only in December and not raise rates until end-2022. This will most likely cause a moderate rise in long-term rates with the 10-year US Treasury yield rising to 1.7% by year-end and 2-2.25% by the time of the first Fed rate hike. Inflation elsewhere in developed economies looks more subdued (except in the UK and Canada), and so long-term rates are likely to rise somewhat more slowly there.Global Equities Chart 23Watch Earning Revisions

Watch Earning Revisions

Watch Earning Revisions

Global equities ended the quarter more or less flat after a very strong performance in the first eight months of the year and a volatile September. Earnings growth continued its strong trend from the first half, powered by margin improvement in both the DM and EM universes. Consequently, the forward PE multiple contracted further (Chart 23).Going forward, despite worries about the potential spillover to the global economy and global financial markets from China’s Evergrande fiasco, the “earnings-driven” theme will likely continue. BCA’s global earnings model points to over 40% earnings growth for the next 12 months, and all sectors have positive forward earnings estimates. However, net revisions by analysts seem to be cresting as the global manufacturing PMI has rolled over from a very high level. Even though valuation is less stretched than at the beginning of the year, equities are still expensive by historical standards. In addition, central banks are preparing for an eventual withdrawal of their massive liquidity injections and there is still plenty of uncertainty concerning Covid variants. GAA has been cautiously optimistic so far this year with overweights on equities and cash relative to bonds, and overweight US equities relative to Japan, Europe and China. These positions have panned out well. After adjustments made in April and July, our sector portfolio has been well positioned by overweighting Industrials, Financials, Real Estate and Healthcare, underweighting Materials, Utilities and Consumer Staples, and being neutral on Tech, Consumer Discretionary and Communication Services. We have not made any changes to our sector recommendations this quarter.In accordance with our long-held belief of “taking risk where risk will likely be rewarded the most,” we make the following adjustments to our country allocations: close the underweights in China and Japan and the overweight in the UK; and initiate one new position: Underweight EM-ex-China. Overall, our country portfolio has a defensive tilt with an overweight in the US (defensive) and underweights in the euro area and EM-ex China (cyclical), while being neutral on the UK, Japan, Australia and Canada. Country Allocation: Upgrade MSCI China And Japan, Downgrade UK And EM-ex-China. We have been underweight MSCI China and overweight the UK since April 2021, and underweight Japan since July 2019.The China underweight generated outperformance of 23% and the UK overweight -2%, while the Japanese position produced an outperformance of 7%. Chart 24Favor China vs The Rest of The EM

Favor China vs The Rest of The EM

Favor China vs The Rest of The EM

While the fate of Evergrande Group, China’s second largest property developer, remains uncertain, our view is that the government will come up with a restructuring plan to minimize damaging ripple effects on the Chinese economy. This view is supported by the behavior of the domestic A-share market and also the CNY/USD, which has diverged from the offshore equity market (Chart 24, Panel 5).BCA Research’s house view is that China will now stimulate its economy, but only at a measured pace. This means that further underperformance of MSCI China is likely to be limited relative to the global benchmark, as shown in Chart 24, panel 1. The ongoing deleveraging in the Chinese real estate sector, however, means that activity in the sector will probably slow further, reducing demand for construction materials. This may put a dent on the strength of metal prices, therefore negatively impacting the ex-China EM equity index, as shown in panel 2.Moreover, the relative performance of China vs non-China EM is approaching a very oversold level while the relative valuation measure is at an extreme (Chart 24, panels 3 and 4). As such, we switch our positioning by upgrading Chinese equities to neutral from underweight and downgrade EM ex China to underweight from neutral. This implies an overall underweight to Emerging Markets.We also close the UK overweight to support an upgrade in Japan (see more details on page 13). The UK overweight was largely based on a positive view of the GBP, which has now risen to fair value.Government Bonds Chart 25Watch Inflation In 2022

Watch Inflation in 2022

Watch Inflation in 2022

Maintain Below-Benchmark Duration. Global bond yields ignored the sharp rise in core inflation in Q3. The US 10-year Treasury yield actually declined in the first two months of the quarter in response to the muted inflation readings in non-Covid related segments of the economy. Even with the fast run-up in yields in September, the US 10-year yield finished the quarter at 1.52%, only about 5 bps higher than the level on June 30th (Chart 25).We have advised clients to focus on the jobs market to determine when the Fed will lift the Fed Funds Rate off its zero bound because of the Fed’s emphasis on “maximum employment” as a pre-condition for this. However, the Fed has not clearly defined what “maximum employment” means. According to calculations by our US bond strategists, the US unemployment rate will fall to 3.8%, with a 63% participation rate, by the end of 2022 if job creation averages a reasonably achievable 414,000 per month until then. Our bond strategists think that the Fed will be forced to clarify its definition of “maximum unemployment” over the coming months and, as we get close to it next year, the key indicator to watch will shift back to inflation. If inflation remains high, then the Fed will be quicker to declare that the labor market is at “maximum employment”, and vice versa.Currently, the overnight index swap curve indicates the first rate hike will be in January 2023 with a total rate increase of 123 bps by the end of 2024. BCA Research’s house view is that the Fed will announce its first hike in December 2022 and will hike at a faster pace than what is priced in by the market. This is based on our view that unemployment will likely reach 3.5% by end-2022 with inflation above the Fed’s target. This would suggest that long-term rates will rise too, and so bond investors should remain below benchmark duration.Corporate BondsSince the beginning of the year, investment-grade credit has provided roughly 200 basis points of excess return over duration-matched Treasurys, while high-yield bonds have generated almost 600 basis points. Chart 26Continue to Favor High-Yield Credit

Continue to Favor High-Yield Credit

Continue to Favor High-Yield Credit

We continue to have a neutral allocation to investment-grade credits within the fixed-income category. While supportive monetary policy should generally favor spread product, we believe there is much better value to be found outside investment-grade bonds, since these bonds are currently trading at historically high valuation levels (Chart 26, panel 1).We think valuations look much more attractive in the high-yield space, and as a result remain overweight within the fixed-income category. Our US Bond Strategy service expects the share of defaults in the space to fall to between 2.3% and 2.8% – below the default rate currently priced in by the market (Chart 26, panel 2). Within high yield, we prefer B-rated bonds since they offer the most attractive spread pickup on a risk-adjusted basis.What about EM debt? Currently we are cautious on EM corporate debt. The default of Chinese real estate developer Evergrande is likely to have ripple effects throughout EM credit markets and currencies. There are already signs of considerable strains, with EM corporate spreads starting to rise (Chart 26, panel 3). We recommend that investors focus on EM sovereign issuers such as Mexico, Russia, and Malaysia, given that they provide a significant yield pickup over US bonds with comparable credit ratings, and are less likely to default than their corporate counterparts.CommoditiesEnergy (Overweight): Oil prices are likely to remain close to current levels for the remainder of this year. However, recovering demand – particularly from Emerging Markets – and production discipline by the OPEC 2.0 coalition should support prices over the next two years. Given this backdrop, our Commodity & Energy strategists expect the price of Brent crude to average $75 and $80 per barrel in 2022 and 2023 respectively, with WTI trading $2-$4/bbl lower. Chart 27Limited Upside For Oil And Metals In The Short-Term

Limited Upside For Oil And Metals In The Short-Term

Limited Upside For Oil And Metals In The Short-Term

Industrial Metals (Neutral): Industrial metals’ prices have bifurcated. Those relating to alternative energy, such as copper, nickel and cobalt, continue to rise and are up 30% on average since the beginning of the year. Iron ore on the other hand has taken a colossal hit, falling over 53% from its May high. The knock-on effects of accelerating Chinese production cuts and softening economic activity, as well as Evergrande’s debt woes, will continue to put downward pressure on prices. In the short-term, we do not expect a significant rebound. However, in the longer-term, demand will recover – particularly if China implements significant stimulus – and supply will remain tight, which will help metal prices to recover.Precious Metals (Neutral): Gold prices did not react positively to the decline in US real rates over the past quarter. In fact, gold prices are slightly down, by ~1.5% since the start of July (Chart 27, panel 4). We expect real rates to rise as economic growth and the labor market recover and the Fed turns slightly more hawkish, while inflation moderates as base and pandemic effects abate. Rising real rates are a negative factor for the gold price. Nevertheless, inflation is likely to be a bit stickier than the market is currently pricing in, and we therefore maintain a neutral exposure to gold, since it is a good inflation hedge.CurrenciesUS Dollar Chart 28Do Not Underweight The Dollar Yet

Do Not Underweight The Dollar Yet

Do Not Underweight The Dollar Yet

Since we went from underweight to neutral on the dollar in April, the DXY has risen by only 1%. Our position remains the same for this quarter. On the one hand, momentum – one of the most reliable indicators for cyclical movements in the dollar – has turned firmly positive. Moreover, pain in the Chinese real-estate sector should weight on commodities and emerging markets – a development which historically has been bullish for the USD (Chart 28, panel 1). However, not all is good news for the greenback. Relative growth and inflation trends are starting to rebound in the rest of the world vis-à-vis the US (Chart 28, panel 2). Additionally, speculators are now firmly overweight the USD, and it remains expensive by 11% relative to PPP fair value. We believe that these forces could eventually be strong enough for the dollar bear market to resume. As a result, we are putting the US dollar on downgrade watch. Canadian DollarWe believe that there is upside to the Canadian dollar. Canada’s employment market is recovering faster than in the US, which should prompt the BoC to normalize interest rates before the Fed. Additionally, while many commodities are likely to suffer as China’s real estate market slows, oil should hold up relatively well since its demand is not as dependent on the Chinese economy. As a result, we are upgrading the CAD from neutral to overweight. Australian DollarWe remain underweight the AUD. While it is true that the AUD is now cheap on a PPP basis, weakness in iron ore from a slowing Chinese real-estate market should continue to weigh on the Aussie dollar. Chinese YuanWe are negative on the yuan on a cyclical basis. Interest-rate differentials should start moving against this currency (Chart 28, panel 3). While the Fed is likely to tighten policy as the labor market enters full employment, Chinese authorities will ease monetary policy to avert a full-blown crisis in their real-estate market.Alternatives Chart 29Outlook Remains Favorable For Private Equity And Real Estate

Quarterly Portfolio Outlook: Stay Bullish But Verify

Quarterly Portfolio Outlook: Stay Bullish But Verify

Return Enhancers: With public markets expensive and unlikely to provide investors with more than single-digit returns, the focus has shifted to alternative assets, particularly private equity (PE). Performance continues to be impressive, with an annualized return of 59% in Q4 2020 (Chart 29, panel 1). This supports our previous research that funds raised during recessions and early in expansions tend to outperform those raised late-cycle. Distributions from existing positions should allow limited partners (LPs – the investors who provide capital to PE funds) to commit to newer funds. Data from Preqin shows that more than $610 billion has been raised so far during 2021 (Chart 29, panel 2). We continue to favor Private Equity over Hedge Funds.Inflation Hedges: Last year’s inflationary pressures should moderate over the coming months as base effects and supply chain bottlenecks abate. Given this backdrop, we maintain our positive view on real estate versus commodity futures. Commodity prices have already shot up over the past 18 months and have limited upside from current levels: Energy prices are up by 61% since the beginning of the year, industrial metals 24%, and agriculture 17%. Over the past 15 years, REITs outperformed commodity futures when inflation was between 0% and 3% (Chart 29, panel 3). There are opportunities within the real-estate sector, despite our concerns about weaknesses in some segments of commercial real estate such as prime office property in major cities.Volatility Dampeners: We continue to favor farmland and timberland over structured products, particularly mortgage-backed securities (MBS). Farmland offers attractive yields and should continue to provide the best portfolio protection in the event of any market distress. MBS spreads, on the other hand, while wider than the pre-pandemic level, remain tight compared to the pace of mortgage refinancing (Chart 29, panel 4).Risks To Our ViewOur main scenario is based on a Goldilocks-like view of the world: That growth will be robust, but not so strong as to push up inflation further and cause central banks to turn hawkish. The risks, therefore, are that the environment turns out to be either too hot or too cold. Chart 30A Resurgence Of Covid

A Resurgence Of Covid

A Resurgence Of Covid

What could cause growth to slow? Covid remains the biggest risk. Cases are still high in many countries, and could rise again as people socialize indoors during the colder months (Chart 30). A more virulent strain is not inconceivable. Governments will be reluctant to impose lockdowns again, but consumers might become wary about going out.We have written elsewhere (see page 11) about the risks coming from a China slowdown and the aftermath of the Evergrande affair. A policy mistake is not improbable: The Chinese authorities want to stimulate the economy, but at the same time keep a lid on property prices. That will be a hard balance to achieve. Slower Chinese growth would hurt commodity producers and many Emerging Markets. Other risks to growth include fiscal tightening as employment-support schemes end and countries look to repair their budget positions (Chart 31), consumers building up precautionary savings and not spending their excess cash (see page 9), and problems caused by rising energy prices.Our view remains that the currently high inflation is transitory. But it is proving quite sticky and could remain high for a while. Inflation expectations are well anchored for the moment (Chart 32) but could rise above central banks’ comfort-zones if recorded core inflation in the US, for example, currently 3.6%, stays above 3% for another 12 months. This could bring forward the date of the first Fed rate hike (currently priced in for January 2023), raise long-term rates and, in turn, push up the dollar. A combination of rising US rates and a stronger dollar would have very negative consequences for heavily indebted Emerging Market economies. Chart 31Fiscal Drag

Fiscal Drag

Fiscal Drag

Chart 32Deanchoring Of Inflation Expectations

Deanchoring Of Inflation Expectations

Deanchoring Of Inflation Expectations

Footnotes1 Please see China Investment Strategy Report "The Evergrande Saga Continues," dated September 29, 2021 and Emerging Markets Strategy Report "On Chinese Internet Stocks, Real Estate And Overall EM," dated September 16, 2021, available at https://www.bcaresearch.com/GAA Asset Allocation

Highlights The fourth quarter will be volatile as China still poses a risk of overtightening policy and undermining the global recovery. US political risks are also elevated. A debt default is likely to be averted in the end. Fiscal stimulus could be excessive. There is a 65% chance that taxes will rise in the New Year. A crisis over Iran’s nuclear program is imminent. Oil supply disruptions are likely. A return to diplomacy is still possible but red lines need to be underscored. European political risks are comparatively low, although they cannot go much lower, Russia still poses threats to its neighbors, and China’s economic wobbles will weigh on European assets. Our views still support Mexican equities and EU industrials over the long run but we are booking some gains in the face of higher volatility. Feature Our annual theme for 2021 was “No Return To Normalcy” and events have borne this out. The pandemic has continued to disrupt life while geopolitics has not reverted to pre-Trump norms. Going forward, the pandemic may subside but the geopolitical backdrop will be disruptive. This is primarily due to Chinese policy, unfinished business with Iran, and the struggle among various nations to remain stable in the aftermath of the pandemic. Chart 1Delta Recedes With Vaccinations

Delta Recedes With Vaccinations

Delta Recedes With Vaccinations

Chart 2Global Recovery Marches On

Global Recovery Marches On

Global Recovery Marches On

Chart 3Global Labor Markets On The Mend

Global Labor Markets On The Mend

Global Labor Markets On The Mend

The underlying driver of markets in the fourth quarter will be the fact that the COVID-19 pandemic is waning as vaccination campaigns make progress (Chart 1). New cases of the Delta variant have rolled over in numerous countries and in US states that are skeptical toward vaccines. Global growth will still face crosswinds. US growth rates are unlikely to be downgraded further while Europe’s growth has been upgraded. However, forecasters are likely to downgrade Chinese growth expectations in the face of the government’s regulatory onslaught against various sectors and property sector instability (Chart 2). Barring a Chinese policy mistake, the global composite PMI is likely to stabilize. Labor markets will continue healing (Chart 3). The tug of war between unemployment and inflation will continue to give way in favor of inflation, given that wage pressures will emerge, stimulus-fueled household demand will be strong, and supply shortages will persist. Central banks will try to normalize policy but will not move aggressively in the face of any new setbacks to the recovery. Will China Spoil The Recovery? Maybe. Chinese policy and structural imbalances pose the greatest threat to the global economic recovery both in the short and the long run. The immediate risk to the recovery is clear from our market-based Chinese growth indicator, which has not yet bottomed (Chart 4). The historic confluence of domestic political and geopolitical risks in China is our key view for the year. China is attempting to make the economic transition that other East Asian states have made – away from the “miracle” manufacturing phase of growth toward something more sustainable. But there are two important differences: China is making its political and economic system less open and free (the opposite of Taiwan and South Korea) and it is confronting rather than befriending the United States. The Xi administration is focused on consolidating power ahead of the twentieth national party congress in fall 2022. Xi is attempting to stay in power beyond the ten-year limit that was in place when he took office. On one hand he is presenting a slate of socioeconomic reforms – dubbed “common prosperity” – to curry popular favor. This agenda represents a tilt from capitalism toward socialism within the context of the Communist Party’s overarching idea of socialism with Chinese characteristics. On the other hand, Xi is cracking down on the private sector – Big Tech, property developers – which theoretically provides the base of power for any political opposition. The crackdowns have caused Chinese equities to collapse relative to global and have reaffirmed the long trend of underperformance of cyclical sectors relative to defensives within Chinese investable shares (Chart 5, top panel). Chart 4China Threatens To Spoil The Party

China Threatens To Spoil The Party

China Threatens To Spoil The Party

In terms of financial distress, so far only high-yield corporate bonds have seen spreads explode, not investment grade. But current policies force property developers to liquidate their holdings, pay off debts, and raise cash while forcing banks to cut bank on loans to property developers and homebuyers. (Not to mention curbs on carbon emissions and other policies squeezing industrial and other sectors.) Chart 5Beijing Could Easily Trigger Global Market Riot

Beijing Could Easily Trigger Global Market Riot

Beijing Could Easily Trigger Global Market Riot

If these policies are not relaxed then property developers will continue to struggle, property prices will fall, credit tightening will intensify, and local governments will be starved of revenue and forced to cut back on their own spending. Yet the government’s signals of policy easing are so far gradual and behind the curve. If policy is not relaxed, then onshore equities will sell off (as well as offshore) and credit spreads will widen more generally (Chart 5, bottom panel). Broad financial turmoil cannot be ruled out in the fourth quarter. Ultimately, however, China will be forced to do whatever it takes to try to secure the post-pandemic recovery. Otherwise it will instigate a socioeconomic crisis ahead of the all-important political reshuffle in fall 2022. That would be the opposite of what Xi Jinping needs as he tries to consolidate power. Chinese households have stored their wealth, built up over decades of economic success, in the housing sector (Chart 6). Economic instability could translate to political instability. Chart 6Beijing Will Provide Bailouts And Stimulus … Or Face Political Instability

Fourth Quarter Outlook: So Much For Normalcy!

Fourth Quarter Outlook: So Much For Normalcy!

Investors often ask how the government can ease policy if doing so will further inflate housing prices, which hurts the middle class and is the opposite of the common prosperity agenda. High housing prices are the biggest of the three “mountains” that are said to be crushing the common folks and weighing on Chinese birthrates and fertility (the other two are high education and medical costs). The answer is that while policymakers want to cap housing prices and encourage fertility, they must prevent a general collapse in prices and economic and financial crisis. There is no evidence that suppressing housing prices will increase fertility or birthrates – if anything, falling fertility is hard to reverse and goes hand in hand with falling prices. Rather, evidence from the US, Japan, South Korea, Thailand, and other countries shows that a bursting property bubble certainly does not increase fertility or birthrates (Charts 7A and 7B). Chart 7AEconomic Crash Not A Recipe For Higher Fertility

Economic Crash Not A Recipe For Higher Fertility

Economic Crash Not A Recipe For Higher Fertility

Chart 7BEconomic Crash Not A Recipe For Higher Fertility

Economic Crash Not A Recipe For Higher Fertility

Economic Crash Not A Recipe For Higher Fertility

Bringing it all together, investors should not play down negative news and financial instability emerging from China. There are no checks and balances on autocrats. Our China Investment Strategy has a high conviction view that policy stimulus is not forthcoming and regulatory curbs will not be eased. The implication is that China’s government could make major policy mistakes and trigger financial instability in the near term before changing its mind to try to preserve overall stability. At that point it could be too late. Will Countries Add More Stimulus? Yes. Chart 8Global Monetary Policy Challenges

Global Monetary Policy Challenges

Global Monetary Policy Challenges

With China’s stability in question, investors face a range of crosswinds. Central banks are struggling with a surge in inflation driven by stimulus-fueled demand and supply bottlenecks. The global output gap is still large but rapid economic normalization will push inflation up further if kinks are not removed (Chart 8). A moderating factor in this regard is that budget deficits are contracting in 2022 and coming years – fiscal policy will shift from thrust to drag (Chart 9). However, the fiscal drag is probably overstated as governments are also likely to increase deficit spending on the margin. The US is certainly likely to do so. But before considering US fiscal policy we must address the immediate question: whether the US will default on national debt. Treasury Secretary Janet Yellen has designated October 18 as the “X-date” at which the Treasury will run out of extraordinary measures to make debt payments if Congress does not raise the statutory debt ceiling. There is presumably a few weeks of leeway after this date but markets will grow very jittery and credit rating agencies will start to downgrade the United States, as Standard & Poor’s did in 2011. Chart 9Global Fiscal Drag Rears Its Head

Fourth Quarter Outlook: So Much For Normalcy!

Fourth Quarter Outlook: So Much For Normalcy!