Financial Markets

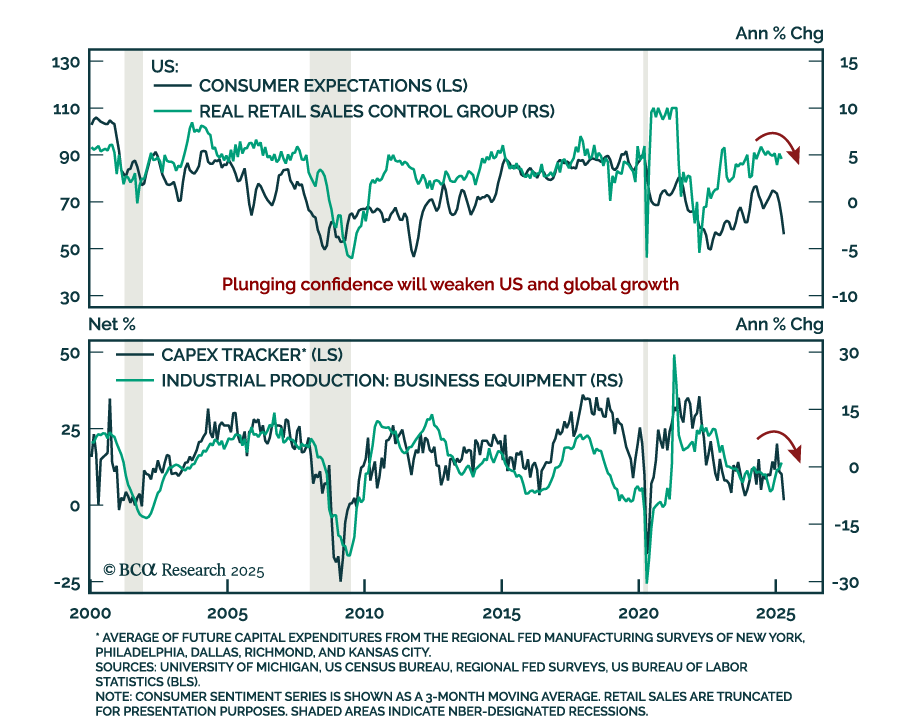

Soft data continues to deteriorate and hard data will soon follow, reinforcing our defensive asset allocation. Consumer and business confidence have plunged as policy uncertainty and inflation expectations rise, with spending, hiring and capex plans…

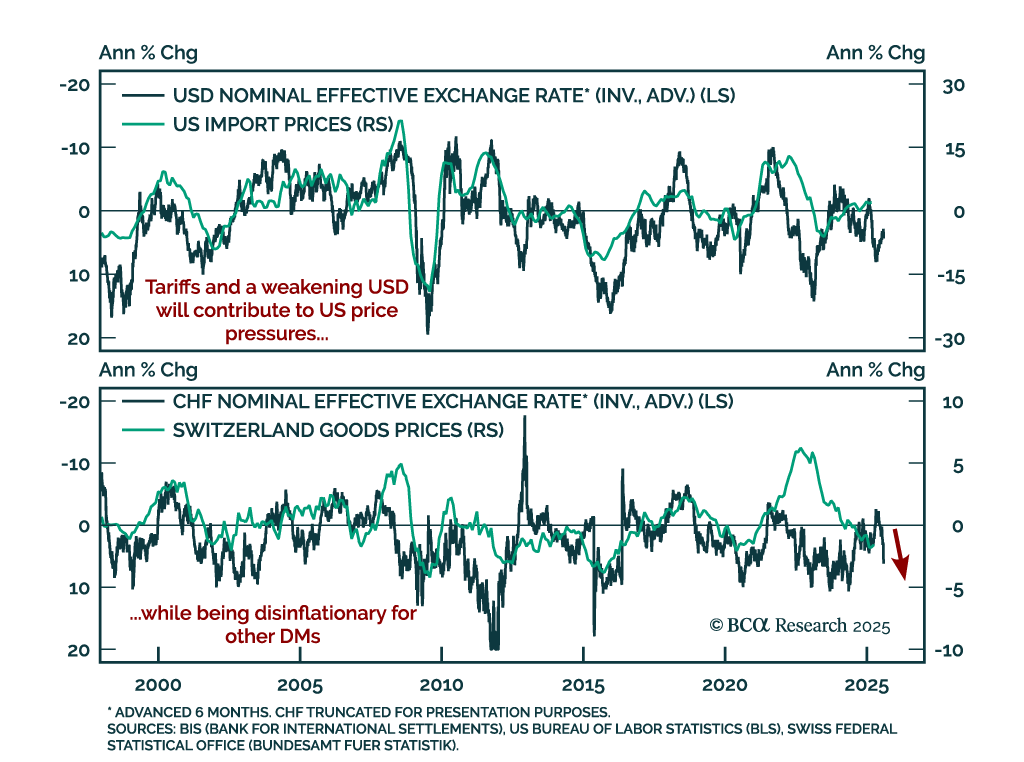

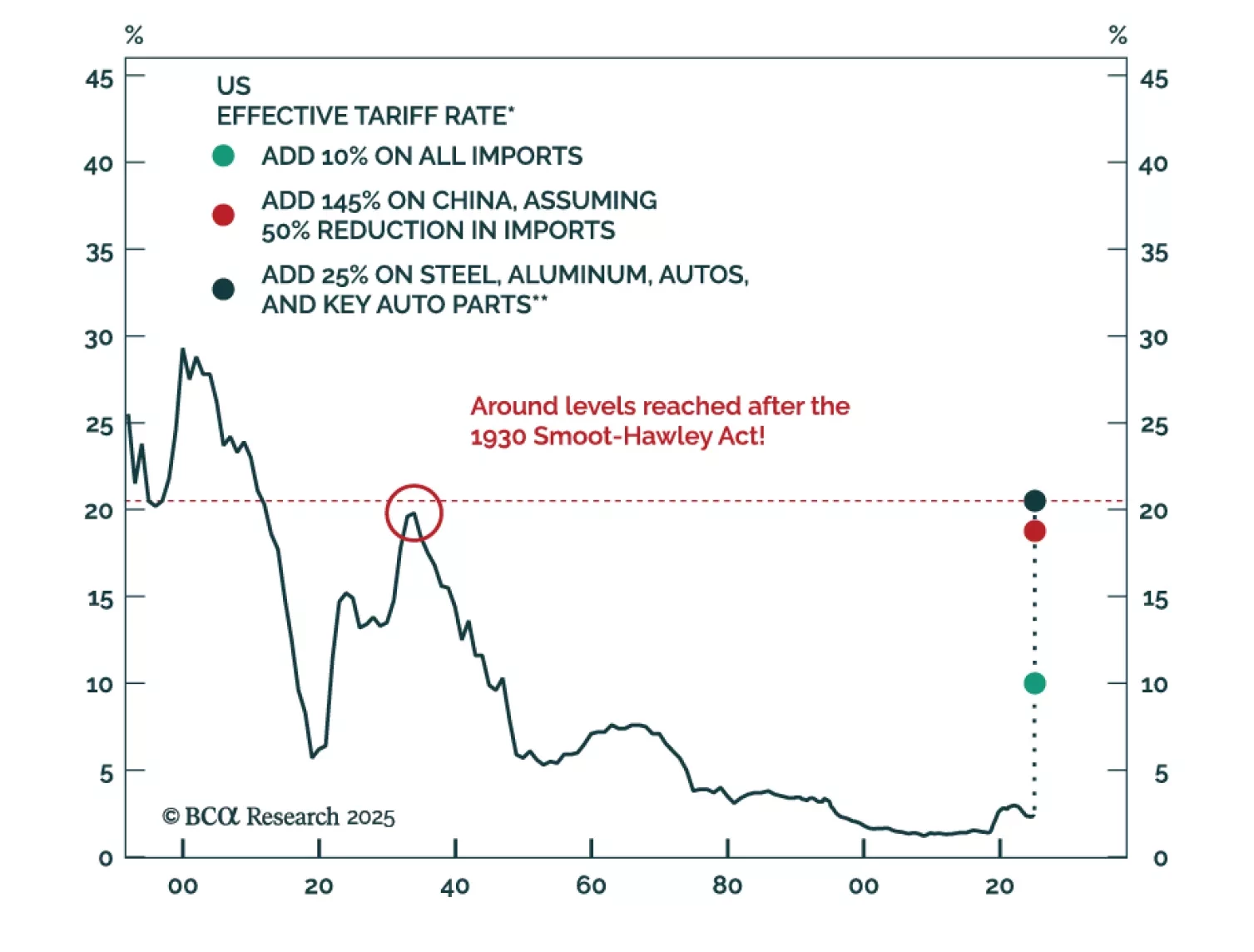

Tariff-driven inflation is diverging across economies, with the US facing mounting pressures while disinflation persists elsewhere. In theory, US tariffs should strengthen the dollar and weaken targeted currencies. In practice, the opposite has occurred: The…

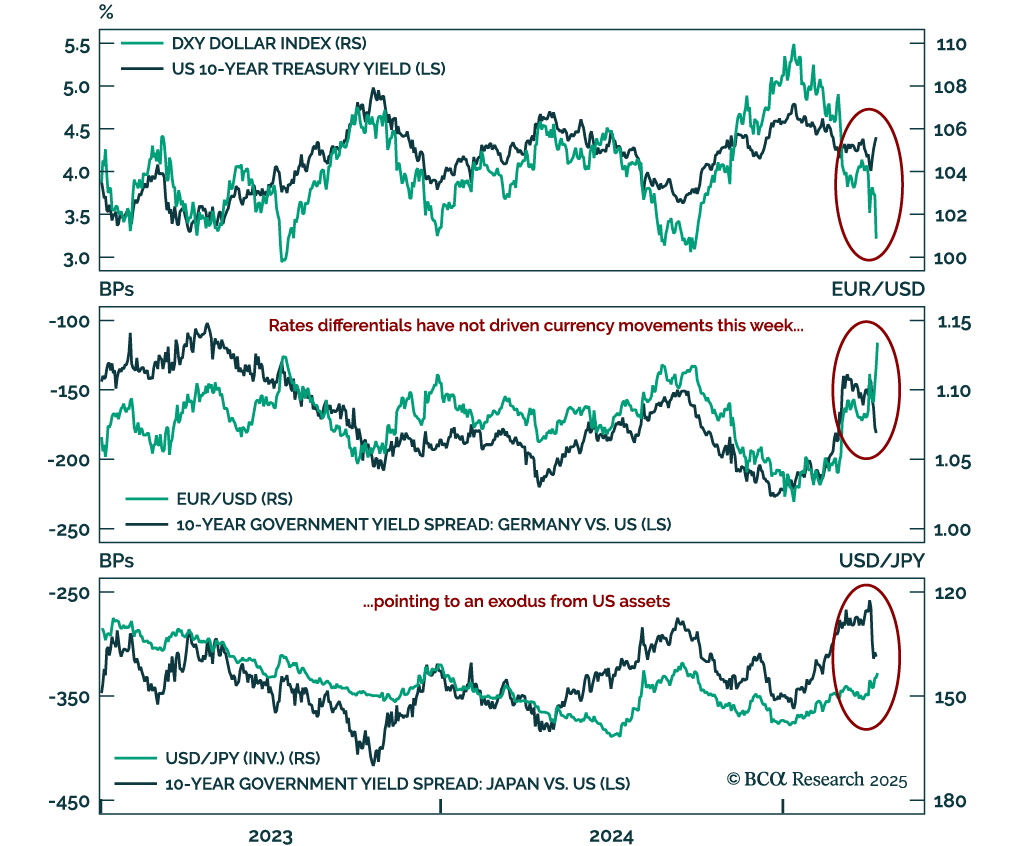

The recent breakdown in cross-asset correlations highlights mounting risk premia on US assets. Last week, the long-standing correlations underpinning our understanding of global markets violently broke down. The Treasury market turmoil had already broken the…

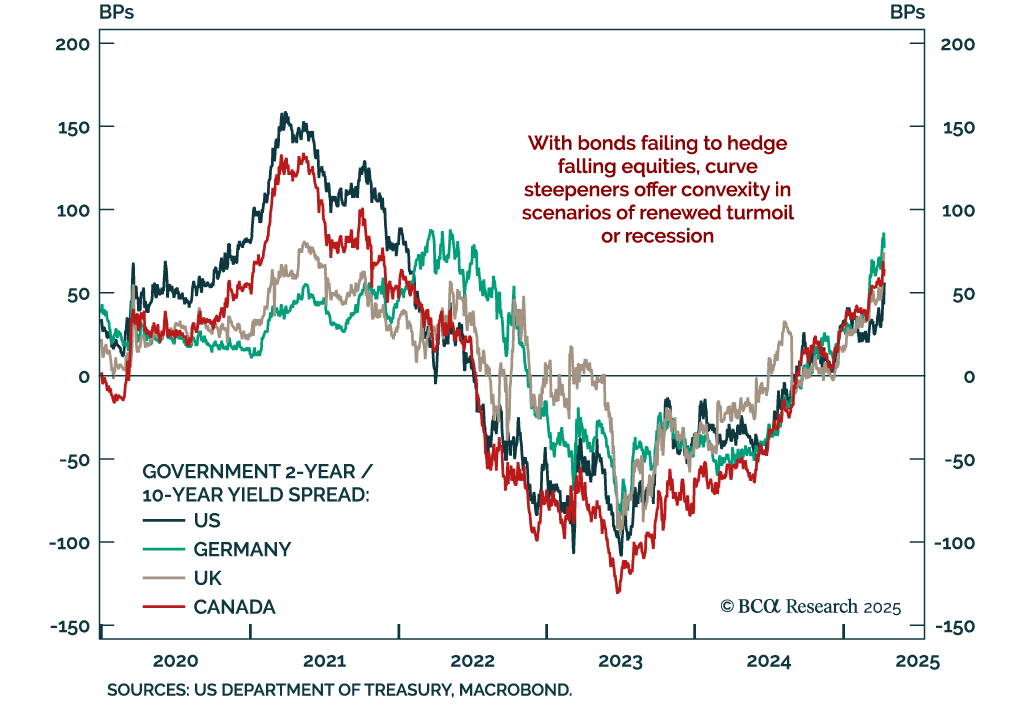

Bonds are failing to deliver defensive convexity; asset allocators should look to tactical curve steepeners for protection. Despite rising growth fears, Treasury yields have risen sharply at the long end. This is a clear break from the typical recession…

Barring a dramatic further de-escalation of the trade war, the US and much of the rest of the world will enter a recession over the next few months. Investors should remain defensively positioned for now.

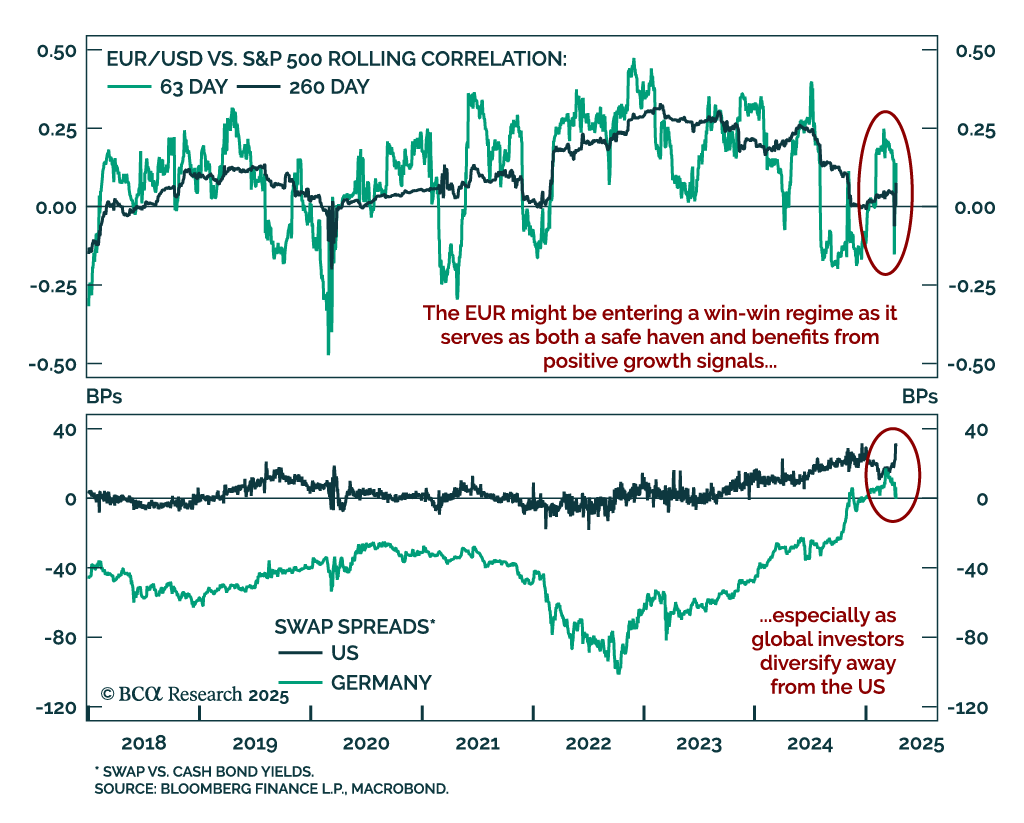

Dips in European assets remain long-term buying opportunities, even though short-term risks abound. A notable feature of the recent selloff is that US safe havens failed to rally. In a global growth scare, both the US dollar and Treasuries typically benefit.…

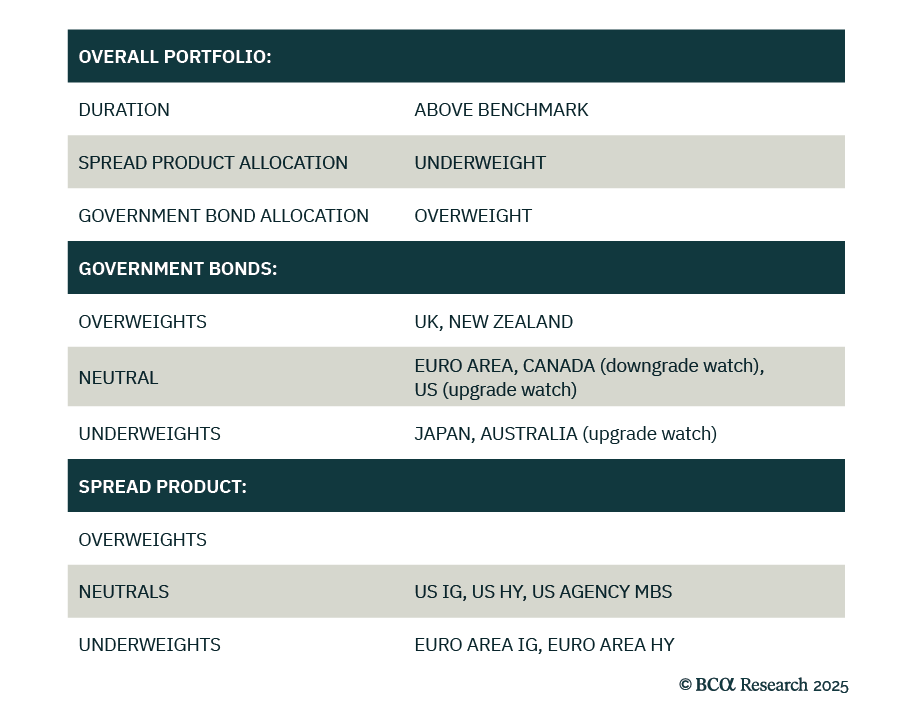

Our Global Fixed Income strategists continue to recommend long duration exposure, curve steepeners, and an underweight in corporate bonds relative to government bonds, as global recession risks rise. The trade war has increased the odds of a downturn, but the…

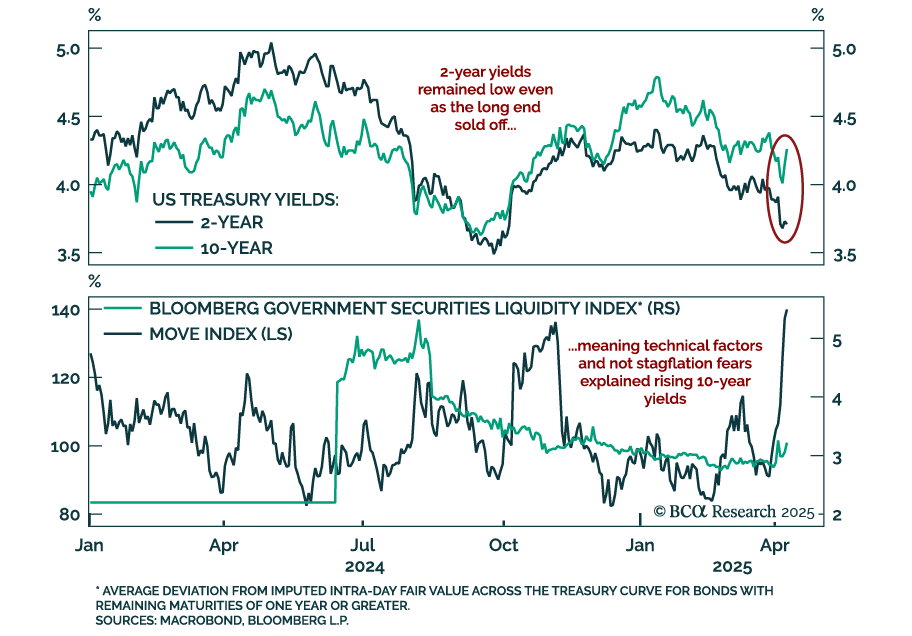

We maintain an overweight in government bonds, as recent yield spikes appear technical and unsustainable. US 10-year Treasury yields have surged even as global markets were selling off on growth fears. The move has spread to higher-yielding DMs like the UK,…

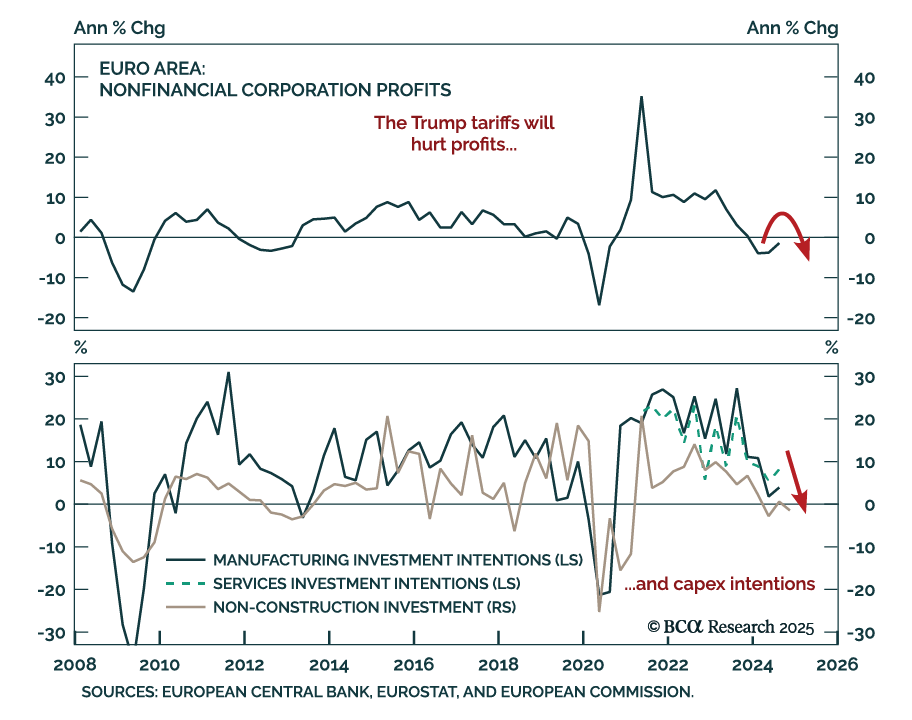

Our European strategists recommend staying defensive in the near term. Favor bonds over equities and defensives over cyclicals, as President Trump’s tariffs are set to push the Eurozone into recession by mid-2025. Industrial production, capital spending, and…

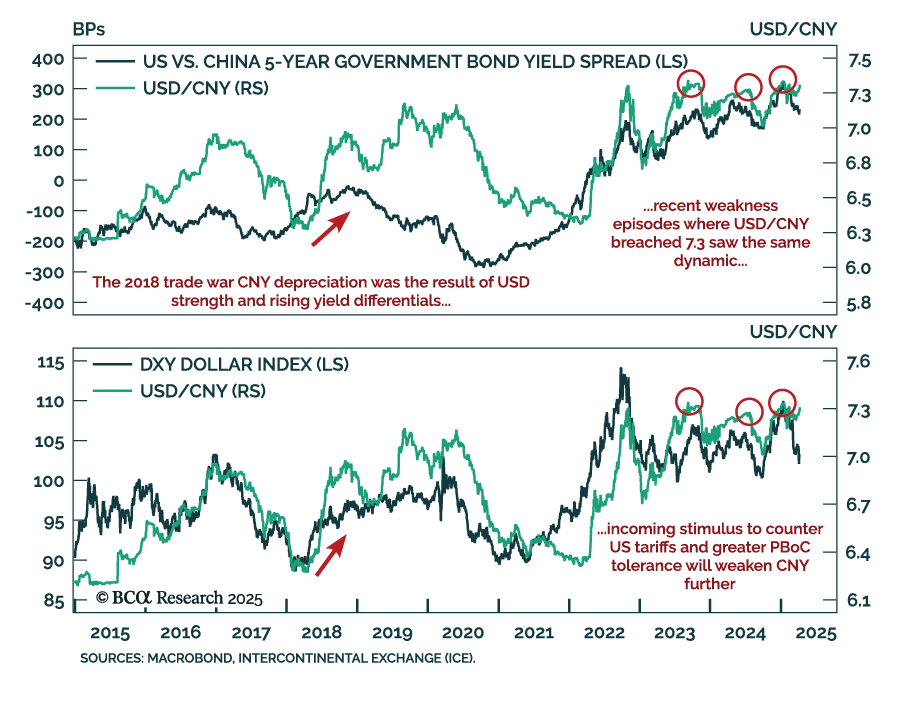

USD/CNY’s break above 7.3 signals more downside is in store for the yuan, supporting short high-beta FX and long CHF and JPY positions. The CNY has weakened in 2025 even as the US dollar has depreciated against most major currencies and gold. USD/CNY…