Financial Markets

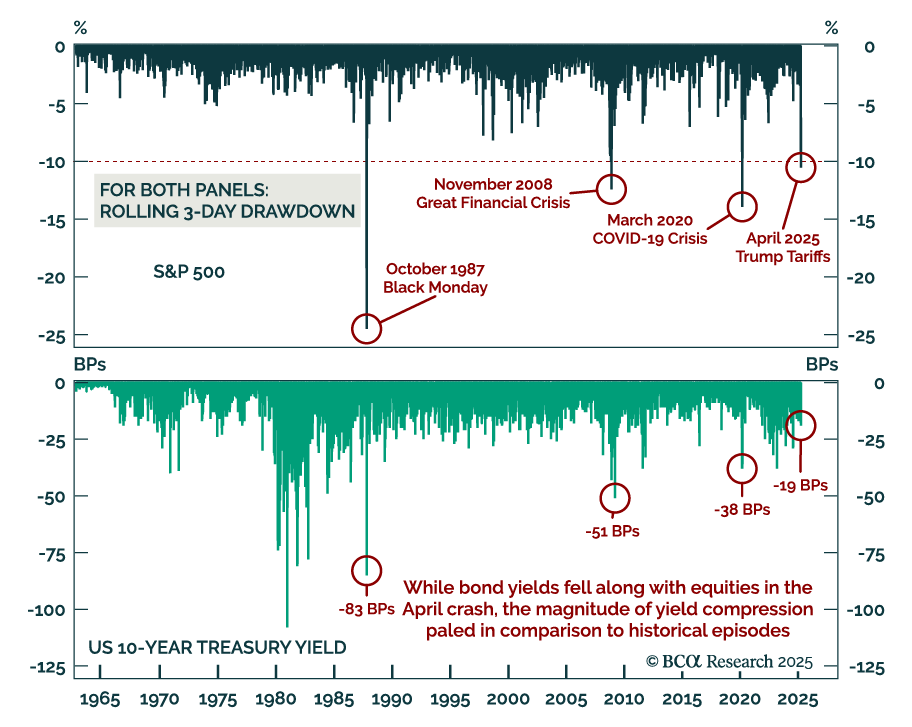

Equities’ post-Liberation Day selloff was historic, but cross-asset signals make it an anomaly. The post-Liberation Day S&P 500’s three-day, 10%+ drawdown joined a list of major episodes that includes the March 2020 COVID-19 crash, the 2008 financial…

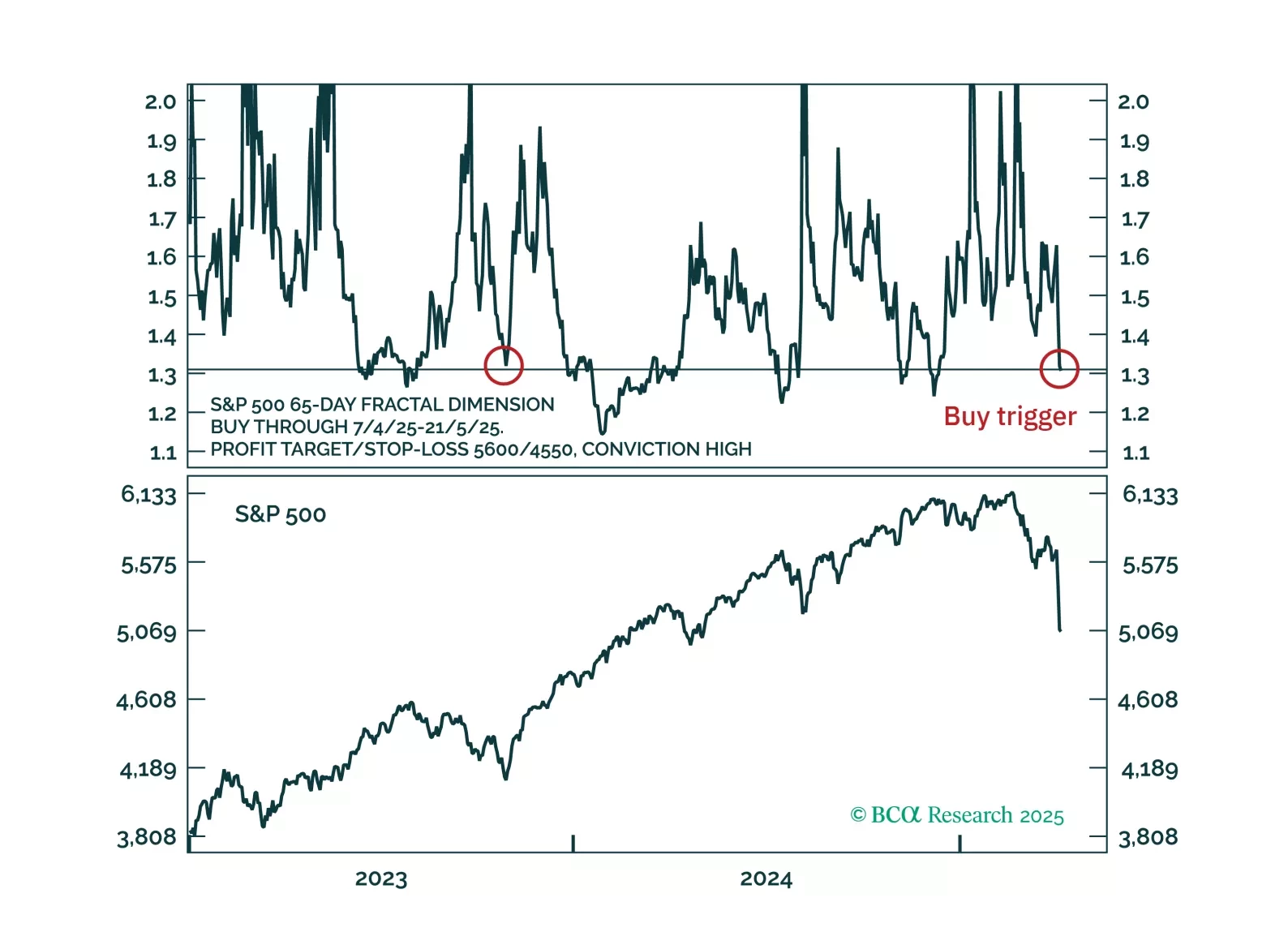

Countertrend buy triggers have been activated for the S&P 500, Nasdaq and Nasdaq versus 30-year T-bond.

Our Commodities strategists remain defensively positioned, recommending a long gold versus oil and copper trade over a cyclical timeframe. While gold may correct near term, it still offers safe-haven appeal in the face of rising policy uncertainty.Silver is…

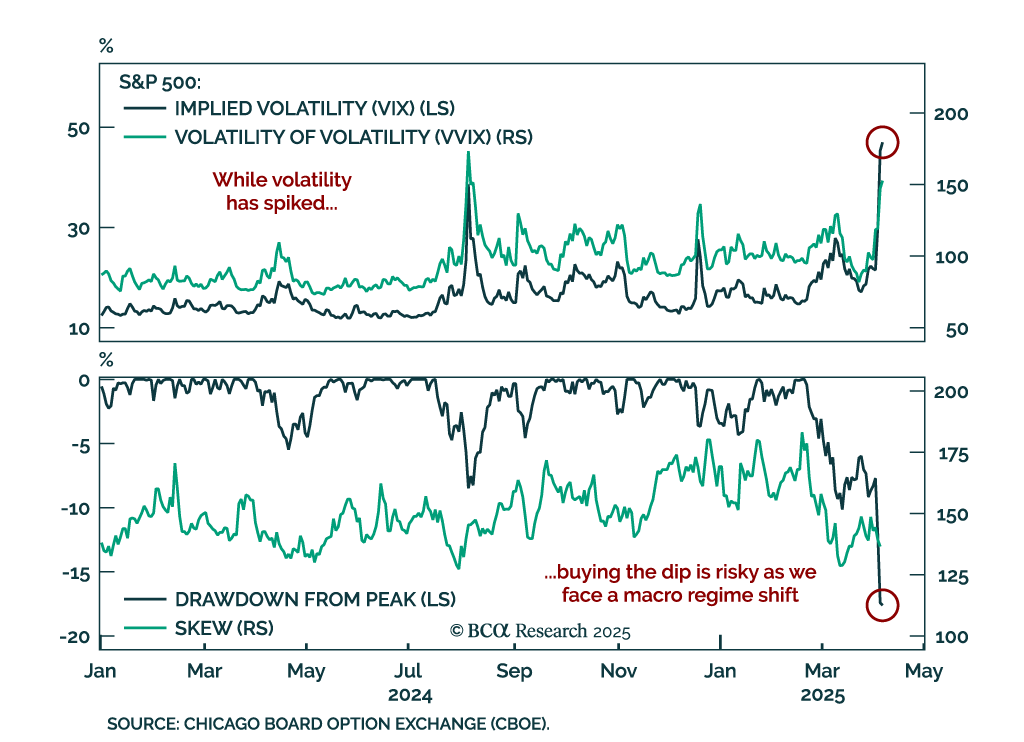

We maintain our defensive positioning as risk assets remain in a lose-lose situation. Monday’s trading session was volatile, and saw a brief rebound on a false headline about a 90-day tariff pause excluding China. The rally partially reversed as the White…

Our Emerging Markets strategists recommend staying defensive and adding exposure to EM local currency bonds, which will benefit from US dollar depreciation over the medium and long term. While tariffs are deflationary for US trading partners and will drive…

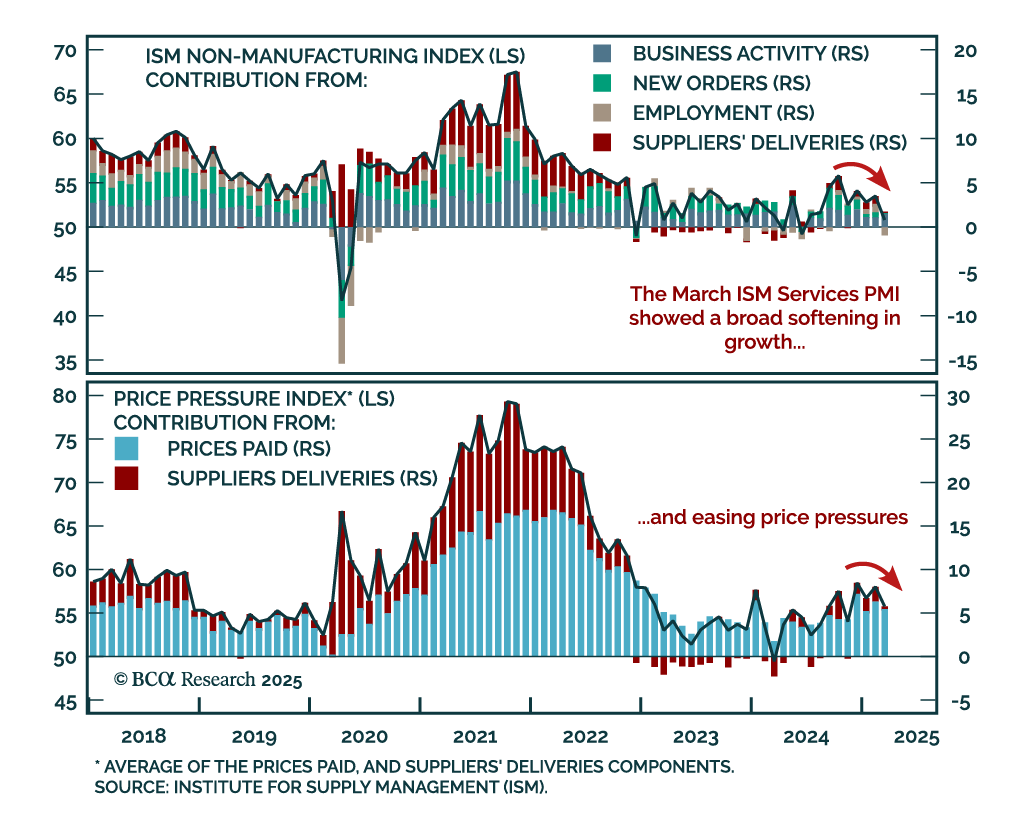

The March ISM Services report sent a recessionary signal, supporting our defensive positioning. The headline index fell sharply to 50.8 from 53.5, missing expectations. New orders dropped to 50.2, while employment collapsed to 46.2 from 53.9. Prices paid also…

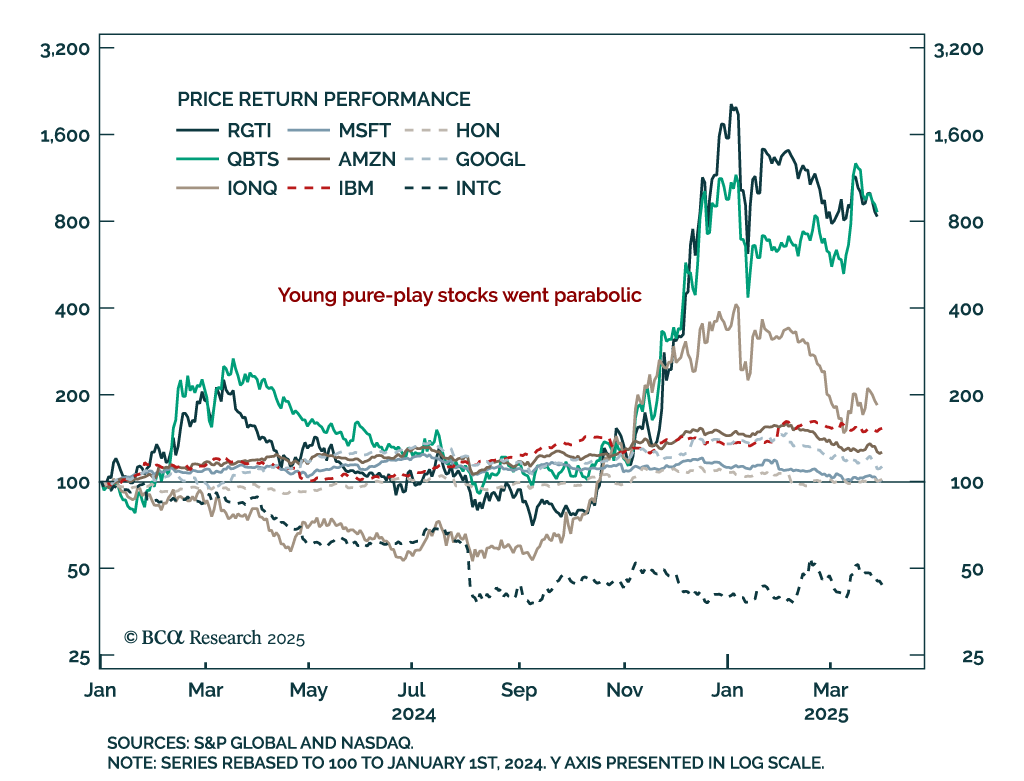

Our US Equity strategists recommend caution on quantum computing, as the industry is still too early-stage for reliable investment exposure. Although quantum computing (QC) is on the verge of major breakthroughs, pure-play QC stocks remain unprofitable and…

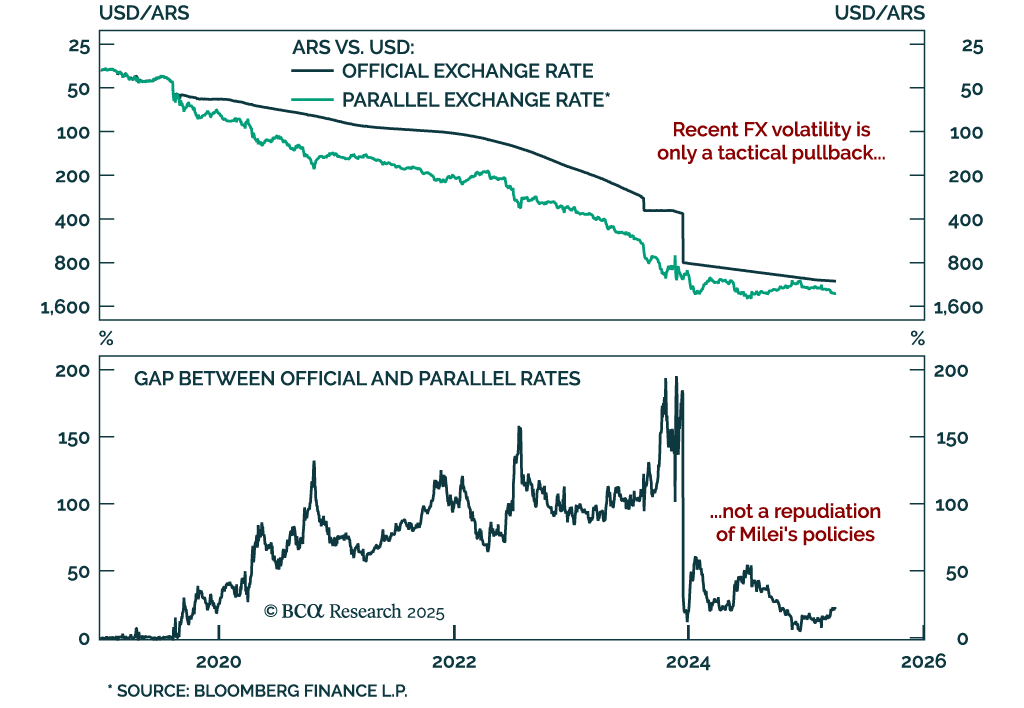

Remain constructive on Argentine assets as recent market moves are a tactical pullback, not a loss of confidence. The gap between official and parallel exchange rates has widened, prompting concerns that markets are questioning President Milei’s liberalizing…

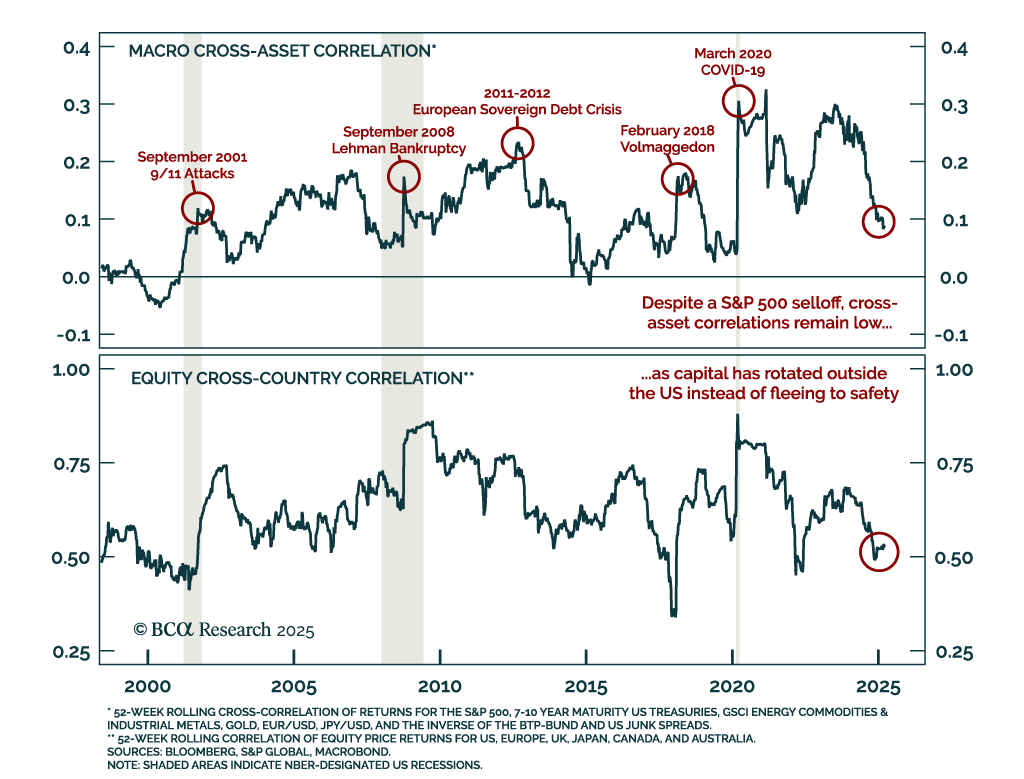

Low correlations and regional dispersion are shaping market dynamics, creating selective opportunities outside the US even as near-term risks remain. Asset classes tend to become highly correlated during crisis episodes, limiting diversification when it is…

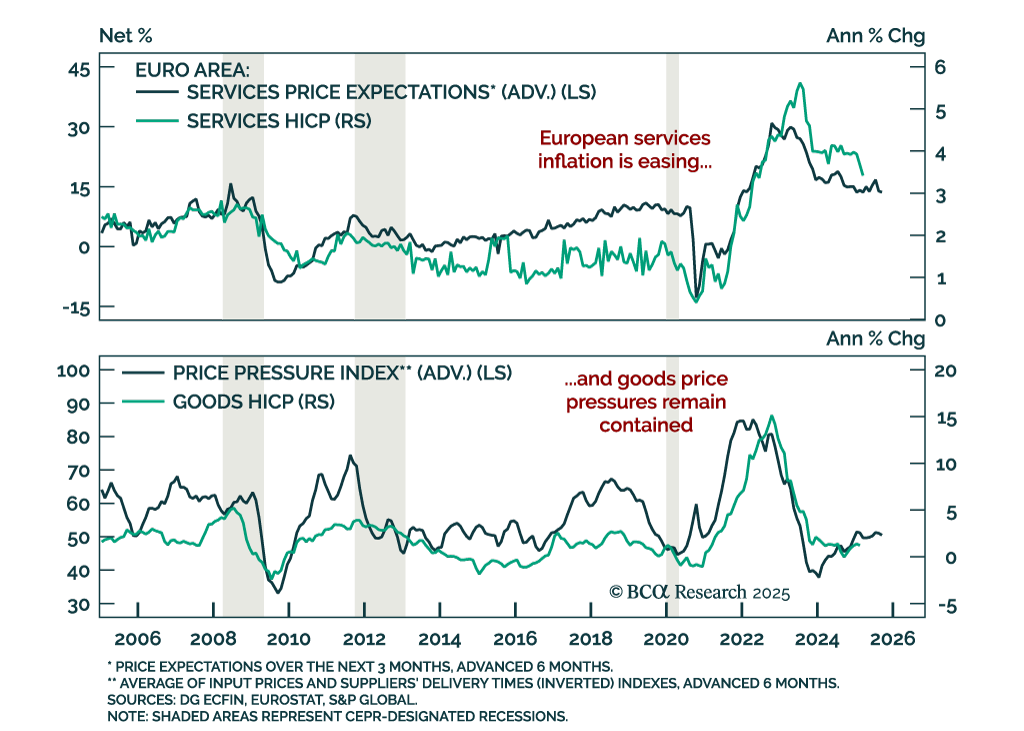

Eurozone inflation is cooling steadily, supporting our tactical overweight in German bunds versus European equities and increasing the odds of an April ECB cut. Headline HICP eased to 2.2% y/y in March from 2.3%, while core came in cooler than expected at…