Financial Markets

Highlights Along with momentum, quality has been the best performing factor over the past 30 years. It has also been less volatile and has exhibited milder drawdowns than other factors. There are multiple traits that are considered as signs of quality. However, profitability explains the lion’s share of the quality premium, though accounting quality and payout dilution also play a role. The reason why quality stocks outperform remains a mystery, though the preference for lottery stocks as well as the failure to account for the persistence of quality are plausible explanations. Both small caps and value stocks have negative tilts to quality. Adjusting for this tilt by buying small-cap quality indices or value indices with quality filters, can help investors exploit these factors more effectively. Feature “Investment must always consider the price as well as the quality of the security” – Benjamin Graham & David Dodd, Security Analysis, Principles and Technique, 1934 Legendary investor Benjamin Graham is one of the most significant figures in the history of finance. His two books, The Intelligent Investor and Security Analysis, stand as foundational pillars in the field of fundamental analysis. Moreover, as the mentor of the most famous investor ever, Warren Buffet, he has influenced a generation of investors into caring deeply about not overpaying for stocks. Thanks to these feats, Graham has come to be known as the “father of value investing”. And yet this moniker, though well-deserved, ignores a substantial portion of his legacy. Graham was not solely concerned with valuations.1 In fact, out of the seven criteria that he used to pick securities, only two of them focused on valuation measures. The rest, focused on metrics like profitability, leverage, and stability. These attributes encompass what is broadly known today as quality. But what exactly is quality? While certain traits have historically been associated with this factor, quality was not seen until more recently as something that you could easily define. Instead, a more holistic approach to quality was preferred.2 It wasn’t until the work of Robert Novy-Marx in the early 2010s, and US investment firm AQR thereafter, that the possibility of measuring quality, as well as systematically exploiting it, became prominent within the factor literature. Since then, quality has become a more popular strategy, with various commercial providers offering quality indices in recent years. However, much remains unknown about this newly discovered factor. Thus, in this report we take a deep dive into quality with the intent of providing some clarity on the following three issues: Definition of quality: What metrics are used to determine if a stock is a “quality” stock? Which of the many quality traits have the best track record? Characteristics of quality: What has been the historical performance of quality? What is its sector exposure? Why does it work? Implementation of quality: How can the quality factor be used in conjunction with other factors to increase returns? In order to answer these questions, we explore the historical performance of the MSCI Quality indices – though we also touch on quality indices by other providers. Moreover, we survey the academic literature around quality, and we propose a couple of ways by which investors can use this factor to exploit the value and small-cap premia more effectively. Definition Of Quality There is no universal agreement on how to measure quality, though there are some general traits that are agreed upon by the academic literature. An often used definition of quality is the “Quality Minus Junk” (QMJ) factor by AQR. In their research, Assness et al. use three traits, each of which is measured by five to six different metrics3 (Table 1). All the metrics are standardized and then averaged to arrive at a single quality measure. This quality measure is then used to build a quality portfolio. Table 1Metrics Used In AQR's Quality Minus Junk Factor (QMJ)

Junk Disposal: The Quality Factor In Equity Markets

Junk Disposal: The Quality Factor In Equity Markets

However, not all quality indices take so many measures into account. In fact, most commercial providers limit themselves to three or four variables to construct their quality indices. As an example, MSCI determines quality using three criteria: Return on equity, earnings variability, and leverage. All three variables are then winsorized,4 standardized, and then averaged to create a quality score. This quality score determines the weight of each stock within the index. Table 2 expands on the methodology of the quality benchmarks offered by various index providers. Table 2Quality Metrics For Popular Index Providers

Junk Disposal: The Quality Factor In Equity Markets

Junk Disposal: The Quality Factor In Equity Markets

The lack of a homogenous definition for quality makes performance evaluation of quality problematic. After all, the outperformance of quality could simply be a function of data mining by optimizing for a group of variables that produce excess returns in a backtest. This approach can lead to a large outperformance in-sample, but which might not necessarily replicate when applied in a real-world portfolio.5 To address this issue, some academics have tried to pinpoint which among the many quality traits truly add value in order to build a simpler and more parsimonious factor. In “What is Quality?”, Hsu et al. found that profitability is the most important quality characteristic, having a large and significant multifactor alpha6 (Table 3). Accounting quality and payout dilution have also been relatively reliable sources of excess returns. On the other hand, there is little evidence that most metrics for capital structure, profitability growth, or earnings stability, provide a premium that is not captured by other factors. Table 3Drivers Of The Quality Premium

Junk Disposal: The Quality Factor In Equity Markets

Junk Disposal: The Quality Factor In Equity Markets

Given the preponderance that profitability has in the overall performance of the quality factor, some academics have suggested that the quality factor should be reduced to profitability.7 However, not everybody agrees with this approach. In fact, other researchers have advocated for including more metrics such as ESG or corporate governance, in an effort to bring back the more holistic approach that Graham practiced.8 Overall, much disagreement about how to measure quality remains, and the subject is still an open debate. Characteristics Of Quality Historical Performance, Composition And Valuation Over the past 30 years, the MSCI Quality Index has, along with momentum, been the best performing factor in the equity markets (Chart 1, top panel). During this time frame, quality stocks have outperformed minimum volatility stocks by 2.6% per year, the global benchmark by 3.5% per year, and value stocks by 4% per year. The performance of quality has also been relatively robust, though the factor has performed better in some countries than others (Chart 1, bottom panel). Quality has performed best in European countries and Canada, while its outperformance has been more muted in Australia and Japan. Historically, quality has been the second most defensive factor after minimum volatility (Chart 2, panels 1 and 2). Moreover, it has exhibited lower volatility, and smaller drawdowns than the overall market. The defensive tilt of quality seems to arise because of the “flight to quality” phenomenon, where investors flock to higher quality assets during periods of markets stress. Interestingly, quality tends to outperform in equity markets and bond markets at the same time (Chart 2, bottom panel). This suggests that quality might be a common risk factor that is captured across asset classes. Chart 1Quality Has Outperformed Most Other Factors

Quality Has Outperformed Most Other Factors

Quality Has Outperformed Most Other Factors

Chart 2Quality Is A Defensive Factor

Quality Is A Defensive Factor

Quality Is A Defensive Factor

Chart 3Quality Overweights Expensive Sectors

Quality Overweights Expensive Sectors

Quality Overweights Expensive Sectors

What about composition? Within the global index, the quality factor currently has a large country bias to defensive markets like the US and Switzerland. This is mostly the result of its overweight to Information Technology, Consumer Staples and Health Care, and a large underweight position in Financials (Chart 3, top panel). This sector positioning also results in quality having high valuations relative to the overall market (Chart 3, bottom panel). It must be noted that valuations for quality stocks have risen significantly over the past few years. It is hard to know how this valuation compares to the past for the MSCI indices, given that valuation measures for MSCI Quality are only available starting in 2013. However, research by AQR has shown that relatively high prices for quality tend to result in lower returns.9 Thus, high valuations could pose a risk for quality going forward. Explanations For The Quality Anomaly Using a dividend-discount framework, one can show that, in theory, high-quality companies should trade at higher price-to-book values than low quality ones (for more details please see Appendix 1). Asness et at have shown that this is the case empirically – high-quality stocks trade at a valuation premium to low-quality stocks (Chart 4, top panel). Chart 4Analysts Are Most Optimistic On Low Quality Stocks

Junk Disposal: The Quality Factor In Equity Markets

Junk Disposal: The Quality Factor In Equity Markets

However, the mystery of quality lies in the fact that this premium does not appear to be as large as it should be. In other words, while analyst and market participants correctly assign higher multiples to high-quality stocks, this multiple is not large enough, and results in high-quality stocks being undervalued. Ultimately, this leads to the outperformance of high-quality stocks versus low-quality ones (Chart 4, bottom panel). Why do market participants overvalue low quality/junk stocks and undervalue high quality stocks? One reason could be a preference for lottery-like stocks. As we discussed in our January report on the low- volatility anomaly, investors tend to prefer “home-run” stocks – a result of behavioral biases as well as the incentives in the money management industry.10 Thus, distressed companies with low levels of profitability and large levels of debt, may attract some investors betting on a turnaround in the hope of a large windfall if the company survives.11 On the flip side, investors might perceive that high-quality companies – which are usually stable, profitable, and more expensive – cannot produce the same type of extreme payoff, and may even be prone to mean reversion, given that their success is evident and well known. But this last assumption is a mistake. Quality is a highly persistent characteristic, which means that a high-quality stock today is very likely to remain a high-quality stock in the future (Table 4). It is easy to see why this is the case. A company with very high levels of profitability has likely achieved this by building a moat around its business through a strong brand, proprietary technology, or network effects. It is possible that failure to take this into account results in an undervaluation of high-quality stocks. Table 4Quality Is Persistent

Junk Disposal: The Quality Factor In Equity Markets

Junk Disposal: The Quality Factor In Equity Markets

BOX 1 The Behavior Of Quality In Equity And Credit Markets Chart 5Quality Delivers A Different Premium In Different Asset Classes

Quality Delivers A Different Premium In Different Asset Classes

Quality Delivers A Different Premium In Different Asset Classes

While there is a very tight correlation between the performance of quality in credit and equity markets, the structural premium obtained from this factor in each market is very different. Over a long period, investors are rewarded for investing in high-quality equities, while the opposite occurs when investing in high-quality credit issues (Chart 5). Why would the same risk factor provide a positive premium in one market but provide a negative one in another? The exact reason remains unclear, but the behavioral explanations for the quality factor might provide a clue. As opposed to equity markets, returns in credit markets – even if very high – are naturally capped. As an example: An investor who buys a low-quality issue with a 20% yield-to-maturity, knows that in the absence of a default, the most he or she can earn from holding the issue to maturity is 20%. The fact that the maximum return is well established beforehand might prevent investors from displaying behavioral biases. Specifically, a well-defined upside might cause investors to think more rationally and mechanically about an investment. In contrast, securities where the upside is high but not well-defined might make it more likely for investors to see a very risky investment as a lottery, since extraordinary returns are technically within the realm of possibility. Whatever the reason is, the different premium that this factor offers in these two asset classes presents a potentially attractive opportunity for asset allocators. We will explore how investors could take advantage of this discrepancy in future reports on factor allocation. Implementation Of Quality Using Quality And Size Chart 6The Small-Cap Premium Is Higher When Adjusted For Quality

The Small-Cap Premium Is Higher When Adjusted For Quality

The Small-Cap Premium Is Higher When Adjusted For Quality

Historically, small-cap stocks have delivered excess returns over large cap-stocks – a well-documented phenomenon known as the size premium. However, this premium has been very unstable and extremely seasonal, occurring mostly in the month of January, and providing no excess returns in all other months. Moreover, some research has suggested that the size premium cannot be harvested easily in practice, since most of the premium is concentrated in the very smallest stocks (microcaps), which are highly illiquid.12 The issues surrounding the size premium have prompted some academics to question its existence. However, recent research on the interaction of quality and size has brought back interest to this topic. In the paper “Size Matters, If You Control Your Junk”, Assness et al show that many of the problems with the size premium are caused by the bias that small caps have to low quality. Once this low-quality bias is accounted for, the size premium becomes much larger and stable – a result that also holds when controlling for a quality proxy like profitability (Chart 6). Notably, the concentration of returns in January and in microcaps also disappears when the bias is removed.13 This bias to low quality is a significant problem in most popular small-cap indices. The profitability of indices like the S&P 600 has historically been lower than its large-cap counterparts (Chart 7, top panel). Moreover, a similar story holds for leverage: While the much maligned increase in corporate debt is evident in small-cap indices, it is virtually nonexistent when looking at large-cap indices like the S&P 500, where leverage measures stand barely above 30- year lows (Chart 7, bottom panel). How can this bias be removed? Stock-level filters for quality might be difficult to implement for many investors. Instead, an easier solution is to exploit the size premium through a small-cap quality index. S&P currently offers the S&P 600 Quality Index, which selects the 120 highest-quality stocks out of the S&P 600. Importantly, since this quality adjustment removes some of the low-quality bias from the S&P 600, the S&P 600 Quality index is able to maintain performance on the upside, while also limiting the sharp periods of underperformance that usually affect small caps during bear markets (Chart 8). Chart 7Small-Cap Stocks Have A Lot Of Junk

Small-Cap Stocks Have A Lot Of Junk

Small-Cap Stocks Have A Lot Of Junk

Chart 8Small-Cap Quality Is A Better Way To Exploit The Size Anomaly

Small-Cap Quality Is A Better Way To Exploit The Size Anomaly

Small-Cap Quality Is A Better Way To Exploit The Size Anomaly

Using Quality And Value The intersection between value and quality – a pair of factors that have a negative correlation – has been a topic of interest since quality was first discovered.14 They stand as perfect complements of each other: The value factor tries to find cheap stocks, regardless of their quality, while the quality factor tries to find quality stocks regardless of their price. Together they make for a powerful combination: Quality stocks at affordable prices. Some research has suggested that this combination of value and quality lies behind the success of Graham’s greatest student. According to the seminal paper titled “Buffet’s Alpha”, the biggest factor exposures of the Berkshire Hathaway portfolio from 1980 to 2011, outside of overall market risk, were quality and value15 (Chart 9). Exposure to these factors, along with low beta, as well as the ability of Berkshire Hathaway to obtain cheap leverage thanks to its insurance business, explained most of the excess returns that Warren Buffet was able to achieve. Chart 9Buffett's Motto: High Quality, Cheap, And Low Risk

Junk Disposal: The Quality Factor In Equity Markets

Junk Disposal: The Quality Factor In Equity Markets

Commercial providers have started to offer indices which combine value and quality. As an example, MSCI offers the Prime Value indices, where stocks are first screened for quality and then ranked according to a value score. This methodology has outperformed its normal value counterparts in both the euro area and the US (Chart 10). Chart 10Quality Adjustments By MSCI Improve Value In The Euro Area

Quality Adjustments By MSCI Improve Value In The Euro Area

Quality Adjustments By MSCI Improve Value In The Euro Area

Chart 11Stronger Quality Filters Are Needed In The US To Enhance Value

Stronger Quality Filters Are Needed In The US To Enhance Value

Stronger Quality Filters Are Needed In The US To Enhance Value

Interestingly, despite value’s recent doldrums, the quality adjustment done in the Prime Value index has helped value perform relatively well in the euro area for the past couple years. However, the same cannot be said in the US where performance of Value and Prime Value has been almost identical since 2003. This suggest a couple of options: It could be that, even when adjusting for quality, value behaves fundamentally differently in different countries. Alternatively, it could also mean that the US market is more efficient at pricing quality, which would imply that a simple quality filter would not do much, since quality at an attractive valuation would be harder to find. We suspect the reason might be the latter. In this case a stronger quality filter might be needed to substantially enhance the performance of value. The newly released Russell 1000 QARP (Quality At A Reasonable Price) Index follows this methodology. It applies a double quality filter and then compounds it by a value score. This index has substantially enhanced performance relatively to the Russell 1000 Value index (Chart 11). Moreover, it has also been able to fare better relative to the broad market and has avoided the large underperformance that value has undergone since 2018. Bottom Line Quality has been one of the most successful factors over the past three decades. But will this performance continue? While the exact reason behind the quality anomaly remains unclear, the evidence suggests that institutional incentives and behavioral biases, which are likely to persist in the future, might be responsible for the outperformance of quality in the market. Thus, investors should consider adding quality stocks to their portfolios. Moreover, quality can also be used to enhance the performance of other popular factors in the following ways: Correcting for the low-quality bias of small caps, makes the small-cap premium larger and much more stable over the long term. A practical way to correct for this low-quality bias is to buy small-cap quality portfolios such as the S&P 600 Quality Index. Value stocks also tend to have low quality. Investors can improve the performance of the value factor by using quality filters to find quality stocks that are also cheap. The quality filters in the MSCI Prime Value Index has significantly improved the performance of value in the euro area. Meanwhile, the Russell 1000 QARP index, which selects for value stocks using a stronger quality filter than MSCI, has kept pace with the overall market even amidst value’s collapse. Juan Correa Ossa, CFA Associate Editor juanc@bcaresearch.com Appendix 1

Junk Disposal: The Quality Factor In Equity Markets

Junk Disposal: The Quality Factor In Equity Markets

Footnotes 1 Robert Novy-Marx, “Quality Investing,” Working Paper, 1-28 (2014) 2 In Graham’s own words: “An indefinite and approximate measure of the intrinsic value may be sufficient. To use a homely simile, it is quite possible to decide by inspection that a woman is old enough to vote without knowing her age or that a man is heavier than he should be without knowing his exact weight.” 3 Asness, C.S., Frazzini, A. & Pedersen, L.H. “Quality minus junk,” Rev Account Stud 24, 34–112 (2019). 4 Winsorization is a way to remove the effects of outliers in the data. In this case all the values above the 95th percentile are set to the 95th percentile value and all the values below the 5th percentile are set to the 5th percentile value. 5 Robert Novy-Marx, “Backtesting Strategies Based on Multiple Signals,” NBER Working Paper No. w21329 (2015). 6 Jason Hsu, Vitali Kalesnik, Engin Kose, “What Is Quality?” Financial Analysts Journal, 75:2, 44-61 (2019). 7 Amanda White, “Quality is Explained by Profitability,” Top1000funds.com, (2015). 8 Dan Hanson and Rohan Dhanuka, “The ‘Science’ and ‘Art’ of High Quality Investing,” Journal of Applied Corporate Finance, 27:2 (2015). 9 C.S. Asness, A. Frazzini, and L.H. Pedersen, “Quality minus junk,” Rev Account Stud 24, 34–112 (2019). 10 Please see Global Asset Allocation Special Report, “Less Risk And More Reward? The Low-Volatility Factor In Equity Markets”, dated January 29, 2020. 11 This theory on the quality anomaly might explain the different performance of quality in credit and equity markets. For more details, please see Box 1. 12 Please see Global Asset Allocation Special Report, “Small Cap Outperformance: Fact Or Myth?” dated April 7, 2020. 13 Cliff S. Asness, Andrea Frazzini, Ronen Israel, and Lasse Heje Pedersen, “Size Matters, If You Control Your Junk,” CEPR Discussion Paper, No. DP12684 (2018). 14 Robert Novy - Marx, “The Other Side of Value: The Gross Profitability Premium,” Journal of Financial Economics, 108(1) , 1 - 28, (2013) and “The Quality Dimension of Value Investing,” University of Rochester, Working Paper (2014). 15 Andrea Frazzini, David Kabiller, and Lasse Heje Pedersen, "Buffett’s Alpha," Financial Analysts Journal, 74-4, 35-55 (2018).

Highlights Chart 1Permanent Job Losses Still Rising

Permanent Job Losses Still Rising

Permanent Job Losses Still Rising

The biggest event in bond markets last month was the Fed’s shift toward a regime of average inflation targeting. Treasuries sold off in the days following the announcement and, overall, the Bloomberg Barclays Treasury index underperformed cash by 111 basis points in August (Chart 1). We view this market reaction as sensible, since it seems clear that the Fed’s new commitment to tolerate an overshoot of its 2% inflation target will be bearish for bonds in the long run. However, for this bond bear market to play out the US economy must first generate some inflation. This will take time. Despite the drop in the headline U3 unemployment rate, August’s employment report showed that permanent job losses continue to rise (bottom panel). This is a clear sign that the economic recovery is not yet on a solid footing. We advise bond investors to keep portfolio duration close to benchmark for the time being. We also recommend several yield curve trades across the nominal, real and inflation compensation curves (see pages 10 & 11). Feature Investment Grade: Overweight Chart 2Investment Grade Market Overview

Investment Grade Market Overview

Investment Grade Market Overview

Investment grade corporate bonds outperformed the duration-equivalent Treasury index by 5 basis points in August, bringing year-to-date excess returns up to -356 bps. Spreads on Baa-rated corporate bonds continued their tightening trend through August, even as spreads were roughly flat for bonds rated A and above. As a result, Baa-rated bonds outperformed duration-matched Treasuries by 30 bps on the month while higher-rated credits underperformed. Valuation remains more attractive for the Baa space than for higher-rated credits (Chart 2), but spreads for all credit tiers look cheaper than they did near the end of 2019. Given the Fed’s strong support for the market through both its emergency lending facilities, and now, its extraordinarily dovish forward rate guidance, we see further room for spread compression across all credit tiers. At the sector level, we continue to recommend a focus on high-quality Baa-rated issuers. That is, Baa-rated bonds that are unlikely to face a ratings downgrade during the next 12 months. Subordinate bank bonds are a prime example of debt that falls into this sweet spot.1 We also recommend overweight allocations to Healthcare and Energy bonds2 and underweight allocations to Technology3 and Pharmaceutical bonds.4 Table 3ACorporate Sector Relative Valuation And Recommended Allocation*

The Fed’s New Framework Is Bond Bearish … But Not Yet

The Fed’s New Framework Is Bond Bearish … But Not Yet

Table 3BCorporate Sector Risk Vs. Reward*

The Fed’s New Framework Is Bond Bearish … But Not Yet

The Fed’s New Framework Is Bond Bearish … But Not Yet

High-Yield: Neutral Chart 3High-Yield Market Overview

High-Yield Market Overview

High-Yield Market Overview

High-Yield outperformed the duration-equivalent Treasury index by 121 basis points in August, bringing year-to-date excess returns up to -351 bps. All junk credit tiers delivered strong returns in August, but the lowest-rated credits performed best. Caa-rated & below junk bonds outperformed Treasuries by 255 bps on the month compared to 98 bps of outperformance for Ba-rated bonds (Chart 3). The recent strong performance of low-rated junk bonds makes us question whether our focus on the Ba-rated credit tier is overly conservative. If the economy is indeed on a quick road to recovery, then we are leaving some return on the table by avoiding the B-rated and lower credit tiers. However, we aren’t yet confident enough in the economic recovery to move down in quality. Last week’s employment report showed that permanent job losses continue to rise and Congress has still not passed a much needed follow-up to the CARES act. What’s more, current junk spreads imply a very rapid decline in the corporate default rate during the next 12 months, from its current level of 8.4% all the way to 4.4% (panel 3).5 In this regard, August’s steep drop in layoff announcements is a positive development (bottom panel), though job cuts are still running well above pre-pandemic levels. At the sector level, we advise overweight allocations to high-yield Technology6 and Energy7 bonds. We are underweight the Healthcare and Pharmaceutical sectors.8 MBS: Underweight Chart 4MBS Market Overview

MBS Market Overview

MBS Market Overview

Mortgage-Backed Securities outperformed the duration-equivalent Treasury index by 9 basis points in August, bringing year-to-date excess returns up to -37 bps. The conventional 30-year MBS index option-adjusted spread (OAS) tightened 7 bps in August, but it still offers a small spread pick-up compared to other similarly risky sectors. The MBS OAS of 77 bps is greater than the 75 bps offered by Aa-rated corporate bonds, the 67 bps offered by Agency CMBS and the 35 bps offered by Aaa-rated consumer ABS. Despite the spread advantage, we are concerned that the elevated primary mortgage spread is a warning that refinancing risk could flare later this year (Chart 4). Even if Treasury yields are unchanged, a further 50 bps drop in the mortgage rate due to spread compression cannot be ruled out. Such a move would lead to a significant increase in prepayment losses. With that in mind, we are concerned about the low level of expected prepayment losses (option cost) priced into the MBS index (panel 3). A fourth quarter refi wave would undoubtedly send that option cost higher, eating into the returns implied by the OAS. The recent spike in the mortgage delinquency rate does not pose a near-term risk to spreads as it is being driven by households that have been granted forbearance from the federal government (panel 4). The risk for MBS holders only comes into play if many households are unable to resume their regular mortgage payments when the forbearance period expires early next year. But even in that case, further government action to either support household incomes or extend the forbearance period could mitigate the risk. Government-Related: Underweight Chart 5Government-Related Market Overview

Government-Related Market Overview

Government-Related Market Overview

The Government-Related index outperformed the duration-equivalent Treasury index by 31 basis points in August, bringing year-to-date excess returns up to -295 bps. Sovereign debt outperformed duration-equivalent Treasuries by 105 bps on the month, bringing year-to-date excess returns up to -468 bps. Foreign Agencies outperformed the Treasury benchmark by 13 bps in August, bringing year-to-date excess returns up to -694 bps. Local Authority debt outperformed Treasuries by 33 bps in August, bringing year-to-date excess returns up to -337 bps. Domestic Agency bonds outperformed by 8 bps, bringing year-to-date excess returns up to -54 bps. Supranationals outperformed by 5 bps, bringing year-to-date excess returns up to -9 bps. US dollar weakness is usually a boon for Sovereign and Foreign Agency returns. However, most of the dollar’s recent depreciation has occurred against other Developed Market currencies, not Emerging Markets (Chart 5). Added to that, dollar weakness against all trading partners helps US corporate sector profits, and Baa-rated corporate bonds continue to offer a spread pick-up versus EM sovereigns (panel 4). Within the Emerging Market Sovereign space: Turkey, South Africa, Mexico, Colombia and Russia all offer a spread pick-up relative to quality and duration-matched US corporate bonds. Of those attractively priced countries, Mexico stands out as particularly compelling on a risk/reward basis.9 Municipal Bonds: Overweight Chart 6Municipal Market Overview

Municipal Market Overview

Municipal Market Overview

Municipal bonds underperformed the duration-equivalent Treasury index by 19 basis points in August, dragging year-to-date excess returns down to -492 bps (before adjusting for the tax advantage). Municipal bond spreads versus Treasuries have widened during the past month, more so at the long-end than at the short-end, and the entire Aaa muni curve remains above the Treasury curve, despite municipal debt’s tax-exempt status (Chart 6). Municipal bonds also remain attractively priced relative to corporate bonds across the entire investment grade credit spectrum, as we demonstrated in a recent report.10 The Fed reduced the pricing on its Municipal Liquidity Facility (MLF) by 50 basis points last month. Most likely, it felt pressure to act as Congress has still not passed a state & local government aid package. However, the Fed’s move will not have much impact on municipal bond spreads. Even after the reduction, municipal yields continue to run well below the cost offered by the MLF (panel 3). Extremely attractive valuation causes us to stick with our municipal bond overweight, though spreads will widen in the near-term if much needed stimulus doesn’t arrive soon. In the long-run, we remain optimistic that elevated state rainy day funds will help cushion the fiscal blow and lessen the risk of ratings downgrades (bottom panel). Treasury Curve: Buy 5-Year Bullet Versus 2/10 Barbell Chart 7Treasury Yield Curve Overview

Treasury Yield Curve Overview

Treasury Yield Curve Overview

The Treasury curve bear-steepened in August. The 2/10 and 5/30 Treasury slopes steepened 14 bps and 22 bps, reaching 58 bps and 121 bps, respectively. One easy way to think about nominal Treasury yields is as the market’s expectation of future changes in the federal funds rate.11 With that in mind, the Fed’s recent shift toward a regime of average inflation targeting will likely lead to nominal yield curve steepening. That is, the Fed will keep a firm grip on the front-end of the curve, but long-maturity yields could rise as investors price-in the possibility that the Fed will have to eventually respond to high inflation by quickly tightening policy. For this reason, we retain a core position in nominal yield curve steepeners. Specifically, we recommend buying the 5-year bullet and shorting a duration-matched 2/10 barbell. This position is designed to profit from 2/10 Treasury curve steepening, which should play out over the next 6-12 months, assuming the economic recovery is sustained. Valuation is a concern with this recommended positioning. The 5-year yield is below the yield on the duration-matched 2/10 barbell (Chart 7), and the 5-year bullet looks expensive on our yield curve models (Appendix B). However, the 5-year bullet traded at much more expensive levels during the last zero-lower-bound period between 2010 and 2013 (bottom panel). With short rates once again pinned at zero, we expect the 5-year to once again hit extreme levels of overvaluation. TIPS: Overweight Chart 8TIPS Market Overview

TIPS Market Overview

TIPS Market Overview

TIPS outperformed the duration-equivalent nominal Treasury index by 240 basis points in August, bringing year-to-date excess returns up to -76 bps. The 10-year and 5-year/5-year forward TIPS breakeven inflation rates rose 25 bps and 22 bps on the month. They currently sit at 1.67% and 1.78%, respectively. TIPS breakeven inflation rates have moved up rapidly during the past couple months, a trend that was supercharged by the Fed’s Jackson Hole announcement. In fact, the 10-year TIPS breakeven inflation rate is now right around fair value according to our Adaptive Expectations Model (Chart 8).12 TIPS will soon turn expensive if current trends continue. That is, unless stronger CPI inflation sends our model’s fair value reading higher. We place strong odds on the latter occurring during the next few months, with trimmed mean inflation measures still running well above core (panel 3). However, we cautioned in a recent report that inflation is likely to moderate in 2021 after core inflation re-converges with the trimmed mean.13 In addition to our overweight stance on TIPS, we continue to recommend real yield curve steepeners and inflation curve flatteners. With the Fed now officially targeting an overshoot of its 2% inflation goal, we would expect the cost of 2-year inflation protection to rise above the cost of 10-year inflation protection (panel 4). With the Fed also keeping a firmer grip over short-dated nominal yields than over long-dated ones, this means that short-maturity real yields will come under downward pressure relative to the long end (bottom panel). ABS: Overweight Chart 9ABS Market Overview

ABS Market Overview

ABS Market Overview

Asset-Backed Securities outperformed the duration-equivalent Treasury index by 30 basis points in August, bringing year-to-date excess returns up to +53 bps. Aaa-rated ABS outperformed the Treasury benchmark by 24 bps on the month, bringing year-to-date excess returns up to +46 bps. Non-Aaa ABS outperformed by 73 bps, bringing year-to-date excess returns up to +95 bps. Aaa ABS are a high conviction overweight, given that spreads remain elevated compared to historical levels and that the sector benefits from Fed support through the Term Asset-Backed Loan Facility (TALF). However, spreads are even more attractive in non-Aaa ABS (Chart 9) and we recommend owning those securities as well. This is despite the fact that only Aaa-rated bonds are eligible for TALF. We explained our rationale for owning non-Aaa consumer ABS in a recent report.14 We noted that the stimulus received from the CARES act caused real disposable personal income to increase significantly between February and July and, faced with fewer spending opportunities, households used that windfall to pay down consumer debt (bottom panel). Granted, further income support from fiscal policymakers is needed now that the CARES act’s enhanced unemployment benefits have expired. But given the substantial boost to savings that has already occurred, we are confident that more stimulus will arrive in time to prevent a wave of consumer bankruptcies. Non-Agency CMBS: Neutral Chart 10CMBS Market Overview

CMBS Market Overview

CMBS Market Overview

Non-Agency Commercial Mortgage-Backed Securities outperformed the duration-equivalent Treasury index by 77 basis points in August, bringing year-to-date excess returns up to -320 bps. Aaa Non-Agency CMBS outperformed Treasuries by 57 bps on the month, bringing year-to-date excess returns up to -108 bps. Non-Aaa Non-Agency CMBS outperformed by 160 bps, bringing year-to-date excess returns up to -1008 bps (Chart 10). We continue to recommend an overweight allocation to Aaa non-agency CMBS and an underweight allocation to non-Aaa CMBS. Our reasoning is simple. Aaa CMBS are eligible for TALF, meaning that spreads can still tighten even as the hardship in commercial real estate continues. Without Fed support, non-Aaa CMBS will struggle to deal with a climbing delinquency rate (panel 3).15 Agency CMBS: Overweight Agency CMBS outperformed the duration-equivalent Treasury index by 38 basis points in August, bringing year-to-date excess returns up to -4 bps. The average index spread tightened 6 bps on the month to 66 bps, still well above typical historical levels (bottom panel). The Fed is supporting the Agency CMBS market by directly purchasing the securities as part of its Agency MBS purchase program. The combination of strong Fed support and elevated spreads makes the sector a high conviction overweight. Appendix A: Buy What The Fed Is Buying The Fed rolled out a number of aggressive lending facilities on March 23. These facilities focused on different specific sectors of the US bond market. The fact that the Fed has decided to support some parts of the market and not others has caused some traditional bond market correlations to break down. It has also led us to adopt of a strategy of “Buy What The Fed Is Buying”. That is, we favor those sectors that offer attractive spreads and that benefit from Fed support. The below Table tracks the performance of different bond sectors since the March 23 announcement. We will use this to monitor bond market correlations and evaluate our strategy’s success. TablePerformance Since March 23 Announcement Of Emergency Fed Facilities

The Fed’s New Framework Is Bond Bearish … But Not Yet

The Fed’s New Framework Is Bond Bearish … But Not Yet

Appendix B: Butterfly Strategy Valuations The following tables present the current read-outs from our butterfly spread models. We use these models to identify opportunities to take duration-neutral positions across the Treasury curve. The following two Special Reports explain the models in more detail: US Bond Strategy Special Report, “Bullets, Barbells And Butterflies”, dated July 25, 2017, available at usbs.bcaresearch.com US Bond Strategy Special Report, “More Bullets, Barbells And Butterflies”, dated May 15, 2018, available at usbs.bcaresearch.com Table 4 shows the raw residuals from each model. A positive value indicates that the bullet is cheap relative to the duration-matched barbell. A negative value indicates that the barbell is cheap relative to the bullet. Table 4Butterfly Strategy Valuation: Raw Residuals In Basis Points (As Of September 3, 2020)

The Fed’s New Framework Is Bond Bearish … But Not Yet

The Fed’s New Framework Is Bond Bearish … But Not Yet

Table 5 scales the raw residuals in Table 4 by their historical means and standard deviations. This facilitates comparison between the different butterfly spreads. Table 5Butterfly Strategy Valuation: Standardized Residuals (As Of September 3, 2020)

The Fed’s New Framework Is Bond Bearish … But Not Yet

The Fed’s New Framework Is Bond Bearish … But Not Yet

Table 6 flips the models on their heads. It shows the change in the slope between the two barbell maturities that must be realized during the next six months to make returns between the bullet and barbell equal. For example, a reading of 72 bps in the 5 over 2/10 cell means that we would only expect the 5-year to outperform the 2/10 if the 2/10 slope steepens by more than 72 bps during the next six months. Otherwise, we would expect the 2/10 barbell to outperform the 5-year bullet. Table 6Discounted Slope Change During Next 6 Months (BPs)

The Fed’s New Framework Is Bond Bearish … But Not Yet

The Fed’s New Framework Is Bond Bearish … But Not Yet

Appendix C: Excess Return Bond Map The Excess Return Bond Map is used to assess the relative risk/reward trade-off between different sectors of the US bond market. It is a purely computational exercise and does not impose any macroeconomic view. The Map’s vertical axis shows 12-month expected excess returns. These are proxied by each sector’s option-adjusted spread. Sectors plotting further toward the top of the Map have higher expected returns and vice-versa. Our novel risk measure called the “Risk Of Losing 100 bps” is shown on the Map’s horizontal axis. To calculate it, we first compute the spread widening required on a 12-month horizon for each sector to lose 100 bps or more relative to a duration-matched position in Treasury securities. Then, we divide that amount of spread widening by each sector’s historical spread volatility. The end result is the number of standard deviations of 12-month spread widening required for each sector to lose 100 bps or more versus a position in Treasuries. Lower risk sectors plot further to the right of the Map, and higher risk sectors plot further to the left. Chart 11Excess Return Bond Map (As Of September 3, 2020)

The Fed’s New Framework Is Bond Bearish … But Not Yet

The Fed’s New Framework Is Bond Bearish … But Not Yet

Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see US Bond Strategy Weekly Report, “The Case Against The Money Supply”, dated June 30, 2020, available at usbs.bcaresearch.com 2 Please see US Bond Strategy Special Report, “The Outlook For Energy Bonds Part 1: A Model Of Energy Bond Excess Returns”, dated July 14, 2020 and US Bond Strategy Special Report, “The Outlook For Energy Bonds Part 2: Buy The Dip In High-Yield Energy”, dated July 21, 2020, available at usbs.bcaresearch.com 3 Please see US Bond Strategy Weekly Report, “Take A Look At High-Yield Technology Bonds”, dated June 23, 2020, available at usbs.bcaresearch.com 4 Please see US Bond Strategy Weekly Report, “Assessing Healthcare & Pharma Bonds In A Pandemic”, dated June 9, 2020, available at usbs.bcaresearch.com 5 We assume a 25% recovery rate and target a spread of 150 bps in excess of default losses. For more details on this calculation please see US Bond Strategy Weekly Report, “No Holding Back”, dated June 16, 2020, available at usbs.bcaresearch.com 6 Please see US Bond Strategy Weekly Report, “Take A Look At High-Yield Technology Bonds”, dated June 23, 2020, available at usbs.bcaresearch.com 7 Please see US Bond Strategy Special Report, “The Outlook For Energy Bonds Part 1: A Model Of Energy Bond Excess Returns”, dated July 14, 2020, and US Bond Strategy Special Report, “The Outlook For Energy Bonds Part 2: Buy The Dip In High-Yield Energy”, dated July 21, 2020, available at usbs.bcaresearch.com 8 Please see US Bond Strategy Weekly Report, “Assessing Healthcare & Pharma Bonds In A Pandemic”, dated June 9, 2020, available at usbs.bcaresearch.com 9 Please see US Bond Strategy Weekly Report, “The Treasury Market Amid Surging Supply”, dated May 12, 2020, available at usbs.bcaresearch.com 10 Please see US Bond Strategy Weekly Report, “Bonds Are Vulnerable As North America Re-Opens”, dated May 26, 2020, available at usbs.bcaresearch.com 11 For more details on this forecasting framework please see US Bond Strategy Weekly Report, “Positioning For Reflation And Avoiding Deflation”, dated August 11, 2020, available at usbs.bcaresearch.com 12 For more details on our model please see US Bond Strategy Weekly Report, “How Are Inflation Expectations Adapting?”, dated February 11, 2020, available at usbs.bcaresearch.com 13 Please see US Bond Strategy Weekly Report, “Positioning For Reflation And Avoiding Deflation”, dated August 11, 2020, available at usbs.bcaresearch.com 14 Please see US Bond Strategy Weekly Report, “No Holding Back”, dated June 16, 2020, available at usbs.bcaresearch.com 15 For a deeper dive into the outlook for US commercial real estate please see Global Investment Strategy Special Report, “Working From Home, Urban Flight, And Commercial Real Estate Loans: How Bad Can Things Get?”, dated August 28, 2020, available at gis.bcaresearch.com Fixed Income Sector Performance Recommended Portfolio Specification Corporate Sector Relative Valuation And Recommended Allocation

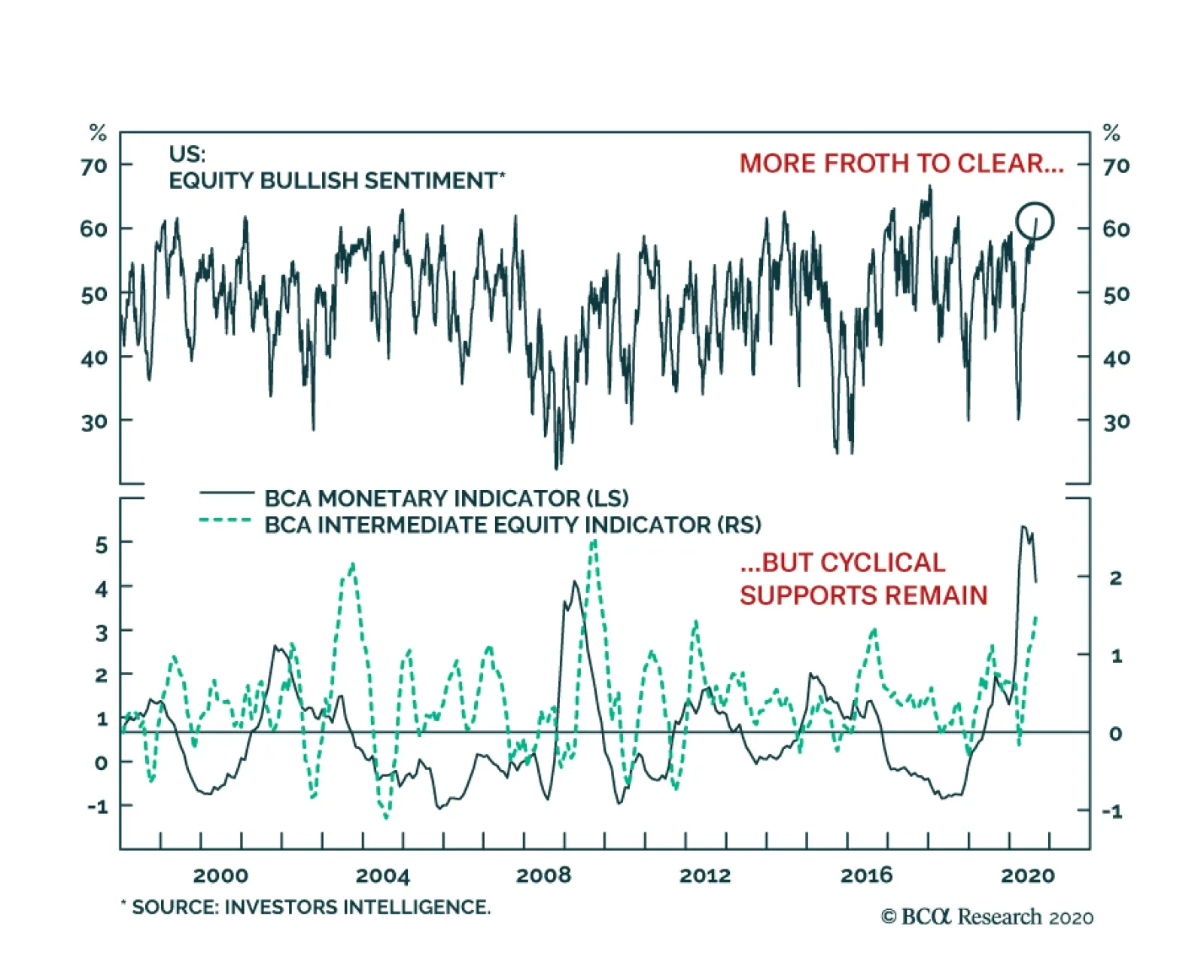

Highlights Stocks, particularly tech stocks, are technically overbought and highly vulnerable to a further correction. Nevertheless, investors should continue to overweight global equities relative to bonds on a 12-month horizon, while rotating equity allocations into cheaper sectors and regions. What should policymakers do if they wish to maximize growth and restore full employment? In the feature section of this report, we argue that the optimal course of action for most countries is to loosen fiscal policy until labor slack has been eliminated and the central bank’s inflation target has been met. Once this has been achieved, governments should trim the budget deficit to keep inflation from accelerating too much. What will policymakers actually do? While today’s budget deficits are smaller than what most economies need, they will ultimately prove to be too big once private sector demand recovers. The upshot is that inflation will increase by the middle of the decade, first in the US and then everywhere else. The secular bull market in equities will end only when central banks are forced to scramble to contain inflation. Fortunately, that day of reckoning is at least a few years away. Feature Apparently, Stocks Don’t Always Go Up After a relentless rally, stocks buckled under the pressure on Thursday. The MSCI All-Country World index lost 3%, the S&P 500 shed 3.5%, and the tech-heavy Nasdaq Composite plunged 5%. Two weeks ago, in a report titled “The Return Of Nasdog,” we argued that the leadership role was set to pivot away from tech and health care, as pandemic angst subsided and investors began to price in a recovery in the sectors of the stock market that had been crushed by lockdown measures. Chart 1A Weaker Dollar Is Generally Associated With Non-US Equity Outperformance, But Not Since The Covid Crash

A Weaker Dollar Is Generally Associated With Non-US Equity Outperformance, But Not Since The Covid Crash

A Weaker Dollar Is Generally Associated With Non-US Equity Outperformance, But Not Since The Covid Crash

Historically, non-US equities have outperformed their US peers when the dollar has weakened (Chart 1). This relationship broke down this year because of the outsized weight that tech and health care command in US indices. If the relative performance of tech and health care stocks peaks over the coming weeks, this should translate into a clear outperformance for non-US stock markets. Value stocks should also start outperforming growth stocks. Stock market leadership changes often occur within the context of broad-based equity corrections. Our near-term view on stocks, as illustrated in the view matrix at the end of this report, is more cautious than our 12-month view. Thus, we would not be surprised if the major indices sell off over the coming weeks, with tech stocks leading the way down. The same sort of technical factors that amplified the move up in stocks over the past few weeks could exacerbate the move down. Most notably, so-called delta hedge option strategies, in which an investor sells calls and hedges the risk by purchasing the underlying stock, can create a self-reinforcing feedback loop where rising call prices force investors to buy more shares, leading to even higher call prices. Once the stock market starts falling, the process goes into reverse. Nevertheless, we do not expect tech stocks to suffer the sort of crash they experienced in 2000. Tech valuations are not as stretched as they were back then, earnings growth is stronger, and balance sheets are much healthier. Moreover, unlike in 2000, when the Fed lifted rates to as high as 6.5% in May, monetary policy is at no risk of turning hawkish. All this suggests that tech stocks are more likely to go sideways than down over a 12-month horizon (albeit in a fairly volatile manner). Investors should continue to overweight global equities relative to bonds on a 12-month horizon, while tilting equity allocations towards cheaper sectors and regions. Feature: Should Versus Will Investors want to know what the future will bring. As such, our primary interest at BCA Research is in predicting what policymakers will do rather than what they should do. Sometimes, however, it is useful to ask the “should” question since the answer may shape one’s view on the “will” question. This is especially the case when a particular set of goals is aligned with both the incentives and constraints that policymakers face. With that in mind, let us ask what the optimal mix of monetary and fiscal policy should be, assuming that policymakers have the goal of maximizing growth and moving the economy towards full employment. As we argue below, this is a relevant question to ask not because we necessarily share this goal – our personal value judgments are besides the point here – but because most policymakers think this is the correct goal. Propping Up Demand Chart 2Labor Markets In Developed Economies Have Rarely Overheated Over The Past Few Decades

Labor Markets In Developed Economies Have Rarely Overheated Over The Past Few Decades

Labor Markets In Developed Economies Have Rarely Overheated Over The Past Few Decades

Maintaining full employment requires that spending match the economy’s productive capacity. In theory, this should not be a difficult objective to achieve. After all, people like to spend. Increasing demand should be easy. The hard part should be raising supply. In practice, it has not worked out that way. Even before the pandemic, unemployment rates rarely fell below their full employment level across the G7 economies (Chart 2). High Unemployment: Cyclical Or Structural? Some will argue that surplus unemployment is necessary to shift workers from sectors of the economy where they are not needed to sectors where they are. The failure to facilitate such resource reallocation could, it is alleged, stymie long-term growth. This is largely a spurious claim. As Chart 3 shows, there is always a huge amount of churn in the labor market. In 2019, a year in which total employment rose by 2.1 million, a total of 70 million people were hired in the US compared to 64 million who quit or lost their jobs. In fact, labor market churn tends to decrease during recessions as workers become reluctant to quit their jobs. Chart 3Labor Market Turnover Tends To Increase During Expansions

Labor Market Turnover Tends To Increase During Expansions

Labor Market Turnover Tends To Increase During Expansions

Chart 4Residential Construction Accounted For Less Than 20% Of The Job Losses During The Great Recession

The Outlook For Monetary And Fiscal Policy: What Should Be Done Vs. What Will Be Done

The Outlook For Monetary And Fiscal Policy: What Should Be Done Vs. What Will Be Done

Far from reflecting structural factors, the vast majority of the rise in joblessness during economic downturns is gratuitous in nature. For example, more than 80% of the jobs lost during the Great Recession were outside the residential real estate sector (Chart 4). Moreover, employment growth is highly correlated with investment spending (Chart 5). The easiest way to induce firms to boost capex – and, in the process, augment the economy’s productive capacity – is to adopt policies that raise overall employment. A stronger labor market will generate more demand for goods and services. It will also make labor more expensive in relation to capital, thereby incentivizing labor-saving capital investment. Chart 5Employment Growth And Investment Spending Go Hand-In-Hand

Employment Growth And Investment Spending Go Hand-In-Hand

Employment Growth And Investment Spending Go Hand-In-Hand

Today, unemployment is elevated once again. As was the case during prior recessions, some workers will need to transition from sectors of the economy that will be slow to recover (retail, travel, and hospitality, for example) to sectors where jobs will be more plentiful. The risk is that there will not be enough job vacancies in the latter sectors to compensate for job losses in the former. The fact that permanent job losses have been creeping higher in the US over the past few months, even as temporary layoffs have come down, is evidence that such an outcome is a clear and present danger (Chart 6). Chart 6Many Are Returning To Work, But The Number Of Permanent Layoffs Is Slowly Increasing As Well

Many Are Returning To Work, But The Number Of Permanent Layoffs Is Slowly Increasing As Well

Many Are Returning To Work, But The Number Of Permanent Layoffs Is Slowly Increasing As Well

Central Banks Can’t Do It All One does not need to refill a leaky bucket through the same hole the water escaped. As long as there is enough demand throughout the economy, workers who lose their jobs in declining sectors will eventually find new jobs in other sectors. So why has the bucket seemed chronically short of water in recent years? The answer is that monetary policy has been tasked to do more than it is realistically capable of achieving. Monetary policy operates with “long and variable lags.” When unemployment rises, the best that central banks can do is cut interest rates and hope that the more interest-rate sensitive parts of the economy eventually perk up. If the interest-rate sensitive sectors of the economy are tapped out, just as housing was following the financial crisis, or policy rates are near their lower bound, as they are now, monetary policy will be even less potent than usual. The Role Of Fiscal Policy This is where fiscal policy ought to fill the void. Even if monetary policy is exhausted, governments can cut taxes, raise transfers to households and businesses, or increase direct spending on goods and services. The extent to which fiscal policy is loosened should not be preordained. Rather, it should simply reflect the state of the economy. There is no limit to how much money governments can transfer to the public. In fact, one can easily imagine a system where governments cut taxes and increase transfer payments whenever unemployment moves up. Such a powerful system of automatic stabilizers would go a long way towards keeping the economy on an even keel. Why have governments been reluctant to embrace such a system? One key reason is that such a system would produce open-ended budget deficits. That would not be much of a problem if the red ink lasted just a few years, but what if the need for large budget deficits did not go away? The Japanese Example Consider the case of Japan. Starting in the early 1990s, Japan’s private sector became a chronic net saver, as demand for credit evaporated amid savage deleveraging (Chart 7). In order to keep the economy from falling into a full-blown depression, the government started to run continual budget deficits. Effectively, the government had to soak up persistent private savings with its own dissavings. As a result, the debt-to-GDP ratio ballooned from 64% in 1991 to 237% by 2019 and is set to rise further this year. Many people predicted a debt crisis would engulf Japan. Takeshi Fujimaki, a former banker turned politician, has been forecasting a debt crisis for more than two decades.In 2010, financial pundit John Mauldin described Japan as a “bug in search of a windshield.” He reckoned that the country would “implode within the next two-to-three years,” with the yen falling to 300 against the dollar. Kyle Bass has made similarly dire predictions.1 How was Japan able to escape what seemed like certain doom? The answer is that the same factor that necessitated persistent budget deficits, namely excess private-sector savings, also allowed interest rates to fall. Despite a rising debt-to-GDP ratio, government interest payments have been trending lower over time (Chart 8). Today, the government actually earns more interest than it pays because two-thirds of all Japanese debt bears negative yields. Chart 7The Japanese Government Runs Persistent Budget Deficits Amid The Private Sector's Desire To Save

The Japanese Government Runs Persistent Budget Deficits Amid The Private Sector's Desire To Save

The Japanese Government Runs Persistent Budget Deficits Amid The Private Sector's Desire To Save

Chart 8Japan: Ballooning Debt And Declining Interest Payments

Japan: Ballooning Debt And Declining Interest Payments

Japan: Ballooning Debt And Declining Interest Payments

If anything, Japan erred in not easing fiscal policy by enough. Had Japan run even larger budget deficits, deflationary pressures would have been less acute, and as a result, real interest rates would have fallen even more than they actually did (Chart 9). Chart 9Japanese Real Yields Are Higher Than In Many Other Major Economies

Japanese Real Yields Are Higher Than In Many Other Major Economies

Japanese Real Yields Are Higher Than In Many Other Major Economies

A Fiscal Free Lunch? The standard equation for public debt sustainability says that as long as the government’s borrowing rate is below the growth rate of the economy, the debt-to-GDP ratio will converge to a stable level no matter how large the fiscal deficit happens to be (See Box 1 for details). The caveat is that this “stable” debt-to-GDP ratio could turn out to be quite high. For example, if the government wants to run a primary budget deficit of 10% of GDP indefinitely, and GDP growth exceeds the real interest rate by two percentage points, the debt-to-GDP ratio will eventually converge to 500%. If interest rates were guaranteed to stay at zero forever, even a debt-to-GDP ratio of 500% would be no cause for alarm. But, of course, there is no such guarantee. For a country such as Italy, letting debt levels soar into the stratosphere would be highly risky. Countries that do not possess a central bank capable of acting as a lender of last resort could find themselves in a vicious spiral where rising bond yields raise the probability of default, leading to even higher bond yields (Chart 10). Chart 10Multiple Equilibria In The Debt Market Are Possible Without A Lender Of Last Resort

The Outlook For Monetary And Fiscal Policy: What Should Be Done Vs. What Will Be Done

The Outlook For Monetary And Fiscal Policy: What Should Be Done Vs. What Will Be Done

For countries that do issue debt in their own currencies, default risk is less of a problem since their central banks can set short-term rates at any level they want and, if necessary, target long-term rates with yield curve control strategies. Nevertheless, even these countries would face difficult choices if the excess savings that permitted interest rates to stay low disappeared. A decline in national savings would raise the neutral rate of interest (the rate which equalizes aggregate demand with aggregate supply). If policy rates remained unchanged, the neutral rate of interest would end up being higher than policy rates, which would eventually cause the economy to overheat. At that point, policymakers would have two options: First, they could simply let the economy overheat such that inflation rises. If inflation is very low to begin with, modestly higher inflation would be welcome, as it would make the zero lower bound constraint less of a problem.2 Higher inflation would also speed up the pace of nominal income growth, leading to a lower debt-to-GDP ratio. That said, if inflation were to rise too much, it could have destabilizing effects on the economy. Second, they could tighten fiscal policy. A smaller budget deficit would add to national savings, while giving the government more resources to pay back debt. Tighter fiscal policy would also subtract from aggregate demand, thus reducing the neutral rate of interest. This would diminish the need for central banks to raise rates in the first place. Putting it all together, the optimal course of action, at least for countries that can issue debt in their own currencies, is to loosen fiscal policy until full employment has been restored and the central bank’s inflation target has been met. Once this has been achieved, the government should trim the budget deficit to keep inflation from getting out of hand. What Will Be Done Okay, so much for the idealized strategy. What will actually happen? As was the case following the Great Recession, there is a risk that some countries will tighten fiscal policy prematurely, causing the economic recovery from the pandemic to be slower than it would otherwise be. In the US, this is already happening. Federal emergency unemployment benefits under the CARES Act expired at the end of July; funding for the small business paycheck protection program has run out; and state and local governments are facing a severe cash crunch. BCA Research’s Geopolitical Strategy team, led by Matt Gertken, expects the logjam in Washington to be resolved in September. Most voters, including the majority of Republicans, want emergency unemployment benefits to be restored (Table 1). Additional fiscal stimulus would cushion the economy in the lead up to the November election, which would arguably benefit President Trump and the Republican party. Hence, there is a good chance that Congressional Republicans will accede to a fairly generous fiscal package. Table 1The Majority Continues To Support Expanded Unemployment Insurance

The Outlook For Monetary And Fiscal Policy: What Should Be Done Vs. What Will Be Done

The Outlook For Monetary And Fiscal Policy: What Should Be Done Vs. What Will Be Done

Globally, the prevalence of negative real rates (and in some cases, negative nominal rates) should incentivize governments to run larger budget deficits than they have in the past. Increasing political populism will amplify this trend. Thus, despite some near-term hiccups, fiscal policy will remain highly stimulative. The Inflation End Game Chart 11The Ratio Of Workers-To-Consumers Is Now Falling

The Ratio Of Workers-To-Consumers Is Now Falling

The Ratio Of Workers-To-Consumers Is Now Falling

What will happen when unemployment rates return to their pre-pandemic level in three or four years? Will governments tighten fiscal policy to prevent overheating or will they let inflation run loose? Our guess is that they will let inflation rise. National savings can shrink either because the private sector is spending more or because the private sector is earning less. Looking out beyond the next few years, the latter is more likely than the former. This is because the ratio of workers-to-consumers globally will decline sharply over the coming decade as more baby boomers exit the labor force (Chart 11). Spending will decelerate, but output and income will decelerate even more by virtue of this demographic reality. It is difficult to boost tax revenue in an environment of slowing real income growth. If output falls in relation to spending, inflation will rise. At least initially, central banks will welcome the burst of inflation. They have been trying to push up inflation for years. Past inflation undershoots will be used to justify future inflation overshoots, a doctrine the Fed officially blessed at the virtual Jackson Hole symposium last week. Other central banks will be loath to raise rates if the Fed stands pat for fear that their own currencies will surge against the US dollar. The end result is that inflation will increase, first in the US and then everywhere else. A quick glance at long-term inflation expectations suggests that markets do not discount this risk at all (Chart 12). What does all this mean for investors? For the next few years, the combination of ample fiscal stimulus and easy monetary policy will foster a supportive backdrop for global equities. Despite the rally in stocks since March, the global equity risk premium remains quite elevated, especially outside the US (Chart 13). Investors should remain overweight global stocks versus bonds on a 12-month horizon. Chart 12Investors Believe Inflation Will Stay Muted In The Long Term

Investors Believe Inflation Will Stay Muted In The Long Term

Investors Believe Inflation Will Stay Muted In The Long Term

Chart 13Non-US Stocks Look Cheaper Than Their US Peers In Both Absolute Terms And In Relation To Bond Yields

Non-US Stocks Look Cheaper Than Their US Peers In Both Absolute Terms And In Relation To Bond Yields

Non-US Stocks Look Cheaper Than Their US Peers In Both Absolute Terms And In Relation To Bond Yields

Looking further out, the secular bull market in equities will end only when central banks are forced to scramble to contain inflation. Fortunately, that day of reckoning is at least a few years away. Peter Berezin Chief Global Strategist peterb@bcaresearch.com Footnotes 1 Ben McLannahan, “Japanese Bonds Defy the Debt Doomsters,” Financial Times, dated August 8, 2012; Mariko Ishikawa, Kenneth Kohn and Yumi Ikeda, “Soros Adviser Turned Lawmaker Sees Crisis by 2020,” Bloomberg News, dated September 27, 2013; and Dan McCrum, “Kyle Bass bets on full-blown Japan crisis,” Financial Times, May 21, 2013. 2 For example, if inflation is 3%, a central bank could produce a real rate of -3% by bringing policy rates down to zero. In contrast, if inflation is only 1%, the lowest that real rates could fall is -1%, which may not be stimulative enough for the economy. Box 1The Arithmetic Of Debt Sustainability

The Outlook For Monetary And Fiscal Policy: What Should Be Done Vs. What Will Be Done

The Outlook For Monetary And Fiscal Policy: What Should Be Done Vs. What Will Be Done

Global Investment Strategy View Matrix

The Outlook For Monetary And Fiscal Policy: What Should Be Done Vs. What Will Be Done

The Outlook For Monetary And Fiscal Policy: What Should Be Done Vs. What Will Be Done

Current MacroQuant Model Scores

The Outlook For Monetary And Fiscal Policy: What Should Be Done Vs. What Will Be Done

The Outlook For Monetary And Fiscal Policy: What Should Be Done Vs. What Will Be Done

The recent market selloff continues to bear the mark of a correction. A pullback had become nearly unavoidable. Growth stocks had moved vertically and reached furious valuations. Yet, bond yields were not declining anymore. The correction could run further as…

BCA Research’s Emerging Markets Strategy service concludes that increased central bank intervention may diminish the importance of fundamentals in determining asset prices. Excluding debt securities owned by the Fed and commercial banks, cash on the sidelines…

Highlights Oil-price volatility will remain subdued as markets correctly downgrade measurable risks on the supply side and upgrade financial conditions supporting demand (Chart of the Week). OPEC 2.0’s spare capacity – ~ 7mm b/d – presents the producer coalition with an opportunity to gain control of the evolution of global supply, and to restrain price volatility as global storage levels fall. Scaling production and delivery of a COVID-19 vaccine will be challenging, given limited global production and distribution capacity.1 This will slow down – but not derail – a recovery in demand. Lingering policy uncertainty will restrain a speedy return to pre-COVID-19 demand levels. Looming large are US election uncertainty and mounting geopolitical tensions. Our forecast attaches a significantly higher probability to Brent crude oil prices trading above $65/bbl next year, vs. the 15% probability the market is discounting in options for December 2021 delivery. Feature As OPEC 2.0 gains control of the evolution of the supply side, global fiscal and monetary policy accommodation will keep global financial conditions supportive of demand. Oil-price volatility will remain subdued, as market participants correctly price in continued OPEC 2.0 production discipline and cohesion within the coalition led by the Kingdom of Saudi Arabia (KSA) and Russia. In addition, the coalition’s substantial spare capacity – ~ 7mm b/d, most of which is in KSA – will, as we have argued elsewhere, present OPEC 2.0 with an opportunity to influence production moreso than in pre-COVID-19 markets: It will be able to respond to higher prices quicker than US shale oil producers, as was demonstrated in 2018 when KSA took its production from less than 10mm b/d to 11.1mm b/d between June and November (Chart 2). This means OPEC 2.0 can move quickly to capture economic rents, which will slow the recovery of the shales – already limited by parsimonious capital markets – and increase OPEC 2.0’s global market share (Chart 3).2 Chart of the WeekVol Falls As Known Unknowns Are Resolved

Vol Falls As Known Unknowns Are Resolved

Vol Falls As Known Unknowns Are Resolved

Chart 2OPEC 2.0 Quick Response Spare Capacity Advantage

OPEC 2.0 Quick Response Spare Capacity Advantage

OPEC 2.0 Quick Response Spare Capacity Advantage

Chart 3Ensures Production Restraint

Ensures Production Restraint

Ensures Production Restraint

As OPEC 2.0 gains control of the evolution of the supply side, global fiscal and monetary policy accommodation will keep global financial conditions supportive of demand (Chart 4). We expect the US Federal Reserve’s monetary policy, which will now focus on reviving the labor market and on achieving a 2% average PCE index core inflation rate, to weaken the USD, which also will be supportive of oil demand.3 Demand also will be supported by expectations – and the realization – of a COVID-19 vaccine, which is expected later this year or early next year. Limited production and logistical constraints will make it difficult to scale delivery of a vaccine globally until infrastructure is built out. This will restrain – but not derail – the recovery in demand we expect (Chart 5). Lingering policy uncertainty – particularly around the upcoming US elections and mounting geopolitical tensions – remain obstacles for the recovery. Chart 4Global Financial Conditions Will Support Demand

Global Financial Conditions Will Support Demand

Global Financial Conditions Will Support Demand

Chart 5Demand Expected To Recover Smartly

Demand Expected To Recover Smartly

Demand Expected To Recover Smartly

Well-managed supply, coupled with steadily improving demand already apparent in the data, will allow storage to draw over the next year without raising oil-price volatility, which typically occurs when spare capacity is low (Chart 6).4 Chart 6Falling Storage Will Not Spike Vol This Time

Lower Vol As OPEC 2.0 Gains Control

Lower Vol As OPEC 2.0 Gains Control

Oil Vol Will Stay Lower Volatility bursts typically are presaged by increases in implied volatility as hedgers and speculators react to new information coming into the market. As the Chart of the Week indicates, a surge in volatility caused by either a supply or demand shock typically is followed by a more tranquil period after markets adjust to the shock. These volatility bursts typically are presaged by increases in implied volatility as hedgers and speculators react to new information coming into the market.5 Following the resolution of the elevated risk conditions prompting the increased option trading, historical volatility, which is calculated using the annualized returns of the underlying assets, typically increases then tails off, as can be seen in the experience of 2019-20 – i.e., pre- and intra-COVID-19 markets (Chart 7). Chart 7Implied Vol Typically Leads Realized Vol

Lower Vol As OPEC 2.0 Gains Control

Lower Vol As OPEC 2.0 Gains Control

Ahead of meetings of OPEC and its Ministerial Monitoring Subcommittee, internet searches move upward along with implied volatilities. Increases in oil-price volatility also are accompanied by heightened interest in news specific to oil markets or OPEC. Market participants usually expect OPEC countries will adjust output as needed following swift changes in underlying global demand – e.g., the COVID-19 demand shock – and non-OPEC supply. Ahead of meetings of OPEC and its Ministerial Monitoring Subcommittee, internet searches move upward along with implied volatilities in expectation of supply adjustments from OPEC (Chart 8). The relationship actually has strengthened since 2014, following OPEC’s market-share war and the ensuing OPEC 2.0 agreement to drain the accumulated global oil inventories. Since its formation, OPEC 2.0 has played a crucial role in balancing oil markets. This makes every meeting highly relevant for markets. Moreover, when oil prices move abruptly, internet searches for “OPEC” or “OPEC MEETING” generally move higher as investors seek guidance from the producer coalition to assess where prices will go next. High levels of speculation can affect oil price volatility. Hence, the higher the interest in oil prices from retail and institutional investors, the larger the increase in implied volatility ahead of these meetings.6 Chart 8Implied Vol Follows Google Search Activity

Implied Vol Follows Google Search Activity

Implied Vol Follows Google Search Activity

Implied Volatility And Efficient Markets Implied volatility, like prices discovered in competitive trading markets, impounds all information available to market participants buying and selling options. As it is an estimate of the standard deviations of returns for the underlying asset against which options are traded, it can be used to estimate the probability market participants assign to the realization of a particular price outcome (Chart 9). As an be seen in Chart 9, the market is pricing more in line with the US EIA’s expectation Brent prices will average $50/bbl next year, as opposed to our estimate of $65/bbl. Based on the settlement values for prices and volatilities on Monday, the December 2021 Brent futures contract has a 15% probability of expiring above $65/bbl (Chart 10). Chart 9Markets Pricing To EIA Assumptions

Lower Vol As OPEC 2.0 Gains Control

Lower Vol As OPEC 2.0 Gains Control

Chart 10BCA Price Forecasts

Lower Vol As OPEC 2.0 Gains Control

Lower Vol As OPEC 2.0 Gains Control