Financial Markets

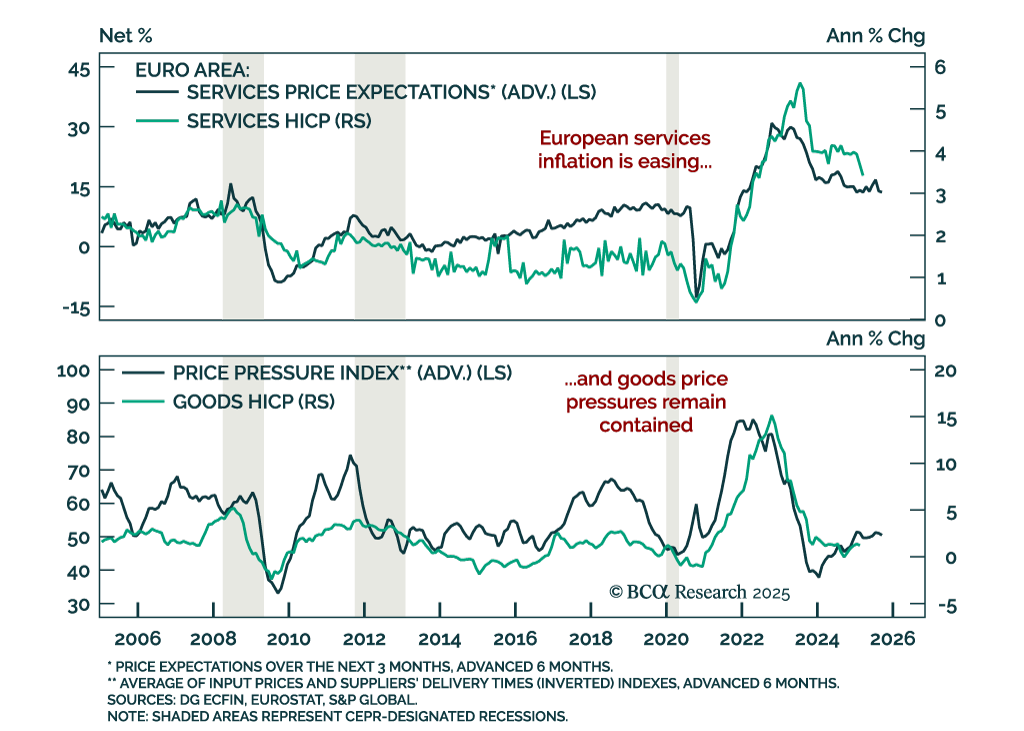

Eurozone inflation is cooling steadily, supporting our tactical overweight in German bunds versus European equities and increasing the odds of an April ECB cut. Headline HICP eased to 2.2% y/y in March from 2.3%, while core came in cooler than expected at…

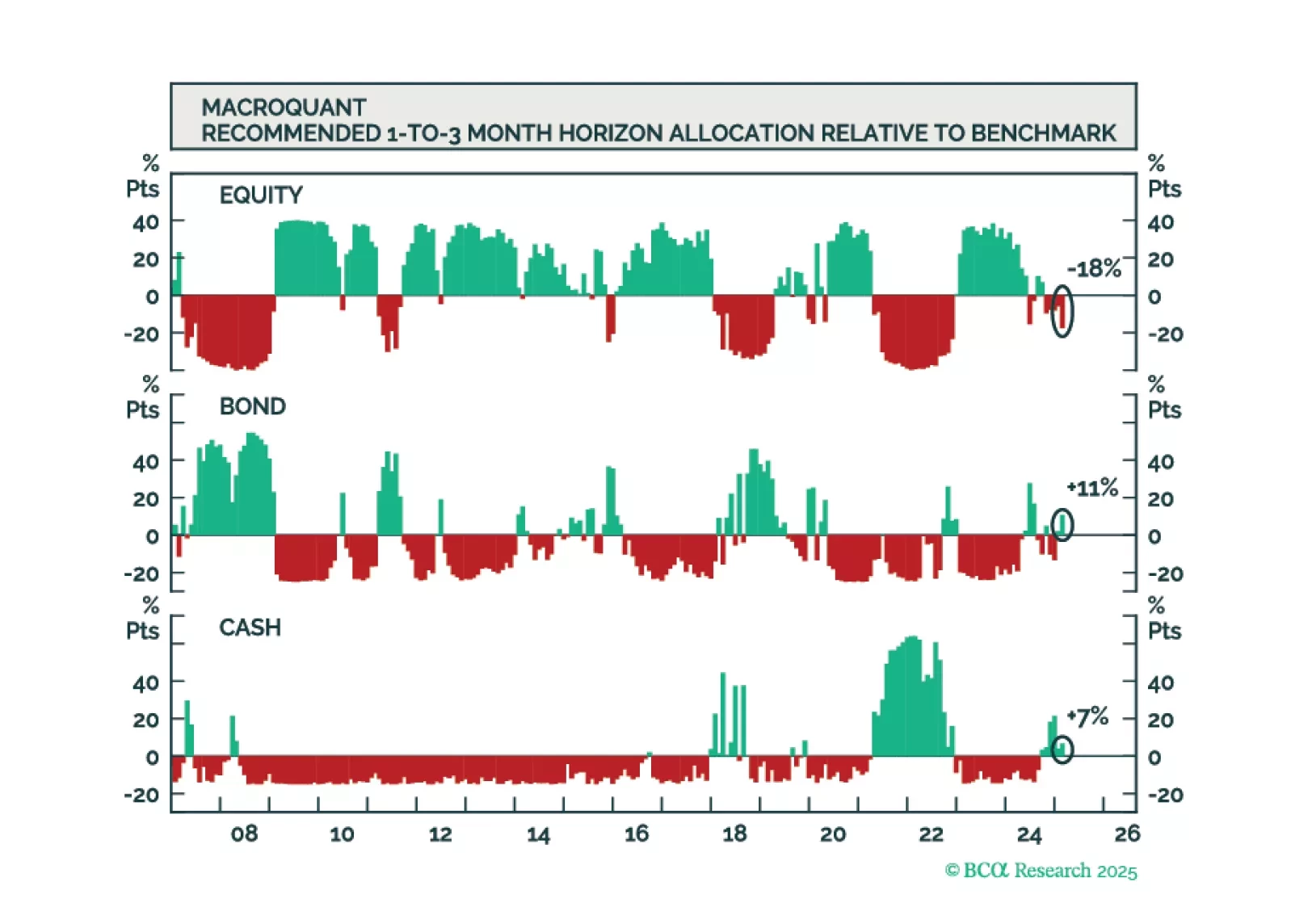

Going into April, MacroQuant recommends a modest underweight on stocks, offset by an overweight on bonds and cash. While MacroQuant is modestly bearish on stocks, we suspect that the downside risks to equities may be greater than what the model assumes.

Going into April, MacroQuant recommends a modest underweight on stocks, offset by an overweight on bonds and cash. While MacroQuant is modestly bearish on stocks, we suspect that the downside risks to equities may be greater than what the model assumes.

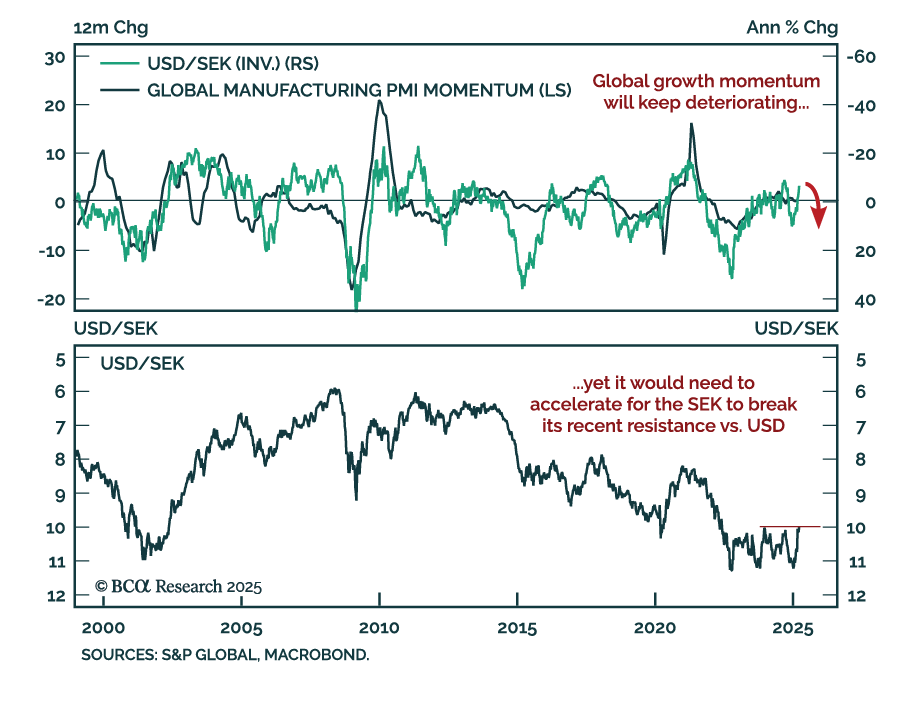

The SEK’s sharp rally is losing steam as local data weakens and EUR strength looks stretched. After appreciating more than 10% against the USD year-to-date, the krona is now showing signs of fatigue. Recent Swedish data has disappointed, with the Economic…

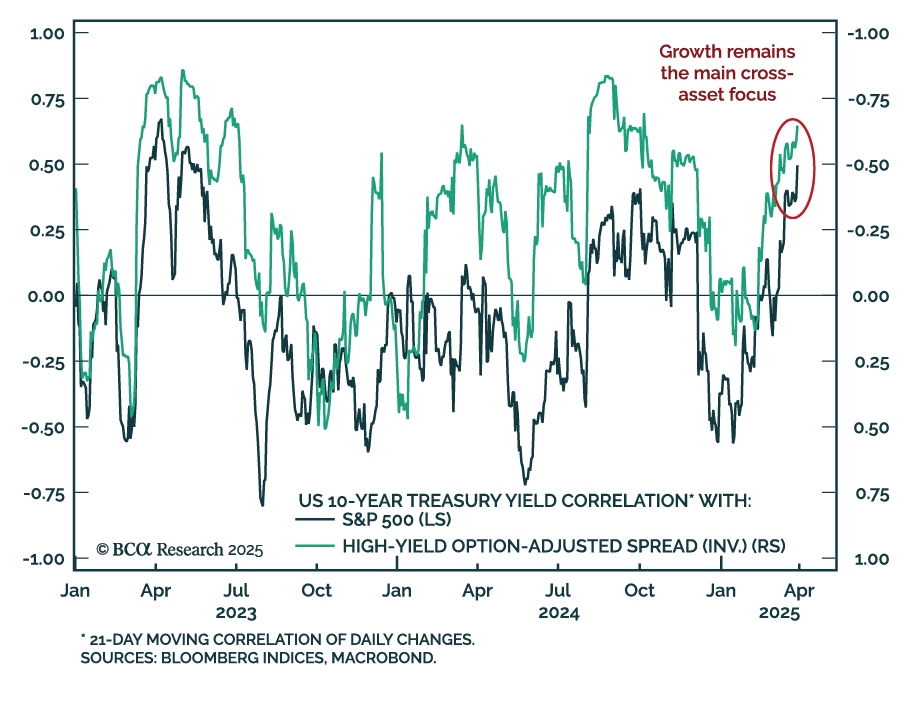

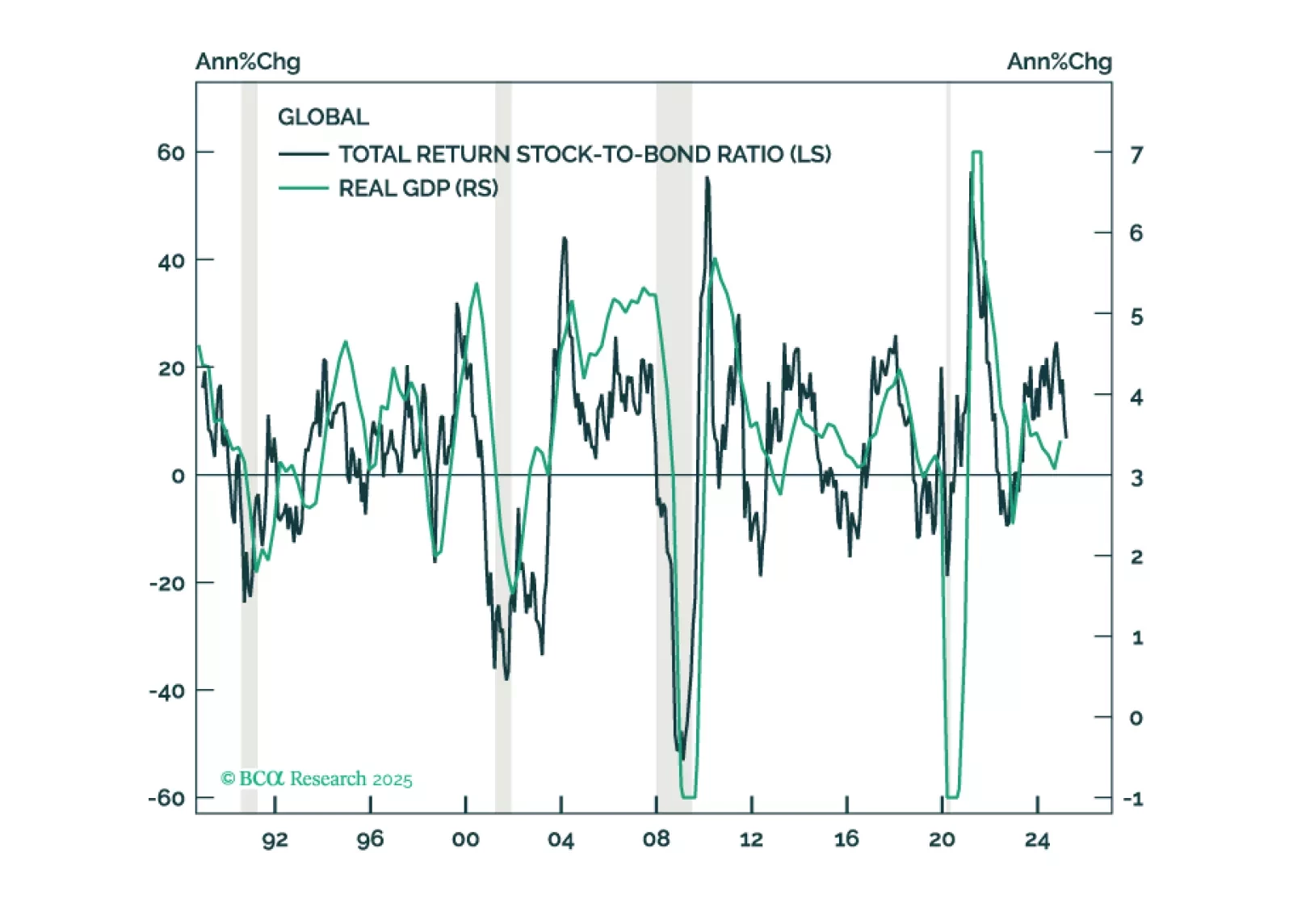

Markets are responding to the growth drag of stagflation, not the inflation impulse, reinforcing our defensive stance. Despite rising short-term inflation pressures in the US, risk assets and bond yields continue to move together, with the stock–bond yield…

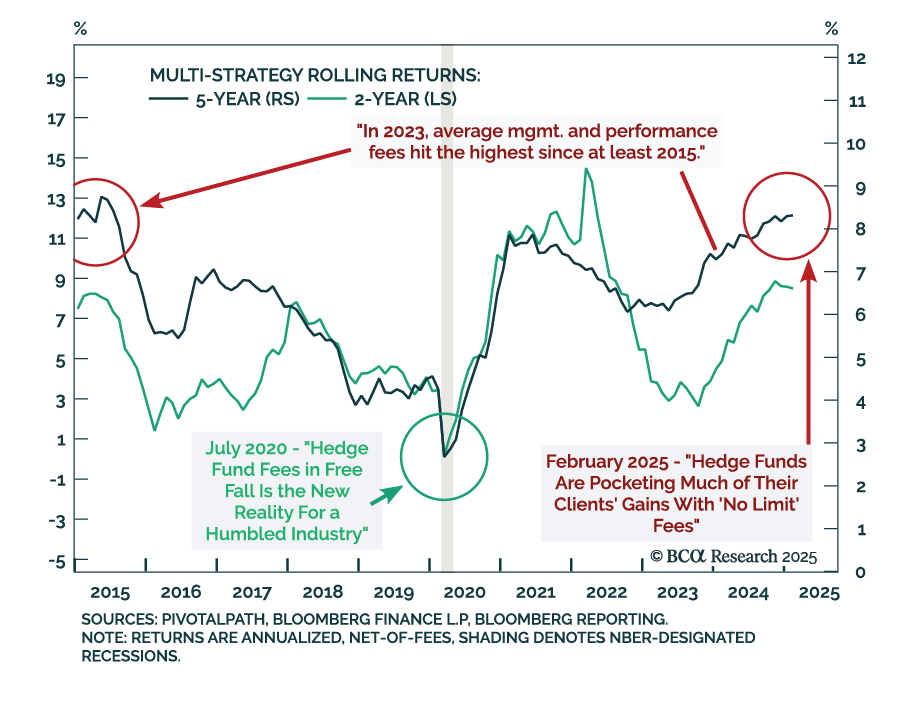

Our Private Markets & Alternatives strategists remain structurally positive but cyclically underweight on Multi-Strategy Hedge Funds. While these funds have delivered consistent alpha and valuable diversification, current market conditions offer more…

Our Commodities Strategy team advises against positioning for a near-term rebound in lithium prices, given the current headwinds from soft EV sales growth. They recommend patience, with more compelling opportunities likely to emerge later in the decade as…

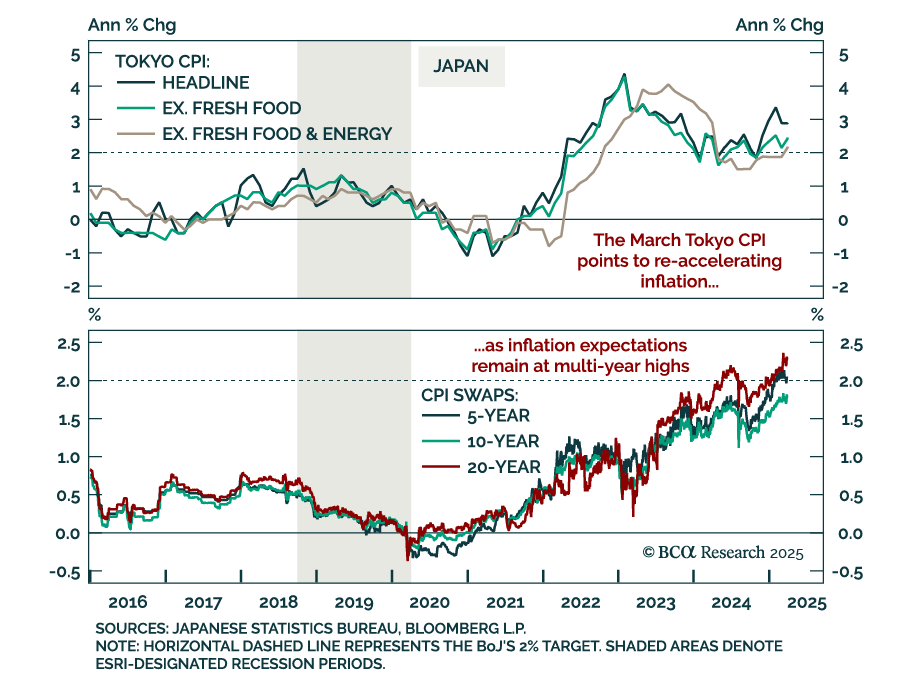

Japan’s inflation pulse remains firm, reinforcing our long JPY stance and cautious view on JGBs. Tokyo CPI for March surprised to the upside, with headline inflation slightly up at 2.9% y/y and “core core” accelerating above the BoJ’s target to 2.2% from…

In this Second Quarter Strategy Outlook, we explore the major trends that are set to drive financial markets for the rest of 2025 and beyond.

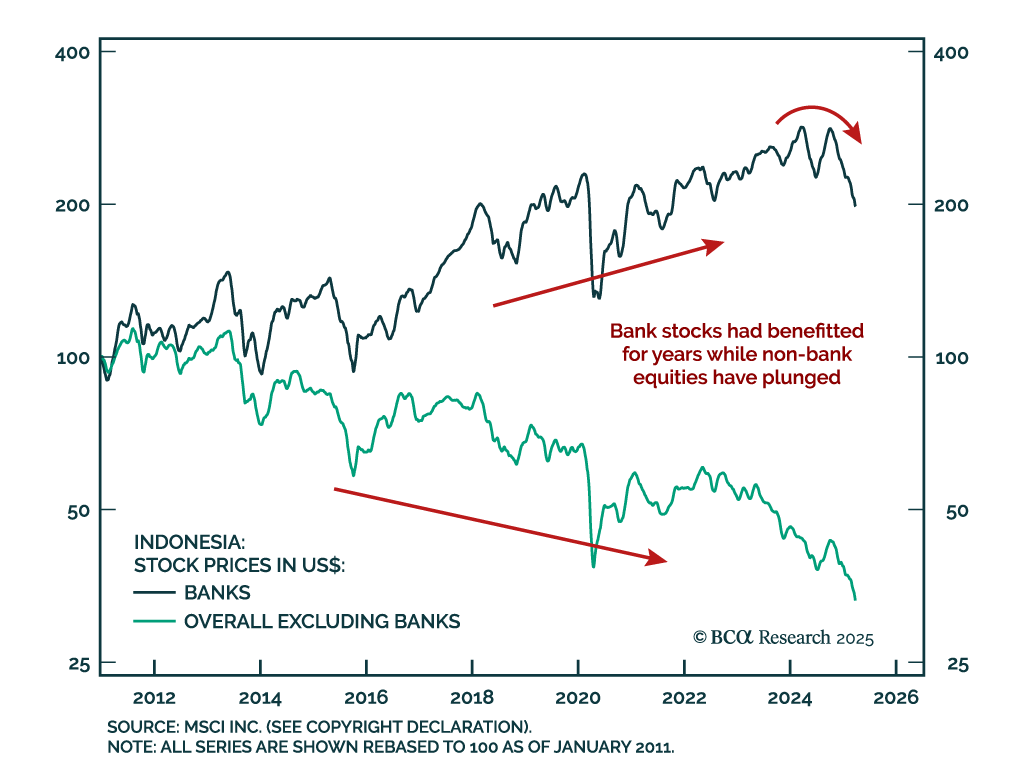

Our Emerging Markets strategists maintain a neutral view on Indonesia within EM equity and bond portfolios but continues to recommend shorting the rupiah versus the US dollar. They are closing their long Indonesian banks/short EM banks position due to…