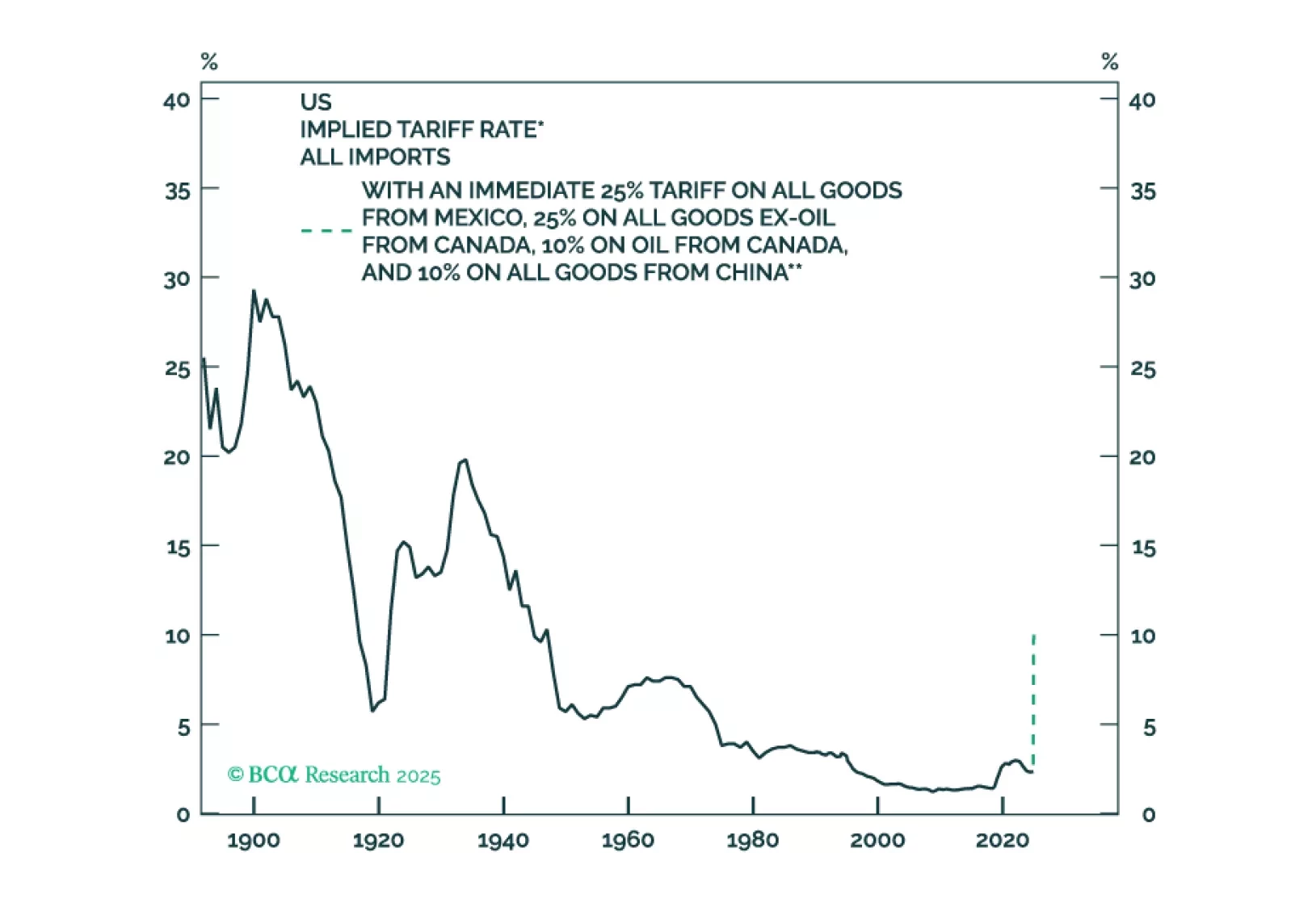

Trump’s Tariff ObsessionDonald Trump was elected on his promise to reduce inflation, curb illegal immigration, and expunge woke ideology. Tariffs were never very high on the agenda for most voters. Nevertheless, Trump has been obsessed with tariffs for years, largely because he thinks of international trade as a win/lose proposition rather than a mutually beneficial arrangement. This weekend’s tariff announcement was the culmination of this obsession.In this Strategy Insight, we answer some of the key questions that clients have been asking us.Q: Trump just announced that he is delaying the tariffs on Mexico by one month after the Mexican president promised to send 10,000 more troops to the border. Can we rest easy now?A: Probably not. Trump has promised to shift the tax burden away from domestic income to foreign sources, with tariffs presumably being the most important element in that. His entire obsession with President William McKinley is centered on this pledge. Given that the budget deficit is over 6% of GDP, he will need to rely on tariffs to some extent.There is also the matter of politics. The majority of US voters think that the US loses more from trade than it gains. Among Republicans, the gap is 3-to-1 (Chart 1). Until that sentiment shifts, Trump will have little incentive to change course. Q: Won’t the stock market discipline Trump?A: Potentially, yes, and the decline in stocks this morning probably played a role in Trump’s decision to pause tariffs on Mexico. While the US is a fairly closed economy, the S&P 500 is not. According to FactSet, 41% of S&P 500 revenues are sourced from abroad. For the IT sector, that number rises to 57% (Chart 2).The problem is that we are in a catch-22 situation: Trump will not abandon his fondness for tariffs unless the stock market falls significantly, but the stock market will not fall significantly if investors continue to think that a major trade war will be avoided. Q: What can Canada do to avoid a tariff shock?A: It is not clear what Canada can realistically do. Outside of oil, Canada runs a trade deficit with the US (Chart 3). Last year, the US seized over 21,000 pounds of fentanyl at the Mexican border compared to only 43 pounds at the Canadian border. As late as 2023, more people crossed illegally from the US into Canada than the other way around. Trump complained earlier today that US banks are unable to do business in Canada. Although that is not strictly true, the Canadian government could offer to facilitate the entry of US banks into the Canadian market. That might be enough for Canada to earn a temporary reprieve.Q: Assuming that the tariffs announced over the weekend are ultimately implemented, how would they compare to what transpired during Trump’s first term?A: The recently announced tariffs are much larger. The effective US tariff rate rose from 1.4% in 2017 to 2.8% by the end of Trump’s first term. It then declined to the current level of 2.3%, partly because the Biden administration removed some tariffs on US allies and because China rerouted some of its exports through third countries such as Mexico and Vietnam.If ultimately implemented, a 25% tariff against Canada and Mexico, along with an additional 10% tariff on Chinese imports, would raise the effective US tariff rate to nearly 10%, which would be the highest since 1946 (Chart 4). The effective tariff rate would rise further if Trump were to extend the tariffs to the EU and other regions, which he has pledged to do. Q: How much economic damage could a trade war cause the US and the rest of the world? A: Most studies have found that the announced tariffs against Canada, Mexico, and China would reduce US real GDP by a fairly modest 0.5% while lifting consumer prices by 0.7%. However, we think these studies significantly understate the potential growth damage from a trade war because they focus mainly on the impact on aggregate demand from higher import prices when, in reality, the bigger shock is likely to come from the supply side. More than half of North American trade is in intermediate goods, with the auto industry in particular being highly integrated across the region. A trade war would pull the rug from under a supply chain that has been created over many decades, leading to significant blowback to the rest of the economy.As bad as the impact on the US would be, the fallout for Canada and Mexico would be substantially worse. Exports to the US account for 18% of Canada’s GDP and 29% of Mexico’s. It is likely that both economies will experience a recession if the tariffs are put in place. As for China, BCA’s China strategist, Jing Sima, estimates that all things equal, a 10% additional tariff would lower Chinese export growth from 6% in 2024 to less than 3% in 2025. This would shave about 0.6 percentage points off real GDP growth.Even for those countries that have not yet been subject to Trump’s tariffs, there will be adverse consequences. As the IMF has shown, uncertainty over trade policy can be as much of a problem as the tariffs themselves (Chart 5). Unsure as to what will happen next, companies will just sit on their hands, leading to less investment and hiring.Q: Won’t central banks mitigate the economic damage by cutting interest rates?A: To some extent yes, but the potential stagflationary effect of tariffs could blunt the response. Inflation is still somewhat above target in the US. Although the imposition of tariffs would represent a one-off increase in the price level, there is a risk that inflation expectations could still move higher. In general, prices that are constantly in the public’s eye drive inflation expectations more than other prices. This is why gas prices tend to be more correlated with economy-wide inflation expectations than one would naively assume based on how much households spend on gasoline. Polls show that Americans expect tariffs to raise prices (Chart 6). As such, the Fed may wish to wait to see what happens to inflation expectations before adjusting monetary policy. The policy response to a trade war will be more forceful outside the US. Nevertheless, there is a limit to what policy can do. While inflation in Mexico is coming down, it is still above 4%. Inflation is less of an issue in Canada and China, but both economies face formidable structural changes, especially around their housing markets.Q: The specific issues around Canada and Mexico aside, doesn’t Trump have a point? The US has been running structurally large trade deficits for over 40 years.A: As a matter of arithmetic, if a country is running a current account deficit, it must also run a capital account surplus (Chart 7). For many years, the US has been perceived as a good place to invest. Thus, rather than purchasing US goods, foreigners have bought US stocks, bonds, and real estate. The only way for the US to return to running trade surpluses is if foreigners dump US assets. This would drive down the value of the dollar, making exports competitive again. Q: In conclusion, what should investors do now?A: At current valuations, US equities are not adequately pricing in the risk of an extended trade war. Foreign equities are cheaper than their US counterparts, but they are more cyclically-sensitive and have struggled to generate meaningful earnings growth. Hence, a modest underweight to global equities is warranted. We expect to turn even more defensive if the global economy shows further signs of losing momentum.Treasury yields will likely decline over the coming weeks, although the prospect of ever-larger budget deficits will continue to be a headwind for bonds. The US dollar should strengthen further despite being very expensive on a Purchasing Power Parity (PPP) basis (Chart 8).Looking further out, the outlook for US assets – stocks, bonds, and the dollar – is troubling. I am writing this report in Canada. It is difficult to convey how much anger there is at the moment towards the US in general, and Trump specifically. Almost everyone I know is planning to boycott US goods where possible. Trump likes to talk about “law and order” but his decision to violate the USMCA – a deal that his own administration negotiated – runs contrary to the rule-based global trading system that the US helped create after the Second World War. Other countries are no doubt asking themselves what bogus reason Trump will come up with to raise tariffs on them in the future. The net effect of Trump’s actions will be to reduce US geopolitical influence in the world and push more countries into China’s arms. It will also undermine the US dollar’s hegemony while increasing risk premia associated with owning US assets.Peter BerezinChief Global Strategistpeterb@bcaresearch.comPlease follow me onLinkedIn & X