Financial Markets

There is no better way to gauge the macro policies of the new US administration than being privy to President Donald Trump’s discussions with the new Treasury Secretary, Scott Bessent. While we do not have inside information, we have put the pieces of the puzzle together to help clients see the big picture. This report presents our take on a hypothetical conversation between President Trump and Scott Bessent that led to the latter’s appointment as Treasury secretary.

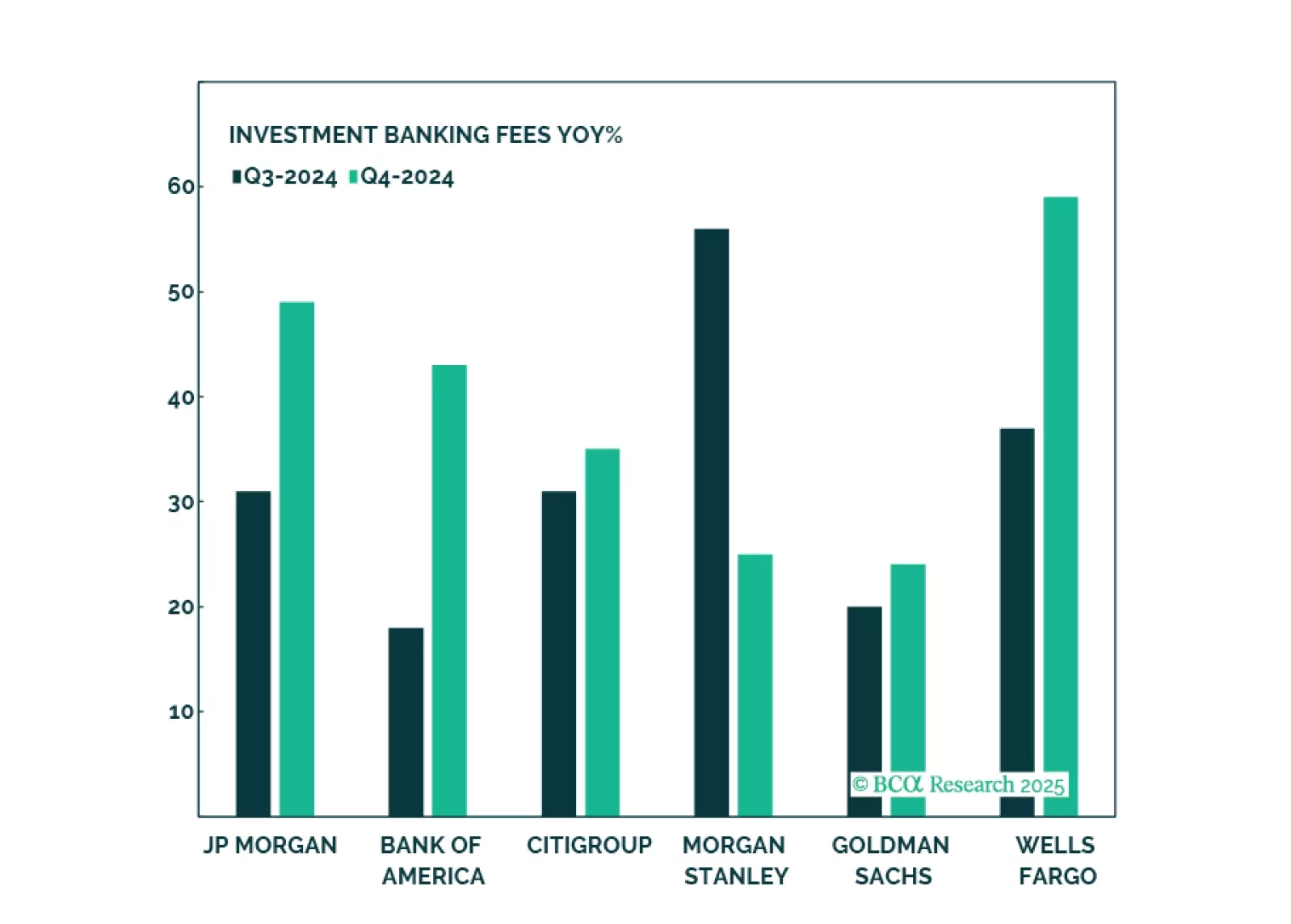

Banks have had an amazing run, and while such strong performance is unlikely to repeat, there is still oomph left in the trade thanks to a more favorable regulatory environment, stronger demand for loans, a steeper yield curve, and a strong pipeline of capital market activity. Key risks are further tightening of monetary policy and an increase in bad loans. We reiterate our overweight on Capital Markets, Diversified Banks, and Regional Banks.

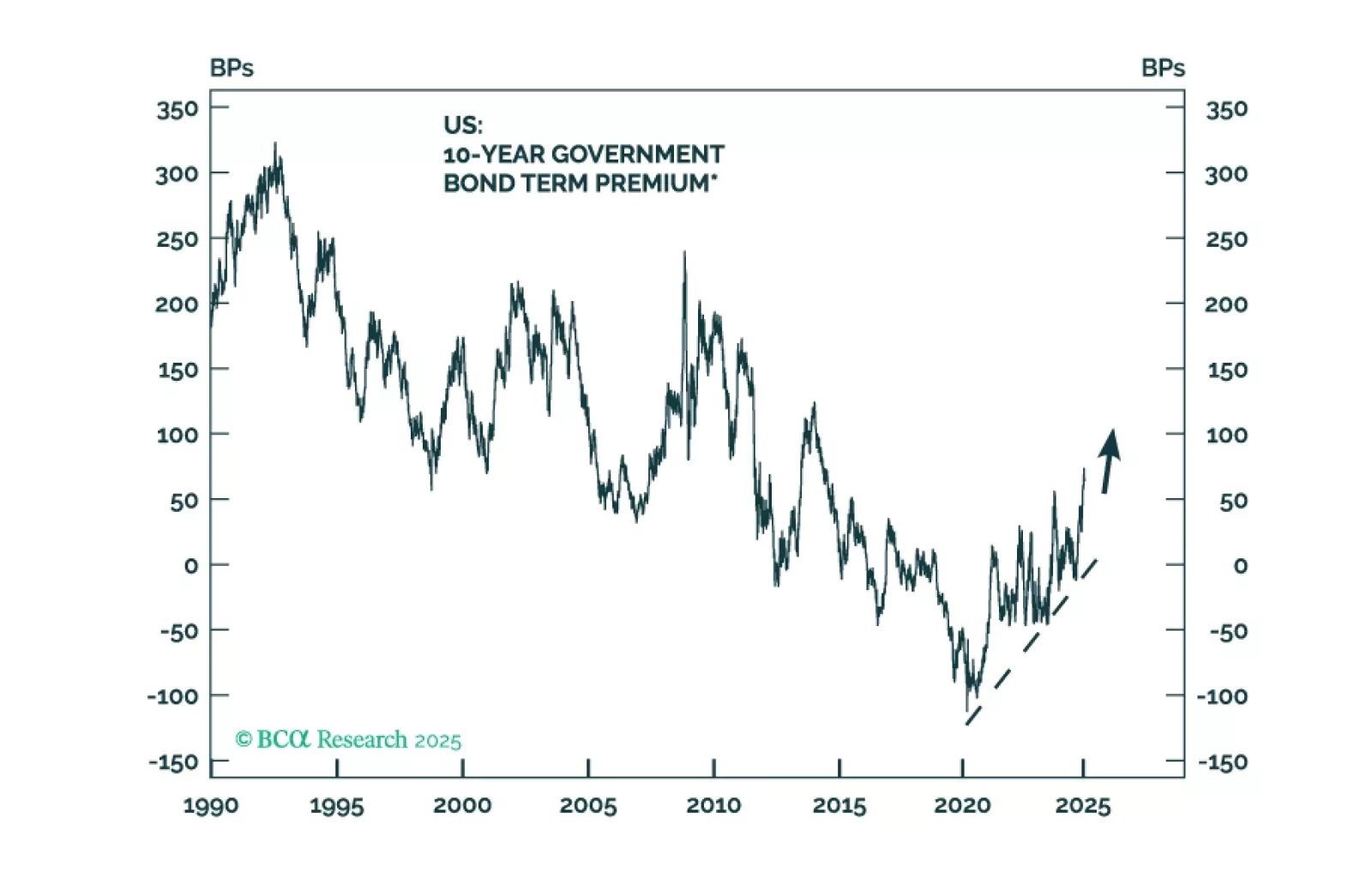

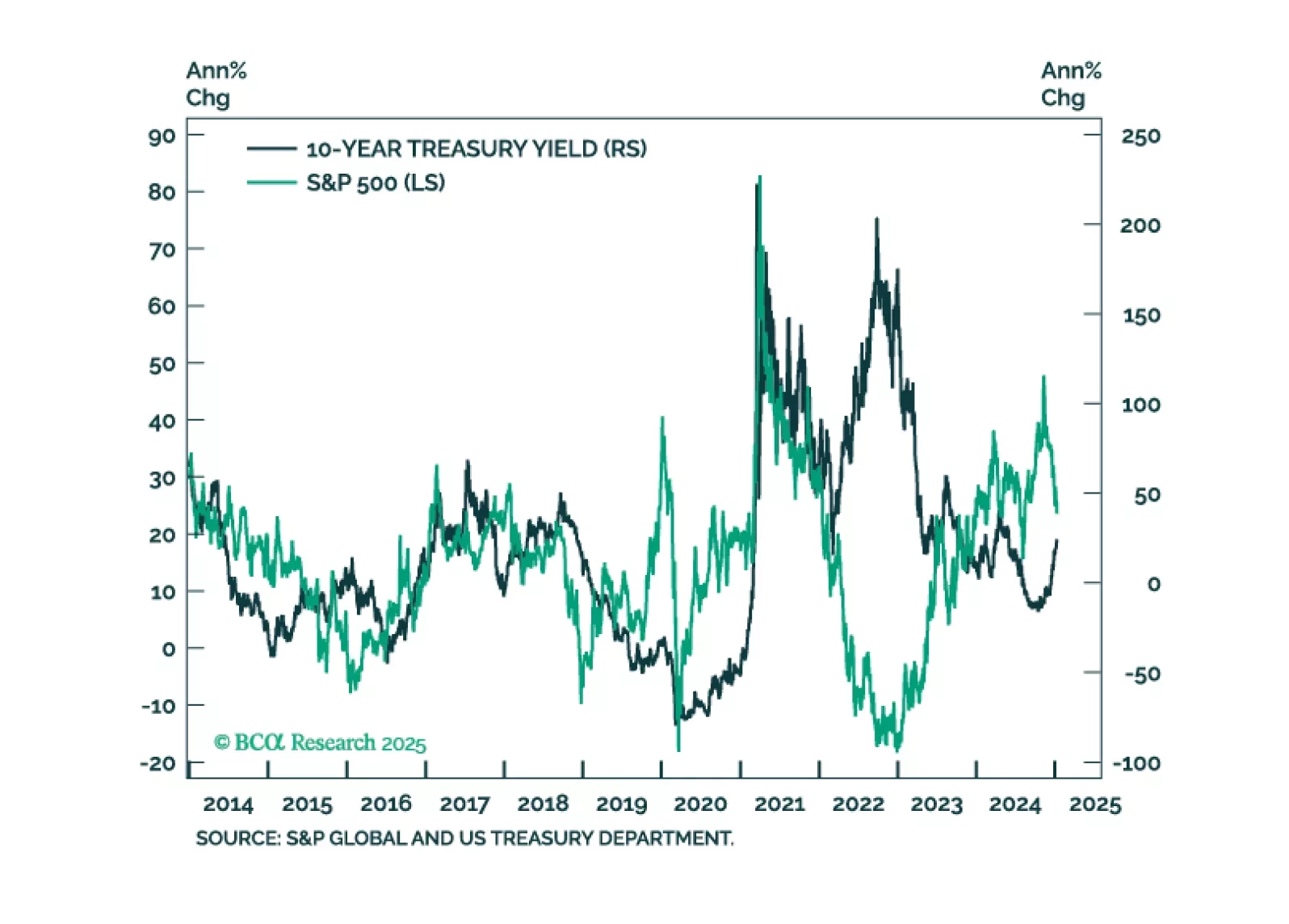

We examine Treasury market valuation and look for indicators that could help us time the next peak in yields. We also update the forecasts from our Treasury yield model.

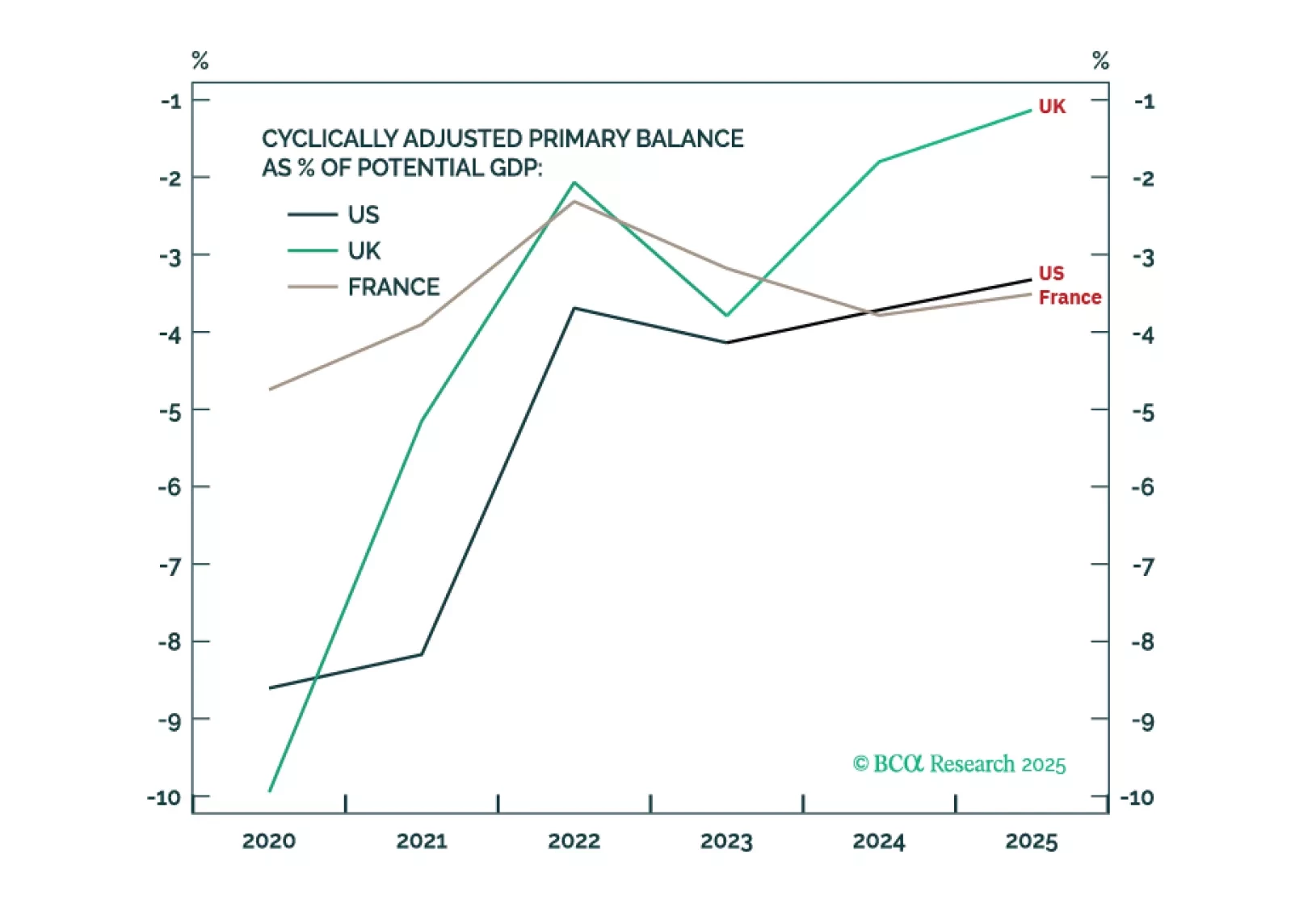

Political instability combined with the maths of debt sustainability is much more concerning in France than in either the UK or the US. Go long UK gilts versus French OATs and go tactically long GBP/USD.

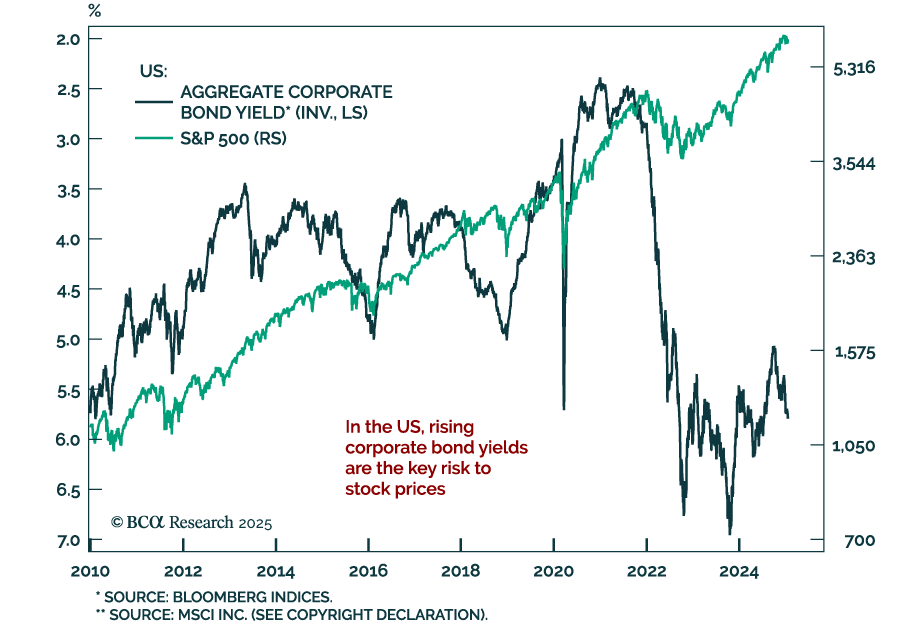

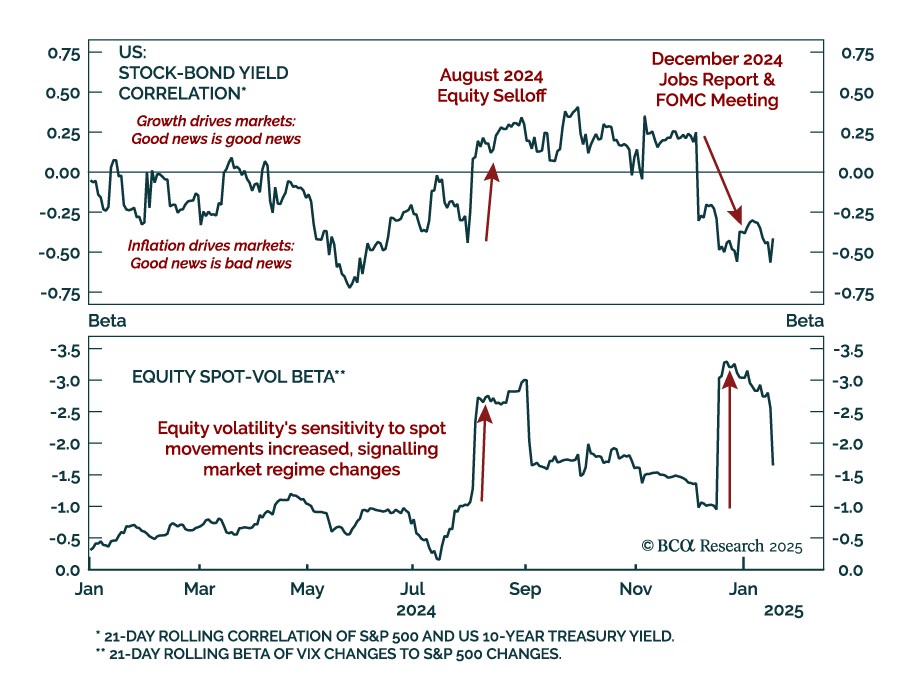

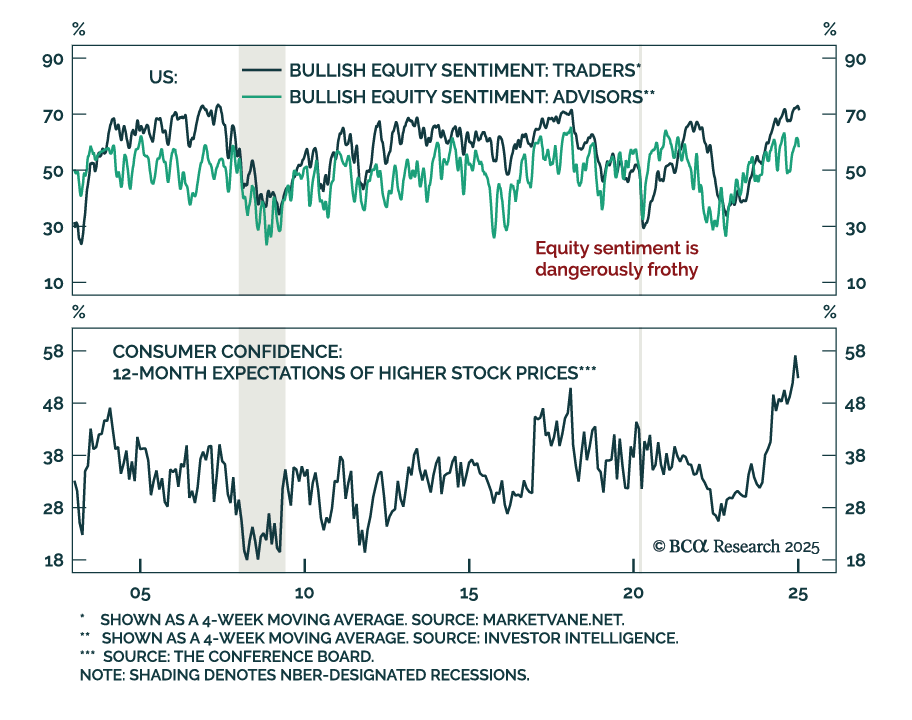

In this first presentation of 2025, we start with an overview of the 2025 outlook webcast polls, and a brief post-mortem of the 2024 market performance. Then, we shift gears and examine what is behind the recent surge in bond yields and its implications for equities. We also review market technicals and positioning and conclude with a list of trades to prepare our portfolio for continued moves in yields.

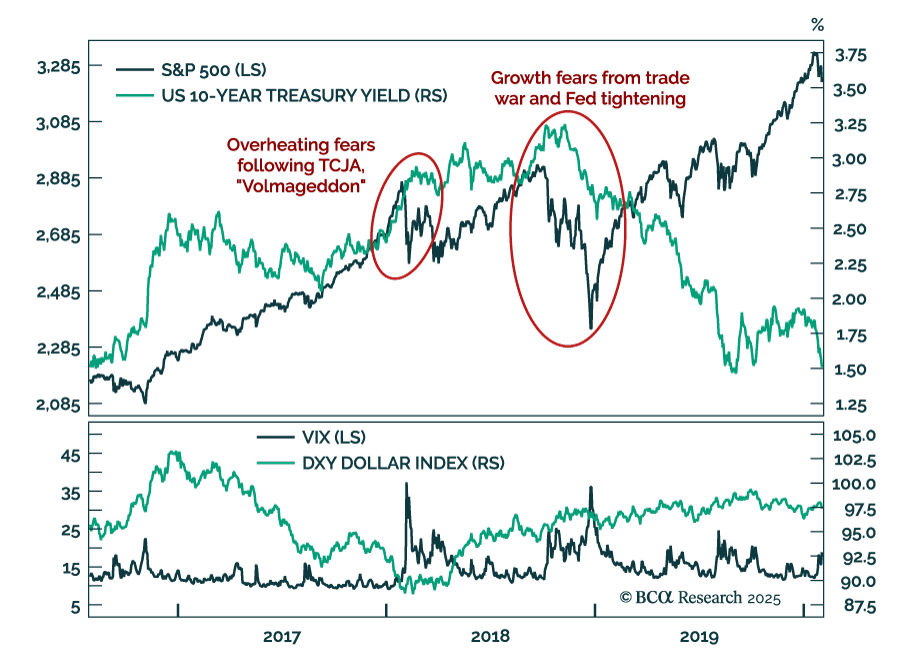

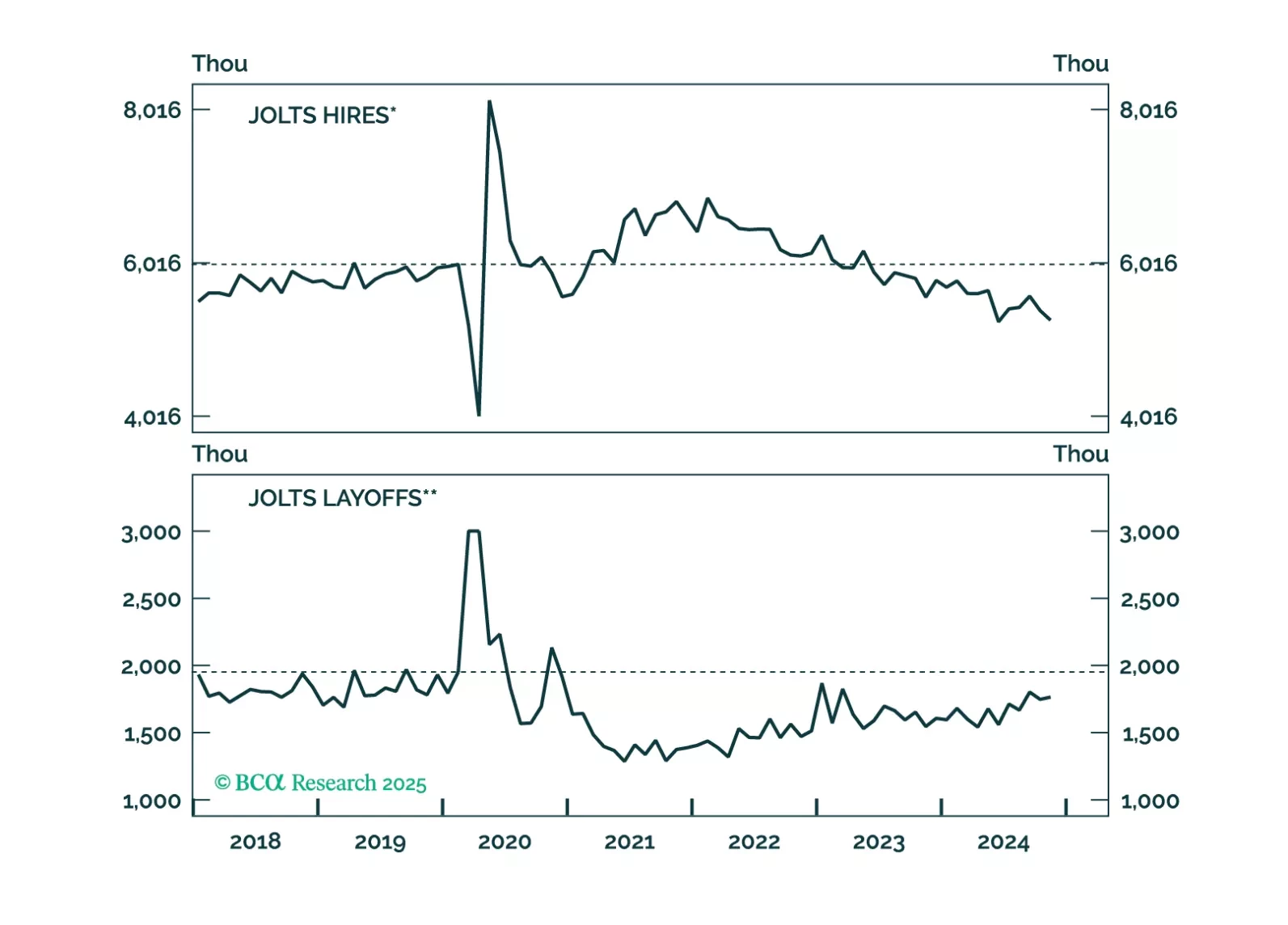

Thoughts on the increase in bond yields and this morning’s employment data.