Financial Markets

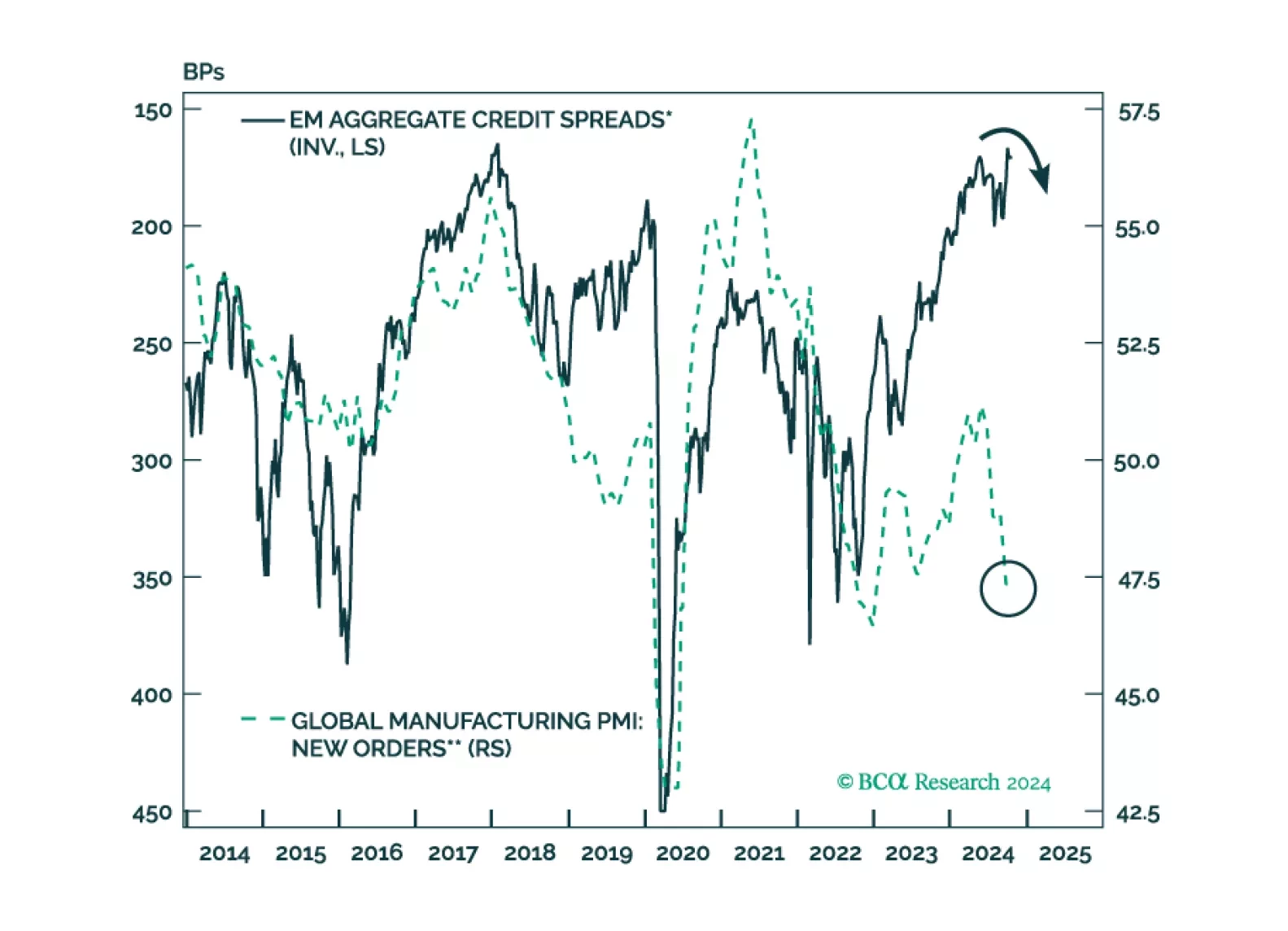

EM credit markets have recently defied the selloffs in EM equities, currencies, local currency bonds, and commodity prices. Such a decoupling is unusual. Resilient US growth and Fed easing are not sufficient to justify very low EM credit spreads.

Germany’s economy has lagged that of the rest of Europe for nearly 10 years. So have German stocks. Investors are extrapolating these trends to bet on the country’s deindustrialization. Could Germany manage to beat dismal expectations?

Middle-aged households have lagged youngish and older households since the pandemic and the 40-to-54 cohort is worse off than it was at the end of 2019. The fragmenting of the seemingly monolithic US consumer widens the path to a recession and we reiterate our defensive asset allocation recommendations.