Financial Markets

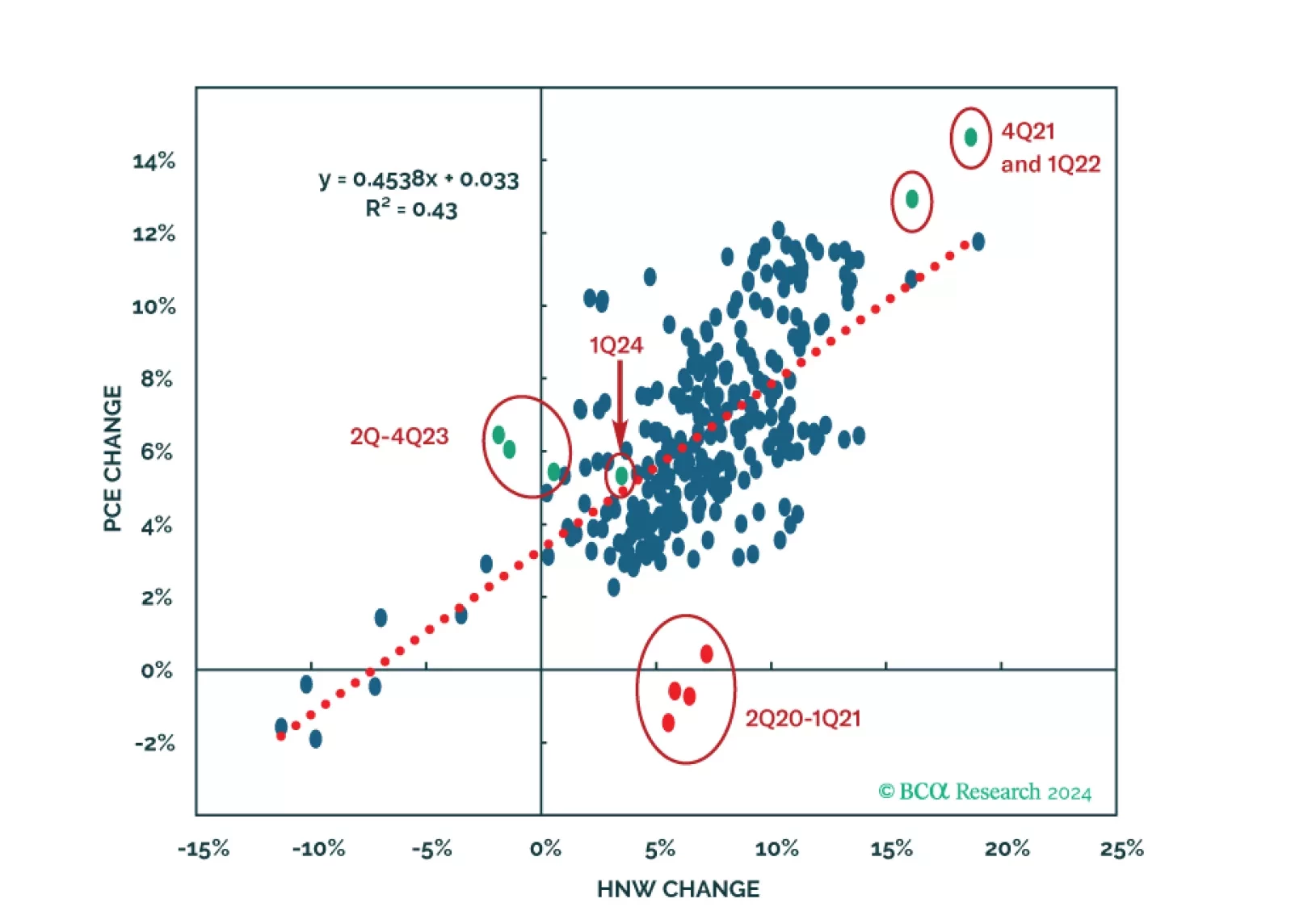

Stress among lower-income households is often cited as an early indication of deteriorating aggregate consumer fundamentals. The data indeed suggests that this cohort’s cash holdings are depleting. However, the Fed’s quarterly estimates of household wealth…

Despite the recent correction, US equity leadership remains intact. The MSCI US index has outperformed global markets by 3.8% in 2024YTD. A 7.8% expansion in forward earnings drove the MSCI US index’ 2024YTD gains which was higher than the increases in…

This Special Report examines the post-pandemic evolution of consumption growth, relative equity sector and subindustry performance and recent commentary from consumer-facing companies to assess the likelihood that softer spending among lower-income households will spread to middle- and upper-income households.

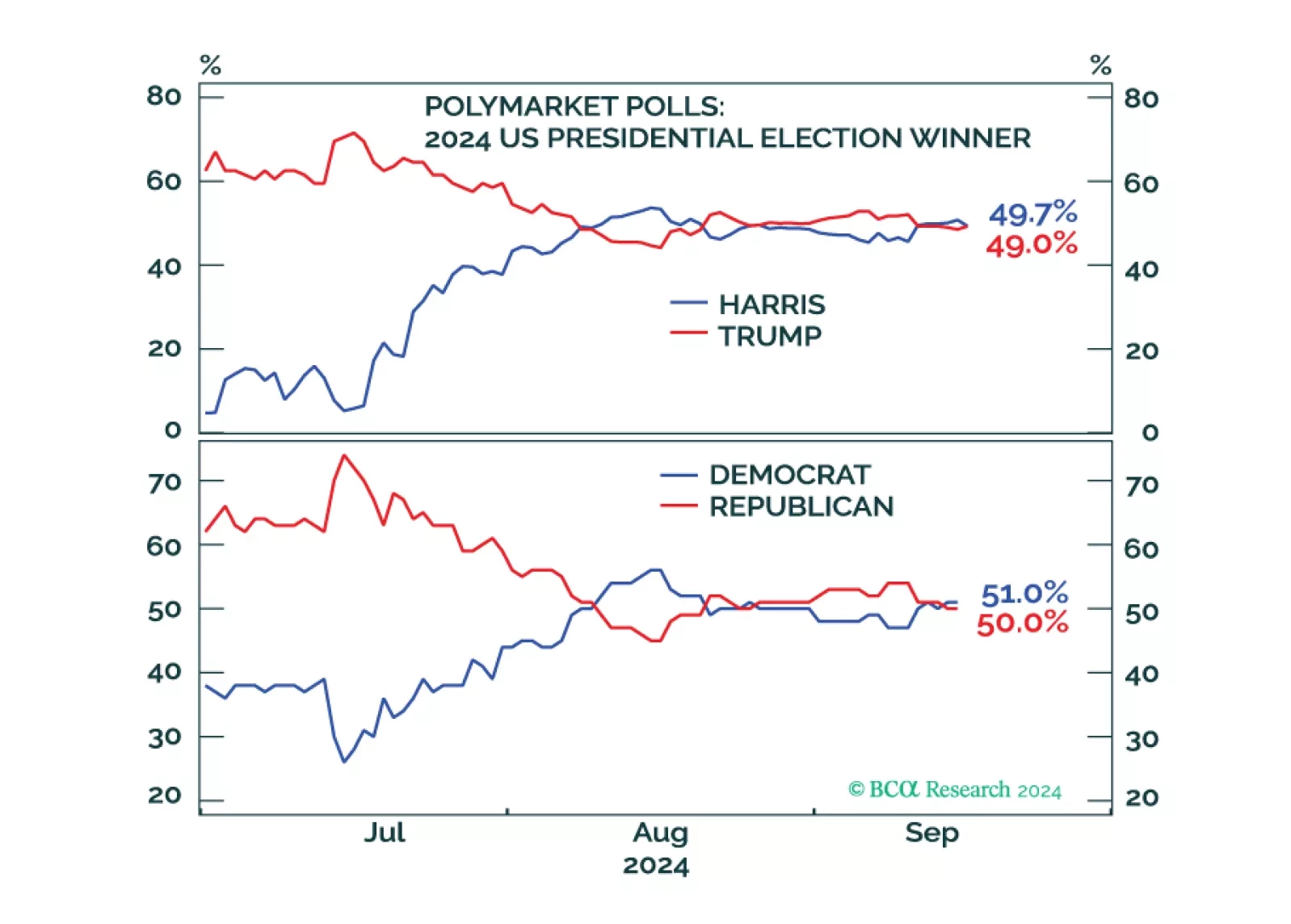

Investors should de-risk tactically in expectation of shocks and surprises ahead of the US election and an uncertain aftermath. Democratic victory with a gridlocked Congress is our base case but would bring minor tax hikes and nuclear brinksmanship with Russia. A Republican single-party sweep offers huge tax cuts but also a global trade war. Recession looms regardless.

The Chinese economic data in its totality was uninspiring in August. Industrial production and retail sales growth decelerated year-on-year and corroborate the message from August’s import and credit growth data that domestic demand remains lackluster.…

Trade data from small open economies act as a bellwether for global growth developments. In August, Korean exports expanded by 11.4% y/y in USD and 5.7% y/y in KRW terms, marking their eleventh and eighth consecutive month of expansion, respectively.…

Investors are pricing in a soft landing in the US. Notably, we noted that pro-cyclical assets topped the performance ranking in August. At the same time, the S&P 500 is currently trading only 1% below its all-time highs. However, investors are…

According to BCA Research’s Global Asset Allocation Strategy service, a common objection to buying Bitcoin raised by traditional investors is that it is too volatile. In the past it has been argued that this is irrelevant, however, this also turns out to be…

We noted earlier this month that the Fed would be unlikely to deliver a jumbo rate cut without telegraphing it first. President Williams' and Governor Waller’s September 6 speeches offered policymakers one last chance to do so before the customary pre-FOMC…

Volkswagen’s CEO has been making the point that the market for European carmakers has been deteriorating. Earlier last week, he went on to make a rather pointed reference at Chinese EV manufacturers. He was quoted saying that, "The pie has become…