Financial Markets

The equal-weighted S&P 500 index reached a new all-time high of 7,096.12 on Monday. Chair Powell’s comments at the Jackson Hole Symposium last week dispelled any remaining doubt about a September rate cut and sent smaller stocks higher. The Russell…

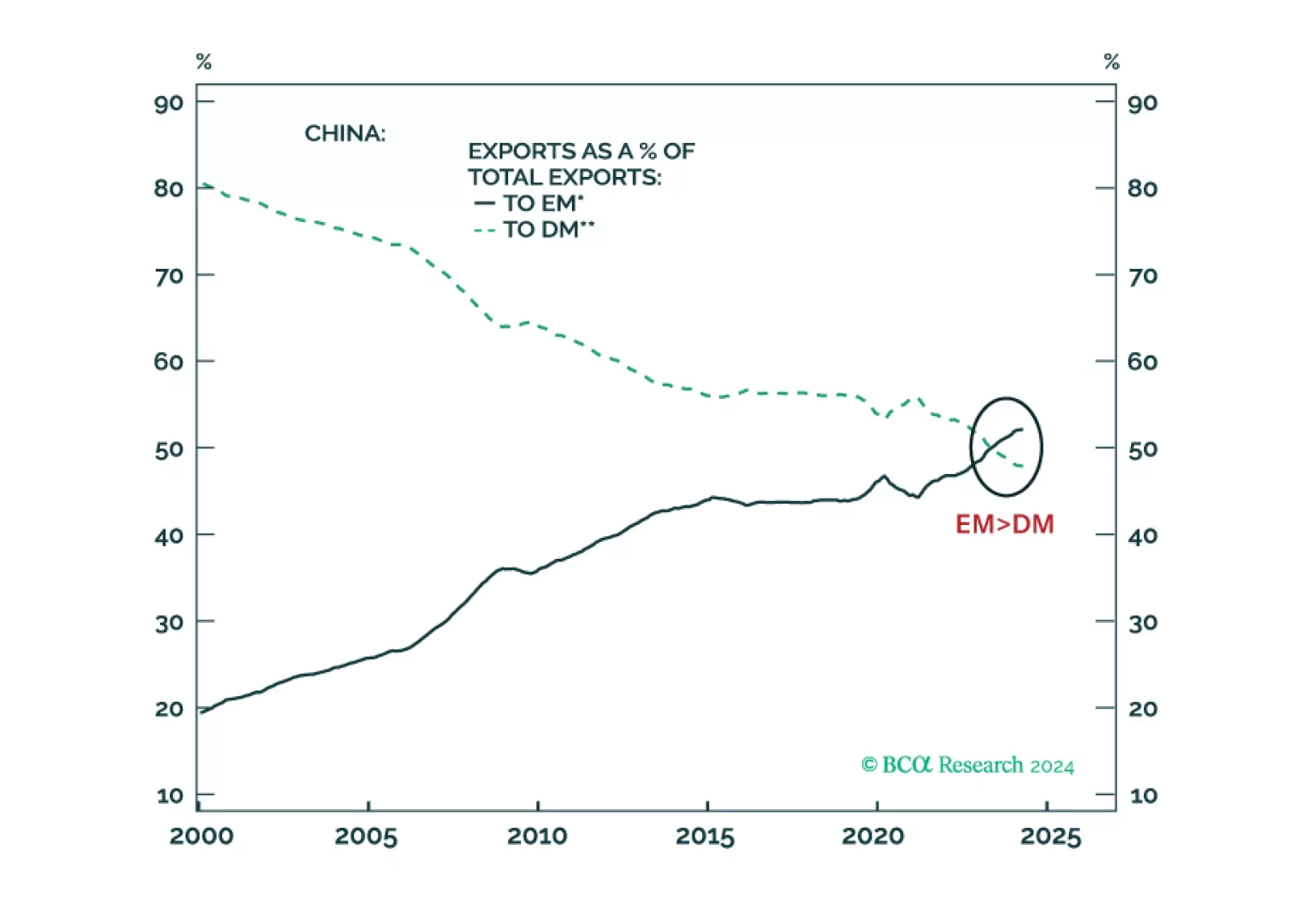

China has become less reliant on exports to advanced economies, and its products have successfully penetrated developing economies. Exports to the US make up 3% of Chinese GDP, while exports to all developing economies account for 10% of its GDP. China’s trade pivot from advanced to developing economies has economic, political, and geopolitical ramifications.

We’ve highlighted that continued deterioration in consumer fundamentals will tip the US economy into a recession. Slower compensation growth, tighter lending standards for consumer loans and dwindling excess savings will constrain spending in an economy where…

According to Goldman Sachs’ Financial Conditions Index (FCI) financial conditions have become considerably more supportive since the fall of 2023. More recently, the index ticked noticeably lower from 99.4 earlier in August to 98.8. US equities have indeed…

According to BCA Research’s Foreign Exchange Strategy service, the domestic economy does not really explain the recent weakness in the Norwegian krone. Some of this weakness can be attributed to structural and idiosyncratic factors, one being persistent…

Back in May, our Commodity and Energy strategists argued that OPEC, EIA, and IEA oil demand forecasts were likely too optimistic. Indeed, while all three major oil price forecasters projected a moderation in demand this year, none of them anticipated weak…

It didn't take long for markets to utterly shrug off the surprise rise in July's unemployment rate. On Tuesday, the S&P 500 closed higher than it was the day before the July Employment Situation report was released. The Russell 2000 gained 5.2% since…

EM equities have dramatically underperformed their US and Eurozone peers in USD terms over the past 15 years. The inability of EM and EM Asia companies to grow their EPS largely explains EM equities “lost decade” (and a half). Since 2010, US EPS have grown…

Markets have recouped some of the losses incurred in the aftermath of the July US Employment Situation report. Was the surprise rise in the unemployment rate a false alarm? Supply-side dynamics alone cannot explain the overall rise in the unemployment…

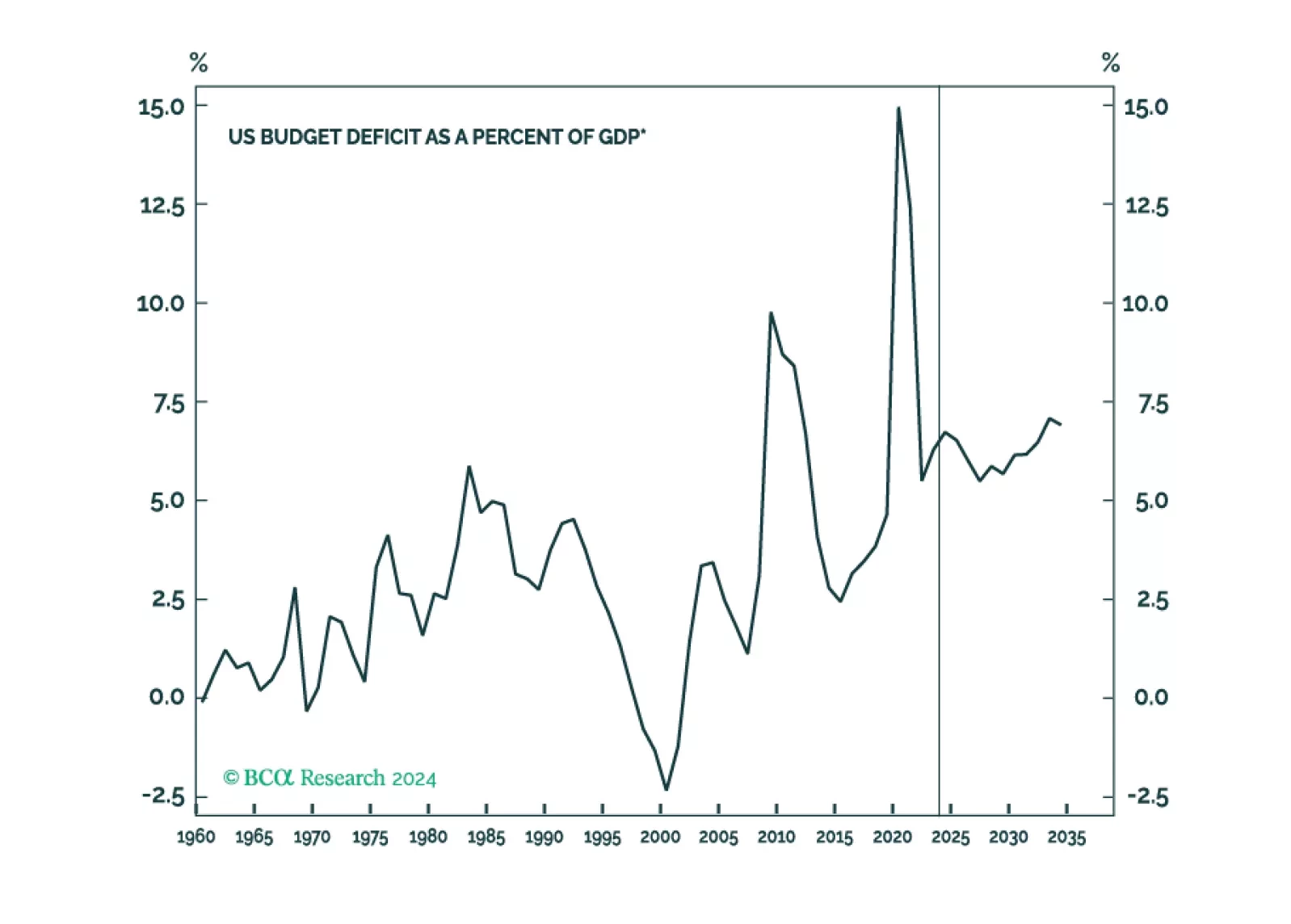

The US fiscal outlook is more unappetizing than it was before the pandemic, but we are not convinced that a difficult day of reckoning awaits. A Treasury market crisis is conceivable, but it is far from inevitable.