Financial Markets

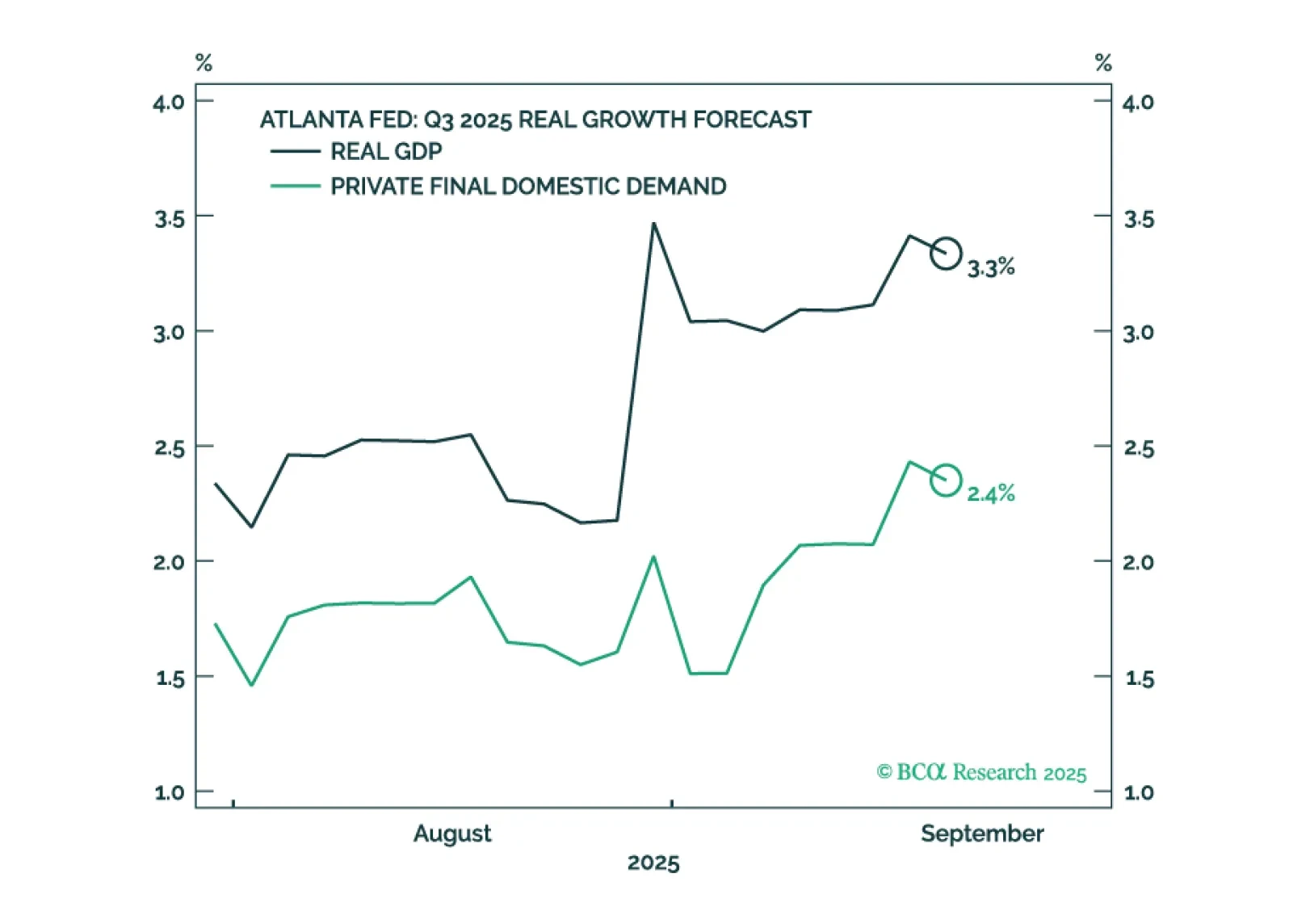

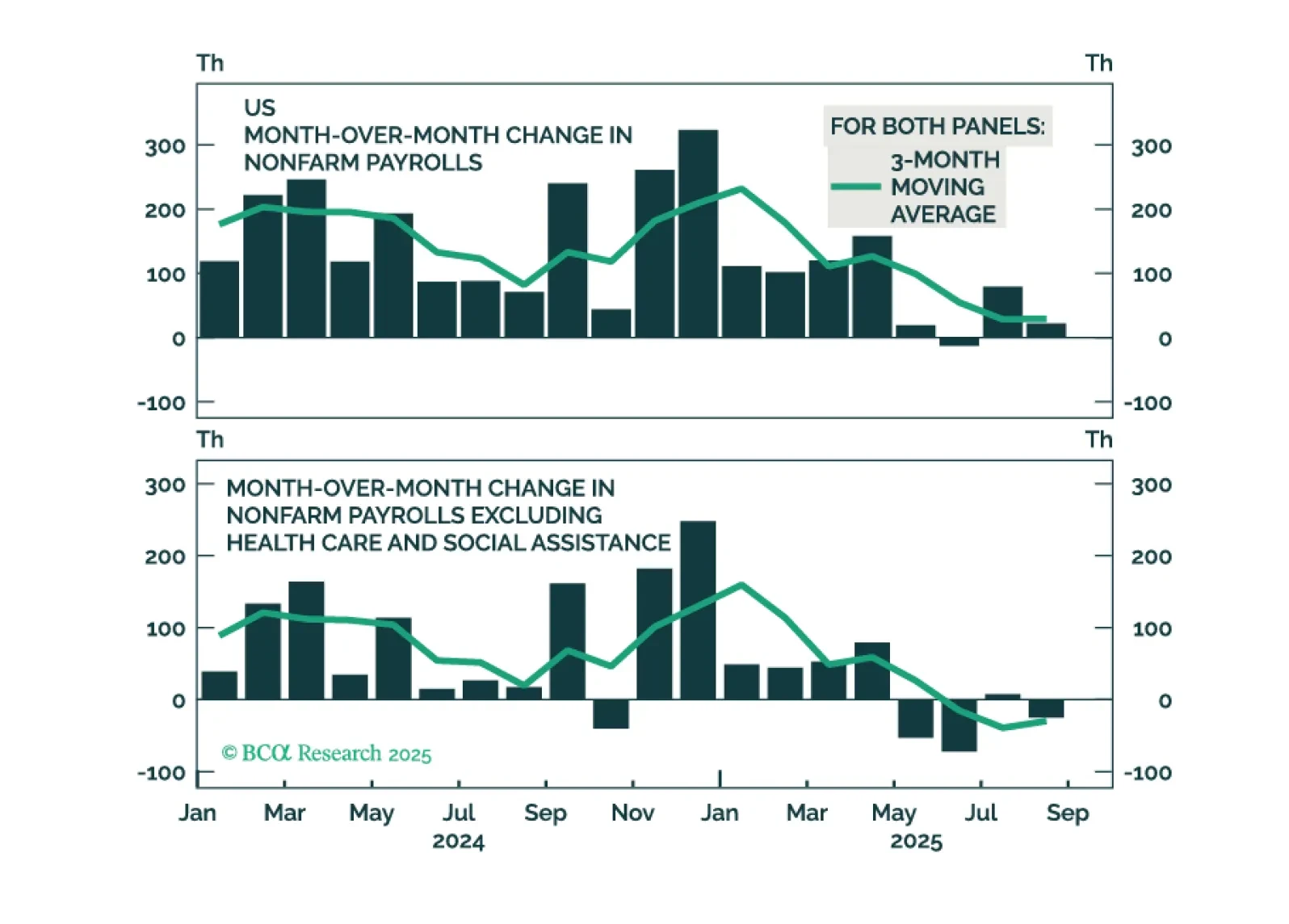

US GDP growth appears to have accelerated even as employment growth has faltered. We will make a final decision in early October when we publish our next Strategy Outlook, but most likely, we will cut our 12-month US recession probability to 40%-to-50% from 60% and turn tactically neutral on stocks, while still retaining a modest equity underweight over a 12-month horizon.

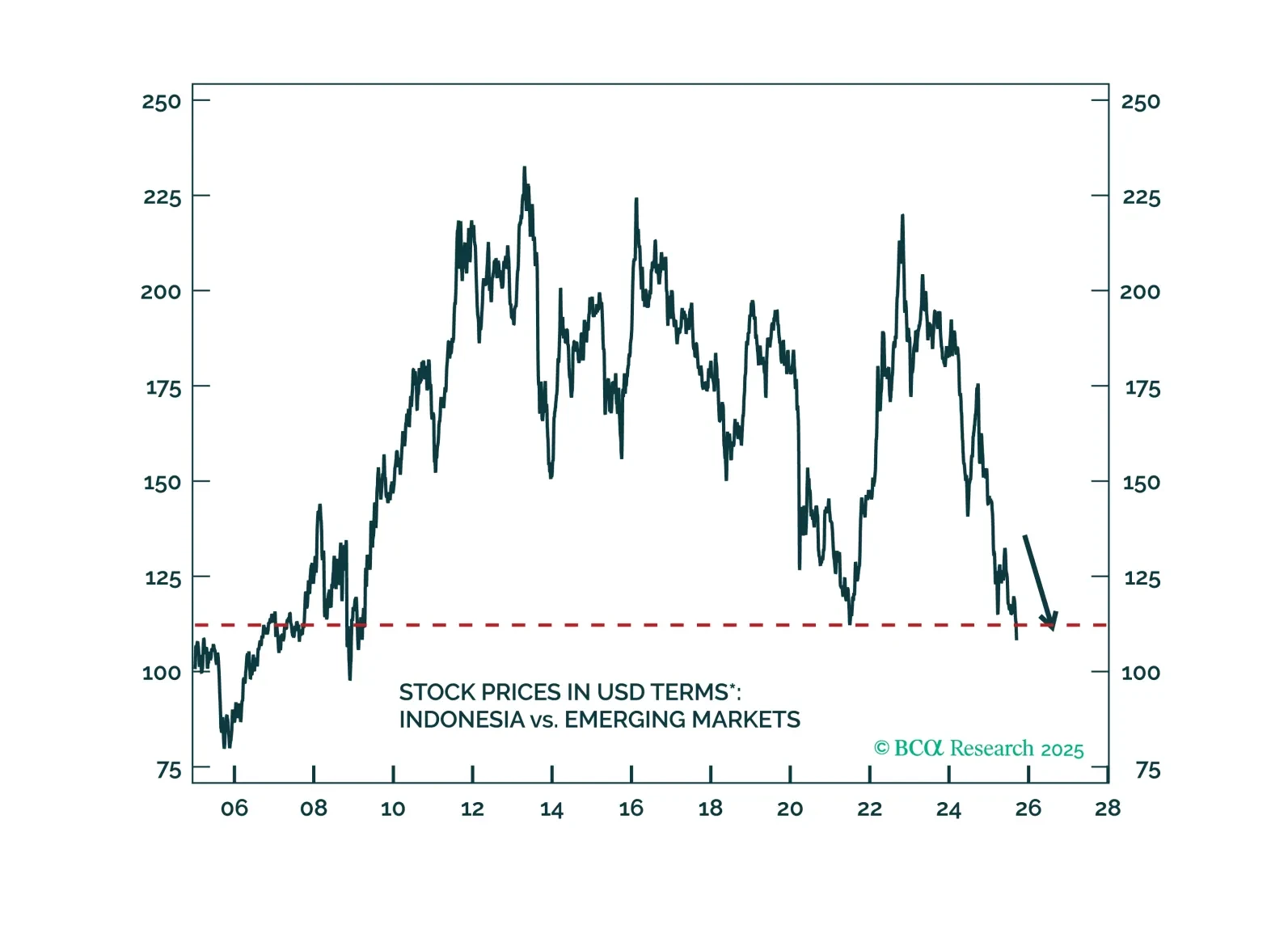

Indonesia’s policy easing will boost domestic demand, but fuel inflation. Current account deficit will widen, and the rupiah will weaken. Stay short the rupiah and go underweight Indonesian stocks, domestic bonds, and sovereign credit in their respective EM portfolios.

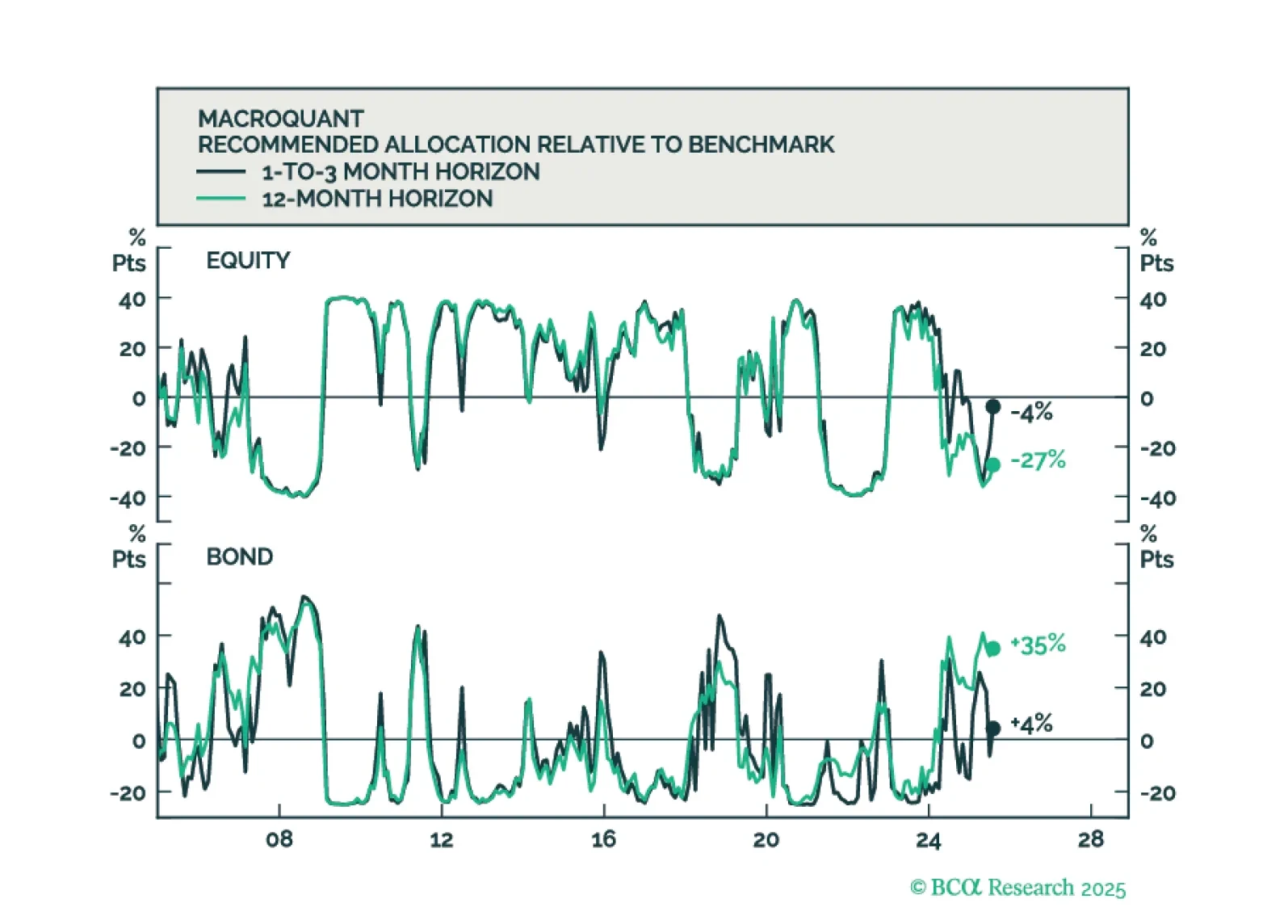

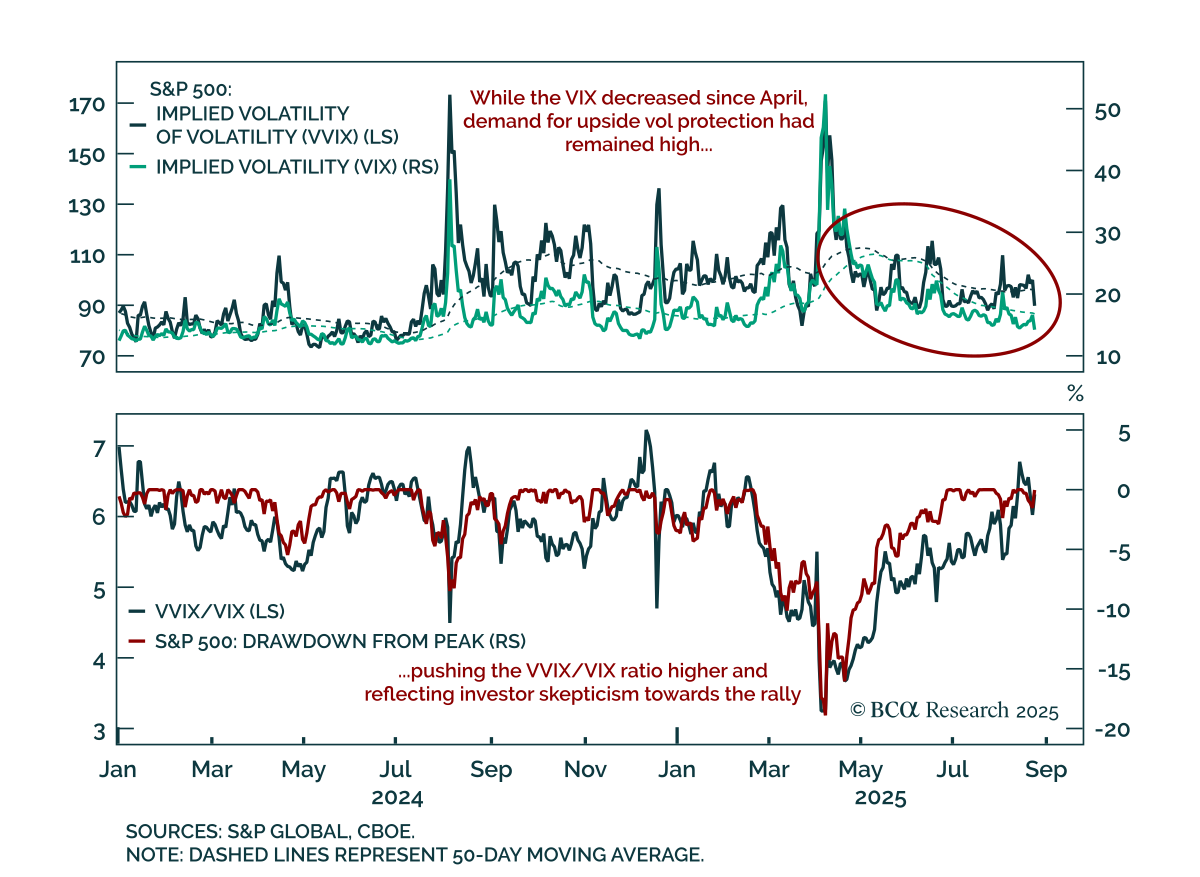

While it is impossible to know exactly when global equities will peak, there are now enough vulnerabilities to justify keeping one’s finger near the eject button.

MacroQuant sees downside risks to stocks over a long-term horizon but is not yet saying that we are at imminent risk of an equity bear market.

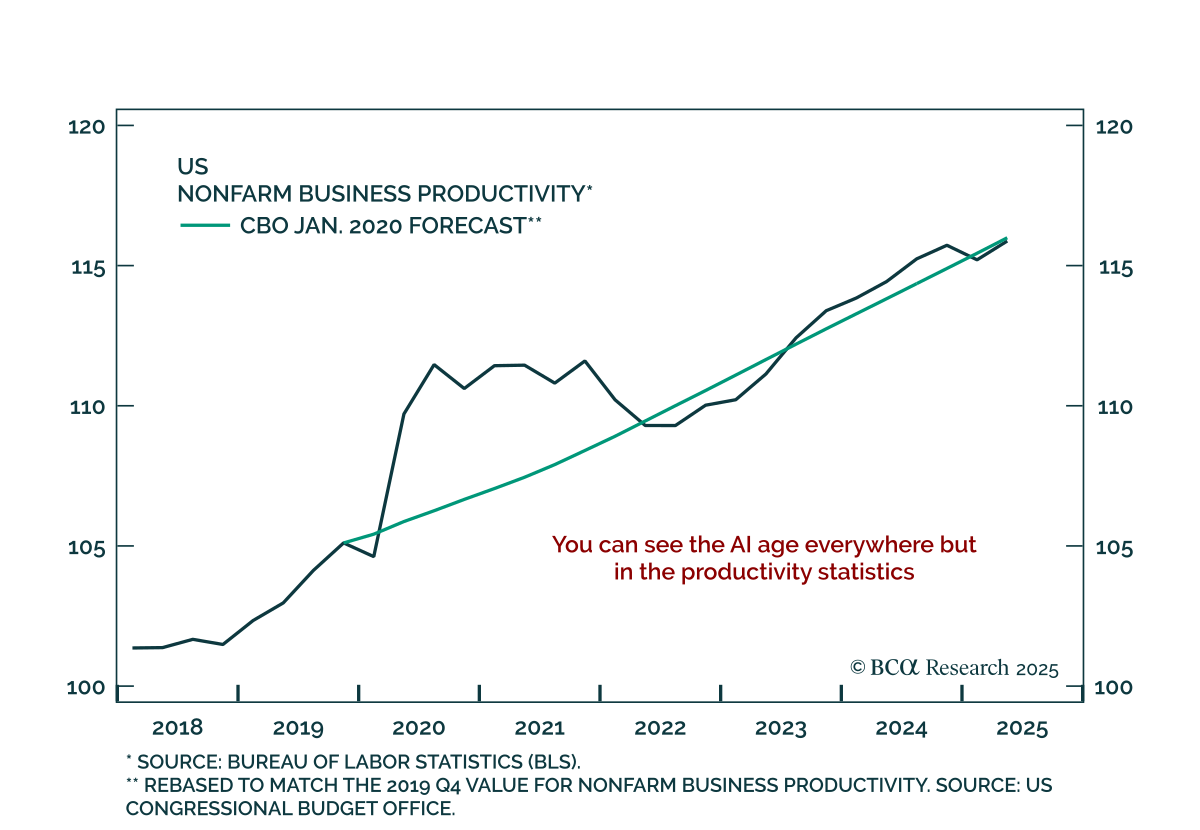

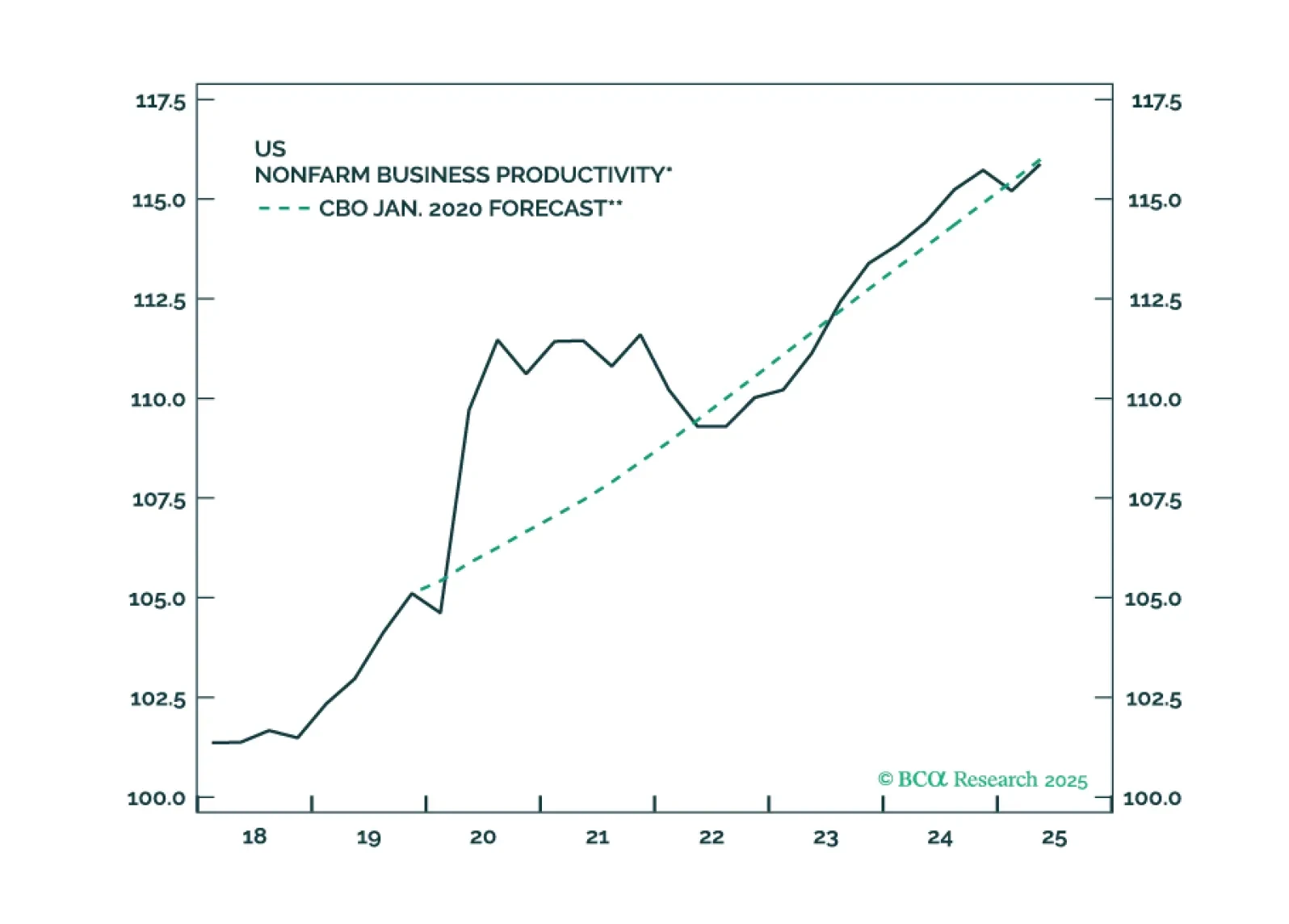

The AI boom has had less of an impact on the economy than widely believed. This may eventually change, but the risk is that investors grow impatient before it does.