Financial Markets

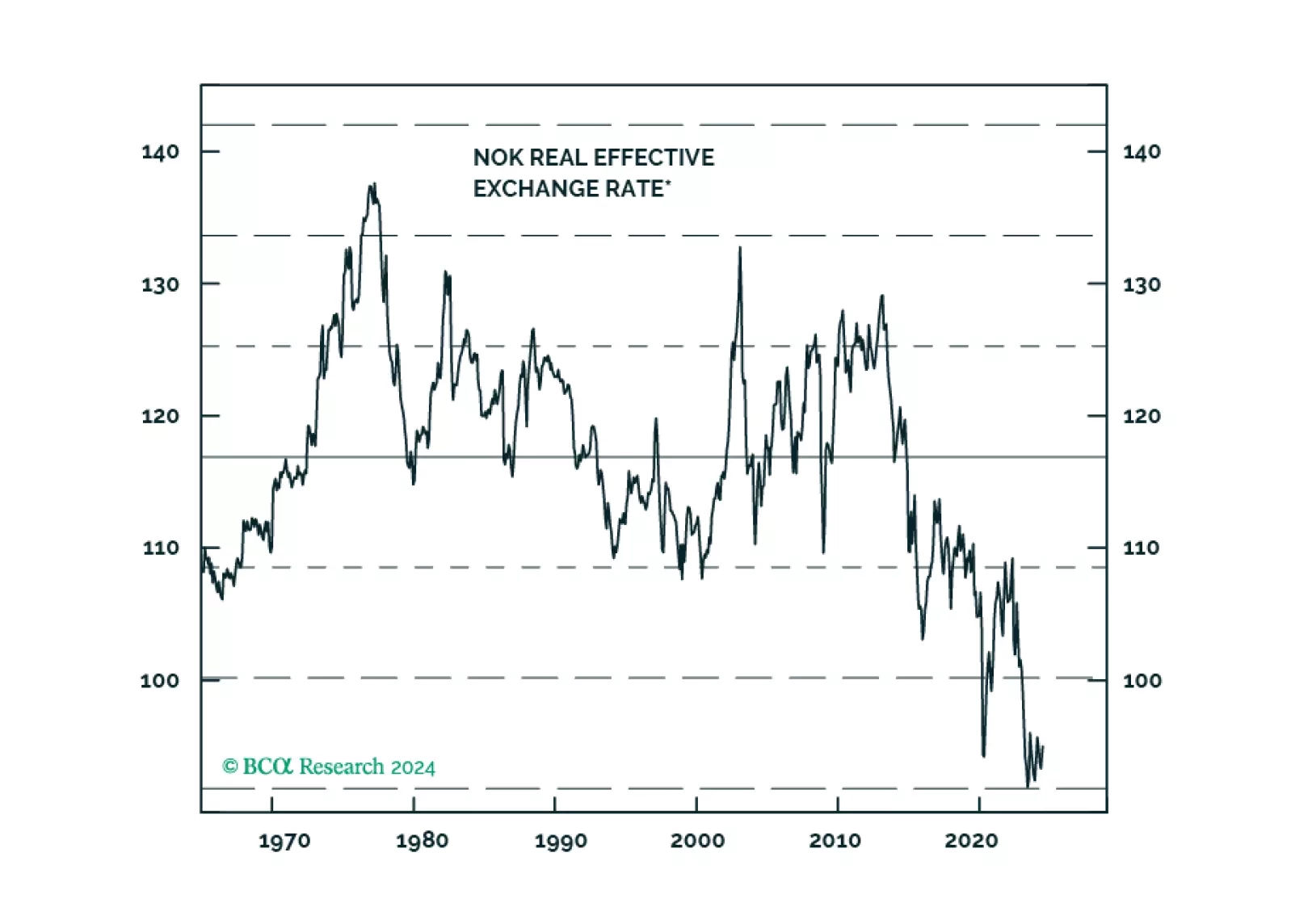

In this report, we gauge the reasons behind the persistently weak Norwegian krone, despite what appears to be benign domestic economic conditions.

The current Fed easing cycle will likely be a “buy the rumor, sell the news” phenomenon. The basis is our expectation that the US economy is heading into a rough landing. The primary driver of EM currencies is not US interest rates but the global manufacturing cycle.

Indonesian stocks have sold off sharply and underperformed their EM and emerging Asian peers – both in local currency and in common currency terms – despite the nation’s 5.1% real GDP growth rate (the highest rate among G-20 countries, second only to India).…

Market and economic observers have devoted a lot of attention to the Sahm Rule following July’s employment report, and whether or not it has been triggered. BCA’s analysis has highlighted that the overall direction of the labor market is far more important…

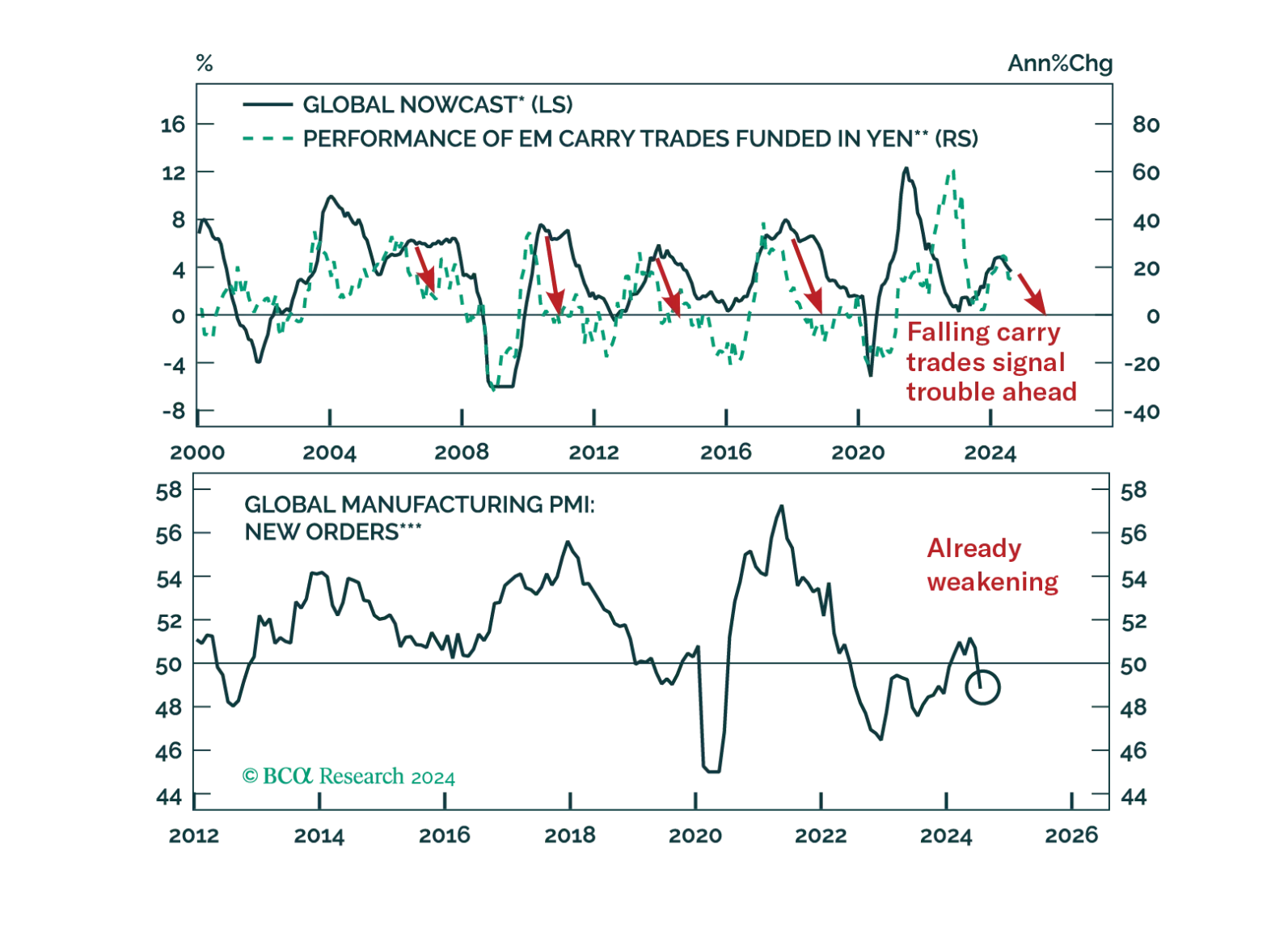

The unwind of yen carry trades caused violent tremors across the globe. Was this shock a one-off event or the prelude to more troubles?

The market backdrop changed a lot between the preparation and the publication of our equity downgrade report. We publish this companion Insight to help investors navigate the new environment.

Chinese exports in USD terms missed expectations in July, growing by 7.0% y/y, down from 8.6% in June. Conversely, imports rebounded smartly from a 2.3% contraction, rising by 7.2% in July and upending expectations of 3.2%. Slower export growth is…

The BoJ delivered a surprise rate hike last week, then proceeded to sending a more dovish signal on Wednesday. Deputy Governor Shinichi Uchida strongly hinted at a central bank that would refrain from hiking further in times of market instability. The yen,…

According to BCA Research’s GeoMacro Strategy service, the reason that the bears have been wrong for the past 18 months is that consumers have defied the expectations of most learned economists. As our colleagues posited in late 2023, US consumers would not…