Financial Markets

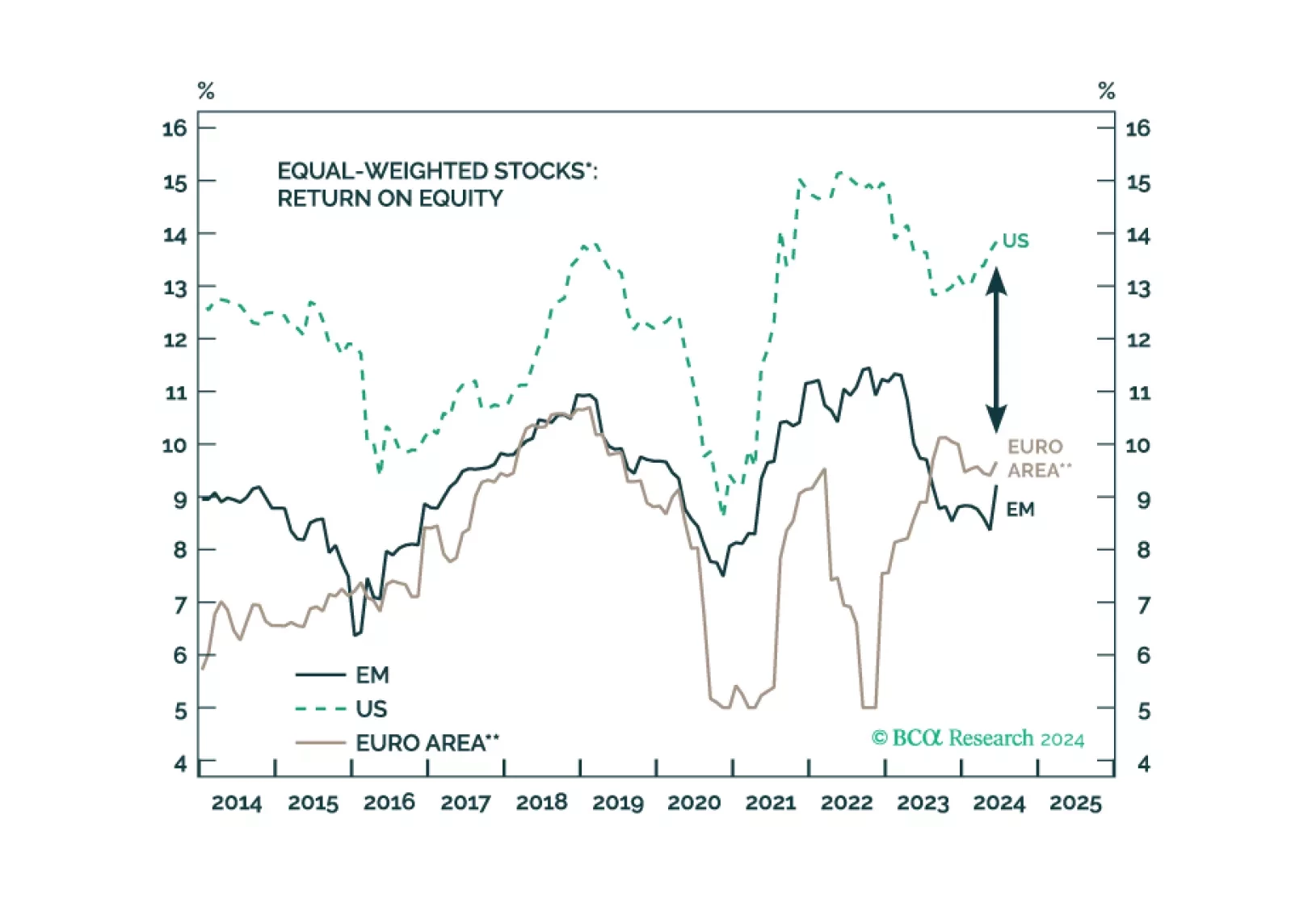

The failure of EM stock prices to rally over the past 13 years is rooted in their companies’ inability to grow their profits. Even though EM equities appear cheap based on their cyclically adjusted P/E ratio, there has been a regime change in EM corporate profitability. Therefore, the CAPE model should not be used to value EM stocks now.

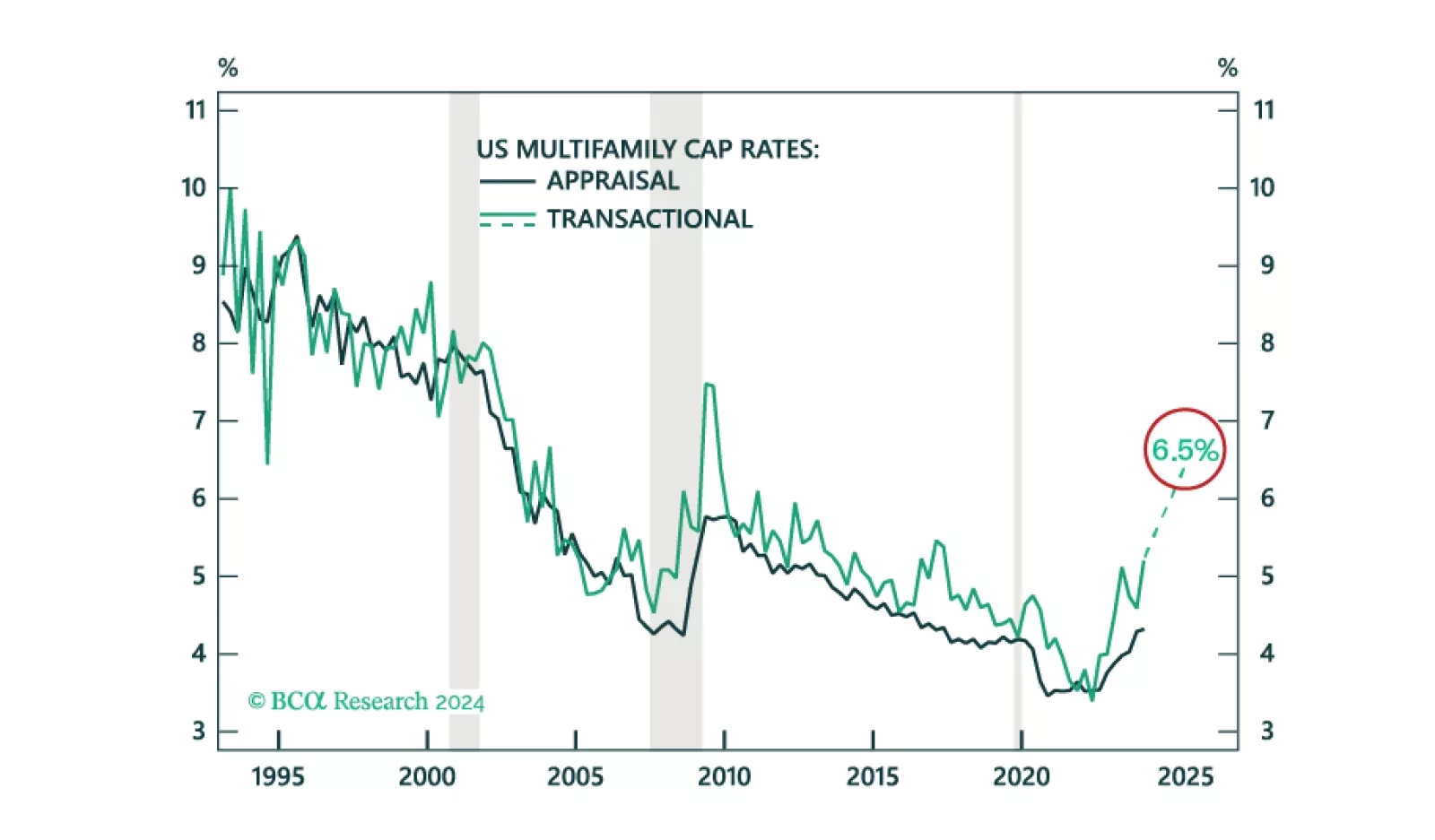

We project US Multifamily cap rates to increase from 5.2% to 6.5%. While we find an unfavorable risk-adjusted return on the asset, especially relative to other opportunities in CRE, cap rates are moving closer to peak.

At first glance, France has moved to the far left. However, this coalition is fragile, and Macron’s allies still hold the balance of power. What are the assets that will benefit from this new political setup, and those that will not?

Although we ticked a second box on our checklist, the incoming data still do not indicate that a recession is imminent. We remain tactically equal weight equities with a strong bias to underweight them, but we’re not exiting the party just yet.

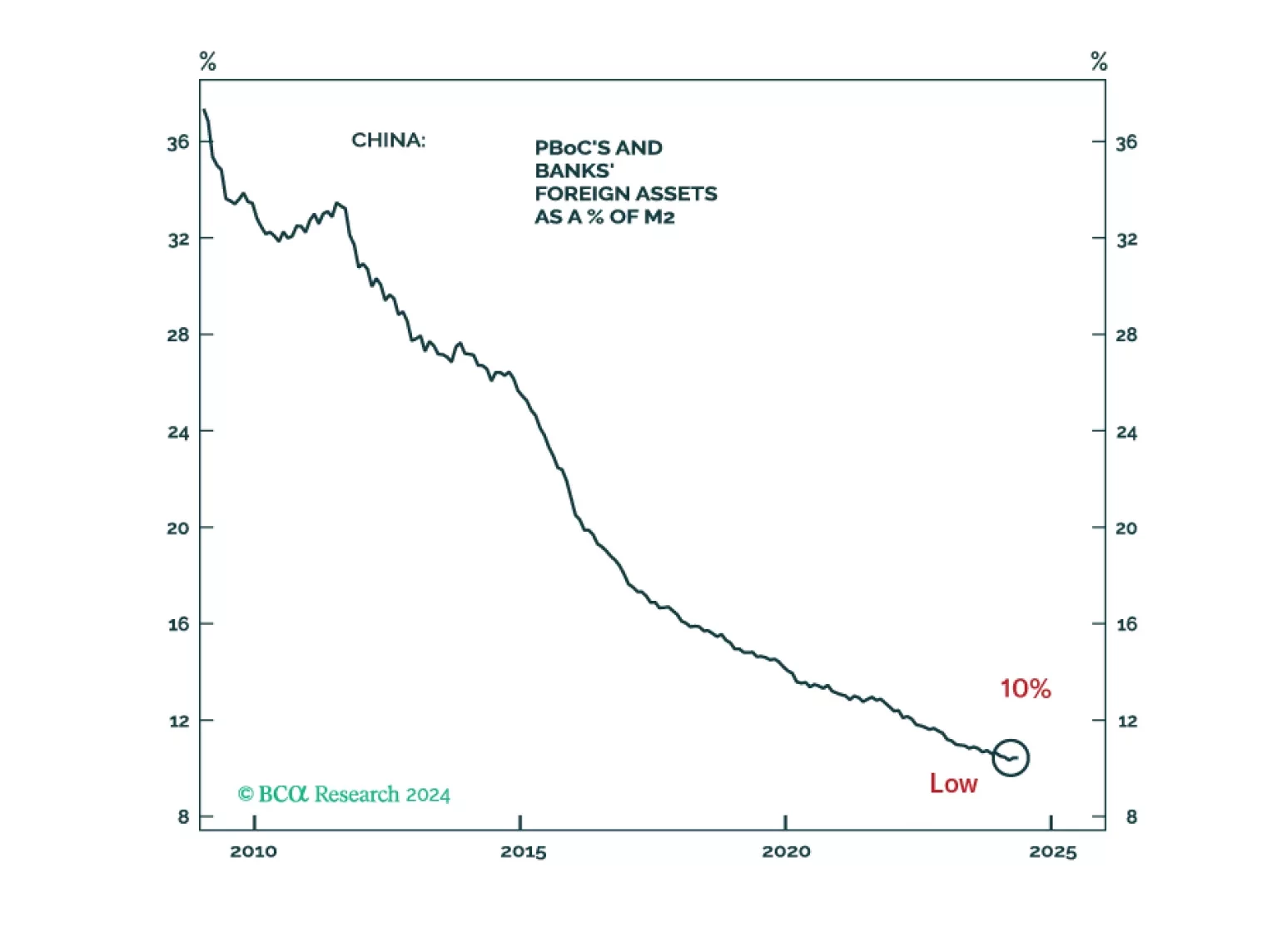

Is the RMB cheap or expensive? Based on trade accounts, the yuan is inexpensive, but the RMB is vulnerable due to capital outflows. Yet, Beijing will not resort to a rapid devaluation for now, and the option of floating the currency is improbable. The PBoC will allow a gradual depreciation of the yuan versus the dollar, say around 5%, in the next six months.

The PBoC appears increasingly uncomfortable with the rapid decline in the Chinese government bond yields. While the PBoC will succeed in temporarily curbing investors’ enthusiasm for bonds, the central bank will be unwilling to raise interest rates and unable to intervene in the bond market in any meaningful and lasting way.

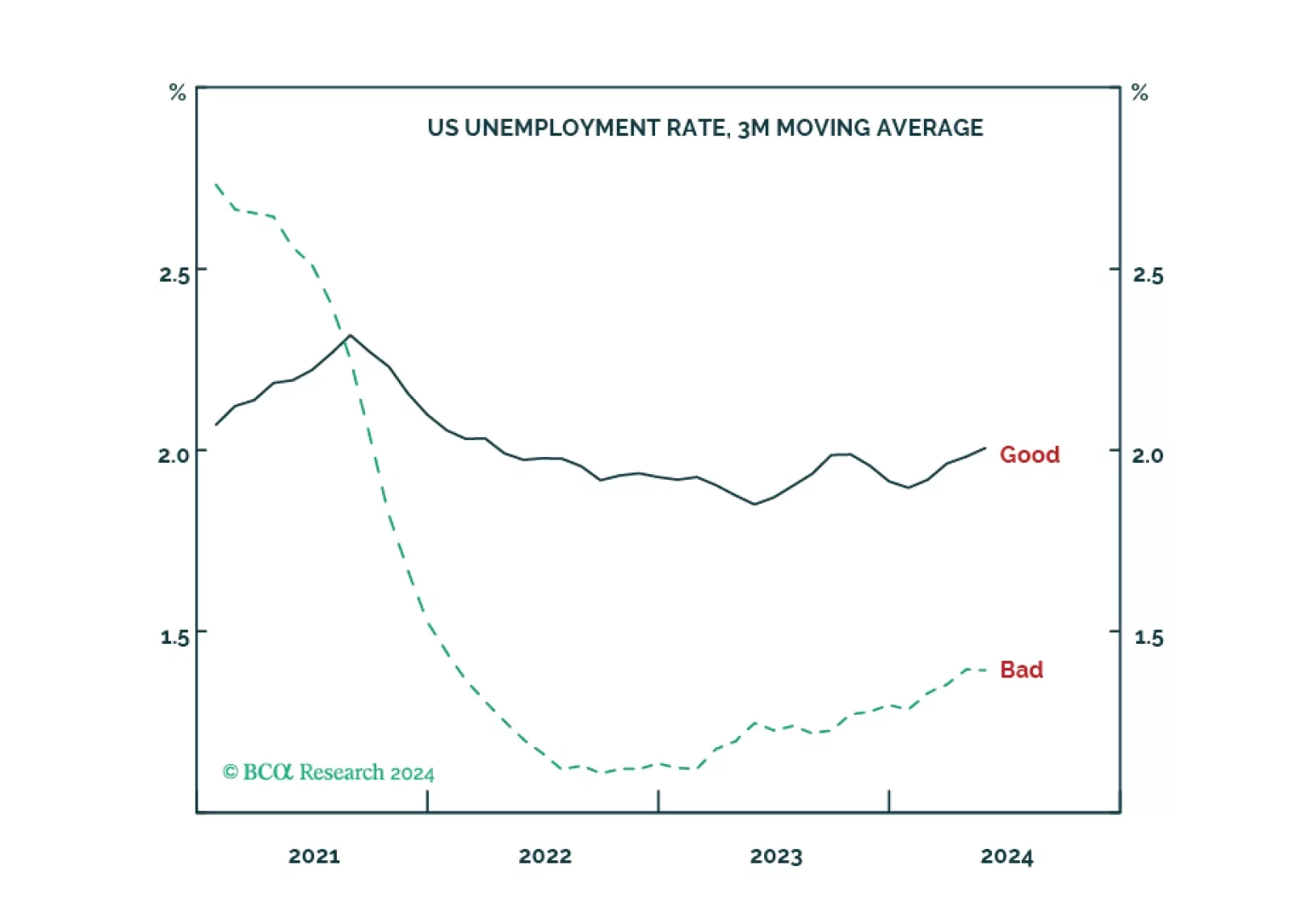

We explain how to distinguish between ‘good’, ‘bad’ and ‘ugly’ unemployment, why bad unemployment is a much better gauge of the jobs market than headline unemployment, and what this means for the tactical positioning in bonds and stocks. Plus: base metals (XBM) have already sold off sharply, so take profits in the short position and open a tactical overweight in global materials (MXI).