Financial Markets

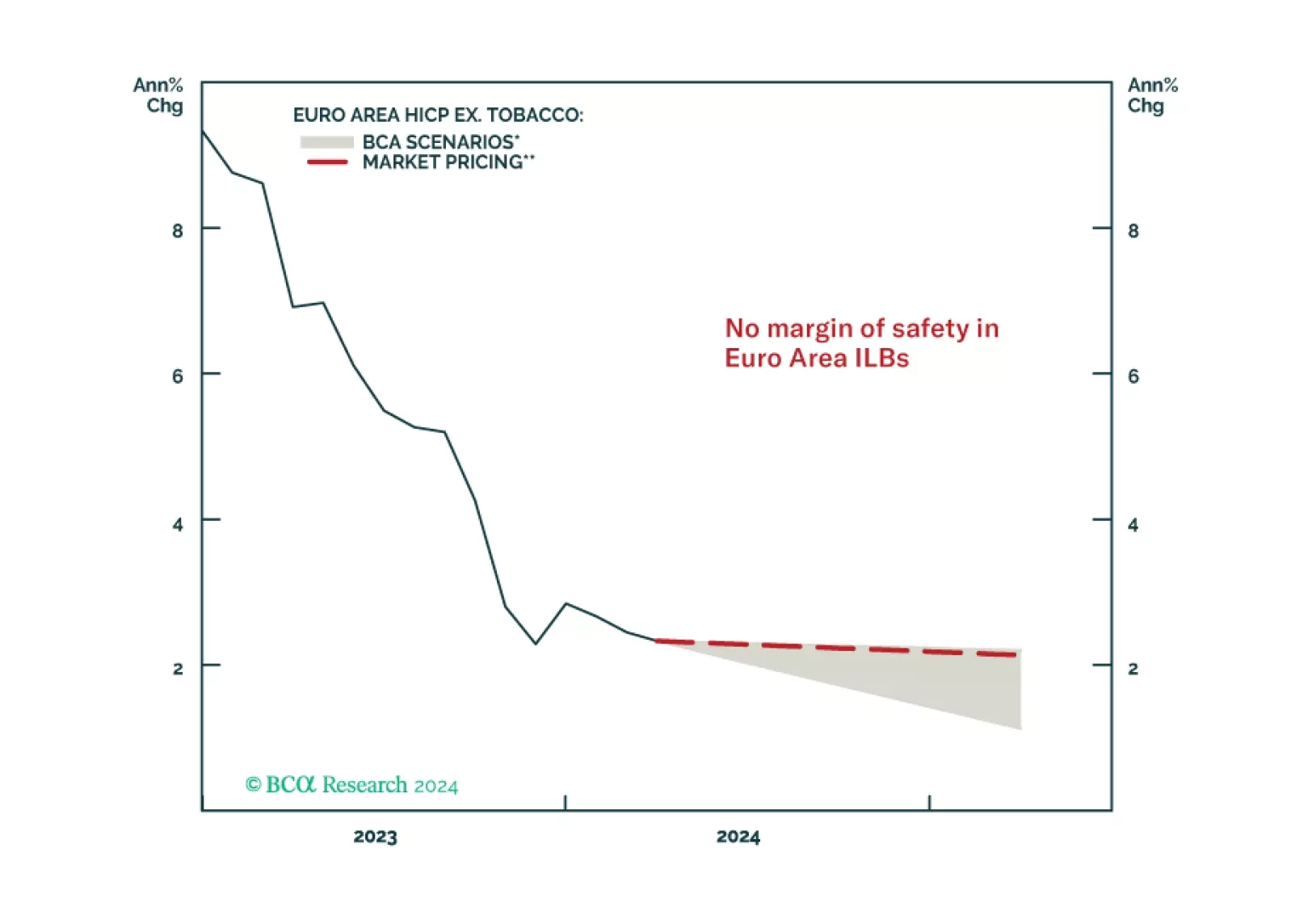

In this Special Report, we introduce our Euro Inflation-Linked Golden Rule – a framework to profitably trade and invest in Euro Area inflation-linked bonds versus nominals. The Rule is currently signaling that nominal government bonds should outperform inflation-linked bonds over the next year as disinflation in the Euro Area continues.

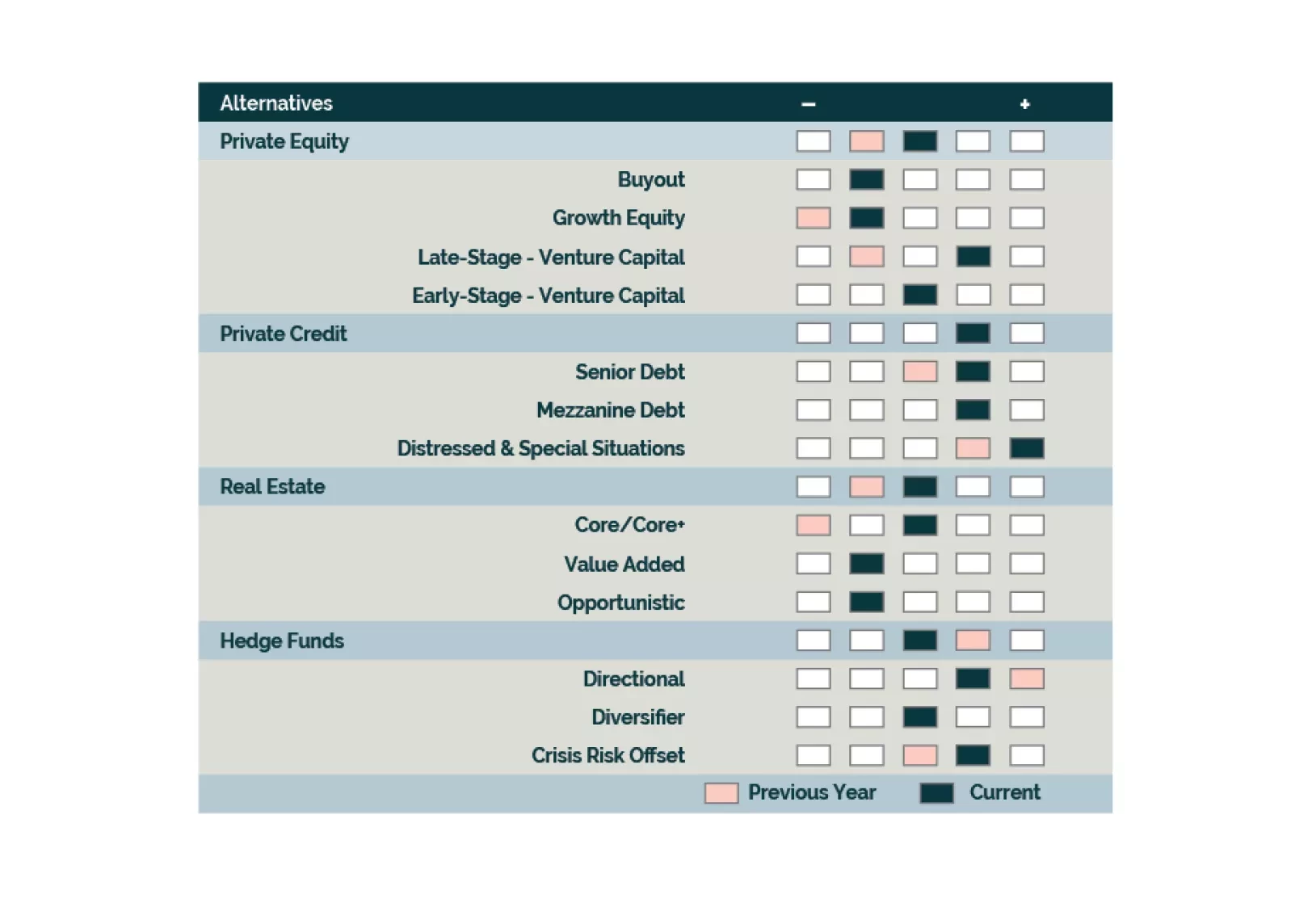

We go overweight Late-Stage Venture Capital and APAC Private Equity but remain underweight North America Buyouts. We maintain our neutral outlook towards Hedge Funds and are positive on Long-Short Equity, Event Driven, and CRO strategies. We are cooling towards Direct Lending strategies as competition and relative opportunities increase. CRE’s downturn continues to unfold; we are starting to be buyers.

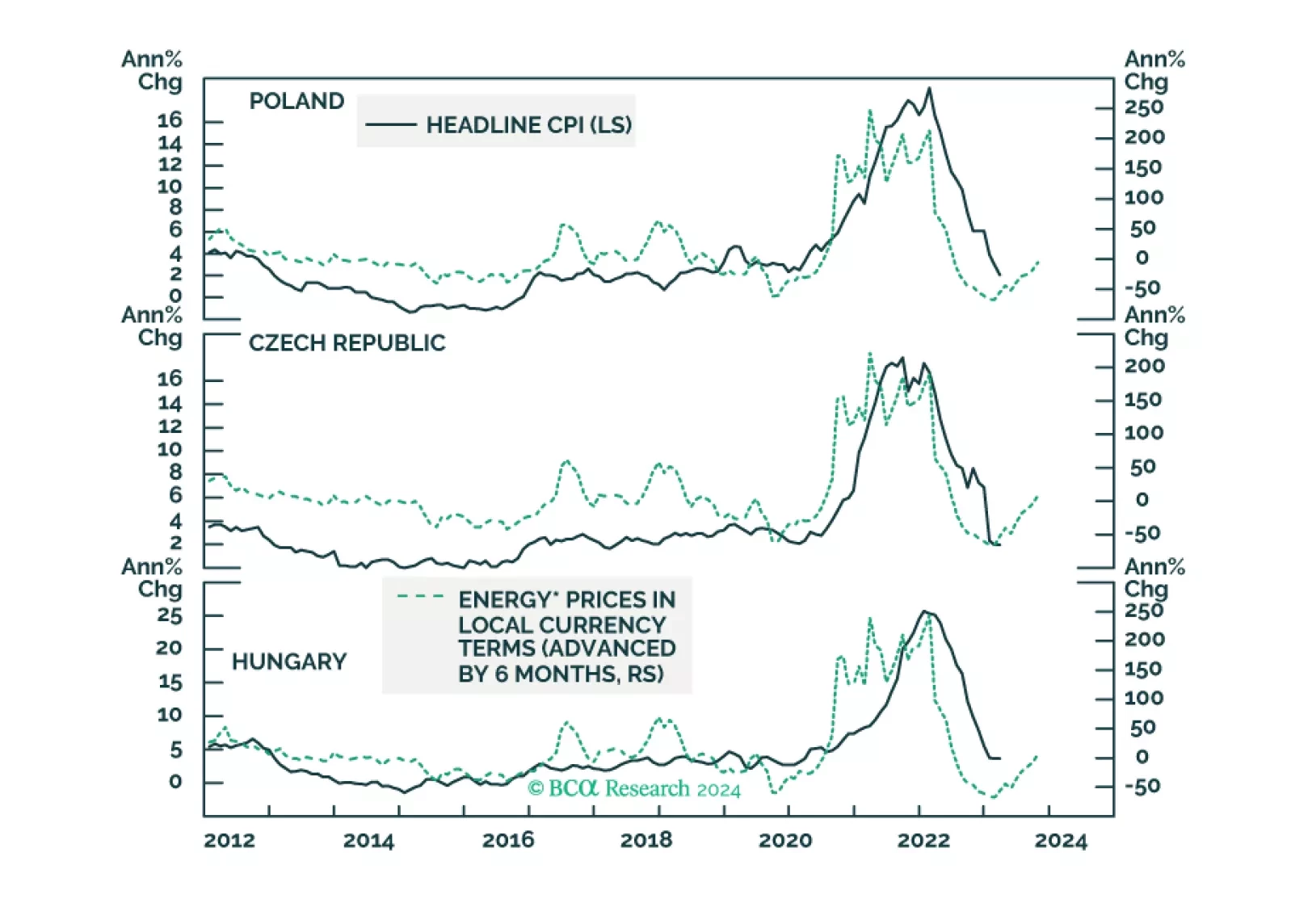

The disinflation process is over in Poland and Hungary. Only the Czech Republic will see its core inflation meet its central bank target this year. The reason is much tighter labor market dynamics in the first two. Investors should continue to short a basket of CE3 currencies vis-à-vis the US dollar.

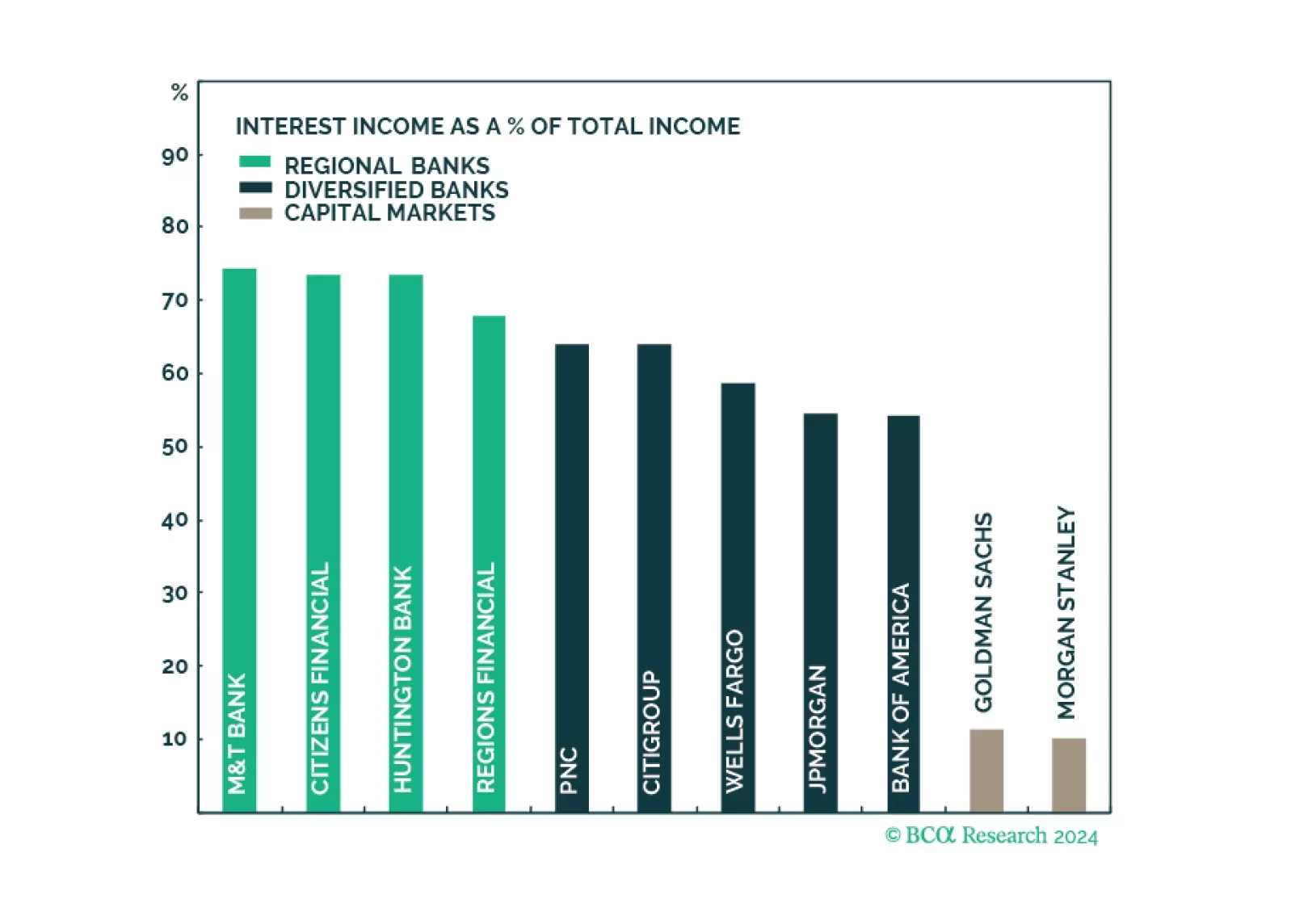

Q1 earnings results of the largest US banks have demonstrated that the engine of recent growth in profitability, NII, has faltered as funding costs are rising fast. However, the resurgence in non-NII thanks to a revival in corporate activity has been a saving grace. Earnings growth appears to have bottomed, while valuations are attractive. To play up portfolio exposure to an upcoming surge in capital markets activity, and minimize exposure to declining profitability in traditional banking services, overweight Diversified Banks and Capital Markets, and underweight Regional Banks.

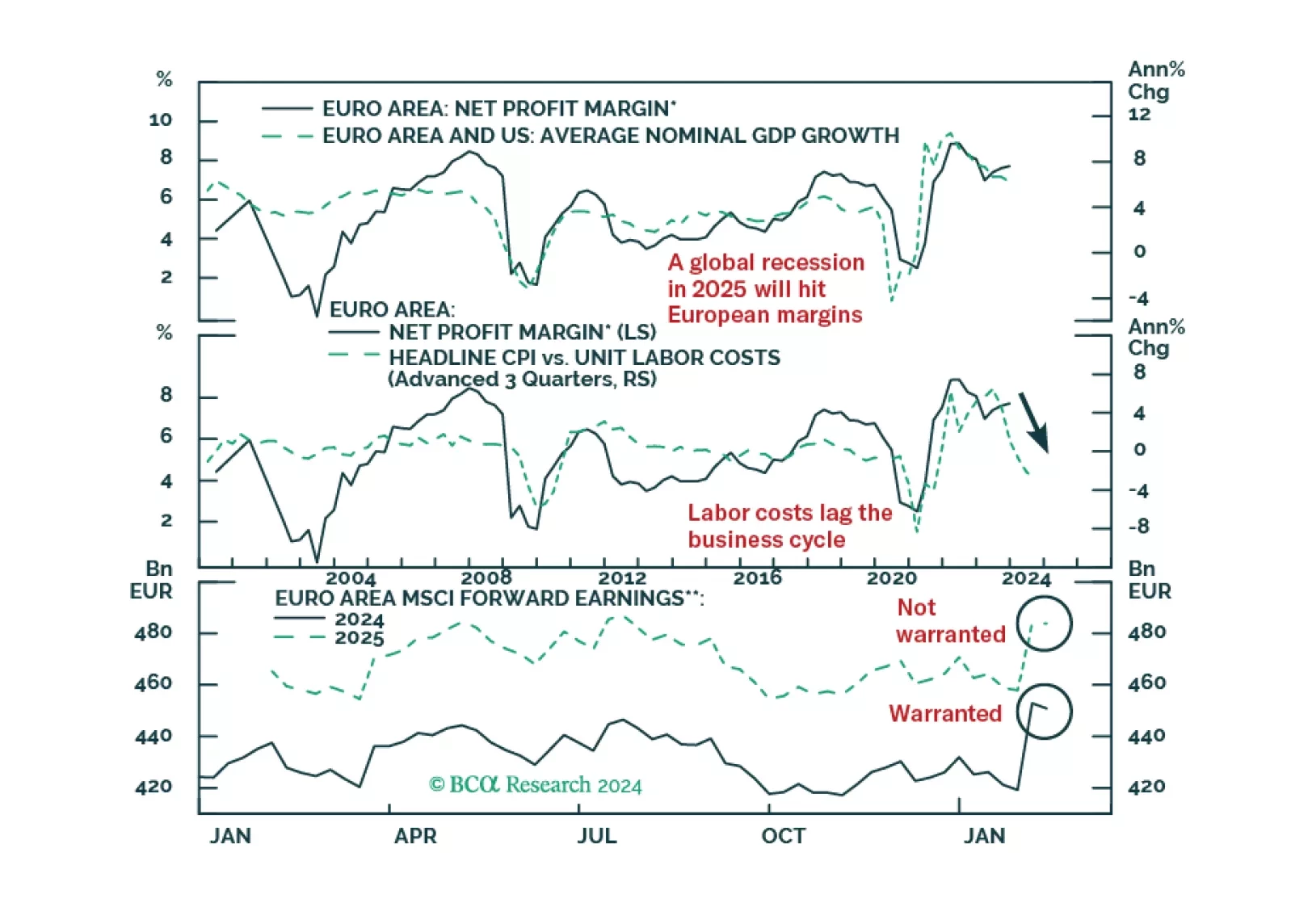

European profits margins are elevated. Will a mild recession be enough to bring them down?

This Special Report introduces a framework for assessing the relative importance of slope change and initial yield in curve trade performance. The yield penalty for curve steepeners has fallen significantly since the beginning of the year, and we recommend shifting out of Treasury curve flatteners and into Treasury curve steepeners in US bond portfolios.

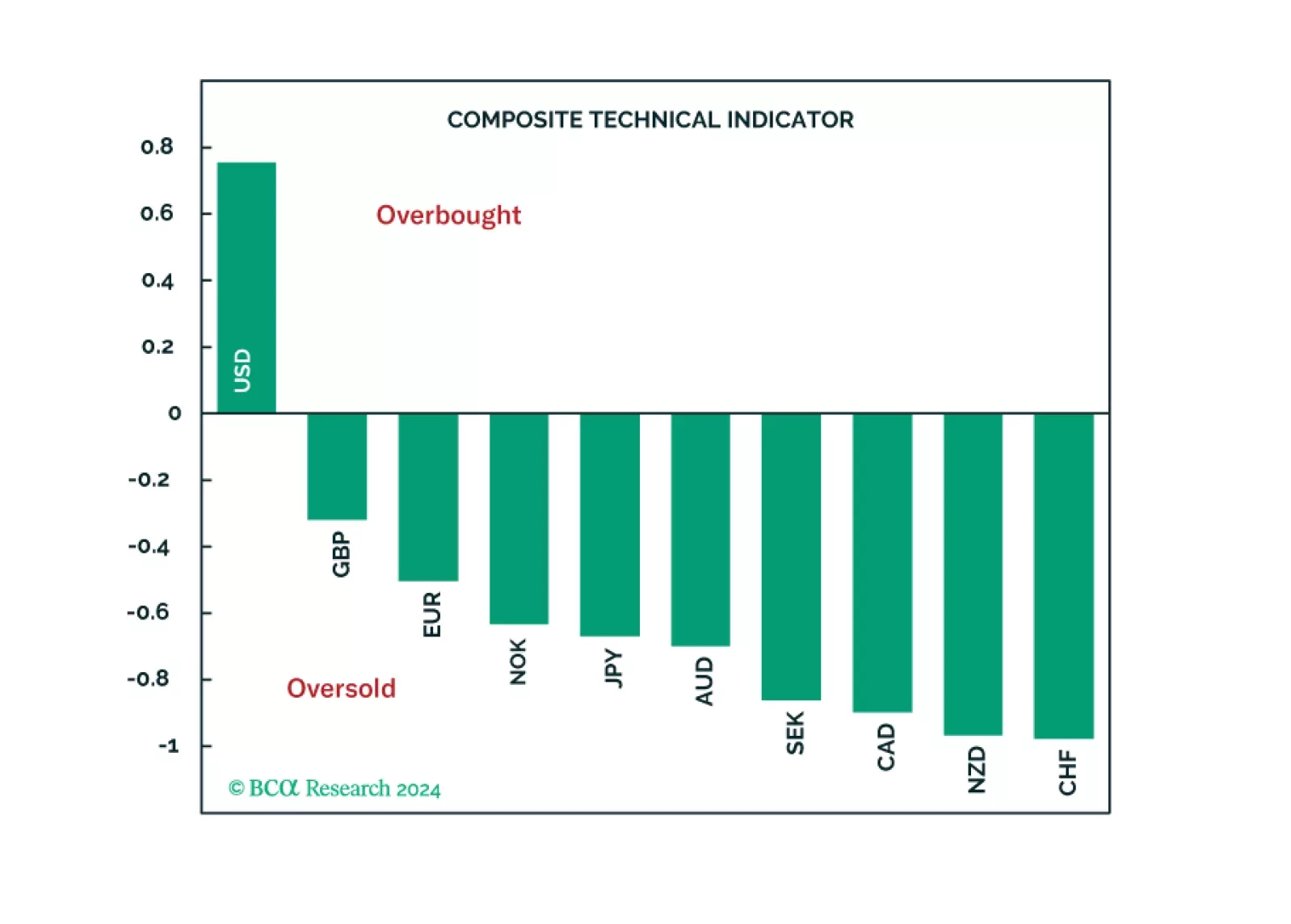

In this report, we review what our technical indicators are telling us about the G10 currencies.

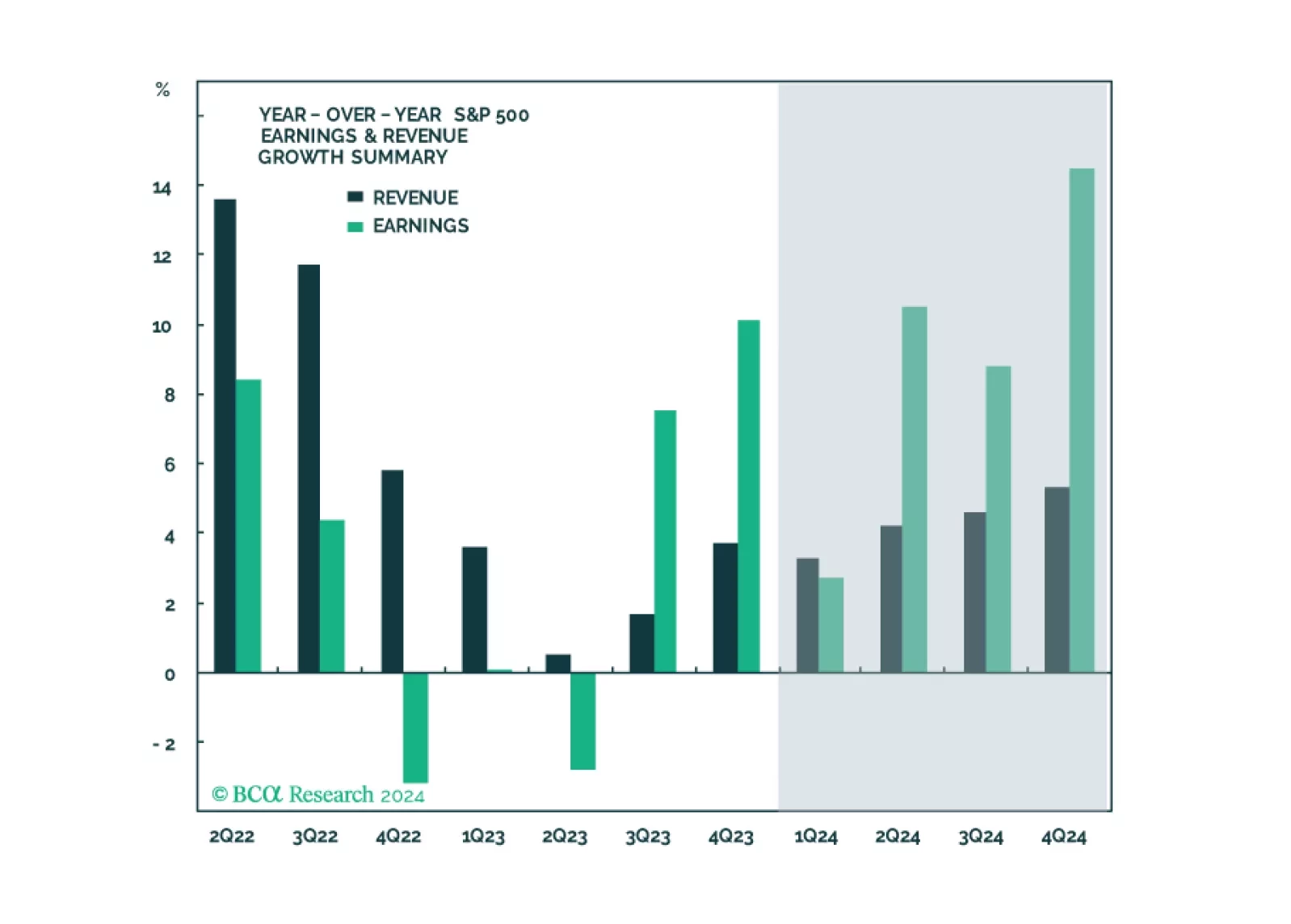

In this note, we preview the Q1-2024 earnings season, give our take on expectations and share what we will be watching.