Financial Markets

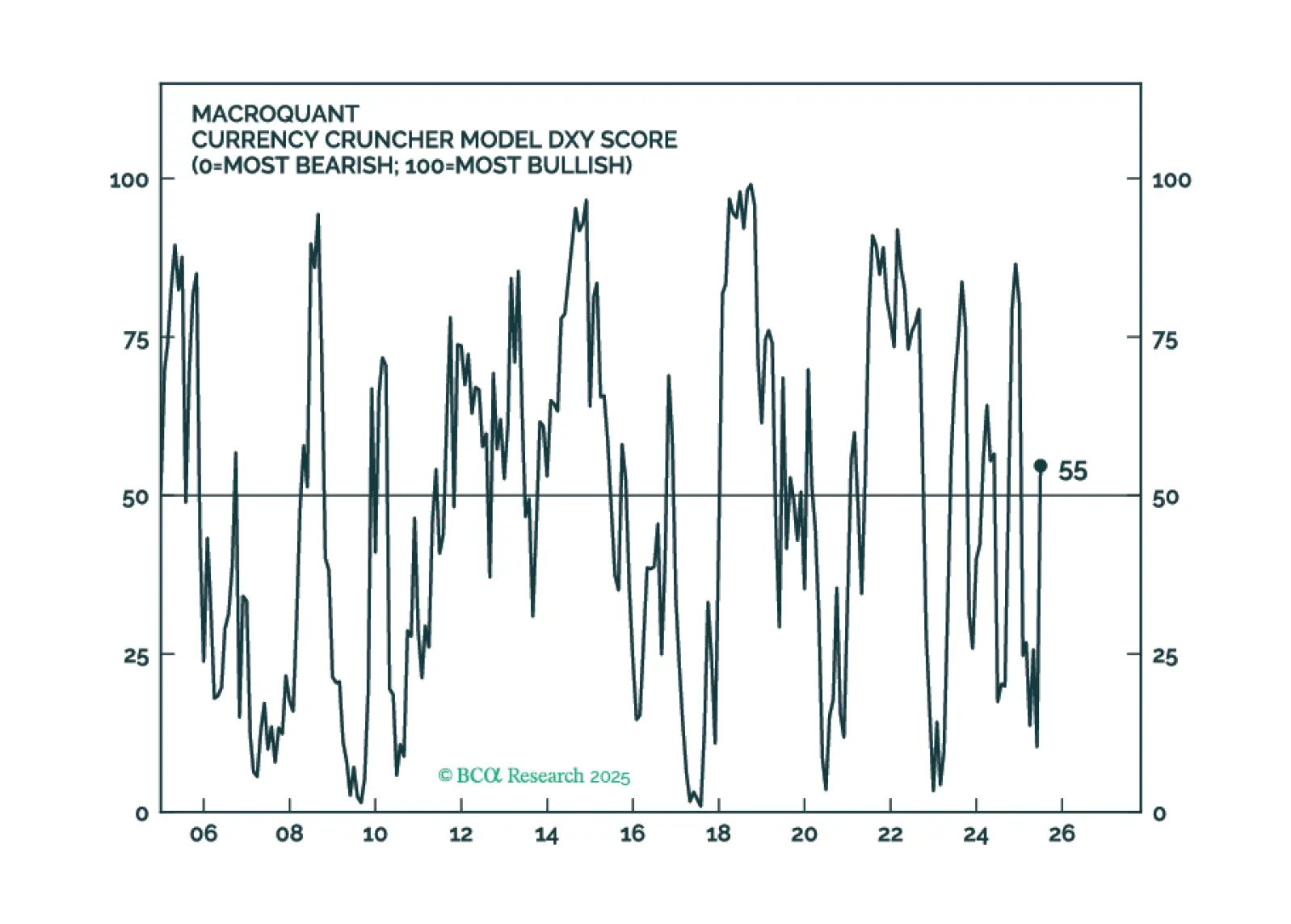

MacroQuant is recommending that equity investors keep their finger near the eject button but avoid pressing it for now. The model is warming up to the dollar again and sees scope for oil prices to rise.

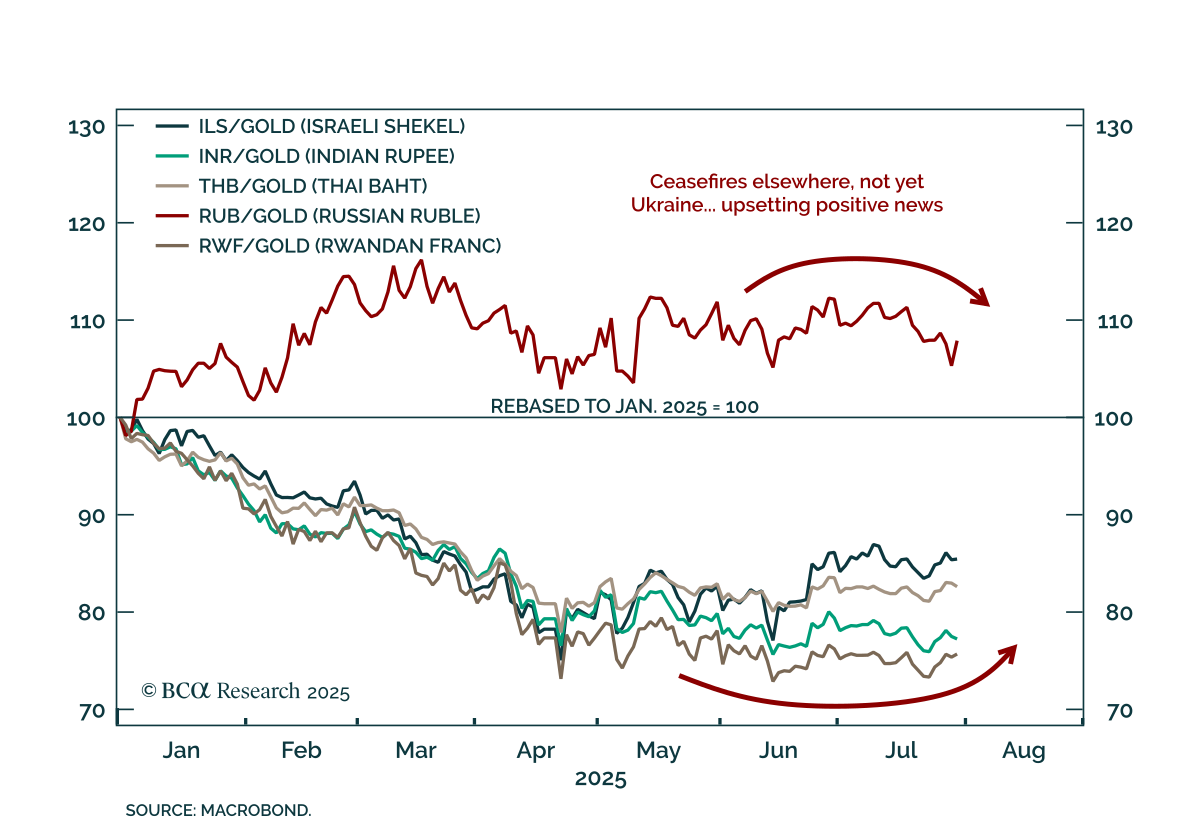

BCA’s US Political strategists warn that Russia presents an immediate market risk, with near-term pullbacks offering potential buying opportunities. President Trump is pivoting toward ceasefires and trade deals, supported by approval ratings and electoral…

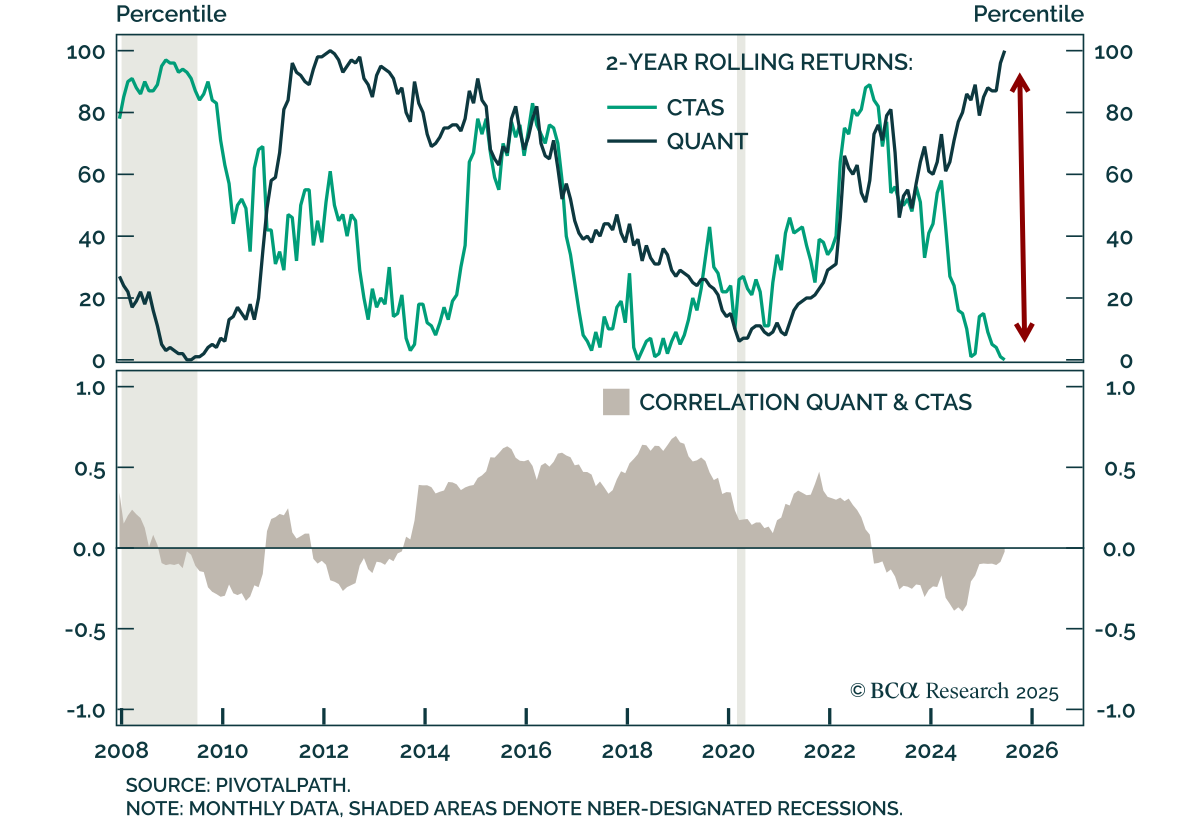

A historic divergence between systematic strategies is creating a compelling entry point into Managed Futures. Our Chart Of The Week comes from Brian Payne, Chief Strategist for our Private Markets & Alternatives team.In their…

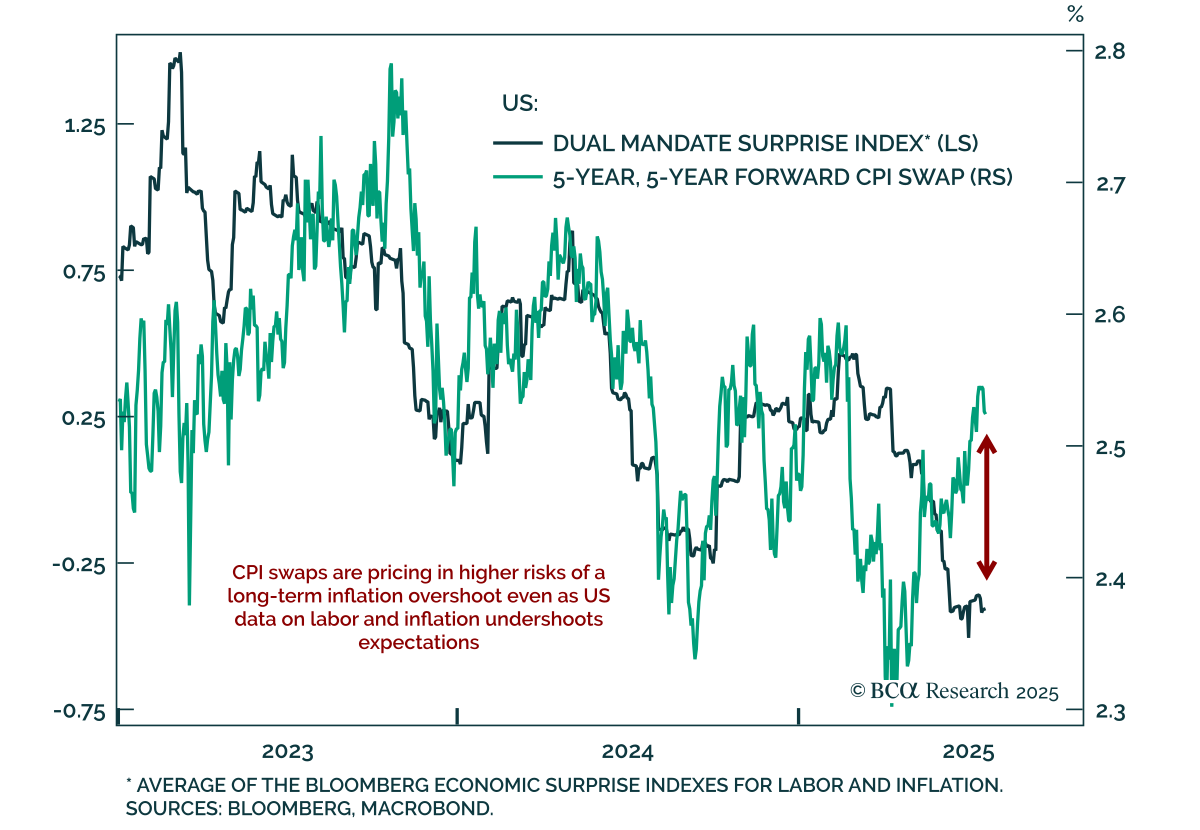

Rising political pressure on the Fed risks undermining policy credibility, risking a de-anchoring of long-term inflation expectations. The Trump administration keeps escalating attacks on Fed Chair Powell. While the Fed cannot ease proactively amid…

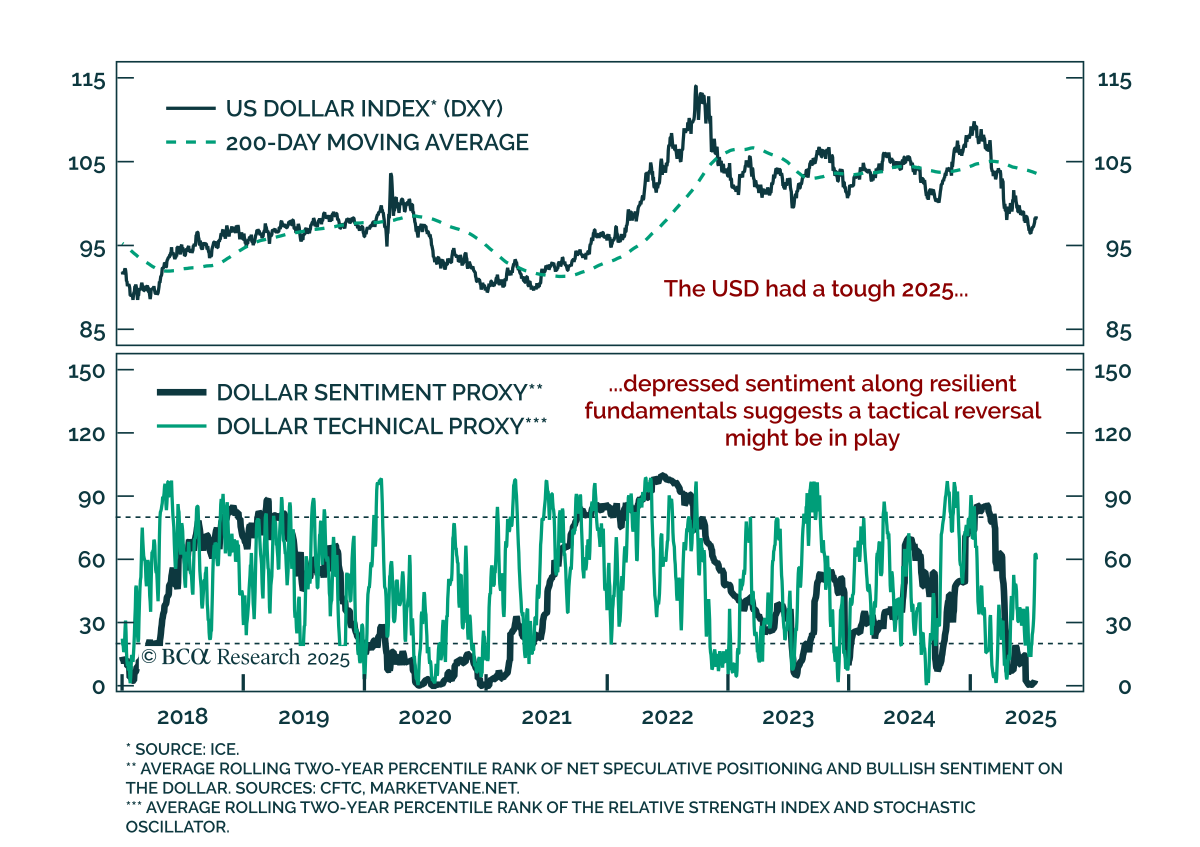

The USD remains structurally challenged, but near-term tactical conditions suggest a temporary bottom is in place. After a sustained selloff and rising concerns around its reserve status, the dollar has decoupled from rate differentials, a behavior more…

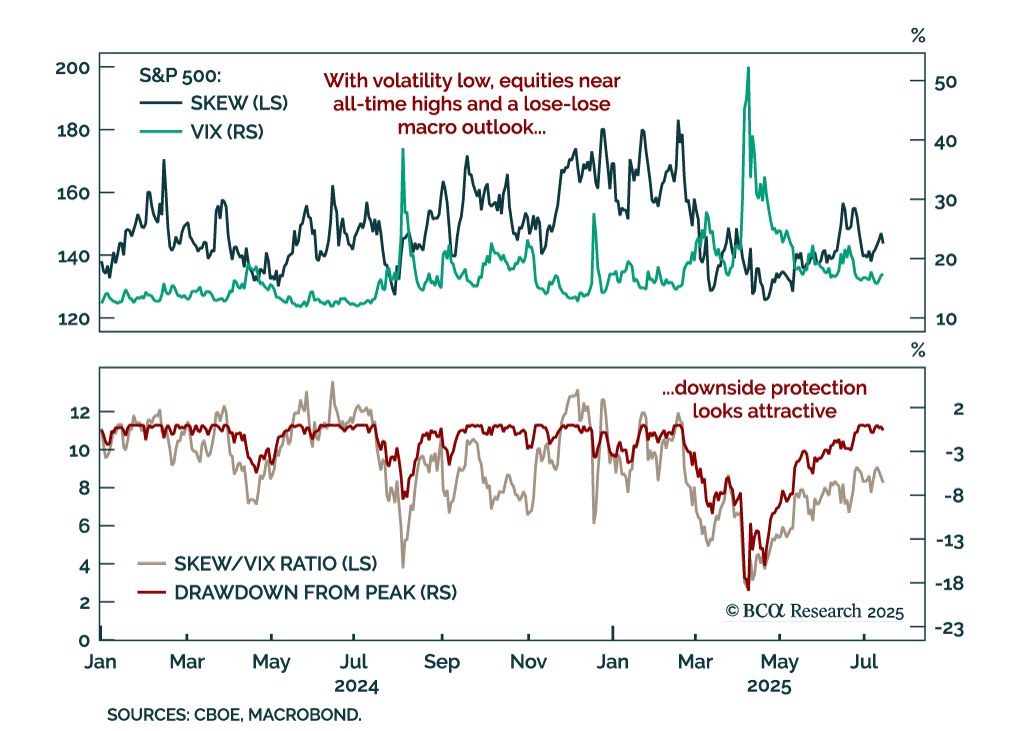

The S&P 500 sits near all-time highs, but sentiment and positioning suggest euphoria has not driven this rally. Prices are elevated, yet the SKEW/VIX ratio sits at 8.3, or its 67th percentile. While not at extreme levels associated with reversals, it…

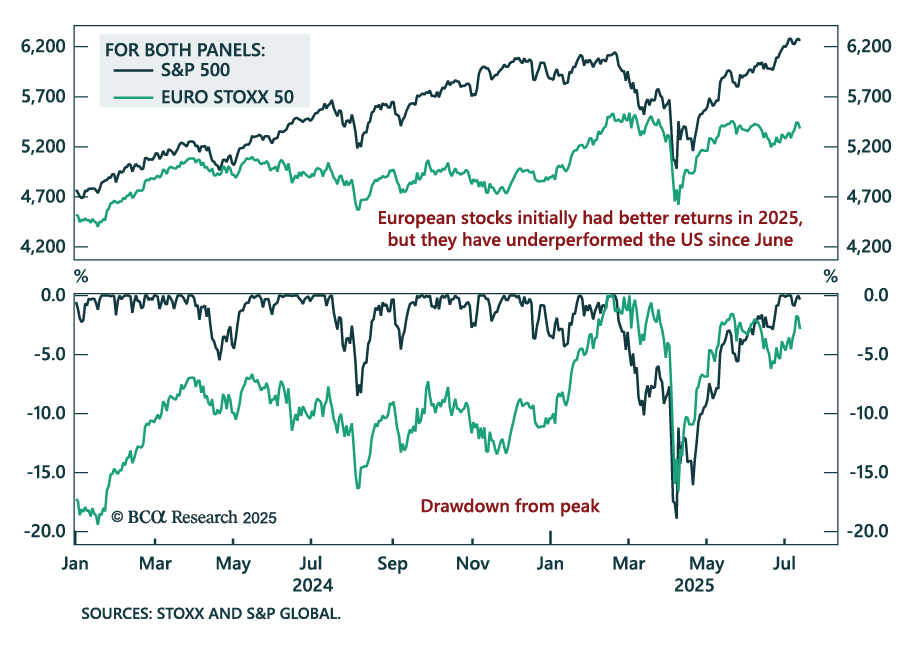

European equities have recently lagged the S&P 500, with short-term risks building despite a constructive long-term outlook. After reaching all-time highs in February, the EURO STOXX 50 began to stall as US markets sold off on Deep Seek headlines. The…

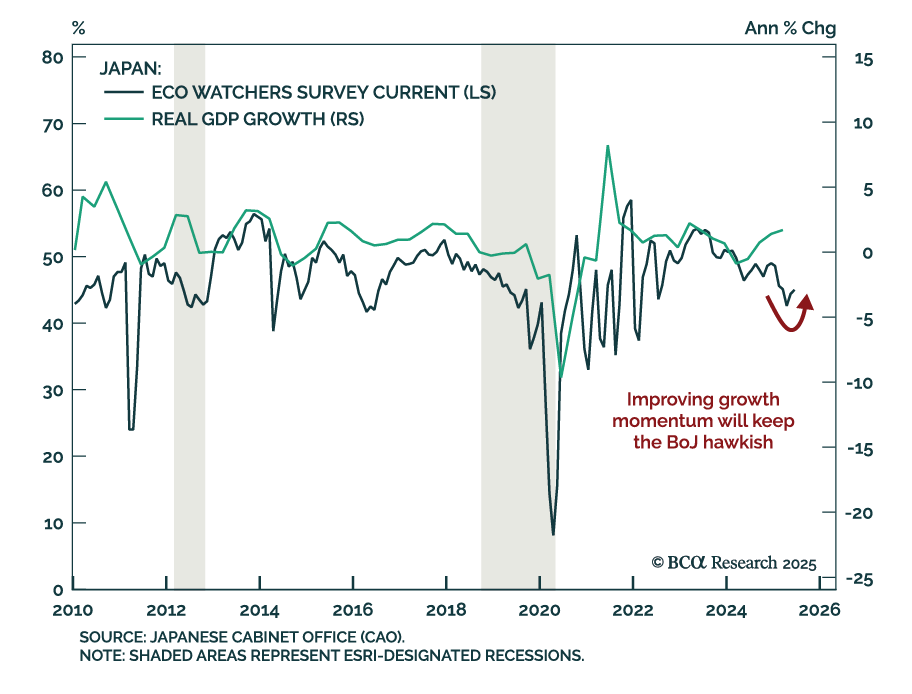

Japan’s improving growth momentum and structural inflation shift support an underweight in JGBs and long JPY positioning. The June Eco Watchers Survey was broadly in line with expectations, with current conditions ticking up to 45.0 and expectations modestly…

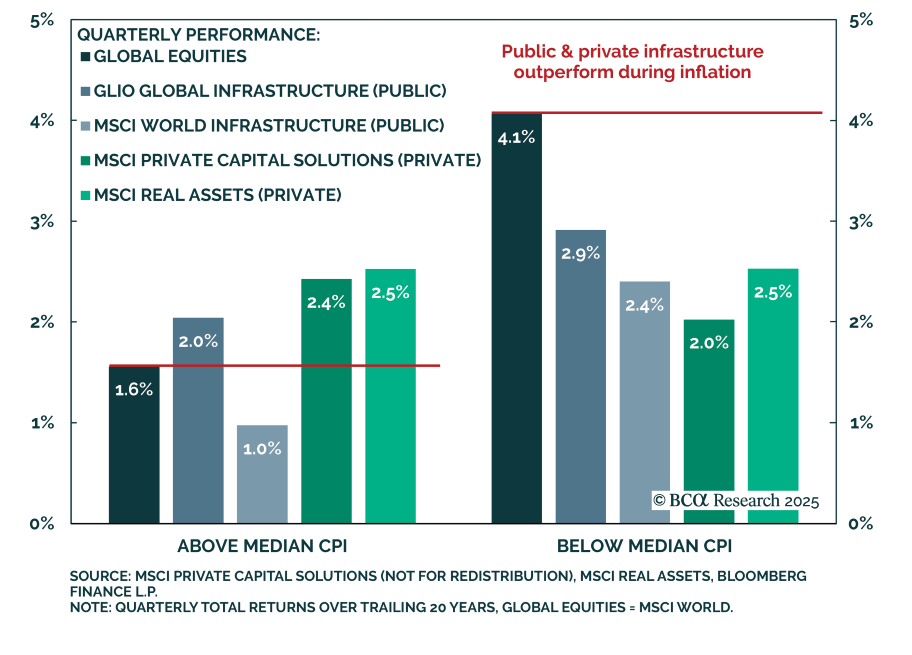

BCA’s Private Markets & Alternatives strategists recommend a balanced allocation across Public and Private Infrastructure, with near-term valuation favoring Public. Structural differences in index construction, sector mix, and regional exposure drive…

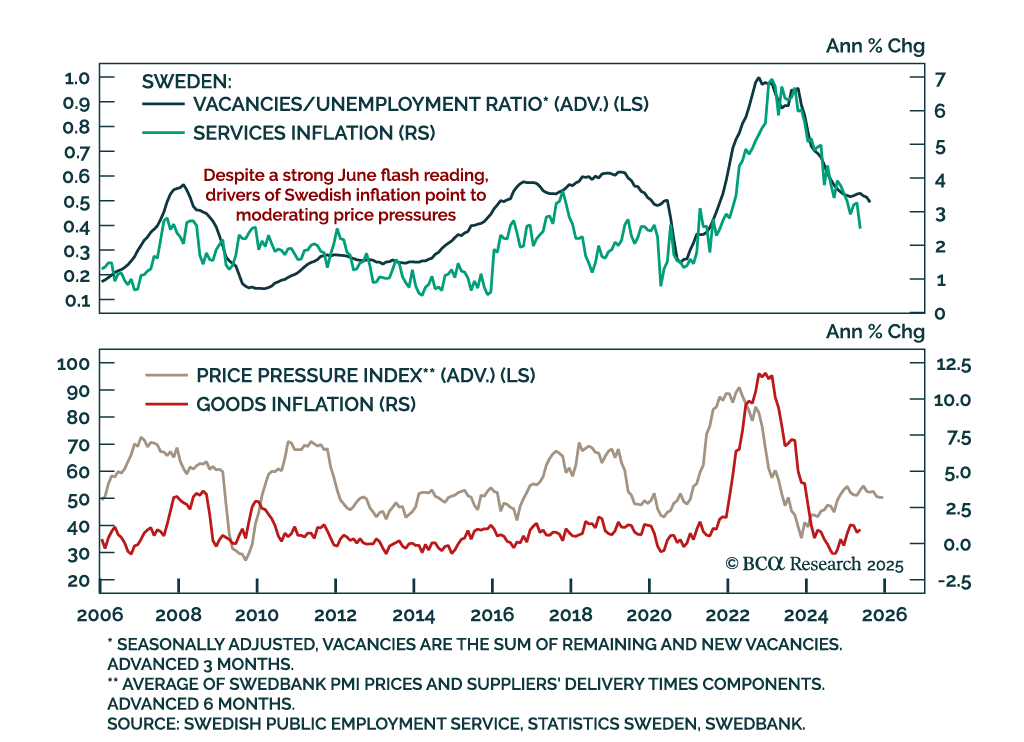

Stronger-than-expected June inflation will likely keep the Riksbank on hold in August, despite soft underlying trends. Headline inflation accelerated more than expected to 0.5% m/m (0.8% y/y), while CPI ex-housing rose to 2.9% y/y and core inflation to 3.3%…